Management Accounting Report: Financial Planning, Budgeting, Variances

VerifiedAdded on 2021/05/31

|23

|4241

|267

Report

AI Summary

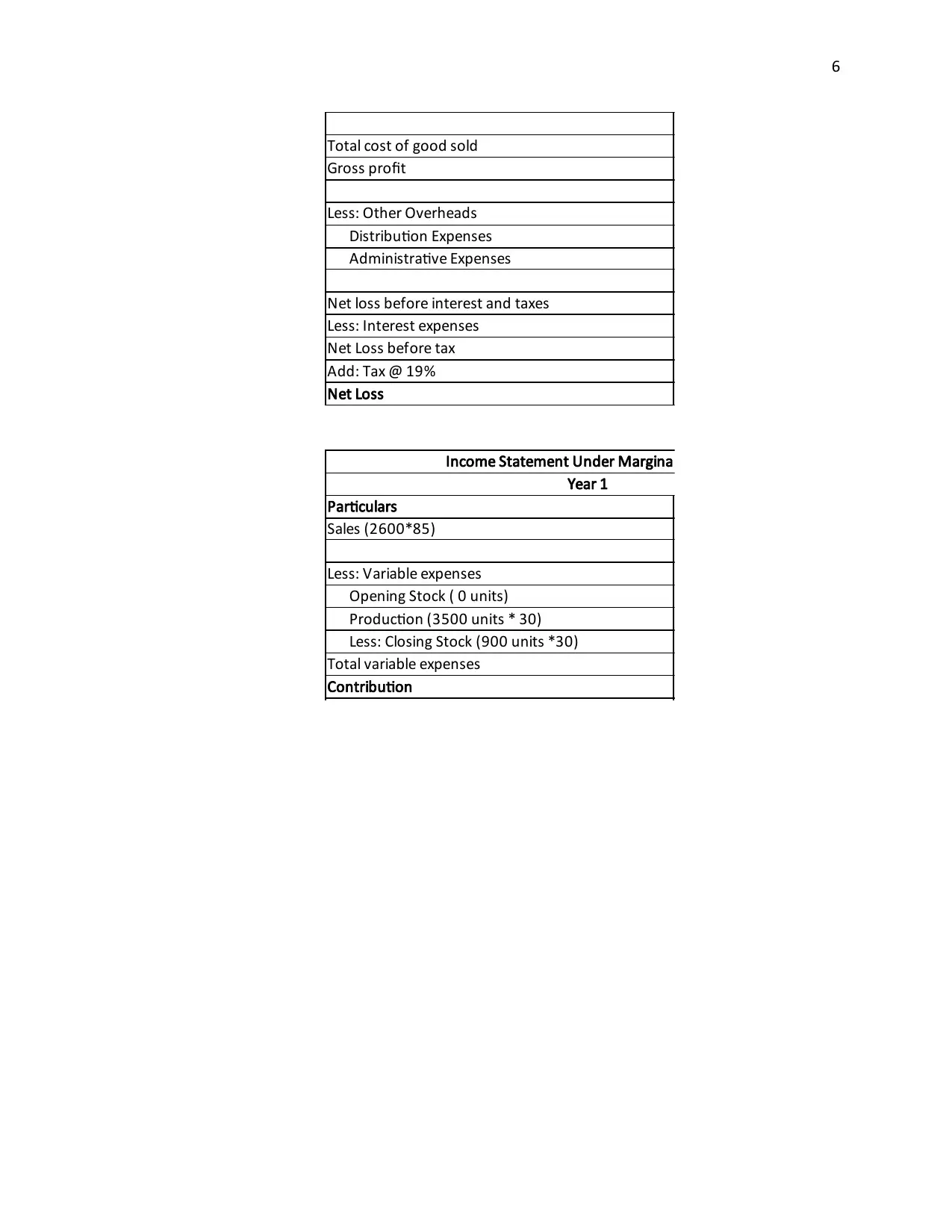

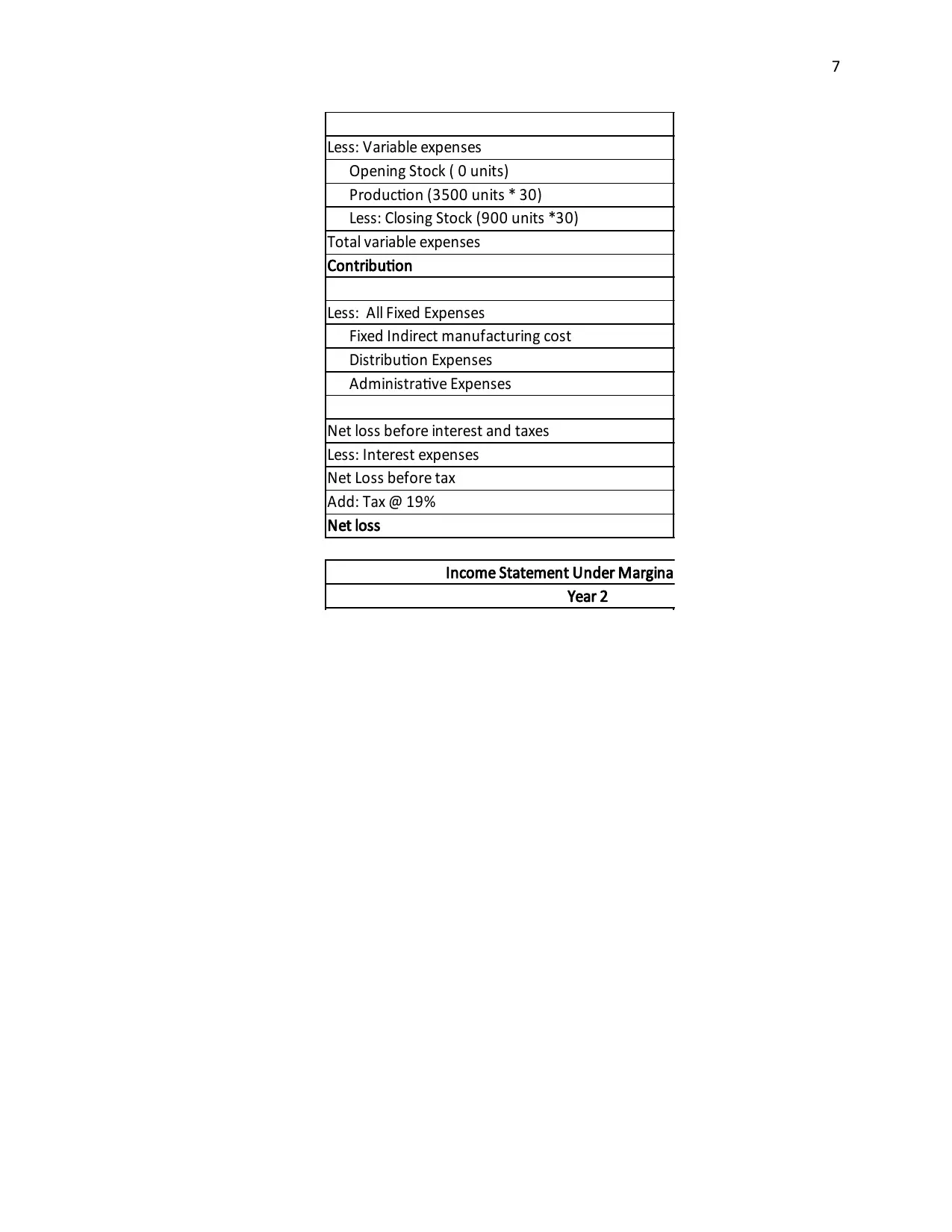

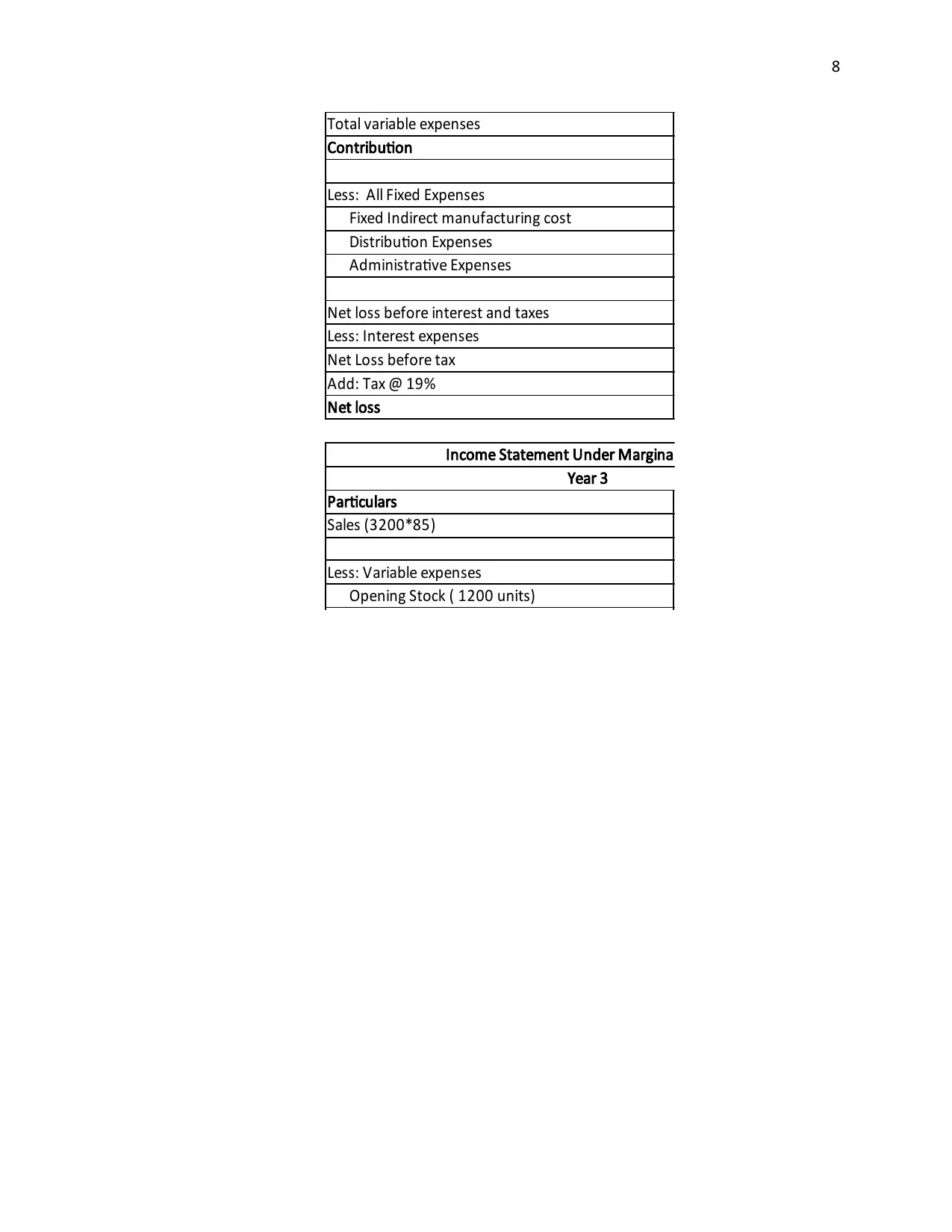

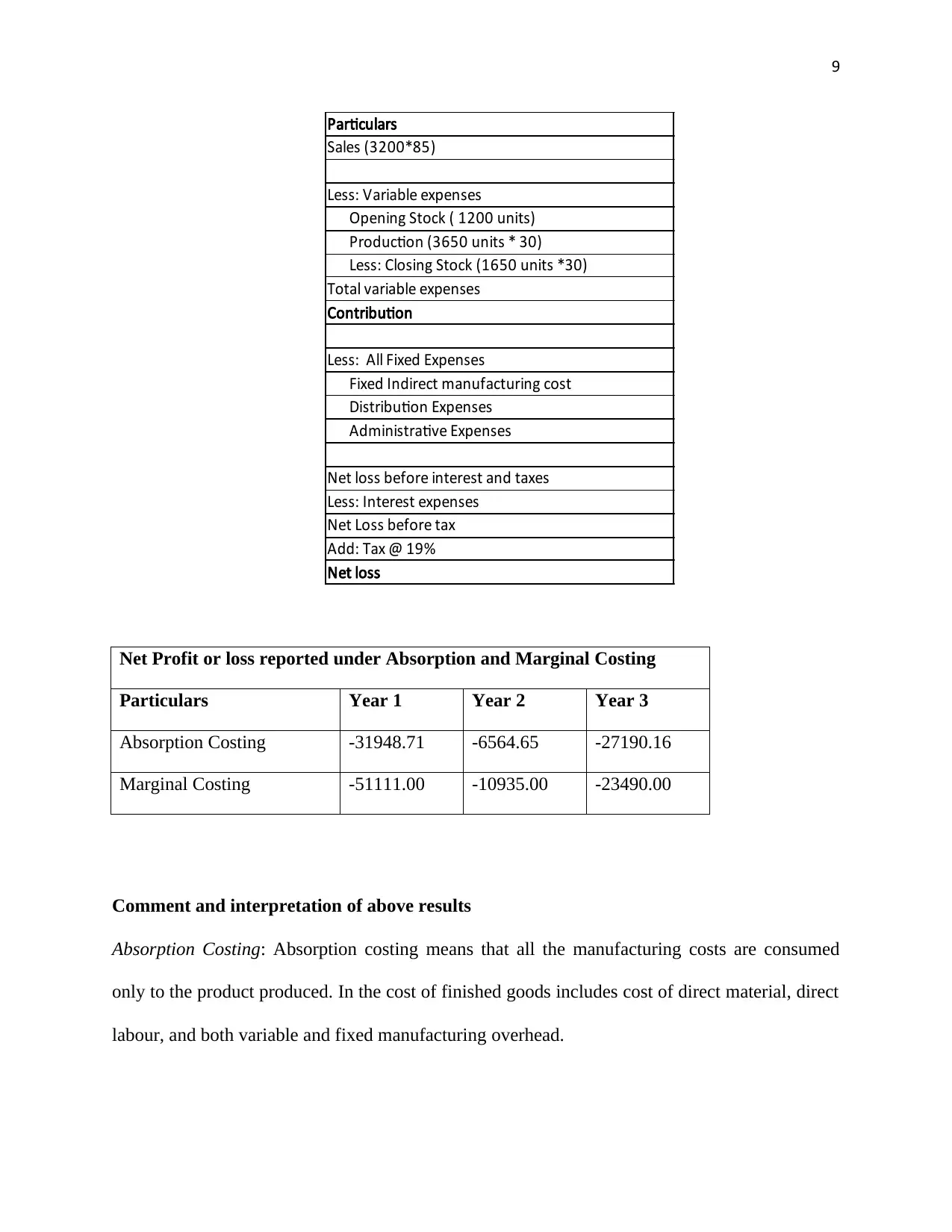

This report, prepared for the NSAB530B5 course, comprehensively examines management accounting principles and their application. It begins with a portfolio of calculations and commentary comparing absorption and marginal costing methods, highlighting their impact on reported profit or loss. The report then delves into budgetary planning tools, including budgets and variance analysis, discussing their advantages and disadvantages. It further explores the adoption of management accounting systems by organizations to address financial challenges, tracing the evolution of these systems from cost identification to strategic decision-making. The report emphasizes the use of management accounting for achieving sustainable success and provides insights into employing accounting planning tools to effectively resolve organizational financial issues. It covers a range of topics including sales, purchase, and cash flow budgets, and the importance of variance analysis in identifying and correcting deviations from planned performance, all supported by relevant references.

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.