BBE604: Entrepreneurial Finance Assessment One: Financial Plan

VerifiedAdded on 2022/02/19

|20

|3442

|243

Project

AI Summary

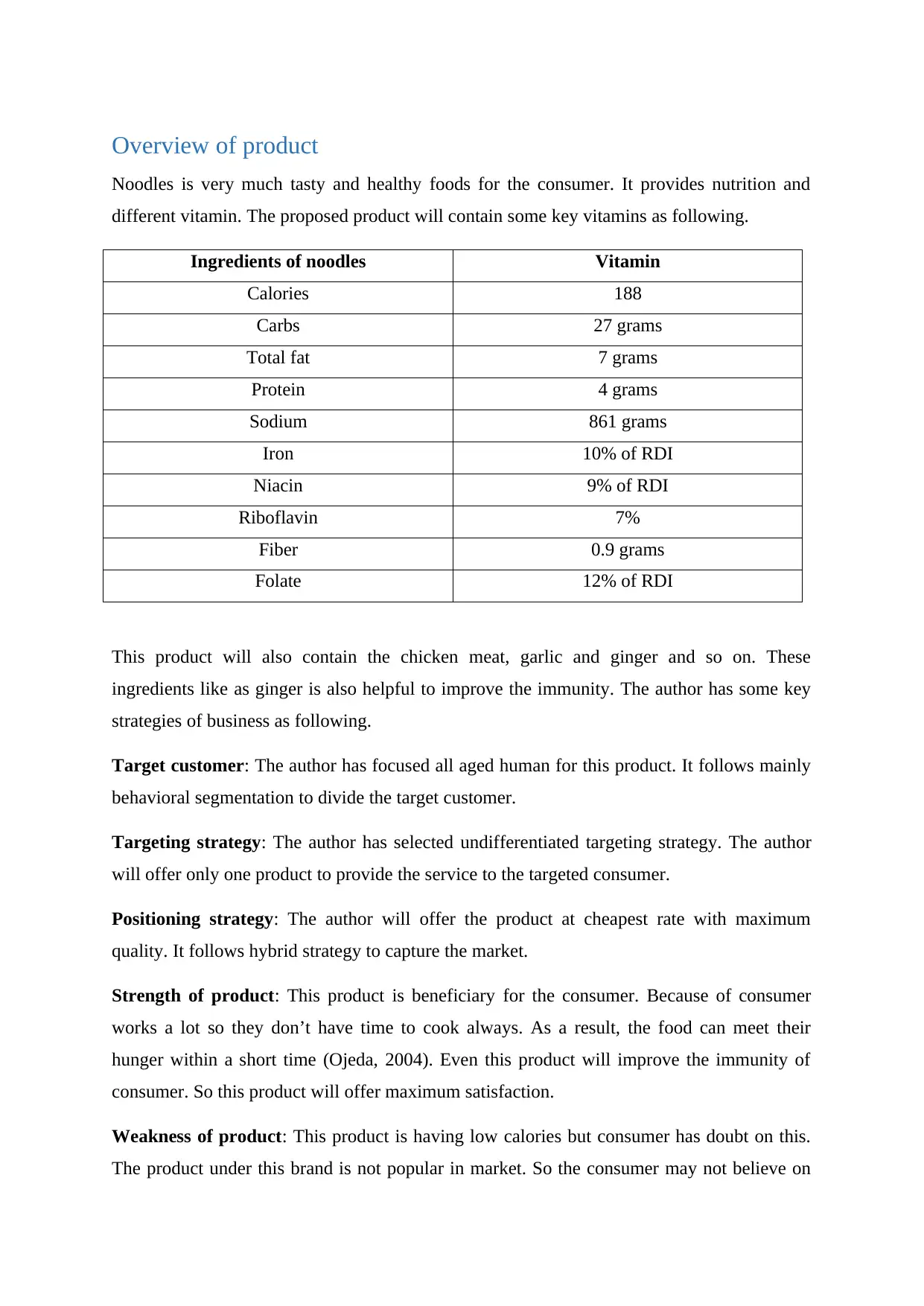

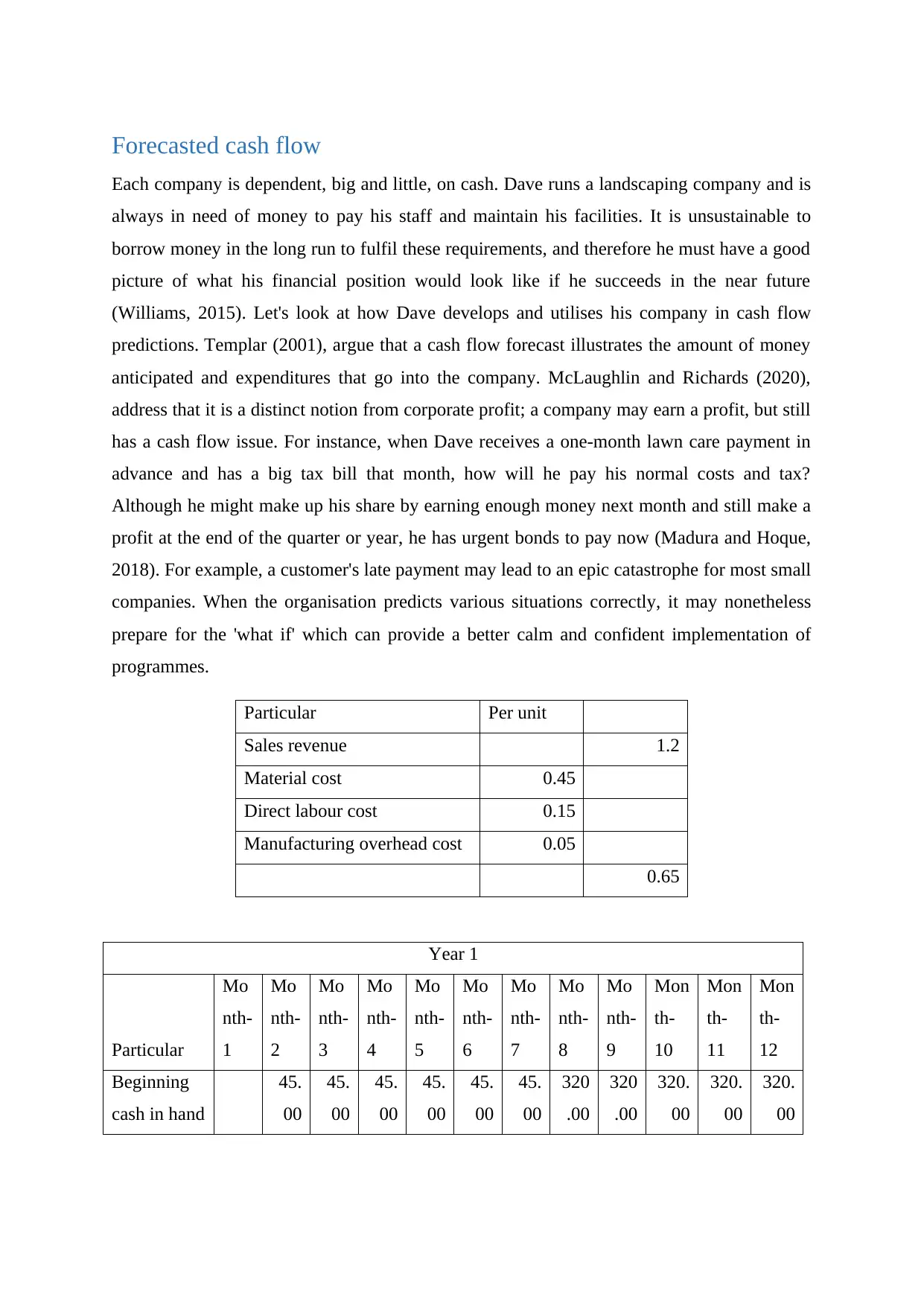

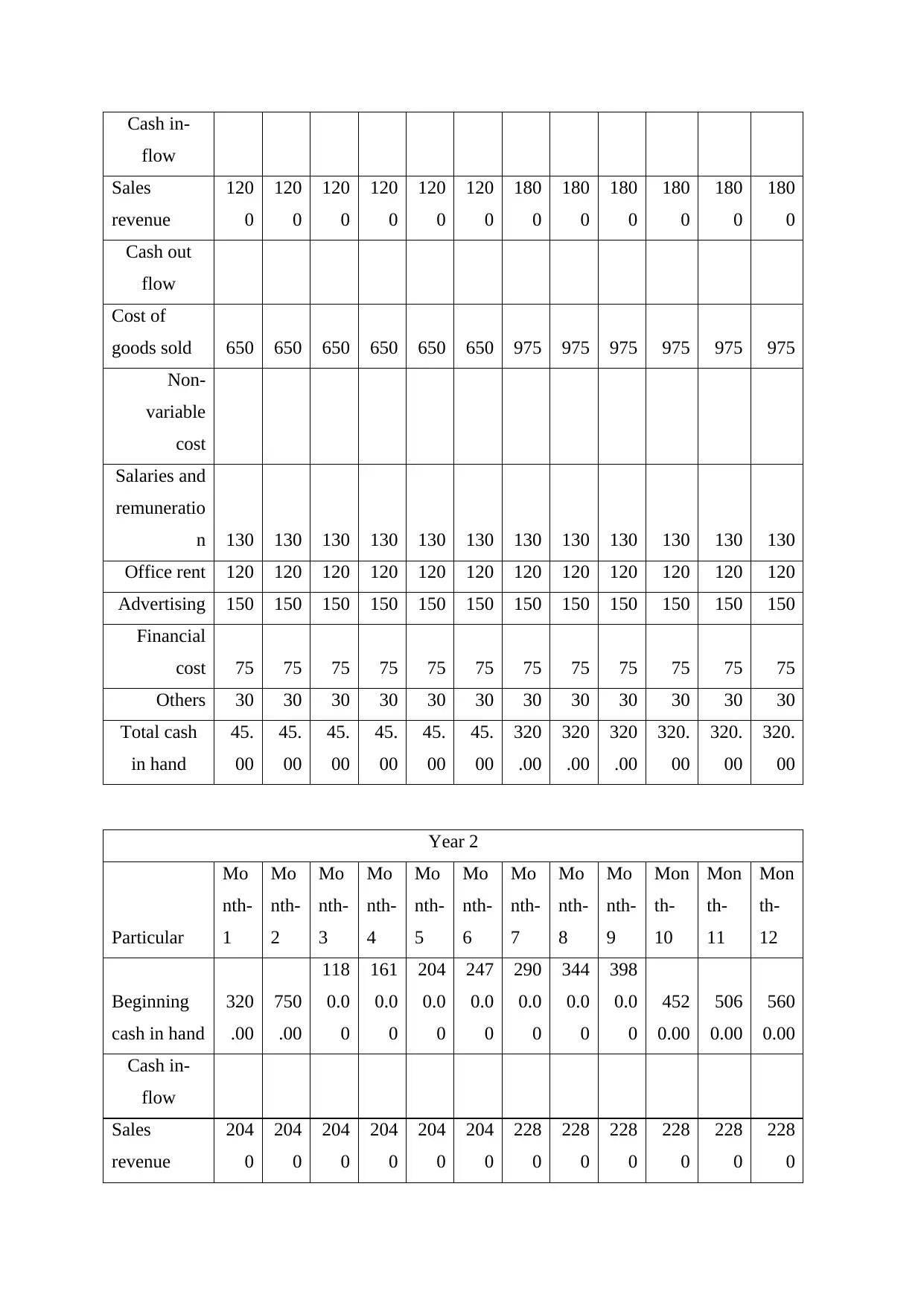

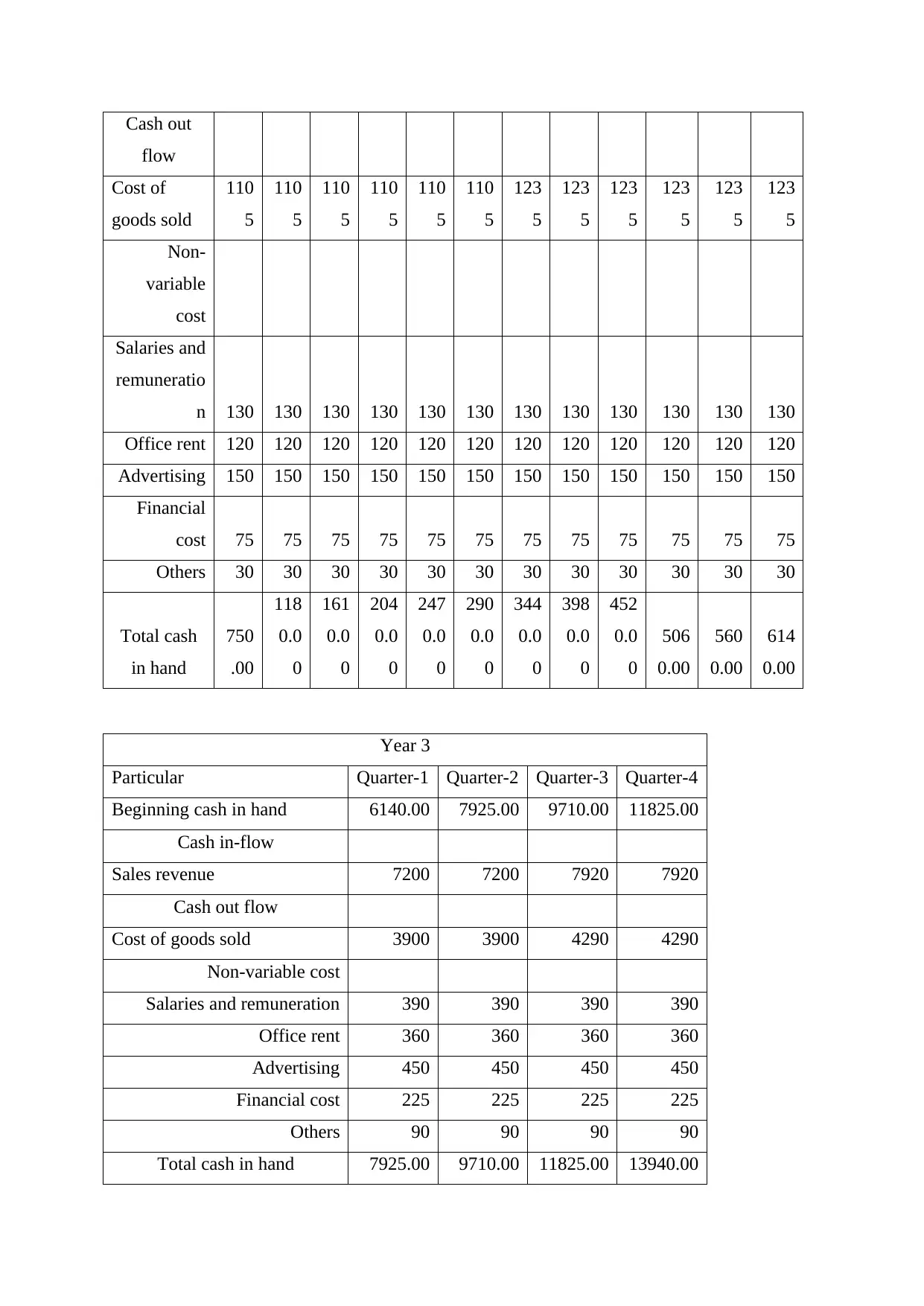

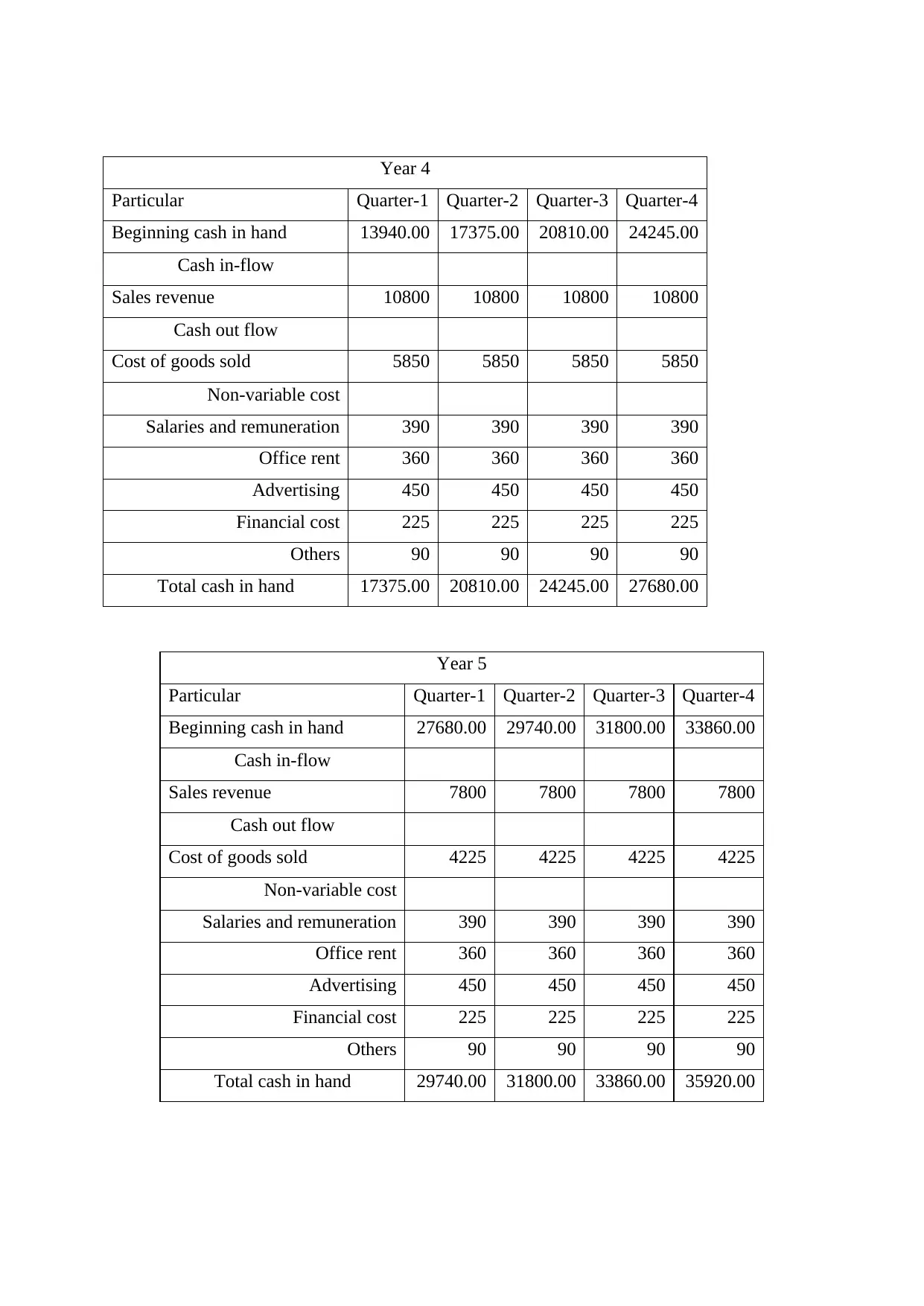

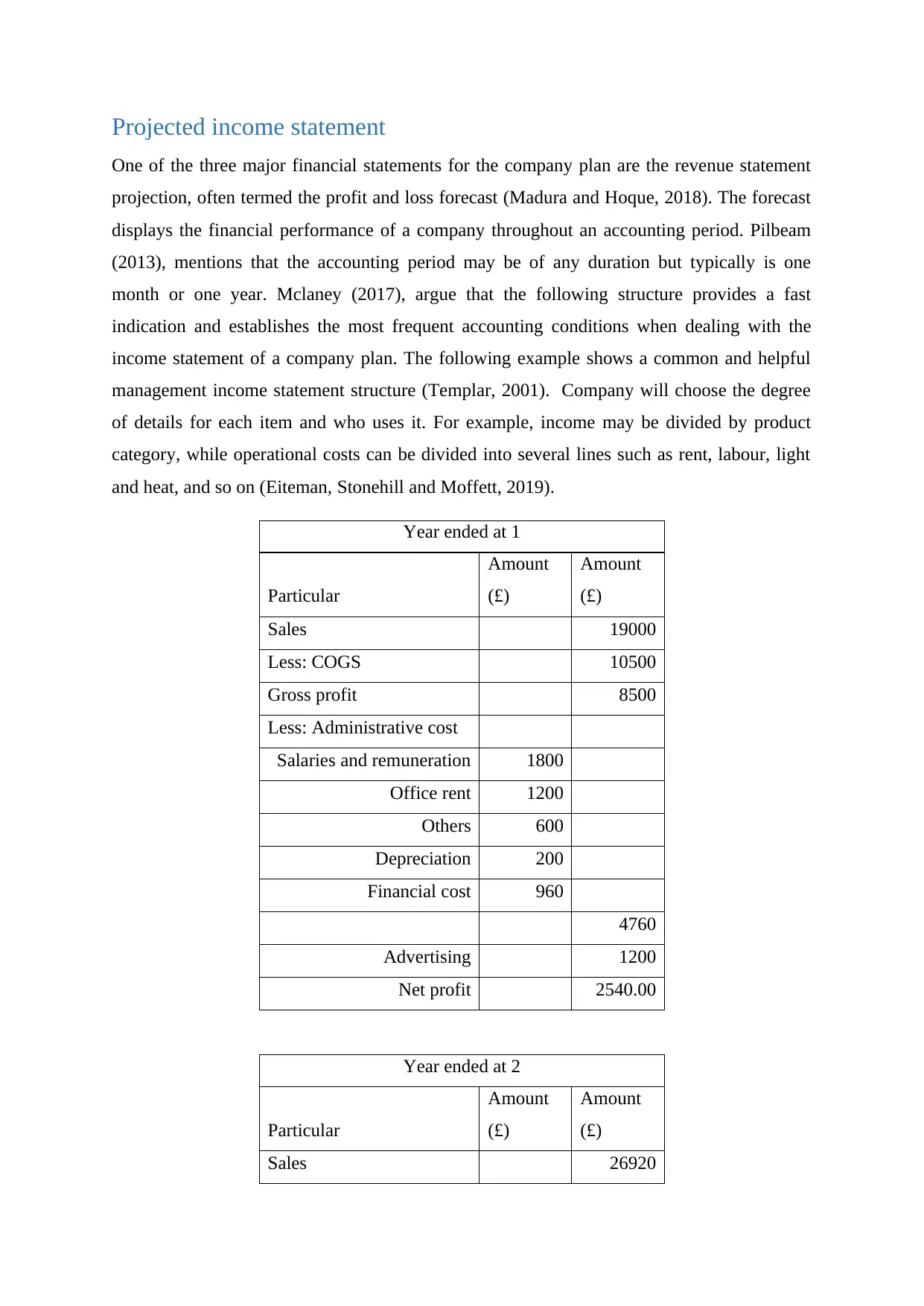

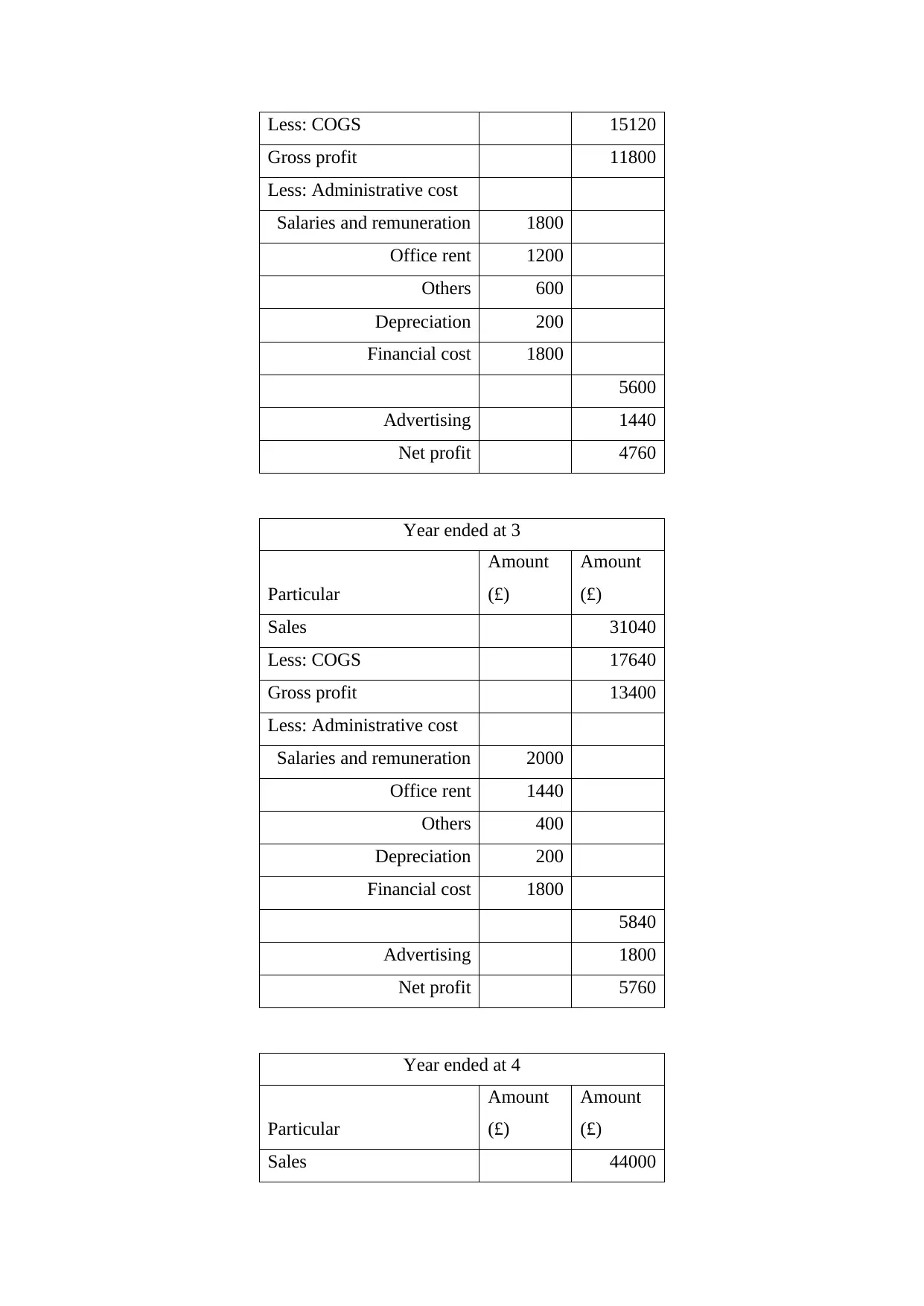

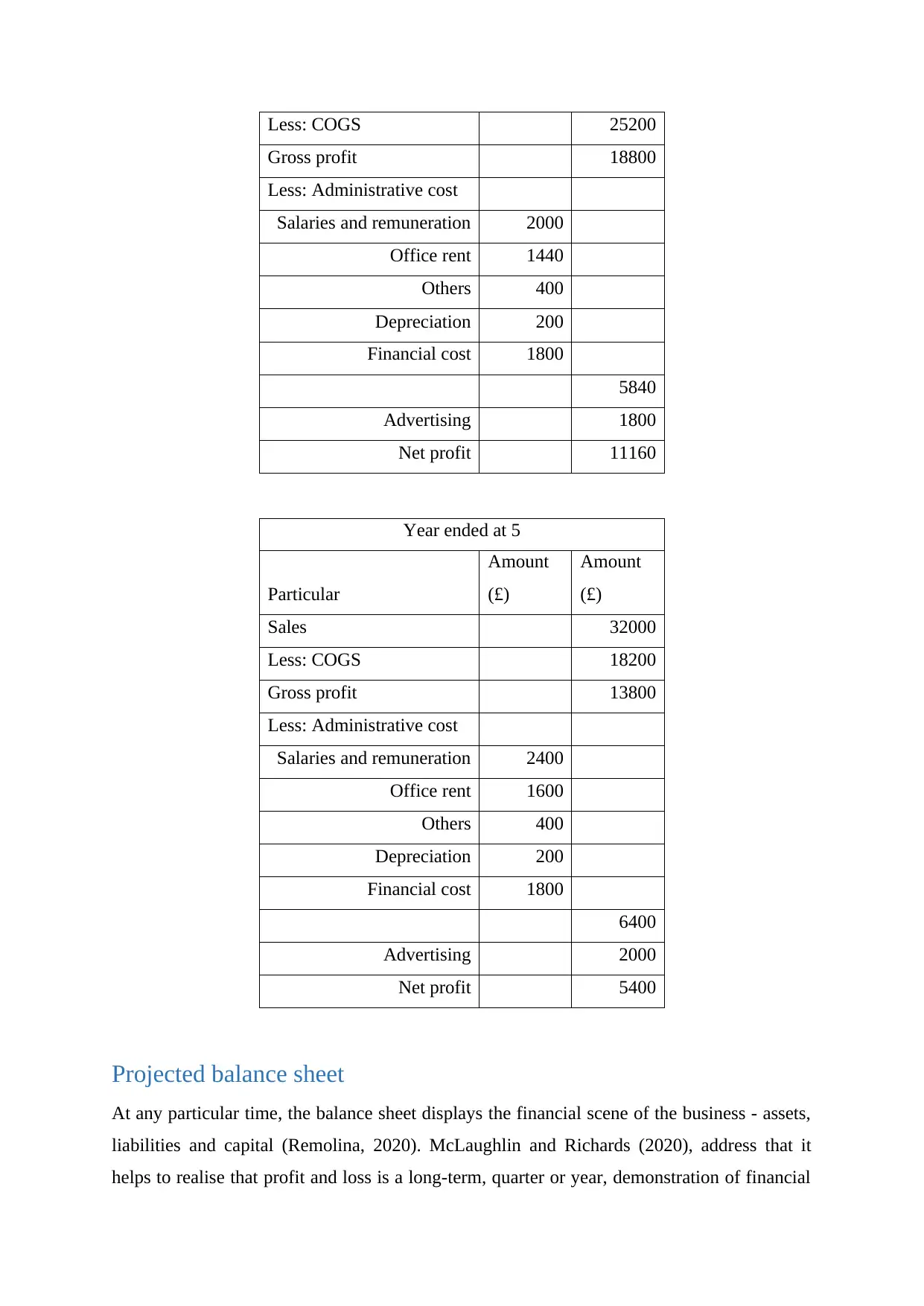

This project presents a comprehensive financial plan for a new food business venture specializing in instant noodles with immunity-boosting ingredients like garlic, ginger, and chicken. The plan includes an overview of the product, its strengths, and weaknesses, along with a detailed analysis of the target market and marketing strategies. The financial projections cover various scenarios, including reasonable, high-performing, and low-performing cases. The core of the project involves forecasted cash flow statements, projected income statements, and balance sheets over a five-year period, providing insights into the financial viability and sustainability of the business. The financial statements provide detailed information on sales revenue, cost of goods sold, operating expenses, and profitability, offering a clear picture of the financial performance and position of the business. The project also addresses the sources of funding for the venture. The student has meticulously analyzed financial data, providing a robust assessment of the business's potential and financial health.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.