Personal Financial Planning Case Study for Raj Brar's Class

VerifiedAdded on 2023/05/29

|13

|3270

|184

Case Study

AI Summary

This case study delves into the personal financial planning of Paul Smith and Olivia Watson, a young couple navigating their financial future. It begins by outlining their family situation, current living arrangements, and future plans, including marriage and children. The study details their expenses, assets (including savings, RRSPs, and personal property), and employment situations, highlighting Paul's conservative financial views shaped by his upbringing and Olivia's more carefree spending habits. The impact of these differing views on their financial management is explored, along with their strategies for handling student loans. A net worth statement is presented, followed by an analysis of their existing and proposed budgets. The study concludes by outlining their financial goals and providing a Gantt chart for visualizing their progress. This document is designed to show students an example of a financial planning case study, and Desklib offers a wide array of similar documents, including solved assignments and past papers, for further learning.

Personal financial planning

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Overview and family situation...............................................................................................................2

Current living situation..........................................................................................................................2

Future plans...........................................................................................................................................3

Expenses................................................................................................................................................3

Assets....................................................................................................................................................3

Employment..........................................................................................................................................4

Financial management...........................................................................................................................5

Impact of financial management............................................................................................................6

Student loan...........................................................................................................................................6

Net worth statement...............................................................................................................................6

Budgets..................................................................................................................................................7

Goals...................................................................................................................................................10

Gantt chart...........................................................................................................................................11

Background and benefits.....................................................................................................................11

References...........................................................................................................................................12

1

Overview and family situation...............................................................................................................2

Current living situation..........................................................................................................................2

Future plans...........................................................................................................................................3

Expenses................................................................................................................................................3

Assets....................................................................................................................................................3

Employment..........................................................................................................................................4

Financial management...........................................................................................................................5

Impact of financial management............................................................................................................6

Student loan...........................................................................................................................................6

Net worth statement...............................................................................................................................6

Budgets..................................................................................................................................................7

Goals...................................................................................................................................................10

Gantt chart...........................................................................................................................................11

Background and benefits.....................................................................................................................11

References...........................................................................................................................................12

1

Overview and family situation

Paul Smith and Olivia Watson met in college and they have been dating for three years.

Paul Smith

Paul Smith is 27 years old and works as a sales executive in an organization. He has also

enrolled himself in a college for completing Management of Business Administration. He

belongs to a middle-class family with two siblings. They live in Montreal. His mother is a

teacher and his father is an engineer in software organizations (Wolf, 2010). The

unpredictable income of his family has forced them to live a cost-conscious lifestyle. He is

always careful to avoid any kind of debts such as a mortgage. Paul Smith has facing many

difficulties in life and enabled his skills and knowledge. Paul Smith is very much concern in

managing its financial aspects. Paul Smith is very conservative with spending.

Olivia Watson

Olivia Watson is 24 years old and completed her Bachelor of Commerce. Olivia grew up in

an upper-middle-class family. Her parents and two siblings live in Toronto. Her father is a

businessman and her mother is an accountant. She has a carefree attitude with spending.

Olivia has maintained an appropriate relationship with her family (Prasanna Chandra., 2011).

Current living situation

Paul and Olivia live together in a rented house. The house consists of two bedrooms, one

kitchen and one bathroom. They also take care of the younger brother of Paul. The

responsibilities of Paul have been increased due to the unpredictable income of his family.

Both of them incur the expenses of his younger brother. They will get engaged in three years

and will get married in five years. It has also planned by them that they would have at least

three children (Melicher, Norton & Town, 2007). They need few years to establish

themselves and to enjoy their life. They have also planned to buy a house in future. Both of

them have a defined benefit pension plan and a registered retirement savings plan. The

defined benefit pension is being provided by the organization as a benefit on the basis of the

salary history and employment length after the retirement. The registered retirement savings

plan is referred to a special investment type designed for assisting Canadians to save money

after retirement.

2

Paul Smith and Olivia Watson met in college and they have been dating for three years.

Paul Smith

Paul Smith is 27 years old and works as a sales executive in an organization. He has also

enrolled himself in a college for completing Management of Business Administration. He

belongs to a middle-class family with two siblings. They live in Montreal. His mother is a

teacher and his father is an engineer in software organizations (Wolf, 2010). The

unpredictable income of his family has forced them to live a cost-conscious lifestyle. He is

always careful to avoid any kind of debts such as a mortgage. Paul Smith has facing many

difficulties in life and enabled his skills and knowledge. Paul Smith is very much concern in

managing its financial aspects. Paul Smith is very conservative with spending.

Olivia Watson

Olivia Watson is 24 years old and completed her Bachelor of Commerce. Olivia grew up in

an upper-middle-class family. Her parents and two siblings live in Toronto. Her father is a

businessman and her mother is an accountant. She has a carefree attitude with spending.

Olivia has maintained an appropriate relationship with her family (Prasanna Chandra., 2011).

Current living situation

Paul and Olivia live together in a rented house. The house consists of two bedrooms, one

kitchen and one bathroom. They also take care of the younger brother of Paul. The

responsibilities of Paul have been increased due to the unpredictable income of his family.

Both of them incur the expenses of his younger brother. They will get engaged in three years

and will get married in five years. It has also planned by them that they would have at least

three children (Melicher, Norton & Town, 2007). They need few years to establish

themselves and to enjoy their life. They have also planned to buy a house in future. Both of

them have a defined benefit pension plan and a registered retirement savings plan. The

defined benefit pension is being provided by the organization as a benefit on the basis of the

salary history and employment length after the retirement. The registered retirement savings

plan is referred to a special investment type designed for assisting Canadians to save money

after retirement.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Future plans

Paul and Olivia have planned to improve the quality of their life. They are living together and

moving towards their future. They have also decided to get married and have children. They

need assistance to carry out their financial planning. The main focus is to decrease expenses

and increase savings (Pandey, 2015). The increase in the cash flows will assist to pay the

expenses, cover debts and enjoy their life in an appropriate manner. They have focused on

their career because the establishment of their career will assist in the increase in the flowing

cash.

Expenses

Paul and Olivia live together and they have to pay money for the expenses incurred for

running their life. The expenses incurred by them are groceries, entertainment, rent, student

loan, clothing, personal, education and credit card payments. The expenditures are associated

with their life. The management of expenses is considered to be very much important for the

couples (Phylaktis, 2014).

Assets

The assets that are being held by the couple are a savings account, TFSA, RRSP, home,

automobile and jewellery. The financial assets are being used for improving the quality of

life. The personal assets of Paul Smith and Olivia Watson are being estimated (Pilbeam,

2013).

Assets Paul Smith

($)

Olivia Watson

($)

Total

Non-registered assets

Savings account 5400 2100 7500

Total non-registered

assets

5400 2100 7500

Registered assets

RRSP 900 0 900

DBPP 500 300 800

Total registered assets 1400 300 1700

3

Paul and Olivia have planned to improve the quality of their life. They are living together and

moving towards their future. They have also decided to get married and have children. They

need assistance to carry out their financial planning. The main focus is to decrease expenses

and increase savings (Pandey, 2015). The increase in the cash flows will assist to pay the

expenses, cover debts and enjoy their life in an appropriate manner. They have focused on

their career because the establishment of their career will assist in the increase in the flowing

cash.

Expenses

Paul and Olivia live together and they have to pay money for the expenses incurred for

running their life. The expenses incurred by them are groceries, entertainment, rent, student

loan, clothing, personal, education and credit card payments. The expenditures are associated

with their life. The management of expenses is considered to be very much important for the

couples (Phylaktis, 2014).

Assets

The assets that are being held by the couple are a savings account, TFSA, RRSP, home,

automobile and jewellery. The financial assets are being used for improving the quality of

life. The personal assets of Paul Smith and Olivia Watson are being estimated (Pilbeam,

2013).

Assets Paul Smith

($)

Olivia Watson

($)

Total

Non-registered assets

Savings account 5400 2100 7500

Total non-registered

assets

5400 2100 7500

Registered assets

RRSP 900 0 900

DBPP 500 300 800

Total registered assets 1400 300 1700

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

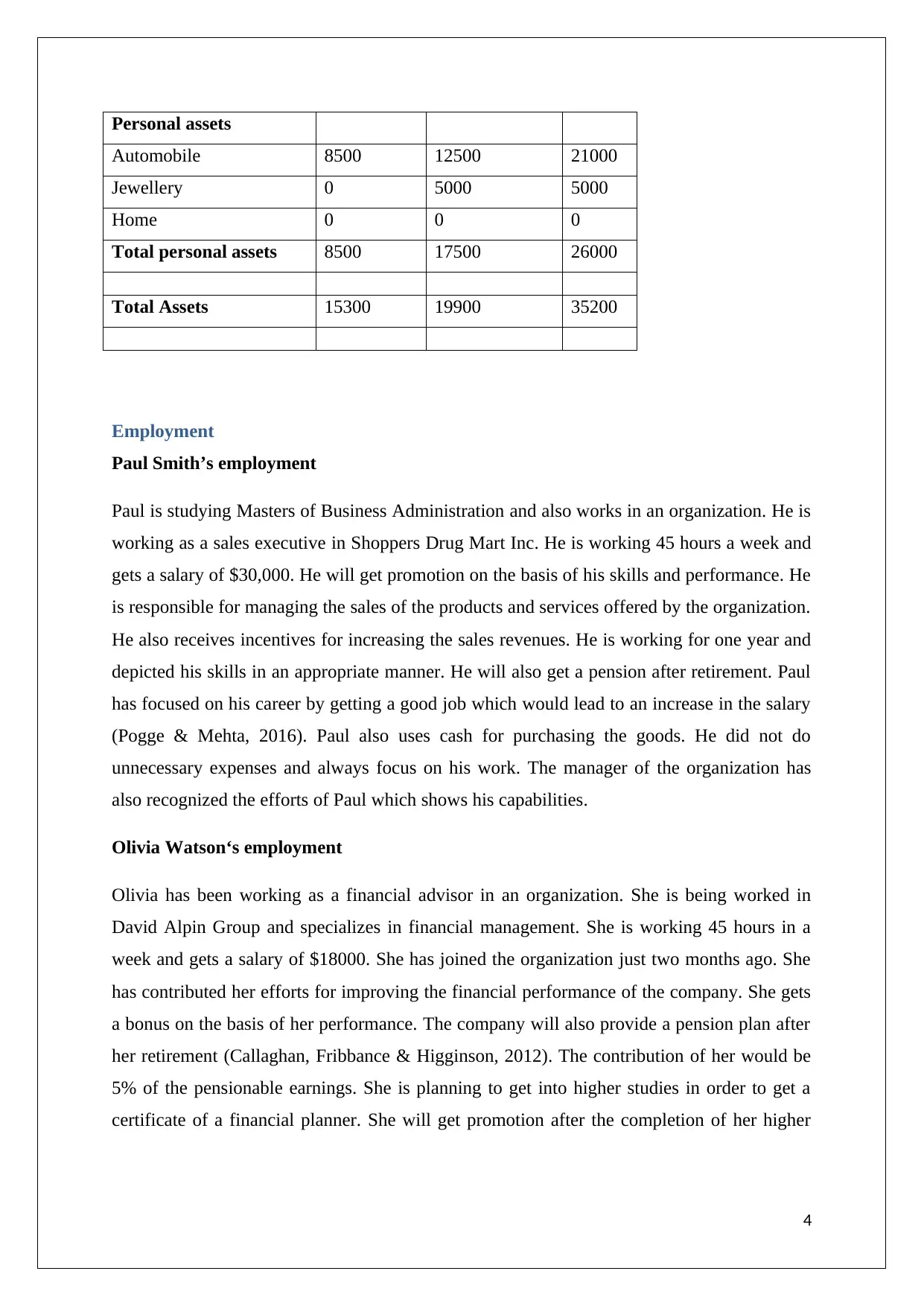

Personal assets

Automobile 8500 12500 21000

Jewellery 0 5000 5000

Home 0 0 0

Total personal assets 8500 17500 26000

Total Assets 15300 19900 35200

Employment

Paul Smith’s employment

Paul is studying Masters of Business Administration and also works in an organization. He is

working as a sales executive in Shoppers Drug Mart Inc. He is working 45 hours a week and

gets a salary of $30,000. He will get promotion on the basis of his skills and performance. He

is responsible for managing the sales of the products and services offered by the organization.

He also receives incentives for increasing the sales revenues. He is working for one year and

depicted his skills in an appropriate manner. He will also get a pension after retirement. Paul

has focused on his career by getting a good job which would lead to an increase in the salary

(Pogge & Mehta, 2016). Paul also uses cash for purchasing the goods. He did not do

unnecessary expenses and always focus on his work. The manager of the organization has

also recognized the efforts of Paul which shows his capabilities.

Olivia Watson‘s employment

Olivia has been working as a financial advisor in an organization. She is being worked in

David Alpin Group and specializes in financial management. She is working 45 hours in a

week and gets a salary of $18000. She has joined the organization just two months ago. She

has contributed her efforts for improving the financial performance of the company. She gets

a bonus on the basis of her performance. The company will also provide a pension plan after

her retirement (Callaghan, Fribbance & Higginson, 2012). The contribution of her would be

5% of the pensionable earnings. She is planning to get into higher studies in order to get a

certificate of a financial planner. She will get promotion after the completion of her higher

4

Automobile 8500 12500 21000

Jewellery 0 5000 5000

Home 0 0 0

Total personal assets 8500 17500 26000

Total Assets 15300 19900 35200

Employment

Paul Smith’s employment

Paul is studying Masters of Business Administration and also works in an organization. He is

working as a sales executive in Shoppers Drug Mart Inc. He is working 45 hours a week and

gets a salary of $30,000. He will get promotion on the basis of his skills and performance. He

is responsible for managing the sales of the products and services offered by the organization.

He also receives incentives for increasing the sales revenues. He is working for one year and

depicted his skills in an appropriate manner. He will also get a pension after retirement. Paul

has focused on his career by getting a good job which would lead to an increase in the salary

(Pogge & Mehta, 2016). Paul also uses cash for purchasing the goods. He did not do

unnecessary expenses and always focus on his work. The manager of the organization has

also recognized the efforts of Paul which shows his capabilities.

Olivia Watson‘s employment

Olivia has been working as a financial advisor in an organization. She is being worked in

David Alpin Group and specializes in financial management. She is working 45 hours in a

week and gets a salary of $18000. She has joined the organization just two months ago. She

has contributed her efforts for improving the financial performance of the company. She gets

a bonus on the basis of her performance. The company will also provide a pension plan after

her retirement (Callaghan, Fribbance & Higginson, 2012). The contribution of her would be

5% of the pensionable earnings. She is planning to get into higher studies in order to get a

certificate of a financial planner. She will get promotion after the completion of her higher

4

education. The hard work and her ambition will assist her to achieve success in her life.

Olivia has been always in a comfortable life but she has managed it in an appropriate manner.

Financial management

Paul Smith’s view on the financial management

Paul Smith has grown up in very tough conditions where his family faced problems in

earning money. From an early age, he learned many things and realized his goals. He is

focusing on saving money for himself and for his younger brother. He has always focused on

the practical side and never thought of living a luxurious lifestyle. It is clear that the attitude

of Paul towards financial management is influenced strongly by the way his family budgeted

(Leimberg, Satinsky, Doyle & Jackson, 2009).

Paul does not spend money on unnecessary things and also save money on paying his student

loan. The student loan is considered to be an appropriate investment for Paul in future and

also very much careful in avoiding debts. He has also not applied for the credit card because

he has recently entered into a job. The debit card is being used by him for carrying out

transactions. He also follows personal policy to make a withdrawal of amount $100 per week

from the bank account for covering the discretionary spending. He spends this money only in

an emergency situation (Holton, 2012).

Olivia Watson’s view on the financial management

Olivia grew up in a comfortable zone where she did not face any financial problems. Her

parents were able to provide all the things that she wanted such as mobile phones, video

games, fashionable clothes. Her parents provided her with a luxurious life where she enjoyed

vacations every week (Gowthorpe, 2005). However, it can also be stated that Olivia has

grown up in a surrounding where she did not understand the real value of money. When she

was with her parents she used to spent her salary earned from part-time jobs in maintaining

her lifestyle.

Olivia uses a credit card for purchasing products from shops. She also pays bills with her

credit card and pays a minimum amount of money each month on her credit card in order to

maintain the flow of cash. When she started her life with Paul, she believed that lifestyle will

be maintained appropriately (Amatucci, 2012).

5

Olivia has been always in a comfortable life but she has managed it in an appropriate manner.

Financial management

Paul Smith’s view on the financial management

Paul Smith has grown up in very tough conditions where his family faced problems in

earning money. From an early age, he learned many things and realized his goals. He is

focusing on saving money for himself and for his younger brother. He has always focused on

the practical side and never thought of living a luxurious lifestyle. It is clear that the attitude

of Paul towards financial management is influenced strongly by the way his family budgeted

(Leimberg, Satinsky, Doyle & Jackson, 2009).

Paul does not spend money on unnecessary things and also save money on paying his student

loan. The student loan is considered to be an appropriate investment for Paul in future and

also very much careful in avoiding debts. He has also not applied for the credit card because

he has recently entered into a job. The debit card is being used by him for carrying out

transactions. He also follows personal policy to make a withdrawal of amount $100 per week

from the bank account for covering the discretionary spending. He spends this money only in

an emergency situation (Holton, 2012).

Olivia Watson’s view on the financial management

Olivia grew up in a comfortable zone where she did not face any financial problems. Her

parents were able to provide all the things that she wanted such as mobile phones, video

games, fashionable clothes. Her parents provided her with a luxurious life where she enjoyed

vacations every week (Gowthorpe, 2005). However, it can also be stated that Olivia has

grown up in a surrounding where she did not understand the real value of money. When she

was with her parents she used to spent her salary earned from part-time jobs in maintaining

her lifestyle.

Olivia uses a credit card for purchasing products from shops. She also pays bills with her

credit card and pays a minimum amount of money each month on her credit card in order to

maintain the flow of cash. When she started her life with Paul, she believed that lifestyle will

be maintained appropriately (Amatucci, 2012).

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Impact of financial management

Paul Smith and Olivia Watson have been in a strong relationship and it can be considered that

they are ideally suited to each other. The attitude is identified to be different which is also

related to financial management. The financial management is considered to be the main

source argument for both the couples (Leonard, 2007). Both of them have the required

qualification which can be used appropriately for achieving success in their life. Paul is very

much concern about his future goals such as marriage, down payment for the purchase of a

home, paying the education loan and even after retirement. However, it is being found that

Paul is not being able to convey this message to Olivia whose main priority is purchasing a

new car and do parties, shopping and even parties. From Olivia's perspective, in many

circumstances, she feels resentful towards Paul because of his insistence to be more

responsible and conservative. She believes that life should be enjoyed without thinking too

much about the future. However, they have agreed to carry out a discussion in which they can

discuss their financial goals. The financial management is considered to be crucial for the

couples (Avi-Yonah, 2007).

Student loan

Paul is going to fund his education through the savings from the salary that he will receive

from the job. However, Paul has to still borrow some amount of month for funding his

course. The student loan needs to be paid by him on time with interest. The increase in salary

will assist him to cover his loan payments. On the other hand, Olivia has also entered into

education and need funds for her education. She has less saving in comparison to Paul

because of the increase in the expenditures (Littell, Tacchino & Cordell, 2004). It is expected

that she would be going to borrow some amount of money from her family.

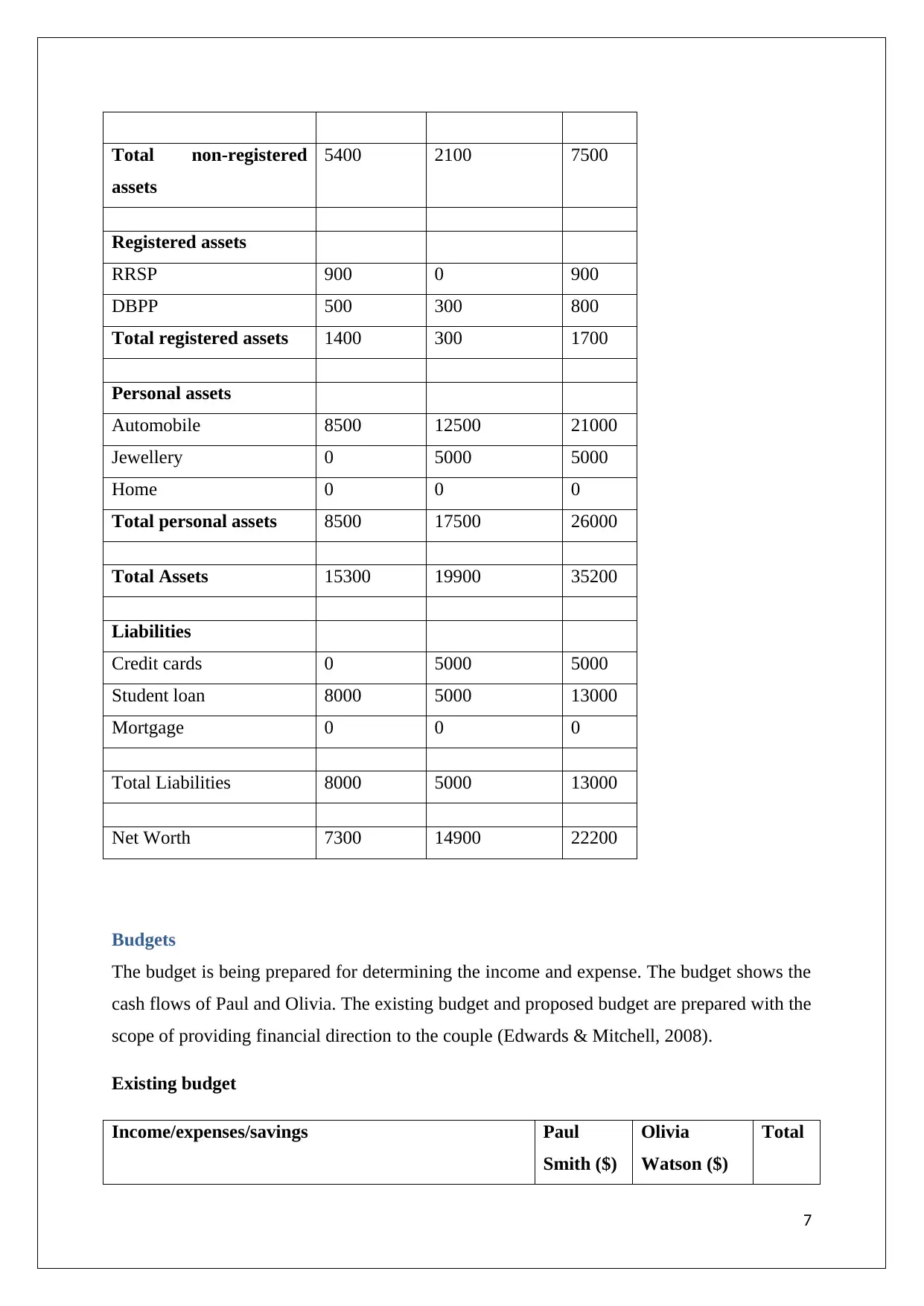

Net worth statement

The net worth statement has been prepared for the couple which shows their assets and

liabilities. The assets and liabilities need to be maintained in an appropriate manner in order

to balance all the financial aspects of life (Avi-Yonah, 2015).

Assets Paul Smith

($)

Olivia Watson

($)

Total

Non-registered assets

Savings account 5400 2100 7500

6

Paul Smith and Olivia Watson have been in a strong relationship and it can be considered that

they are ideally suited to each other. The attitude is identified to be different which is also

related to financial management. The financial management is considered to be the main

source argument for both the couples (Leonard, 2007). Both of them have the required

qualification which can be used appropriately for achieving success in their life. Paul is very

much concern about his future goals such as marriage, down payment for the purchase of a

home, paying the education loan and even after retirement. However, it is being found that

Paul is not being able to convey this message to Olivia whose main priority is purchasing a

new car and do parties, shopping and even parties. From Olivia's perspective, in many

circumstances, she feels resentful towards Paul because of his insistence to be more

responsible and conservative. She believes that life should be enjoyed without thinking too

much about the future. However, they have agreed to carry out a discussion in which they can

discuss their financial goals. The financial management is considered to be crucial for the

couples (Avi-Yonah, 2007).

Student loan

Paul is going to fund his education through the savings from the salary that he will receive

from the job. However, Paul has to still borrow some amount of month for funding his

course. The student loan needs to be paid by him on time with interest. The increase in salary

will assist him to cover his loan payments. On the other hand, Olivia has also entered into

education and need funds for her education. She has less saving in comparison to Paul

because of the increase in the expenditures (Littell, Tacchino & Cordell, 2004). It is expected

that she would be going to borrow some amount of money from her family.

Net worth statement

The net worth statement has been prepared for the couple which shows their assets and

liabilities. The assets and liabilities need to be maintained in an appropriate manner in order

to balance all the financial aspects of life (Avi-Yonah, 2015).

Assets Paul Smith

($)

Olivia Watson

($)

Total

Non-registered assets

Savings account 5400 2100 7500

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total non-registered

assets

5400 2100 7500

Registered assets

RRSP 900 0 900

DBPP 500 300 800

Total registered assets 1400 300 1700

Personal assets

Automobile 8500 12500 21000

Jewellery 0 5000 5000

Home 0 0 0

Total personal assets 8500 17500 26000

Total Assets 15300 19900 35200

Liabilities

Credit cards 0 5000 5000

Student loan 8000 5000 13000

Mortgage 0 0 0

Total Liabilities 8000 5000 13000

Net Worth 7300 14900 22200

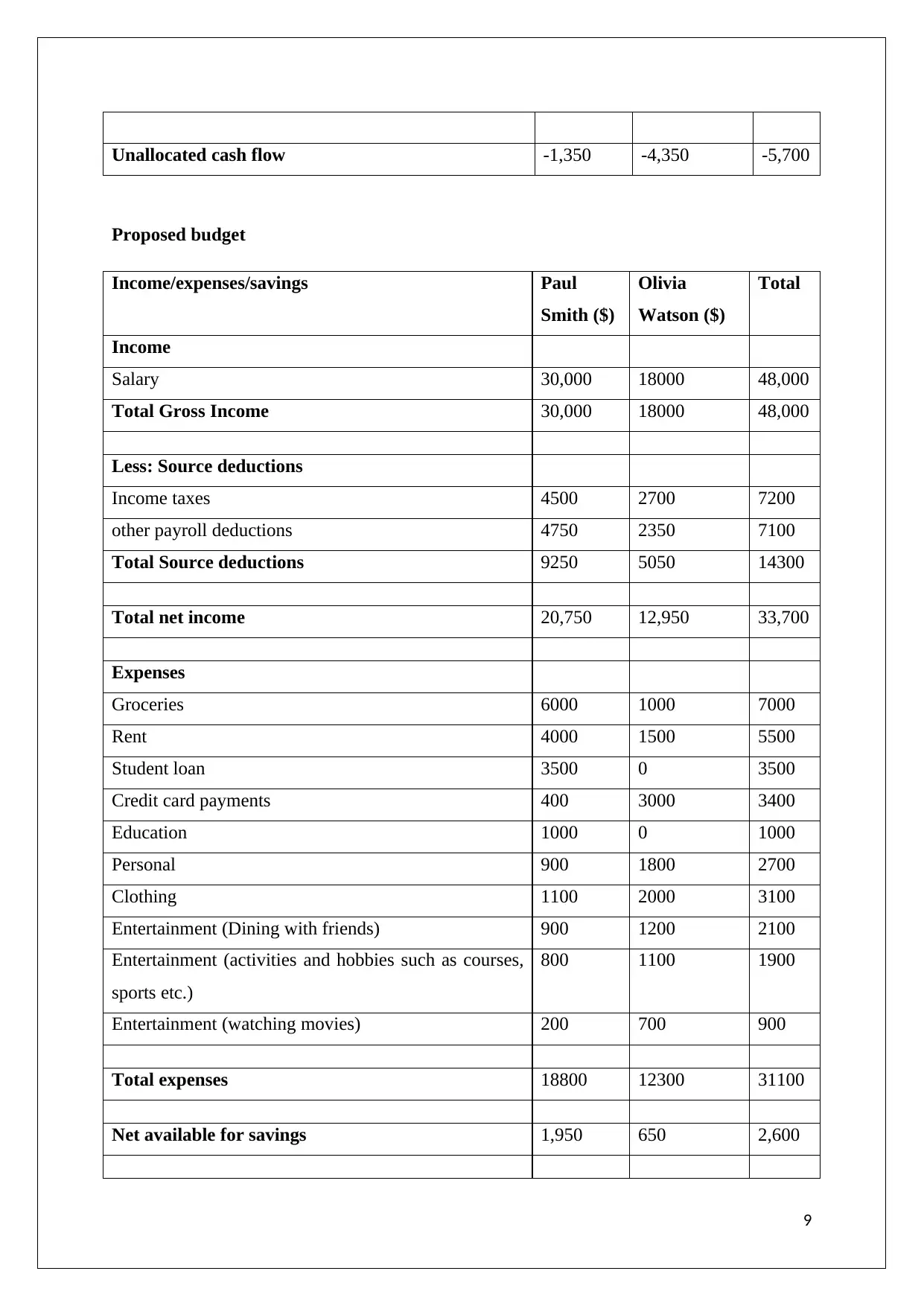

Budgets

The budget is being prepared for determining the income and expense. The budget shows the

cash flows of Paul and Olivia. The existing budget and proposed budget are prepared with the

scope of providing financial direction to the couple (Edwards & Mitchell, 2008).

Existing budget

Income/expenses/savings Paul

Smith ($)

Olivia

Watson ($)

Total

7

assets

5400 2100 7500

Registered assets

RRSP 900 0 900

DBPP 500 300 800

Total registered assets 1400 300 1700

Personal assets

Automobile 8500 12500 21000

Jewellery 0 5000 5000

Home 0 0 0

Total personal assets 8500 17500 26000

Total Assets 15300 19900 35200

Liabilities

Credit cards 0 5000 5000

Student loan 8000 5000 13000

Mortgage 0 0 0

Total Liabilities 8000 5000 13000

Net Worth 7300 14900 22200

Budgets

The budget is being prepared for determining the income and expense. The budget shows the

cash flows of Paul and Olivia. The existing budget and proposed budget are prepared with the

scope of providing financial direction to the couple (Edwards & Mitchell, 2008).

Existing budget

Income/expenses/savings Paul

Smith ($)

Olivia

Watson ($)

Total

7

Income

Salary 30,000 18000 48,00

0

Total Gross Income 30,000 18000 48,00

0

Less: Source deductions

Income taxes 4500 2700 7200

other payroll deductions 4750 2350 7100

Total Source deductions 9250 5050 14300

Total net income 20,750 12,950 33,70

0

Expenses

Groceries 6000 1000 7000

Rent 4000 1500 5500

Student loan 3500 0 3500

Credit card payments 400 4000 4400

Education 1000 0 1000

Personal 1500 3500 5000

Clothing 2000 3000 5000

Entertainment (Dining with friends) 1100 1500 2600

Entertainment (activities and hobbies such as courses,

sports etc.)

900 1500 2400

Entertainment (watching movies) 300 1000 1300

Total expenses 20700 17000 37700

Net available for savings 50 -4,050 -4,000

Savings

RRSP contribution 900 0 900

DBPP contribution 500 300 800

Total savings 1400 300 1700

8

Salary 30,000 18000 48,00

0

Total Gross Income 30,000 18000 48,00

0

Less: Source deductions

Income taxes 4500 2700 7200

other payroll deductions 4750 2350 7100

Total Source deductions 9250 5050 14300

Total net income 20,750 12,950 33,70

0

Expenses

Groceries 6000 1000 7000

Rent 4000 1500 5500

Student loan 3500 0 3500

Credit card payments 400 4000 4400

Education 1000 0 1000

Personal 1500 3500 5000

Clothing 2000 3000 5000

Entertainment (Dining with friends) 1100 1500 2600

Entertainment (activities and hobbies such as courses,

sports etc.)

900 1500 2400

Entertainment (watching movies) 300 1000 1300

Total expenses 20700 17000 37700

Net available for savings 50 -4,050 -4,000

Savings

RRSP contribution 900 0 900

DBPP contribution 500 300 800

Total savings 1400 300 1700

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Unallocated cash flow -1,350 -4,350 -5,700

Proposed budget

Income/expenses/savings Paul

Smith ($)

Olivia

Watson ($)

Total

Income

Salary 30,000 18000 48,000

Total Gross Income 30,000 18000 48,000

Less: Source deductions

Income taxes 4500 2700 7200

other payroll deductions 4750 2350 7100

Total Source deductions 9250 5050 14300

Total net income 20,750 12,950 33,700

Expenses

Groceries 6000 1000 7000

Rent 4000 1500 5500

Student loan 3500 0 3500

Credit card payments 400 3000 3400

Education 1000 0 1000

Personal 900 1800 2700

Clothing 1100 2000 3100

Entertainment (Dining with friends) 900 1200 2100

Entertainment (activities and hobbies such as courses,

sports etc.)

800 1100 1900

Entertainment (watching movies) 200 700 900

Total expenses 18800 12300 31100

Net available for savings 1,950 650 2,600

9

Proposed budget

Income/expenses/savings Paul

Smith ($)

Olivia

Watson ($)

Total

Income

Salary 30,000 18000 48,000

Total Gross Income 30,000 18000 48,000

Less: Source deductions

Income taxes 4500 2700 7200

other payroll deductions 4750 2350 7100

Total Source deductions 9250 5050 14300

Total net income 20,750 12,950 33,700

Expenses

Groceries 6000 1000 7000

Rent 4000 1500 5500

Student loan 3500 0 3500

Credit card payments 400 3000 3400

Education 1000 0 1000

Personal 900 1800 2700

Clothing 1100 2000 3100

Entertainment (Dining with friends) 900 1200 2100

Entertainment (activities and hobbies such as courses,

sports etc.)

800 1100 1900

Entertainment (watching movies) 200 700 900

Total expenses 18800 12300 31100

Net available for savings 1,950 650 2,600

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

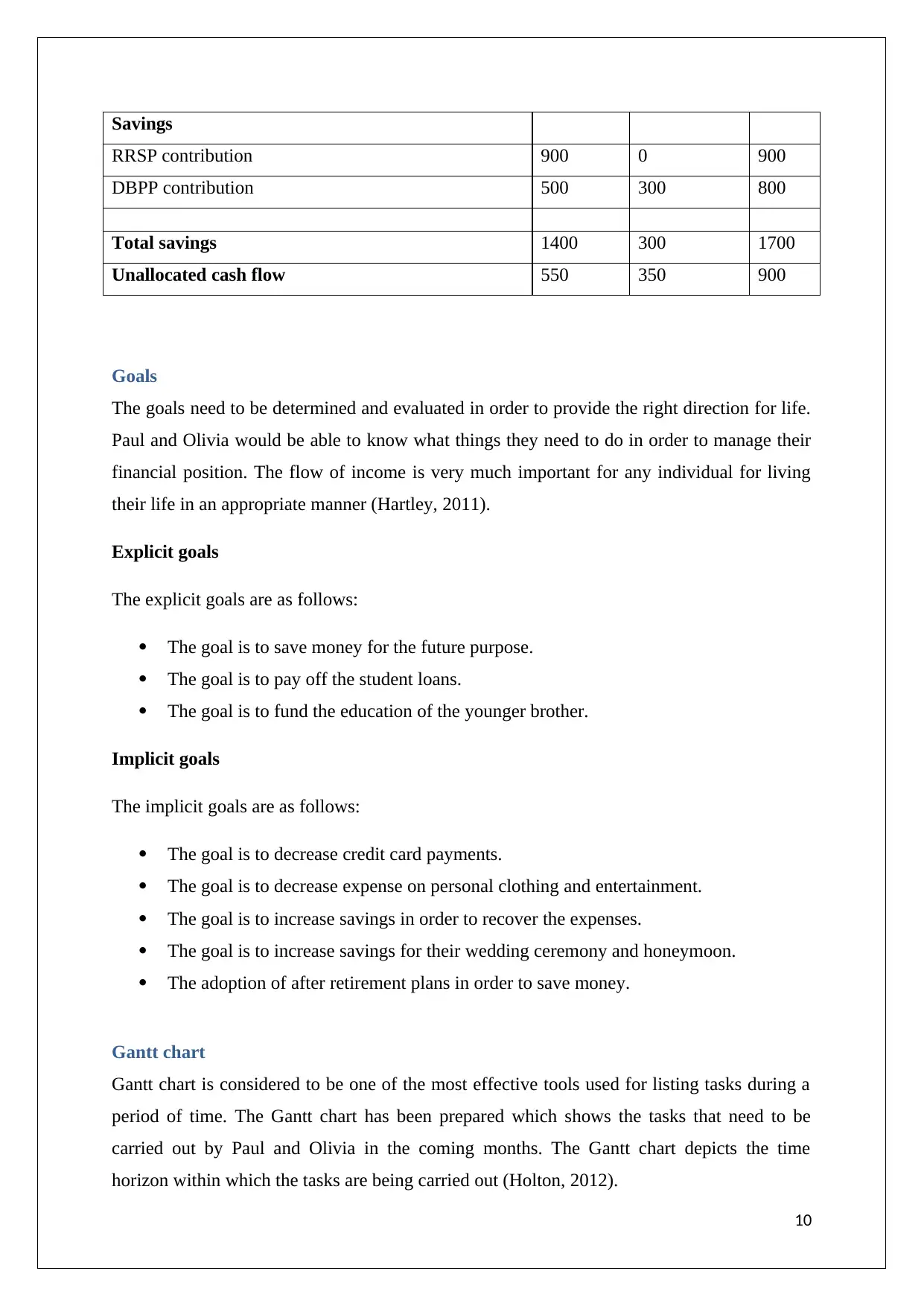

Savings

RRSP contribution 900 0 900

DBPP contribution 500 300 800

Total savings 1400 300 1700

Unallocated cash flow 550 350 900

Goals

The goals need to be determined and evaluated in order to provide the right direction for life.

Paul and Olivia would be able to know what things they need to do in order to manage their

financial position. The flow of income is very much important for any individual for living

their life in an appropriate manner (Hartley, 2011).

Explicit goals

The explicit goals are as follows:

The goal is to save money for the future purpose.

The goal is to pay off the student loans.

The goal is to fund the education of the younger brother.

Implicit goals

The implicit goals are as follows:

The goal is to decrease credit card payments.

The goal is to decrease expense on personal clothing and entertainment.

The goal is to increase savings in order to recover the expenses.

The goal is to increase savings for their wedding ceremony and honeymoon.

The adoption of after retirement plans in order to save money.

Gantt chart

Gantt chart is considered to be one of the most effective tools used for listing tasks during a

period of time. The Gantt chart has been prepared which shows the tasks that need to be

carried out by Paul and Olivia in the coming months. The Gantt chart depicts the time

horizon within which the tasks are being carried out (Holton, 2012).

10

RRSP contribution 900 0 900

DBPP contribution 500 300 800

Total savings 1400 300 1700

Unallocated cash flow 550 350 900

Goals

The goals need to be determined and evaluated in order to provide the right direction for life.

Paul and Olivia would be able to know what things they need to do in order to manage their

financial position. The flow of income is very much important for any individual for living

their life in an appropriate manner (Hartley, 2011).

Explicit goals

The explicit goals are as follows:

The goal is to save money for the future purpose.

The goal is to pay off the student loans.

The goal is to fund the education of the younger brother.

Implicit goals

The implicit goals are as follows:

The goal is to decrease credit card payments.

The goal is to decrease expense on personal clothing and entertainment.

The goal is to increase savings in order to recover the expenses.

The goal is to increase savings for their wedding ceremony and honeymoon.

The adoption of after retirement plans in order to save money.

Gantt chart

Gantt chart is considered to be one of the most effective tools used for listing tasks during a

period of time. The Gantt chart has been prepared which shows the tasks that need to be

carried out by Paul and Olivia in the coming months. The Gantt chart depicts the time

horizon within which the tasks are being carried out (Holton, 2012).

10

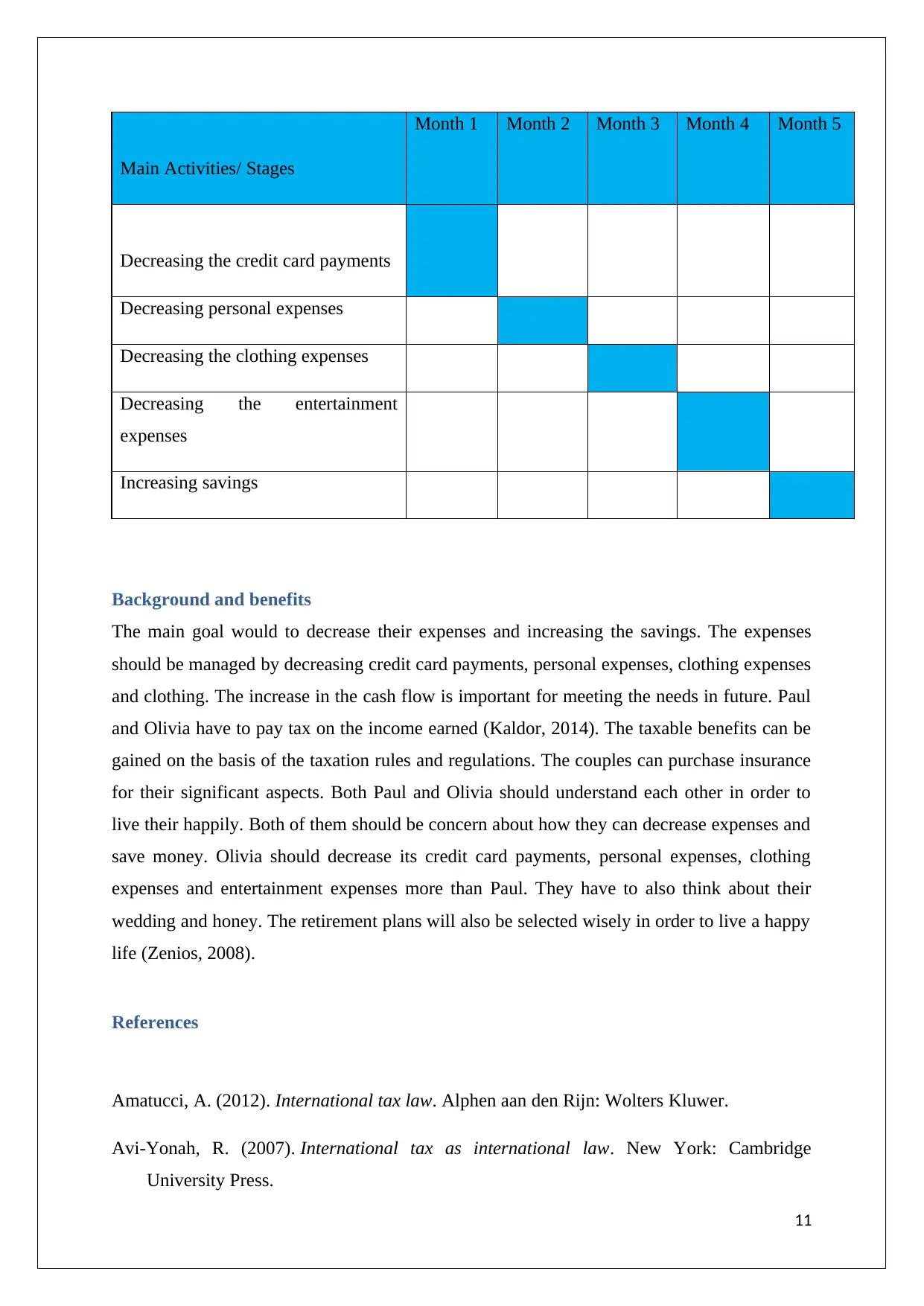

Main Activities/ Stages

Month 1 Month 2 Month 3 Month 4 Month 5

Decreasing the credit card payments

Decreasing personal expenses

Decreasing the clothing expenses

Decreasing the entertainment

expenses

Increasing savings

Background and benefits

The main goal would to decrease their expenses and increasing the savings. The expenses

should be managed by decreasing credit card payments, personal expenses, clothing expenses

and clothing. The increase in the cash flow is important for meeting the needs in future. Paul

and Olivia have to pay tax on the income earned (Kaldor, 2014). The taxable benefits can be

gained on the basis of the taxation rules and regulations. The couples can purchase insurance

for their significant aspects. Both Paul and Olivia should understand each other in order to

live their happily. Both of them should be concern about how they can decrease expenses and

save money. Olivia should decrease its credit card payments, personal expenses, clothing

expenses and entertainment expenses more than Paul. They have to also think about their

wedding and honey. The retirement plans will also be selected wisely in order to live a happy

life (Zenios, 2008).

References

Amatucci, A. (2012). International tax law. Alphen aan den Rijn: Wolters Kluwer.

Avi-Yonah, R. (2007). International tax as international law. New York: Cambridge

University Press.

11

Month 1 Month 2 Month 3 Month 4 Month 5

Decreasing the credit card payments

Decreasing personal expenses

Decreasing the clothing expenses

Decreasing the entertainment

expenses

Increasing savings

Background and benefits

The main goal would to decrease their expenses and increasing the savings. The expenses

should be managed by decreasing credit card payments, personal expenses, clothing expenses

and clothing. The increase in the cash flow is important for meeting the needs in future. Paul

and Olivia have to pay tax on the income earned (Kaldor, 2014). The taxable benefits can be

gained on the basis of the taxation rules and regulations. The couples can purchase insurance

for their significant aspects. Both Paul and Olivia should understand each other in order to

live their happily. Both of them should be concern about how they can decrease expenses and

save money. Olivia should decrease its credit card payments, personal expenses, clothing

expenses and entertainment expenses more than Paul. They have to also think about their

wedding and honey. The retirement plans will also be selected wisely in order to live a happy

life (Zenios, 2008).

References

Amatucci, A. (2012). International tax law. Alphen aan den Rijn: Wolters Kluwer.

Avi-Yonah, R. (2007). International tax as international law. New York: Cambridge

University Press.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.