Comprehensive Financial Plan for Peter and Lisa Clarke Family

VerifiedAdded on 2023/06/13

|25

|3841

|198

Report

AI Summary

This report presents a comprehensive financial plan for Peter and Lisa Clarke, addressing their current financial position, objectives, risk profile, and recommended strategies for investment and retirement. It covers various aspects including assets, liabilities, income, expenses, existing insurance, and superannuation. The plan outlines short, medium, and long-term goals such as minimizing tax, paying off mortgages, accumulating wealth for retirement, and funding their children's education. The recommended investment strategy aims to generate a sustainable income stream while managing risk, with considerations for Peter's inheritance and existing investments. The report also includes disclosures and a disclaimer, ensuring transparency and adherence to ASIC guidelines, offering a roadmap for the Clarkes to achieve their financial milestones and secure their future.

Running head: INDIVIDUAL FINANCIAL PLANNING

Individual Financial Planning

Name of the Student:

Name of the University:

Author’s Note:

Individual Financial Planning

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

INDIVIDUAL FINANCIAL PLANNING

Table of Contents

Covering Letter................................................................................................................................3

Executive Summary.........................................................................................................................5

Introduction......................................................................................................................................5

Current Position...............................................................................................................................6

Personal Details...............................................................................................................................6

Dependents......................................................................................................................................7

Assets and Liabilities.......................................................................................................................8

Income.............................................................................................................................................9

Expenses........................................................................................................................................10

Existing Insurance.........................................................................................................................10

Objectives......................................................................................................................................11

Risk Profile and Asset Allocation..................................................................................................13

Risk Profile and Asset Allocation..................................................................................................13

Recommended Financial Strategy.................................................................................................18

Recommended Investment Strategy..............................................................................................19

Implementation..............................................................................................................................20

Disclosures.....................................................................................................................................21

Disclaimer......................................................................................................................................21

Bibliography..................................................................................................................................23

INDIVIDUAL FINANCIAL PLANNING

Table of Contents

Covering Letter................................................................................................................................3

Executive Summary.........................................................................................................................5

Introduction......................................................................................................................................5

Current Position...............................................................................................................................6

Personal Details...............................................................................................................................6

Dependents......................................................................................................................................7

Assets and Liabilities.......................................................................................................................8

Income.............................................................................................................................................9

Expenses........................................................................................................................................10

Existing Insurance.........................................................................................................................10

Objectives......................................................................................................................................11

Risk Profile and Asset Allocation..................................................................................................13

Risk Profile and Asset Allocation..................................................................................................13

Recommended Financial Strategy.................................................................................................18

Recommended Investment Strategy..............................................................................................19

Implementation..............................................................................................................................20

Disclosures.....................................................................................................................................21

Disclaimer......................................................................................................................................21

Bibliography..................................................................................................................................23

2

INDIVIDUAL FINANCIAL PLANNING

INDIVIDUAL FINANCIAL PLANNING

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

INDIVIDUAL FINANCIAL PLANNING

Covering Letter

To Peter and Lisa Clarke

Address: 25 Ashington Dr Warners Bay NSW 2282

Dear Peter and Lisa,

I am highly grateful that you have given me the privilege to serve you with your financial

consultations and therefore accepting my offering to come to this face to face meeting so that I

would be able to give out effective suggestions with respect to your financial activities. the

recommendations that would be provided to you would be on the basis on the information that

you have given me and I am sure that these suggestions would be helpful for your future life.

The information that I would provide would be helpful to you in undertaking future investments

so that you can earn effective level of returns and income from the investments. This would

enhance your life and secure life post retirement.

The responses you have given through the Fact Finder and the questions related to the risk

profile has been of great help as I have been able to attain greater level of knowledge through the

same with respect to your present objectives and goals and the present condition and your notion

towards risks, income returns, security and volatility.

The suggestions and the outcomes that would be collected can be utilised in order to construct

your Statement of Advice. This document will be a record that can be used for the purpose of

suggestions even in the future course of time in order to attain your goals and objectives that is

even inclusive of the interests and the fees that are related to the advice.

INDIVIDUAL FINANCIAL PLANNING

Covering Letter

To Peter and Lisa Clarke

Address: 25 Ashington Dr Warners Bay NSW 2282

Dear Peter and Lisa,

I am highly grateful that you have given me the privilege to serve you with your financial

consultations and therefore accepting my offering to come to this face to face meeting so that I

would be able to give out effective suggestions with respect to your financial activities. the

recommendations that would be provided to you would be on the basis on the information that

you have given me and I am sure that these suggestions would be helpful for your future life.

The information that I would provide would be helpful to you in undertaking future investments

so that you can earn effective level of returns and income from the investments. This would

enhance your life and secure life post retirement.

The responses you have given through the Fact Finder and the questions related to the risk

profile has been of great help as I have been able to attain greater level of knowledge through the

same with respect to your present objectives and goals and the present condition and your notion

towards risks, income returns, security and volatility.

The suggestions and the outcomes that would be collected can be utilised in order to construct

your Statement of Advice. This document will be a record that can be used for the purpose of

suggestions even in the future course of time in order to attain your goals and objectives that is

even inclusive of the interests and the fees that are related to the advice.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

INDIVIDUAL FINANCIAL PLANNING

If there are any changes in the lifestyle with the transformation of time, then advices can be

provided in the future as well which would be useful in maintaining a secured and safe lifestyle.

Hence, I am looking forward to come to your assistance with other suggestions and consultation

with respect to the plans and strategies in order to provide you extensive and sustainable

services. All the suggestions and the advices that will be provided to you will be based on the

ASIC guidelines.

Regards

Malcolm Starc

Signature

Financial Consultant

INDIVIDUAL FINANCIAL PLANNING

If there are any changes in the lifestyle with the transformation of time, then advices can be

provided in the future as well which would be useful in maintaining a secured and safe lifestyle.

Hence, I am looking forward to come to your assistance with other suggestions and consultation

with respect to the plans and strategies in order to provide you extensive and sustainable

services. All the suggestions and the advices that will be provided to you will be based on the

ASIC guidelines.

Regards

Malcolm Starc

Signature

Financial Consultant

5

INDIVIDUAL FINANCIAL PLANNING

Executive Summary

The summary provides an overview that would be helpful to the client in understanding

the recommendations and the suggestions that would be given out to them. The overview is

actually the present condition, the objectives and the aims and the plans and guidelines that

would be recommended in order to assist the client to attain their future objectives and goals.

The best result can be given with the incorporation of the strategies. The client would be

requiring knowledge and therefore by reading the executive summary, they would be able to

attain better knowledge about the suggestions that have been given out to them and thereby able

to understand whether aims and goals have been reached. There is sufficient data which would

assist the client to take effective decisions by looking at the risks that they may undergo. The

fees and the charges that are related to SOA are even reported. The data that has been provided

to them will be written in a clear and lucid language with the unavailability of expressions and

therefore is ideal to their degree of the financial knowledge.

Introduction

The introduction of the paper would address the client about the aspects that would be

covered in the SOA and accordingly the advices and the suggestions that would be provided to

them on the basis of their plans and objectives in order to help the clients reach their financial

milestones. The SOA would cover the areas like the insurance, superannuation, cash flow

planning, investment planning and estate planning for the couple. The advices would even

include the other non-financial aims and objectives of the couple that would include the securing

their life even after retirement and assisting their dependent children to undergo college and

support them till they become independent. The clients would be made aware of the risks and the

INDIVIDUAL FINANCIAL PLANNING

Executive Summary

The summary provides an overview that would be helpful to the client in understanding

the recommendations and the suggestions that would be given out to them. The overview is

actually the present condition, the objectives and the aims and the plans and guidelines that

would be recommended in order to assist the client to attain their future objectives and goals.

The best result can be given with the incorporation of the strategies. The client would be

requiring knowledge and therefore by reading the executive summary, they would be able to

attain better knowledge about the suggestions that have been given out to them and thereby able

to understand whether aims and goals have been reached. There is sufficient data which would

assist the client to take effective decisions by looking at the risks that they may undergo. The

fees and the charges that are related to SOA are even reported. The data that has been provided

to them will be written in a clear and lucid language with the unavailability of expressions and

therefore is ideal to their degree of the financial knowledge.

Introduction

The introduction of the paper would address the client about the aspects that would be

covered in the SOA and accordingly the advices and the suggestions that would be provided to

them on the basis of their plans and objectives in order to help the clients reach their financial

milestones. The SOA would cover the areas like the insurance, superannuation, cash flow

planning, investment planning and estate planning for the couple. The advices would even

include the other non-financial aims and objectives of the couple that would include the securing

their life even after retirement and assisting their dependent children to undergo college and

support them till they become independent. The clients would be made aware of the risks and the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

INDIVIDUAL FINANCIAL PLANNING

challenges they would face with respect to these issues and thereby assisting them to create

contingency and a buffer in order to mitigate these risks in an effective manner.

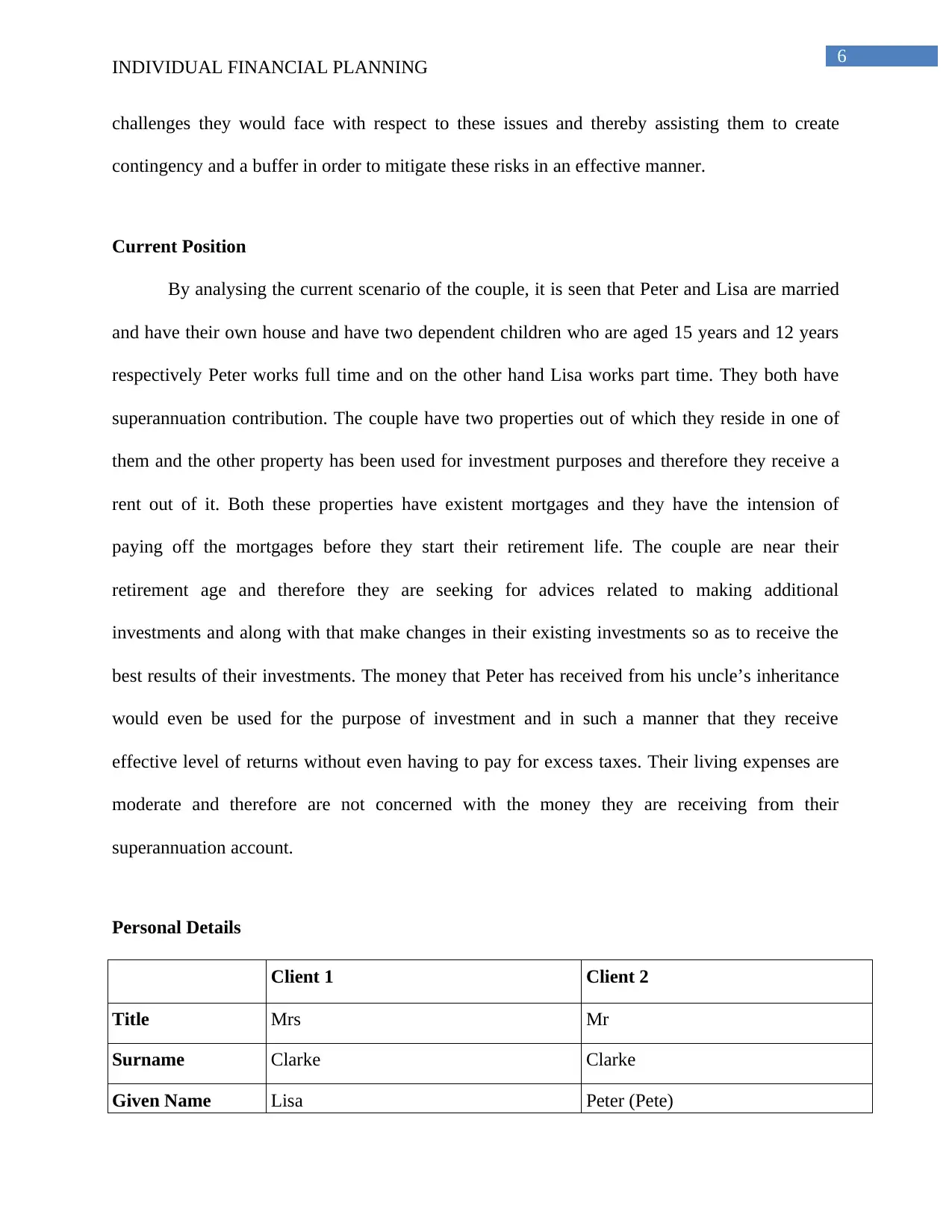

Current Position

By analysing the current scenario of the couple, it is seen that Peter and Lisa are married

and have their own house and have two dependent children who are aged 15 years and 12 years

respectively Peter works full time and on the other hand Lisa works part time. They both have

superannuation contribution. The couple have two properties out of which they reside in one of

them and the other property has been used for investment purposes and therefore they receive a

rent out of it. Both these properties have existent mortgages and they have the intension of

paying off the mortgages before they start their retirement life. The couple are near their

retirement age and therefore they are seeking for advices related to making additional

investments and along with that make changes in their existing investments so as to receive the

best results of their investments. The money that Peter has received from his uncle’s inheritance

would even be used for the purpose of investment and in such a manner that they receive

effective level of returns without even having to pay for excess taxes. Their living expenses are

moderate and therefore are not concerned with the money they are receiving from their

superannuation account.

Personal Details

Client 1 Client 2

Title Mrs Mr

Surname Clarke Clarke

Given Name Lisa Peter (Pete)

INDIVIDUAL FINANCIAL PLANNING

challenges they would face with respect to these issues and thereby assisting them to create

contingency and a buffer in order to mitigate these risks in an effective manner.

Current Position

By analysing the current scenario of the couple, it is seen that Peter and Lisa are married

and have their own house and have two dependent children who are aged 15 years and 12 years

respectively Peter works full time and on the other hand Lisa works part time. They both have

superannuation contribution. The couple have two properties out of which they reside in one of

them and the other property has been used for investment purposes and therefore they receive a

rent out of it. Both these properties have existent mortgages and they have the intension of

paying off the mortgages before they start their retirement life. The couple are near their

retirement age and therefore they are seeking for advices related to making additional

investments and along with that make changes in their existing investments so as to receive the

best results of their investments. The money that Peter has received from his uncle’s inheritance

would even be used for the purpose of investment and in such a manner that they receive

effective level of returns without even having to pay for excess taxes. Their living expenses are

moderate and therefore are not concerned with the money they are receiving from their

superannuation account.

Personal Details

Client 1 Client 2

Title Mrs Mr

Surname Clarke Clarke

Given Name Lisa Peter (Pete)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

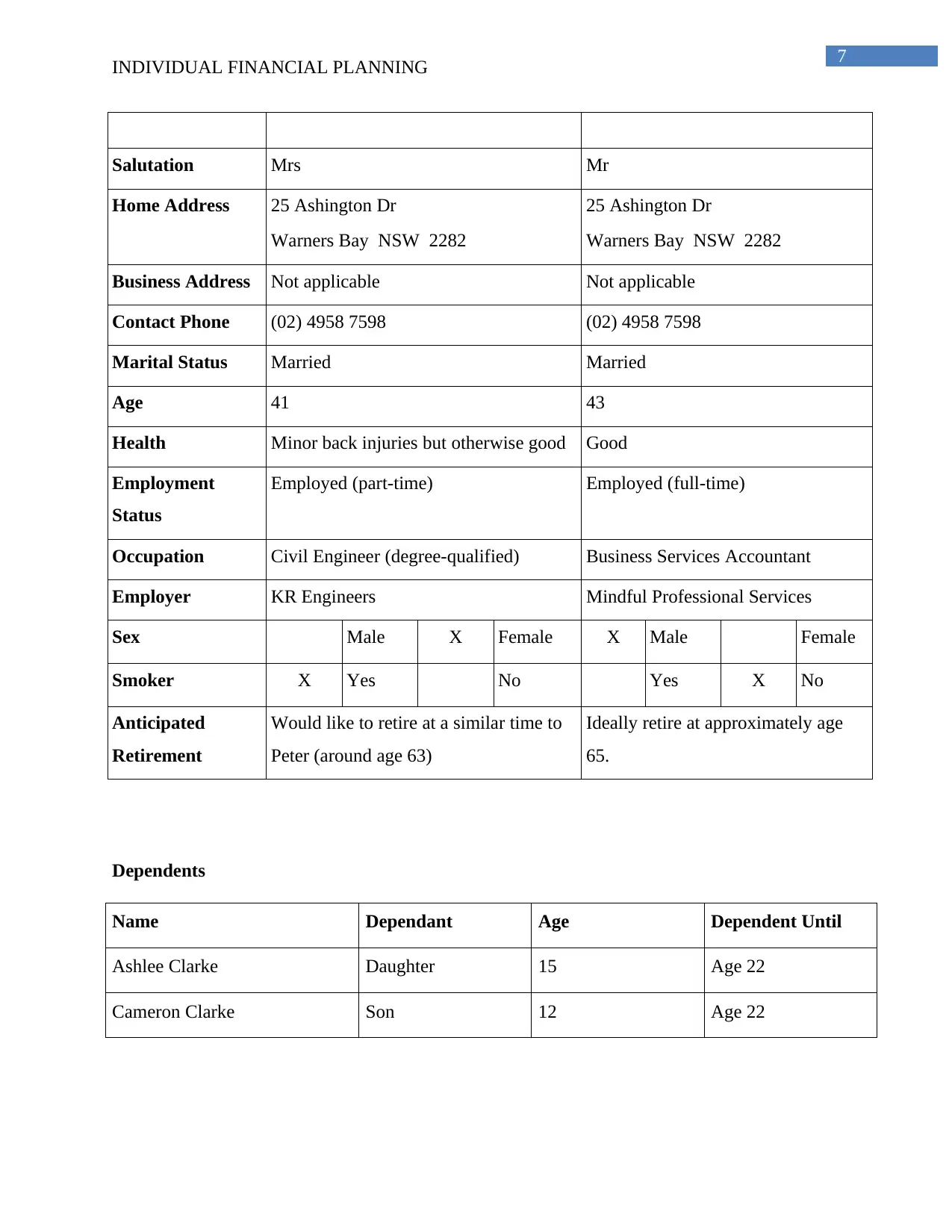

INDIVIDUAL FINANCIAL PLANNING

Salutation Mrs Mr

Home Address 25 Ashington Dr

Warners Bay NSW 2282

25 Ashington Dr

Warners Bay NSW 2282

Business Address Not applicable Not applicable

Contact Phone (02) 4958 7598 (02) 4958 7598

Marital Status Married Married

Age 41 43

Health Minor back injuries but otherwise good Good

Employment

Status

Employed (part-time) Employed (full-time)

Occupation Civil Engineer (degree-qualified) Business Services Accountant

Employer KR Engineers Mindful Professional Services

Sex Male X Female X Male Female

Smoker X Yes No Yes X No

Anticipated

Retirement

Would like to retire at a similar time to

Peter (around age 63)

Ideally retire at approximately age

65.

Dependents

Name Dependant Age Dependent Until

Ashlee Clarke Daughter 15 Age 22

Cameron Clarke Son 12 Age 22

INDIVIDUAL FINANCIAL PLANNING

Salutation Mrs Mr

Home Address 25 Ashington Dr

Warners Bay NSW 2282

25 Ashington Dr

Warners Bay NSW 2282

Business Address Not applicable Not applicable

Contact Phone (02) 4958 7598 (02) 4958 7598

Marital Status Married Married

Age 41 43

Health Minor back injuries but otherwise good Good

Employment

Status

Employed (part-time) Employed (full-time)

Occupation Civil Engineer (degree-qualified) Business Services Accountant

Employer KR Engineers Mindful Professional Services

Sex Male X Female X Male Female

Smoker X Yes No Yes X No

Anticipated

Retirement

Would like to retire at a similar time to

Peter (around age 63)

Ideally retire at approximately age

65.

Dependents

Name Dependant Age Dependent Until

Ashlee Clarke Daughter 15 Age 22

Cameron Clarke Son 12 Age 22

8

INDIVIDUAL FINANCIAL PLANNING

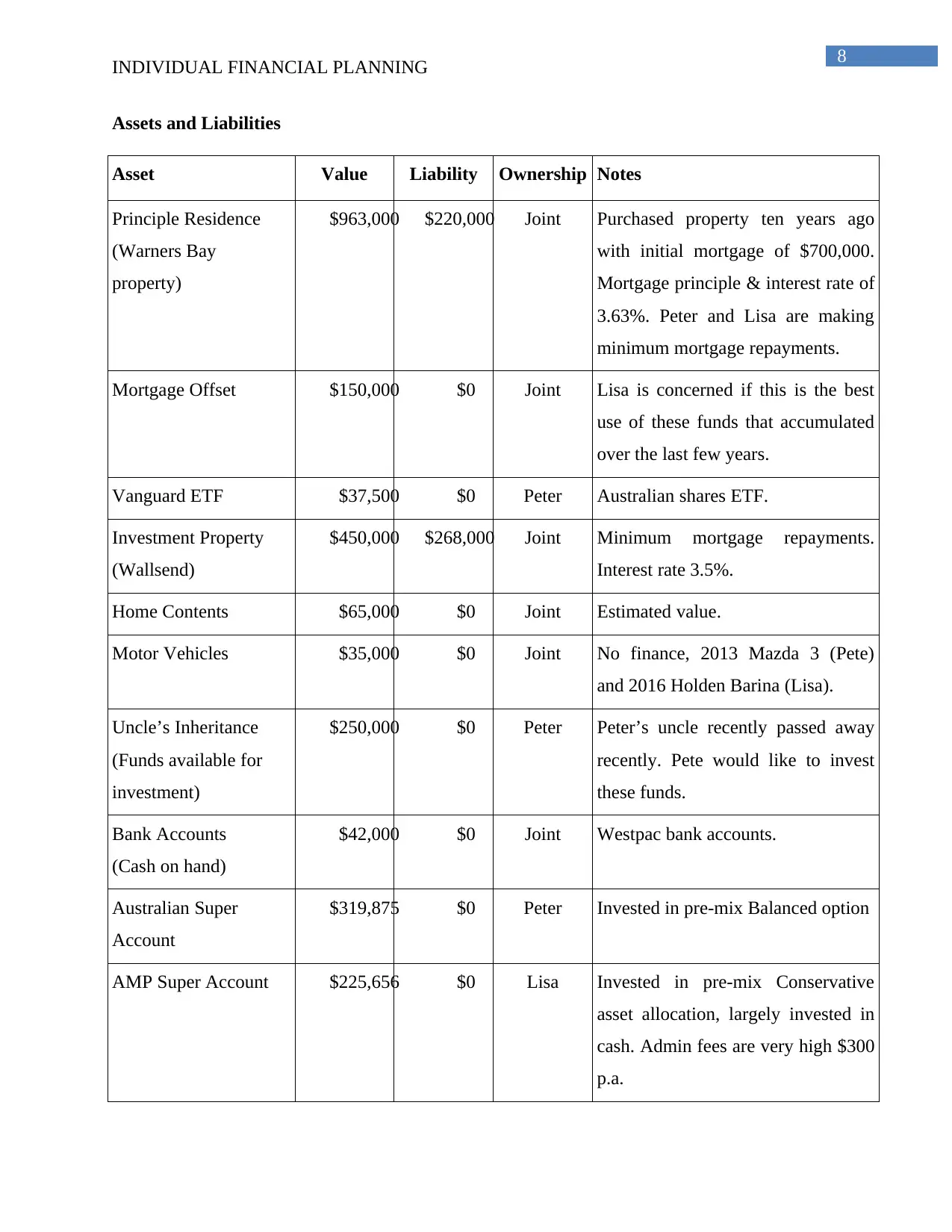

Assets and Liabilities

Asset Value Liability Ownership Notes

Principle Residence

(Warners Bay

property)

$963,000 $220,000 Joint Purchased property ten years ago

with initial mortgage of $700,000.

Mortgage principle & interest rate of

3.63%. Peter and Lisa are making

minimum mortgage repayments.

Mortgage Offset $150,000 $0 Joint Lisa is concerned if this is the best

use of these funds that accumulated

over the last few years.

Vanguard ETF $37,500 $0 Peter Australian shares ETF.

Investment Property

(Wallsend)

$450,000 $268,000 Joint Minimum mortgage repayments.

Interest rate 3.5%.

Home Contents $65,000 $0 Joint Estimated value.

Motor Vehicles $35,000 $0 Joint No finance, 2013 Mazda 3 (Pete)

and 2016 Holden Barina (Lisa).

Uncle’s Inheritance

(Funds available for

investment)

$250,000 $0 Peter Peter’s uncle recently passed away

recently. Pete would like to invest

these funds.

Bank Accounts

(Cash on hand)

$42,000 $0 Joint Westpac bank accounts.

Australian Super

Account

$319,875 $0 Peter Invested in pre-mix Balanced option

AMP Super Account $225,656 $0 Lisa Invested in pre-mix Conservative

asset allocation, largely invested in

cash. Admin fees are very high $300

p.a.

INDIVIDUAL FINANCIAL PLANNING

Assets and Liabilities

Asset Value Liability Ownership Notes

Principle Residence

(Warners Bay

property)

$963,000 $220,000 Joint Purchased property ten years ago

with initial mortgage of $700,000.

Mortgage principle & interest rate of

3.63%. Peter and Lisa are making

minimum mortgage repayments.

Mortgage Offset $150,000 $0 Joint Lisa is concerned if this is the best

use of these funds that accumulated

over the last few years.

Vanguard ETF $37,500 $0 Peter Australian shares ETF.

Investment Property

(Wallsend)

$450,000 $268,000 Joint Minimum mortgage repayments.

Interest rate 3.5%.

Home Contents $65,000 $0 Joint Estimated value.

Motor Vehicles $35,000 $0 Joint No finance, 2013 Mazda 3 (Pete)

and 2016 Holden Barina (Lisa).

Uncle’s Inheritance

(Funds available for

investment)

$250,000 $0 Peter Peter’s uncle recently passed away

recently. Pete would like to invest

these funds.

Bank Accounts

(Cash on hand)

$42,000 $0 Joint Westpac bank accounts.

Australian Super

Account

$319,875 $0 Peter Invested in pre-mix Balanced option

AMP Super Account $225,656 $0 Lisa Invested in pre-mix Conservative

asset allocation, largely invested in

cash. Admin fees are very high $300

p.a.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

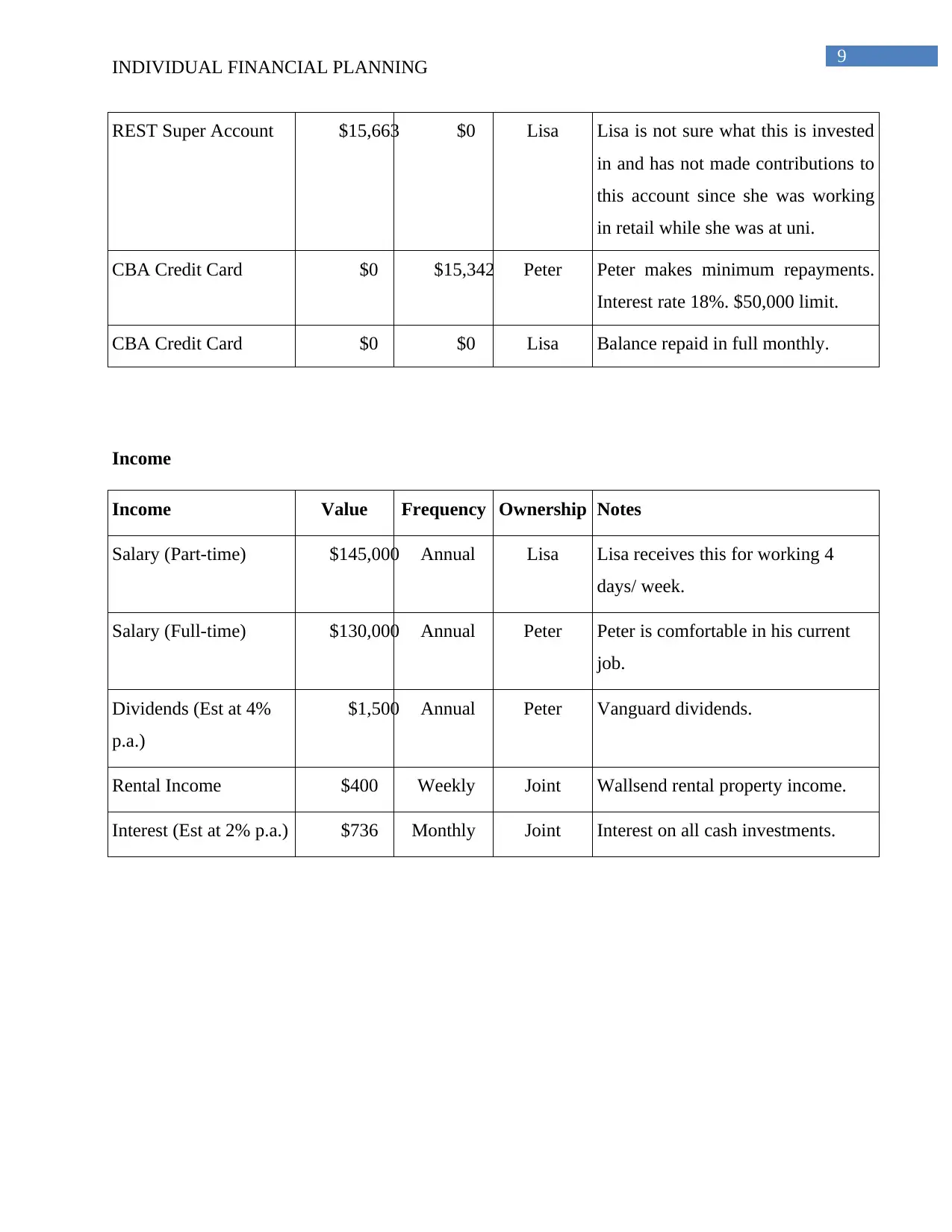

INDIVIDUAL FINANCIAL PLANNING

REST Super Account $15,663 $0 Lisa Lisa is not sure what this is invested

in and has not made contributions to

this account since she was working

in retail while she was at uni.

CBA Credit Card $0 $15,342 Peter Peter makes minimum repayments.

Interest rate 18%. $50,000 limit.

CBA Credit Card $0 $0 Lisa Balance repaid in full monthly.

Income

Income Value Frequency Ownership Notes

Salary (Part-time) $145,000 Annual Lisa Lisa receives this for working 4

days/ week.

Salary (Full-time) $130,000 Annual Peter Peter is comfortable in his current

job.

Dividends (Est at 4%

p.a.)

$1,500 Annual Peter Vanguard dividends.

Rental Income $400 Weekly Joint Wallsend rental property income.

Interest (Est at 2% p.a.) $736 Monthly Joint Interest on all cash investments.

INDIVIDUAL FINANCIAL PLANNING

REST Super Account $15,663 $0 Lisa Lisa is not sure what this is invested

in and has not made contributions to

this account since she was working

in retail while she was at uni.

CBA Credit Card $0 $15,342 Peter Peter makes minimum repayments.

Interest rate 18%. $50,000 limit.

CBA Credit Card $0 $0 Lisa Balance repaid in full monthly.

Income

Income Value Frequency Ownership Notes

Salary (Part-time) $145,000 Annual Lisa Lisa receives this for working 4

days/ week.

Salary (Full-time) $130,000 Annual Peter Peter is comfortable in his current

job.

Dividends (Est at 4%

p.a.)

$1,500 Annual Peter Vanguard dividends.

Rental Income $400 Weekly Joint Wallsend rental property income.

Interest (Est at 2% p.a.) $736 Monthly Joint Interest on all cash investments.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

INDIVIDUAL FINANCIAL PLANNING

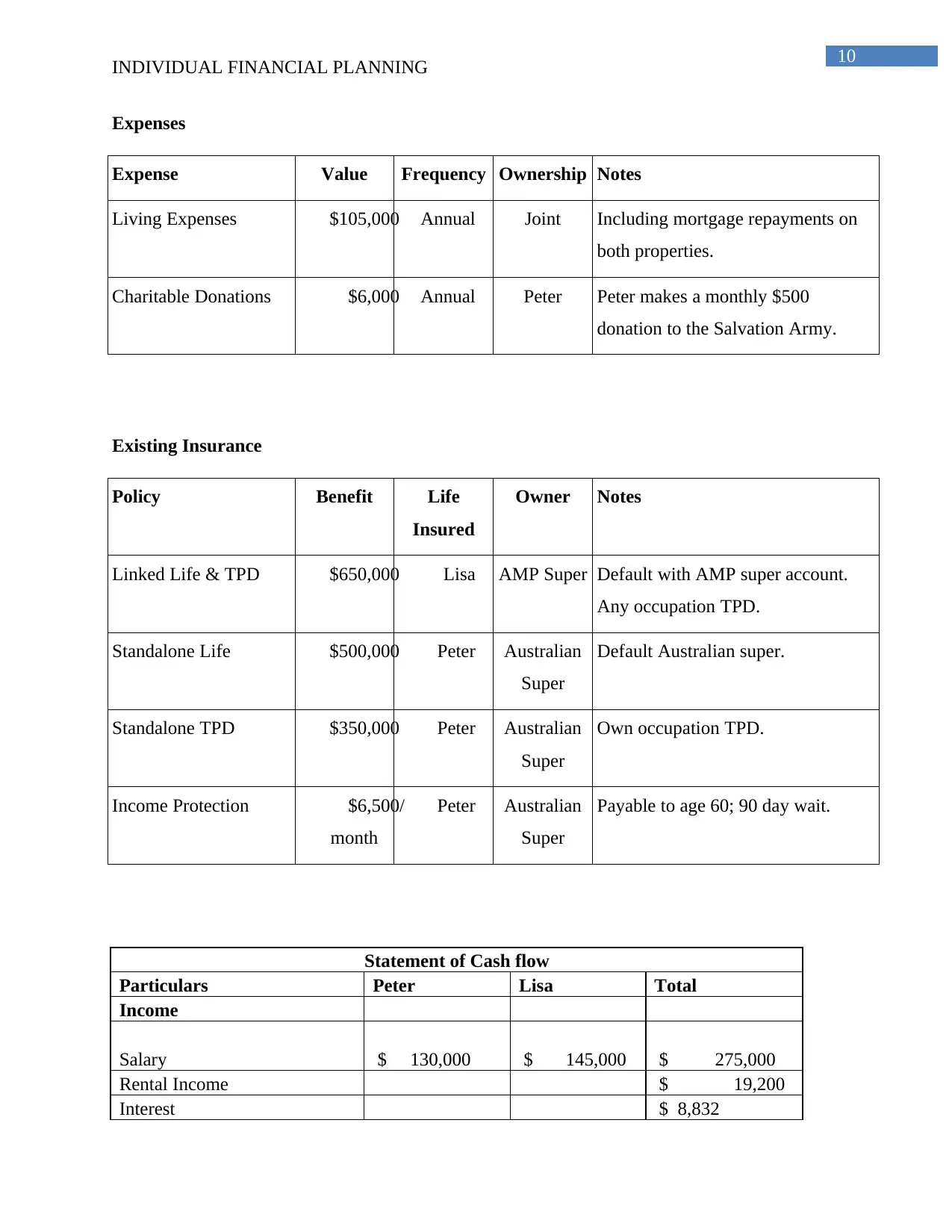

Expenses

Expense Value Frequency Ownership Notes

Living Expenses $105,000 Annual Joint Including mortgage repayments on

both properties.

Charitable Donations $6,000 Annual Peter Peter makes a monthly $500

donation to the Salvation Army.

Existing Insurance

Policy Benefit Life

Insured

Owner Notes

Linked Life & TPD $650,000 Lisa AMP Super Default with AMP super account.

Any occupation TPD.

Standalone Life $500,000 Peter Australian

Super

Default Australian super.

Standalone TPD $350,000 Peter Australian

Super

Own occupation TPD.

Income Protection $6,500/

month

Peter Australian

Super

Payable to age 60; 90 day wait.

Statement of Cash flow

Particulars Peter Lisa Total

Income

Salary $ 130,000 $ 145,000 $ 275,000

Rental Income $ 19,200

Interest $ 8,832

INDIVIDUAL FINANCIAL PLANNING

Expenses

Expense Value Frequency Ownership Notes

Living Expenses $105,000 Annual Joint Including mortgage repayments on

both properties.

Charitable Donations $6,000 Annual Peter Peter makes a monthly $500

donation to the Salvation Army.

Existing Insurance

Policy Benefit Life

Insured

Owner Notes

Linked Life & TPD $650,000 Lisa AMP Super Default with AMP super account.

Any occupation TPD.

Standalone Life $500,000 Peter Australian

Super

Default Australian super.

Standalone TPD $350,000 Peter Australian

Super

Own occupation TPD.

Income Protection $6,500/

month

Peter Australian

Super

Payable to age 60; 90 day wait.

Statement of Cash flow

Particulars Peter Lisa Total

Income

Salary $ 130,000 $ 145,000 $ 275,000

Rental Income $ 19,200

Interest $ 8,832

11

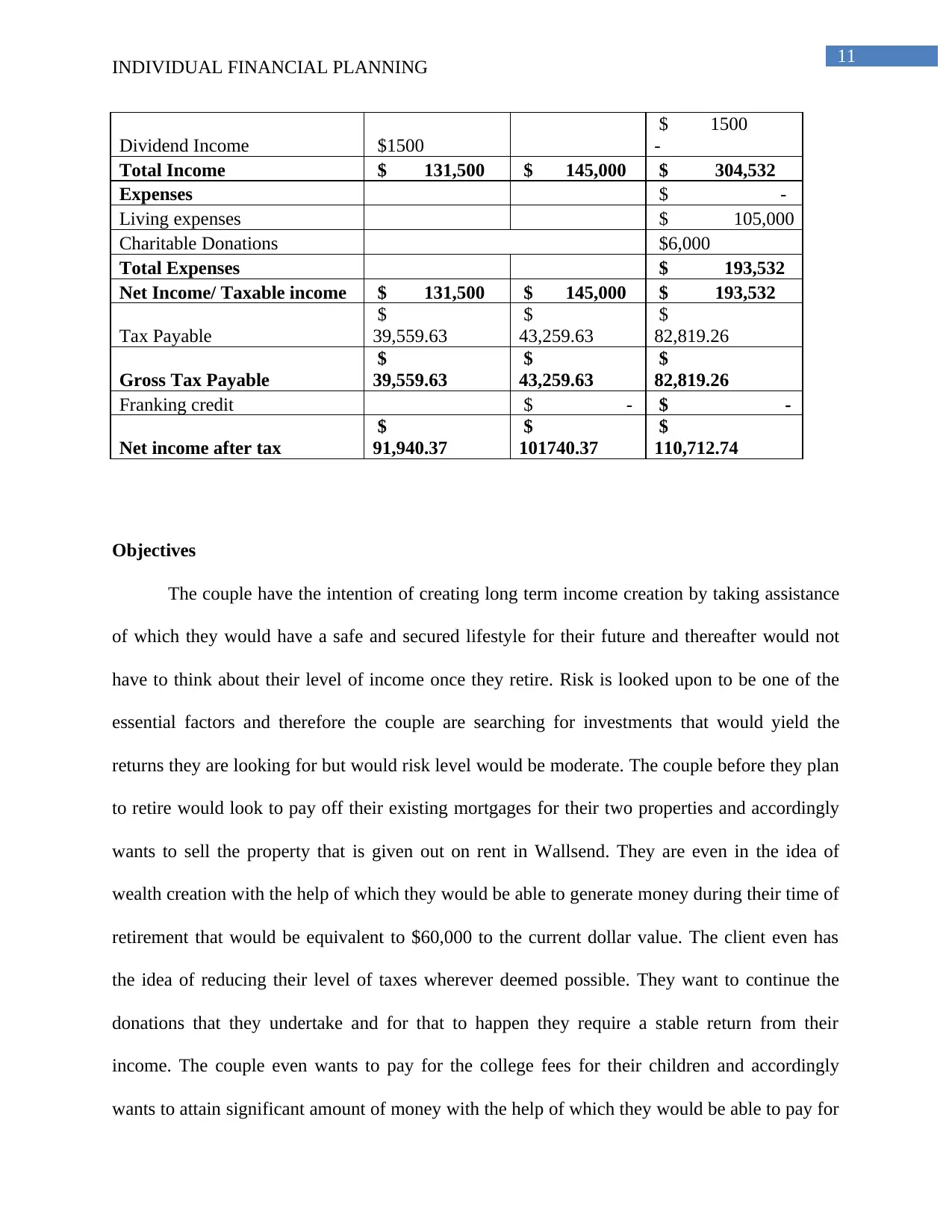

INDIVIDUAL FINANCIAL PLANNING

Dividend Income $1500

$ 1500

-

Total Income $ 131,500 $ 145,000 $ 304,532

Expenses $ -

Living expenses $ 105,000

Charitable Donations $6,000

Total Expenses $ 193,532

Net Income/ Taxable income $ 131,500 $ 145,000 $ 193,532

Tax Payable

$

39,559.63

$

43,259.63

$

82,819.26

Gross Tax Payable

$

39,559.63

$

43,259.63

$

82,819.26

Franking credit $ - $ -

Net income after tax

$

91,940.37

$

101740.37

$

110,712.74

Objectives

The couple have the intention of creating long term income creation by taking assistance

of which they would have a safe and secured lifestyle for their future and thereafter would not

have to think about their level of income once they retire. Risk is looked upon to be one of the

essential factors and therefore the couple are searching for investments that would yield the

returns they are looking for but would risk level would be moderate. The couple before they plan

to retire would look to pay off their existing mortgages for their two properties and accordingly

wants to sell the property that is given out on rent in Wallsend. They are even in the idea of

wealth creation with the help of which they would be able to generate money during their time of

retirement that would be equivalent to $60,000 to the current dollar value. The client even has

the idea of reducing their level of taxes wherever deemed possible. They want to continue the

donations that they undertake and for that to happen they require a stable return from their

income. The couple even wants to pay for the college fees for their children and accordingly

wants to attain significant amount of money with the help of which they would be able to pay for

INDIVIDUAL FINANCIAL PLANNING

Dividend Income $1500

$ 1500

-

Total Income $ 131,500 $ 145,000 $ 304,532

Expenses $ -

Living expenses $ 105,000

Charitable Donations $6,000

Total Expenses $ 193,532

Net Income/ Taxable income $ 131,500 $ 145,000 $ 193,532

Tax Payable

$

39,559.63

$

43,259.63

$

82,819.26

Gross Tax Payable

$

39,559.63

$

43,259.63

$

82,819.26

Franking credit $ - $ -

Net income after tax

$

91,940.37

$

101740.37

$

110,712.74

Objectives

The couple have the intention of creating long term income creation by taking assistance

of which they would have a safe and secured lifestyle for their future and thereafter would not

have to think about their level of income once they retire. Risk is looked upon to be one of the

essential factors and therefore the couple are searching for investments that would yield the

returns they are looking for but would risk level would be moderate. The couple before they plan

to retire would look to pay off their existing mortgages for their two properties and accordingly

wants to sell the property that is given out on rent in Wallsend. They are even in the idea of

wealth creation with the help of which they would be able to generate money during their time of

retirement that would be equivalent to $60,000 to the current dollar value. The client even has

the idea of reducing their level of taxes wherever deemed possible. They want to continue the

donations that they undertake and for that to happen they require a stable return from their

income. The couple even wants to pay for the college fees for their children and accordingly

wants to attain significant amount of money with the help of which they would be able to pay for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.