Financial Performance Analysis: Tata International Limited (2015-2017)

VerifiedAdded on 2023/01/17

|19

|3958

|96

Report

AI Summary

This report presents a financial analysis of Tata International Limited, evaluating its performance from 2015 to 2017. The analysis focuses on key financial ratios, including liquidity ratios (current and quick ratios), efficiency ratios (accounts receivable and payable turnover), and leverage ratios (debt-to-equity ratio). The study examines the company's financial statements to assess its ability to meet short-term and long-term obligations, manage its assets and liabilities efficiently, and maintain a healthy capital structure. The report highlights the trends in these ratios over the three-year period, identifies areas of strength and weakness, and offers recommendations for improving the company's financial position. The findings provide insights into Tata International Limited's financial health and offer a basis for informed decision-making.

Running head: ADVANCED FINANCIAL ACCOUNTING

Advanced Financial Accounting

Name of the student:

Name of the university:

Author Note:

Advanced Financial Accounting

Name of the student:

Name of the university:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................3

Answer to Question 1.............................................................................................................3

Answer to Question 2...........................................................................................................13

Conclusion................................................................................................................................14

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................3

Answer to Question 1.............................................................................................................3

Answer to Question 2...........................................................................................................13

Conclusion................................................................................................................................14

2ADVANCED FINANCIAL ACCOUNTING

Introduction:

The aim of the assignment deals with the financial analysis of the Tata international

limited for the financial years 2015, 2016 and 2017 by evaluating the annual report. In depth

financial analysis of the company has been performed and accordingly the changes which the

company needs to adopt has also been discussed in the conducted analysis. The whole

research is based on the tools and techniques which are the key financial ratios of the

company.

The detailed significance of each ratio has been discussed in the conducted analysis

and further strong recommendation to improve the financial position of the business or the

ratios have been depicted in the analysis. As a financial analyst of the company the main

responsibility is to identify the associated in the management system of the company and

further suggestion by evaluating the tool and techniques of the company have been duly

presented in the case study.

Introduction:

The aim of the assignment deals with the financial analysis of the Tata international

limited for the financial years 2015, 2016 and 2017 by evaluating the annual report. In depth

financial analysis of the company has been performed and accordingly the changes which the

company needs to adopt has also been discussed in the conducted analysis. The whole

research is based on the tools and techniques which are the key financial ratios of the

company.

The detailed significance of each ratio has been discussed in the conducted analysis

and further strong recommendation to improve the financial position of the business or the

ratios have been depicted in the analysis. As a financial analyst of the company the main

responsibility is to identify the associated in the management system of the company and

further suggestion by evaluating the tool and techniques of the company have been duly

presented in the case study.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ADVANCED FINANCIAL ACCOUNTING

Discussion:

The research is based on the chosen company here which is the Tata International

Limited which is a global distribution and the trading company. The business of the Tata

International Limited is spread over 39 countries. The sustainable growth of the company all

over the world created a value addition of the company. Effective sourcing and the marketing

strategies of the company is taking the key business of the company in the next level (Grant

2016).

The main area of the business of the company is based on the trading business of

Metals where the key products offered by the business is the steel, metallic and roll as well as

the various aluminum products. Apart from this products, there are the other products of the

company which are the mineral trading, agricultural trading and many more.

As per the corporate sustainability, the company takes certain measures regarding

maintaining the responsibility towards community and the environment. The company

constantly concentrates to achieve the overall objectives of the business in that case. The

management system of the company is effective which is further reflected in the financial

statement of the company.

Answer to Question 1

In this particular case study, the performance measurement of the Tata international

limited has been performed accordingly with the help of the fundamental ratios associated

with the values of the company. The key elements in the conducted study has been depicted

in the research by analyzing the business of the company for the last three years from the

annual reports. Ratio analysis is a significant tool adopted by the company as a measurement

Discussion:

The research is based on the chosen company here which is the Tata International

Limited which is a global distribution and the trading company. The business of the Tata

International Limited is spread over 39 countries. The sustainable growth of the company all

over the world created a value addition of the company. Effective sourcing and the marketing

strategies of the company is taking the key business of the company in the next level (Grant

2016).

The main area of the business of the company is based on the trading business of

Metals where the key products offered by the business is the steel, metallic and roll as well as

the various aluminum products. Apart from this products, there are the other products of the

company which are the mineral trading, agricultural trading and many more.

As per the corporate sustainability, the company takes certain measures regarding

maintaining the responsibility towards community and the environment. The company

constantly concentrates to achieve the overall objectives of the business in that case. The

management system of the company is effective which is further reflected in the financial

statement of the company.

Answer to Question 1

In this particular case study, the performance measurement of the Tata international

limited has been performed accordingly with the help of the fundamental ratios associated

with the values of the company. The key elements in the conducted study has been depicted

in the research by analyzing the business of the company for the last three years from the

annual reports. Ratio analysis is a significant tool adopted by the company as a measurement

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ADVANCED FINANCIAL ACCOUNTING

of the financial statement analysis of the company. The key ratios of the company must be

analyzed in order to understand the performance of the business.

The key ratios which is focused in the conducted study is the liquidity, efficiency,

profitability and leverage ratios of the business in that case. The ratios of the company have

been computed from the financial statement of the three years which are the 2015, 2016 and

2017. The value or figures has been taken from the consolidated financial statement of the

company’s annual report.

(A)

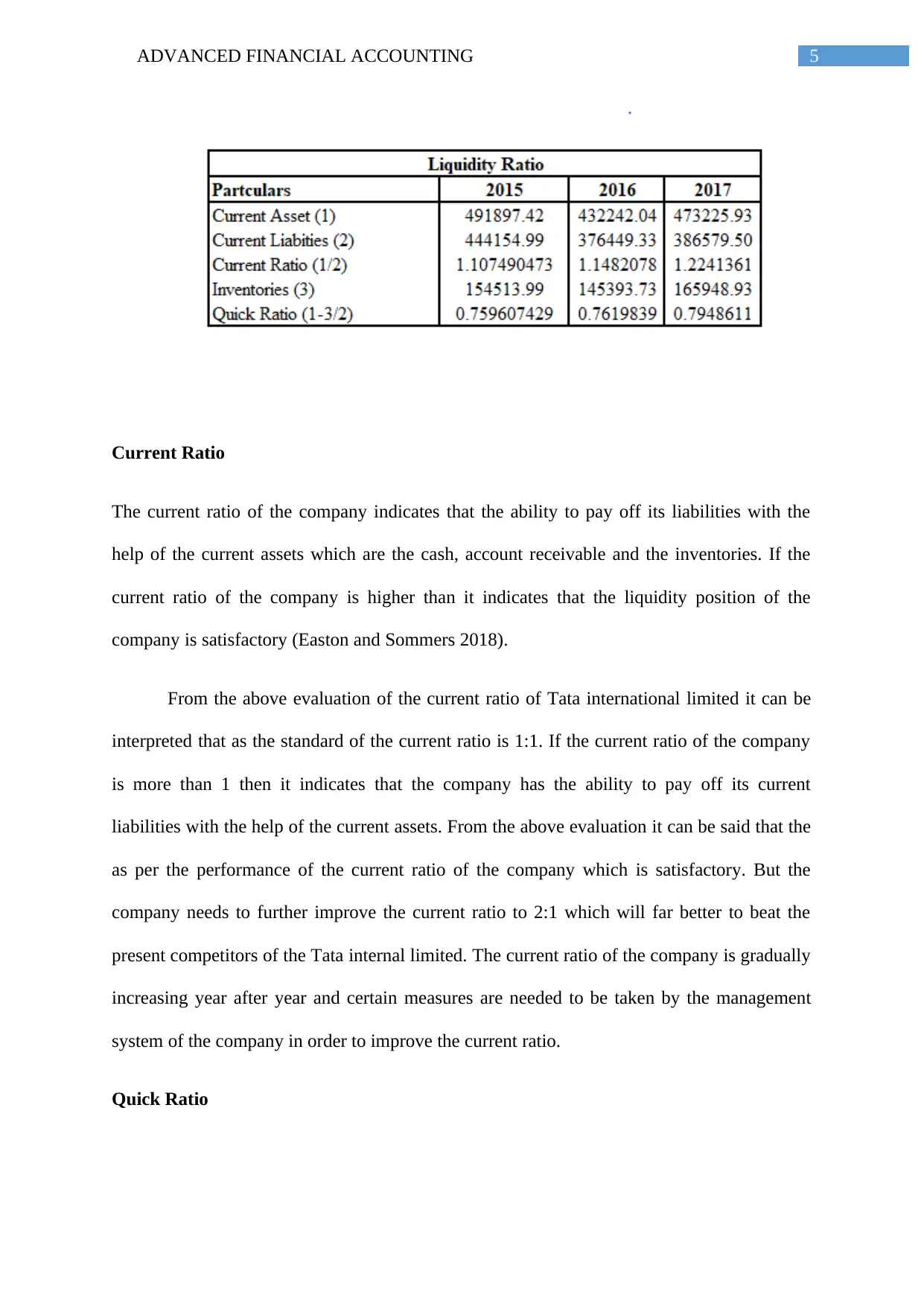

Liquidity Ratio

Liquidity ratio is one of the important financial ratios which indicate that whether the

current assets of the company are sufficient to meet the short term and the long term

obligations of the company when it becomes due. Under the liqu9idity ratio there are two

ratios which are the current ratio and the quick ratios.

From the liquidity ratio of the company, the performance of the working capital of the

company can be analyzed which is further known as the indicator of liquidity. The term

liquidity refers to the ability of a company to covert assets into cash quickly and cheaply. A

higher liquidity ratio indicates that company is more liquid and has better exposure of the

outstanding debts.

of the financial statement analysis of the company. The key ratios of the company must be

analyzed in order to understand the performance of the business.

The key ratios which is focused in the conducted study is the liquidity, efficiency,

profitability and leverage ratios of the business in that case. The ratios of the company have

been computed from the financial statement of the three years which are the 2015, 2016 and

2017. The value or figures has been taken from the consolidated financial statement of the

company’s annual report.

(A)

Liquidity Ratio

Liquidity ratio is one of the important financial ratios which indicate that whether the

current assets of the company are sufficient to meet the short term and the long term

obligations of the company when it becomes due. Under the liqu9idity ratio there are two

ratios which are the current ratio and the quick ratios.

From the liquidity ratio of the company, the performance of the working capital of the

company can be analyzed which is further known as the indicator of liquidity. The term

liquidity refers to the ability of a company to covert assets into cash quickly and cheaply. A

higher liquidity ratio indicates that company is more liquid and has better exposure of the

outstanding debts.

5ADVANCED FINANCIAL ACCOUNTING

Current Ratio

The current ratio of the company indicates that the ability to pay off its liabilities with the

help of the current assets which are the cash, account receivable and the inventories. If the

current ratio of the company is higher than it indicates that the liquidity position of the

company is satisfactory (Easton and Sommers 2018).

From the above evaluation of the current ratio of Tata international limited it can be

interpreted that as the standard of the current ratio is 1:1. If the current ratio of the company

is more than 1 then it indicates that the company has the ability to pay off its current

liabilities with the help of the current assets. From the above evaluation it can be said that the

as per the performance of the current ratio of the company which is satisfactory. But the

company needs to further improve the current ratio to 2:1 which will far better to beat the

present competitors of the Tata internal limited. The current ratio of the company is gradually

increasing year after year and certain measures are needed to be taken by the management

system of the company in order to improve the current ratio.

Quick Ratio

Current Ratio

The current ratio of the company indicates that the ability to pay off its liabilities with the

help of the current assets which are the cash, account receivable and the inventories. If the

current ratio of the company is higher than it indicates that the liquidity position of the

company is satisfactory (Easton and Sommers 2018).

From the above evaluation of the current ratio of Tata international limited it can be

interpreted that as the standard of the current ratio is 1:1. If the current ratio of the company

is more than 1 then it indicates that the company has the ability to pay off its current

liabilities with the help of the current assets. From the above evaluation it can be said that the

as per the performance of the current ratio of the company which is satisfactory. But the

company needs to further improve the current ratio to 2:1 which will far better to beat the

present competitors of the Tata internal limited. The current ratio of the company is gradually

increasing year after year and certain measures are needed to be taken by the management

system of the company in order to improve the current ratio.

Quick Ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ADVANCED FINANCIAL ACCOUNTING

The quick ratio of the company measures the ability of the company to meet the short

term obligation with the help of its liquid assets by excluding the inventories from its current

assets. Quick ratio is also known as the acid test ratio (Zietlow et al. 2018).

From the above evaluation of the quick ratio of Tata international limited it can be

interpreted that as the standard quick ratio of the company is 1:1 which means that the

liquidity position of the company is satisfactory. If the ratio of te company is higher than the

normal standard then it signifies that the overall liquidity position of the company is

satisfactory. On the other hand if the quick ratio of the company is less than 1, then it

indicates that the company is unable to pay off its current liabilities.

In this case, the quick ratio of the company is less than 1 which indicates that

the company is unable to meet its short term and long term obligation. Further the company

needs to adopt some of the stringent policies to increase the ratio so that company may be

able to settle its current obligations in the future.

(B)

Efficiency Ratio

The efficiency ratio of the company indicates the expenses expressed as a

percentage of revenue. This ratio helps to analyze the efficiency of the company to use its

assets and liabilities internally. An efficiency ratio of the company is evaluated to find out the

turnover of the receivables, repayment of the liabilities, and usage of equity and further the

general use of the machinery and inventory (Dyckman and Zeff 2015).

This ratio is used to track the performance of the company in terms of the revenues

and expenses. A lower efficiency ratio of the company indicates that the company is

The quick ratio of the company measures the ability of the company to meet the short

term obligation with the help of its liquid assets by excluding the inventories from its current

assets. Quick ratio is also known as the acid test ratio (Zietlow et al. 2018).

From the above evaluation of the quick ratio of Tata international limited it can be

interpreted that as the standard quick ratio of the company is 1:1 which means that the

liquidity position of the company is satisfactory. If the ratio of te company is higher than the

normal standard then it signifies that the overall liquidity position of the company is

satisfactory. On the other hand if the quick ratio of the company is less than 1, then it

indicates that the company is unable to pay off its current liabilities.

In this case, the quick ratio of the company is less than 1 which indicates that

the company is unable to meet its short term and long term obligation. Further the company

needs to adopt some of the stringent policies to increase the ratio so that company may be

able to settle its current obligations in the future.

(B)

Efficiency Ratio

The efficiency ratio of the company indicates the expenses expressed as a

percentage of revenue. This ratio helps to analyze the efficiency of the company to use its

assets and liabilities internally. An efficiency ratio of the company is evaluated to find out the

turnover of the receivables, repayment of the liabilities, and usage of equity and further the

general use of the machinery and inventory (Dyckman and Zeff 2015).

This ratio is used to track the performance of the company in terms of the revenues

and expenses. A lower efficiency ratio of the company indicates that the company is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ADVANCED FINANCIAL ACCOUNTING

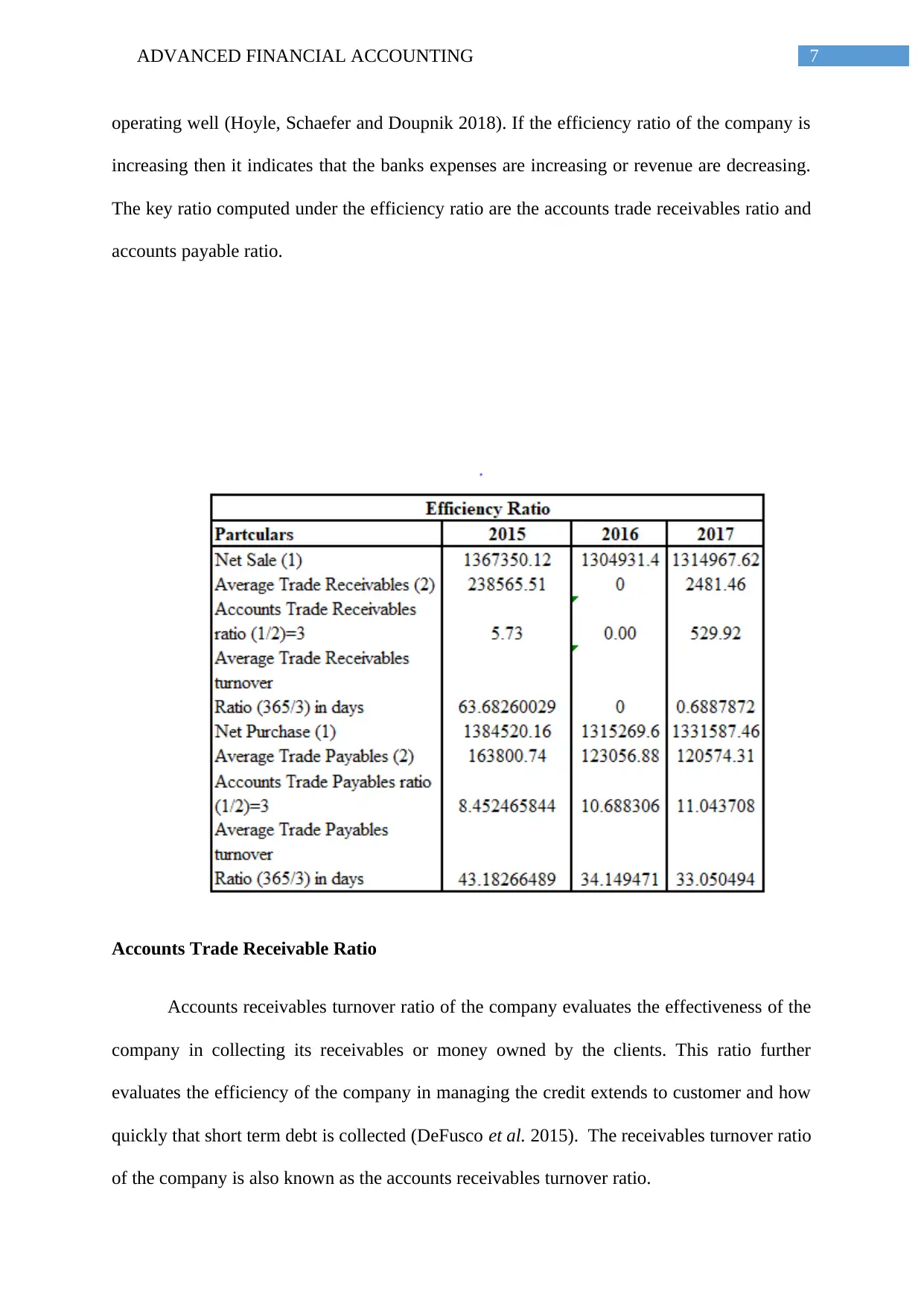

operating well (Hoyle, Schaefer and Doupnik 2018). If the efficiency ratio of the company is

increasing then it indicates that the banks expenses are increasing or revenue are decreasing.

The key ratio computed under the efficiency ratio are the accounts trade receivables ratio and

accounts payable ratio.

Accounts Trade Receivable Ratio

Accounts receivables turnover ratio of the company evaluates the effectiveness of the

company in collecting its receivables or money owned by the clients. This ratio further

evaluates the efficiency of the company in managing the credit extends to customer and how

quickly that short term debt is collected (DeFusco et al. 2015). The receivables turnover ratio

of the company is also known as the accounts receivables turnover ratio.

operating well (Hoyle, Schaefer and Doupnik 2018). If the efficiency ratio of the company is

increasing then it indicates that the banks expenses are increasing or revenue are decreasing.

The key ratio computed under the efficiency ratio are the accounts trade receivables ratio and

accounts payable ratio.

Accounts Trade Receivable Ratio

Accounts receivables turnover ratio of the company evaluates the effectiveness of the

company in collecting its receivables or money owned by the clients. This ratio further

evaluates the efficiency of the company in managing the credit extends to customer and how

quickly that short term debt is collected (DeFusco et al. 2015). The receivables turnover ratio

of the company is also known as the accounts receivables turnover ratio.

8ADVANCED FINANCIAL ACCOUNTING

If a particular company is able to generate a sale to a client, it could further

extend terms of the 30 or 60days which further means that the client has 30 to 60 days to pay

off its product. A higher ratio of the company suggests that a company is conservative when

it comes to extend the credit of the customers. Further a conservative credit policy is

beneficial as it would help the company to avoid extending credit to customers who may not

be able to pay on time (Dosi et al. 2016).

A low receivable turnover ratio of the company indicates that due to company

having poor collection process, bad credit policies, which means that a particular customer is

not financially sound to pay off its credit. Receivables turnover of the company must be

monitored and tracked and further it is needed to correlate the collection of the receivables to

earnings which measures the company’s credit practices have on profitability (Demerjian and

Owens 2016).

As per the above evaluation of accounts receivable ratio of Tata international limited,

it can be interpreted that during the year 2015 the company ratio was better as it was higher

but after that it is decreased. This indicates that during the financial year 2016 and 2017, the

company needs to improve the collection process and for that the company have to adopt

some the strict policies.

Accounts Trade Payables Ratio

The accounts payables ratio of the company measures the rate at which the company

pay off its suppliers. This ratio shows the number of times the company pays off its accounts

payable during a particular period (Carter and Warren 2018). Accounts payable is basically a

short term obligation that the company owes to its supplier or creditors.

If a particular company is able to generate a sale to a client, it could further

extend terms of the 30 or 60days which further means that the client has 30 to 60 days to pay

off its product. A higher ratio of the company suggests that a company is conservative when

it comes to extend the credit of the customers. Further a conservative credit policy is

beneficial as it would help the company to avoid extending credit to customers who may not

be able to pay on time (Dosi et al. 2016).

A low receivable turnover ratio of the company indicates that due to company

having poor collection process, bad credit policies, which means that a particular customer is

not financially sound to pay off its credit. Receivables turnover of the company must be

monitored and tracked and further it is needed to correlate the collection of the receivables to

earnings which measures the company’s credit practices have on profitability (Demerjian and

Owens 2016).

As per the above evaluation of accounts receivable ratio of Tata international limited,

it can be interpreted that during the year 2015 the company ratio was better as it was higher

but after that it is decreased. This indicates that during the financial year 2016 and 2017, the

company needs to improve the collection process and for that the company have to adopt

some the strict policies.

Accounts Trade Payables Ratio

The accounts payables ratio of the company measures the rate at which the company

pay off its suppliers. This ratio shows the number of times the company pays off its accounts

payable during a particular period (Carter and Warren 2018). Accounts payable is basically a

short term obligation that the company owes to its supplier or creditors.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ADVANCED FINANCIAL ACCOUNTING

This ratio further shows the investors of the company that number of times per period

a company pays its accounts payable. On the other hand this ratio measures the speed at

which the company pays off its suppliers. The investors of the company uses the accounts

payable ratio in order to determine that company has enough cash or revenue to meet its short

term obligations.

Decreasing turnover ratio of the company indicates that the company is taking longer

to pays off its obligation to the suppliers than the previous periods. This further indicates that

the company is in financial distress. On the other hand, an increasing accounts payable

turnover ratio of the company indicates that the upper level management of the company is

effective in managing its debt and cash flow (Shawver and Miller 2017).

As per the computation of the accounts trade payables ratio, it can be evaluated that

ratio of the company is gradually decreasing from the financial year 2015. In the year 2015

the ratio of the company was satisfactory but after that the ratio of the company is gradually

decreasing. Hence in this case the company needs to take certain measures in order to

improve the ratio (West and Bhattacharya 2016).

(C)

Leverage Ratio

The leverage ratio of the company is one of the several financial measurement which

evaluates the ability of a company to meet its financial obligations. Evaluating the leverage

ratio of the company is significant as the companies relies on the mixture of the debt and

equity to finance its operation and further it measures that the amount of debt calculated to

know that whether the company can pay its debt off as they come due (Hoyle, Schaefer and

Doupnik 2015).

This ratio further shows the investors of the company that number of times per period

a company pays its accounts payable. On the other hand this ratio measures the speed at

which the company pays off its suppliers. The investors of the company uses the accounts

payable ratio in order to determine that company has enough cash or revenue to meet its short

term obligations.

Decreasing turnover ratio of the company indicates that the company is taking longer

to pays off its obligation to the suppliers than the previous periods. This further indicates that

the company is in financial distress. On the other hand, an increasing accounts payable

turnover ratio of the company indicates that the upper level management of the company is

effective in managing its debt and cash flow (Shawver and Miller 2017).

As per the computation of the accounts trade payables ratio, it can be evaluated that

ratio of the company is gradually decreasing from the financial year 2015. In the year 2015

the ratio of the company was satisfactory but after that the ratio of the company is gradually

decreasing. Hence in this case the company needs to take certain measures in order to

improve the ratio (West and Bhattacharya 2016).

(C)

Leverage Ratio

The leverage ratio of the company is one of the several financial measurement which

evaluates the ability of a company to meet its financial obligations. Evaluating the leverage

ratio of the company is significant as the companies relies on the mixture of the debt and

equity to finance its operation and further it measures that the amount of debt calculated to

know that whether the company can pay its debt off as they come due (Hoyle, Schaefer and

Doupnik 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ADVANCED FINANCIAL ACCOUNTING

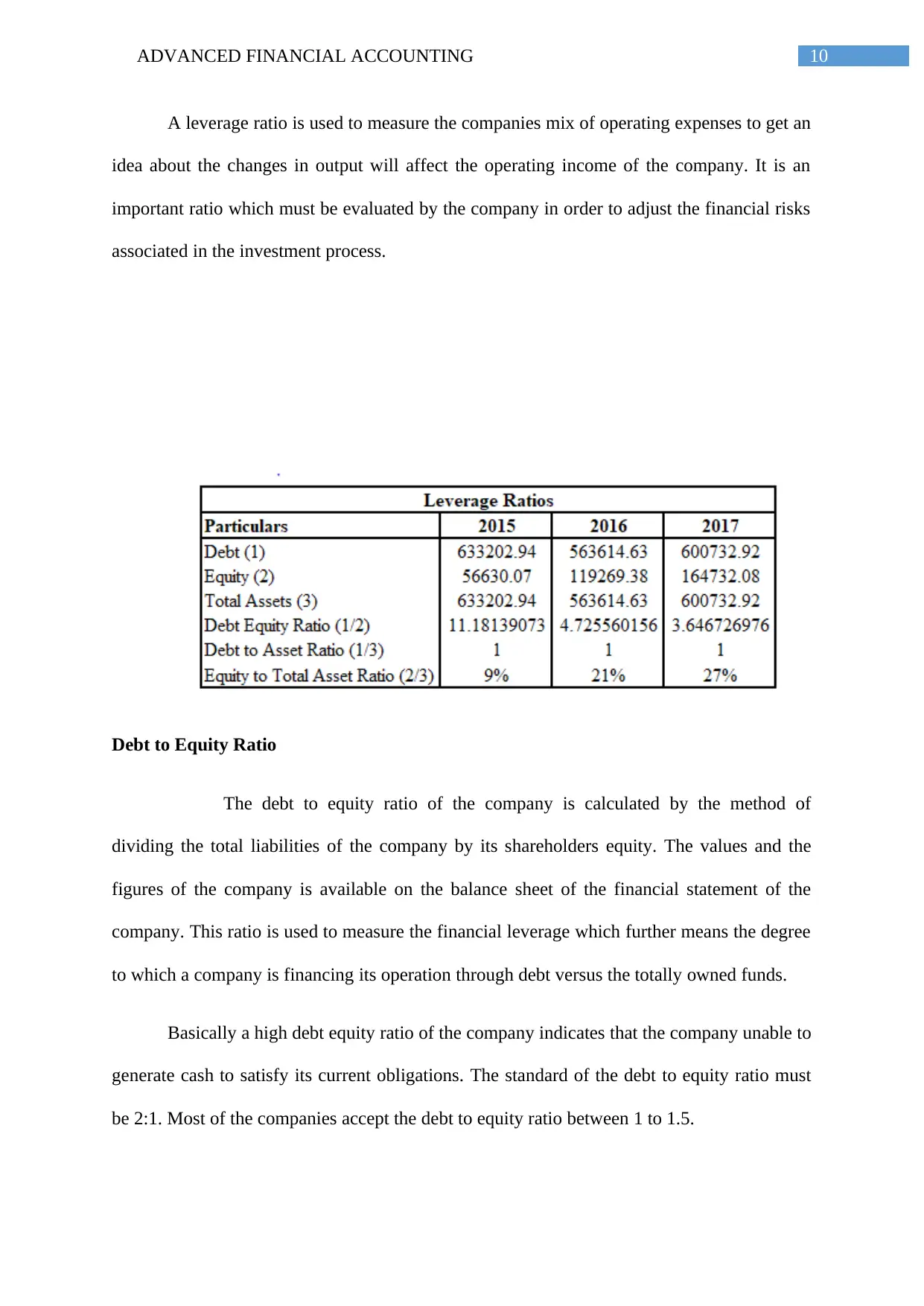

A leverage ratio is used to measure the companies mix of operating expenses to get an

idea about the changes in output will affect the operating income of the company. It is an

important ratio which must be evaluated by the company in order to adjust the financial risks

associated in the investment process.

Debt to Equity Ratio

The debt to equity ratio of the company is calculated by the method of

dividing the total liabilities of the company by its shareholders equity. The values and the

figures of the company is available on the balance sheet of the financial statement of the

company. This ratio is used to measure the financial leverage which further means the degree

to which a company is financing its operation through debt versus the totally owned funds.

Basically a high debt equity ratio of the company indicates that the company unable to

generate cash to satisfy its current obligations. The standard of the debt to equity ratio must

be 2:1. Most of the companies accept the debt to equity ratio between 1 to 1.5.

A leverage ratio is used to measure the companies mix of operating expenses to get an

idea about the changes in output will affect the operating income of the company. It is an

important ratio which must be evaluated by the company in order to adjust the financial risks

associated in the investment process.

Debt to Equity Ratio

The debt to equity ratio of the company is calculated by the method of

dividing the total liabilities of the company by its shareholders equity. The values and the

figures of the company is available on the balance sheet of the financial statement of the

company. This ratio is used to measure the financial leverage which further means the degree

to which a company is financing its operation through debt versus the totally owned funds.

Basically a high debt equity ratio of the company indicates that the company unable to

generate cash to satisfy its current obligations. The standard of the debt to equity ratio must

be 2:1. Most of the companies accept the debt to equity ratio between 1 to 1.5.

11ADVANCED FINANCIAL ACCOUNTING

Here in the evaluation of the ratio of Tata international limited, it can be interpreted

that debt to equity ratio of the company is not satisfactory and hence it is the responsibility of

the company to reduce such ratio. This is only possible if the company is able to generate

more return and pay off its debt on the right time. The company needs to improve the debt to

equity ratio by some of the significant measures in that case (Semanyuk 2017).

Debt to Asset Ratio

The debt to asset ratio of the company is a leverage ratio which measures the amount

of total asset which are financed by the creditors instead of the investors. If te debt to asset

ratio of the company is higher than 1, then it indicates that the company have more liabilities

than assets (Kim et al. 2016). If the debt to asset ratio of the company is less than 1 then it

indicates that the company can settle its liabilities by paying off its assets.

From the above evaluation of the debt to equity ratio, it can be interpreted that the

debt to asset ratio of Tata international limited in all the financial year 2015, 2016 and 2017 is

same and which further indicates that the company has same amount of the liabilities

compared to that of the assets. In order to enhance the ratio, the company needs to adopt

some of the strategies like paying of it debt by selling the selling will further lower the ratio

in that case (Robinson et al. 2015).

Equity to Total Assets Ratio

This ratio is further known as the shareholders equity ratio which indicates that the

company’s asset is funded by the equity shares. If the ratio of the company is lower than it

indicates that the company has used more debts to pay off its assets (Jacobson and Von

Here in the evaluation of the ratio of Tata international limited, it can be interpreted

that debt to equity ratio of the company is not satisfactory and hence it is the responsibility of

the company to reduce such ratio. This is only possible if the company is able to generate

more return and pay off its debt on the right time. The company needs to improve the debt to

equity ratio by some of the significant measures in that case (Semanyuk 2017).

Debt to Asset Ratio

The debt to asset ratio of the company is a leverage ratio which measures the amount

of total asset which are financed by the creditors instead of the investors. If te debt to asset

ratio of the company is higher than 1, then it indicates that the company have more liabilities

than assets (Kim et al. 2016). If the debt to asset ratio of the company is less than 1 then it

indicates that the company can settle its liabilities by paying off its assets.

From the above evaluation of the debt to equity ratio, it can be interpreted that the

debt to asset ratio of Tata international limited in all the financial year 2015, 2016 and 2017 is

same and which further indicates that the company has same amount of the liabilities

compared to that of the assets. In order to enhance the ratio, the company needs to adopt

some of the strategies like paying of it debt by selling the selling will further lower the ratio

in that case (Robinson et al. 2015).

Equity to Total Assets Ratio

This ratio is further known as the shareholders equity ratio which indicates that the

company’s asset is funded by the equity shares. If the ratio of the company is lower than it

indicates that the company has used more debts to pay off its assets (Jacobson and Von

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.