Newcastle University AF5007: Personal Finance Wealth Planning Report

VerifiedAdded on 2022/09/23

|14

|3246

|22

Report

AI Summary

This report presents a comprehensive financial plan for Richard and Stephanie Dando, addressing their objectives and current financial situation. It analyzes their assets, liabilities, income, and expenditure, including pensions, investments, and potential inheritance. The report identifies key issues such as the absence of a will, lack of communication regarding inheritance, and limited understanding of tax implications like capital gains tax. Recommendations include drafting a will, clarifying inheritance plans, and exploring investment strategies. The report also covers topics such as life assurance, the 2015 pension freedom, and retirement planning, providing an overview of key recommendations for the Dando family to achieve their financial goals and secure their future. The report also includes a detailed analysis of their income and expenditure, highlighting their current financial habits and the need for savings and investment strategies. Furthermore, the report provides insights into the couples' retirement plans and potential tax implications, offering recommendations to optimize their financial position. The report also addresses the importance of estate planning and the potential impact of inheritance on their financial well-being.

{Cover Page Here}

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

A) Discussion of the couple’s objectives with reference to timescale..............................................3

B) Logical flow and structure of content.................................................................................................4

B) Evidence of research to form recommendations.........................................................................8

D) Case study relevance and use of up to date material.........................................................................9

E) coverage of issues in the case study at the appropriate level of depth to include an overview of

key recommendations to be expanded on in this report.......................................................................10

References............................................................................................................................................14

A) Discussion of the couple’s objectives with reference to timescale..............................................3

B) Logical flow and structure of content.................................................................................................4

B) Evidence of research to form recommendations.........................................................................8

D) Case study relevance and use of up to date material.........................................................................9

E) coverage of issues in the case study at the appropriate level of depth to include an overview of

key recommendations to be expanded on in this report.......................................................................10

References............................................................................................................................................14

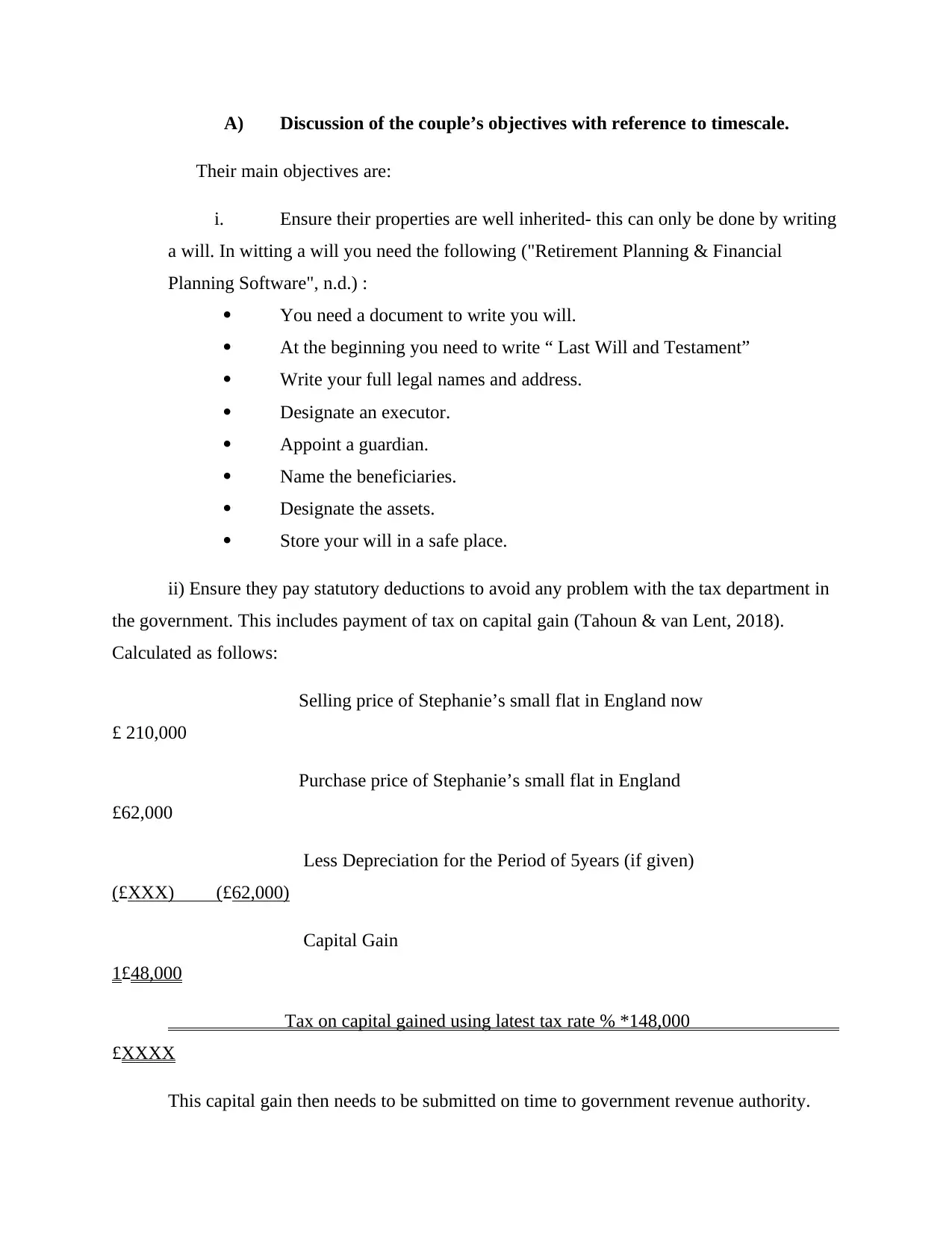

A) Discussion of the couple’s objectives with reference to timescale.

Their main objectives are:

i. Ensure their properties are well inherited- this can only be done by writing

a will. In witting a will you need the following ("Retirement Planning & Financial

Planning Software", n.d.) :

You need a document to write you will.

At the beginning you need to write “ Last Will and Testament”

Write your full legal names and address.

Designate an executor.

Appoint a guardian.

Name the beneficiaries.

Designate the assets.

Store your will in a safe place.

ii) Ensure they pay statutory deductions to avoid any problem with the tax department in

the government. This includes payment of tax on capital gain (Tahoun & van Lent, 2018).

Calculated as follows:

Selling price of Stephanie’s small flat in England now

£ 210,000

Purchase price of Stephanie’s small flat in England

£62,000

Less Depreciation for the Period of 5years (if given)

(£XXX) (£62,000)

Capital Gain

1£48,000

Tax on capital gained using latest tax rate % *148,000

£XXXX

This capital gain then needs to be submitted on time to government revenue authority.

Their main objectives are:

i. Ensure their properties are well inherited- this can only be done by writing

a will. In witting a will you need the following ("Retirement Planning & Financial

Planning Software", n.d.) :

You need a document to write you will.

At the beginning you need to write “ Last Will and Testament”

Write your full legal names and address.

Designate an executor.

Appoint a guardian.

Name the beneficiaries.

Designate the assets.

Store your will in a safe place.

ii) Ensure they pay statutory deductions to avoid any problem with the tax department in

the government. This includes payment of tax on capital gain (Tahoun & van Lent, 2018).

Calculated as follows:

Selling price of Stephanie’s small flat in England now

£ 210,000

Purchase price of Stephanie’s small flat in England

£62,000

Less Depreciation for the Period of 5years (if given)

(£XXX) (£62,000)

Capital Gain

1£48,000

Tax on capital gained using latest tax rate % *148,000

£XXXX

This capital gain then needs to be submitted on time to government revenue authority.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

iii) Ensure they have a well retirement plan. By doing this they have a pension scheme.

In UK, pension is mandatory for working people. Currently men can claim their state

pension from 65 years while women can claim their pension at the age of 62years and

6months.Both will then increase gradually to 66 by 2020 and 67 between 2026 and 2028. Each

year of NICs gives entitlement to 1/30the of the full basic state pension. State Pension cannot be

taken up before the State Pension age, but may be deferred in return for higher State Pension of

10.4% per year of deferral or a one-off lump sum payment with interest annually at 2% above the

bank of England base rate (Chlebikova, Misankova & Kramarova, 2015).

iv) Ensure they have a life assurance scheme. This is to ensure that you family gets what

they miss when you are gone (dead). They need to get peace of mind by receiving quick and easy

compensation each month to sort out what they need in your absence (Chlebikova, Misankova &

Kramarova, 2015). They need to get a good life assurance scheme which will ensure that the

family you leave behind is looked after well. The right cover will cover your needs whether you

want life insurance, mortgage life insurance or critical illness cover.

v) Ensure that they understand well on 2015 pension freedom scheme. This was

introduced in April 2015. Under this reform, people aged 55 or over were given far greater

freedom over how to access their contribution pension posts. This had a right to give people

choice of what to do with their own savings. They have a right to access cash, securities and

investment returns (Chlebikova, Misankova & Kramarova, 2015).

B) Logical flow and structure of content.

This is effective transitions tend to work together. This is smooth, orderly and logical

transitions from one idea to another. In this case we need to arrange each financial income,

expenditure and their assets. We also need to arrange the sequences of inheritance for all of the

persons in this report. We need also to arrange the ownership flow of assets (Doda & Fortuzi,

2015).

Assets, Liabilities, inheritance, benefits for Richard only

Assets Amount (£)

His pension at 58 now 19,740 p.a

In UK, pension is mandatory for working people. Currently men can claim their state

pension from 65 years while women can claim their pension at the age of 62years and

6months.Both will then increase gradually to 66 by 2020 and 67 between 2026 and 2028. Each

year of NICs gives entitlement to 1/30the of the full basic state pension. State Pension cannot be

taken up before the State Pension age, but may be deferred in return for higher State Pension of

10.4% per year of deferral or a one-off lump sum payment with interest annually at 2% above the

bank of England base rate (Chlebikova, Misankova & Kramarova, 2015).

iv) Ensure they have a life assurance scheme. This is to ensure that you family gets what

they miss when you are gone (dead). They need to get peace of mind by receiving quick and easy

compensation each month to sort out what they need in your absence (Chlebikova, Misankova &

Kramarova, 2015). They need to get a good life assurance scheme which will ensure that the

family you leave behind is looked after well. The right cover will cover your needs whether you

want life insurance, mortgage life insurance or critical illness cover.

v) Ensure that they understand well on 2015 pension freedom scheme. This was

introduced in April 2015. Under this reform, people aged 55 or over were given far greater

freedom over how to access their contribution pension posts. This had a right to give people

choice of what to do with their own savings. They have a right to access cash, securities and

investment returns (Chlebikova, Misankova & Kramarova, 2015).

B) Logical flow and structure of content.

This is effective transitions tend to work together. This is smooth, orderly and logical

transitions from one idea to another. In this case we need to arrange each financial income,

expenditure and their assets. We also need to arrange the sequences of inheritance for all of the

persons in this report. We need also to arrange the ownership flow of assets (Doda & Fortuzi,

2015).

Assets, Liabilities, inheritance, benefits for Richard only

Assets Amount (£)

His pension at 58 now 19,740 p.a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

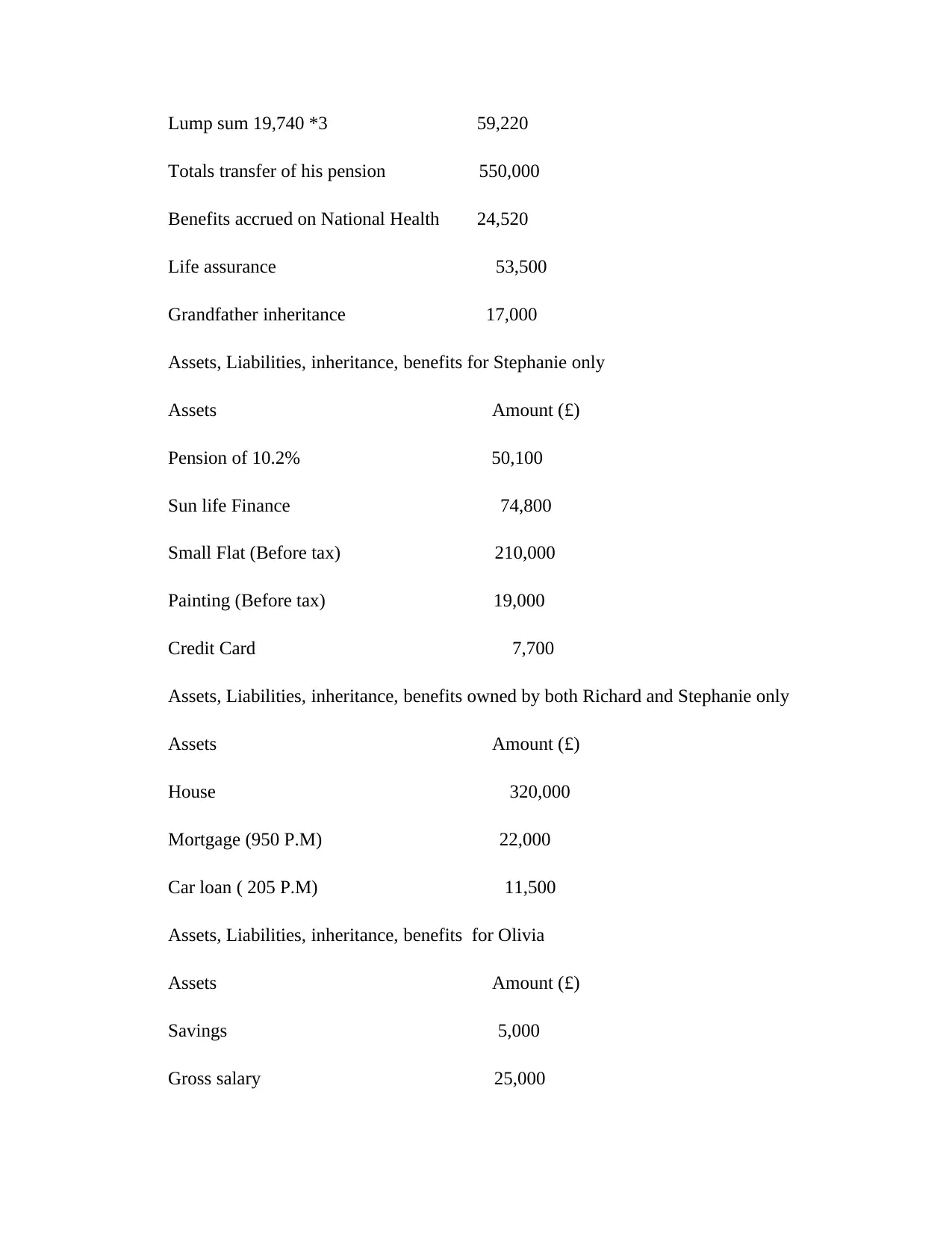

Lump sum 19,740 *3 59,220

Totals transfer of his pension 550,000

Benefits accrued on National Health 24,520

Life assurance 53,500

Grandfather inheritance 17,000

Assets, Liabilities, inheritance, benefits for Stephanie only

Assets Amount (£)

Pension of 10.2% 50,100

Sun life Finance 74,800

Small Flat (Before tax) 210,000

Painting (Before tax) 19,000

Credit Card 7,700

Assets, Liabilities, inheritance, benefits owned by both Richard and Stephanie only

Assets Amount (£)

House 320,000

Mortgage (950 P.M) 22,000

Car loan ( 205 P.M) 11,500

Assets, Liabilities, inheritance, benefits for Olivia

Assets Amount (£)

Savings 5,000

Gross salary 25,000

Totals transfer of his pension 550,000

Benefits accrued on National Health 24,520

Life assurance 53,500

Grandfather inheritance 17,000

Assets, Liabilities, inheritance, benefits for Stephanie only

Assets Amount (£)

Pension of 10.2% 50,100

Sun life Finance 74,800

Small Flat (Before tax) 210,000

Painting (Before tax) 19,000

Credit Card 7,700

Assets, Liabilities, inheritance, benefits owned by both Richard and Stephanie only

Assets Amount (£)

House 320,000

Mortgage (950 P.M) 22,000

Car loan ( 205 P.M) 11,500

Assets, Liabilities, inheritance, benefits for Olivia

Assets Amount (£)

Savings 5,000

Gross salary 25,000

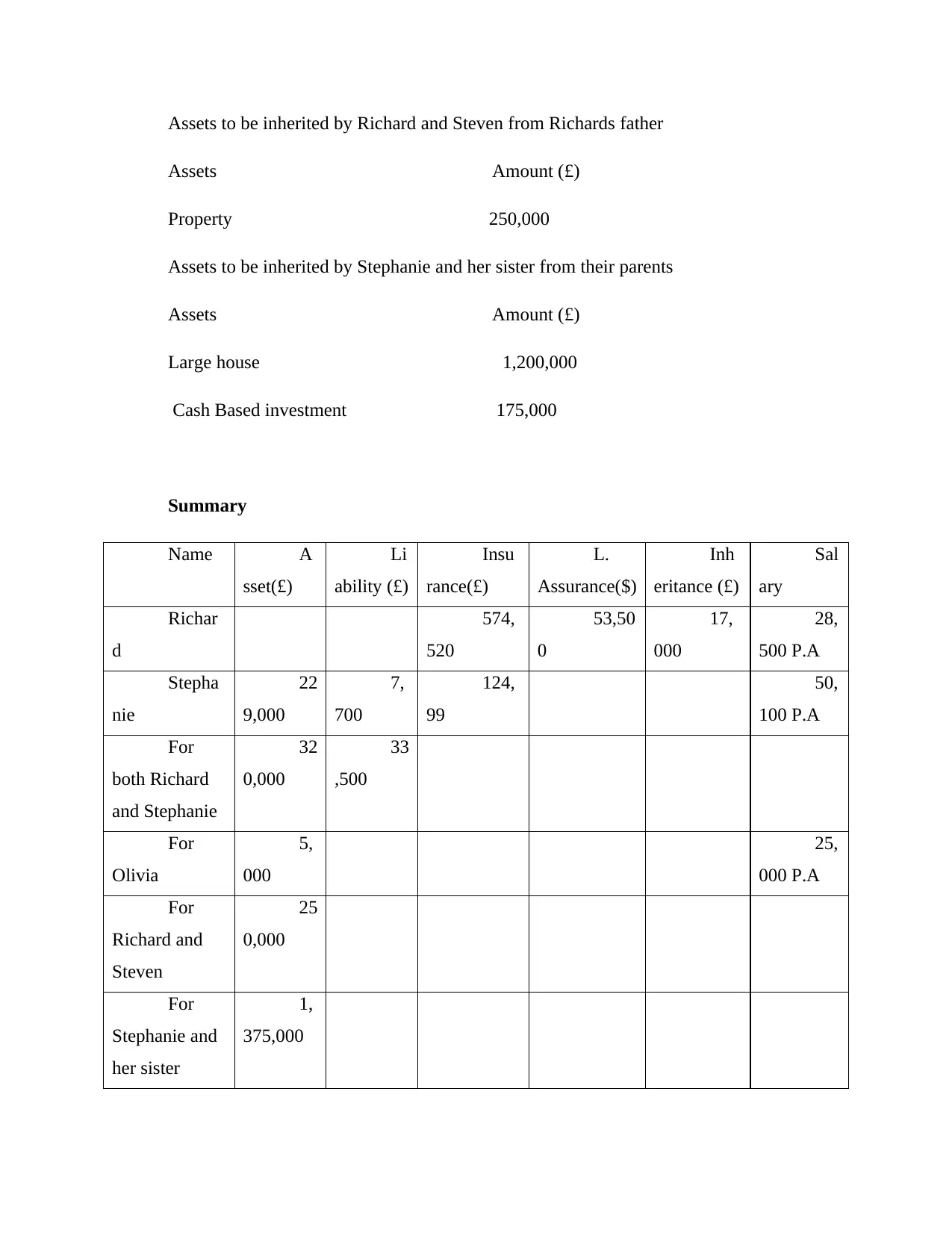

Assets to be inherited by Richard and Steven from Richards father

Assets Amount (£)

Property 250,000

Assets to be inherited by Stephanie and her sister from their parents

Assets Amount (£)

Large house 1,200,000

Cash Based investment 175,000

Summary

Name A

sset(£)

Li

ability (£)

Insu

rance(£)

L.

Assurance($)

Inh

eritance (£)

Sal

ary

Richar

d

574,

520

53,50

0

17,

000

28,

500 P.A

Stepha

nie

22

9,000

7,

700

124,

99

50,

100 P.A

For

both Richard

and Stephanie

32

0,000

33

,500

For

Olivia

5,

000

25,

000 P.A

For

Richard and

Steven

25

0,000

For

Stephanie and

her sister

1,

375,000

Assets Amount (£)

Property 250,000

Assets to be inherited by Stephanie and her sister from their parents

Assets Amount (£)

Large house 1,200,000

Cash Based investment 175,000

Summary

Name A

sset(£)

Li

ability (£)

Insu

rance(£)

L.

Assurance($)

Inh

eritance (£)

Sal

ary

Richar

d

574,

520

53,50

0

17,

000

28,

500 P.A

Stepha

nie

22

9,000

7,

700

124,

99

50,

100 P.A

For

both Richard

and Stephanie

32

0,000

33

,500

For

Olivia

5,

000

25,

000 P.A

For

Richard and

Steven

25

0,000

For

Stephanie and

her sister

1,

375,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

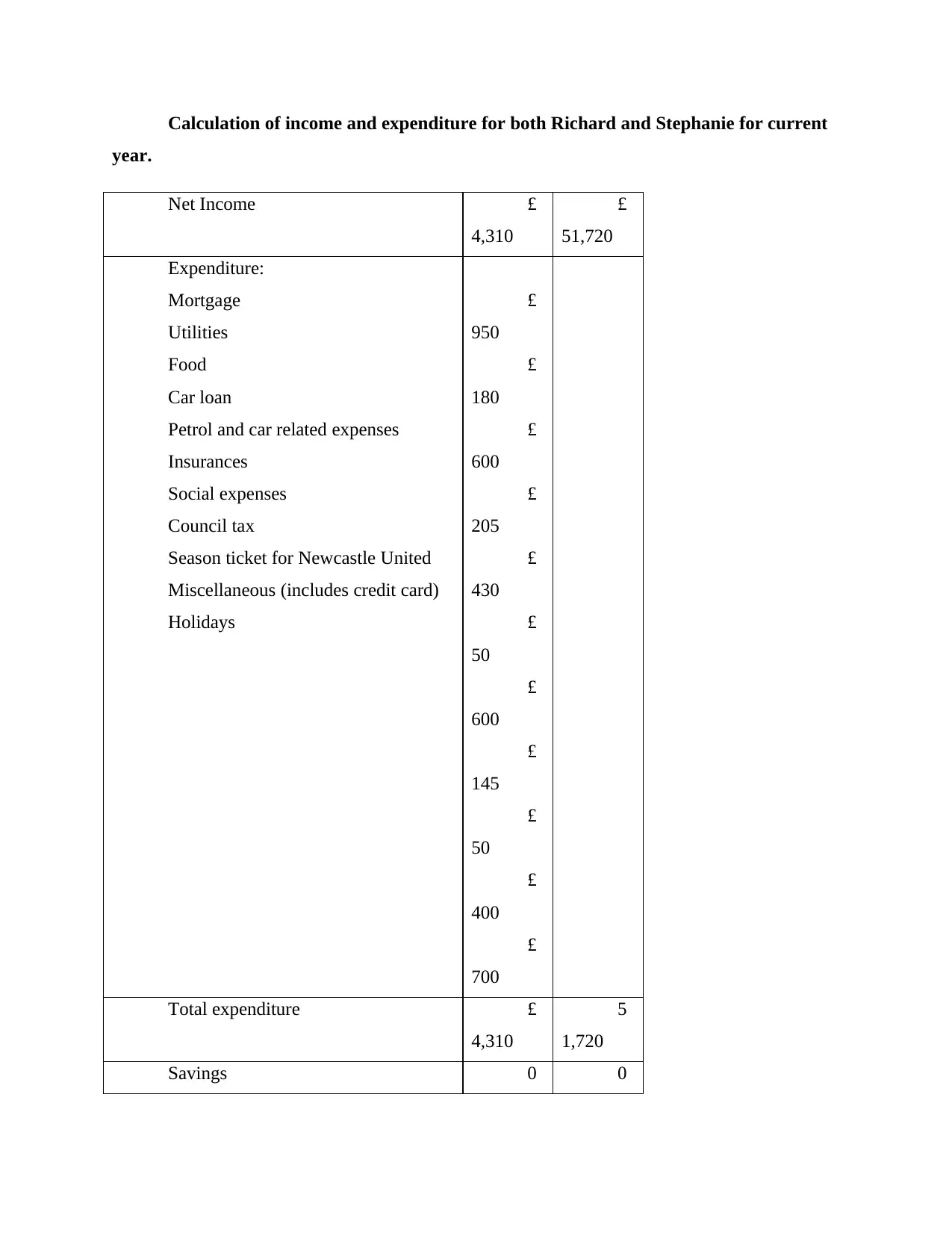

Calculation of income and expenditure for both Richard and Stephanie for current

year.

Net Income £

4,310

£

51,720

Expenditure:

Mortgage

Utilities

Food

Car loan

Petrol and car related expenses

Insurances

Social expenses

Council tax

Season ticket for Newcastle United

Miscellaneous (includes credit card)

Holidays

£

950

£

180

£

600

£

205

£

430

£

50

£

600

£

145

£

50

£

400

£

700

Total expenditure £

4,310

5

1,720

Savings 0 0

year.

Net Income £

4,310

£

51,720

Expenditure:

Mortgage

Utilities

Food

Car loan

Petrol and car related expenses

Insurances

Social expenses

Council tax

Season ticket for Newcastle United

Miscellaneous (includes credit card)

Holidays

£

950

£

180

£

600

£

205

£

430

£

50

£

600

£

145

£

50

£

400

£

700

Total expenditure £

4,310

5

1,720

Savings 0 0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This show that they spend every coin they earn. They don’t make a saving

except the one made in their pension schemes.

This also shows that they cannot be able to increase their expenditure

beyond the above schedule.

It’s not unless they think of an income strategy for them to be able to think

of adding and expense.

B) Evidence of research to form recommendations.

i) Will. They both don’t understand of will testament. Richard and Stephanie says they

don’t understand about the will.

ii) Lack of communication. There is no proper communication among the couples. They

don’t understand how inheritance will be distributed. They don’t look at their age. At this point

in time they should have written a will. For instance Richard’s father doesn’t explain how both

his son Richard and Steven his brother will share the £250,000 in case he dies. He has grown old

enough to make decision of his inheritance to avoid conflicts and war over resources of the

deceased ("Financial health | Planning personal finances | Fidelity", n.d.). This is the same

mistakes that are being inherited even by Richard and Stephanie.

iii) The mare truth. It’s very true that between Richard and Stephanie, one has to die first

and leave the other with the wealth. But they are not ready to speak this truth and put their house

in order always. Stephanie says that if she dies, Richard will inherit her properties or in the case

both are not there Emily and Olivia will inherit their wealthy.

iv) No addition of more expenditure. According to the income and expenditure shown,

Richard and Stephanie have exhausted their income the whole year. They cannot think to add

any expense in their list ("Financial health | Planning personal finances | Fidelity", n.d.).

v) Inheritance. Richard and Stephanie have made their mind on whom to inherit their

wealth in case they are dead and gone. Richard has a daughter Olivia and Stephanie has a niece

Emily. According to the research, they have made their mind to inherit them but they have not

stated in case they are no more how they will share the wealth.

except the one made in their pension schemes.

This also shows that they cannot be able to increase their expenditure

beyond the above schedule.

It’s not unless they think of an income strategy for them to be able to think

of adding and expense.

B) Evidence of research to form recommendations.

i) Will. They both don’t understand of will testament. Richard and Stephanie says they

don’t understand about the will.

ii) Lack of communication. There is no proper communication among the couples. They

don’t understand how inheritance will be distributed. They don’t look at their age. At this point

in time they should have written a will. For instance Richard’s father doesn’t explain how both

his son Richard and Steven his brother will share the £250,000 in case he dies. He has grown old

enough to make decision of his inheritance to avoid conflicts and war over resources of the

deceased ("Financial health | Planning personal finances | Fidelity", n.d.). This is the same

mistakes that are being inherited even by Richard and Stephanie.

iii) The mare truth. It’s very true that between Richard and Stephanie, one has to die first

and leave the other with the wealth. But they are not ready to speak this truth and put their house

in order always. Stephanie says that if she dies, Richard will inherit her properties or in the case

both are not there Emily and Olivia will inherit their wealthy.

iv) No addition of more expenditure. According to the income and expenditure shown,

Richard and Stephanie have exhausted their income the whole year. They cannot think to add

any expense in their list ("Financial health | Planning personal finances | Fidelity", n.d.).

v) Inheritance. Richard and Stephanie have made their mind on whom to inherit their

wealth in case they are dead and gone. Richard has a daughter Olivia and Stephanie has a niece

Emily. According to the research, they have made their mind to inherit them but they have not

stated in case they are no more how they will share the wealth.

vi) Fear to start a business investment. Both of them, Richard and Stephanie fear to risk

in investing in a portfolio since they fear losing the capital in case the portfolio does not succeed.

Richard fears that he has grown old and he can’t indulge in business. He says that he does not

have the passion to do business but has a passion of sports ("Financial Planning and Wealth

Management | Personal Capital", n.d.). He is inherently risk averse. He has invested on the local

premium bonds and some cash in ISA and the remainder in savings account for many years but

very small interest earned for the period. This shows that he is inherent risk averse. Stephanie in

the other hand want to sell the house he bought and the painting but fears to start a portfolio for

her niece. She fears the risk involved. She says that she is very busy.

D) Case study relevance and use of up to date material

In this case we investigate on the couples in this real-life context. In the

case study, it’s true that the couples do not have children together. No one is complaining

about this matter. Not well explained why they happen to be living without the children

and no complain.

It is also material that Richard has a child Olivia. It is in the context that

Stephanie is also aware of this fact and she is not complaining.

The inheritance of Richard’s father £250,000 is to be shared among the

two- Richard and Steven a brother to Richard’s father. All we don’t understand is if

Steven is aware of this fact. All we know is that Richard wants to inherit all the money

for himself saying that by the time his father dies, his uncle will be in USA and will not

be able know about the inheritance. All we don’t understand is, if Richards’s father has a

secret will which Richard doesn’t know ("Financial Planning and Wealth Management |

Personal Capital", n.d.).

It is evident from the context that Richard and Stephanie don’t have a will.

All that is said is that both would like to inherit their assets when they die and have

assumed this will happen. Eventuality may arise from the day to day happenings and

change the mare truth in their mind.

It is evident that Richard is to retire two years to come. He is 58 years now

but we are not told the present age of Stephanie as at now. We also understand that

Richard is older than Stephanie. Their age difference will be able to make us make some

decisions. For example on inheritance. If Stephanie is too young who knows if she will

in investing in a portfolio since they fear losing the capital in case the portfolio does not succeed.

Richard fears that he has grown old and he can’t indulge in business. He says that he does not

have the passion to do business but has a passion of sports ("Financial Planning and Wealth

Management | Personal Capital", n.d.). He is inherently risk averse. He has invested on the local

premium bonds and some cash in ISA and the remainder in savings account for many years but

very small interest earned for the period. This shows that he is inherent risk averse. Stephanie in

the other hand want to sell the house he bought and the painting but fears to start a portfolio for

her niece. She fears the risk involved. She says that she is very busy.

D) Case study relevance and use of up to date material

In this case we investigate on the couples in this real-life context. In the

case study, it’s true that the couples do not have children together. No one is complaining

about this matter. Not well explained why they happen to be living without the children

and no complain.

It is also material that Richard has a child Olivia. It is in the context that

Stephanie is also aware of this fact and she is not complaining.

The inheritance of Richard’s father £250,000 is to be shared among the

two- Richard and Steven a brother to Richard’s father. All we don’t understand is if

Steven is aware of this fact. All we know is that Richard wants to inherit all the money

for himself saying that by the time his father dies, his uncle will be in USA and will not

be able know about the inheritance. All we don’t understand is, if Richards’s father has a

secret will which Richard doesn’t know ("Financial Planning and Wealth Management |

Personal Capital", n.d.).

It is evident from the context that Richard and Stephanie don’t have a will.

All that is said is that both would like to inherit their assets when they die and have

assumed this will happen. Eventuality may arise from the day to day happenings and

change the mare truth in their mind.

It is evident that Richard is to retire two years to come. He is 58 years now

but we are not told the present age of Stephanie as at now. We also understand that

Richard is older than Stephanie. Their age difference will be able to make us make some

decisions. For example on inheritance. If Stephanie is too young who knows if she will

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

be married again if Richard dies first. We cannot be able to make a decision of pension

for Stephanie ("Personal Finance - Investing, Planning, Retirement, Tax ...", n.d.).

It is evident from the context that Stephanie does not understand tax on

capital gain. This is a very crucial item that Stephanie should understand. All she knows

is to sell the house on profit. She cannot make decision on this income because she does

not know how much will be left to her after tax.

From the context the two couples do not understand about the 2015

pension freedoms. They just had heard it in the media. This is accessing the pension at

the age of 55 years and makes decision on it ("Personal Finance - Investing, Planning,

Retirement, Tax ...", n.d.).

E) coverage of issues in the case study at the appropriate level of depth to include an

overview of key recommendations to be expanded on in this report.

Issues in the case study include:

i) Will Testament.

ii) Inheritance.

iii) Tax on Capital gain.

iv) Life assurances.

v) 2015 pension freedom.

vi) Income and expenditure.

vii) Asset ownership.

viii) Retirement period.

ix) After retirement what next.

x) Consequences early retirement.

xi) Tax on capital investment.

Level of depth and overview of recommendations of the issues above.

i) Will Testament

This is well shown in the context by Richard and Stephanie.

for Stephanie ("Personal Finance - Investing, Planning, Retirement, Tax ...", n.d.).

It is evident from the context that Stephanie does not understand tax on

capital gain. This is a very crucial item that Stephanie should understand. All she knows

is to sell the house on profit. She cannot make decision on this income because she does

not know how much will be left to her after tax.

From the context the two couples do not understand about the 2015

pension freedoms. They just had heard it in the media. This is accessing the pension at

the age of 55 years and makes decision on it ("Personal Finance - Investing, Planning,

Retirement, Tax ...", n.d.).

E) coverage of issues in the case study at the appropriate level of depth to include an

overview of key recommendations to be expanded on in this report.

Issues in the case study include:

i) Will Testament.

ii) Inheritance.

iii) Tax on Capital gain.

iv) Life assurances.

v) 2015 pension freedom.

vi) Income and expenditure.

vii) Asset ownership.

viii) Retirement period.

ix) After retirement what next.

x) Consequences early retirement.

xi) Tax on capital investment.

Level of depth and overview of recommendations of the issues above.

i) Will Testament

This is well shown in the context by Richard and Stephanie.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Our recommendation is that a will to be drafted

ii) Inheritance

This is shown on the context by the couples and their parents.

A recommendation is that should be well elaborated in the will. This is to avoid conflict

of interest in case of death ("Personal Finance - MSN Money", n.d.).

iii) Tax on capital gain

This is well stipulated in the context than Stephanie does not know if it is required to be

paid and how.

We recommend that tax on capital gain should be paid on the present government tax on

capital gain rate ("Personal Finance Definition - Investopedia", n.d.).

iv) Life assurance

It is well shown in the context by Richard. He has a life assurance cover.

We recommended that he ensures that the cover meets his needs and wishes. This is

important so as when he is gone, the one left behind will be able push on with life without a

problem ("Personal Finance - MSN Money", n.d.).

v) 2015 Pension Freedom

Richard and Stephanie have heard about this idea of 2015 Pension Freedom in the media

but they don’t understand how it works.

Our recommendation is that this pension is giving an individual access to the pension at

the age of 55 years. This is early retirement scheme. This will reduce the pension amount for an

individual.

vi) Income and Expenditure

ii) Inheritance

This is shown on the context by the couples and their parents.

A recommendation is that should be well elaborated in the will. This is to avoid conflict

of interest in case of death ("Personal Finance - MSN Money", n.d.).

iii) Tax on capital gain

This is well stipulated in the context than Stephanie does not know if it is required to be

paid and how.

We recommend that tax on capital gain should be paid on the present government tax on

capital gain rate ("Personal Finance Definition - Investopedia", n.d.).

iv) Life assurance

It is well shown in the context by Richard. He has a life assurance cover.

We recommended that he ensures that the cover meets his needs and wishes. This is

important so as when he is gone, the one left behind will be able push on with life without a

problem ("Personal Finance - MSN Money", n.d.).

v) 2015 Pension Freedom

Richard and Stephanie have heard about this idea of 2015 Pension Freedom in the media

but they don’t understand how it works.

Our recommendation is that this pension is giving an individual access to the pension at

the age of 55 years. This is early retirement scheme. This will reduce the pension amount for an

individual.

vi) Income and Expenditure

The income and expenditure of Richard and Stephanie is well stipulated in the context.

They spend 100% of their net income for the whole month. They don’t have any savings on

emergencies ("Personal Finance: Wealth News, Money Tips, Personal ...", n.d.).

Our recommendations are that they cut on expenses and at least have a little saving on

their income and should be put in the savings account. This will help if emergencies arises.

vii) Asset ownership

Some asset is not well explained on the percentage ownership. For example the house

Richard and Stephanie lives in. It is not well defined. Another one is the one owned by the

parents of Stephanie is not well defined the share of Stephanie and her sister. Another one is the

one owned by Richard’s father how they will share among the two- Richard and his uncle Steven

("Personal Financial Planning (Wealth Management)", n.d.).

Our recommendation is that all the assets should be well defined the ownership. This

should be done when the mind is sober. Sometime old people may be confused on decision

making. So they should do it when their mind is sober.

viii) Retirement period

Retirement period in UK is 60 years. Early retirement is a decision made by an individual

based on their reasons. However this has an implication on their pension. It will reduce the

amount anticipated at the normal retirement and other benefits thereof.

Our recommendation is that if there is no any forcing issue, one to wait normal retirement

of 60 years. This will ensure one receives his/her full pension and benefits ("Personal Financial

Planning - TTU", n.d.).

ix) After retirement what next

This is a question asked by Richard. He is 58 years and will retire soon after two years.

He is trying to calculate what he will do next. He says that he is good at his work but is a keen

sportsman and would love to have more time to devote to training and competing.

They spend 100% of their net income for the whole month. They don’t have any savings on

emergencies ("Personal Finance: Wealth News, Money Tips, Personal ...", n.d.).

Our recommendations are that they cut on expenses and at least have a little saving on

their income and should be put in the savings account. This will help if emergencies arises.

vii) Asset ownership

Some asset is not well explained on the percentage ownership. For example the house

Richard and Stephanie lives in. It is not well defined. Another one is the one owned by the

parents of Stephanie is not well defined the share of Stephanie and her sister. Another one is the

one owned by Richard’s father how they will share among the two- Richard and his uncle Steven

("Personal Financial Planning (Wealth Management)", n.d.).

Our recommendation is that all the assets should be well defined the ownership. This

should be done when the mind is sober. Sometime old people may be confused on decision

making. So they should do it when their mind is sober.

viii) Retirement period

Retirement period in UK is 60 years. Early retirement is a decision made by an individual

based on their reasons. However this has an implication on their pension. It will reduce the

amount anticipated at the normal retirement and other benefits thereof.

Our recommendation is that if there is no any forcing issue, one to wait normal retirement

of 60 years. This will ensure one receives his/her full pension and benefits ("Personal Financial

Planning - TTU", n.d.).

ix) After retirement what next

This is a question asked by Richard. He is 58 years and will retire soon after two years.

He is trying to calculate what he will do next. He says that he is good at his work but is a keen

sportsman and would love to have more time to devote to training and competing.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.