In-depth Financial Performance Analysis of Spritzer BHD, Malaysia

VerifiedAdded on 2023/04/07

|20

|3359

|221

Report

AI Summary

This report provides a comprehensive financial performance analysis of Spritzer BHD, a Malaysian water bottling company. It examines various financial aspects, including competitor and industry analysis, liquidity, profitability, and efficiency ratios. The report calculates working capital, analyzes the company's capital structure, and evaluates stock performance. Key findings indicate improvements in liquidity ratios, stable gross profit margins, but concerns regarding net profit margins and return on capital employed. The efficiency analysis reveals a good inventory control system, but challenges in collecting receivables. The report concludes with recommendations for maintaining optimal working capital levels and improving profitability.

Running head: FINANCIAL PERFORMANCE ANALYSIS

Financial Performance Analysis

Name of the Student

Name of the University

Author Note

Financial Performance Analysis

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL PERFORMANCE ANALYSIS

Executive Summary

The purpose of the project is to determine the financial position of a company by measuring the

financial performances of the Spritzer Company. Different tools of measuring the financial

performance has been utilised in this report. A water producing, packaging and bottling

manufacturing company, namely Spritzer has been selected in this report. The profitability,

liquidity and efficiency ratios have been calculated. The working capital has been calculated and

the capital structure of the company is also analysed. The stock performance analysis has also

been portrayed in this report. The report is concluded by proper discussion of the financial

position of the company with lights on all the key financial indicators.

Executive Summary

The purpose of the project is to determine the financial position of a company by measuring the

financial performances of the Spritzer Company. Different tools of measuring the financial

performance has been utilised in this report. A water producing, packaging and bottling

manufacturing company, namely Spritzer has been selected in this report. The profitability,

liquidity and efficiency ratios have been calculated. The working capital has been calculated and

the capital structure of the company is also analysed. The stock performance analysis has also

been portrayed in this report. The report is concluded by proper discussion of the financial

position of the company with lights on all the key financial indicators.

2FINANCIAL PERFORMANCE ANALYSIS

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................3

Competitor Analysis....................................................................................................................3

Industry Analysis.........................................................................................................................4

Financial Analysis.......................................................................................................................4

Ratio Analysis..............................................................................................................................5

Working Capital Management.....................................................................................................9

Stock Ratio Analysis..................................................................................................................12

Stock Performance Analysis......................................................................................................14

Conclusion and Recommendations................................................................................................14

References......................................................................................................................................16

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................3

Competitor Analysis....................................................................................................................3

Industry Analysis.........................................................................................................................4

Financial Analysis.......................................................................................................................4

Ratio Analysis..............................................................................................................................5

Working Capital Management.....................................................................................................9

Stock Ratio Analysis..................................................................................................................12

Stock Performance Analysis......................................................................................................14

Conclusion and Recommendations................................................................................................14

References......................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL PERFORMANCE ANALYSIS

Introduction

The financial performance of a company determines the financial stability of that

company. The goodwill and the stability of the business in the long run solely depend upon how

the company is performing. Financial performance therefore refers to performing all such

financial activities that helps the organisation in achieving the financial objectives in a flexible

manner. The financial performance helps in analysing about the financial condition and the

position of a given organisation at a given period of time and how are the financial indicators

performing over the time. The financial performance analysis thus involves analysing the

balance sheet and thereafter finding out about the capital structure, the working capital and the

ratio values of the organisation. In the given report the financial performance analysis of Spritzer

BHD has been done (SPTZ 2018).

Discussion

Spritzer is one of the bestselling mineral water in Malaysia. This company specifically

manufactures and distributes natural mineral water, drinking water that is distilled, flavoured

drinks, carbonated and non carbonated flavoured food drinks, sparkling natural mineral water. It

is also involved in the packaging of the water bottles. The sources of the water are pure and they

are kept clean and protected by the people of Taiping (Perak Lakshmi et al. 2016).

Competitor Analysis

The company is one of the largest producers of bottled water in Malaysia and is having

more than 40% of market share. The top competitors of Spritzer are One Water, Ocean Mineral

Water, Malee Mineral Water and Dasani. The company is dominating inspite of having these top

Introduction

The financial performance of a company determines the financial stability of that

company. The goodwill and the stability of the business in the long run solely depend upon how

the company is performing. Financial performance therefore refers to performing all such

financial activities that helps the organisation in achieving the financial objectives in a flexible

manner. The financial performance helps in analysing about the financial condition and the

position of a given organisation at a given period of time and how are the financial indicators

performing over the time. The financial performance analysis thus involves analysing the

balance sheet and thereafter finding out about the capital structure, the working capital and the

ratio values of the organisation. In the given report the financial performance analysis of Spritzer

BHD has been done (SPTZ 2018).

Discussion

Spritzer is one of the bestselling mineral water in Malaysia. This company specifically

manufactures and distributes natural mineral water, drinking water that is distilled, flavoured

drinks, carbonated and non carbonated flavoured food drinks, sparkling natural mineral water. It

is also involved in the packaging of the water bottles. The sources of the water are pure and they

are kept clean and protected by the people of Taiping (Perak Lakshmi et al. 2016).

Competitor Analysis

The company is one of the largest producers of bottled water in Malaysia and is having

more than 40% of market share. The top competitors of Spritzer are One Water, Ocean Mineral

Water, Malee Mineral Water and Dasani. The company is dominating inspite of having these top

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL PERFORMANCE ANALYSIS

competitors because of its differentiation in the product, the low cost of production and the high

entry of entry and exit barriers in this industry (Easton and Sommers 2018).

Industry Analysis

The company has a good and clean source of water at the facility at Taiping facility

because of which it can sell its product at higher prices than the other drinking waters. The

company also have its own bottle and cap manufacturing unit, its own warehouse and also owns

a distribution channel (Finance.yahoo.com 2017). The bottles produced by the company also

have a unique shape that does not waste any spaces unnecessarily. There are different bottles for

different types of age group for example the Spritzer pop bottles are targeted towards the kids.

The green colour on the bottle with a large logo on the front has been done in order to make the

bottle look nature friendly. Therefore the company has positioned themselves as one of the most

nature friendly water producer as well as bottle manufacturers (Markets.ft.com 2017). The

market of this company is segmented as per the basis of its flavour type, origin as well as sales

channel. The company involves a number of friendly hands in their activities. The key players

involved with this company are Hoxie Spritzer, The Grand Canyon Wine Co., Union Wine

Company, Porch Pounder, Latitude Beverage Co. Mancan Wine LLC. and Francis and Ford

Coppola Winery (Rodrigues and Rodrigues 2018).

Financial Analysis

The financial position of the company has been determined by calculating the various

kinds of ratios like the liquidity ratio, the profitability ratios, capital structure ratios, working

capital as well as the stock performance analysis. The following paragraphs explains the

company’s performance with respect to each of these financial ratios (Islam 2014).

competitors because of its differentiation in the product, the low cost of production and the high

entry of entry and exit barriers in this industry (Easton and Sommers 2018).

Industry Analysis

The company has a good and clean source of water at the facility at Taiping facility

because of which it can sell its product at higher prices than the other drinking waters. The

company also have its own bottle and cap manufacturing unit, its own warehouse and also owns

a distribution channel (Finance.yahoo.com 2017). The bottles produced by the company also

have a unique shape that does not waste any spaces unnecessarily. There are different bottles for

different types of age group for example the Spritzer pop bottles are targeted towards the kids.

The green colour on the bottle with a large logo on the front has been done in order to make the

bottle look nature friendly. Therefore the company has positioned themselves as one of the most

nature friendly water producer as well as bottle manufacturers (Markets.ft.com 2017). The

market of this company is segmented as per the basis of its flavour type, origin as well as sales

channel. The company involves a number of friendly hands in their activities. The key players

involved with this company are Hoxie Spritzer, The Grand Canyon Wine Co., Union Wine

Company, Porch Pounder, Latitude Beverage Co. Mancan Wine LLC. and Francis and Ford

Coppola Winery (Rodrigues and Rodrigues 2018).

Financial Analysis

The financial position of the company has been determined by calculating the various

kinds of ratios like the liquidity ratio, the profitability ratios, capital structure ratios, working

capital as well as the stock performance analysis. The following paragraphs explains the

company’s performance with respect to each of these financial ratios (Islam 2014).

5FINANCIAL PERFORMANCE ANALYSIS

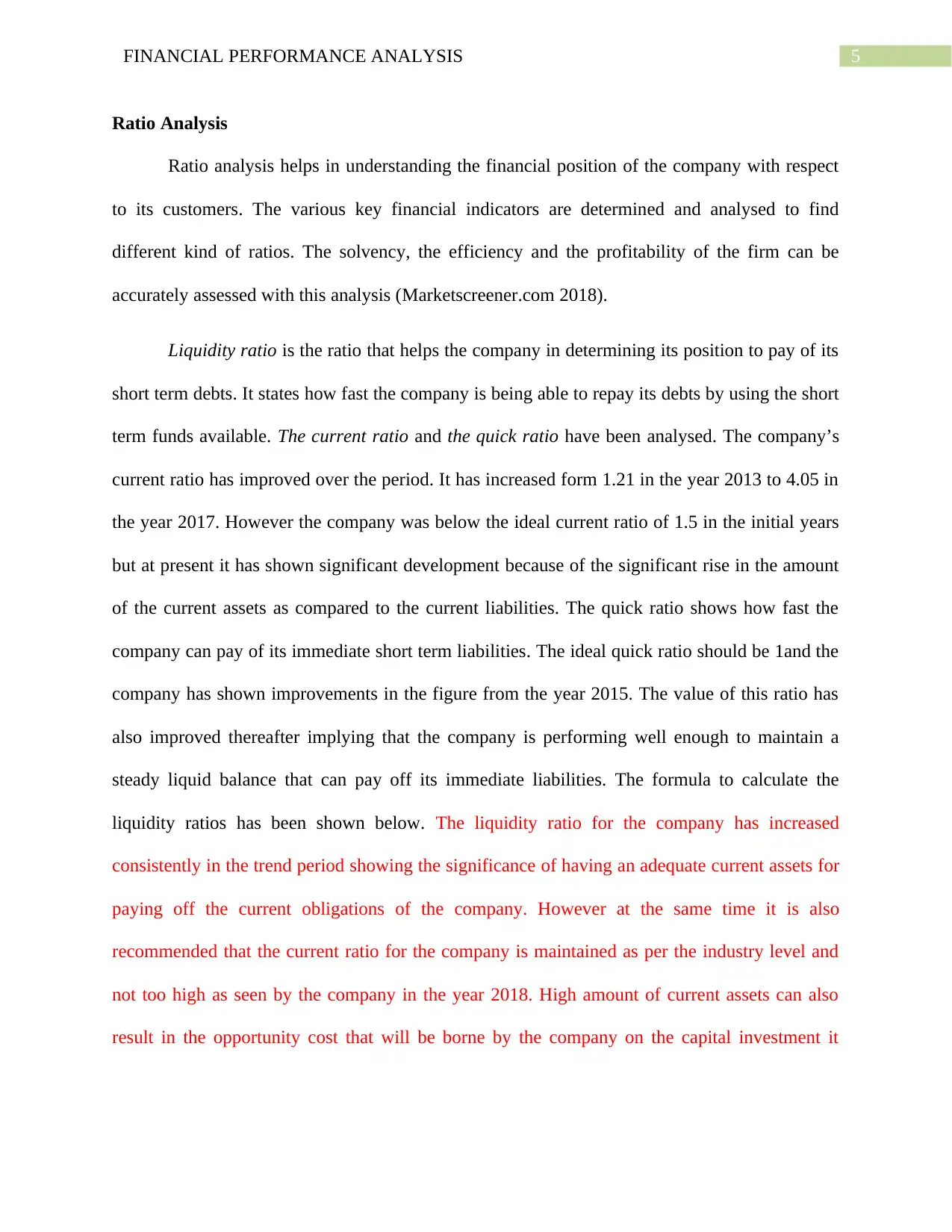

Ratio Analysis

Ratio analysis helps in understanding the financial position of the company with respect

to its customers. The various key financial indicators are determined and analysed to find

different kind of ratios. The solvency, the efficiency and the profitability of the firm can be

accurately assessed with this analysis (Marketscreener.com 2018).

Liquidity ratio is the ratio that helps the company in determining its position to pay of its

short term debts. It states how fast the company is being able to repay its debts by using the short

term funds available. The current ratio and the quick ratio have been analysed. The company’s

current ratio has improved over the period. It has increased form 1.21 in the year 2013 to 4.05 in

the year 2017. However the company was below the ideal current ratio of 1.5 in the initial years

but at present it has shown significant development because of the significant rise in the amount

of the current assets as compared to the current liabilities. The quick ratio shows how fast the

company can pay of its immediate short term liabilities. The ideal quick ratio should be 1and the

company has shown improvements in the figure from the year 2015. The value of this ratio has

also improved thereafter implying that the company is performing well enough to maintain a

steady liquid balance that can pay off its immediate liabilities. The formula to calculate the

liquidity ratios has been shown below. The liquidity ratio for the company has increased

consistently in the trend period showing the significance of having an adequate current assets for

paying off the current obligations of the company. However at the same time it is also

recommended that the current ratio for the company is maintained as per the industry level and

not too high as seen by the company in the year 2018. High amount of current assets can also

result in the opportunity cost that will be borne by the company on the capital investment it

Ratio Analysis

Ratio analysis helps in understanding the financial position of the company with respect

to its customers. The various key financial indicators are determined and analysed to find

different kind of ratios. The solvency, the efficiency and the profitability of the firm can be

accurately assessed with this analysis (Marketscreener.com 2018).

Liquidity ratio is the ratio that helps the company in determining its position to pay of its

short term debts. It states how fast the company is being able to repay its debts by using the short

term funds available. The current ratio and the quick ratio have been analysed. The company’s

current ratio has improved over the period. It has increased form 1.21 in the year 2013 to 4.05 in

the year 2017. However the company was below the ideal current ratio of 1.5 in the initial years

but at present it has shown significant development because of the significant rise in the amount

of the current assets as compared to the current liabilities. The quick ratio shows how fast the

company can pay of its immediate short term liabilities. The ideal quick ratio should be 1and the

company has shown improvements in the figure from the year 2015. The value of this ratio has

also improved thereafter implying that the company is performing well enough to maintain a

steady liquid balance that can pay off its immediate liabilities. The formula to calculate the

liquidity ratios has been shown below. The liquidity ratio for the company has increased

consistently in the trend period showing the significance of having an adequate current assets for

paying off the current obligations of the company. However at the same time it is also

recommended that the current ratio for the company is maintained as per the industry level and

not too high as seen by the company in the year 2018. High amount of current assets can also

result in the opportunity cost that will be borne by the company on the capital investment it

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL PERFORMANCE ANALYSIS

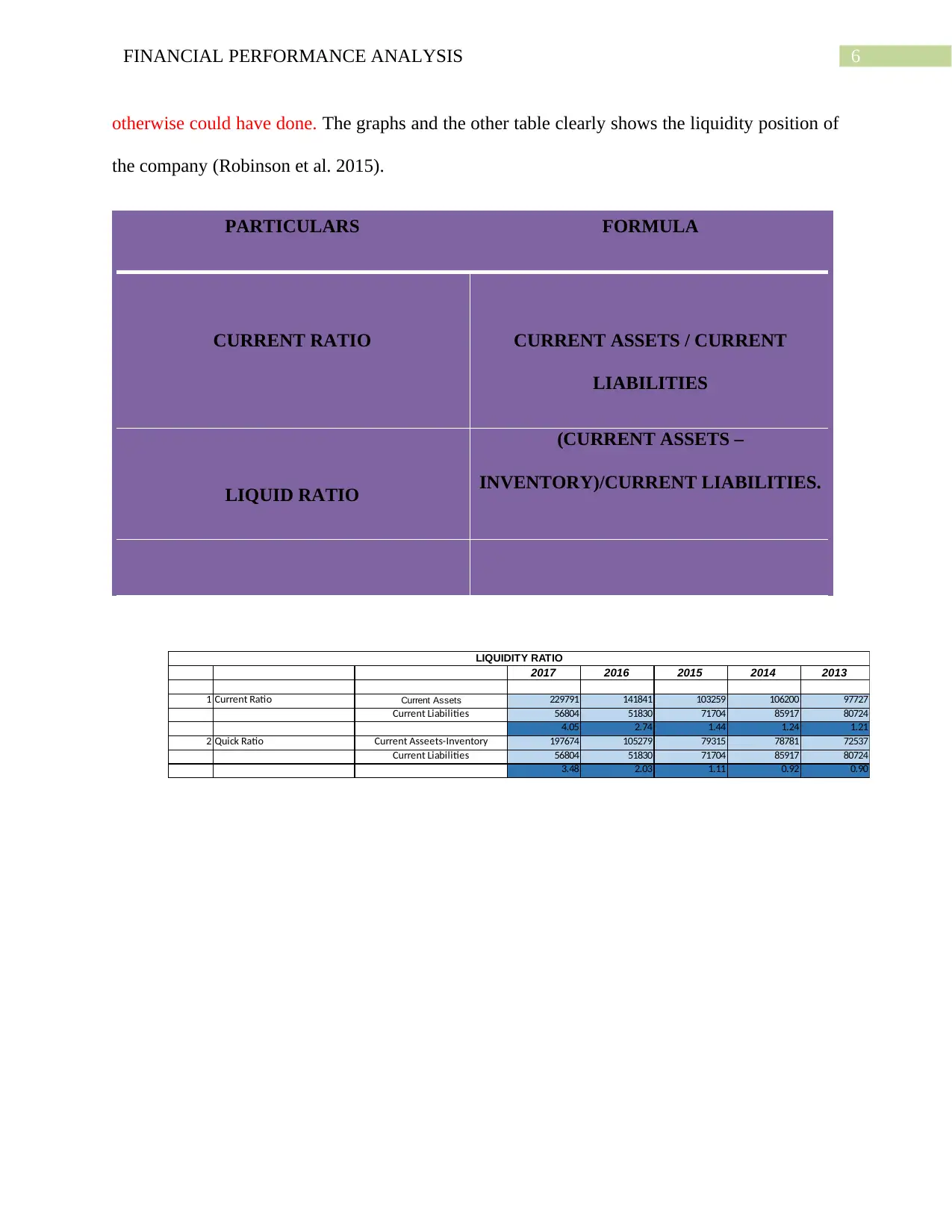

otherwise could have done. The graphs and the other table clearly shows the liquidity position of

the company (Robinson et al. 2015).

PARTICULARS FORMULA

CURRENT RATIO CURRENT ASSETS / CURRENT

LIABILITIES

LIQUID RATIO

(CURRENT ASSETS –

INVENTORY)/CURRENT LIABILITIES.

2017 2016 2015 2014 2013

1 Current Ratio Current Assets 229791 141841 103259 106200 97727

Current Liabilities 56804 51830 71704 85917 80724

4.05 2.74 1.44 1.24 1.21

2 Quick Ratio Current Asseets-Inventory 197674 105279 79315 78781 72537

Current Liabilities 56804 51830 71704 85917 80724

3.48 2.03 1.11 0.92 0.90

LIQUIDITY RATIO

otherwise could have done. The graphs and the other table clearly shows the liquidity position of

the company (Robinson et al. 2015).

PARTICULARS FORMULA

CURRENT RATIO CURRENT ASSETS / CURRENT

LIABILITIES

LIQUID RATIO

(CURRENT ASSETS –

INVENTORY)/CURRENT LIABILITIES.

2017 2016 2015 2014 2013

1 Current Ratio Current Assets 229791 141841 103259 106200 97727

Current Liabilities 56804 51830 71704 85917 80724

4.05 2.74 1.44 1.24 1.21

2 Quick Ratio Current Asseets-Inventory 197674 105279 79315 78781 72537

Current Liabilities 56804 51830 71704 85917 80724

3.48 2.03 1.11 0.92 0.90

LIQUIDITY RATIO

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL PERFORMANCE ANALYSIS

2017 2016 2015 2014 2013

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

Liquidity Rati o

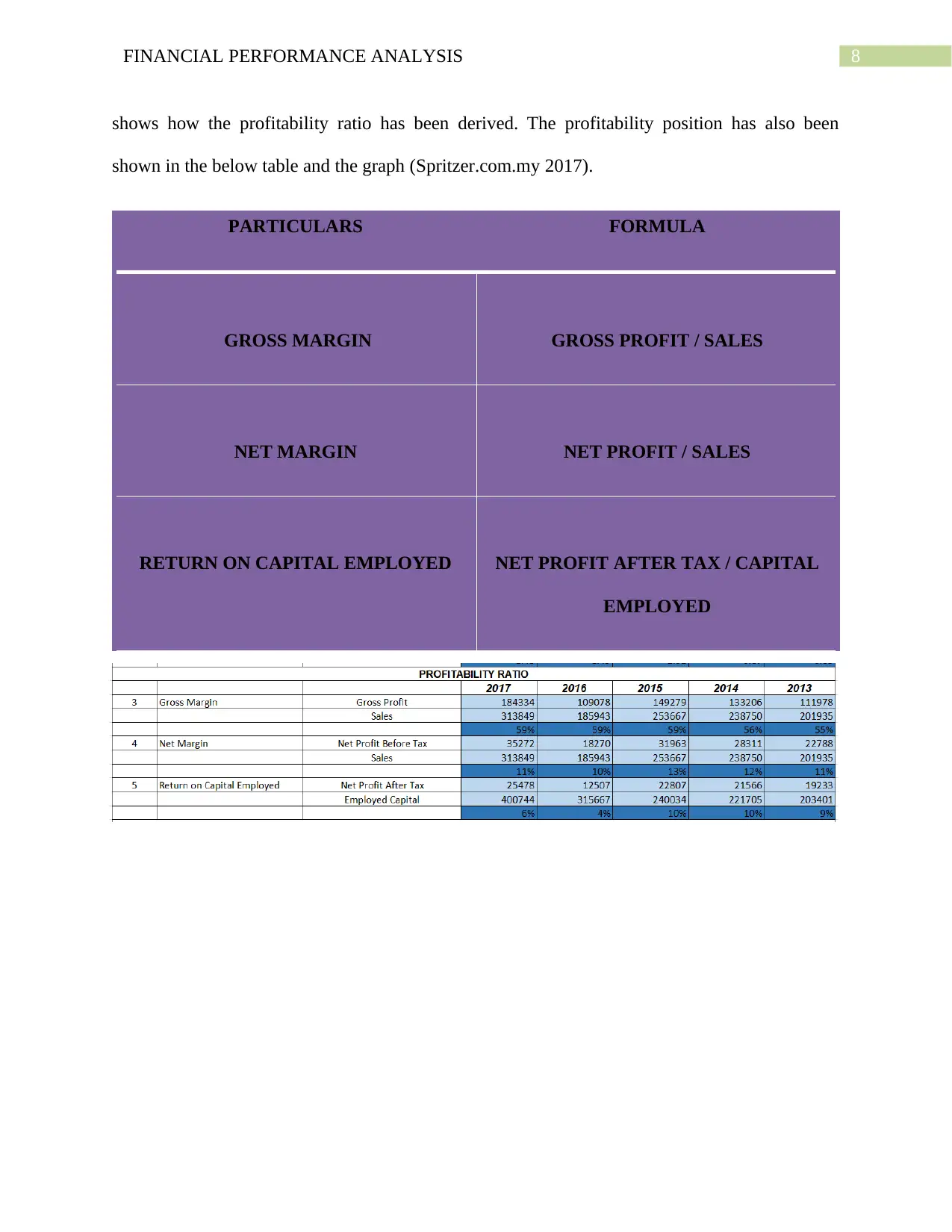

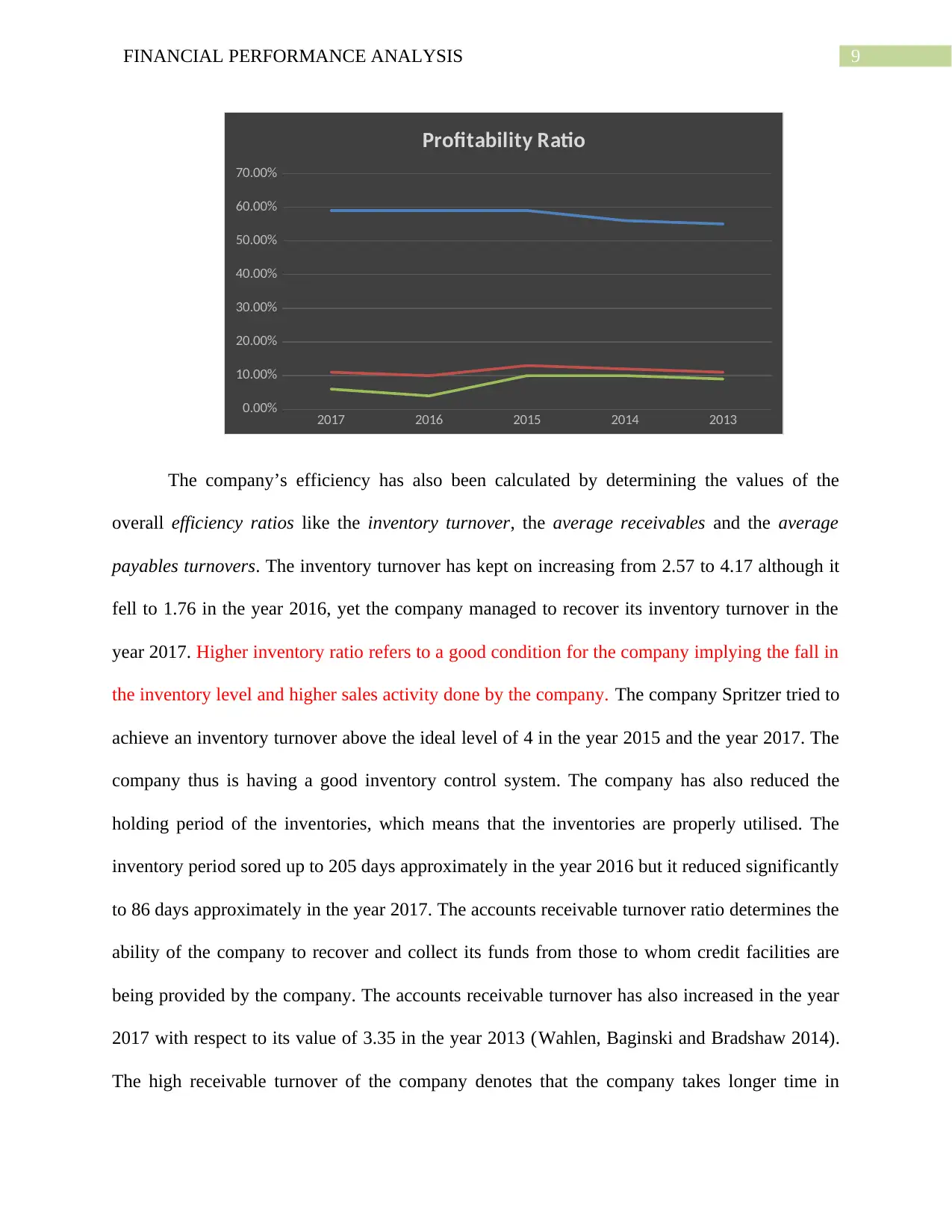

The profitability ratio helps the company in understanding the amount of revenue that has

been generated by it in relation to its costs. High profitability means a good financial condition

and low profitability is a bad indicator. The gross margin, net margin and the return on the

capital employed has been calculated here in order to understand the profitability of the firm. The

gross margin has been calculated by dividing the gross profit with the sales. The firm has

maintained a stable gross margin above the ideal margin of 50% (Spritzer.com.my 2017). The

gross profit margin is more or less stable (Spritzer.com.my 2016). The net profit margin is

however below 15%, which is a concern. This means the operating expenses are high. The net

profit margin was improving but it fell down in the year 2016. The return on capital employees

has been stable in the initial years but it also reduced significantly in the year 2016, which means

that the capital is not being properly used and is not giving enough returns. The higher the return

on the capital employed the better it will be for the company. In the context of profitability the

operating profitability of the company looks stable but the return on capital employed for the

company has been volatile due to the changing equity base of the company. The following table

2017 2016 2015 2014 2013

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

Liquidity Rati o

The profitability ratio helps the company in understanding the amount of revenue that has

been generated by it in relation to its costs. High profitability means a good financial condition

and low profitability is a bad indicator. The gross margin, net margin and the return on the

capital employed has been calculated here in order to understand the profitability of the firm. The

gross margin has been calculated by dividing the gross profit with the sales. The firm has

maintained a stable gross margin above the ideal margin of 50% (Spritzer.com.my 2017). The

gross profit margin is more or less stable (Spritzer.com.my 2016). The net profit margin is

however below 15%, which is a concern. This means the operating expenses are high. The net

profit margin was improving but it fell down in the year 2016. The return on capital employees

has been stable in the initial years but it also reduced significantly in the year 2016, which means

that the capital is not being properly used and is not giving enough returns. The higher the return

on the capital employed the better it will be for the company. In the context of profitability the

operating profitability of the company looks stable but the return on capital employed for the

company has been volatile due to the changing equity base of the company. The following table

8FINANCIAL PERFORMANCE ANALYSIS

shows how the profitability ratio has been derived. The profitability position has also been

shown in the below table and the graph (Spritzer.com.my 2017).

PARTICULARS FORMULA

GROSS MARGIN GROSS PROFIT / SALES

NET MARGIN NET PROFIT / SALES

RETURN ON CAPITAL EMPLOYED NET PROFIT AFTER TAX / CAPITAL

EMPLOYED

shows how the profitability ratio has been derived. The profitability position has also been

shown in the below table and the graph (Spritzer.com.my 2017).

PARTICULARS FORMULA

GROSS MARGIN GROSS PROFIT / SALES

NET MARGIN NET PROFIT / SALES

RETURN ON CAPITAL EMPLOYED NET PROFIT AFTER TAX / CAPITAL

EMPLOYED

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL PERFORMANCE ANALYSIS

2017 2016 2015 2014 2013

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

Profitability Ratio

The company’s efficiency has also been calculated by determining the values of the

overall efficiency ratios like the inventory turnover, the average receivables and the average

payables turnovers. The inventory turnover has kept on increasing from 2.57 to 4.17 although it

fell to 1.76 in the year 2016, yet the company managed to recover its inventory turnover in the

year 2017. Higher inventory ratio refers to a good condition for the company implying the fall in

the inventory level and higher sales activity done by the company. The company Spritzer tried to

achieve an inventory turnover above the ideal level of 4 in the year 2015 and the year 2017. The

company thus is having a good inventory control system. The company has also reduced the

holding period of the inventories, which means that the inventories are properly utilised. The

inventory period sored up to 205 days approximately in the year 2016 but it reduced significantly

to 86 days approximately in the year 2017. The accounts receivable turnover ratio determines the

ability of the company to recover and collect its funds from those to whom credit facilities are

being provided by the company. The accounts receivable turnover has also increased in the year

2017 with respect to its value of 3.35 in the year 2013 (Wahlen, Baginski and Bradshaw 2014).

The high receivable turnover of the company denotes that the company takes longer time in

2017 2016 2015 2014 2013

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

Profitability Ratio

The company’s efficiency has also been calculated by determining the values of the

overall efficiency ratios like the inventory turnover, the average receivables and the average

payables turnovers. The inventory turnover has kept on increasing from 2.57 to 4.17 although it

fell to 1.76 in the year 2016, yet the company managed to recover its inventory turnover in the

year 2017. Higher inventory ratio refers to a good condition for the company implying the fall in

the inventory level and higher sales activity done by the company. The company Spritzer tried to

achieve an inventory turnover above the ideal level of 4 in the year 2015 and the year 2017. The

company thus is having a good inventory control system. The company has also reduced the

holding period of the inventories, which means that the inventories are properly utilised. The

inventory period sored up to 205 days approximately in the year 2016 but it reduced significantly

to 86 days approximately in the year 2017. The accounts receivable turnover ratio determines the

ability of the company to recover and collect its funds from those to whom credit facilities are

being provided by the company. The accounts receivable turnover has also increased in the year

2017 with respect to its value of 3.35 in the year 2013 (Wahlen, Baginski and Bradshaw 2014).

The high receivable turnover of the company denotes that the company takes longer time in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL PERFORMANCE ANALYSIS

collecting the receivables. The company takes more than 2 months approximately in minimum to

collect its receivables. However it has been seen that the company faced troubles in the year

2016 and has performed much better in order to improve in the year 2017. The year 2017 shows

that in this year the company has taken the minimum number of days to collect its revenues. The

company has also reduced its average payment period to a large extent. The quick payment of

the payables determines the high liquidity and the efficiency of the company in paying of its

liabilities at a fast pace. The accounts payable ratio measures the number of days that the

company usually takes to pay off its creditors. The average payment period in the year 2013 was

110days and it reduced to 74 days in the year 2017 (Williams and Dobelman 2017).

Working Capital Management

Working capital is the difference between the current assets and the current liabilities of

the companies. Working capital should be strictly maintained within the organisation. Neither

very high working capital and nor too low working capital is acceptable. The mid value between

the high and the low is always preferred. The working capital of the company has kept on

increasing and it shows a good indication about the company that the operations of the company

will be smooth. However on the other hand the company should also look after an optimum ratio

of maintaining the same and the same should be kept as per the industry levels. The working

capital as seen in the year 2013 is RM 17003 (in 000) and it has increased every year and the

amount in 2017 is RM 172987 (in 000). When this result is properly noticed it has been seen that

the value of the current assets has more or less increased every year at a higher rate than the

change in the current liabilities. There is an increasing trend in the current assets as seen from the

calculations apart from the period 2015 when the current assets were reduced in comparison to

the year 2014 (Vogel 2014).

collecting the receivables. The company takes more than 2 months approximately in minimum to

collect its receivables. However it has been seen that the company faced troubles in the year

2016 and has performed much better in order to improve in the year 2017. The year 2017 shows

that in this year the company has taken the minimum number of days to collect its revenues. The

company has also reduced its average payment period to a large extent. The quick payment of

the payables determines the high liquidity and the efficiency of the company in paying of its

liabilities at a fast pace. The accounts payable ratio measures the number of days that the

company usually takes to pay off its creditors. The average payment period in the year 2013 was

110days and it reduced to 74 days in the year 2017 (Williams and Dobelman 2017).

Working Capital Management

Working capital is the difference between the current assets and the current liabilities of

the companies. Working capital should be strictly maintained within the organisation. Neither

very high working capital and nor too low working capital is acceptable. The mid value between

the high and the low is always preferred. The working capital of the company has kept on

increasing and it shows a good indication about the company that the operations of the company

will be smooth. However on the other hand the company should also look after an optimum ratio

of maintaining the same and the same should be kept as per the industry levels. The working

capital as seen in the year 2013 is RM 17003 (in 000) and it has increased every year and the

amount in 2017 is RM 172987 (in 000). When this result is properly noticed it has been seen that

the value of the current assets has more or less increased every year at a higher rate than the

change in the current liabilities. There is an increasing trend in the current assets as seen from the

calculations apart from the period 2015 when the current assets were reduced in comparison to

the year 2014 (Vogel 2014).

11FINANCIAL PERFORMANCE ANALYSIS

WORKING CAPITAL = CURRENT ASSETS – CURRENT LIABILITIES

2017

2016

2015

2014

2013

0 20000 40000 60000 80000 100000 120000 140000 160000 180000 200000

Working Capital

Capital Structure

The capital structure of a business organisation is determined by the combination of the

different funds used by it. The fund can be comprised of funds sourced out of own resources as

well as funds that are taken from other financial institutions or corporations. The own funds are

consisted of the equity shares and the preference shares where as the loaned funds consists of the

long term borrowings as well as the debentures. The analysis of the financial statement of

Spritzer has been done and it has been seen that the gearing ratio has shown a continuous

decrease in the value. It has gone down to 6% from 18%. The gearing ratio has been calculated

by dividing the non-current liabilities with the summation of non-current liabilities and equities.

It helps in determining the leverage of the company’s funds that is to analyse to what extent the

operations of the firm are being funded by the equity capital. Higher gearing ratios indicate

WORKING CAPITAL = CURRENT ASSETS – CURRENT LIABILITIES

2017

2016

2015

2014

2013

0 20000 40000 60000 80000 100000 120000 140000 160000 180000 200000

Working Capital

Capital Structure

The capital structure of a business organisation is determined by the combination of the

different funds used by it. The fund can be comprised of funds sourced out of own resources as

well as funds that are taken from other financial institutions or corporations. The own funds are

consisted of the equity shares and the preference shares where as the loaned funds consists of the

long term borrowings as well as the debentures. The analysis of the financial statement of

Spritzer has been done and it has been seen that the gearing ratio has shown a continuous

decrease in the value. It has gone down to 6% from 18%. The gearing ratio has been calculated

by dividing the non-current liabilities with the summation of non-current liabilities and equities.

It helps in determining the leverage of the company’s funds that is to analyse to what extent the

operations of the firm are being funded by the equity capital. Higher gearing ratios indicate

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.