Detailed Financial Plan for First Home Buyers in Sydney/Melbourne

VerifiedAdded on 2023/06/11

|8

|1521

|158

Report

AI Summary

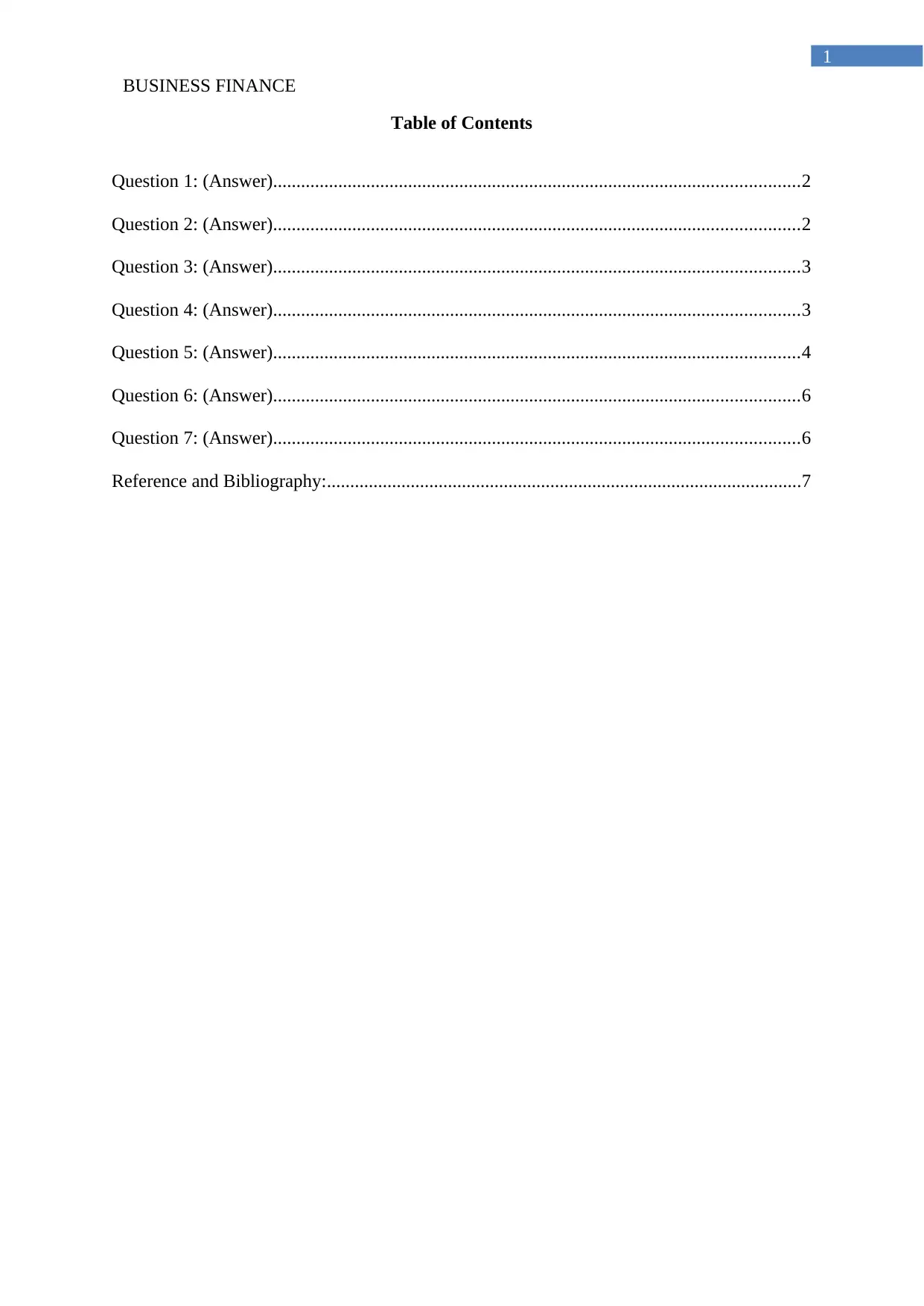

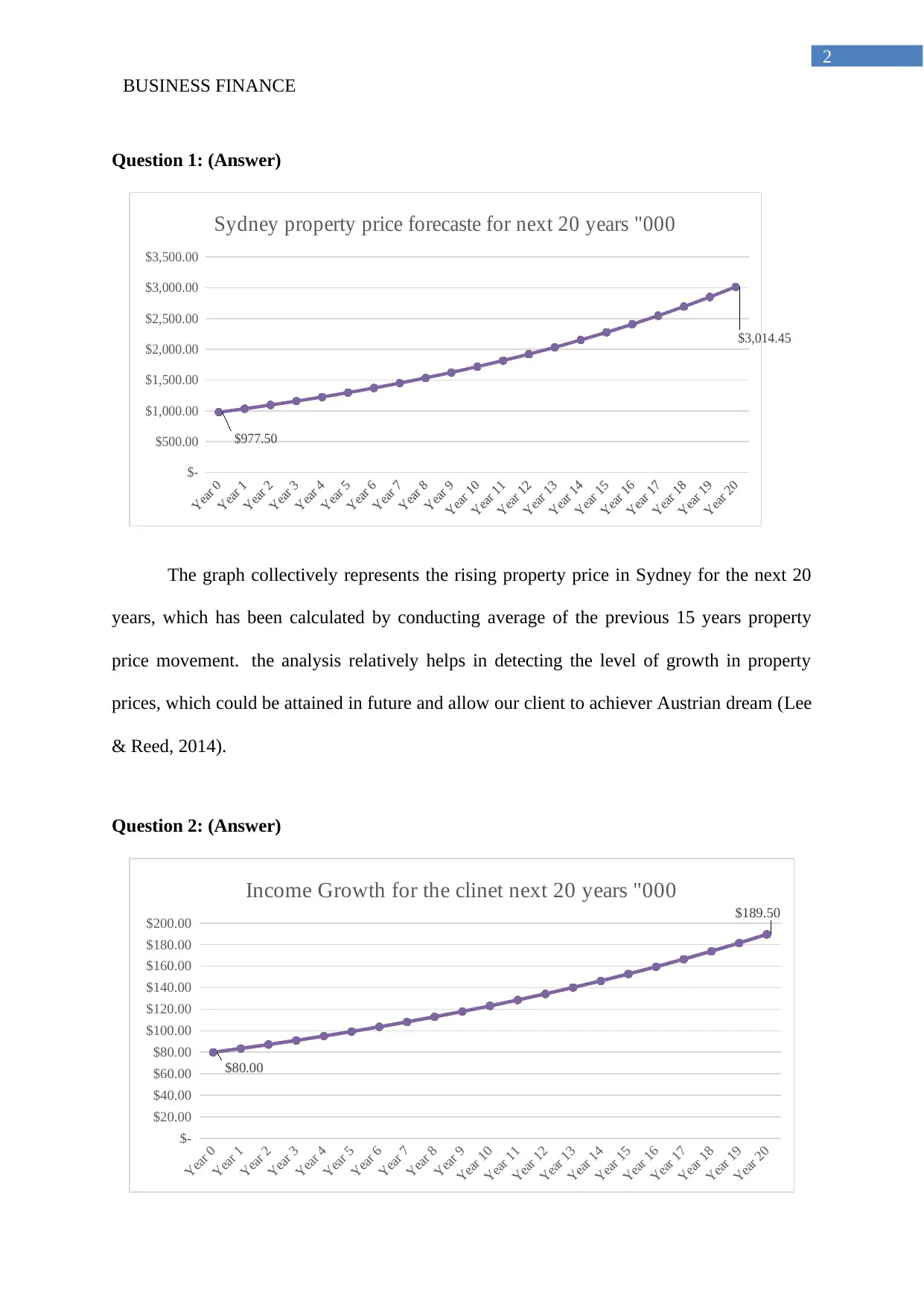

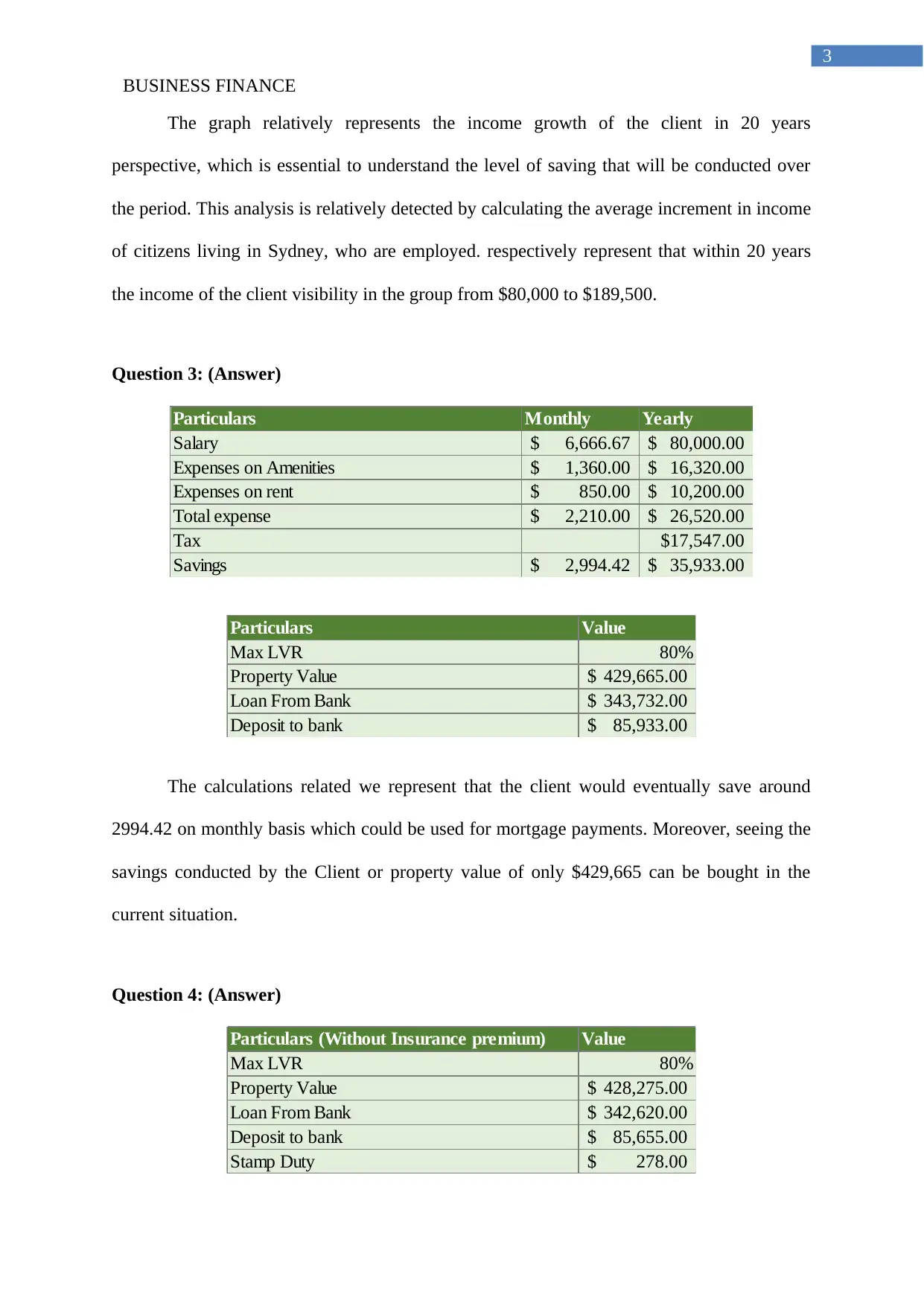

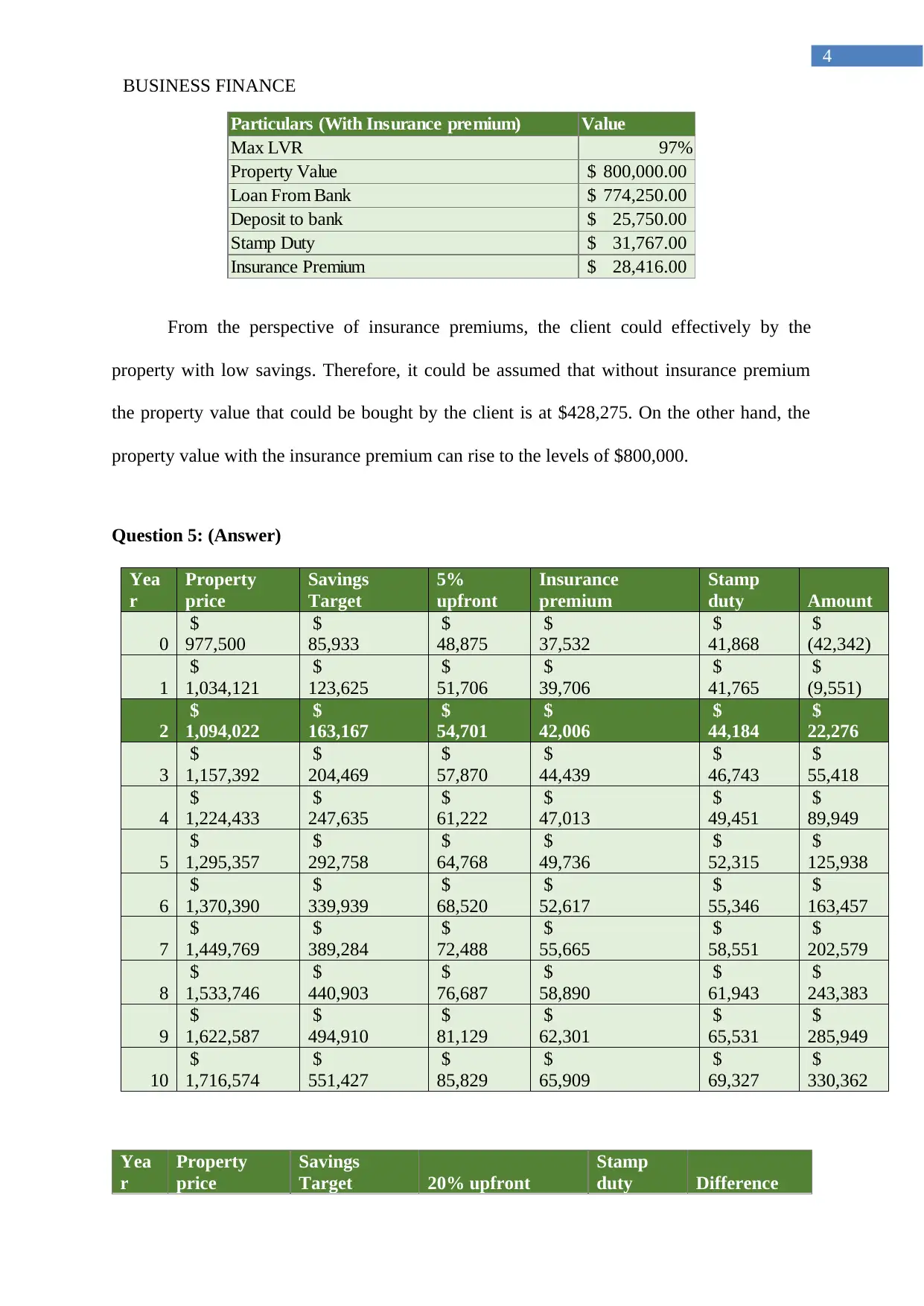

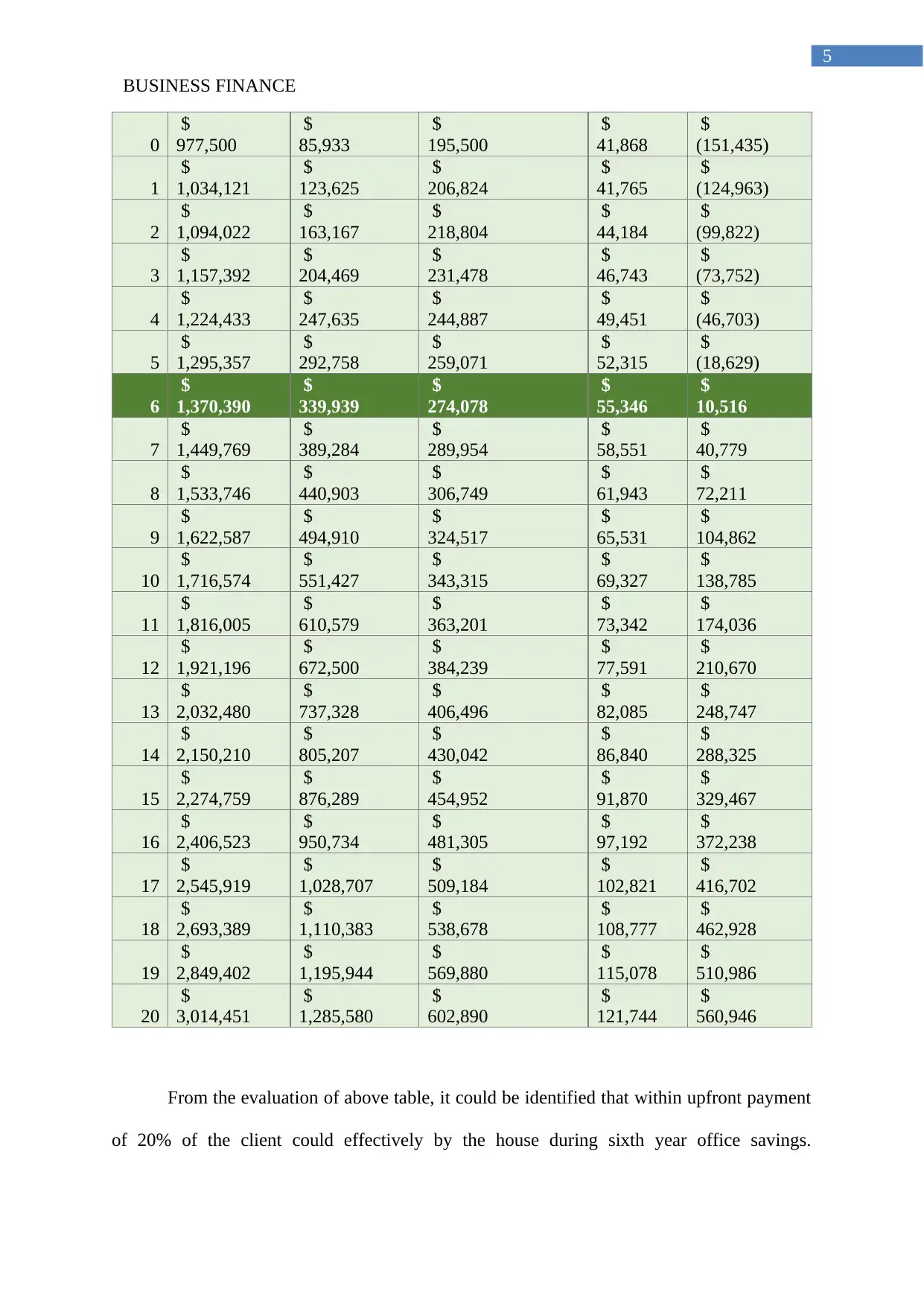

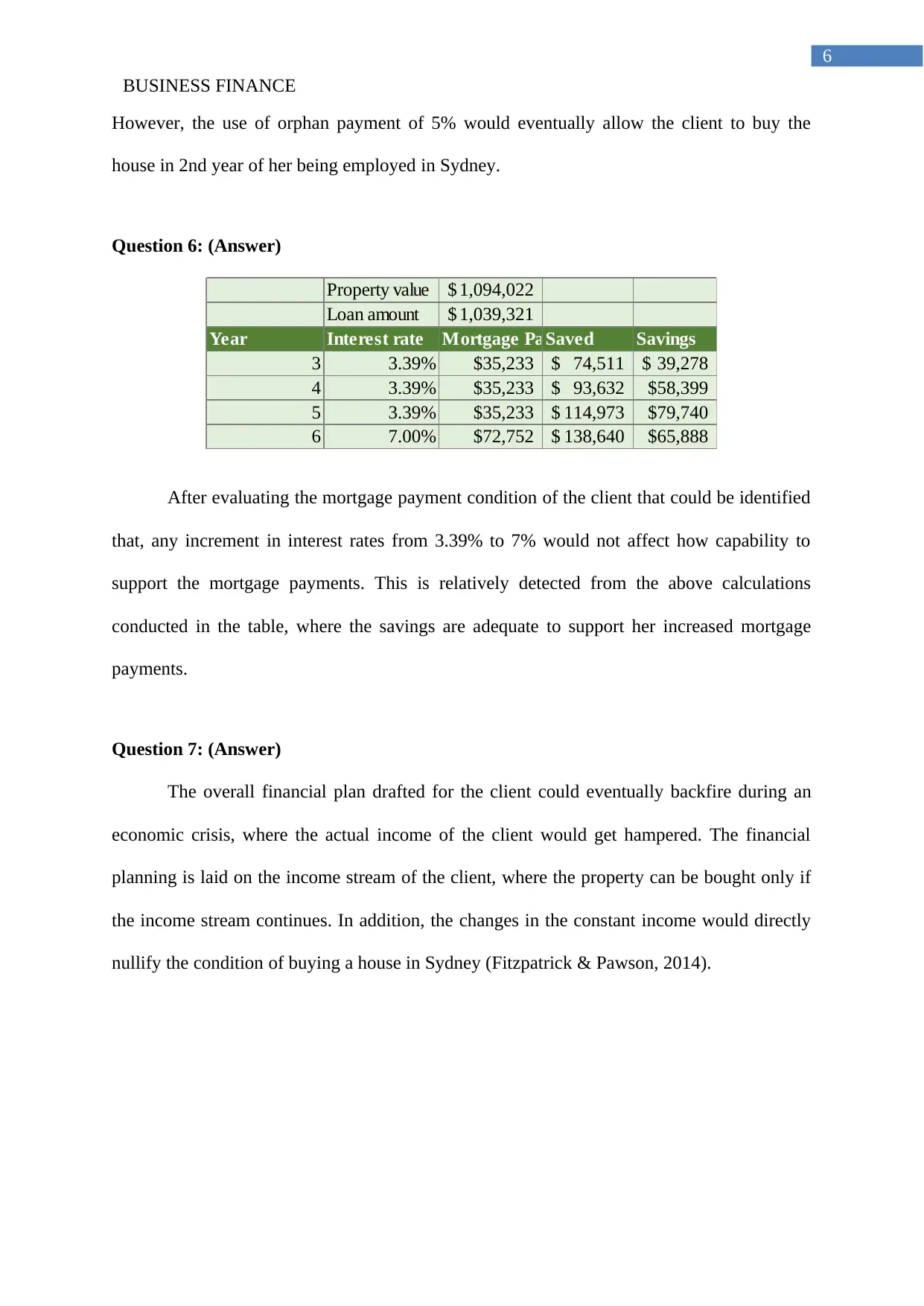

This report outlines a financial plan for a young technical migrant in Sydney aiming to purchase a home within 10 years, despite the high property prices. The plan considers the client's initial savings of $50,000 and an entry salary of $80,000 per year. It includes forecasting property price increases and income growth over the next 20 years, calculating potential savings, and evaluating the impact of insurance premiums on property affordability. The analysis determines the feasibility of buying a home with and without insurance, considering both 5% and 20% upfront payments. Furthermore, the report evaluates mortgage payment conditions and the potential impact of interest rate changes on the client's ability to manage mortgage payments. The plan also acknowledges the risks associated with economic crises that could affect the client's income stream, potentially hindering the home-buying process. This comprehensive financial plan aims to guide the client toward achieving the 'Australian Dream' of homeownership in Sydney, with access to additional resources available on Desklib.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.