Financial Analysis Report: Comparing Volkswagen and BMW Financials

VerifiedAdded on 2019/12/03

|20

|4239

|152

Report

AI Summary

This report presents a comprehensive financial statement analysis comparing the performance of Volkswagen and BMW. It begins with an overview of Volkswagen, a major player in the automotive industry, and then delves into the core of the analysis: ratio analysis. The report examines profitability ratios (gross profit, operating profit, and net profit), liquidity ratios (current ratio and quick ratio), activity ratios (total assets turnover and inventory turnover), and solvency ratios to assess the financial health and efficiency of both companies from 2012 to 2014. The analysis includes tables with calculated ratios and comparative discussions, highlighting trends and differences in their financial performance. The report also considers the impact of external factors on the financial outcomes of both companies, providing a well-rounded view of their financial positions and strategic approaches. The conclusion summarizes the key findings, emphasizing areas of strength and weakness for each company, and the references provide the sources used for the analysis.

Financial statement analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

Overview of organization................................................................................................................3

APPROACHES TO ANALYZE AND INTERPRETE FINANCIAL STATEMENTS.................3

INTERNAL AND EXTERNAL FACTORS WHICH BRING CHANGE IN THE RATIOS......13

CONCLUSION .............................................................................................................................15

REFERENCES..............................................................................................................................17

2

INTRODUCTION...........................................................................................................................3

Overview of organization................................................................................................................3

APPROACHES TO ANALYZE AND INTERPRETE FINANCIAL STATEMENTS.................3

INTERNAL AND EXTERNAL FACTORS WHICH BRING CHANGE IN THE RATIOS......13

CONCLUSION .............................................................................................................................15

REFERENCES..............................................................................................................................17

2

Index of Tables

Table 1: Profitability ratio of Volkswagen......................................................................................5

Table 2: Profitability ratio of BMW................................................................................................6

Table 3: Liquidity ratio of Volkswagen.........................................................................................10

Table 4: Liquidity ratio of BMW...................................................................................................10

Table 5: Table 5: Activity ratio of Volkswagen............................................................................12

Table 6: Activity ratio of BMW.....................................................................................................12

Table 7: Table 7: Solvency ratio of Volkswagen...........................................................................14

Table 8: Solvency ratio of BMW...................................................................................................15

3

Table 1: Profitability ratio of Volkswagen......................................................................................5

Table 2: Profitability ratio of BMW................................................................................................6

Table 3: Liquidity ratio of Volkswagen.........................................................................................10

Table 4: Liquidity ratio of BMW...................................................................................................10

Table 5: Table 5: Activity ratio of Volkswagen............................................................................12

Table 6: Activity ratio of BMW.....................................................................................................12

Table 7: Table 7: Solvency ratio of Volkswagen...........................................................................14

Table 8: Solvency ratio of BMW...................................................................................................15

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial statement of any organization are the main documents which contain detail

information related to performance of an organization for particular time span. It assists

corporation to integrate all resources together in order to ensure long run success with increased

rate of return. Present report is based on The Volkswagen group which manufactures and

distributes passenger and commercial vehicles. Along with that other products such as

motorcyles, engines and turbomachinery. In addition to this, ratio analysis has been done to

analyze the performance. Furthermore, impact of external factors has also assessed which aid to

determine future.

OVERVIEW OF ORGANIZATION

Volkswagen is German manufacturer of car which was established in 1946. It was

created by German Labour Front and group of labor played active role in the formation of this

organization. The corporation is operating in Automotive industry which consists of range of

companies and organizations. The corporation under study is second largest automaker after

Toyota. The Volkswagen Golf, the Volkswagen Beetle and the Volkswagen Passat come under

top 10 list of best selling cars. Further, key products sold by the company consists of Cars,

Trucks and buses. In 2010 company posted record for sales of 6.29 million vehicles with the

global market share 11.4%. Furthermore, Similarly, in 2013 the sales turnover of corporation

has increased by 9.7 million. However, it was 9.3 million in 2012. It is showing slow growth of

corporation of marketplace. Apart from this, Volkswagen is performing good in context of

environment and also registered with a Corporate Average Fuel Economy. It was the first car

manufacturer which applied ISO 14000. Later on, 2013 the Volkswagen XL1 considered as most

fuel efficient production car of the world.

APPROACHES TO ANALYZE AND INTERPRETE FINANCIAL

STATEMENTS

There are two methods to analyze the financial statement of an organization. The first one

is horizontal and vertical analysis. Here, horizontal analysis is done with comparison of financial

statement over a series of reporting period. On the other hand, vertical analysis is done on the

basis of proportional analysis of financial statement (Acton, 2013). However, percentage of each

4

Financial statement of any organization are the main documents which contain detail

information related to performance of an organization for particular time span. It assists

corporation to integrate all resources together in order to ensure long run success with increased

rate of return. Present report is based on The Volkswagen group which manufactures and

distributes passenger and commercial vehicles. Along with that other products such as

motorcyles, engines and turbomachinery. In addition to this, ratio analysis has been done to

analyze the performance. Furthermore, impact of external factors has also assessed which aid to

determine future.

OVERVIEW OF ORGANIZATION

Volkswagen is German manufacturer of car which was established in 1946. It was

created by German Labour Front and group of labor played active role in the formation of this

organization. The corporation is operating in Automotive industry which consists of range of

companies and organizations. The corporation under study is second largest automaker after

Toyota. The Volkswagen Golf, the Volkswagen Beetle and the Volkswagen Passat come under

top 10 list of best selling cars. Further, key products sold by the company consists of Cars,

Trucks and buses. In 2010 company posted record for sales of 6.29 million vehicles with the

global market share 11.4%. Furthermore, Similarly, in 2013 the sales turnover of corporation

has increased by 9.7 million. However, it was 9.3 million in 2012. It is showing slow growth of

corporation of marketplace. Apart from this, Volkswagen is performing good in context of

environment and also registered with a Corporate Average Fuel Economy. It was the first car

manufacturer which applied ISO 14000. Later on, 2013 the Volkswagen XL1 considered as most

fuel efficient production car of the world.

APPROACHES TO ANALYZE AND INTERPRETE FINANCIAL

STATEMENTS

There are two methods to analyze the financial statement of an organization. The first one

is horizontal and vertical analysis. Here, horizontal analysis is done with comparison of financial

statement over a series of reporting period. On the other hand, vertical analysis is done on the

basis of proportional analysis of financial statement (Acton, 2013). However, percentage of each

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

items is calculated according to total assets and accordingly financial statements are analyzed.

The foremost approach to analysis the financial statement is ratio analysis. This help to calculate

ratio of all figures and accordingly provide the detail information to organization with regards to

liquidity, productivity and profitability (Elearn, 2013). Ratio analysis of organization has been

done as follows-

Ratio analysis of Volkswagen and BMW

Ratio analysis is the effective means to measure the performance of company for

particular time span. It assists investors to take right decision for investment project.

Furthermore, Volkswagen performance is compared with BMW which is operating in the same

industry and serve as the competitors of firm. With the help of ratio analysis company is judged

on specific parameter like liquidity, solvency and efficiency as well as profitability. However, it

provides only quantitative measure (Healy and Palepu, 2007). There are several other means

such as contribution of firm towards social activities, employee welfare and expansion as well as

creation of goodwill serve major factors through which qualitative analysis can be done. Also,

brand image of firm is also the main factors through which number of customer's are increased

towards offering of company. In addition to this, qualitative analysis is done with the help of

assessing annual report of corporation so as to get fruitful outcomes for the performance of the

corporation under study (Kierulff and Petersen, 2009).

It is very important to analyze the performance of company with its competitor. It assists

management to bring improvement in the current position of the firm by focusing on several

factors. These factors can be related to cost of production, additional expense and other strategies

which might have been used by competitors in order to retain customers for longer time span.

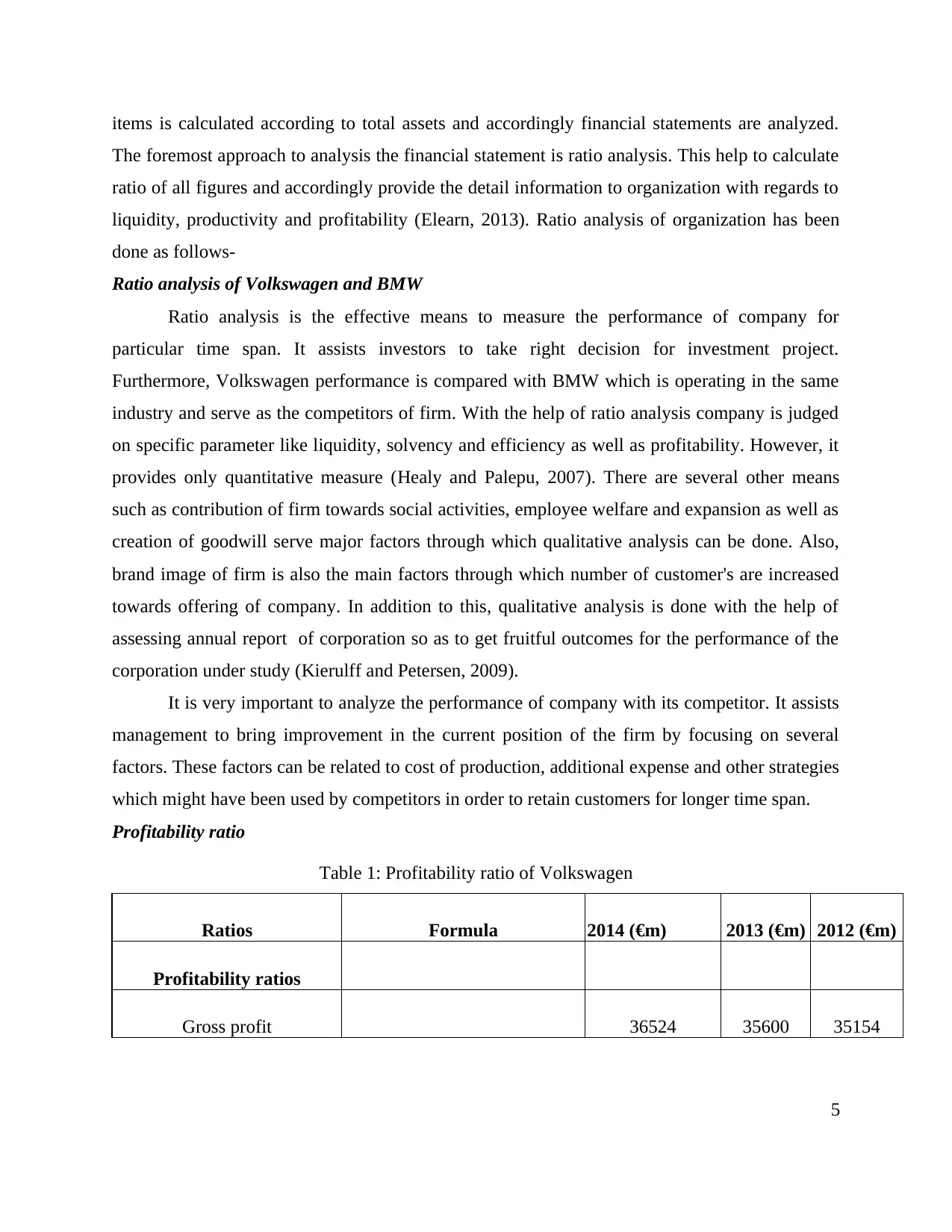

Profitability ratio

Table 1: Profitability ratio of Volkswagen

Ratios Formula 2014 (€m) 2013 (€m) 2012 (€m)

Profitability ratios

Gross profit 36524 35600 35154

5

The foremost approach to analysis the financial statement is ratio analysis. This help to calculate

ratio of all figures and accordingly provide the detail information to organization with regards to

liquidity, productivity and profitability (Elearn, 2013). Ratio analysis of organization has been

done as follows-

Ratio analysis of Volkswagen and BMW

Ratio analysis is the effective means to measure the performance of company for

particular time span. It assists investors to take right decision for investment project.

Furthermore, Volkswagen performance is compared with BMW which is operating in the same

industry and serve as the competitors of firm. With the help of ratio analysis company is judged

on specific parameter like liquidity, solvency and efficiency as well as profitability. However, it

provides only quantitative measure (Healy and Palepu, 2007). There are several other means

such as contribution of firm towards social activities, employee welfare and expansion as well as

creation of goodwill serve major factors through which qualitative analysis can be done. Also,

brand image of firm is also the main factors through which number of customer's are increased

towards offering of company. In addition to this, qualitative analysis is done with the help of

assessing annual report of corporation so as to get fruitful outcomes for the performance of the

corporation under study (Kierulff and Petersen, 2009).

It is very important to analyze the performance of company with its competitor. It assists

management to bring improvement in the current position of the firm by focusing on several

factors. These factors can be related to cost of production, additional expense and other strategies

which might have been used by competitors in order to retain customers for longer time span.

Profitability ratio

Table 1: Profitability ratio of Volkswagen

Ratios Formula 2014 (€m) 2013 (€m) 2012 (€m)

Profitability ratios

Gross profit 36524 35600 35154

5

Operating profit 12697 11671 11948

Net profit 11068 9145 21881

Net Sales 202458 197007 192676

Gross Profit Ratio (Gross Profit/ Net Sales) *100 18.04% 18.07% 18.25%

Operating Profit Ratio

(Operating Profit/ Net Sales)

*100 6.27% 5.92% 6.20%

Net Profit Ratio (Net Profit/ Net Sales) *100 5.47% 4.64% 11.36%

Table 2: Profitability ratio of BMW

Ratios Formula 2014 (€m) 2013 (€m) 2012 (€m)

Profitability ratios

Gross profit 17005 15268 15494

Operating profit 9118 7978 8275

Net profit 5817 5329 5111

Net Sales 80401 76059 76848

Gross Profit Ratio (Gross Profit/ Net Sales) *100 21.15% 20.07% 20.16%

Operating Profit Ratio

(Operating Profit/ Net Sales)

*100 11.34% 10.49% 10.77%

Net Profit Ratio (Net Profit/ Net Sales) *100 7.23% 7.01% 6.65%

6

Net profit 11068 9145 21881

Net Sales 202458 197007 192676

Gross Profit Ratio (Gross Profit/ Net Sales) *100 18.04% 18.07% 18.25%

Operating Profit Ratio

(Operating Profit/ Net Sales)

*100 6.27% 5.92% 6.20%

Net Profit Ratio (Net Profit/ Net Sales) *100 5.47% 4.64% 11.36%

Table 2: Profitability ratio of BMW

Ratios Formula 2014 (€m) 2013 (€m) 2012 (€m)

Profitability ratios

Gross profit 17005 15268 15494

Operating profit 9118 7978 8275

Net profit 5817 5329 5111

Net Sales 80401 76059 76848

Gross Profit Ratio (Gross Profit/ Net Sales) *100 21.15% 20.07% 20.16%

Operating Profit Ratio

(Operating Profit/ Net Sales)

*100 11.34% 10.49% 10.77%

Net Profit Ratio (Net Profit/ Net Sales) *100 7.23% 7.01% 6.65%

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

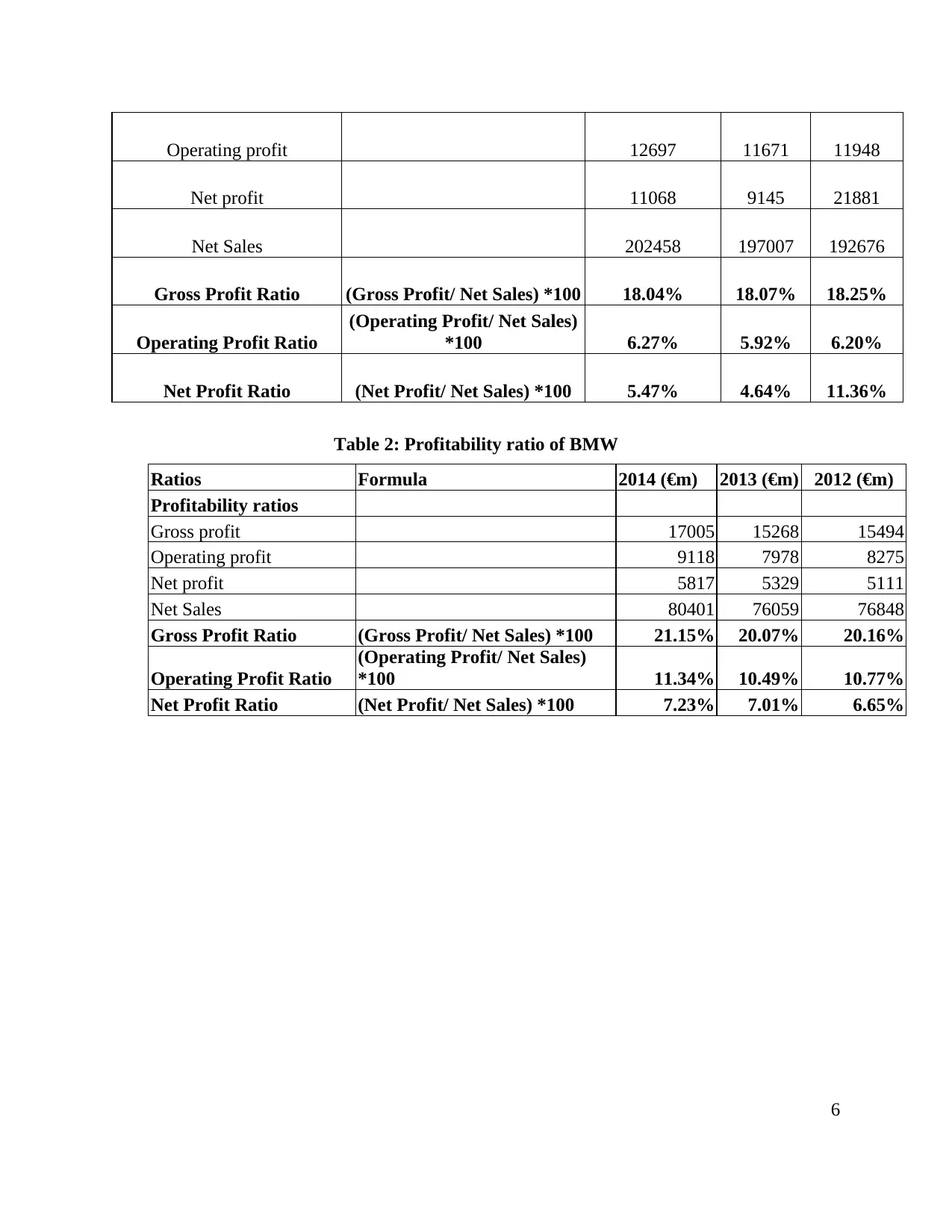

According the above calculation it can be said that profitability of BMW is increased

rapid speed up in comparison to Volkswagen. However, there is downward trend in the return of

BMW. Further, Volkswagen’s rate of return is keep on increasing. Further, in 2012 profit of

Volkswagen was 18.04% which rose in 2014 by 18.25%. However, the reason behind low

profitability is higher cost paid to suppliers (Nga and Yien,2013).

Comparison on the basis of operating profit

7

04/07/1905 05/07/1905 06/07/1905

0.16

0.17

0.18

0.19

0.2

0.21

0.22

18.04%18.07%18.25%

21.15%

20.07%20.16%

Gross profit ratio

Volkswagen

BMW

rapid speed up in comparison to Volkswagen. However, there is downward trend in the return of

BMW. Further, Volkswagen’s rate of return is keep on increasing. Further, in 2012 profit of

Volkswagen was 18.04% which rose in 2014 by 18.25%. However, the reason behind low

profitability is higher cost paid to suppliers (Nga and Yien,2013).

Comparison on the basis of operating profit

7

04/07/1905 05/07/1905 06/07/1905

0.16

0.17

0.18

0.19

0.2

0.21

0.22

18.04%18.07%18.25%

21.15%

20.07%20.16%

Gross profit ratio

Volkswagen

BMW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

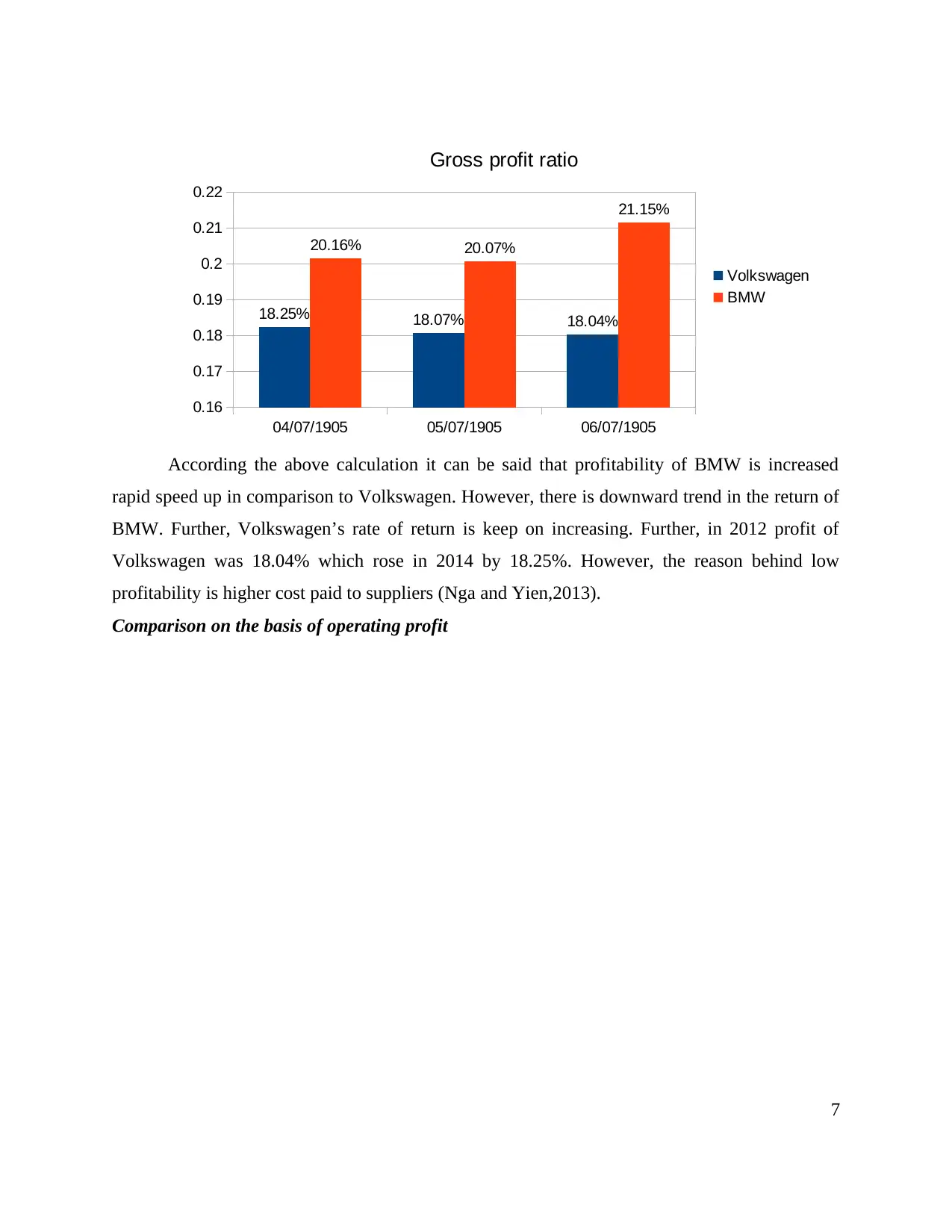

The aforementioned operating profit ratio is showing that BMW's operating profit is

constantly increasing. On the other hand, Volkswagen's return has high variation in the return.

However, the variation in the profitability of corporation is almost similar (Atkinson, 2007). This

is because both corporation is getting downward trend from 2012 to 2013. Furthermore, in 2014

there is increased rate of return in profitability of both firms. In addition to this, favorable market

condition assists BMW to enhance overall rate of return in the marketplace.

Comparison on the basis of net profit

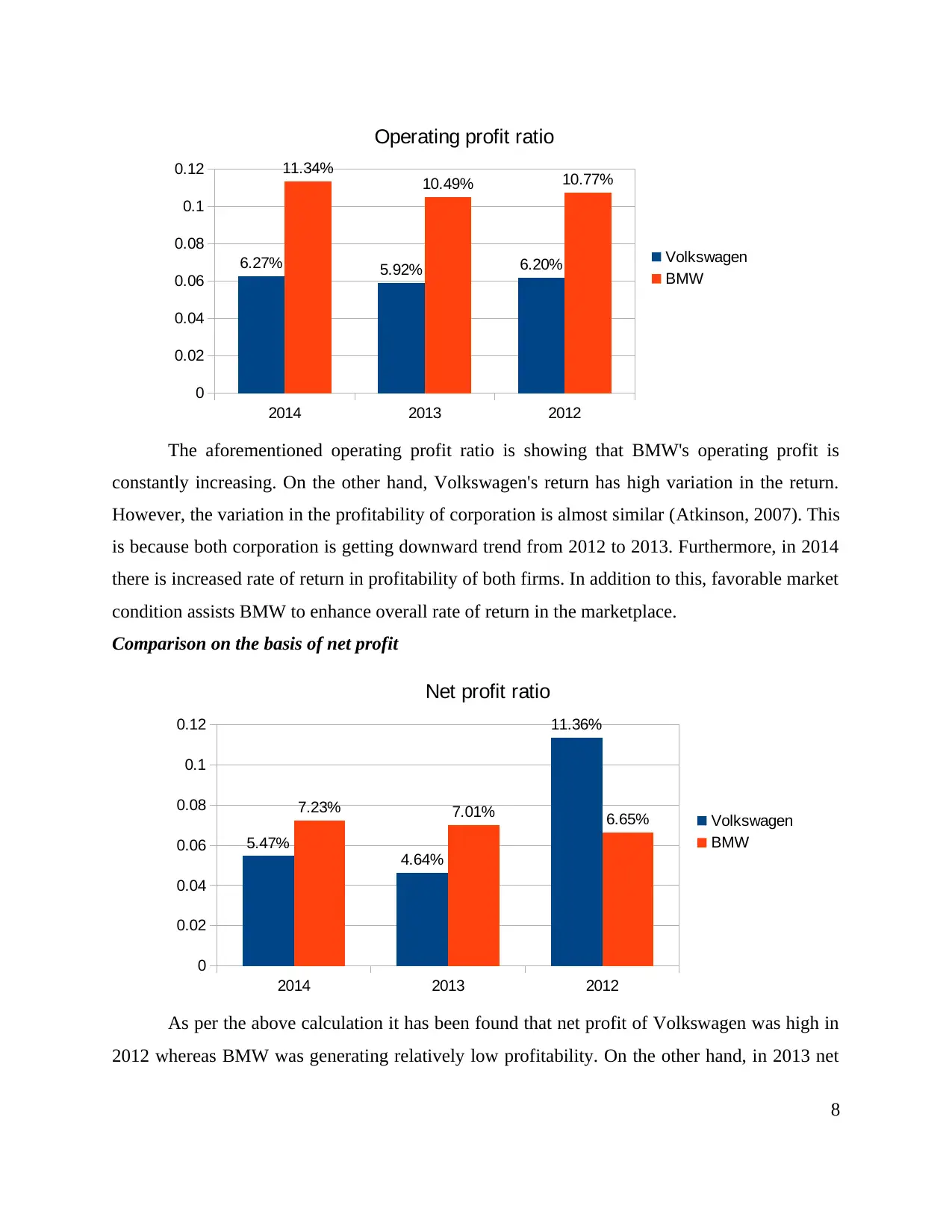

As per the above calculation it has been found that net profit of Volkswagen was high in

2012 whereas BMW was generating relatively low profitability. On the other hand, in 2013 net

8

2014 2013 2012

0

0.02

0.04

0.06

0.08

0.1

0.12

6.27% 5.92% 6.20%

11.34%

10.49% 10.77%

Operating profit ratio

Volkswagen

BMW

2014 2013 2012

0

0.02

0.04

0.06

0.08

0.1

0.12

5.47%

4.64%

11.36%

7.23% 7.01% 6.65%

Net profit ratio

Volkswagen

BMW

constantly increasing. On the other hand, Volkswagen's return has high variation in the return.

However, the variation in the profitability of corporation is almost similar (Atkinson, 2007). This

is because both corporation is getting downward trend from 2012 to 2013. Furthermore, in 2014

there is increased rate of return in profitability of both firms. In addition to this, favorable market

condition assists BMW to enhance overall rate of return in the marketplace.

Comparison on the basis of net profit

As per the above calculation it has been found that net profit of Volkswagen was high in

2012 whereas BMW was generating relatively low profitability. On the other hand, in 2013 net

8

2014 2013 2012

0

0.02

0.04

0.06

0.08

0.1

0.12

6.27% 5.92% 6.20%

11.34%

10.49% 10.77%

Operating profit ratio

Volkswagen

BMW

2014 2013 2012

0

0.02

0.04

0.06

0.08

0.1

0.12

5.47%

4.64%

11.36%

7.23% 7.01% 6.65%

Net profit ratio

Volkswagen

BMW

profit of BMW was 7.01% which has increased in 2014 by 7.23%. In addition to this, in 2014 net

profit for the Volkswagen is 5.47. It depicts that there is drastic decline in profitability of

Volkswagen. Also, the profitability is varying to a great extent. Ont the other hand, BMW is

continuously growing at rapid speed (Yazdifar, 2004). It shows that corporation is making use of

competitive strategies in order to cope up with changing scenario. It aids to achieve long as well

as short term objectives of firm in the marketplace. On the other side, Volkswagen profitability is

going down due to high additional expenses. Furthermore, it can be said that BMW is

performing good in term of rate of return.

Comparison of Volkswagen and BMW on the basis of liquidity ratio

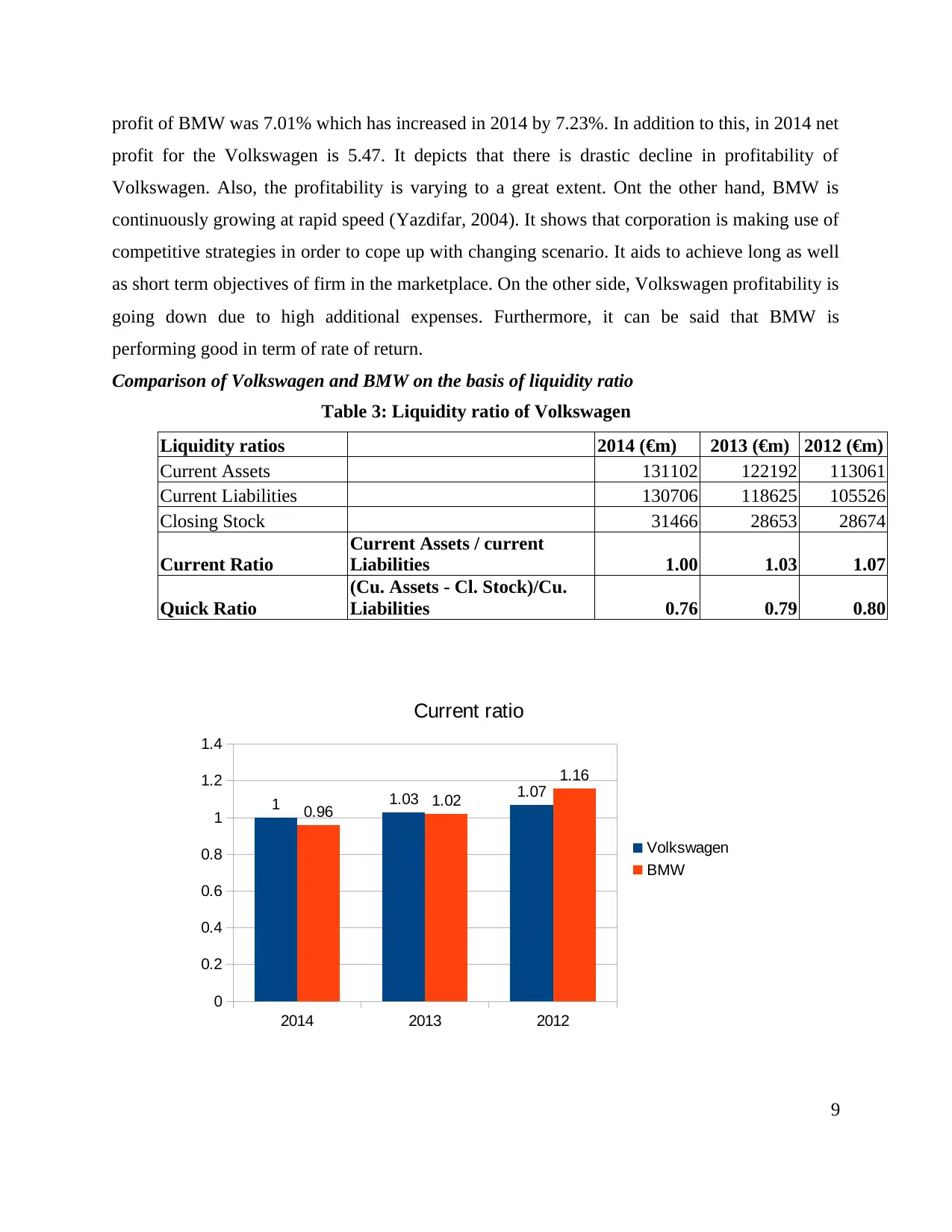

Table 3: Liquidity ratio of Volkswagen

Liquidity ratios 2014 (€m) 2013 (€m) 2012 (€m)

Current Assets 131102 122192 113061

Current Liabilities 130706 118625 105526

Closing Stock 31466 28653 28674

Current Ratio

Current Assets / current

Liabilities 1.00 1.03 1.07

Quick Ratio

(Cu. Assets - Cl. Stock)/Cu.

Liabilities 0.76 0.79 0.80

9

2014 2013 2012

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1 1.03 1.07

0.96 1.02

1.16

Current ratio

Volkswagen

BMW

profit for the Volkswagen is 5.47. It depicts that there is drastic decline in profitability of

Volkswagen. Also, the profitability is varying to a great extent. Ont the other hand, BMW is

continuously growing at rapid speed (Yazdifar, 2004). It shows that corporation is making use of

competitive strategies in order to cope up with changing scenario. It aids to achieve long as well

as short term objectives of firm in the marketplace. On the other side, Volkswagen profitability is

going down due to high additional expenses. Furthermore, it can be said that BMW is

performing good in term of rate of return.

Comparison of Volkswagen and BMW on the basis of liquidity ratio

Table 3: Liquidity ratio of Volkswagen

Liquidity ratios 2014 (€m) 2013 (€m) 2012 (€m)

Current Assets 131102 122192 113061

Current Liabilities 130706 118625 105526

Closing Stock 31466 28653 28674

Current Ratio

Current Assets / current

Liabilities 1.00 1.03 1.07

Quick Ratio

(Cu. Assets - Cl. Stock)/Cu.

Liabilities 0.76 0.79 0.80

9

2014 2013 2012

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1 1.03 1.07

0.96 1.02

1.16

Current ratio

Volkswagen

BMW

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The current ratio depicts ability of firm to meet its short term obligation in order to meet

organizational objectives. This ratio depict combination of both current assets and liabilities.

From the calculation it has been found that current ratio of both corporation is up to the mark.

However, in 2014 BMW's current ratio is .96. It indicate that organization can find problem in

managing its short term obligation after a certain time span (Macintosh and Quattrone, 2010).

Furthermore, it might be possible that BMW accessed to costly sources of finance which in turn

current liabilities has been increased in comparison to current assets. Thus, current ratio of

Volkswagen is appropriate in comparison to other.

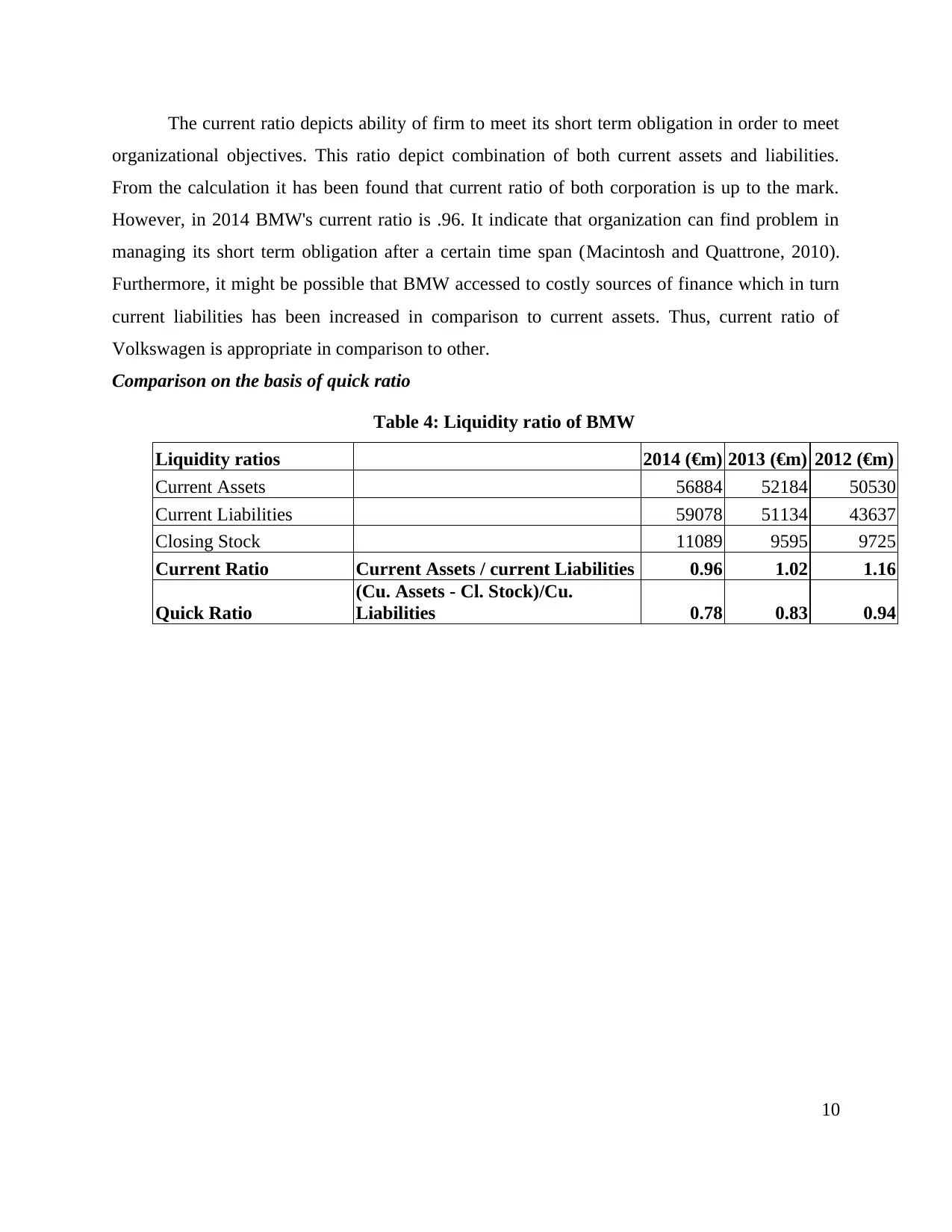

Comparison on the basis of quick ratio

Table 4: Liquidity ratio of BMW

Liquidity ratios 2014 (€m) 2013 (€m) 2012 (€m)

Current Assets 56884 52184 50530

Current Liabilities 59078 51134 43637

Closing Stock 11089 9595 9725

Current Ratio Current Assets / current Liabilities 0.96 1.02 1.16

Quick Ratio

(Cu. Assets - Cl. Stock)/Cu.

Liabilities 0.78 0.83 0.94

10

organizational objectives. This ratio depict combination of both current assets and liabilities.

From the calculation it has been found that current ratio of both corporation is up to the mark.

However, in 2014 BMW's current ratio is .96. It indicate that organization can find problem in

managing its short term obligation after a certain time span (Macintosh and Quattrone, 2010).

Furthermore, it might be possible that BMW accessed to costly sources of finance which in turn

current liabilities has been increased in comparison to current assets. Thus, current ratio of

Volkswagen is appropriate in comparison to other.

Comparison on the basis of quick ratio

Table 4: Liquidity ratio of BMW

Liquidity ratios 2014 (€m) 2013 (€m) 2012 (€m)

Current Assets 56884 52184 50530

Current Liabilities 59078 51134 43637

Closing Stock 11089 9595 9725

Current Ratio Current Assets / current Liabilities 0.96 1.02 1.16

Quick Ratio

(Cu. Assets - Cl. Stock)/Cu.

Liabilities 0.78 0.83 0.94

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

According the above table, it has been found that quick ratio of BMW is appropriate in

comparison to Volkswagen. This is because Volkswagen's quick ratio is going down year by

year which indicate that credit policy of firm not up to the mark. It may create financial burden

by which management cannot be able to meet its short term obligation. On the other hand, quick

ratio of BMW also have downward direction. It indicate poor performance of firm. It might be

possible that creditors are paid in less time span whereas extensive time has been given to

debtors. In such kind of circumstances firm need to have proper control on cash in order to

ensure about smooth flow of production.

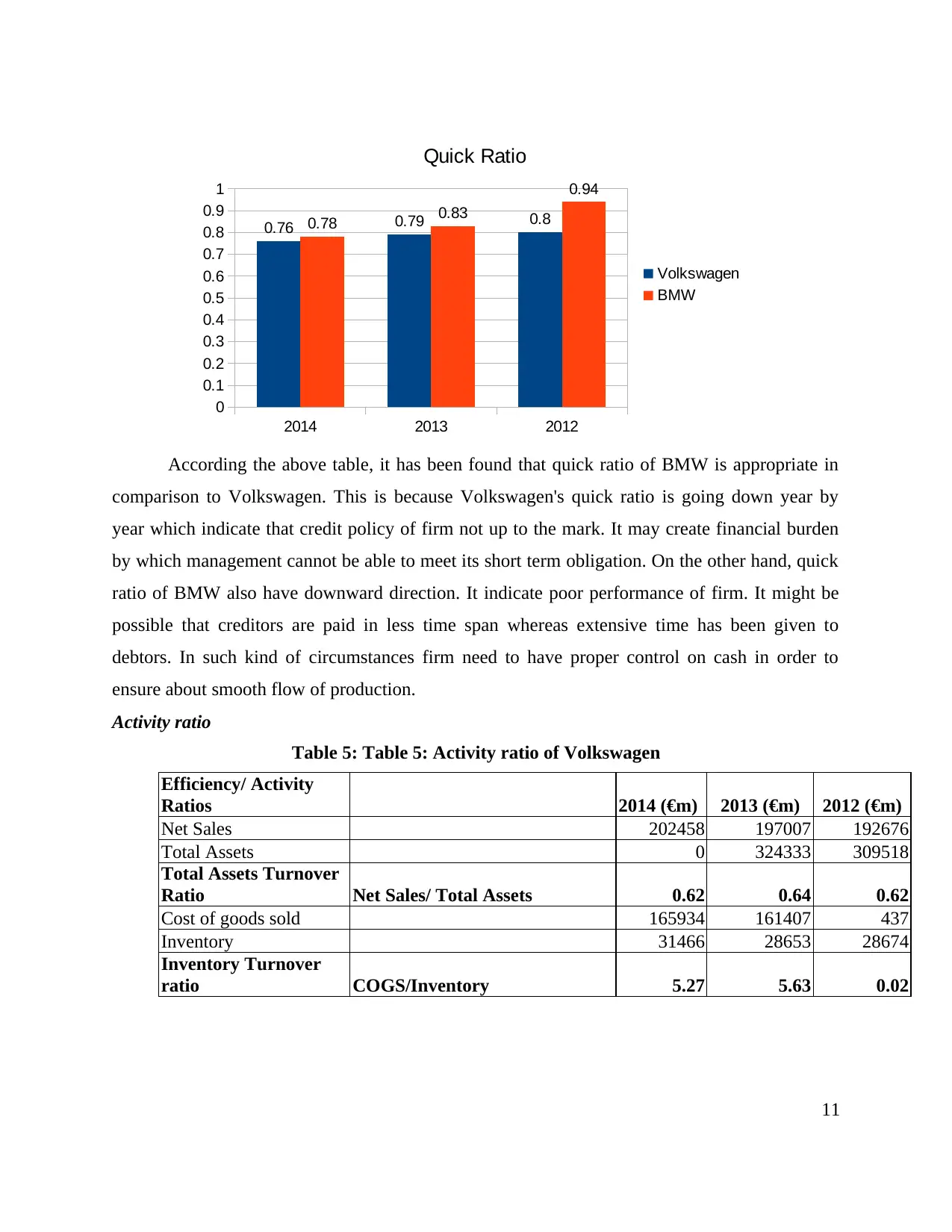

Activity ratio

Table 5: Table 5: Activity ratio of Volkswagen

Efficiency/ Activity

Ratios 2014 (€m) 2013 (€m) 2012 (€m)

Net Sales 202458 197007 192676

Total Assets 0 324333 309518

Total Assets Turnover

Ratio Net Sales/ Total Assets 0.62 0.64 0.62

Cost of goods sold 165934 161407 437

Inventory 31466 28653 28674

Inventory Turnover

ratio COGS/Inventory 5.27 5.63 0.02

11

2014 2013 2012

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

0.76 0.79 0.80.78 0.83

0.94

Quick Ratio

Volkswagen

BMW

comparison to Volkswagen. This is because Volkswagen's quick ratio is going down year by

year which indicate that credit policy of firm not up to the mark. It may create financial burden

by which management cannot be able to meet its short term obligation. On the other hand, quick

ratio of BMW also have downward direction. It indicate poor performance of firm. It might be

possible that creditors are paid in less time span whereas extensive time has been given to

debtors. In such kind of circumstances firm need to have proper control on cash in order to

ensure about smooth flow of production.

Activity ratio

Table 5: Table 5: Activity ratio of Volkswagen

Efficiency/ Activity

Ratios 2014 (€m) 2013 (€m) 2012 (€m)

Net Sales 202458 197007 192676

Total Assets 0 324333 309518

Total Assets Turnover

Ratio Net Sales/ Total Assets 0.62 0.64 0.62

Cost of goods sold 165934 161407 437

Inventory 31466 28653 28674

Inventory Turnover

ratio COGS/Inventory 5.27 5.63 0.02

11

2014 2013 2012

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

0.76 0.79 0.80.78 0.83

0.94

Quick Ratio

Volkswagen

BMW

Table 6: Activity ratio of BMW

Efficiency/ Activity

Ratios 2014 (€m) 2013 (€m) 2012 (€m)

Net Sales 80401 76059 76848

Total Assets 154803 138377 131835

Total Assets Turnover

Ratio Net Sales/ Total Assets 0.58 0.58 0.58

Cost of goods sold 63396 60791 61354

Inventory 11089 9595 9725

Inventory Turnover

ratio COGS/Inventory 5.72 6.34 6.31

Comparing the efficiency of firm on the basis of total assets turnover

The total assets turnover of both organization has greater variation as it is showing steady

growth. The total assets turnover generally depicts that how an organization manage its assets by

ensuring optimum utilization of limited resources. The graph indicates that total assets turnover

ratio of Volkswagen is higher than BMW (Tauringana and Afrifa, 2013). It depicts that

corporation is able to utilize its assets in more effective manner. However, management make

sure that all limited resources are utilized properly in order to generate high rate of return.

Furthermore, BMW is having problem related to maintaining enough cash for its production

activities. Also, management is having while managing current assets like inventories etc.

12

2014 2013 2012

0.54

0.56

0.58

0.6

0.62

0.64

0.66

0.62

0.64

0.62

0.58 0.58 0.58

Total Assets Turnover Ratio

Volkswagen

BMW

Efficiency/ Activity

Ratios 2014 (€m) 2013 (€m) 2012 (€m)

Net Sales 80401 76059 76848

Total Assets 154803 138377 131835

Total Assets Turnover

Ratio Net Sales/ Total Assets 0.58 0.58 0.58

Cost of goods sold 63396 60791 61354

Inventory 11089 9595 9725

Inventory Turnover

ratio COGS/Inventory 5.72 6.34 6.31

Comparing the efficiency of firm on the basis of total assets turnover

The total assets turnover of both organization has greater variation as it is showing steady

growth. The total assets turnover generally depicts that how an organization manage its assets by

ensuring optimum utilization of limited resources. The graph indicates that total assets turnover

ratio of Volkswagen is higher than BMW (Tauringana and Afrifa, 2013). It depicts that

corporation is able to utilize its assets in more effective manner. However, management make

sure that all limited resources are utilized properly in order to generate high rate of return.

Furthermore, BMW is having problem related to maintaining enough cash for its production

activities. Also, management is having while managing current assets like inventories etc.

12

2014 2013 2012

0.54

0.56

0.58

0.6

0.62

0.64

0.66

0.62

0.64

0.62

0.58 0.58 0.58

Total Assets Turnover Ratio

Volkswagen

BMW

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.