Management Accounting Report: Financial Performance and Strategies

VerifiedAdded on 2020/12/18

|21

|5695

|223

Report

AI Summary

This management accounting report, prepared for Professional Leads, a UK-based accounting firm, provides a detailed overview of management accounting systems. It covers the definition and essential requirements of management accounting, differentiating it from financial accounting, and explores various types of management accounting systems like cost accounting, inventory management, job costing, and price optimizing systems, along with their benefits. The report further delves into different methods of management accounting reporting, including financial, cash, sales, and item cost reports. It includes the preparation of income statements using marginal and absorption costing techniques, comparing their outcomes and advantages. Additionally, it discusses the advantages and disadvantages of budgetary control planning tools and various management accounting systems to address financial problems, along with key performance indicators, offering valuable insights into financial performance and strategic decision-making within organizations.

Management accounting

report

report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

LO 1.................................................................................................................................................1

Management accounting and essential requirements...................................................................1

Different types of methods for management accounting.............................................................2

LO 2.................................................................................................................................................3

Preparation of income statements using different management accounting techniques.............3

LO.3 ................................................................................................................................................5

Explaining the advantages and disadvantages of different planning tools for budgetary control.

......................................................................................................................................................5

LO 4.................................................................................................................................................9

Different management accounting system to be used for reposnding various financial

accounting problems....................................................................................................................9

Key performance indicators.........................................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

LO 1.................................................................................................................................................1

Management accounting and essential requirements...................................................................1

Different types of methods for management accounting.............................................................2

LO 2.................................................................................................................................................3

Preparation of income statements using different management accounting techniques.............3

LO.3 ................................................................................................................................................5

Explaining the advantages and disadvantages of different planning tools for budgetary control.

......................................................................................................................................................5

LO 4.................................................................................................................................................9

Different management accounting system to be used for reposnding various financial

accounting problems....................................................................................................................9

Key performance indicators.........................................................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Management Accounting system is refers to a system adopted by managers as to develop

the efficiency of the company in context with its financial performance. It is a process of

providing all the relevant financial information to the managers so that they could use them and

develop effective strategies for enhancing financial performance of the company and its cost

efficiency as well. Professional leads is a famous accounting firm of UK. It provides accounting

services to various companies. The present study shows a report of an intern as to provide a

brief information about the management accounting system to a client of the company. The

report includes a description of management accounting and management accounting system.

Further, it also shows various types of management accounting system and their requirements

within a business organisation. It shows numerous methods for the management accounting

reporting.

The report also shows preparation of income statement using different techniques of

management accounting. Furthermore, it also shows different planning tools of budgetary control

system and various systems of management accounting that can be adopted by managers as to

respond different financial problems.

LO 1

Management accounting and essential requirements.

Management accounting is a process that helps in prepare financial report and it helps in

making decision for achieve organizational goal and meet objective. This account statement

prepare by managers for evaluate and analyze all data for making decision and improve work. It

main purpose is make plan and strategy and policy formation for set goals and take action

according to prepared statement. All data helpful in making decision by manages like cost,

profit, price and saving so they make any strategy for achieve goal after evaluation and analyze

of all data. So this is a tool of evaluate all costs and data than making decision and make plan

(Malmi, 2016).

financial accounting is a system that records all data and double entries book keeping of

financial year (Dutta and Patatoukas, 2016). It track all transaction that related to finance and

record, summarize and analysis of data and information.

1

Management Accounting system is refers to a system adopted by managers as to develop

the efficiency of the company in context with its financial performance. It is a process of

providing all the relevant financial information to the managers so that they could use them and

develop effective strategies for enhancing financial performance of the company and its cost

efficiency as well. Professional leads is a famous accounting firm of UK. It provides accounting

services to various companies. The present study shows a report of an intern as to provide a

brief information about the management accounting system to a client of the company. The

report includes a description of management accounting and management accounting system.

Further, it also shows various types of management accounting system and their requirements

within a business organisation. It shows numerous methods for the management accounting

reporting.

The report also shows preparation of income statement using different techniques of

management accounting. Furthermore, it also shows different planning tools of budgetary control

system and various systems of management accounting that can be adopted by managers as to

respond different financial problems.

LO 1

Management accounting and essential requirements.

Management accounting is a process that helps in prepare financial report and it helps in

making decision for achieve organizational goal and meet objective. This account statement

prepare by managers for evaluate and analyze all data for making decision and improve work. It

main purpose is make plan and strategy and policy formation for set goals and take action

according to prepared statement. All data helpful in making decision by manages like cost,

profit, price and saving so they make any strategy for achieve goal after evaluation and analyze

of all data. So this is a tool of evaluate all costs and data than making decision and make plan

(Malmi, 2016).

financial accounting is a system that records all data and double entries book keeping of

financial year (Dutta and Patatoukas, 2016). It track all transaction that related to finance and

record, summarize and analysis of data and information.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

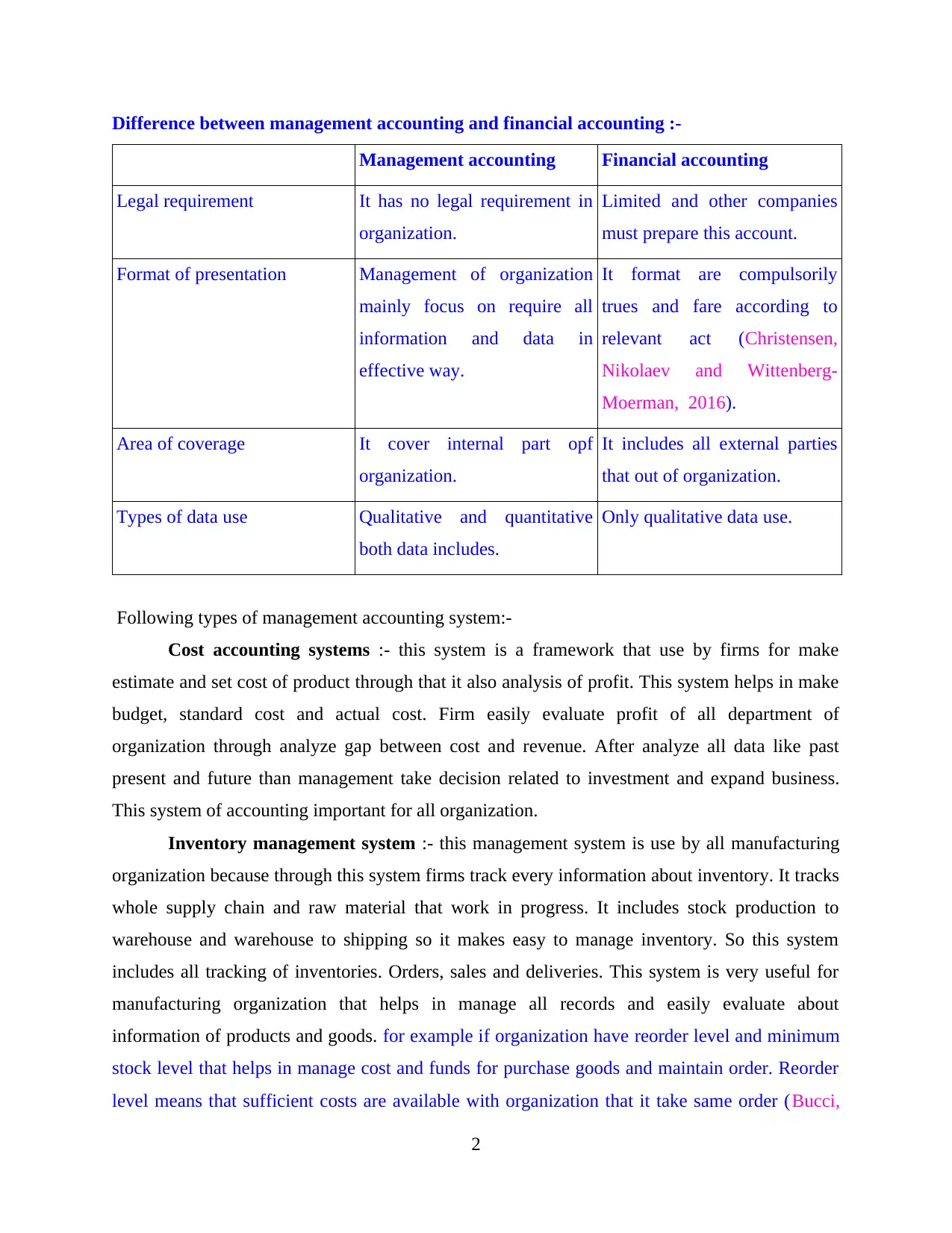

Difference between management accounting and financial accounting :-

Management accounting Financial accounting

Legal requirement It has no legal requirement in

organization.

Limited and other companies

must prepare this account.

Format of presentation Management of organization

mainly focus on require all

information and data in

effective way.

It format are compulsorily

trues and fare according to

relevant act (Christensen,

Nikolaev and Wittenberg‐

Moerman, 2016).

Area of coverage It cover internal part opf

organization.

It includes all external parties

that out of organization.

Types of data use Qualitative and quantitative

both data includes.

Only qualitative data use.

Following types of management accounting system:-

Cost accounting systems :- this system is a framework that use by firms for make

estimate and set cost of product through that it also analysis of profit. This system helps in make

budget, standard cost and actual cost. Firm easily evaluate profit of all department of

organization through analyze gap between cost and revenue. After analyze all data like past

present and future than management take decision related to investment and expand business.

This system of accounting important for all organization.

Inventory management system :- this management system is use by all manufacturing

organization because through this system firms track every information about inventory. It tracks

whole supply chain and raw material that work in progress. It includes stock production to

warehouse and warehouse to shipping so it makes easy to manage inventory. So this system

includes all tracking of inventories. Orders, sales and deliveries. This system is very useful for

manufacturing organization that helps in manage all records and easily evaluate about

information of products and goods. for example if organization have reorder level and minimum

stock level that helps in manage cost and funds for purchase goods and maintain order. Reorder

level means that sufficient costs are available with organization that it take same order (Bucci,

2

Management accounting Financial accounting

Legal requirement It has no legal requirement in

organization.

Limited and other companies

must prepare this account.

Format of presentation Management of organization

mainly focus on require all

information and data in

effective way.

It format are compulsorily

trues and fare according to

relevant act (Christensen,

Nikolaev and Wittenberg‐

Moerman, 2016).

Area of coverage It cover internal part opf

organization.

It includes all external parties

that out of organization.

Types of data use Qualitative and quantitative

both data includes.

Only qualitative data use.

Following types of management accounting system:-

Cost accounting systems :- this system is a framework that use by firms for make

estimate and set cost of product through that it also analysis of profit. This system helps in make

budget, standard cost and actual cost. Firm easily evaluate profit of all department of

organization through analyze gap between cost and revenue. After analyze all data like past

present and future than management take decision related to investment and expand business.

This system of accounting important for all organization.

Inventory management system :- this management system is use by all manufacturing

organization because through this system firms track every information about inventory. It tracks

whole supply chain and raw material that work in progress. It includes stock production to

warehouse and warehouse to shipping so it makes easy to manage inventory. So this system

includes all tracking of inventories. Orders, sales and deliveries. This system is very useful for

manufacturing organization that helps in manage all records and easily evaluate about

information of products and goods. for example if organization have reorder level and minimum

stock level that helps in manage cost and funds for purchase goods and maintain order. Reorder

level means that sufficient costs are available with organization that it take same order (Bucci,

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Hyde and Keen, 2019). Minimum stock level mange minimum amount compulsorily with it and

maximum stock level fix limit of cost for purchase stock.

Job costing system :- this system is very useful for organization that make products and

services according to order by customers. That means different types of customers give order for

different design and products so organizations has to produce according to demand and order

receive. In this process more cost incur so firms use job costing system that helps in calculate

easily all cost and revenue. Through this system they can easily calculate per item cost and

revenue. Firms evaluate that revenue is earned or not more than expenses that means profit earn

on per item or not so it helps in evaluate and making decision that order accept or not that

depend on profit and loss (Maas, Schaltegger and Crutzen, 2016).

Price optimizing system :- this system is use by all types of organization because

through these firms evaluate customers reaction regard price of products. Customer wants to

quality products on low price and if organization provide products at low price so customer

demand increase and if price is high for customers that effect on customers demand. So firm

easily evaluate and analyze customers reaction and they can set their price of products and also

take decision about price of products.

Benefits of management accounting system :- management accounting system helps in

organization for measure actual performance (Gunarathne and Lee, 2015). It also beneficial in

comparison of actual budget with required budget so management easily take decision according

to reports and also make plan for improve and develop of performance for achieve target.

LO 2

Different types of methods for management accounting reporting

Management accounting reports is tool that helps in understanding everything related to business

and activities of firms. It includes expenses, revenue, tax and collection of data. Following

methods are used for management accounting report:-

Financial report :- Financial reports shows the overall financial transactions of the

company. With the help of these reports, management can analyse overall financial performance

of the business. Further, it can also be seen as a summarised report of the overall business

operations. In this regard, with the help of these reports, the managers can analyse various

financial information and developing strategies for the company.

3

maximum stock level fix limit of cost for purchase stock.

Job costing system :- this system is very useful for organization that make products and

services according to order by customers. That means different types of customers give order for

different design and products so organizations has to produce according to demand and order

receive. In this process more cost incur so firms use job costing system that helps in calculate

easily all cost and revenue. Through this system they can easily calculate per item cost and

revenue. Firms evaluate that revenue is earned or not more than expenses that means profit earn

on per item or not so it helps in evaluate and making decision that order accept or not that

depend on profit and loss (Maas, Schaltegger and Crutzen, 2016).

Price optimizing system :- this system is use by all types of organization because

through these firms evaluate customers reaction regard price of products. Customer wants to

quality products on low price and if organization provide products at low price so customer

demand increase and if price is high for customers that effect on customers demand. So firm

easily evaluate and analyze customers reaction and they can set their price of products and also

take decision about price of products.

Benefits of management accounting system :- management accounting system helps in

organization for measure actual performance (Gunarathne and Lee, 2015). It also beneficial in

comparison of actual budget with required budget so management easily take decision according

to reports and also make plan for improve and develop of performance for achieve target.

LO 2

Different types of methods for management accounting reporting

Management accounting reports is tool that helps in understanding everything related to business

and activities of firms. It includes expenses, revenue, tax and collection of data. Following

methods are used for management accounting report:-

Financial report :- Financial reports shows the overall financial transactions of the

company. With the help of these reports, management can analyse overall financial performance

of the business. Further, it can also be seen as a summarised report of the overall business

operations. In this regard, with the help of these reports, the managers can analyse various

financial information and developing strategies for the company.

3

cash reports :- cash reports shows overall cash flow of the organisation. It includes all

the cash flow in organization (Nitzl, 2016). With the help of this report, managers can develop

better control over the business activities.

Sales report :- Sales report shows information about the sales activities of the company.

With the help of this report, overall sales activities of the business organisation. In this regard,

the managers can develop effective strategies through which the company could achieve its

business gaols.

Item cost report :- this report is very lengthy and consume more cost because this

includes all cost and expenses according to material, labor and other expenses on per product so

that helps in evaluate and calculate profit on per products. This report divides all cost according

to different expenditure and then analyze about earn profit.

Management accounting system is a process of control and effective manage through

evaluate of data and profit for making decision. It is very best way of evaluate all things and

make strategy very effectively for earn more profitability. It also helps in compare past present

and future year records. It affects to top management because they have to evaluate time to time

all records and evaluate performance in short term. Management accounting reporting is measure

actual performance of organization and compare require budget and available budget. It

consumes more cost and time because it evaluates and calculate profit on per product according

to labor and material and other expenses (Van der Stede, 2016).

Preparation of income statements using different management accounting techniques

Marginal costing:

marginal costing is a technique of costing in which all variable costs are being considered

as as the product cost (Jermias, Gani and Juliana, 2018). Whereas, all the fixed costs are being

considered as period cost. In this regard, fixed costs are nit being taken into account while

calculating cost of production.

Importance of marginal costing

Marginal costing method is helpful for business for taking its short term decisions.

Marginal costing helps in controlling cost of production because it eliminates overhead

cost.

Marginal costing helps in effective decision making and profit planning.

Absorption costing:

4

the cash flow in organization (Nitzl, 2016). With the help of this report, managers can develop

better control over the business activities.

Sales report :- Sales report shows information about the sales activities of the company.

With the help of this report, overall sales activities of the business organisation. In this regard,

the managers can develop effective strategies through which the company could achieve its

business gaols.

Item cost report :- this report is very lengthy and consume more cost because this

includes all cost and expenses according to material, labor and other expenses on per product so

that helps in evaluate and calculate profit on per products. This report divides all cost according

to different expenditure and then analyze about earn profit.

Management accounting system is a process of control and effective manage through

evaluate of data and profit for making decision. It is very best way of evaluate all things and

make strategy very effectively for earn more profitability. It also helps in compare past present

and future year records. It affects to top management because they have to evaluate time to time

all records and evaluate performance in short term. Management accounting reporting is measure

actual performance of organization and compare require budget and available budget. It

consumes more cost and time because it evaluates and calculate profit on per product according

to labor and material and other expenses (Van der Stede, 2016).

Preparation of income statements using different management accounting techniques

Marginal costing:

marginal costing is a technique of costing in which all variable costs are being considered

as as the product cost (Jermias, Gani and Juliana, 2018). Whereas, all the fixed costs are being

considered as period cost. In this regard, fixed costs are nit being taken into account while

calculating cost of production.

Importance of marginal costing

Marginal costing method is helpful for business for taking its short term decisions.

Marginal costing helps in controlling cost of production because it eliminates overhead

cost.

Marginal costing helps in effective decision making and profit planning.

Absorption costing:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

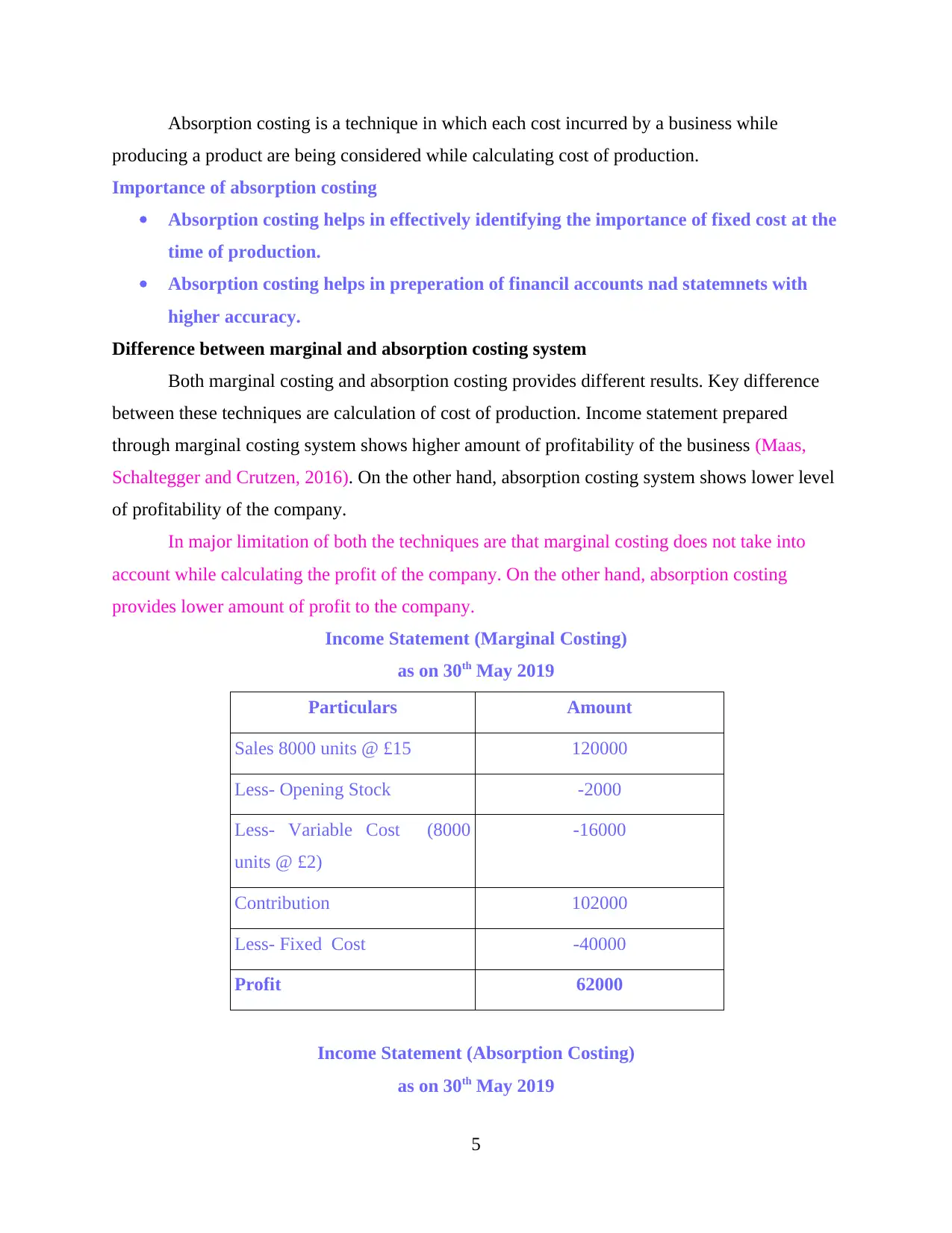

Absorption costing is a technique in which each cost incurred by a business while

producing a product are being considered while calculating cost of production.

Importance of absorption costing

Absorption costing helps in effectively identifying the importance of fixed cost at the

time of production.

Absorption costing helps in preperation of financil accounts nad statemnets with

higher accuracy.

Difference between marginal and absorption costing system

Both marginal costing and absorption costing provides different results. Key difference

between these techniques are calculation of cost of production. Income statement prepared

through marginal costing system shows higher amount of profitability of the business (Maas,

Schaltegger and Crutzen, 2016). On the other hand, absorption costing system shows lower level

of profitability of the company.

In major limitation of both the techniques are that marginal costing does not take into

account while calculating the profit of the company. On the other hand, absorption costing

provides lower amount of profit to the company.

Income Statement (Marginal Costing)

as on 30th May 2019

Particulars Amount

Sales 8000 units @ £15 120000

Less- Opening Stock -2000

Less- Variable Cost (8000

units @ £2)

-16000

Contribution 102000

Less- Fixed Cost -40000

Profit 62000

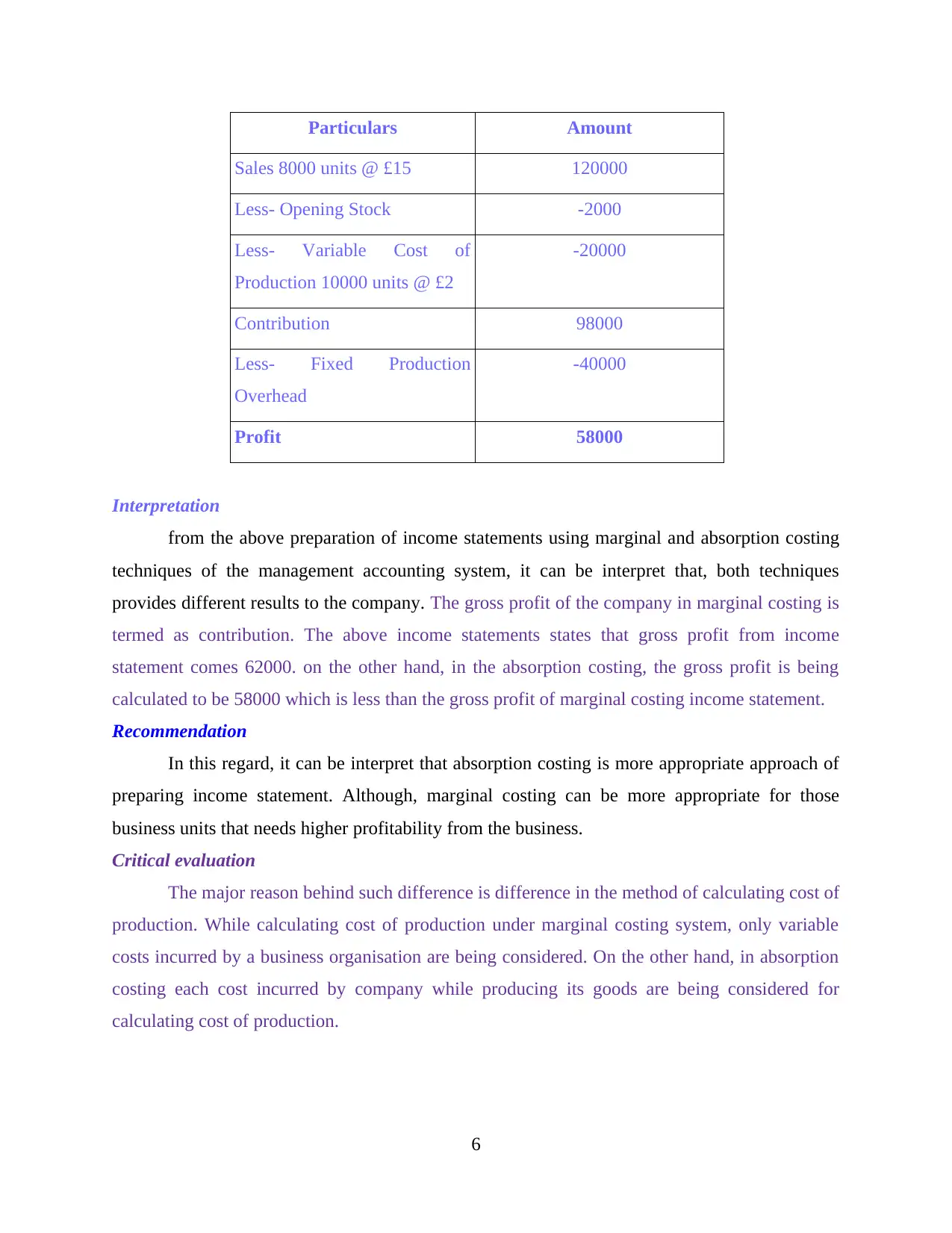

Income Statement (Absorption Costing)

as on 30th May 2019

5

producing a product are being considered while calculating cost of production.

Importance of absorption costing

Absorption costing helps in effectively identifying the importance of fixed cost at the

time of production.

Absorption costing helps in preperation of financil accounts nad statemnets with

higher accuracy.

Difference between marginal and absorption costing system

Both marginal costing and absorption costing provides different results. Key difference

between these techniques are calculation of cost of production. Income statement prepared

through marginal costing system shows higher amount of profitability of the business (Maas,

Schaltegger and Crutzen, 2016). On the other hand, absorption costing system shows lower level

of profitability of the company.

In major limitation of both the techniques are that marginal costing does not take into

account while calculating the profit of the company. On the other hand, absorption costing

provides lower amount of profit to the company.

Income Statement (Marginal Costing)

as on 30th May 2019

Particulars Amount

Sales 8000 units @ £15 120000

Less- Opening Stock -2000

Less- Variable Cost (8000

units @ £2)

-16000

Contribution 102000

Less- Fixed Cost -40000

Profit 62000

Income Statement (Absorption Costing)

as on 30th May 2019

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particulars Amount

Sales 8000 units @ £15 120000

Less- Opening Stock -2000

Less- Variable Cost of

Production 10000 units @ £2

-20000

Contribution 98000

Less- Fixed Production

Overhead

-40000

Profit 58000

Interpretation

from the above preparation of income statements using marginal and absorption costing

techniques of the management accounting system, it can be interpret that, both techniques

provides different results to the company. The gross profit of the company in marginal costing is

termed as contribution. The above income statements states that gross profit from income

statement comes 62000. on the other hand, in the absorption costing, the gross profit is being

calculated to be 58000 which is less than the gross profit of marginal costing income statement.

Recommendation

In this regard, it can be interpret that absorption costing is more appropriate approach of

preparing income statement. Although, marginal costing can be more appropriate for those

business units that needs higher profitability from the business.

Critical evaluation

The major reason behind such difference is difference in the method of calculating cost of

production. While calculating cost of production under marginal costing system, only variable

costs incurred by a business organisation are being considered. On the other hand, in absorption

costing each cost incurred by company while producing its goods are being considered for

calculating cost of production.

6

Sales 8000 units @ £15 120000

Less- Opening Stock -2000

Less- Variable Cost of

Production 10000 units @ £2

-20000

Contribution 98000

Less- Fixed Production

Overhead

-40000

Profit 58000

Interpretation

from the above preparation of income statements using marginal and absorption costing

techniques of the management accounting system, it can be interpret that, both techniques

provides different results to the company. The gross profit of the company in marginal costing is

termed as contribution. The above income statements states that gross profit from income

statement comes 62000. on the other hand, in the absorption costing, the gross profit is being

calculated to be 58000 which is less than the gross profit of marginal costing income statement.

Recommendation

In this regard, it can be interpret that absorption costing is more appropriate approach of

preparing income statement. Although, marginal costing can be more appropriate for those

business units that needs higher profitability from the business.

Critical evaluation

The major reason behind such difference is difference in the method of calculating cost of

production. While calculating cost of production under marginal costing system, only variable

costs incurred by a business organisation are being considered. On the other hand, in absorption

costing each cost incurred by company while producing its goods are being considered for

calculating cost of production.

6

LO.3

Explaining the advantages and disadvantages of different planning tools for budgetary control.

Budgetary control is an effective process of determining and evaluating the actual results

with the budget plan to effectively analyses the results. In case of any deviation it helps

management of the Excite entertainment ltd. to take corrective actions accordingly in order to

increase the performance and productivity of the Excite entertainment ltd.

Budget: It is the financial plan for a defined period, often one year. It might be include

planned sales, volumes and revenues, resource capabilities, costs and expenses, asserts,

liabilities and cash flows (Chenhall and Moers, 2015).

Different planning tools for Budgetary control

Cash budget

Cash budget is the budget plan which includes inflow and outflow of cash of an organization for

a particular period of time. Cash inflow and outflow comprises expenses paid, revenue collected,

loan payments and receipts (Appelbaum and et.al., 2017)). Cash budget helps in measuring the

cash position of the Excite entertainment ltd. Cash budget helps in forecasting cash inflows, cash

outflows and cash balance.

Advantages of cash budget

Cash budget helps in planning the resources effectively and efficiently (15 Cash Budget

Advantages and Disadvantages, 2018).

Cash budget helps in performance evaluation and leads to higher operational efficiency of

the organization. Cash budget helps in avoiding debt and focus on activity which will generate more

revenue and income for Excite entertainment ltd.

Disadvantages of cash budget

Cash budget is not flexible i.e., it is strategically rigid. Cash budget only includes financial transaction, it does not take into consideration non-

financial transaction. Hence, cash budget limits the ability to consider credit transaction

for accurate and reliable information (Yılmaz, 2018).

7

Explaining the advantages and disadvantages of different planning tools for budgetary control.

Budgetary control is an effective process of determining and evaluating the actual results

with the budget plan to effectively analyses the results. In case of any deviation it helps

management of the Excite entertainment ltd. to take corrective actions accordingly in order to

increase the performance and productivity of the Excite entertainment ltd.

Budget: It is the financial plan for a defined period, often one year. It might be include

planned sales, volumes and revenues, resource capabilities, costs and expenses, asserts,

liabilities and cash flows (Chenhall and Moers, 2015).

Different planning tools for Budgetary control

Cash budget

Cash budget is the budget plan which includes inflow and outflow of cash of an organization for

a particular period of time. Cash inflow and outflow comprises expenses paid, revenue collected,

loan payments and receipts (Appelbaum and et.al., 2017)). Cash budget helps in measuring the

cash position of the Excite entertainment ltd. Cash budget helps in forecasting cash inflows, cash

outflows and cash balance.

Advantages of cash budget

Cash budget helps in planning the resources effectively and efficiently (15 Cash Budget

Advantages and Disadvantages, 2018).

Cash budget helps in performance evaluation and leads to higher operational efficiency of

the organization. Cash budget helps in avoiding debt and focus on activity which will generate more

revenue and income for Excite entertainment ltd.

Disadvantages of cash budget

Cash budget is not flexible i.e., it is strategically rigid. Cash budget only includes financial transaction, it does not take into consideration non-

financial transaction. Hence, cash budget limits the ability to consider credit transaction

for accurate and reliable information (Yılmaz, 2018).

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Operating budget

Operating budget portrays expenses, income and expected cost for a particular financial year

(Yılmaz, 2018). Operating budget helps in evaluating income generating activities of the Excite

entertainment ltd and also helps in forecasting revenue and expenses for a particular period.

Advantages of Operating budget

Operating budget helps in projecting future expenses which helps in building financial

reserves fort the organization. Operating budget helps in managing current expenses of the organization and also helps

in determining financial position of the company.

Disadvantages of Operating budget

Preparation of operating budget is time consuming which leads to delay in decision

making. The allocation of the budgeted plan do not match the actual cost of running each

departmental unit of Excite entertainment ltd.

Fixed budget

A fixed budget is also referred to as static budget. Fixed budget is not flexible it remains constant

regardless of the activity in the organization. It remains constant throughout the budgeting period

(Stea and Andresen, 2017).

Advantages of Fixed budget

Fixed budget helps in prioritizing the expenses and set clear distinction between the

activities to meet the desired goals and objectives of the organization.

Fixed budget helps in tracking the budget and in case of any deviation necessary action is

taken effectively and efficiently. Fixed budget helps in controlling the cost of the business.

Disadvantages of Fixed budget

The major disadvantage of fixed budget is that it lacks flexibility.

8

Operating budget portrays expenses, income and expected cost for a particular financial year

(Yılmaz, 2018). Operating budget helps in evaluating income generating activities of the Excite

entertainment ltd and also helps in forecasting revenue and expenses for a particular period.

Advantages of Operating budget

Operating budget helps in projecting future expenses which helps in building financial

reserves fort the organization. Operating budget helps in managing current expenses of the organization and also helps

in determining financial position of the company.

Disadvantages of Operating budget

Preparation of operating budget is time consuming which leads to delay in decision

making. The allocation of the budgeted plan do not match the actual cost of running each

departmental unit of Excite entertainment ltd.

Fixed budget

A fixed budget is also referred to as static budget. Fixed budget is not flexible it remains constant

regardless of the activity in the organization. It remains constant throughout the budgeting period

(Stea and Andresen, 2017).

Advantages of Fixed budget

Fixed budget helps in prioritizing the expenses and set clear distinction between the

activities to meet the desired goals and objectives of the organization.

Fixed budget helps in tracking the budget and in case of any deviation necessary action is

taken effectively and efficiently. Fixed budget helps in controlling the cost of the business.

Disadvantages of Fixed budget

The major disadvantage of fixed budget is that it lacks flexibility.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Additional resources can't be allocated which impacts the revenues of the business

(Webb, 2016). The major drawback of fixed budget is that the budget is no change in the budgeted plan

of the business even if there is a change in the level of the business activity.

Budgetary control system

Zero based budgeting

Zero based budgeting is a type of budgetary control in which the budget is prepared from the

scratch. Zero based budgeting ensure cost effectiveness and the management of the Excite

entertainment ltd do not take into account previous year's budget plan.

Advantages of Zero based budgeting

Zero based budgeting helps management of the organization to effectively evaluate the

operations and programmes. Zero based budgeting focus on maximizing the profits of the organization and helps in

reducing error (Strengths and Weaknesses of Different Budget Systems, 2016).

Disadvantages of Zero based budgeting

Zero based budgeting do not focus on cost centres and are highly complex budgetary

control tool.

Zero based budgeting is a very time consuming process and resource intensive as the

budget is prepared from zero i.e. from the scratch. Implementation of Zero based budgeting is difficult as employees of the organization

might have problem adjusting the whole new budget plan.

Incremental budgeting

Incremental budgeting is a type of budgetary control which are prepared using budget of the last

financial year (Ho, 2018). This helps in adding incremental value to the new budget plan which

helps in improving the financial position and performance of the Excite entertainment ltd

effectively and efficiently.

Advantages of Incremental budgeting

9

(Webb, 2016). The major drawback of fixed budget is that the budget is no change in the budgeted plan

of the business even if there is a change in the level of the business activity.

Budgetary control system

Zero based budgeting

Zero based budgeting is a type of budgetary control in which the budget is prepared from the

scratch. Zero based budgeting ensure cost effectiveness and the management of the Excite

entertainment ltd do not take into account previous year's budget plan.

Advantages of Zero based budgeting

Zero based budgeting helps management of the organization to effectively evaluate the

operations and programmes. Zero based budgeting focus on maximizing the profits of the organization and helps in

reducing error (Strengths and Weaknesses of Different Budget Systems, 2016).

Disadvantages of Zero based budgeting

Zero based budgeting do not focus on cost centres and are highly complex budgetary

control tool.

Zero based budgeting is a very time consuming process and resource intensive as the

budget is prepared from zero i.e. from the scratch. Implementation of Zero based budgeting is difficult as employees of the organization

might have problem adjusting the whole new budget plan.

Incremental budgeting

Incremental budgeting is a type of budgetary control which are prepared using budget of the last

financial year (Ho, 2018). This helps in adding incremental value to the new budget plan which

helps in improving the financial position and performance of the Excite entertainment ltd

effectively and efficiently.

Advantages of Incremental budgeting

9

Incremental budgeting is simple and are based on the historical data for future predictions

which leads to improved budget plan. Incremental budgeting is easy to implement and understand which leads to higher

operational efficiency, performance and productivity.

Disadvantages of Incremental budgeting

Incremental budgeting do not take into account future and present situations which leads

to outdated budget plan and lower growth and sustainability of the budget plan (White

and Fancy, 2017). Incremental budgeting do not develop new ideas and techniques to reduce cost and

expenses of the organization (Miller, 2018).

Activity based budgeting

Activity based budgeting helps in critically analysing the cost of the business to carry out a

particular activity (Ho, 2018). Activity based budgeting helps in high degree of refinement

within the cost planning and also helps in analysing the activities which are crucial for the

development of Excite entertainment ltd. Activity based budgeting helps in analysing cost

attached with each activity.

Advantages of Activity based budgeting

Activity based budgeting helps in identifying critical success factors which helps in

sustainable growth and development of the Excite entertainment ltd.

Activity based budgeting helps management in critical evaluation and building in- depth

knowledge on the particular activities which leads to higher operational efficiency of the

business. Activity based budgeting helps in better and effective understanding of the overhead and

also helps in identifying non valuable activities in the organization.

Disadvantages of Activity based budgeting

Activity based budgeting is not useful for small businesses (de Campos and Rodrigues, 2016).

Activity based budgeting is costly to maintain and can be easily misinterpreted.

10

which leads to improved budget plan. Incremental budgeting is easy to implement and understand which leads to higher

operational efficiency, performance and productivity.

Disadvantages of Incremental budgeting

Incremental budgeting do not take into account future and present situations which leads

to outdated budget plan and lower growth and sustainability of the budget plan (White

and Fancy, 2017). Incremental budgeting do not develop new ideas and techniques to reduce cost and

expenses of the organization (Miller, 2018).

Activity based budgeting

Activity based budgeting helps in critically analysing the cost of the business to carry out a

particular activity (Ho, 2018). Activity based budgeting helps in high degree of refinement

within the cost planning and also helps in analysing the activities which are crucial for the

development of Excite entertainment ltd. Activity based budgeting helps in analysing cost

attached with each activity.

Advantages of Activity based budgeting

Activity based budgeting helps in identifying critical success factors which helps in

sustainable growth and development of the Excite entertainment ltd.

Activity based budgeting helps management in critical evaluation and building in- depth

knowledge on the particular activities which leads to higher operational efficiency of the

business. Activity based budgeting helps in better and effective understanding of the overhead and

also helps in identifying non valuable activities in the organization.

Disadvantages of Activity based budgeting

Activity based budgeting is not useful for small businesses (de Campos and Rodrigues, 2016).

Activity based budgeting is costly to maintain and can be easily misinterpreted.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.