Financial Analysis of Roast Ltd. and Investment Appraisal Report

VerifiedAdded on 2023/01/17

|17

|4576

|1

Report

AI Summary

This report presents a comprehensive financial analysis of Roast Ltd., focusing on its performance and potential for acquisition by Starbucks. It begins with an executive summary highlighting key findings from the profit and loss statement, which shows increasing net profits, and the company's ability to manage its debts, despite negative cash flows. The report then delves into an industry review of the coffee house sector in the UK, including market size, key players, opportunities, and challenges. Part 2 provides a detailed business performance analysis, examining the statement of profit or loss, statement of financial position, and statement of cash flows, supported by ratio analysis such as gross profit margin, net profit margin, operating profit margin, current ratio, quick ratio, and debt-equity ratio. The analysis reveals trends in revenue, profitability, and financial stability. Part 3 focuses on investment appraisal, specifically the potential for launching new outlets in Romania, and explores the sources of finance available to Roast Ltd. The report concludes that investment in new outlets will enhance sales and cash position, making Roast Ltd. a potentially attractive acquisition target. The financial analysis provides valuable insights into Roast Ltd.'s performance, aiding in informed decision-making regarding investment and acquisition.

Financial Decision Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................1

Part 1: Industry Review...................................................................................................................1

Part 2: Business Performance Analysis...........................................................................................2

2.1 Statement of Profit or Loss...................................................................................................2

2.2 Statement of Financial Position............................................................................................4

2.3 Statement of Cash Flows.......................................................................................................6

Part 3: Investment Appraisal and Sources of Finance.....................................................................8

3.1 Investment Appraisal............................................................................................................8

3.2. Sources of Finance.............................................................................................................10

REFERENCES..............................................................................................................................12

EXECUTIVE SUMMARY.............................................................................................................1

Part 1: Industry Review...................................................................................................................1

Part 2: Business Performance Analysis...........................................................................................2

2.1 Statement of Profit or Loss...................................................................................................2

2.2 Statement of Financial Position............................................................................................4

2.3 Statement of Cash Flows.......................................................................................................6

Part 3: Investment Appraisal and Sources of Finance.....................................................................8

3.1 Investment Appraisal............................................................................................................8

3.2. Sources of Finance.............................................................................................................10

REFERENCES..............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

EXECUTIVE SUMMARY

Financial decision can be defined as the process in which all the decisions associated

with stake holder's equity and liability of business entity along with issuance of bonds. In Roast

Limited, the P&L statement depicts that the net profit of firm in year 2018 is 81000 pounds

which raised from £36000. This increase in profits of firm shows that this company's product

demand is high which assists in its growth and development in market. The business entity has

the ability to pay its debts even though it is facing problems because of paying more for

procuring high quality coffee beans. The company's cash position depicts that it is confronting

issue of negative cash flows but, because of its constantly improving growth rate, it can be

conclude that firm can acquire Roast Ltd. The second part of project depicts that Roast Ltd.

must make investment in launching project of new outlets in Romania as this will contributes in

enhancing sales revenues as well as cash position of company.

Part 1: Industry Review

In today's competitive business environment, the coffee house industry is one of the

fastest growing sector in United Kingdom which is developing constantly because of current

social status of people in UK. By utilizing top line review, the summary of coffee house industry

is mentioned below:

As per the survey performed by ibis, the total revenue of £6 billions has recorded in

coffee house sector of UK. In this industry, the main players includes Café Nero, Starbucks, Cafe

Ritazza, Costa coffee etc. All these organisations are performing well in sector and an yearly

growth of 6.1 percent has recorded that depicts the success of industry (Correia, Dussault, and

Pontes, 2015). In the cafe coffee industry of United Kingdom, there are around 16199

businesses are operating which has been raised with the improving rate in comparison to the

last year. Various opportunities are exist in coffee house market that can be exploit by refereed

firm such as introducing organic coffee which is beneficial for the health of people. This

opportunity can help company in satisfying the needs of customers of being healthy and gaining

competitive advantage in market (Current coffee house industry of United Kingdom. 2019).

Besides the above mentioned opportunities, some challenges are some challenges which

the coffee house industry of United Kingdom faced. These challenges involves changing needs

of customers as they are becoming more aware regarding their health and prefers to have healthy

1

Financial decision can be defined as the process in which all the decisions associated

with stake holder's equity and liability of business entity along with issuance of bonds. In Roast

Limited, the P&L statement depicts that the net profit of firm in year 2018 is 81000 pounds

which raised from £36000. This increase in profits of firm shows that this company's product

demand is high which assists in its growth and development in market. The business entity has

the ability to pay its debts even though it is facing problems because of paying more for

procuring high quality coffee beans. The company's cash position depicts that it is confronting

issue of negative cash flows but, because of its constantly improving growth rate, it can be

conclude that firm can acquire Roast Ltd. The second part of project depicts that Roast Ltd.

must make investment in launching project of new outlets in Romania as this will contributes in

enhancing sales revenues as well as cash position of company.

Part 1: Industry Review

In today's competitive business environment, the coffee house industry is one of the

fastest growing sector in United Kingdom which is developing constantly because of current

social status of people in UK. By utilizing top line review, the summary of coffee house industry

is mentioned below:

As per the survey performed by ibis, the total revenue of £6 billions has recorded in

coffee house sector of UK. In this industry, the main players includes Café Nero, Starbucks, Cafe

Ritazza, Costa coffee etc. All these organisations are performing well in sector and an yearly

growth of 6.1 percent has recorded that depicts the success of industry (Correia, Dussault, and

Pontes, 2015). In the cafe coffee industry of United Kingdom, there are around 16199

businesses are operating which has been raised with the improving rate in comparison to the

last year. Various opportunities are exist in coffee house market that can be exploit by refereed

firm such as introducing organic coffee which is beneficial for the health of people. This

opportunity can help company in satisfying the needs of customers of being healthy and gaining

competitive advantage in market (Current coffee house industry of United Kingdom. 2019).

Besides the above mentioned opportunities, some challenges are some challenges which

the coffee house industry of United Kingdom faced. These challenges involves changing needs

of customers as they are becoming more aware regarding their health and prefers to have healthy

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

alternatives like sugar free beverages, green tea instead of consuming coffee. Intense competition

within industry is the another challenge that coffee house industry faces as there are many

organisations operating in sector which gives tough competition to the refereed company. Apart

from these entry of new entrants in the industry also creates threat for the firms operating in

sector. The main reason of intense rivalry in industry is high margin of profits which are enjoyed

by the companies involved in it (Finke, 2013).

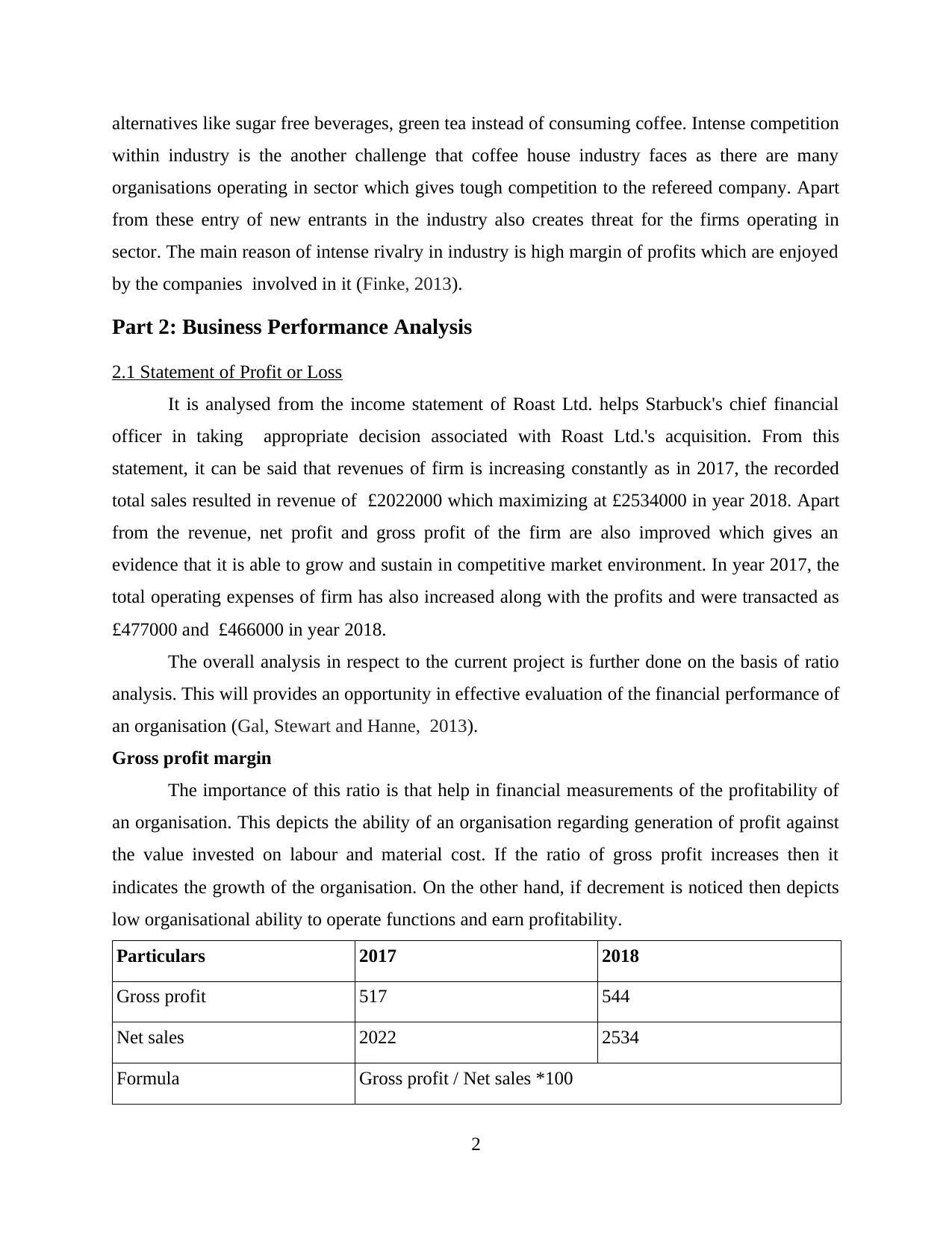

Part 2: Business Performance Analysis

2.1 Statement of Profit or Loss

It is analysed from the income statement of Roast Ltd. helps Starbuck's chief financial

officer in taking appropriate decision associated with Roast Ltd.'s acquisition. From this

statement, it can be said that revenues of firm is increasing constantly as in 2017, the recorded

total sales resulted in revenue of £2022000 which maximizing at £2534000 in year 2018. Apart

from the revenue, net profit and gross profit of the firm are also improved which gives an

evidence that it is able to grow and sustain in competitive market environment. In year 2017, the

total operating expenses of firm has also increased along with the profits and were transacted as

£477000 and £466000 in year 2018.

The overall analysis in respect to the current project is further done on the basis of ratio

analysis. This will provides an opportunity in effective evaluation of the financial performance of

an organisation (Gal, Stewart and Hanne, 2013).

Gross profit margin

The importance of this ratio is that help in financial measurements of the profitability of

an organisation. This depicts the ability of an organisation regarding generation of profit against

the value invested on labour and material cost. If the ratio of gross profit increases then it

indicates the growth of the organisation. On the other hand, if decrement is noticed then depicts

low organisational ability to operate functions and earn profitability.

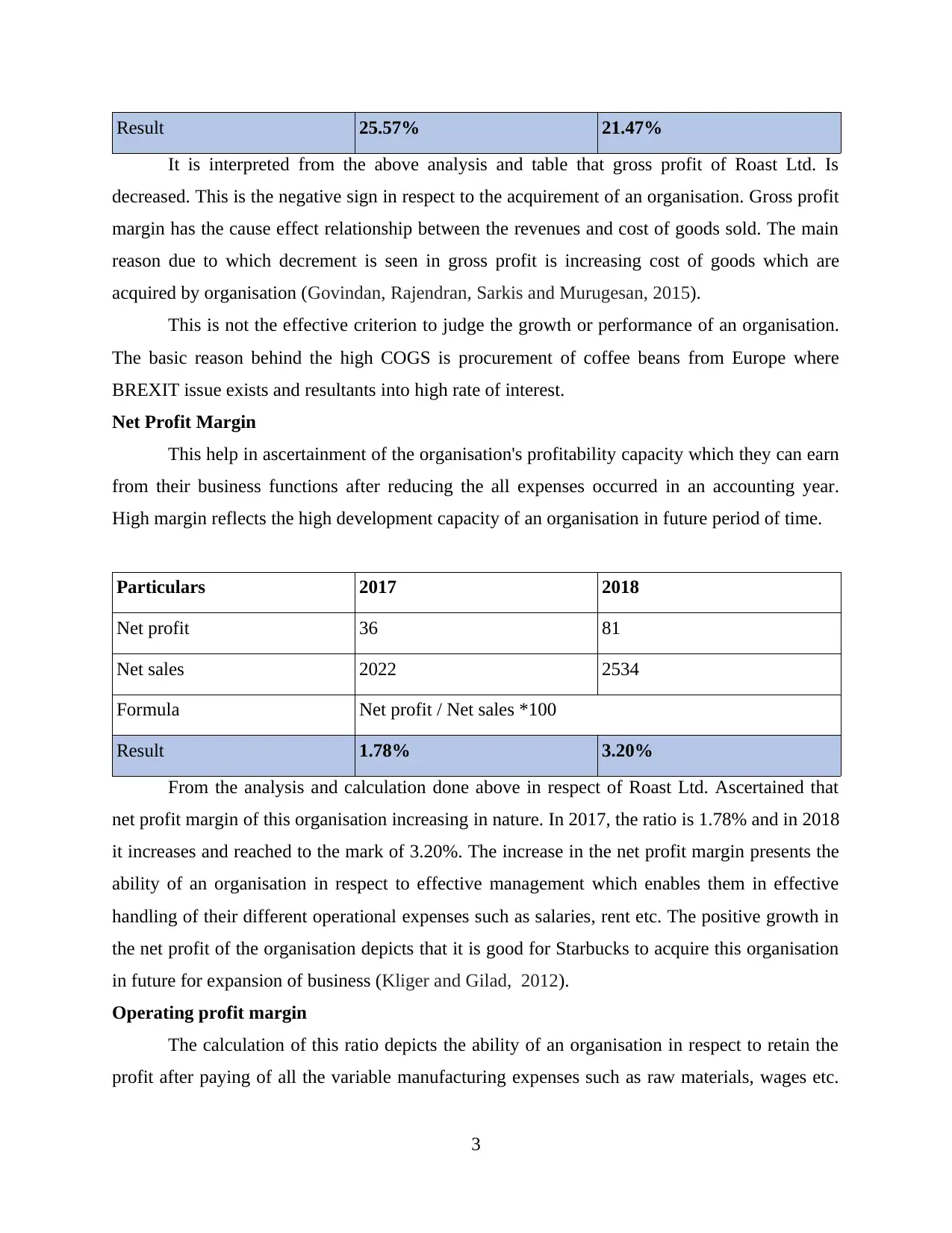

Particulars 2017 2018

Gross profit 517 544

Net sales 2022 2534

Formula Gross profit / Net sales *100

2

within industry is the another challenge that coffee house industry faces as there are many

organisations operating in sector which gives tough competition to the refereed company. Apart

from these entry of new entrants in the industry also creates threat for the firms operating in

sector. The main reason of intense rivalry in industry is high margin of profits which are enjoyed

by the companies involved in it (Finke, 2013).

Part 2: Business Performance Analysis

2.1 Statement of Profit or Loss

It is analysed from the income statement of Roast Ltd. helps Starbuck's chief financial

officer in taking appropriate decision associated with Roast Ltd.'s acquisition. From this

statement, it can be said that revenues of firm is increasing constantly as in 2017, the recorded

total sales resulted in revenue of £2022000 which maximizing at £2534000 in year 2018. Apart

from the revenue, net profit and gross profit of the firm are also improved which gives an

evidence that it is able to grow and sustain in competitive market environment. In year 2017, the

total operating expenses of firm has also increased along with the profits and were transacted as

£477000 and £466000 in year 2018.

The overall analysis in respect to the current project is further done on the basis of ratio

analysis. This will provides an opportunity in effective evaluation of the financial performance of

an organisation (Gal, Stewart and Hanne, 2013).

Gross profit margin

The importance of this ratio is that help in financial measurements of the profitability of

an organisation. This depicts the ability of an organisation regarding generation of profit against

the value invested on labour and material cost. If the ratio of gross profit increases then it

indicates the growth of the organisation. On the other hand, if decrement is noticed then depicts

low organisational ability to operate functions and earn profitability.

Particulars 2017 2018

Gross profit 517 544

Net sales 2022 2534

Formula Gross profit / Net sales *100

2

Result 25.57% 21.47%

It is interpreted from the above analysis and table that gross profit of Roast Ltd. Is

decreased. This is the negative sign in respect to the acquirement of an organisation. Gross profit

margin has the cause effect relationship between the revenues and cost of goods sold. The main

reason due to which decrement is seen in gross profit is increasing cost of goods which are

acquired by organisation (Govindan, Rajendran, Sarkis and Murugesan, 2015).

This is not the effective criterion to judge the growth or performance of an organisation.

The basic reason behind the high COGS is procurement of coffee beans from Europe where

BREXIT issue exists and resultants into high rate of interest.

Net Profit Margin

This help in ascertainment of the organisation's profitability capacity which they can earn

from their business functions after reducing the all expenses occurred in an accounting year.

High margin reflects the high development capacity of an organisation in future period of time.

Particulars 2017 2018

Net profit 36 81

Net sales 2022 2534

Formula Net profit / Net sales *100

Result 1.78% 3.20%

From the analysis and calculation done above in respect of Roast Ltd. Ascertained that

net profit margin of this organisation increasing in nature. In 2017, the ratio is 1.78% and in 2018

it increases and reached to the mark of 3.20%. The increase in the net profit margin presents the

ability of an organisation in respect to effective management which enables them in effective

handling of their different operational expenses such as salaries, rent etc. The positive growth in

the net profit of the organisation depicts that it is good for Starbucks to acquire this organisation

in future for expansion of business (Kliger and Gilad, 2012).

Operating profit margin

The calculation of this ratio depicts the ability of an organisation in respect to retain the

profit after paying of all the variable manufacturing expenses such as raw materials, wages etc.

3

It is interpreted from the above analysis and table that gross profit of Roast Ltd. Is

decreased. This is the negative sign in respect to the acquirement of an organisation. Gross profit

margin has the cause effect relationship between the revenues and cost of goods sold. The main

reason due to which decrement is seen in gross profit is increasing cost of goods which are

acquired by organisation (Govindan, Rajendran, Sarkis and Murugesan, 2015).

This is not the effective criterion to judge the growth or performance of an organisation.

The basic reason behind the high COGS is procurement of coffee beans from Europe where

BREXIT issue exists and resultants into high rate of interest.

Net Profit Margin

This help in ascertainment of the organisation's profitability capacity which they can earn

from their business functions after reducing the all expenses occurred in an accounting year.

High margin reflects the high development capacity of an organisation in future period of time.

Particulars 2017 2018

Net profit 36 81

Net sales 2022 2534

Formula Net profit / Net sales *100

Result 1.78% 3.20%

From the analysis and calculation done above in respect of Roast Ltd. Ascertained that

net profit margin of this organisation increasing in nature. In 2017, the ratio is 1.78% and in 2018

it increases and reached to the mark of 3.20%. The increase in the net profit margin presents the

ability of an organisation in respect to effective management which enables them in effective

handling of their different operational expenses such as salaries, rent etc. The positive growth in

the net profit of the organisation depicts that it is good for Starbucks to acquire this organisation

in future for expansion of business (Kliger and Gilad, 2012).

Operating profit margin

The calculation of this ratio depicts the ability of an organisation in respect to retain the

profit after paying of all the variable manufacturing expenses such as raw materials, wages etc.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

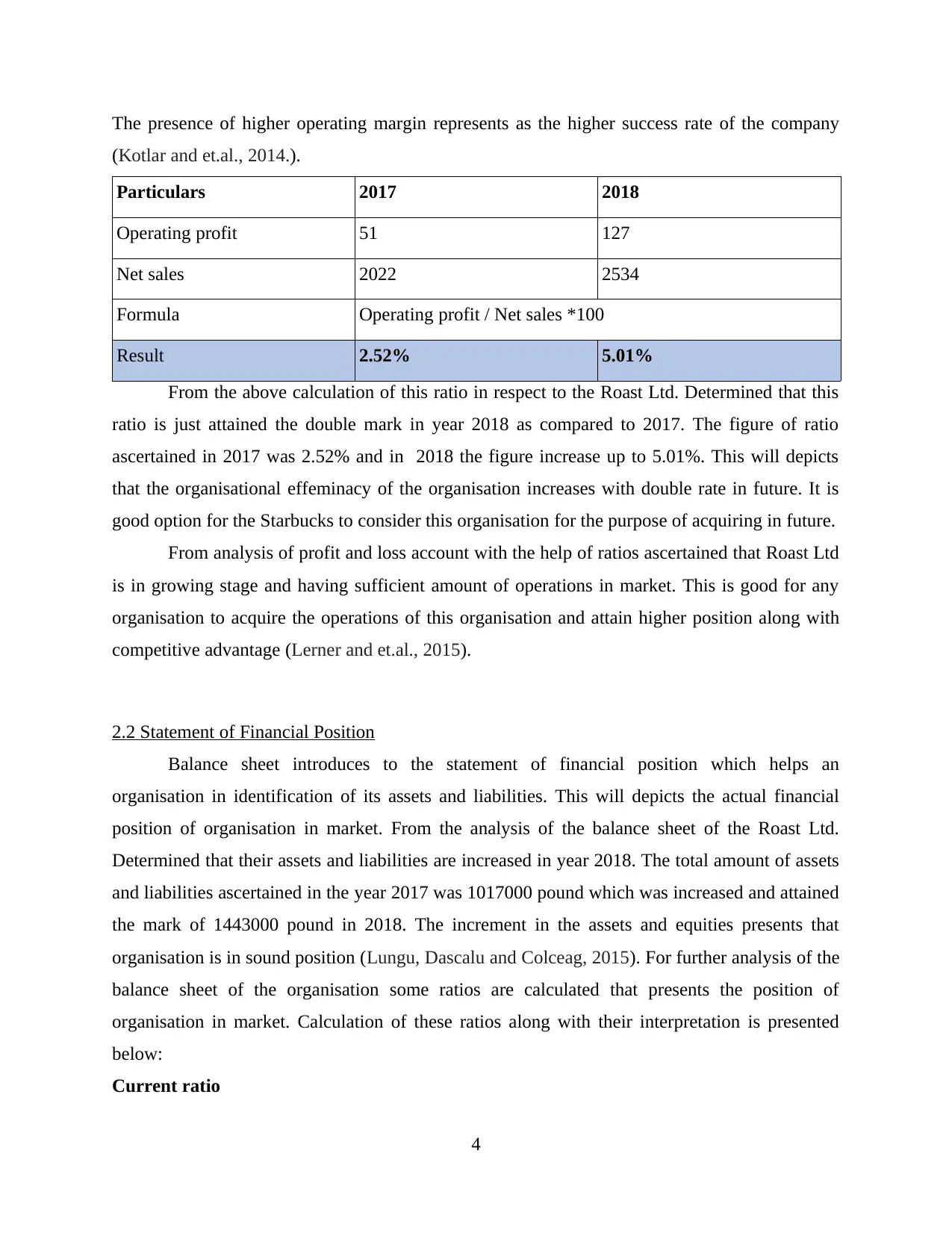

The presence of higher operating margin represents as the higher success rate of the company

(Kotlar and et.al., 2014.).

Particulars 2017 2018

Operating profit 51 127

Net sales 2022 2534

Formula Operating profit / Net sales *100

Result 2.52% 5.01%

From the above calculation of this ratio in respect to the Roast Ltd. Determined that this

ratio is just attained the double mark in year 2018 as compared to 2017. The figure of ratio

ascertained in 2017 was 2.52% and in 2018 the figure increase up to 5.01%. This will depicts

that the organisational effeminacy of the organisation increases with double rate in future. It is

good option for the Starbucks to consider this organisation for the purpose of acquiring in future.

From analysis of profit and loss account with the help of ratios ascertained that Roast Ltd

is in growing stage and having sufficient amount of operations in market. This is good for any

organisation to acquire the operations of this organisation and attain higher position along with

competitive advantage (Lerner and et.al., 2015).

2.2 Statement of Financial Position

Balance sheet introduces to the statement of financial position which helps an

organisation in identification of its assets and liabilities. This will depicts the actual financial

position of organisation in market. From the analysis of the balance sheet of the Roast Ltd.

Determined that their assets and liabilities are increased in year 2018. The total amount of assets

and liabilities ascertained in the year 2017 was 1017000 pound which was increased and attained

the mark of 1443000 pound in 2018. The increment in the assets and equities presents that

organisation is in sound position (Lungu, Dascalu and Colceag, 2015). For further analysis of the

balance sheet of the organisation some ratios are calculated that presents the position of

organisation in market. Calculation of these ratios along with their interpretation is presented

below:

Current ratio

4

(Kotlar and et.al., 2014.).

Particulars 2017 2018

Operating profit 51 127

Net sales 2022 2534

Formula Operating profit / Net sales *100

Result 2.52% 5.01%

From the above calculation of this ratio in respect to the Roast Ltd. Determined that this

ratio is just attained the double mark in year 2018 as compared to 2017. The figure of ratio

ascertained in 2017 was 2.52% and in 2018 the figure increase up to 5.01%. This will depicts

that the organisational effeminacy of the organisation increases with double rate in future. It is

good option for the Starbucks to consider this organisation for the purpose of acquiring in future.

From analysis of profit and loss account with the help of ratios ascertained that Roast Ltd

is in growing stage and having sufficient amount of operations in market. This is good for any

organisation to acquire the operations of this organisation and attain higher position along with

competitive advantage (Lerner and et.al., 2015).

2.2 Statement of Financial Position

Balance sheet introduces to the statement of financial position which helps an

organisation in identification of its assets and liabilities. This will depicts the actual financial

position of organisation in market. From the analysis of the balance sheet of the Roast Ltd.

Determined that their assets and liabilities are increased in year 2018. The total amount of assets

and liabilities ascertained in the year 2017 was 1017000 pound which was increased and attained

the mark of 1443000 pound in 2018. The increment in the assets and equities presents that

organisation is in sound position (Lungu, Dascalu and Colceag, 2015). For further analysis of the

balance sheet of the organisation some ratios are calculated that presents the position of

organisation in market. Calculation of these ratios along with their interpretation is presented

below:

Current ratio

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

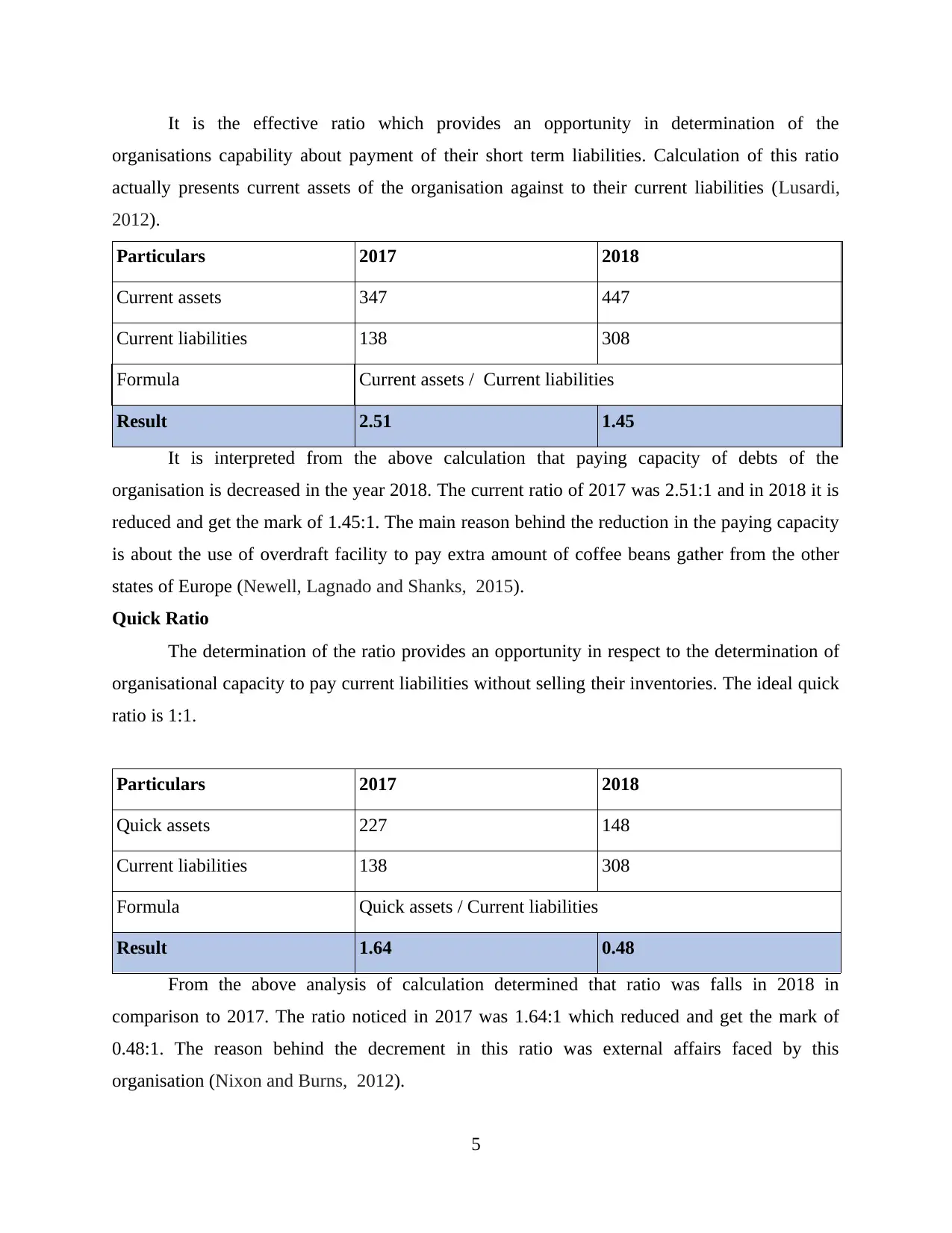

It is the effective ratio which provides an opportunity in determination of the

organisations capability about payment of their short term liabilities. Calculation of this ratio

actually presents current assets of the organisation against to their current liabilities (Lusardi,

2012).

Particulars 2017 2018

Current assets 347 447

Current liabilities 138 308

Formula Current assets / Current liabilities

Result 2.51 1.45

It is interpreted from the above calculation that paying capacity of debts of the

organisation is decreased in the year 2018. The current ratio of 2017 was 2.51:1 and in 2018 it is

reduced and get the mark of 1.45:1. The main reason behind the reduction in the paying capacity

is about the use of overdraft facility to pay extra amount of coffee beans gather from the other

states of Europe (Newell, Lagnado and Shanks, 2015).

Quick Ratio

The determination of the ratio provides an opportunity in respect to the determination of

organisational capacity to pay current liabilities without selling their inventories. The ideal quick

ratio is 1:1.

Particulars 2017 2018

Quick assets 227 148

Current liabilities 138 308

Formula Quick assets / Current liabilities

Result 1.64 0.48

From the above analysis of calculation determined that ratio was falls in 2018 in

comparison to 2017. The ratio noticed in 2017 was 1.64:1 which reduced and get the mark of

0.48:1. The reason behind the decrement in this ratio was external affairs faced by this

organisation (Nixon and Burns, 2012).

5

organisations capability about payment of their short term liabilities. Calculation of this ratio

actually presents current assets of the organisation against to their current liabilities (Lusardi,

2012).

Particulars 2017 2018

Current assets 347 447

Current liabilities 138 308

Formula Current assets / Current liabilities

Result 2.51 1.45

It is interpreted from the above calculation that paying capacity of debts of the

organisation is decreased in the year 2018. The current ratio of 2017 was 2.51:1 and in 2018 it is

reduced and get the mark of 1.45:1. The main reason behind the reduction in the paying capacity

is about the use of overdraft facility to pay extra amount of coffee beans gather from the other

states of Europe (Newell, Lagnado and Shanks, 2015).

Quick Ratio

The determination of the ratio provides an opportunity in respect to the determination of

organisational capacity to pay current liabilities without selling their inventories. The ideal quick

ratio is 1:1.

Particulars 2017 2018

Quick assets 227 148

Current liabilities 138 308

Formula Quick assets / Current liabilities

Result 1.64 0.48

From the above analysis of calculation determined that ratio was falls in 2018 in

comparison to 2017. The ratio noticed in 2017 was 1.64:1 which reduced and get the mark of

0.48:1. The reason behind the decrement in this ratio was external affairs faced by this

organisation (Nixon and Burns, 2012).

5

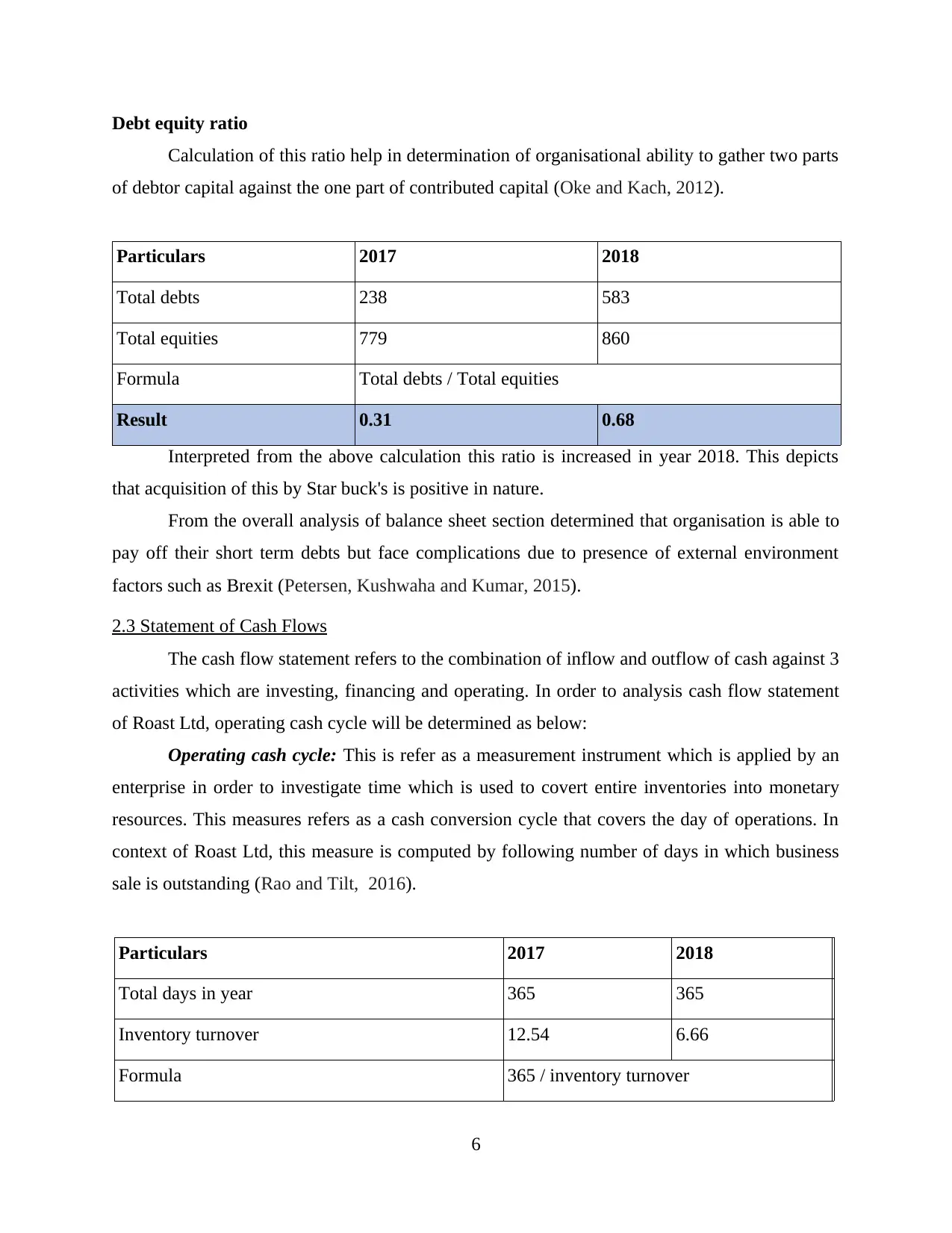

Debt equity ratio

Calculation of this ratio help in determination of organisational ability to gather two parts

of debtor capital against the one part of contributed capital (Oke and Kach, 2012).

Particulars 2017 2018

Total debts 238 583

Total equities 779 860

Formula Total debts / Total equities

Result 0.31 0.68

Interpreted from the above calculation this ratio is increased in year 2018. This depicts

that acquisition of this by Star buck's is positive in nature.

From the overall analysis of balance sheet section determined that organisation is able to

pay off their short term debts but face complications due to presence of external environment

factors such as Brexit (Petersen, Kushwaha and Kumar, 2015).

2.3 Statement of Cash Flows

The cash flow statement refers to the combination of inflow and outflow of cash against 3

activities which are investing, financing and operating. In order to analysis cash flow statement

of Roast Ltd, operating cash cycle will be determined as below:

Operating cash cycle: This is refer as a measurement instrument which is applied by an

enterprise in order to investigate time which is used to covert entire inventories into monetary

resources. This measures refers as a cash conversion cycle that covers the day of operations. In

context of Roast Ltd, this measure is computed by following number of days in which business

sale is outstanding (Rao and Tilt, 2016).

Particulars 2017 2018

Total days in year 365 365

Inventory turnover 12.54 6.66

Formula 365 / inventory turnover

6

Calculation of this ratio help in determination of organisational ability to gather two parts

of debtor capital against the one part of contributed capital (Oke and Kach, 2012).

Particulars 2017 2018

Total debts 238 583

Total equities 779 860

Formula Total debts / Total equities

Result 0.31 0.68

Interpreted from the above calculation this ratio is increased in year 2018. This depicts

that acquisition of this by Star buck's is positive in nature.

From the overall analysis of balance sheet section determined that organisation is able to

pay off their short term debts but face complications due to presence of external environment

factors such as Brexit (Petersen, Kushwaha and Kumar, 2015).

2.3 Statement of Cash Flows

The cash flow statement refers to the combination of inflow and outflow of cash against 3

activities which are investing, financing and operating. In order to analysis cash flow statement

of Roast Ltd, operating cash cycle will be determined as below:

Operating cash cycle: This is refer as a measurement instrument which is applied by an

enterprise in order to investigate time which is used to covert entire inventories into monetary

resources. This measures refers as a cash conversion cycle that covers the day of operations. In

context of Roast Ltd, this measure is computed by following number of days in which business

sale is outstanding (Rao and Tilt, 2016).

Particulars 2017 2018

Total days in year 365 365

Inventory turnover 12.54 6.66

Formula 365 / inventory turnover

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

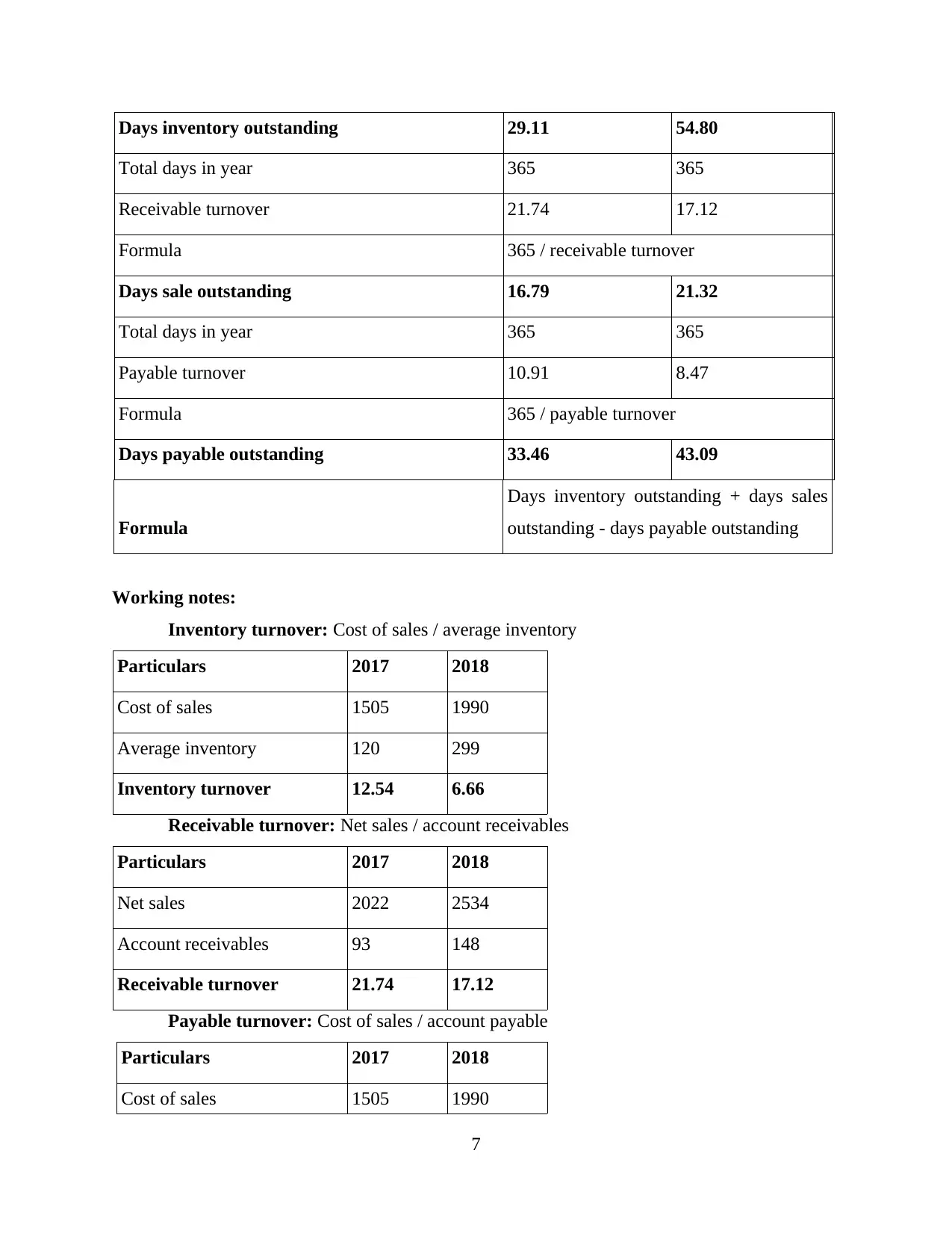

Days inventory outstanding 29.11 54.80

Total days in year 365 365

Receivable turnover 21.74 17.12

Formula 365 / receivable turnover

Days sale outstanding 16.79 21.32

Total days in year 365 365

Payable turnover 10.91 8.47

Formula 365 / payable turnover

Days payable outstanding 33.46 43.09

Formula

Days inventory outstanding + days sales

outstanding - days payable outstanding

Working notes:

Inventory turnover: Cost of sales / average inventory

Particulars 2017 2018

Cost of sales 1505 1990

Average inventory 120 299

Inventory turnover 12.54 6.66

Receivable turnover: Net sales / account receivables

Particulars 2017 2018

Net sales 2022 2534

Account receivables 93 148

Receivable turnover 21.74 17.12

Payable turnover: Cost of sales / account payable

Particulars 2017 2018

Cost of sales 1505 1990

7

Total days in year 365 365

Receivable turnover 21.74 17.12

Formula 365 / receivable turnover

Days sale outstanding 16.79 21.32

Total days in year 365 365

Payable turnover 10.91 8.47

Formula 365 / payable turnover

Days payable outstanding 33.46 43.09

Formula

Days inventory outstanding + days sales

outstanding - days payable outstanding

Working notes:

Inventory turnover: Cost of sales / average inventory

Particulars 2017 2018

Cost of sales 1505 1990

Average inventory 120 299

Inventory turnover 12.54 6.66

Receivable turnover: Net sales / account receivables

Particulars 2017 2018

Net sales 2022 2534

Account receivables 93 148

Receivable turnover 21.74 17.12

Payable turnover: Cost of sales / account payable

Particulars 2017 2018

Cost of sales 1505 1990

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

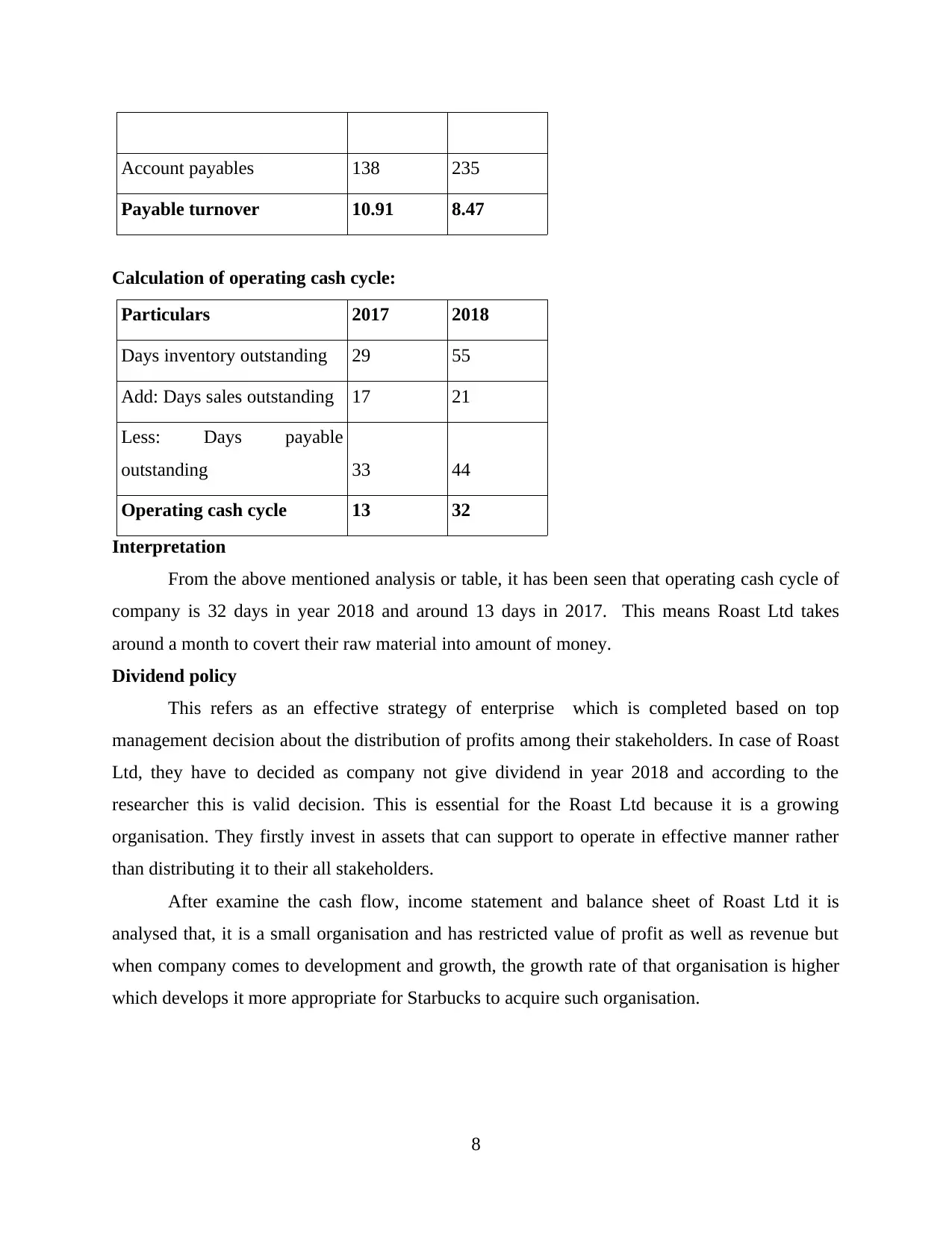

Account payables 138 235

Payable turnover 10.91 8.47

Calculation of operating cash cycle:

Particulars 2017 2018

Days inventory outstanding 29 55

Add: Days sales outstanding 17 21

Less: Days payable

outstanding 33 44

Operating cash cycle 13 32

Interpretation

From the above mentioned analysis or table, it has been seen that operating cash cycle of

company is 32 days in year 2018 and around 13 days in 2017. This means Roast Ltd takes

around a month to covert their raw material into amount of money.

Dividend policy

This refers as an effective strategy of enterprise which is completed based on top

management decision about the distribution of profits among their stakeholders. In case of Roast

Ltd, they have to decided as company not give dividend in year 2018 and according to the

researcher this is valid decision. This is essential for the Roast Ltd because it is a growing

organisation. They firstly invest in assets that can support to operate in effective manner rather

than distributing it to their all stakeholders.

After examine the cash flow, income statement and balance sheet of Roast Ltd it is

analysed that, it is a small organisation and has restricted value of profit as well as revenue but

when company comes to development and growth, the growth rate of that organisation is higher

which develops it more appropriate for Starbucks to acquire such organisation.

8

Payable turnover 10.91 8.47

Calculation of operating cash cycle:

Particulars 2017 2018

Days inventory outstanding 29 55

Add: Days sales outstanding 17 21

Less: Days payable

outstanding 33 44

Operating cash cycle 13 32

Interpretation

From the above mentioned analysis or table, it has been seen that operating cash cycle of

company is 32 days in year 2018 and around 13 days in 2017. This means Roast Ltd takes

around a month to covert their raw material into amount of money.

Dividend policy

This refers as an effective strategy of enterprise which is completed based on top

management decision about the distribution of profits among their stakeholders. In case of Roast

Ltd, they have to decided as company not give dividend in year 2018 and according to the

researcher this is valid decision. This is essential for the Roast Ltd because it is a growing

organisation. They firstly invest in assets that can support to operate in effective manner rather

than distributing it to their all stakeholders.

After examine the cash flow, income statement and balance sheet of Roast Ltd it is

analysed that, it is a small organisation and has restricted value of profit as well as revenue but

when company comes to development and growth, the growth rate of that organisation is higher

which develops it more appropriate for Starbucks to acquire such organisation.

8

Part 3: Investment Appraisal and Sources of Finance

3.1 Investment Appraisal

Management Forecast

Roast limited is one of the growing firm which is planning to expand its business

operations in Romania by introducing new coffee outlet in the region. The company's

administration has decided to introduced this project in year 2017. The prediction by

management reflects that company will earn £300 million of revenue in year 2017 which will

increase in 2018 as £560 million, £740 million in year 2019, £900 million in 2020 and in year

2021, £1120 millions. High variable cost will be incur by company on its operations and will

secure adequate cash flows. The forecasted values of cash inflows includes £60 million in year

2017, in 2018 the value is £112 million, £148 millions in year 2019, £180 millions and £224

millions in year 2020 and 2021.

The above mentioned analysis depicts that organisation will generate higher profits and

revenues in tenure of 5 years. In the forecast of management, no contingencies are included

which may results in financial problems (Seshan and Yang, 2014).

Investment Appraisal Techniques

Payback period

Payback period can be defined as the time which a company needed to recover the initial

investment made by it. This is an investment appraisal approach that is assistive to company in

determining that how much time is taken by it to recoup the initial investments made. It is

observed that the payback period of company is to be 4 years which determines that it recovers

£500 millions of investment in the period of four years only. There are some advantages and

drawbacks of utilizing payback period technique. Companies use this tool as it is easily

understandable and simple to use which do not require any additional skills to calculate payback

period. It administers quick solution and is utilize in uncertainty situation. Apart from these

advantages, there are some disadvantages also as the technique involves unlike coverage of cash

flows and ignorance to time value of money. An analysis can be limit by this approach by

disregard return on investment as well profitability margin (Starcke and Brand, 2012).

Accounting Rate of Return

Accounting rate of return is also average rate of return (ARR) which can be defined as a

financial ratio that is utilized in capital budgeting. The time value of money concept is not taken

9

3.1 Investment Appraisal

Management Forecast

Roast limited is one of the growing firm which is planning to expand its business

operations in Romania by introducing new coffee outlet in the region. The company's

administration has decided to introduced this project in year 2017. The prediction by

management reflects that company will earn £300 million of revenue in year 2017 which will

increase in 2018 as £560 million, £740 million in year 2019, £900 million in 2020 and in year

2021, £1120 millions. High variable cost will be incur by company on its operations and will

secure adequate cash flows. The forecasted values of cash inflows includes £60 million in year

2017, in 2018 the value is £112 million, £148 millions in year 2019, £180 millions and £224

millions in year 2020 and 2021.

The above mentioned analysis depicts that organisation will generate higher profits and

revenues in tenure of 5 years. In the forecast of management, no contingencies are included

which may results in financial problems (Seshan and Yang, 2014).

Investment Appraisal Techniques

Payback period

Payback period can be defined as the time which a company needed to recover the initial

investment made by it. This is an investment appraisal approach that is assistive to company in

determining that how much time is taken by it to recoup the initial investments made. It is

observed that the payback period of company is to be 4 years which determines that it recovers

£500 millions of investment in the period of four years only. There are some advantages and

drawbacks of utilizing payback period technique. Companies use this tool as it is easily

understandable and simple to use which do not require any additional skills to calculate payback

period. It administers quick solution and is utilize in uncertainty situation. Apart from these

advantages, there are some disadvantages also as the technique involves unlike coverage of cash

flows and ignorance to time value of money. An analysis can be limit by this approach by

disregard return on investment as well profitability margin (Starcke and Brand, 2012).

Accounting Rate of Return

Accounting rate of return is also average rate of return (ARR) which can be defined as a

financial ratio that is utilized in capital budgeting. The time value of money concept is not taken

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.