Financial Decision Making Report: Analysis of Roast Ltd's Finances

VerifiedAdded on 2023/01/18

|16

|4516

|95

Report

AI Summary

This report provides a comprehensive analysis of financial decision-making, focusing on the case of Roast Ltd. It begins with an executive summary and an industry review of the UK beverage sector, highlighting key players and market trends. The core of the report centers on financial statement analysis, including the P&L statement, balance sheet, and statement of cash flows for 2017 and 2018, with a detailed examination of relevant financial ratios such as gross profit margin, net profit margin, operating profit ratio, current ratio, quick ratio, debt-to-equity ratio, and return on capital employed. The report also delves into investment appraisal techniques and explores various sources of finance available to the company. Through this analysis, the report aims to provide insights into Roast Ltd's financial performance, profitability, and stability, offering valuable information for strategic decision-making and business growth.

Financial Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Executive summary..........................................................................................................................1

PART 1............................................................................................................................................1

Industry Review..........................................................................................................................1

PART 2............................................................................................................................................2

2.1 Statement of P&L..................................................................................................................2

2.2 Balance sheet Statement of financial position......................................................................4

2.3 Statement of cash Flows........................................................................................................6

Part 3: Investment Appraisal and Sources of Finance.....................................................................8

3.1 Investment Appraisal............................................................................................................8

3.2 Sources of finance...............................................................................................................10

REFERENCES .............................................................................................................................12

Executive summary..........................................................................................................................1

PART 1............................................................................................................................................1

Industry Review..........................................................................................................................1

PART 2............................................................................................................................................2

2.1 Statement of P&L..................................................................................................................2

2.2 Balance sheet Statement of financial position......................................................................4

2.3 Statement of cash Flows........................................................................................................6

Part 3: Investment Appraisal and Sources of Finance.....................................................................8

3.1 Investment Appraisal............................................................................................................8

3.2 Sources of finance...............................................................................................................10

REFERENCES .............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Executive summary

Financial decision-making involves the method of formulating potential plans that will

assist the company in achieving stable growth possibilities. It is also the responsibility of each

organization's administration to devise the best-in-kind approaches for achieving success in

business activities. The report summaries, balance sheet, P&L account and importance of cash

flow statement that help to analysis the position of company in marketplace. The entire analysis

is also carried out with regard to investment assessment methods along with funding sources.

The primary objective of this study is to analyse various financial records in order to create

successful decision-making.

Main key finding through this assessment is that ratio analysis is an important element

which helps to define the overall profitability of Roast Ltd. Evaluation of financial document

describes the entire market structure, financial stability and strength and number of existing

shareholder in an accounting year. External sources of finance are better for company as it

maintain the continuity within operations and handle cash balance.

PART 1

Industry Review

UK's beverage sector is very large in scope and has a major contribution to UK's

development (Bond, Edmans and Goldstein, 2012). The various elements together with details

leading to the evaluation of the condition of the industry are provided in different stages below:

The industry's total contribution to UK GDP is about 3.7 billion pounds in 2017.

There are number of companies which plays a major role in increasing the beverage

industry such as Starbucks, Cafe2U, Soho coffee, Cafe Nero, Costa Coffee and Republic

coffee house.

In the recent year it has been determined that the actual development and growth in

respective sector is almost 7.9%. This state that customer in UK are mostly attached with

beverage in order to satisfy their daily requirement.

The greatest possibility within this industry is to extend enterprise across such areas

where there are still few cafe being operated. It will give all existing companies with an

ability to expand their activities and take advantage of growth opportunities.

1

Financial decision-making involves the method of formulating potential plans that will

assist the company in achieving stable growth possibilities. It is also the responsibility of each

organization's administration to devise the best-in-kind approaches for achieving success in

business activities. The report summaries, balance sheet, P&L account and importance of cash

flow statement that help to analysis the position of company in marketplace. The entire analysis

is also carried out with regard to investment assessment methods along with funding sources.

The primary objective of this study is to analyse various financial records in order to create

successful decision-making.

Main key finding through this assessment is that ratio analysis is an important element

which helps to define the overall profitability of Roast Ltd. Evaluation of financial document

describes the entire market structure, financial stability and strength and number of existing

shareholder in an accounting year. External sources of finance are better for company as it

maintain the continuity within operations and handle cash balance.

PART 1

Industry Review

UK's beverage sector is very large in scope and has a major contribution to UK's

development (Bond, Edmans and Goldstein, 2012). The various elements together with details

leading to the evaluation of the condition of the industry are provided in different stages below:

The industry's total contribution to UK GDP is about 3.7 billion pounds in 2017.

There are number of companies which plays a major role in increasing the beverage

industry such as Starbucks, Cafe2U, Soho coffee, Cafe Nero, Costa Coffee and Republic

coffee house.

In the recent year it has been determined that the actual development and growth in

respective sector is almost 7.9%. This state that customer in UK are mostly attached with

beverage in order to satisfy their daily requirement.

The greatest possibility within this industry is to extend enterprise across such areas

where there are still few cafe being operated. It will give all existing companies with an

ability to expand their activities and take advantage of growth opportunities.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

There are many problems in the coffee industry which the company working in this field

has had to face. The first problem surrounding the in the industry is introduction of

various types of beverages which have a significant impact on industry and share of the

market (Carraher and Van Auken, 2013). Furthermore, customer understanding where

they concentrate on drink consumption at a specific time. It will have a significant impact

to their activities in this situation.

Challenges for beverage sector

Ban of plastic which increase cost for the companies dealing in beverage sectors as they

have to look for some other alternative.

The rise of health consciousness among customer dye to which consumption for fast food

have rapidly decreases.

Opportunities for beverage sector

1. Company can include natural soft drinks that will contain low level of sugar and other

harmful ingredients.

2. These innovations mean that artisanal beverages are starting to attract the attention of the

large multinational companies that dominate the international landscape, such as Nestlé

in coffee and Unilever in tea.

PART 2

2.1 Statement of P&L

In modern business era, every company prepares the trading account document to

determine the actual figures of profit and loss with an accounting year. This is the final accounts

section which is addressed to inner and external business persons and customers. It majorly

supports to determine the correct and exact information about the profitability and financial

strength of company. This is mostly used by the various types of workers, including investors,

vendors, clients, stakeholders (Hershey, Austin and Gutierrez, 2015). This helps to improve their

ability to make decisions. The numerous decisions to be taken include providence of credit,

savings, production and purchase of goods. In UK, Roast LTD is a famous coffee house which is

operating well in market by providing number of useful necessary daily product. From the

assessment of the organization's income statement account, it was found that the sales achieved

in 2017 were 2022 GBP, however the figure extended in 2018 and reached 2534 GBP. This

2

has had to face. The first problem surrounding the in the industry is introduction of

various types of beverages which have a significant impact on industry and share of the

market (Carraher and Van Auken, 2013). Furthermore, customer understanding where

they concentrate on drink consumption at a specific time. It will have a significant impact

to their activities in this situation.

Challenges for beverage sector

Ban of plastic which increase cost for the companies dealing in beverage sectors as they

have to look for some other alternative.

The rise of health consciousness among customer dye to which consumption for fast food

have rapidly decreases.

Opportunities for beverage sector

1. Company can include natural soft drinks that will contain low level of sugar and other

harmful ingredients.

2. These innovations mean that artisanal beverages are starting to attract the attention of the

large multinational companies that dominate the international landscape, such as Nestlé

in coffee and Unilever in tea.

PART 2

2.1 Statement of P&L

In modern business era, every company prepares the trading account document to

determine the actual figures of profit and loss with an accounting year. This is the final accounts

section which is addressed to inner and external business persons and customers. It majorly

supports to determine the correct and exact information about the profitability and financial

strength of company. This is mostly used by the various types of workers, including investors,

vendors, clients, stakeholders (Hershey, Austin and Gutierrez, 2015). This helps to improve their

ability to make decisions. The numerous decisions to be taken include providence of credit,

savings, production and purchase of goods. In UK, Roast LTD is a famous coffee house which is

operating well in market by providing number of useful necessary daily product. From the

assessment of the organization's income statement account, it was found that the sales achieved

in 2017 were 2022 GBP, however the figure extended in 2018 and reached 2534 GBP. This

2

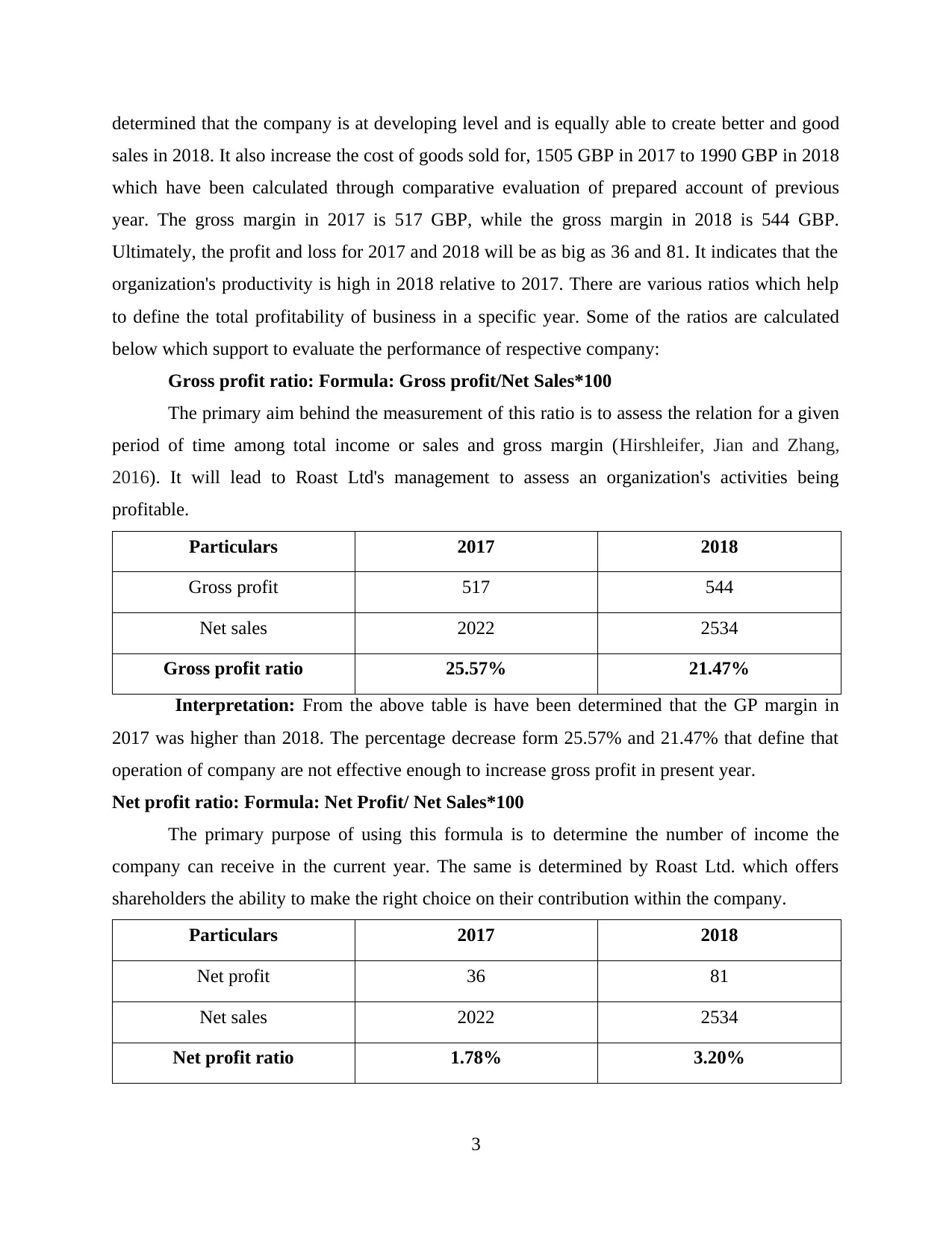

determined that the company is at developing level and is equally able to create better and good

sales in 2018. It also increase the cost of goods sold for, 1505 GBP in 2017 to 1990 GBP in 2018

which have been calculated through comparative evaluation of prepared account of previous

year. The gross margin in 2017 is 517 GBP, while the gross margin in 2018 is 544 GBP.

Ultimately, the profit and loss for 2017 and 2018 will be as big as 36 and 81. It indicates that the

organization's productivity is high in 2018 relative to 2017. There are various ratios which help

to define the total profitability of business in a specific year. Some of the ratios are calculated

below which support to evaluate the performance of respective company:

Gross profit ratio: Formula: Gross profit/Net Sales*100

The primary aim behind the measurement of this ratio is to assess the relation for a given

period of time among total income or sales and gross margin (Hirshleifer, Jian and Zhang,

2016). It will lead to Roast Ltd's management to assess an organization's activities being

profitable.

Particulars 2017 2018

Gross profit 517 544

Net sales 2022 2534

Gross profit ratio 25.57% 21.47%

Interpretation: From the above table is have been determined that the GP margin in

2017 was higher than 2018. The percentage decrease form 25.57% and 21.47% that define that

operation of company are not effective enough to increase gross profit in present year.

Net profit ratio: Formula: Net Profit/ Net Sales*100

The primary purpose of using this formula is to determine the number of income the

company can receive in the current year. The same is determined by Roast Ltd. which offers

shareholders the ability to make the right choice on their contribution within the company.

Particulars 2017 2018

Net profit 36 81

Net sales 2022 2534

Net profit ratio 1.78% 3.20%

3

sales in 2018. It also increase the cost of goods sold for, 1505 GBP in 2017 to 1990 GBP in 2018

which have been calculated through comparative evaluation of prepared account of previous

year. The gross margin in 2017 is 517 GBP, while the gross margin in 2018 is 544 GBP.

Ultimately, the profit and loss for 2017 and 2018 will be as big as 36 and 81. It indicates that the

organization's productivity is high in 2018 relative to 2017. There are various ratios which help

to define the total profitability of business in a specific year. Some of the ratios are calculated

below which support to evaluate the performance of respective company:

Gross profit ratio: Formula: Gross profit/Net Sales*100

The primary aim behind the measurement of this ratio is to assess the relation for a given

period of time among total income or sales and gross margin (Hirshleifer, Jian and Zhang,

2016). It will lead to Roast Ltd's management to assess an organization's activities being

profitable.

Particulars 2017 2018

Gross profit 517 544

Net sales 2022 2534

Gross profit ratio 25.57% 21.47%

Interpretation: From the above table is have been determined that the GP margin in

2017 was higher than 2018. The percentage decrease form 25.57% and 21.47% that define that

operation of company are not effective enough to increase gross profit in present year.

Net profit ratio: Formula: Net Profit/ Net Sales*100

The primary purpose of using this formula is to determine the number of income the

company can receive in the current year. The same is determined by Roast Ltd. which offers

shareholders the ability to make the right choice on their contribution within the company.

Particulars 2017 2018

Net profit 36 81

Net sales 2022 2534

Net profit ratio 1.78% 3.20%

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

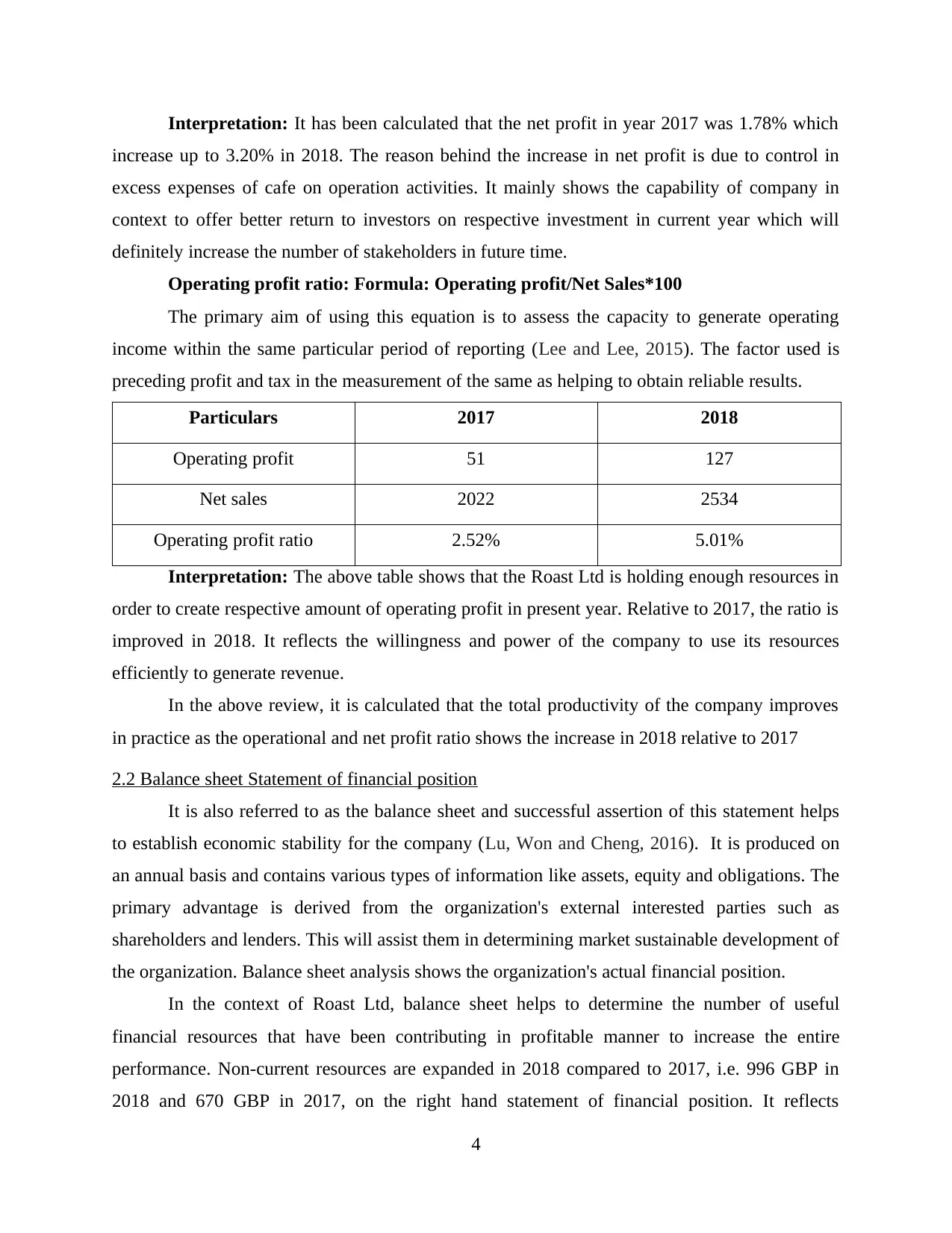

Interpretation: It has been calculated that the net profit in year 2017 was 1.78% which

increase up to 3.20% in 2018. The reason behind the increase in net profit is due to control in

excess expenses of cafe on operation activities. It mainly shows the capability of company in

context to offer better return to investors on respective investment in current year which will

definitely increase the number of stakeholders in future time.

Operating profit ratio: Formula: Operating profit/Net Sales*100

The primary aim of using this equation is to assess the capacity to generate operating

income within the same particular period of reporting (Lee and Lee, 2015). The factor used is

preceding profit and tax in the measurement of the same as helping to obtain reliable results.

Particulars 2017 2018

Operating profit 51 127

Net sales 2022 2534

Operating profit ratio 2.52% 5.01%

Interpretation: The above table shows that the Roast Ltd is holding enough resources in

order to create respective amount of operating profit in present year. Relative to 2017, the ratio is

improved in 2018. It reflects the willingness and power of the company to use its resources

efficiently to generate revenue.

In the above review, it is calculated that the total productivity of the company improves

in practice as the operational and net profit ratio shows the increase in 2018 relative to 2017

2.2 Balance sheet Statement of financial position

It is also referred to as the balance sheet and successful assertion of this statement helps

to establish economic stability for the company (Lu, Won and Cheng, 2016). It is produced on

an annual basis and contains various types of information like assets, equity and obligations. The

primary advantage is derived from the organization's external interested parties such as

shareholders and lenders. This will assist them in determining market sustainable development of

the organization. Balance sheet analysis shows the organization's actual financial position.

In the context of Roast Ltd, balance sheet helps to determine the number of useful

financial resources that have been contributing in profitable manner to increase the entire

performance. Non-current resources are expanded in 2018 compared to 2017, i.e. 996 GBP in

2018 and 670 GBP in 2017, on the right hand statement of financial position. It reflects

4

increase up to 3.20% in 2018. The reason behind the increase in net profit is due to control in

excess expenses of cafe on operation activities. It mainly shows the capability of company in

context to offer better return to investors on respective investment in current year which will

definitely increase the number of stakeholders in future time.

Operating profit ratio: Formula: Operating profit/Net Sales*100

The primary aim of using this equation is to assess the capacity to generate operating

income within the same particular period of reporting (Lee and Lee, 2015). The factor used is

preceding profit and tax in the measurement of the same as helping to obtain reliable results.

Particulars 2017 2018

Operating profit 51 127

Net sales 2022 2534

Operating profit ratio 2.52% 5.01%

Interpretation: The above table shows that the Roast Ltd is holding enough resources in

order to create respective amount of operating profit in present year. Relative to 2017, the ratio is

improved in 2018. It reflects the willingness and power of the company to use its resources

efficiently to generate revenue.

In the above review, it is calculated that the total productivity of the company improves

in practice as the operational and net profit ratio shows the increase in 2018 relative to 2017

2.2 Balance sheet Statement of financial position

It is also referred to as the balance sheet and successful assertion of this statement helps

to establish economic stability for the company (Lu, Won and Cheng, 2016). It is produced on

an annual basis and contains various types of information like assets, equity and obligations. The

primary advantage is derived from the organization's external interested parties such as

shareholders and lenders. This will assist them in determining market sustainable development of

the organization. Balance sheet analysis shows the organization's actual financial position.

In the context of Roast Ltd, balance sheet helps to determine the number of useful

financial resources that have been contributing in profitable manner to increase the entire

performance. Non-current resources are expanded in 2018 compared to 2017, i.e. 996 GBP in

2018 and 670 GBP in 2017, on the right hand statement of financial position. It reflects

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

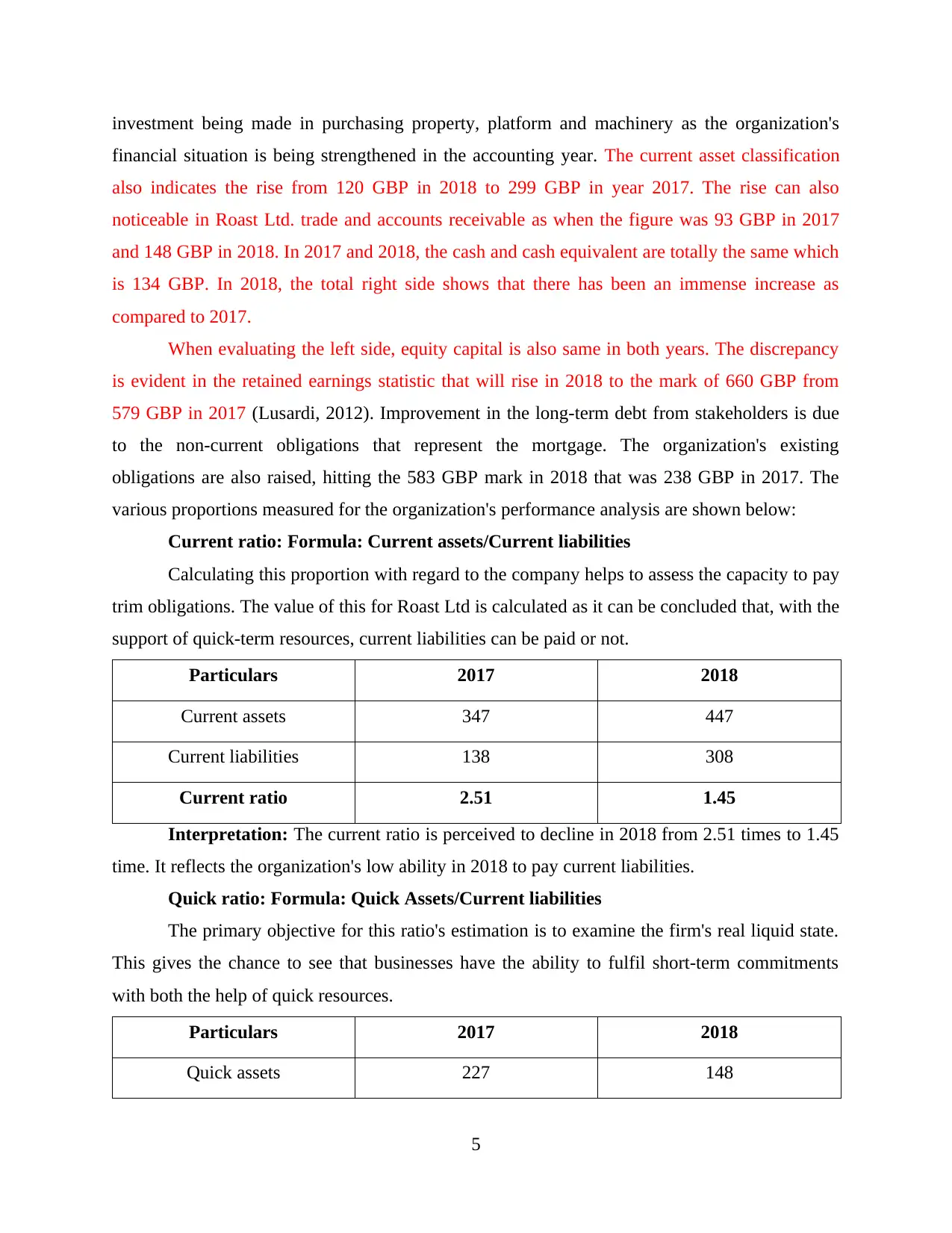

investment being made in purchasing property, platform and machinery as the organization's

financial situation is being strengthened in the accounting year. The current asset classification

also indicates the rise from 120 GBP in 2018 to 299 GBP in year 2017. The rise can also

noticeable in Roast Ltd. trade and accounts receivable as when the figure was 93 GBP in 2017

and 148 GBP in 2018. In 2017 and 2018, the cash and cash equivalent are totally the same which

is 134 GBP. In 2018, the total right side shows that there has been an immense increase as

compared to 2017.

When evaluating the left side, equity capital is also same in both years. The discrepancy

is evident in the retained earnings statistic that will rise in 2018 to the mark of 660 GBP from

579 GBP in 2017 (Lusardi, 2012). Improvement in the long-term debt from stakeholders is due

to the non-current obligations that represent the mortgage. The organization's existing

obligations are also raised, hitting the 583 GBP mark in 2018 that was 238 GBP in 2017. The

various proportions measured for the organization's performance analysis are shown below:

Current ratio: Formula: Current assets/Current liabilities

Calculating this proportion with regard to the company helps to assess the capacity to pay

trim obligations. The value of this for Roast Ltd is calculated as it can be concluded that, with the

support of quick-term resources, current liabilities can be paid or not.

Particulars 2017 2018

Current assets 347 447

Current liabilities 138 308

Current ratio 2.51 1.45

Interpretation: The current ratio is perceived to decline in 2018 from 2.51 times to 1.45

time. It reflects the organization's low ability in 2018 to pay current liabilities.

Quick ratio: Formula: Quick Assets/Current liabilities

The primary objective for this ratio's estimation is to examine the firm's real liquid state.

This gives the chance to see that businesses have the ability to fulfil short-term commitments

with both the help of quick resources.

Particulars 2017 2018

Quick assets 227 148

5

financial situation is being strengthened in the accounting year. The current asset classification

also indicates the rise from 120 GBP in 2018 to 299 GBP in year 2017. The rise can also

noticeable in Roast Ltd. trade and accounts receivable as when the figure was 93 GBP in 2017

and 148 GBP in 2018. In 2017 and 2018, the cash and cash equivalent are totally the same which

is 134 GBP. In 2018, the total right side shows that there has been an immense increase as

compared to 2017.

When evaluating the left side, equity capital is also same in both years. The discrepancy

is evident in the retained earnings statistic that will rise in 2018 to the mark of 660 GBP from

579 GBP in 2017 (Lusardi, 2012). Improvement in the long-term debt from stakeholders is due

to the non-current obligations that represent the mortgage. The organization's existing

obligations are also raised, hitting the 583 GBP mark in 2018 that was 238 GBP in 2017. The

various proportions measured for the organization's performance analysis are shown below:

Current ratio: Formula: Current assets/Current liabilities

Calculating this proportion with regard to the company helps to assess the capacity to pay

trim obligations. The value of this for Roast Ltd is calculated as it can be concluded that, with the

support of quick-term resources, current liabilities can be paid or not.

Particulars 2017 2018

Current assets 347 447

Current liabilities 138 308

Current ratio 2.51 1.45

Interpretation: The current ratio is perceived to decline in 2018 from 2.51 times to 1.45

time. It reflects the organization's low ability in 2018 to pay current liabilities.

Quick ratio: Formula: Quick Assets/Current liabilities

The primary objective for this ratio's estimation is to examine the firm's real liquid state.

This gives the chance to see that businesses have the ability to fulfil short-term commitments

with both the help of quick resources.

Particulars 2017 2018

Quick assets 227 148

5

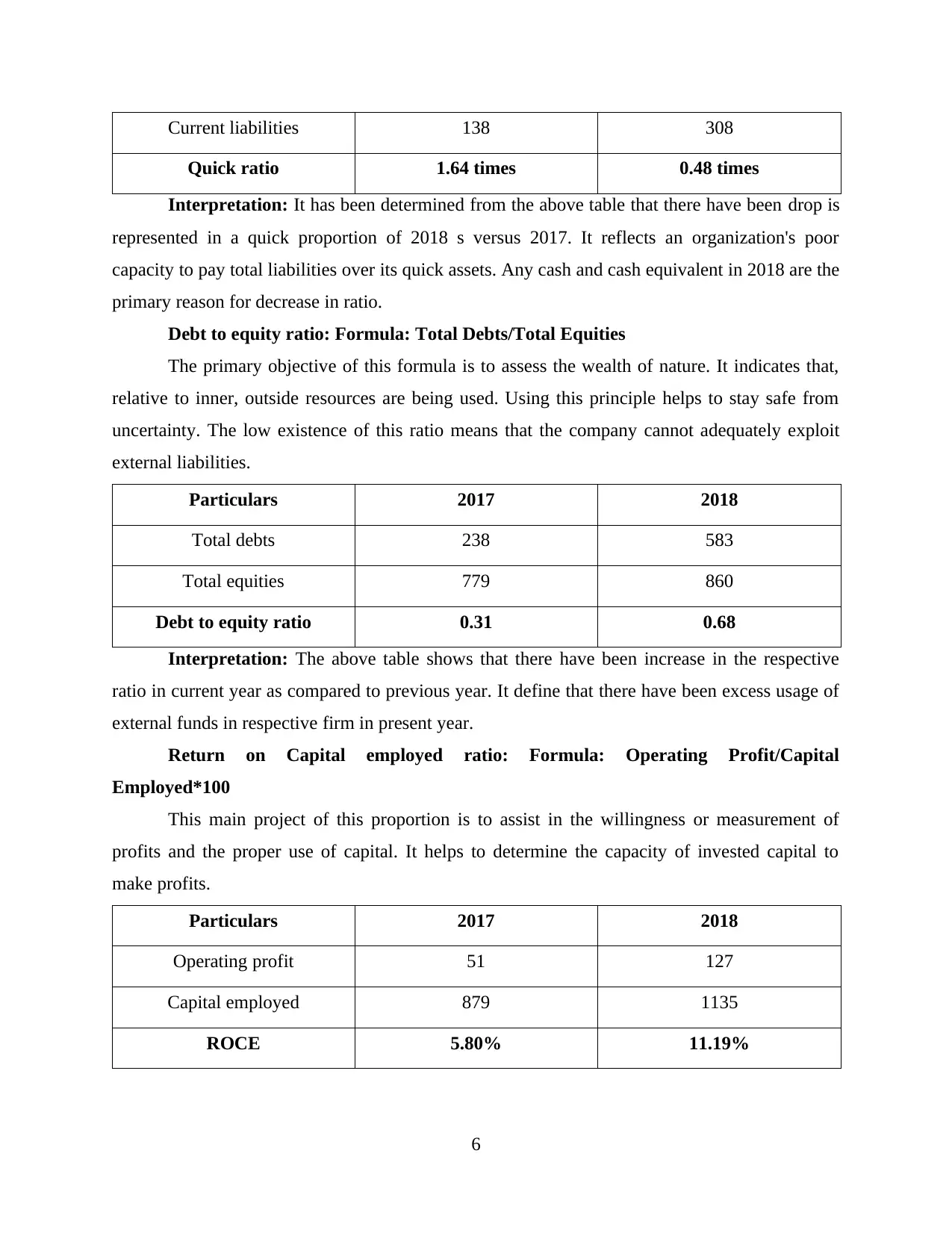

Current liabilities 138 308

Quick ratio 1.64 times 0.48 times

Interpretation: It has been determined from the above table that there have been drop is

represented in a quick proportion of 2018 s versus 2017. It reflects an organization's poor

capacity to pay total liabilities over its quick assets. Any cash and cash equivalent in 2018 are the

primary reason for decrease in ratio.

Debt to equity ratio: Formula: Total Debts/Total Equities

The primary objective of this formula is to assess the wealth of nature. It indicates that,

relative to inner, outside resources are being used. Using this principle helps to stay safe from

uncertainty. The low existence of this ratio means that the company cannot adequately exploit

external liabilities.

Particulars 2017 2018

Total debts 238 583

Total equities 779 860

Debt to equity ratio 0.31 0.68

Interpretation: The above table shows that there have been increase in the respective

ratio in current year as compared to previous year. It define that there have been excess usage of

external funds in respective firm in present year.

Return on Capital employed ratio: Formula: Operating Profit/Capital

Employed*100

This main project of this proportion is to assist in the willingness or measurement of

profits and the proper use of capital. It helps to determine the capacity of invested capital to

make profits.

Particulars 2017 2018

Operating profit 51 127

Capital employed 879 1135

ROCE 5.80% 11.19%

6

Quick ratio 1.64 times 0.48 times

Interpretation: It has been determined from the above table that there have been drop is

represented in a quick proportion of 2018 s versus 2017. It reflects an organization's poor

capacity to pay total liabilities over its quick assets. Any cash and cash equivalent in 2018 are the

primary reason for decrease in ratio.

Debt to equity ratio: Formula: Total Debts/Total Equities

The primary objective of this formula is to assess the wealth of nature. It indicates that,

relative to inner, outside resources are being used. Using this principle helps to stay safe from

uncertainty. The low existence of this ratio means that the company cannot adequately exploit

external liabilities.

Particulars 2017 2018

Total debts 238 583

Total equities 779 860

Debt to equity ratio 0.31 0.68

Interpretation: The above table shows that there have been increase in the respective

ratio in current year as compared to previous year. It define that there have been excess usage of

external funds in respective firm in present year.

Return on Capital employed ratio: Formula: Operating Profit/Capital

Employed*100

This main project of this proportion is to assist in the willingness or measurement of

profits and the proper use of capital. It helps to determine the capacity of invested capital to

make profits.

Particulars 2017 2018

Operating profit 51 127

Capital employed 879 1135

ROCE 5.80% 11.19%

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

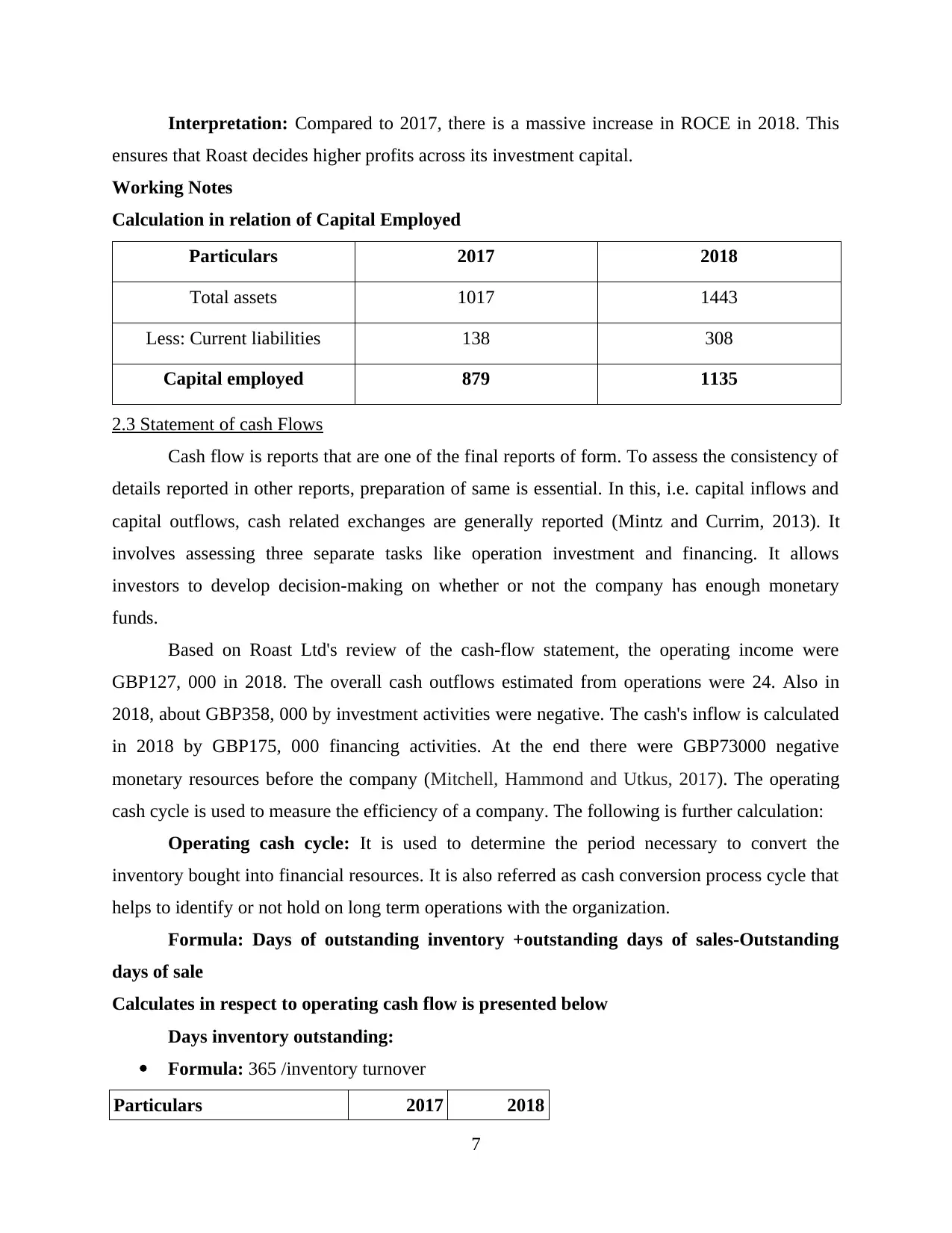

Interpretation: Compared to 2017, there is a massive increase in ROCE in 2018. This

ensures that Roast decides higher profits across its investment capital.

Working Notes

Calculation in relation of Capital Employed

Particulars 2017 2018

Total assets 1017 1443

Less: Current liabilities 138 308

Capital employed 879 1135

2.3 Statement of cash Flows

Cash flow is reports that are one of the final reports of form. To assess the consistency of

details reported in other reports, preparation of same is essential. In this, i.e. capital inflows and

capital outflows, cash related exchanges are generally reported (Mintz and Currim, 2013). It

involves assessing three separate tasks like operation investment and financing. It allows

investors to develop decision-making on whether or not the company has enough monetary

funds.

Based on Roast Ltd's review of the cash-flow statement, the operating income were

GBP127, 000 in 2018. The overall cash outflows estimated from operations were 24. Also in

2018, about GBP358, 000 by investment activities were negative. The cash's inflow is calculated

in 2018 by GBP175, 000 financing activities. At the end there were GBP73000 negative

monetary resources before the company (Mitchell, Hammond and Utkus, 2017). The operating

cash cycle is used to measure the efficiency of a company. The following is further calculation:

Operating cash cycle: It is used to determine the period necessary to convert the

inventory bought into financial resources. It is also referred as cash conversion process cycle that

helps to identify or not hold on long term operations with the organization.

Formula: Days of outstanding inventory +outstanding days of sales-Outstanding

days of sale

Calculates in respect to operating cash flow is presented below

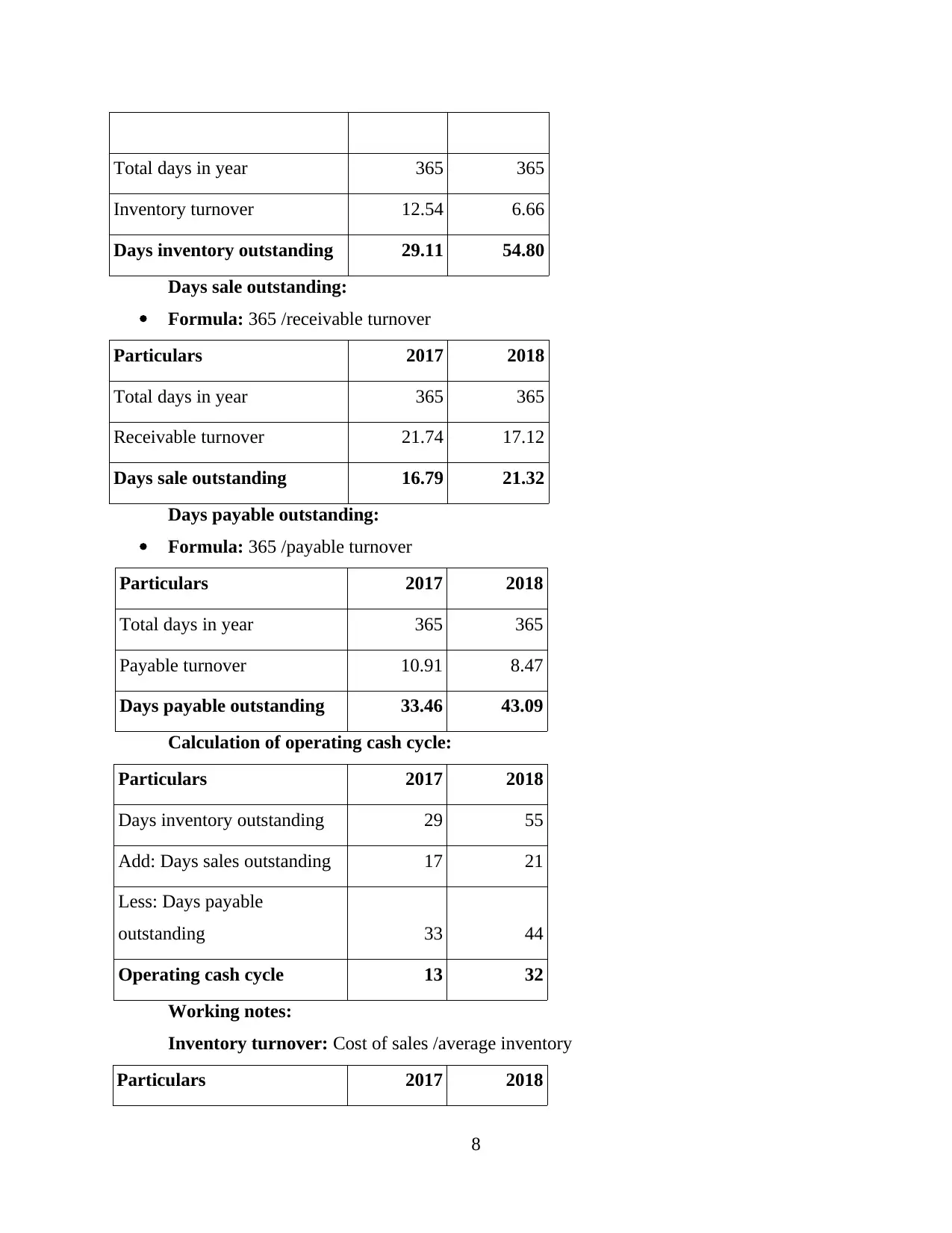

Days inventory outstanding:

Formula: 365 /inventory turnover

Particulars 2017 2018

7

ensures that Roast decides higher profits across its investment capital.

Working Notes

Calculation in relation of Capital Employed

Particulars 2017 2018

Total assets 1017 1443

Less: Current liabilities 138 308

Capital employed 879 1135

2.3 Statement of cash Flows

Cash flow is reports that are one of the final reports of form. To assess the consistency of

details reported in other reports, preparation of same is essential. In this, i.e. capital inflows and

capital outflows, cash related exchanges are generally reported (Mintz and Currim, 2013). It

involves assessing three separate tasks like operation investment and financing. It allows

investors to develop decision-making on whether or not the company has enough monetary

funds.

Based on Roast Ltd's review of the cash-flow statement, the operating income were

GBP127, 000 in 2018. The overall cash outflows estimated from operations were 24. Also in

2018, about GBP358, 000 by investment activities were negative. The cash's inflow is calculated

in 2018 by GBP175, 000 financing activities. At the end there were GBP73000 negative

monetary resources before the company (Mitchell, Hammond and Utkus, 2017). The operating

cash cycle is used to measure the efficiency of a company. The following is further calculation:

Operating cash cycle: It is used to determine the period necessary to convert the

inventory bought into financial resources. It is also referred as cash conversion process cycle that

helps to identify or not hold on long term operations with the organization.

Formula: Days of outstanding inventory +outstanding days of sales-Outstanding

days of sale

Calculates in respect to operating cash flow is presented below

Days inventory outstanding:

Formula: 365 /inventory turnover

Particulars 2017 2018

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total days in year 365 365

Inventory turnover 12.54 6.66

Days inventory outstanding 29.11 54.80

Days sale outstanding:

Formula: 365 /receivable turnover

Particulars 2017 2018

Total days in year 365 365

Receivable turnover 21.74 17.12

Days sale outstanding 16.79 21.32

Days payable outstanding:

Formula: 365 /payable turnover

Particulars 2017 2018

Total days in year 365 365

Payable turnover 10.91 8.47

Days payable outstanding 33.46 43.09

Calculation of operating cash cycle:

Particulars 2017 2018

Days inventory outstanding 29 55

Add: Days sales outstanding 17 21

Less: Days payable

outstanding 33 44

Operating cash cycle 13 32

Working notes:

Inventory turnover: Cost of sales /average inventory

Particulars 2017 2018

8

Inventory turnover 12.54 6.66

Days inventory outstanding 29.11 54.80

Days sale outstanding:

Formula: 365 /receivable turnover

Particulars 2017 2018

Total days in year 365 365

Receivable turnover 21.74 17.12

Days sale outstanding 16.79 21.32

Days payable outstanding:

Formula: 365 /payable turnover

Particulars 2017 2018

Total days in year 365 365

Payable turnover 10.91 8.47

Days payable outstanding 33.46 43.09

Calculation of operating cash cycle:

Particulars 2017 2018

Days inventory outstanding 29 55

Add: Days sales outstanding 17 21

Less: Days payable

outstanding 33 44

Operating cash cycle 13 32

Working notes:

Inventory turnover: Cost of sales /average inventory

Particulars 2017 2018

8

Cost of sales 1505 1990

Average inventory 120 299

Inventory turnover 12.54 6.66

Receivable turnover: Net sales /account receivables

Particulars 2017 2018

Net sales 2022 2534

Account receivables 93 148

Receivable turnover 21.74 17.12

Payable turnover: Cost of sales /account payable

Particulars 2017 2018

Cost of sales 1505 1990

Account payables 138 235

Payable turnover 10.91 8.47

The comparison above shows that the days necessary for the transaction to be covered

were 13 in 2017 and 32 in 2018. It indicates more time to turn investments into cash-funds in

2018.

Dividend policy: This is the procedure whereby the stakeholders are given earnings.

Roast Ltd.-Roast Ltd. For 2018, no dividends were charged. First reason why some companies

do not pay dividends is because they would rather reinvest those profits back into the business.

Moreover, company will hold off on dividend payments and hoard cash is for acquisitions. In

last roast ltd, usually want to tend to offer dividends, because that draws customers, which holds

them going. Often, however, you'll run into a corporation who needs to slash or remove a

dividend owing to financial difficulties. This is not the correct decision as earnings were

improved relative to 2017 in 2018. This has a negative effect on shareholders ' interest and

subsequent capital reduction.

9

Average inventory 120 299

Inventory turnover 12.54 6.66

Receivable turnover: Net sales /account receivables

Particulars 2017 2018

Net sales 2022 2534

Account receivables 93 148

Receivable turnover 21.74 17.12

Payable turnover: Cost of sales /account payable

Particulars 2017 2018

Cost of sales 1505 1990

Account payables 138 235

Payable turnover 10.91 8.47

The comparison above shows that the days necessary for the transaction to be covered

were 13 in 2017 and 32 in 2018. It indicates more time to turn investments into cash-funds in

2018.

Dividend policy: This is the procedure whereby the stakeholders are given earnings.

Roast Ltd.-Roast Ltd. For 2018, no dividends were charged. First reason why some companies

do not pay dividends is because they would rather reinvest those profits back into the business.

Moreover, company will hold off on dividend payments and hoard cash is for acquisitions. In

last roast ltd, usually want to tend to offer dividends, because that draws customers, which holds

them going. Often, however, you'll run into a corporation who needs to slash or remove a

dividend owing to financial difficulties. This is not the correct decision as earnings were

improved relative to 2017 in 2018. This has a negative effect on shareholders ' interest and

subsequent capital reduction.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.