Management Accounting Tools and Methods for Toyota Automotive Business

VerifiedAdded on 2020/10/04

|14

|3827

|413

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices within Toyota, focusing on tools and methods to improve financial performance. The report begins with an introduction to management accounting, its essential requirements, and the different systems used by Toyota, including job costing and process costing. It then explores various management accounting reporting methodologies, such as budget reporting, job cost reports, and inventory management. The core of the report compares marginal and absorption costing methodologies, providing detailed calculations and analysis of their impact on Toyota's financial statements. Finally, the report examines the advantages and disadvantages of different planning tools used for budgeting control, such as cash budgeting. The report concludes with a discussion on how Toyota adopts management accounting systems to address financial issues and achieve its goals.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P.1. Explain the management accounting and essential requirement of different kind of

management accounting system in Toyota firm.........................................................................1

P.2. Different methodologies used for management accounting reporting.................................3

TASK 2............................................................................................................................................4

P.3. Marginal and absorption costing methodology....................................................................4

TASK 3............................................................................................................................................6

P.4. Advantage and disadvantage of using different planning tools that could be utilised for

budgeting control at workplace...................................................................................................6

P.5. Adoption of management accounting system to respond to financial management............8

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P.1. Explain the management accounting and essential requirement of different kind of

management accounting system in Toyota firm.........................................................................1

P.2. Different methodologies used for management accounting reporting.................................3

TASK 2............................................................................................................................................4

P.3. Marginal and absorption costing methodology....................................................................4

TASK 3............................................................................................................................................6

P.4. Advantage and disadvantage of using different planning tools that could be utilised for

budgeting control at workplace...................................................................................................6

P.5. Adoption of management accounting system to respond to financial management............8

REFERENCES..............................................................................................................................10

INTRODUCTION

In this research, we would critically discuss about to management accounting tools and

methods for Toyota automotive business to improve their financial performances and

requirements of different kinds of management accounting system which can be utilised within

Toyota automotive business and explain about to different methods used for management

accounting reporting in the firm as well. We would discuss in this investigation about to using

appropriate techniques of cost analysis to prepare income statement using marginal and

absorption method by using both costing techniques. Furthermore, we would explain the

advantages and disadvantage of different kinds of planning tools used for budgetary control for

Toyota automotive business. Ultimately, we will compare how Toyota firm are adopting

management accounting systems to effectively solve all financial issues within Toyota

automotive corporation.

TASK 1

P.1. Explain the management accounting and essential requirement of different kind of

management accounting system in Toyota firm

To

The general manager of the Toyota automotive, japan, Date 2-2-2018

Sub: Management accounting process and their significant

Management accounting is a methodology in which financial data and information are

measuring, analysing, interpreting and communicate them towards the Toyota business goals

and objectives effectively. This is also concern about to utlise this process as cost accounting in

the firm. The main difference between management accounting and financial accounting is that

data analysis of management accounting assist the company's manager in order to decision

making in right way, whereas financial accounting is the process which furnish external parties

offering information effectively(Wu and Boateng, 2010). The methodology of management

accounting and report provides the information about day to day financial report and static

analyst of financial data are required to manager to make their decision towards company's

short terms and long term goal and also helps in their day to day operation within the business.

There are several types of tools and techniques which are used in the Toyota business in terms

of accomplish their managerial goals and company's financial objectives as well. There are

various type of management accounting which are inventory management, price optimisation,

1

In this research, we would critically discuss about to management accounting tools and

methods for Toyota automotive business to improve their financial performances and

requirements of different kinds of management accounting system which can be utilised within

Toyota automotive business and explain about to different methods used for management

accounting reporting in the firm as well. We would discuss in this investigation about to using

appropriate techniques of cost analysis to prepare income statement using marginal and

absorption method by using both costing techniques. Furthermore, we would explain the

advantages and disadvantage of different kinds of planning tools used for budgetary control for

Toyota automotive business. Ultimately, we will compare how Toyota firm are adopting

management accounting systems to effectively solve all financial issues within Toyota

automotive corporation.

TASK 1

P.1. Explain the management accounting and essential requirement of different kind of

management accounting system in Toyota firm

To

The general manager of the Toyota automotive, japan, Date 2-2-2018

Sub: Management accounting process and their significant

Management accounting is a methodology in which financial data and information are

measuring, analysing, interpreting and communicate them towards the Toyota business goals

and objectives effectively. This is also concern about to utlise this process as cost accounting in

the firm. The main difference between management accounting and financial accounting is that

data analysis of management accounting assist the company's manager in order to decision

making in right way, whereas financial accounting is the process which furnish external parties

offering information effectively(Wu and Boateng, 2010). The methodology of management

accounting and report provides the information about day to day financial report and static

analyst of financial data are required to manager to make their decision towards company's

short terms and long term goal and also helps in their day to day operation within the business.

There are several types of tools and techniques which are used in the Toyota business in terms

of accomplish their managerial goals and company's financial objectives as well. There are

various type of management accounting which are inventory management, price optimisation,

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

cost accounting system, job costing system and process costing system as well. All these

accounting systems benefits provide the basic factor about to formulate standardise format in

terms of data analysed, identified and communicate in better way. These all management

accounting methodologies would help the Toyota business in respect of reducing their

manufacturing and other irrelevant cost within the corporation. Job costing system: This approach which is widely used by those businesses which are

doing their business in manufacturing industry. Several times, it could have been seen

that there are wide amounts of customised product acquired to deliver them sufficient

product demanded by their customers(Cokins, 2013). Due to several specifications of

Toyota company's products and services so that there are several types of costing are

available for them to give each particular product to their fixed and specified rate which

must provide to every product and services. Toyota business need to fix their rate of

each customised product and services to manage their costing rate of essential

instruments within the firm which are required to control their essential material cost

within the firm which are unnecessary. Job costing methodology provides the techniques

of maintaining their separate books of accounts of every product and services and

addition of this, various kind of expenses are calculated in them. Toyota business must

use job costing system in the business to specify each product and service cost of the

company which are using while manufacturing automobile vehicles at the workplace so

that their direct material cost and labor cost which are given to their workers and

employees can be reduced and fixed.

Process costing system: This is the approach which are used when there is mass

production of similar product within the business so that where price are concerned with

them could not be differentiated to each other. In this process cost of each

manufacturing product are as same as another product costing in the firm. Costing of

whole mass production are computed and appropriate cost is recognised in term to

understand whole product line within the business(Shields, 2015). This process must

follow by Toyota automotive business to get advantage of which manufacturing process

in the firm are making high cost at the workplace and essential to reduce and manage

their cost effectively by their managerial activities of management accounting within the

business. In this process it could be stated that mass amount of manufacturing costing

2

accounting systems benefits provide the basic factor about to formulate standardise format in

terms of data analysed, identified and communicate in better way. These all management

accounting methodologies would help the Toyota business in respect of reducing their

manufacturing and other irrelevant cost within the corporation. Job costing system: This approach which is widely used by those businesses which are

doing their business in manufacturing industry. Several times, it could have been seen

that there are wide amounts of customised product acquired to deliver them sufficient

product demanded by their customers(Cokins, 2013). Due to several specifications of

Toyota company's products and services so that there are several types of costing are

available for them to give each particular product to their fixed and specified rate which

must provide to every product and services. Toyota business need to fix their rate of

each customised product and services to manage their costing rate of essential

instruments within the firm which are required to control their essential material cost

within the firm which are unnecessary. Job costing methodology provides the techniques

of maintaining their separate books of accounts of every product and services and

addition of this, various kind of expenses are calculated in them. Toyota business must

use job costing system in the business to specify each product and service cost of the

company which are using while manufacturing automobile vehicles at the workplace so

that their direct material cost and labor cost which are given to their workers and

employees can be reduced and fixed.

Process costing system: This is the approach which are used when there is mass

production of similar product within the business so that where price are concerned with

them could not be differentiated to each other. In this process cost of each

manufacturing product are as same as another product costing in the firm. Costing of

whole mass production are computed and appropriate cost is recognised in term to

understand whole product line within the business(Shields, 2015). This process must

follow by Toyota automotive business to get advantage of which manufacturing process

in the firm are making high cost at the workplace and essential to reduce and manage

their cost effectively by their managerial activities of management accounting within the

business. In this process it could be stated that mass amount of manufacturing costing

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

data are gathered and analysed with the help of process costing system and according to

Toyota firm's manager reduce their costing in favor of business profitability and these

process must give advantage in order to accomplish their desired goals and objectives

efficiently.

P.2. Different methodologies used for management accounting reporting

Several kinds of management accounting reporting methodologies are used within the

business because of different type of operational activities are running in Toyota automotive

business so that in these following kind of management accounting reporting company financial

performance are assessed and analysed at various level within the corporation(Abdel-Kader, ed.,

2011). Different kind of management accounting reporting are as below: Budget reporting: This budget reporting defines about to several kinds of financial data

are formulated and gathered and set to be their standard level which is required to achieve

by the firm within assumed time period. In the firm Toyota automotive business there are

several kinds of financial data are generated in this budgeting report by their accounting

managers and management accounting officer of Toyota company. This budgeting report

not only help in assessment of their financial performance as standard set by their

management accounting officers within the business but also helps to examine its

financial progress and achievements from their previous year financial report of the firm.

Toyota business need to develop their budgeting reports by hiring some management

accounting officers with in the business to formulate a proper budgeting report at yearly

basis and quarterly basis to examine their financial reports and it also assists Toyota

automotive company's manager to make their decision towards company more

profitability gaining so that they would be able to accomplish their goals and objectives

more effectively. Job cost report: This is also an essential another budget reporting in this reporting system

different kind of business project are made in various type of accounts books. Nowadays

this is most useful reporting for each business and they are using in their business to

know their financial fluctuation within the business frequently(Quattrone, 2016). Job

costing report are associated with this all financial data which are expenses, cost and

profitability of every specific business exercises which are being done in the business.

3

Toyota firm's manager reduce their costing in favor of business profitability and these

process must give advantage in order to accomplish their desired goals and objectives

efficiently.

P.2. Different methodologies used for management accounting reporting

Several kinds of management accounting reporting methodologies are used within the

business because of different type of operational activities are running in Toyota automotive

business so that in these following kind of management accounting reporting company financial

performance are assessed and analysed at various level within the corporation(Abdel-Kader, ed.,

2011). Different kind of management accounting reporting are as below: Budget reporting: This budget reporting defines about to several kinds of financial data

are formulated and gathered and set to be their standard level which is required to achieve

by the firm within assumed time period. In the firm Toyota automotive business there are

several kinds of financial data are generated in this budgeting report by their accounting

managers and management accounting officer of Toyota company. This budgeting report

not only help in assessment of their financial performance as standard set by their

management accounting officers within the business but also helps to examine its

financial progress and achievements from their previous year financial report of the firm.

Toyota business need to develop their budgeting reports by hiring some management

accounting officers with in the business to formulate a proper budgeting report at yearly

basis and quarterly basis to examine their financial reports and it also assists Toyota

automotive company's manager to make their decision towards company more

profitability gaining so that they would be able to accomplish their goals and objectives

more effectively. Job cost report: This is also an essential another budget reporting in this reporting system

different kind of business project are made in various type of accounts books. Nowadays

this is most useful reporting for each business and they are using in their business to

know their financial fluctuation within the business frequently(Quattrone, 2016). Job

costing report are associated with this all financial data which are expenses, cost and

profitability of every specific business exercises which are being done in the business.

3

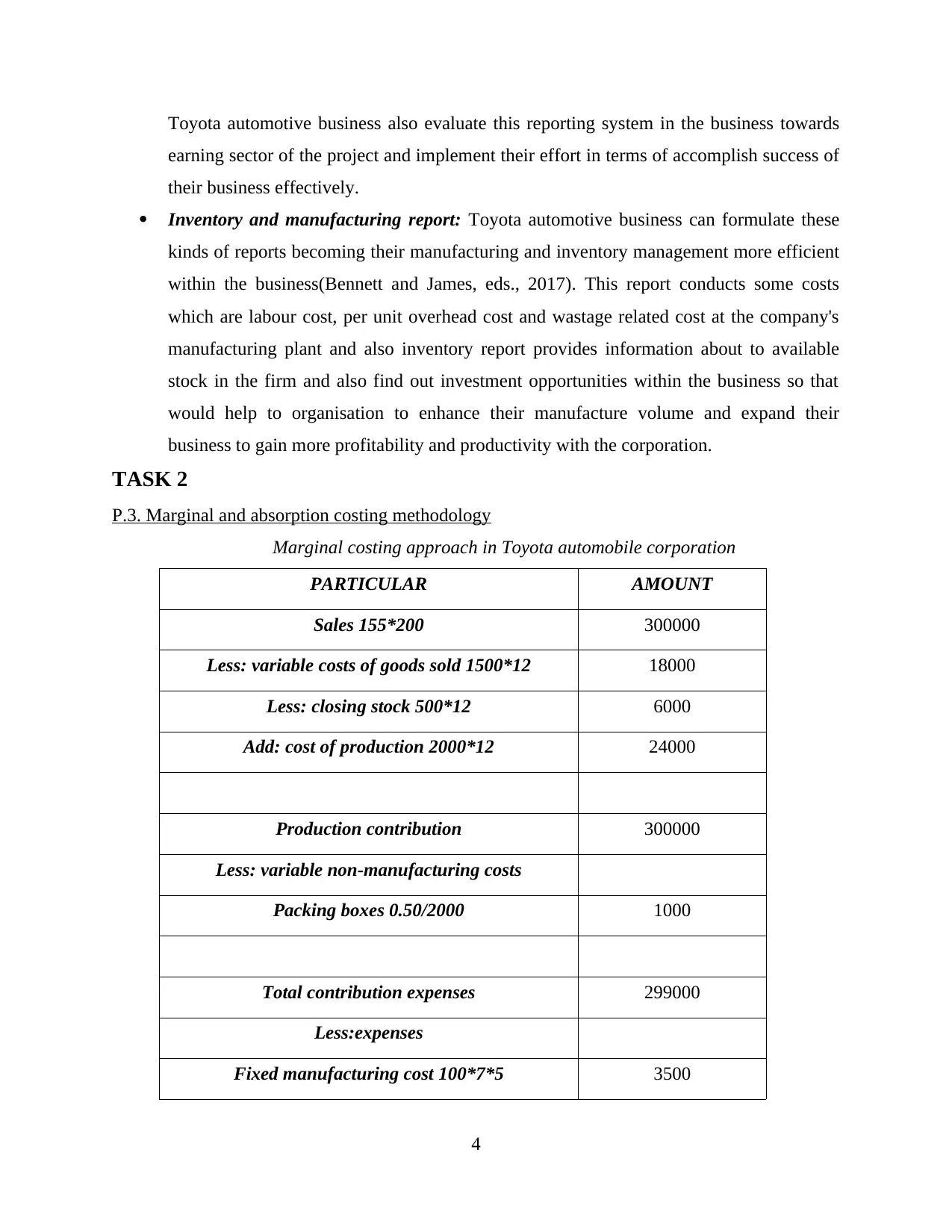

Toyota automotive business also evaluate this reporting system in the business towards

earning sector of the project and implement their effort in terms of accomplish success of

their business effectively.

Inventory and manufacturing report: Toyota automotive business can formulate these

kinds of reports becoming their manufacturing and inventory management more efficient

within the business(Bennett and James, eds., 2017). This report conducts some costs

which are labour cost, per unit overhead cost and wastage related cost at the company's

manufacturing plant and also inventory report provides information about to available

stock in the firm and also find out investment opportunities within the business so that

would help to organisation to enhance their manufacture volume and expand their

business to gain more profitability and productivity with the corporation.

TASK 2

P.3. Marginal and absorption costing methodology

Marginal costing approach in Toyota automobile corporation

PARTICULAR AMOUNT

Sales 155*200 300000

Less: variable costs of goods sold 1500*12 18000

Less: closing stock 500*12 6000

Add: cost of production 2000*12 24000

Production contribution 300000

Less: variable non-manufacturing costs

Packing boxes 0.50/2000 1000

Total contribution expenses 299000

Less:expenses

Fixed manufacturing cost 100*7*5 3500

4

earning sector of the project and implement their effort in terms of accomplish success of

their business effectively.

Inventory and manufacturing report: Toyota automotive business can formulate these

kinds of reports becoming their manufacturing and inventory management more efficient

within the business(Bennett and James, eds., 2017). This report conducts some costs

which are labour cost, per unit overhead cost and wastage related cost at the company's

manufacturing plant and also inventory report provides information about to available

stock in the firm and also find out investment opportunities within the business so that

would help to organisation to enhance their manufacture volume and expand their

business to gain more profitability and productivity with the corporation.

TASK 2

P.3. Marginal and absorption costing methodology

Marginal costing approach in Toyota automobile corporation

PARTICULAR AMOUNT

Sales 155*200 300000

Less: variable costs of goods sold 1500*12 18000

Less: closing stock 500*12 6000

Add: cost of production 2000*12 24000

Production contribution 300000

Less: variable non-manufacturing costs

Packing boxes 0.50/2000 1000

Total contribution expenses 299000

Less:expenses

Fixed manufacturing cost 100*7*5 3500

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

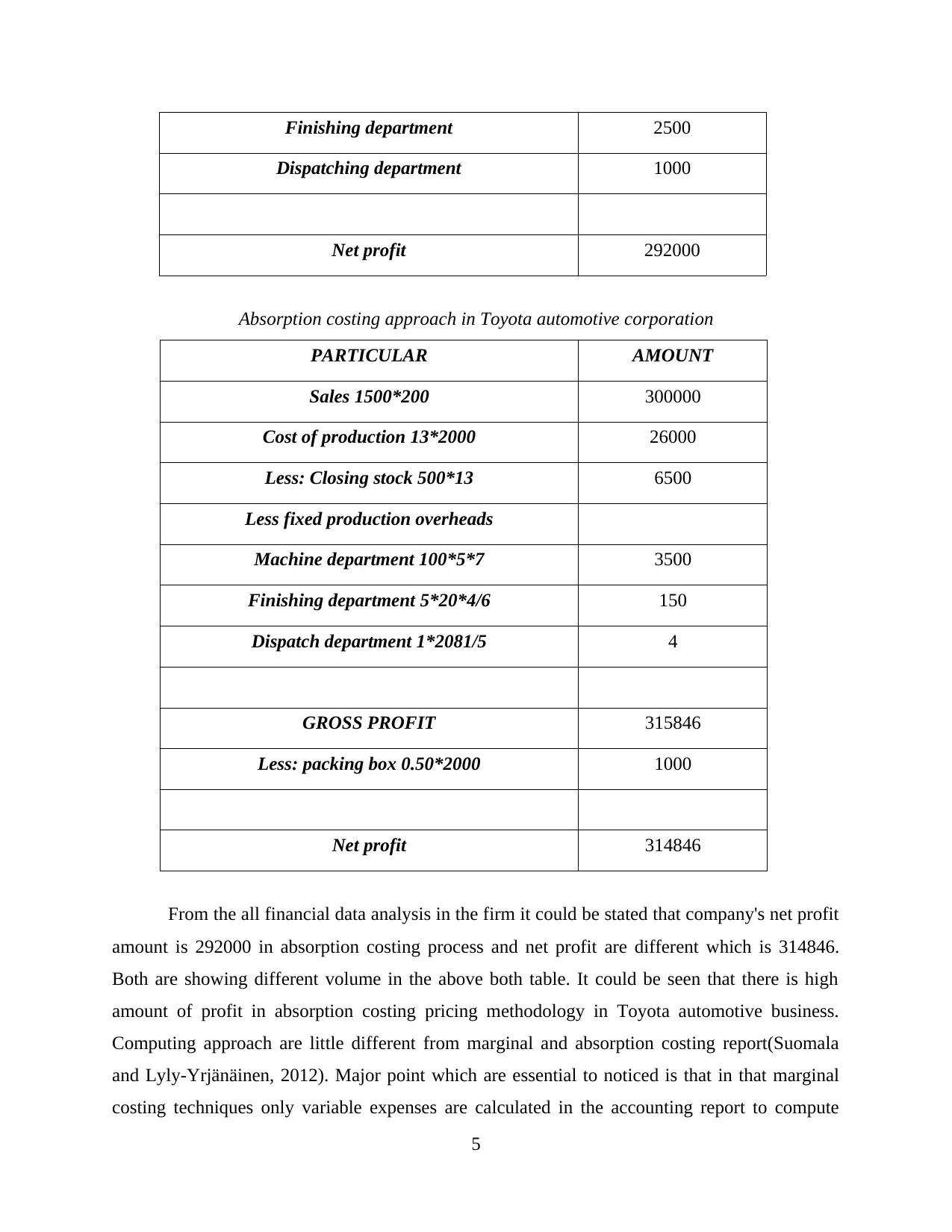

Finishing department 2500

Dispatching department 1000

Net profit 292000

Absorption costing approach in Toyota automotive corporation

PARTICULAR AMOUNT

Sales 1500*200 300000

Cost of production 13*2000 26000

Less: Closing stock 500*13 6500

Less fixed production overheads

Machine department 100*5*7 3500

Finishing department 5*20*4/6 150

Dispatch department 1*2081/5 4

GROSS PROFIT 315846

Less: packing box 0.50*2000 1000

Net profit 314846

From the all financial data analysis in the firm it could be stated that company's net profit

amount is 292000 in absorption costing process and net profit are different which is 314846.

Both are showing different volume in the above both table. It could be seen that there is high

amount of profit in absorption costing pricing methodology in Toyota automotive business.

Computing approach are little different from marginal and absorption costing report(Suomala

and Lyly-Yrjänäinen, 2012). Major point which are essential to noticed is that in that marginal

costing techniques only variable expenses are calculated in the accounting report to compute

5

Dispatching department 1000

Net profit 292000

Absorption costing approach in Toyota automotive corporation

PARTICULAR AMOUNT

Sales 1500*200 300000

Cost of production 13*2000 26000

Less: Closing stock 500*13 6500

Less fixed production overheads

Machine department 100*5*7 3500

Finishing department 5*20*4/6 150

Dispatch department 1*2081/5 4

GROSS PROFIT 315846

Less: packing box 0.50*2000 1000

Net profit 314846

From the all financial data analysis in the firm it could be stated that company's net profit

amount is 292000 in absorption costing process and net profit are different which is 314846.

Both are showing different volume in the above both table. It could be seen that there is high

amount of profit in absorption costing pricing methodology in Toyota automotive business.

Computing approach are little different from marginal and absorption costing report(Suomala

and Lyly-Yrjänäinen, 2012). Major point which are essential to noticed is that in that marginal

costing techniques only variable expenses are calculated in the accounting report to compute

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

overall costing report within Toyota corporation. Moreover, absorption costing techniques are

totally different from marginal costing method and in this technique both fixed and variable

expenses are calculated in the accounting report due to involvement of fixed expenses in these

businesses. Thus, with the help of both these techniques' outcome of these expenses both these

approaches revenue is calculated by their management accounting officers and this reports assist

them to make their decision towards proper form of the business. With the help of above analysis

in this investigation, both techniques are needed to implement in Toyota automotive business and

an appropriate report and judgment of fixed and variable expenses are must be taken in proper

manner so that cost effective decision could be made in respect of Toyota business and their

proper operational activities can be made in reliable manner so that these activities would help

the Toyota automotive business to accomplish their goals and objectives more effectively and

improve their financial performances in better form.

TASK 3

P.4. Advantage and disadvantage of using different planning tools that could be utilised for

budgeting control at workplace

Several kinds of tools and techniques are using by different-different business in terms of

budgeting controlling at their workplaces. These techniques and tools contains some advantage

and disadvantages(Chenhall, 2012). Various type of budgeting planning tools are using in Toyota

business are as below:

Cash Budgeting: Cash budgeting is a most vital tool for planning towards budgeting

control within the business. In Toyota automotive firm, cash budgeting make estimation

about to all cash inflow and outflow financial statements within the business and then net

available cash is identified within the business as well. With the help of all expenses

statements budget planning is made in the firm. Nevertheless, it can be stated that all

expenditure statements are made with assuming of ascertaining limits of cash budgeting

in the corporation so that according to this activities budget are planned in the Toyota

automotive business. There are various advantage and disadvantage of cash budgeting are

as below:

Advantage:

Main advantage of this approach is all cash expenditure within Toyota automotive

business can be identified easily and with the assistance of effective tools and techniques

6

totally different from marginal costing method and in this technique both fixed and variable

expenses are calculated in the accounting report due to involvement of fixed expenses in these

businesses. Thus, with the help of both these techniques' outcome of these expenses both these

approaches revenue is calculated by their management accounting officers and this reports assist

them to make their decision towards proper form of the business. With the help of above analysis

in this investigation, both techniques are needed to implement in Toyota automotive business and

an appropriate report and judgment of fixed and variable expenses are must be taken in proper

manner so that cost effective decision could be made in respect of Toyota business and their

proper operational activities can be made in reliable manner so that these activities would help

the Toyota automotive business to accomplish their goals and objectives more effectively and

improve their financial performances in better form.

TASK 3

P.4. Advantage and disadvantage of using different planning tools that could be utilised for

budgeting control at workplace

Several kinds of tools and techniques are using by different-different business in terms of

budgeting controlling at their workplaces. These techniques and tools contains some advantage

and disadvantages(Chenhall, 2012). Various type of budgeting planning tools are using in Toyota

business are as below:

Cash Budgeting: Cash budgeting is a most vital tool for planning towards budgeting

control within the business. In Toyota automotive firm, cash budgeting make estimation

about to all cash inflow and outflow financial statements within the business and then net

available cash is identified within the business as well. With the help of all expenses

statements budget planning is made in the firm. Nevertheless, it can be stated that all

expenditure statements are made with assuming of ascertaining limits of cash budgeting

in the corporation so that according to this activities budget are planned in the Toyota

automotive business. There are various advantage and disadvantage of cash budgeting are

as below:

Advantage:

Main advantage of this approach is all cash expenditure within Toyota automotive

business can be identified easily and with the assistance of effective tools and techniques

6

of cash budgeting management accounting officer of the firm effectively manage

them(Bebbington, Unerman and O'Dwyer, eds., 2014). This would help the business to

raise their profitability within the Toyota corporation.

Other main advantage of this firm to develop this planning is more easy than other tools

presented there and there is no need to special hire person to prepared this report,

companies management accounting officers also can prepare this type of reports in better

manner.

Disadvantage: Main disadvantage of this planing tools is that it is totally made upon assumption and

approximation within the business so that there are many time approximation goes wrong

in the business so it could make negative effect on Toyota automotive business.

Fixed budget: This is another alternative which are presented to implement in Toyota

automotive corporation. This is unique process from the cash budgeting in terms of

measuring of all budget factors within the business in different manner(Moser, 2012). In

the cash budgeting process there are some deviation of merit and demerit of fixed

budgeting in the firm.

Advantage:

The major advantage of this approach is its value always same in remaining and it will

never change within the business. Hence, Toyota automobile corporation's management

accounting officer are needed to formulate it with full dedication and support of their

efforts.

Other advantages of this approach is that management accounting officer for the Toyota

firm must ensure that implementation of budgeting planning tool is implementing

properly either business climate change continuously.

Disadvantage: The major disadvantage of this approach is that in Toyota business, corporation

circumstance are rapidly change and there is possibility of making not effective result and

implementation within the business so that there is always chances of formulation wrong

decision through utilising this approach within the firm. Zero based budgeting: This is the approach in which all expenses within the business

should be identified properly within each new financial period of firm. This budgeting

7

them(Bebbington, Unerman and O'Dwyer, eds., 2014). This would help the business to

raise their profitability within the Toyota corporation.

Other main advantage of this firm to develop this planning is more easy than other tools

presented there and there is no need to special hire person to prepared this report,

companies management accounting officers also can prepare this type of reports in better

manner.

Disadvantage: Main disadvantage of this planing tools is that it is totally made upon assumption and

approximation within the business so that there are many time approximation goes wrong

in the business so it could make negative effect on Toyota automotive business.

Fixed budget: This is another alternative which are presented to implement in Toyota

automotive corporation. This is unique process from the cash budgeting in terms of

measuring of all budget factors within the business in different manner(Moser, 2012). In

the cash budgeting process there are some deviation of merit and demerit of fixed

budgeting in the firm.

Advantage:

The major advantage of this approach is its value always same in remaining and it will

never change within the business. Hence, Toyota automobile corporation's management

accounting officer are needed to formulate it with full dedication and support of their

efforts.

Other advantages of this approach is that management accounting officer for the Toyota

firm must ensure that implementation of budgeting planning tool is implementing

properly either business climate change continuously.

Disadvantage: The major disadvantage of this approach is that in Toyota business, corporation

circumstance are rapidly change and there is possibility of making not effective result and

implementation within the business so that there is always chances of formulation wrong

decision through utilising this approach within the firm. Zero based budgeting: This is the approach in which all expenses within the business

should be identified properly within each new financial period of firm. This budgeting

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

report also start from zero base within the business and its function also analysed for its

requirements and prices in the corporation(RW Hiebl, 2013). Toyota needs of this

approach in order to check out their previous result and current expenditure measurement

within the firm.

Advantage: This is the approach in which a systematic way are followed while implementation of this

approach within the business and several reliable tools and techniques are using by their

expertise in the firm. Hence, it can define that effective advantages of Toyota firm can be

gained with the help of this approach.

Disadvantage: The major disadvantage of this methodology is that, it takes long process to prepare so

that which can consumer more quality of time of Toyota automotive business.

Capital budgeting method: Capital budgeting method is a long terms investment

planning process such as land, machinery, equipment and building in the business. This

process define about to fixed asset investment within the business in respect to

accomplish goals and objectives effectively(Tessier and Otley, 2012). Toyota automotive

business need to make sure about all the elements of capital budgeting are properly

formulated and it is properly implemented on the business because it needs large amount

of investment to expand their business capital.

Advantage: The main advantage of this approach about it increase business enhancement quality and

their market value of the firm. This is prepared by many of management accounting

experts and manager within Toyota because it makes huge changes within the business

expansion.

Disadvantage:

The main disadvantage of this approach is, it needs wide volume of amount to implement

this strategy in the firm. Toyota need to use many of their resources to formulate this

approach within the firm and it hard to set up within the business and need much time to

implementation of this strategy within the firm.

8

requirements and prices in the corporation(RW Hiebl, 2013). Toyota needs of this

approach in order to check out their previous result and current expenditure measurement

within the firm.

Advantage: This is the approach in which a systematic way are followed while implementation of this

approach within the business and several reliable tools and techniques are using by their

expertise in the firm. Hence, it can define that effective advantages of Toyota firm can be

gained with the help of this approach.

Disadvantage: The major disadvantage of this methodology is that, it takes long process to prepare so

that which can consumer more quality of time of Toyota automotive business.

Capital budgeting method: Capital budgeting method is a long terms investment

planning process such as land, machinery, equipment and building in the business. This

process define about to fixed asset investment within the business in respect to

accomplish goals and objectives effectively(Tessier and Otley, 2012). Toyota automotive

business need to make sure about all the elements of capital budgeting are properly

formulated and it is properly implemented on the business because it needs large amount

of investment to expand their business capital.

Advantage: The main advantage of this approach about it increase business enhancement quality and

their market value of the firm. This is prepared by many of management accounting

experts and manager within Toyota because it makes huge changes within the business

expansion.

Disadvantage:

The main disadvantage of this approach is, it needs wide volume of amount to implement

this strategy in the firm. Toyota need to use many of their resources to formulate this

approach within the firm and it hard to set up within the business and need much time to

implementation of this strategy within the firm.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P.5. Adoption of management accounting system to respond to financial management

There are several business who are facing their financial issues and problems within the

organisation. Many of management accounting system that can be untilised to solve each

financial issues in better ways(van der Steen, 2011). Various management accounting strategies

and approaches which could be used to solve Toyota automotive business financial issues

effectively are as below: Key performance of indicator: This is one of the major necessary tool for Toyota

automotive corporation to solve their financial issues efficiently. Toyota automotive firm

are recently facing their many of financial issues such as lack availability of capital

budget within the business(Otley and Emmanuel, 2013). In this term, Toyota automotive

corporation can use KPI method and in this approach they can compare their actual

financial performance and differences between their stand arid value in the business and

their actual financial performance and assess how much difference are found between

them so with the help of this they can measure how big financial issues they are facing

and in the future how long they are going to face this issues as well. KPI tool can be used

in terms of solving the financial issues of Toyota automotive business.

Financial governance: Financial governance is one of vital approach which can used in

the business in terms of solving their financial issues effectively. In this methodology,

Toyota automotive business can use some rules and regulation which are predetermined

within the business and some demands are followed while performing their task within

the business(Banerjee, 2012). Some circumstance in the firm someone performing their

financial activities within Toyota automotive firm and make any kind of mistake which

become a cause of financial issues arises in the business then individual person would be

responsible of those mistake and all financial losses within Toyota automotive firm as

well. This type of financial issues make any person more conscious and aware about

make sure that think properly about take any decision which are concerned about to

financial within Toyota automotive firm and this management accounting system

provides guideline about to solve all the financial issues which are facing by Toyota

automotive business.

CONCLUSION

9

There are several business who are facing their financial issues and problems within the

organisation. Many of management accounting system that can be untilised to solve each

financial issues in better ways(van der Steen, 2011). Various management accounting strategies

and approaches which could be used to solve Toyota automotive business financial issues

effectively are as below: Key performance of indicator: This is one of the major necessary tool for Toyota

automotive corporation to solve their financial issues efficiently. Toyota automotive firm

are recently facing their many of financial issues such as lack availability of capital

budget within the business(Otley and Emmanuel, 2013). In this term, Toyota automotive

corporation can use KPI method and in this approach they can compare their actual

financial performance and differences between their stand arid value in the business and

their actual financial performance and assess how much difference are found between

them so with the help of this they can measure how big financial issues they are facing

and in the future how long they are going to face this issues as well. KPI tool can be used

in terms of solving the financial issues of Toyota automotive business.

Financial governance: Financial governance is one of vital approach which can used in

the business in terms of solving their financial issues effectively. In this methodology,

Toyota automotive business can use some rules and regulation which are predetermined

within the business and some demands are followed while performing their task within

the business(Banerjee, 2012). Some circumstance in the firm someone performing their

financial activities within Toyota automotive firm and make any kind of mistake which

become a cause of financial issues arises in the business then individual person would be

responsible of those mistake and all financial losses within Toyota automotive firm as

well. This type of financial issues make any person more conscious and aware about

make sure that think properly about take any decision which are concerned about to

financial within Toyota automotive firm and this management accounting system

provides guideline about to solve all the financial issues which are facing by Toyota

automotive business.

CONCLUSION

9

Form the above investigation, it has concluded that some management accounting tools

and techniques assist Toyota automotive business to obtain and acquire the information which is

required by the manager of Toyota business for implementation of business function. Toyota

automotive required to implementation and apply of these all management accounting principles

and techniques in terms of better sustainable growth with the business and we have concluded

about to different methods used for management accounting reporting within Toyota firm.

Moreover, we have alaysed some financial data of Toyota business to calculate cost using

absorption and marginal costing approaches and also explained the advantage and disadvantage

of different types of tools and tech which are used for budgeting control within Toyota

automotive business, ultimately, it is also concluded about how organisation are adopting

different management accounting systems to effectively solve their financial issues within the

business.

10

and techniques assist Toyota automotive business to obtain and acquire the information which is

required by the manager of Toyota business for implementation of business function. Toyota

automotive required to implementation and apply of these all management accounting principles

and techniques in terms of better sustainable growth with the business and we have concluded

about to different methods used for management accounting reporting within Toyota firm.

Moreover, we have alaysed some financial data of Toyota business to calculate cost using

absorption and marginal costing approaches and also explained the advantage and disadvantage

of different types of tools and tech which are used for budgeting control within Toyota

automotive business, ultimately, it is also concluded about how organisation are adopting

different management accounting systems to effectively solve their financial issues within the

business.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.