Financial Management and Control: Zurich Plc Performance Analysis

VerifiedAdded on 2020/02/03

|27

|5277

|77

Report

AI Summary

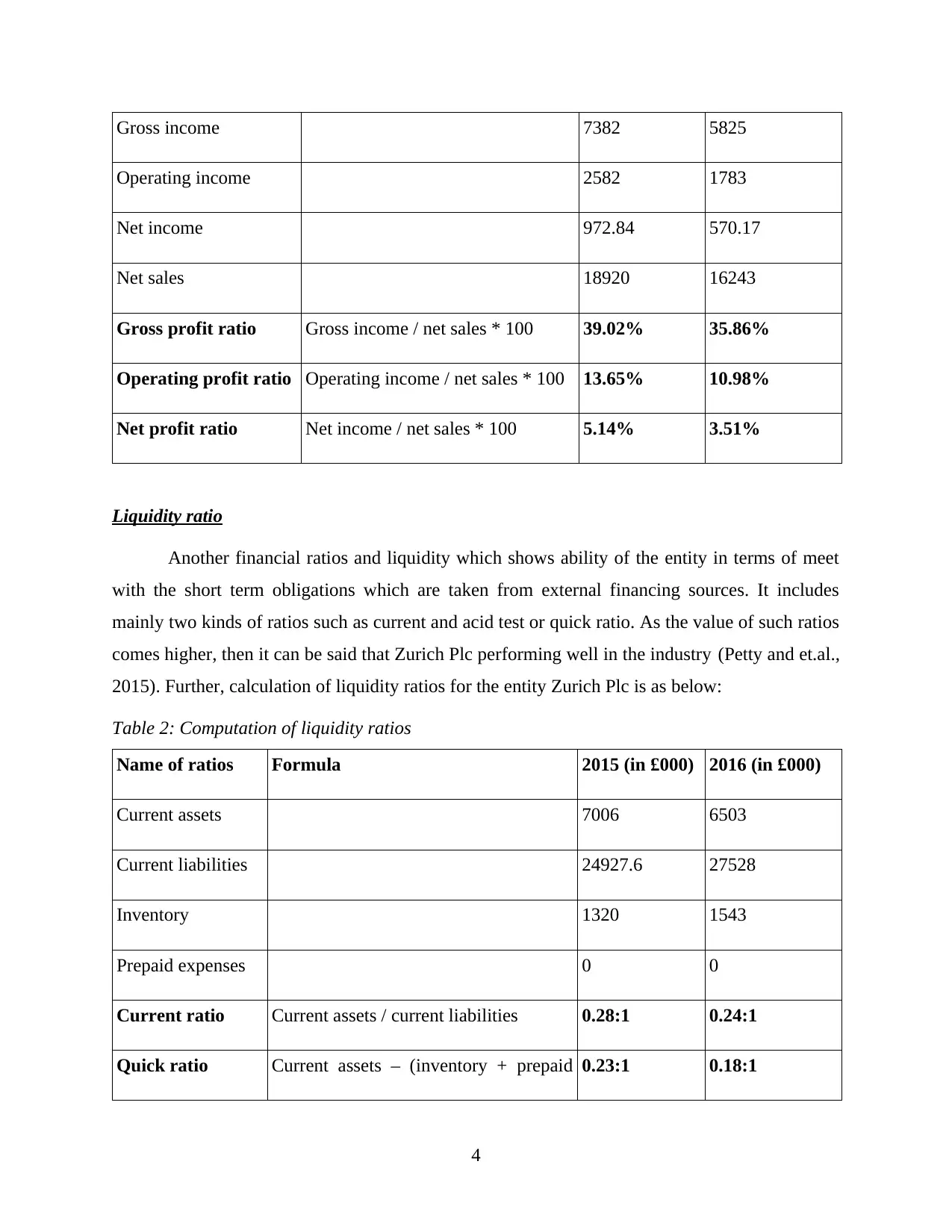

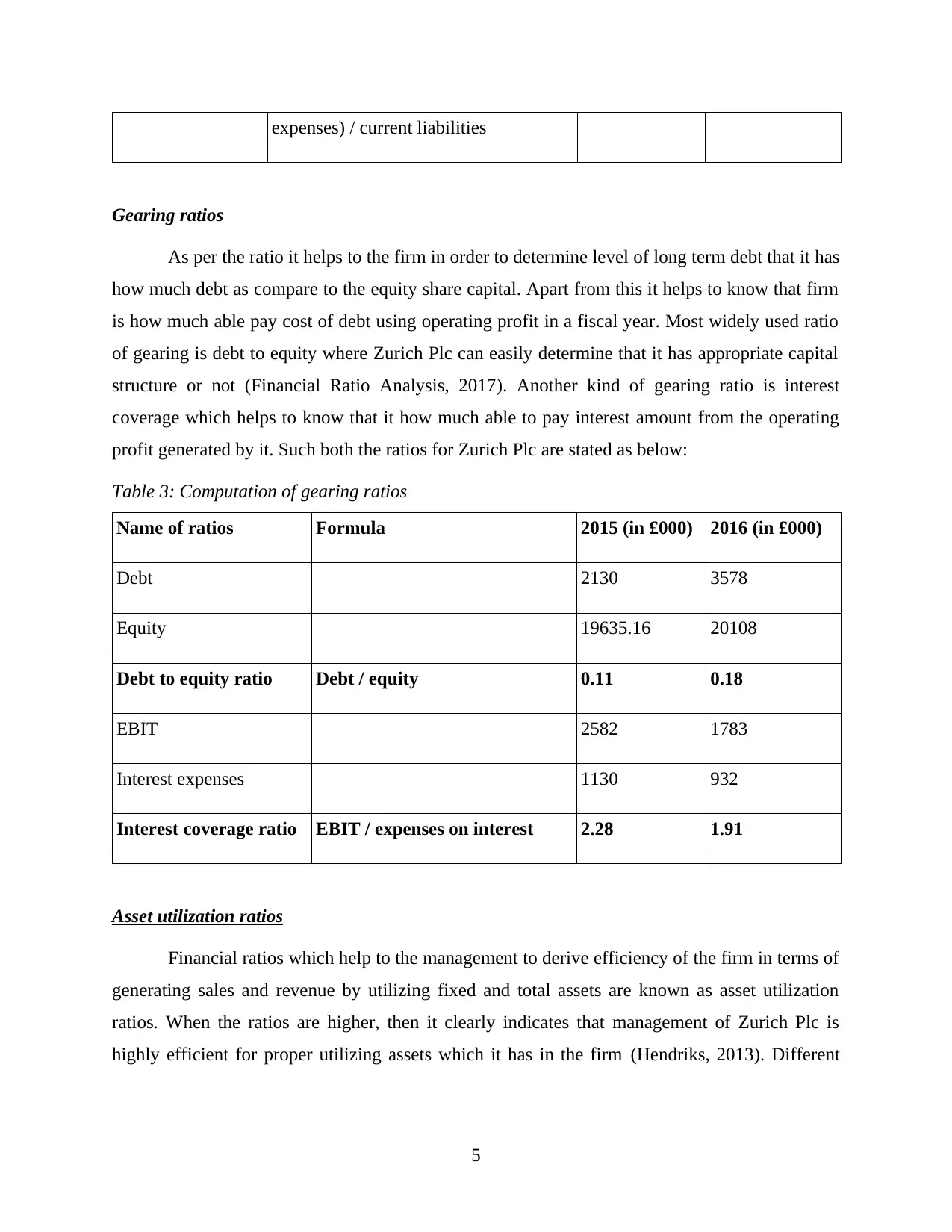

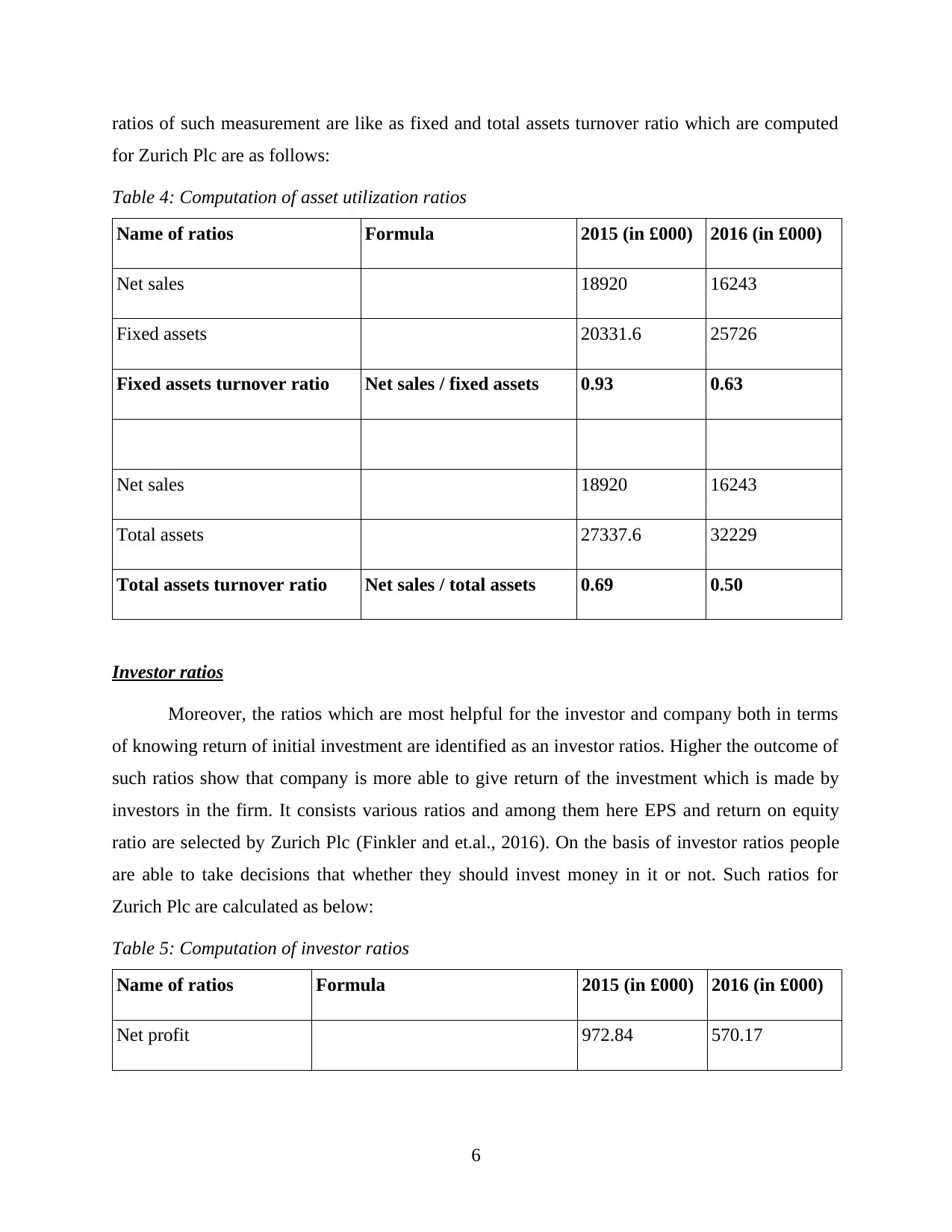

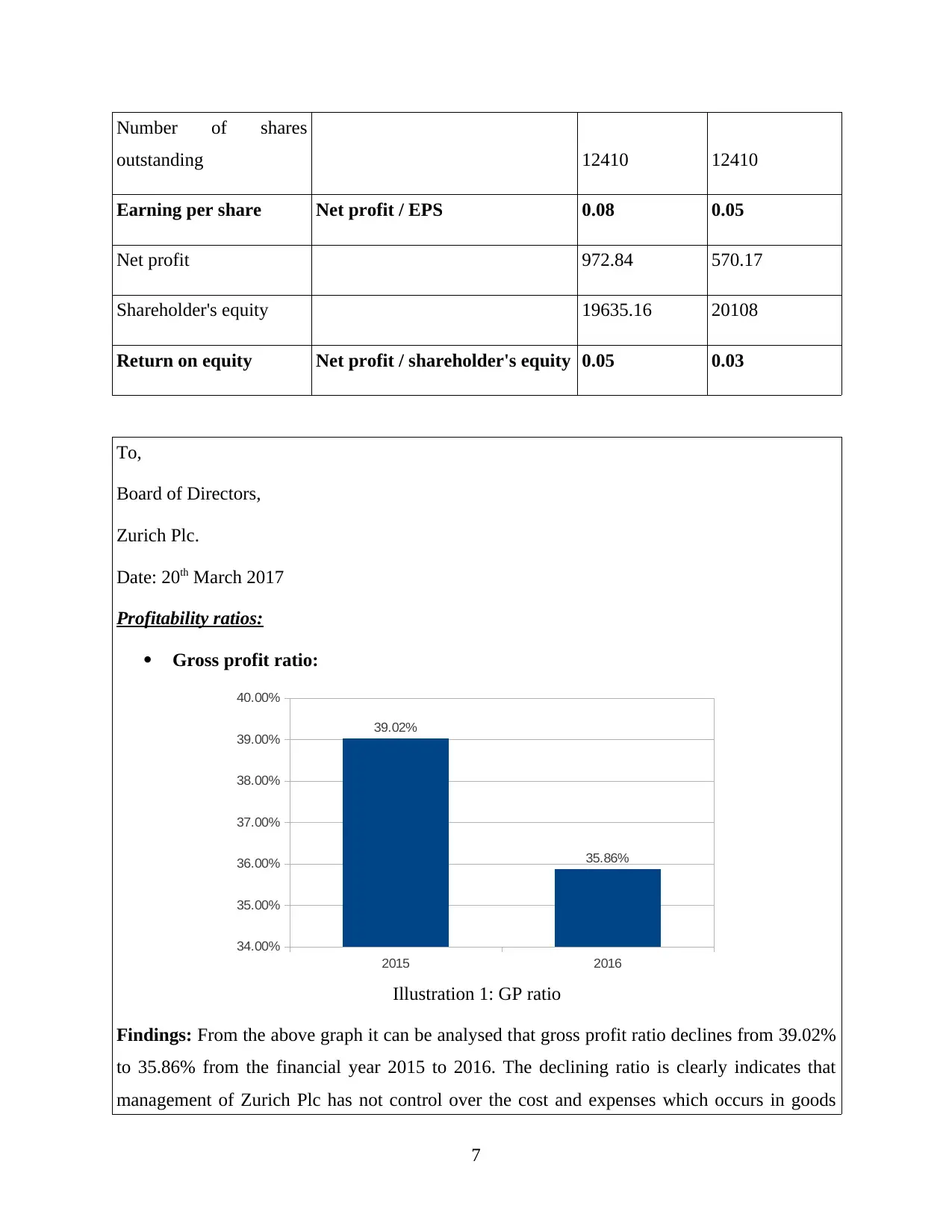

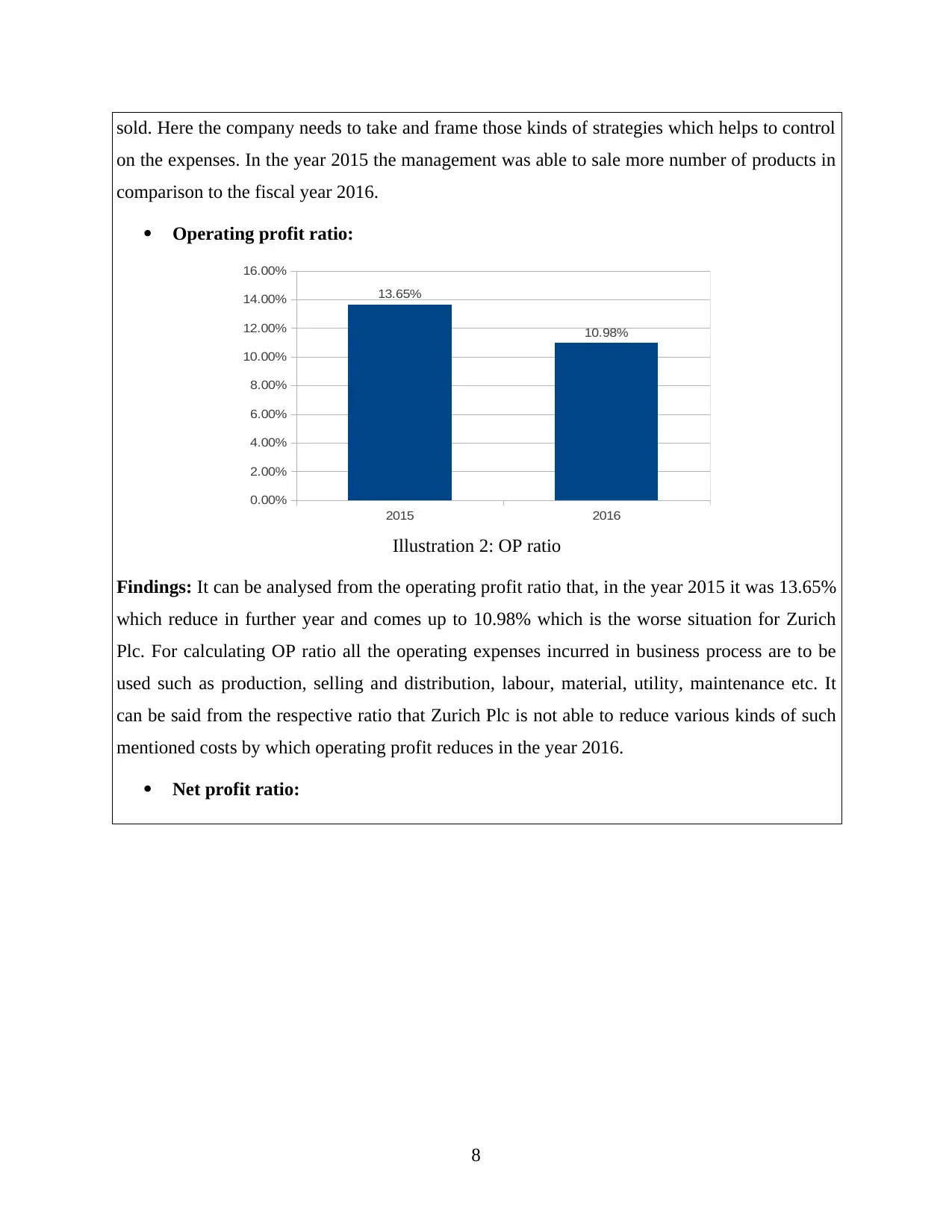

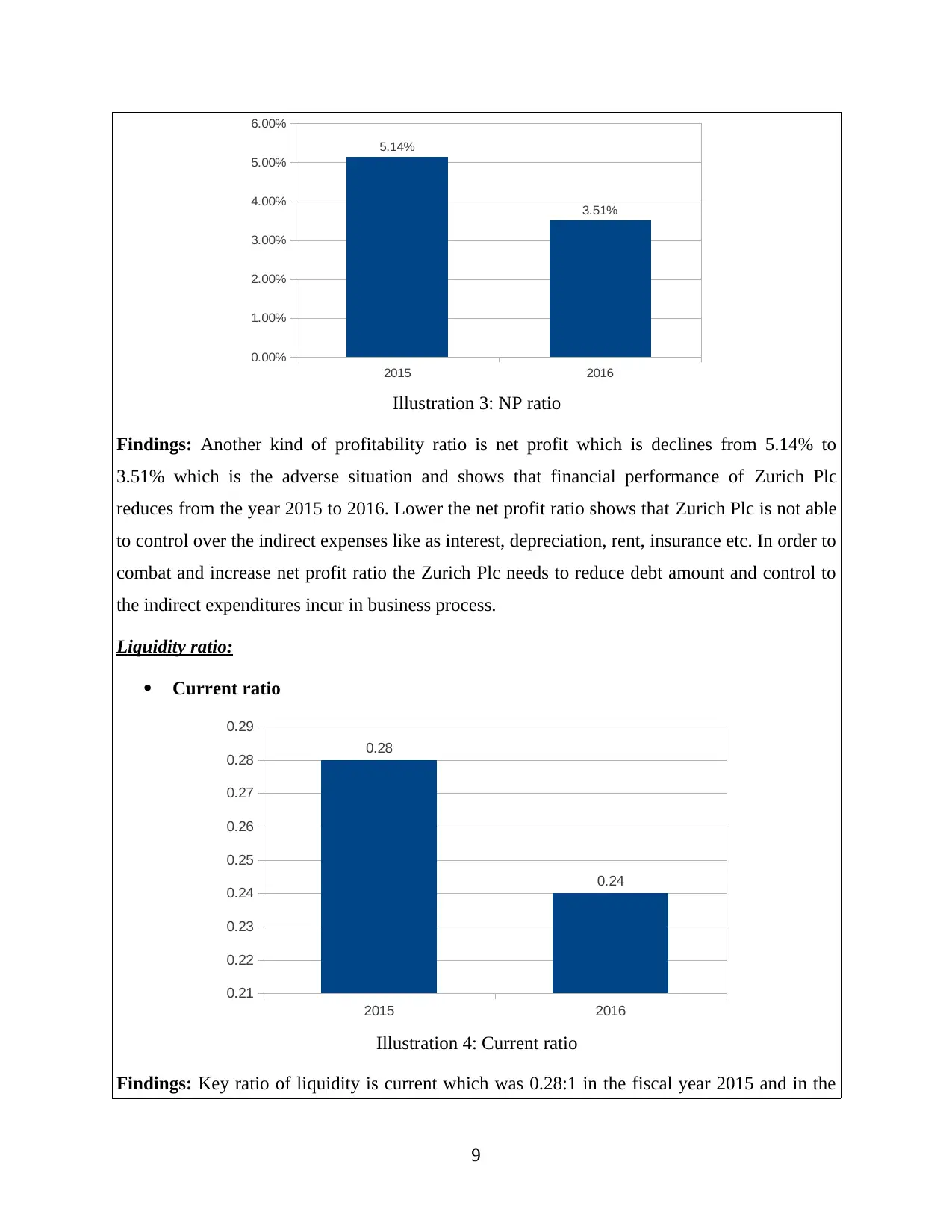

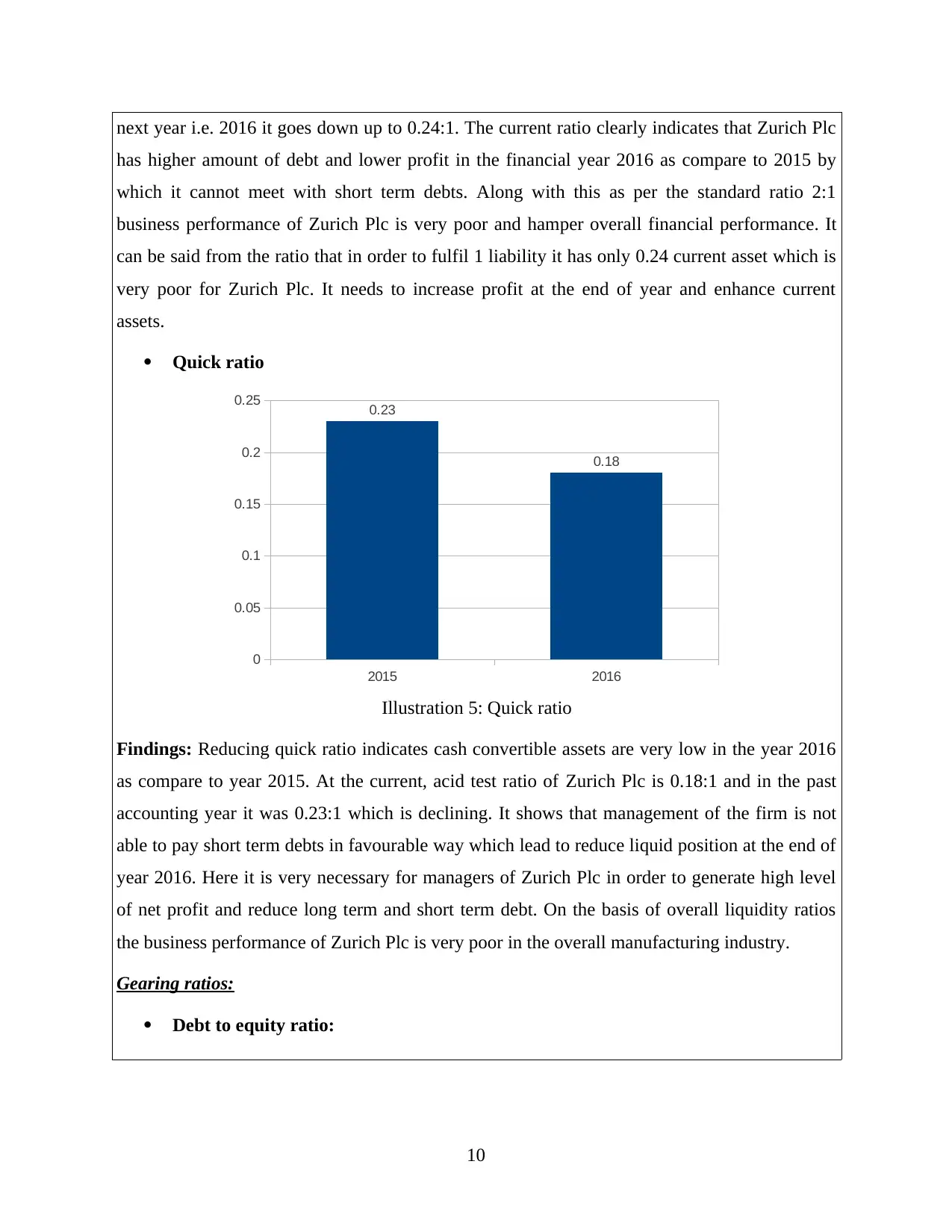

This report provides a comprehensive financial analysis of Zurich Plc, focusing on the evaluation of its performance through various financial ratios. The analysis encompasses profitability ratios (gross profit, operating profit, and net profit), liquidity ratios (current and quick ratios), gearing ratios (debt-to-equity and interest coverage), asset utilization ratios (fixed and total assets turnover), and investor ratios (earnings per share and return on equity). The report compares the financial data of Zurich Plc for the years 2015 and 2016, providing insights into the company's financial health, its ability to manage costs, and its efficiency in utilizing assets. The findings are presented to the board of directors, highlighting trends and offering strategic recommendations to improve financial performance. The report also discusses the limitations of financial ratio analysis.

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.