Monarch Institute DFP Module 1 Assignment: Risk Profile and Allocation

VerifiedAdded on 2020/04/01

|40

|11411

|632

Homework Assignment

AI Summary

This assignment is for the Diploma of Financial Planning Module 1 and focuses on the foundations of the financial planning process. It includes a simulation exercise where the student completes a client risk profile using a questionnaire adapted from RBS Morgans Ltd. Based on the client's responses and the resulting risk profile (assertive), the student recommends an asset allocation strategy, specifying the percentage of income (cash and fixed interest) and growth assets (shares and property). The assignment also explores general versus personal financial advice, the Financial Service Guide (FSG), client questionnaires, and file notes. Additional topics covered include Australian Privacy Principles, managing client complaints, the Financial Ombudsman Service (FOS), identifying financial and non-financial goals, budgeting, advice strategies to promote a cash surplus, scaled advice, the best interests duty, different types of financial advice documents (SOA, Scaled Advice, execution-only instructions), and the Australian economy's influence on investment markets. The assignment is graded as either "competent" or "not-yet-competent" and aligns with the Australian Qualifications Framework. Students are given one opportunity to resubmit if deemed "not-yet-competent".

DFP Module 1 Assignment 1509

Diploma of Financial Planning

Module 1 Assignment

Submission Instructions:

Key steps that must be followed:

1. Please complete the Declaration of Authenticity at the bottom of this page.

2. Once you have completed all parts of the assessment and saved it (eg. to your desktop

computer), login to the Monarch Learning Management System (LMS) to submit your

assessment.

3. In the LMS, click on the file ”Submit DFP Module 1 Assignment” in the Module 1

section of your course and upload your assessment file/s by following the prompts.

4. Please be sure to click “Continue” after clicking “submit”.This ensures your assessor

receives notification – very important!

Declaration of Understanding and Authenticity*

I have read and understood the assessment instructions provided to me in the Learning Management System.

I certify that the attached material is my original work. No other person’s work hasbeen used without due

acknowledgement. I understandthat the work submitted may be reproduced and/or communicated for the purpose

of detecting plagiarism.

Student Name*: Date:

* I understand that by typing my name or inserting a digital signature into this box that I agree and am bound by the

above student declaration.

Rupinder Kaur

Diploma of Financial Planning

Module 1 Assignment

Submission Instructions:

Key steps that must be followed:

1. Please complete the Declaration of Authenticity at the bottom of this page.

2. Once you have completed all parts of the assessment and saved it (eg. to your desktop

computer), login to the Monarch Learning Management System (LMS) to submit your

assessment.

3. In the LMS, click on the file ”Submit DFP Module 1 Assignment” in the Module 1

section of your course and upload your assessment file/s by following the prompts.

4. Please be sure to click “Continue” after clicking “submit”.This ensures your assessor

receives notification – very important!

Declaration of Understanding and Authenticity*

I have read and understood the assessment instructions provided to me in the Learning Management System.

I certify that the attached material is my original work. No other person’s work hasbeen used without due

acknowledgement. I understandthat the work submitted may be reproduced and/or communicated for the purpose

of detecting plagiarism.

Student Name*: Date:

* I understand that by typing my name or inserting a digital signature into this box that I agree and am bound by the

above student declaration.

Rupinder Kaur

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DFP Module 1 Assignment 1509

Important assessment information

Aims of this assessment

This assessment covers the foundations of the financial planning process. It requires completion

of a client risk profile, with a target asset allocation being assigned based on the data extracted.

General advice is contrasted to personal advice, with skill related assessments ensuring formal

procedures are followed in the advice process. These include the provision of a Financial Service

Guide (FSG), a client questionnaire being completed, as well as a risk profile, and first

appointment file note being completed. Australian Privacy Principle obligations are explored in a

client specific scenario. Managing potential client complaints is addressed, as is the Financial

Ombudsman Service (FOS), including how complaints are managed within the FOS. The need to

understand a client situation is fully explored. This includes identifying financial and non-financial

goals including allocating appropriate time frames to them. Completion of a comprehensive

budget is addressed. Based on this completed budget, advice strategies that promote a cash

surplus, including strategies to manage cash deficits (if applicable) are explored. Scaled advice and

the best interests duty is a focus. The documentary areas of financial advice are covered including

the differences between a comprehensive Statement of Advice (SOA), a Scaled Advice document,

and execution-only instructions. The Australian economy is addressed, including how it influences

investment markets within different cycles. Monetary policy and fiscal policy, among other key

economic policy areas is addressed.

Marking and feedback

This assignment contains 7 assessment activities each containing specific instructions.

This particular assessment forms part of your overall assessment for the following units of

competency:

FNSCUS505

FNSCUS506

FNSFPL501

FNSIAD501

FNSFPL505

Grading for this assessment will be deemed “competent” or “not-yet-competent” in line with

specified educational standards under the Australian Qualifications Framework.

Units: FNSCUS505, FNSCUS506, FNSFPL501, FNSIAD501, FNSFPL505

Important assessment information

Aims of this assessment

This assessment covers the foundations of the financial planning process. It requires completion

of a client risk profile, with a target asset allocation being assigned based on the data extracted.

General advice is contrasted to personal advice, with skill related assessments ensuring formal

procedures are followed in the advice process. These include the provision of a Financial Service

Guide (FSG), a client questionnaire being completed, as well as a risk profile, and first

appointment file note being completed. Australian Privacy Principle obligations are explored in a

client specific scenario. Managing potential client complaints is addressed, as is the Financial

Ombudsman Service (FOS), including how complaints are managed within the FOS. The need to

understand a client situation is fully explored. This includes identifying financial and non-financial

goals including allocating appropriate time frames to them. Completion of a comprehensive

budget is addressed. Based on this completed budget, advice strategies that promote a cash

surplus, including strategies to manage cash deficits (if applicable) are explored. Scaled advice and

the best interests duty is a focus. The documentary areas of financial advice are covered including

the differences between a comprehensive Statement of Advice (SOA), a Scaled Advice document,

and execution-only instructions. The Australian economy is addressed, including how it influences

investment markets within different cycles. Monetary policy and fiscal policy, among other key

economic policy areas is addressed.

Marking and feedback

This assignment contains 7 assessment activities each containing specific instructions.

This particular assessment forms part of your overall assessment for the following units of

competency:

FNSCUS505

FNSCUS506

FNSFPL501

FNSIAD501

FNSFPL505

Grading for this assessment will be deemed “competent” or “not-yet-competent” in line with

specified educational standards under the Australian Qualifications Framework.

Units: FNSCUS505, FNSCUS506, FNSFPL501, FNSIAD501, FNSFPL505

DFP Module 1 Assignment 1509

What does “competent” mean?

These answers contain relevant and accurate information in response to the question/s with

limited serious errors in fact or application. If incorrect information is contained in an answer, it

must be fundamentally outweighed by the accurate information provided. This will be assessed

against a marking guide provided to assessors for their determination.

What does “not-yet-competent” mean?

This occurs when an assessment does not meet the marking guide standards provided to

assessors. These answers either do not address the question specifically, or are wrong from a

legislative perspective, or are incorrectly applied. Answers that omit to provide a response to any

significant issue (where multiple issues must be addressed in a question) may also be deemed

not-yet-competent. Answers that have faulty reasoning, a poor standard of expression or include

plagiarism may also be deemed not-yet-competent. Please note, additional information regarding

Monarch’s plagiarism policy is contained in the Student Information Guide which can be found

here: http://www.monarch.edu.au/student-info/

What happens if you are deemed not-yet-competent?

In the event you do not achieve competency by your assessor on this assessment, you will be

given one more opportunity to re-submit the assessment after consultation with your Trainer/

Assessor. You will know your assessment is deemed ‘not-yet-competent’ if your grade book in the

Monarch LMS says “NYC” after you have received an email from your assessor advising your

assessment has been graded.

Important: It is your responsibility to ensure your assessment resubmission addresses all areas

deemed unsatisfactory by your assessor. Please note, if you are still unsuccessful in meeting

competency after resubmitting your assessment, you will be required to repeat those units.

In the event that you have concerns about the assessment decision then you can refer to our

Complaints & Appeals process also contained within the Student Information Guide.

Expectations from your assessor when answering different types of assessment questions

Knowledge based questions:

A knowledge based question requires you to clearly identify and cover the key subject matter

areas raised in the question in full as part of the response.

Skill based questions:

Where you are asked to write as though you are speaking to a client, your answers must show

your ability to:

understand your client’s concerns/perspective/views

Units: FNSCUS505, FNSCUS506, FNSFPL501, FNSIAD501, FNSFPL505

What does “competent” mean?

These answers contain relevant and accurate information in response to the question/s with

limited serious errors in fact or application. If incorrect information is contained in an answer, it

must be fundamentally outweighed by the accurate information provided. This will be assessed

against a marking guide provided to assessors for their determination.

What does “not-yet-competent” mean?

This occurs when an assessment does not meet the marking guide standards provided to

assessors. These answers either do not address the question specifically, or are wrong from a

legislative perspective, or are incorrectly applied. Answers that omit to provide a response to any

significant issue (where multiple issues must be addressed in a question) may also be deemed

not-yet-competent. Answers that have faulty reasoning, a poor standard of expression or include

plagiarism may also be deemed not-yet-competent. Please note, additional information regarding

Monarch’s plagiarism policy is contained in the Student Information Guide which can be found

here: http://www.monarch.edu.au/student-info/

What happens if you are deemed not-yet-competent?

In the event you do not achieve competency by your assessor on this assessment, you will be

given one more opportunity to re-submit the assessment after consultation with your Trainer/

Assessor. You will know your assessment is deemed ‘not-yet-competent’ if your grade book in the

Monarch LMS says “NYC” after you have received an email from your assessor advising your

assessment has been graded.

Important: It is your responsibility to ensure your assessment resubmission addresses all areas

deemed unsatisfactory by your assessor. Please note, if you are still unsuccessful in meeting

competency after resubmitting your assessment, you will be required to repeat those units.

In the event that you have concerns about the assessment decision then you can refer to our

Complaints & Appeals process also contained within the Student Information Guide.

Expectations from your assessor when answering different types of assessment questions

Knowledge based questions:

A knowledge based question requires you to clearly identify and cover the key subject matter

areas raised in the question in full as part of the response.

Skill based questions:

Where you are asked to write as though you are speaking to a client, your answers must show

your ability to:

understand your client’s concerns/perspective/views

Units: FNSCUS505, FNSCUS506, FNSFPL501, FNSIAD501, FNSFPL505

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DFP Module 1 Assignment 1509

show empathy

display a professional response

explain ideas clearly and simply so your client can understand the issues

Good luck

Finally, good luck with your learning and assessments and remember your trainers are here to

assist you

Units: FNSCUS505, FNSCUS506, FNSFPL501, FNSIAD501, FNSFPL505

show empathy

display a professional response

explain ideas clearly and simply so your client can understand the issues

Good luck

Finally, good luck with your learning and assessments and remember your trainers are here to

assist you

Units: FNSCUS505, FNSCUS506, FNSFPL501, FNSIAD501, FNSFPL505

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DFP Module 1 Assignment 1509

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all 3 questions that follow.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the front of this assessment

Estimated time for completion of this assessment activity: 1 hour

Units: FNSCUS505, FNSCUS506, FNSFPL501, FNSIAD501, FNSFPL505

Assessment Activity 1

Simulation Exercise

Risk Profile

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all 3 questions that follow.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the front of this assessment

Estimated time for completion of this assessment activity: 1 hour

Units: FNSCUS505, FNSCUS506, FNSFPL501, FNSIAD501, FNSFPL505

Assessment Activity 1

Simulation Exercise

Risk Profile

DFP Module 1 Assignment 1509

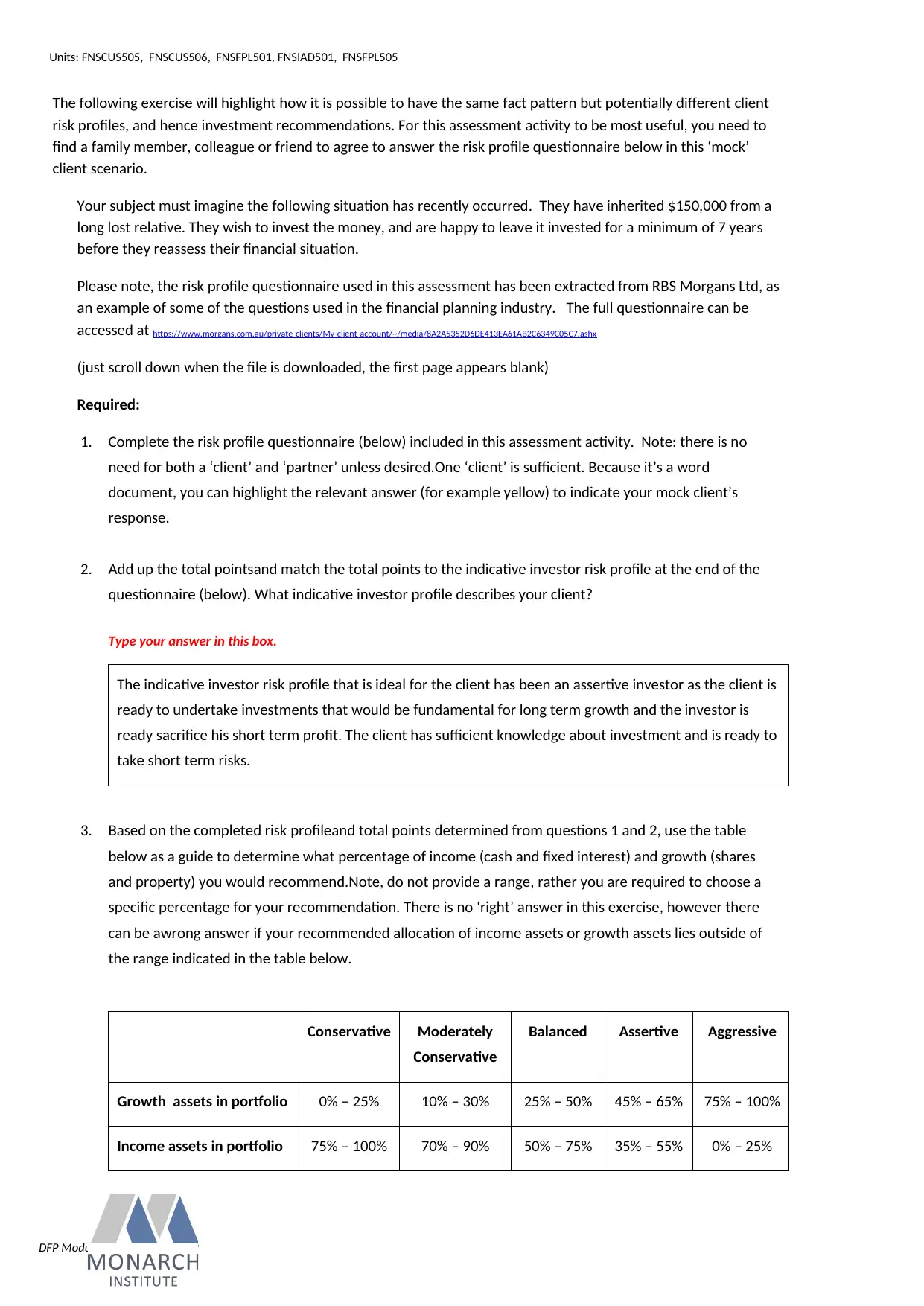

The following exercise will highlight how it is possible to have the same fact pattern but potentially different client

risk profiles, and hence investment recommendations. For this assessment activity to be most useful, you need to

find a family member, colleague or friend to agree to answer the risk profile questionnaire below in this ‘mock’

client scenario.

Your subject must imagine the following situation has recently occurred. They have inherited $150,000 from a

long lost relative. They wish to invest the money, and are happy to leave it invested for a minimum of 7 years

before they reassess their financial situation.

Please note, the risk profile questionnaire used in this assessment has been extracted from RBS Morgans Ltd, as

an example of some of the questions used in the financial planning industry. The full questionnaire can be

accessed at https://www.morgans.com.au/private-clients/My-client-account/~/media/8A2A5352D6DE413EA61AB2C6349C05C7.ashx

(just scroll down when the file is downloaded, the first page appears blank)

Required:

1. Complete the risk profile questionnaire (below) included in this assessment activity. Note: there is no

need for both a ‘client’ and ‘partner’ unless desired.One ‘client’ is sufficient. Because it’s a word

document, you can highlight the relevant answer (for example yellow) to indicate your mock client’s

response.

2. Add up the total pointsand match the total points to the indicative investor risk profile at the end of the

questionnaire (below). What indicative investor profile describes your client?

Type your answer in this box.

The indicative investor risk profile that is ideal for the client has been an assertive investor as the client is

ready to undertake investments that would be fundamental for long term growth and the investor is

ready sacrifice his short term profit. The client has sufficient knowledge about investment and is ready to

take short term risks.

3. Based on the completed risk profileand total points determined from questions 1 and 2, use the table

below as a guide to determine what percentage of income (cash and fixed interest) and growth (shares

and property) you would recommend.Note, do not provide a range, rather you are required to choose a

specific percentage for your recommendation. There is no ‘right’ answer in this exercise, however there

can be awrong answer if your recommended allocation of income assets or growth assets lies outside of

the range indicated in the table below.

Conservative Moderately

Conservative

Balanced Assertive Aggressive

Growth assets in portfolio 0% – 25% 10% – 30% 25% – 50% 45% – 65% 75% – 100%

Income assets in portfolio 75% – 100% 70% – 90% 50% – 75% 35% – 55% 0% – 25%

Units: FNSCUS505, FNSCUS506, FNSFPL501, FNSIAD501, FNSFPL505

The following exercise will highlight how it is possible to have the same fact pattern but potentially different client

risk profiles, and hence investment recommendations. For this assessment activity to be most useful, you need to

find a family member, colleague or friend to agree to answer the risk profile questionnaire below in this ‘mock’

client scenario.

Your subject must imagine the following situation has recently occurred. They have inherited $150,000 from a

long lost relative. They wish to invest the money, and are happy to leave it invested for a minimum of 7 years

before they reassess their financial situation.

Please note, the risk profile questionnaire used in this assessment has been extracted from RBS Morgans Ltd, as

an example of some of the questions used in the financial planning industry. The full questionnaire can be

accessed at https://www.morgans.com.au/private-clients/My-client-account/~/media/8A2A5352D6DE413EA61AB2C6349C05C7.ashx

(just scroll down when the file is downloaded, the first page appears blank)

Required:

1. Complete the risk profile questionnaire (below) included in this assessment activity. Note: there is no

need for both a ‘client’ and ‘partner’ unless desired.One ‘client’ is sufficient. Because it’s a word

document, you can highlight the relevant answer (for example yellow) to indicate your mock client’s

response.

2. Add up the total pointsand match the total points to the indicative investor risk profile at the end of the

questionnaire (below). What indicative investor profile describes your client?

Type your answer in this box.

The indicative investor risk profile that is ideal for the client has been an assertive investor as the client is

ready to undertake investments that would be fundamental for long term growth and the investor is

ready sacrifice his short term profit. The client has sufficient knowledge about investment and is ready to

take short term risks.

3. Based on the completed risk profileand total points determined from questions 1 and 2, use the table

below as a guide to determine what percentage of income (cash and fixed interest) and growth (shares

and property) you would recommend.Note, do not provide a range, rather you are required to choose a

specific percentage for your recommendation. There is no ‘right’ answer in this exercise, however there

can be awrong answer if your recommended allocation of income assets or growth assets lies outside of

the range indicated in the table below.

Conservative Moderately

Conservative

Balanced Assertive Aggressive

Growth assets in portfolio 0% – 25% 10% – 30% 25% – 50% 45% – 65% 75% – 100%

Income assets in portfolio 75% – 100% 70% – 90% 50% – 75% 35% – 55% 0% – 25%

Units: FNSCUS505, FNSCUS506, FNSFPL501, FNSIAD501, FNSFPL505

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DFP Module 1 Assignment 1509

Your Recommendation The investor is assertive

Growth assets in portfolio 45%-65%

Income assets in portfolio 35-55%

Risk Profile Questionnaire

Identifying your investment risk profile

1. Which of the following best describes your current stage of life?

Single with few financial burdens. Ready to accumulate wealth for future

short term

and long term goals.

(5 points)

a) b) A couple without children. Preparing for the future by establishing a

b) home. Expecting to have or already have a high purchase rate of

c) household and consumer items.

(4 points)

c) Young family with a home. You have a mortgage and childcare costs and

maintain only small cash balances.

(3 points)

d) d) Mature family. You are in your peak earning years and your mortgage is

e) under control. You both work and you may or may not have children that

are growing up or have left home. You’re ready to start thinking about

g) your retirement years.

(5 points)

e) Preparing for retirement. You own your home and have few financial

burdens; you want to ensure you can afford a comfortable retirement.

(2 points)

(5 f) Retired. You rely on existing funds and investments to maintain your

(6 lifestyle in retirement. You may already be receiving a Government

(7 pension and/or Superannuation pension.

(1 point)

2. How familiar are you with investment matters?

a) Not familiar at all with investments and feel uncomfortable with the

complexity.

(0 points)

b) Not very familiar when it comes to investments. (1 point)

c) Somewhat familiar. I don’t fully understand investments, including the

share market.

(2 points)

d) Fairly familiar. I understand the various factors which influence

investment

performance.

(3 points)

e) Very familiar. I use research and other investment information to make

investment decisions. I understand the various factors which influence

investment performance.

(7 points)

Units: FNSCUS505, FNSCUS506, FNSFPL501, FNSIAD501, FNSFPL505

Your Recommendation The investor is assertive

Growth assets in portfolio 45%-65%

Income assets in portfolio 35-55%

Risk Profile Questionnaire

Identifying your investment risk profile

1. Which of the following best describes your current stage of life?

Single with few financial burdens. Ready to accumulate wealth for future

short term

and long term goals.

(5 points)

a) b) A couple without children. Preparing for the future by establishing a

b) home. Expecting to have or already have a high purchase rate of

c) household and consumer items.

(4 points)

c) Young family with a home. You have a mortgage and childcare costs and

maintain only small cash balances.

(3 points)

d) d) Mature family. You are in your peak earning years and your mortgage is

e) under control. You both work and you may or may not have children that

are growing up or have left home. You’re ready to start thinking about

g) your retirement years.

(5 points)

e) Preparing for retirement. You own your home and have few financial

burdens; you want to ensure you can afford a comfortable retirement.

(2 points)

(5 f) Retired. You rely on existing funds and investments to maintain your

(6 lifestyle in retirement. You may already be receiving a Government

(7 pension and/or Superannuation pension.

(1 point)

2. How familiar are you with investment matters?

a) Not familiar at all with investments and feel uncomfortable with the

complexity.

(0 points)

b) Not very familiar when it comes to investments. (1 point)

c) Somewhat familiar. I don’t fully understand investments, including the

share market.

(2 points)

d) Fairly familiar. I understand the various factors which influence

investment

performance.

(3 points)

e) Very familiar. I use research and other investment information to make

investment decisions. I understand the various factors which influence

investment performance.

(7 points)

Units: FNSCUS505, FNSCUS506, FNSFPL501, FNSIAD501, FNSFPL505

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DFP Module 1 Assignment 1509

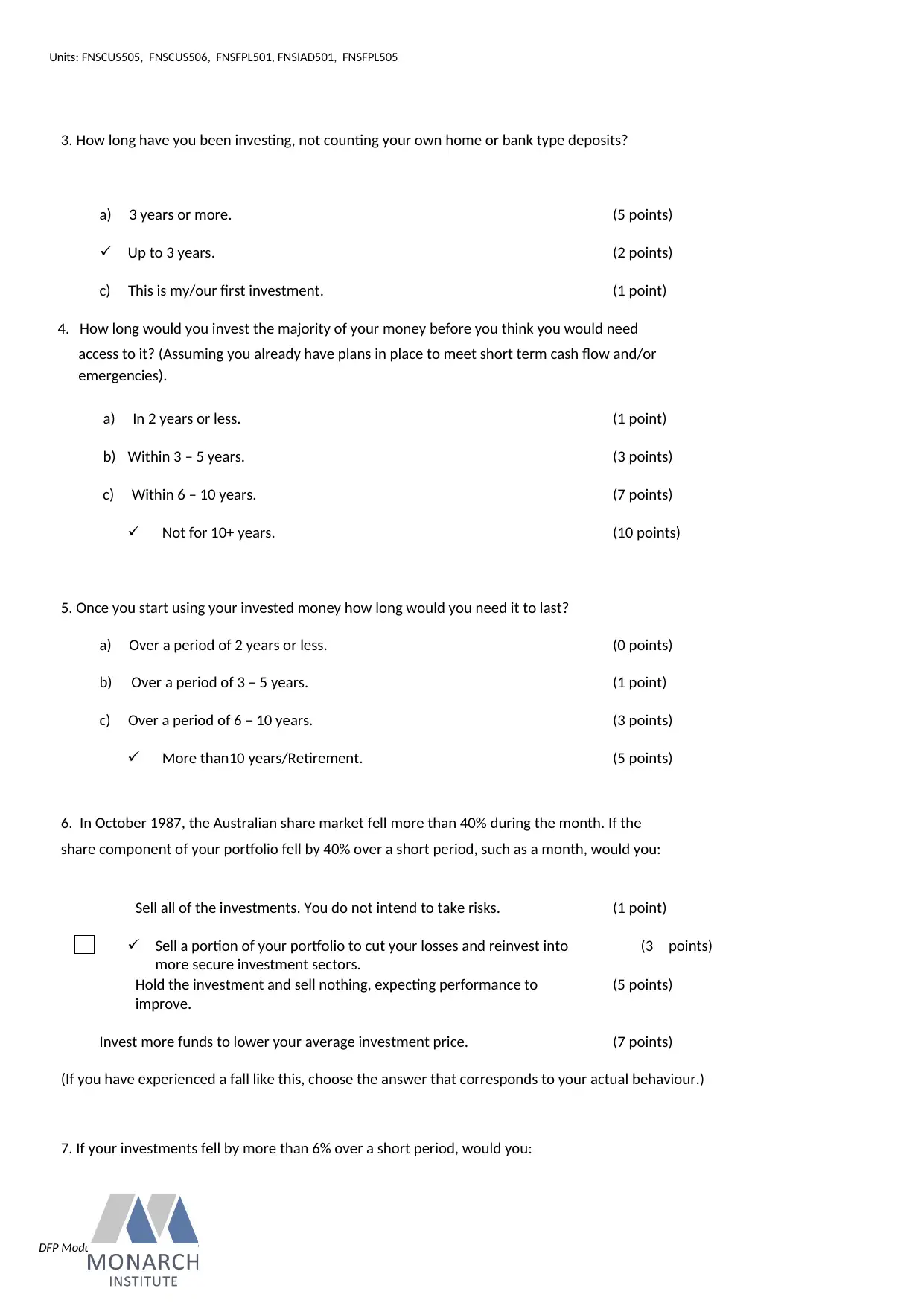

3. How long have you been investing, not counting your own home or bank type deposits?

a) 3 years or more. (5 points)

Up to 3 years. (2 points)

c) This is my/our first investment. (1 point)

4. How long would you invest the majority of your money before you think you would need

access to it? (Assuming you already have plans in place to meet short term cash flow and/or

emergencies).

a) In 2 years or less. (1 point)

b) Within 3 – 5 years. (3 points)

c) Within 6 – 10 years. (7 points)

Not for 10+ years. (10 points)

5. Once you start using your invested money how long would you need it to last?

a) Over a period of 2 years or less. (0 points)

b) Over a period of 3 – 5 years. (1 point)

c) Over a period of 6 – 10 years. (3 points)

More than10 years/Retirement. (5 points)

6. In October 1987, the Australian share market fell more than 40% during the month. If the

share component of your portfolio fell by 40% over a short period, such as a month, would you:

Sell all of the investments. You do not intend to take risks. (1 point)

Sell a portion of your portfolio to cut your losses and reinvest into

more secure investment sectors.

(3 points)

Hold the investment and sell nothing, expecting performance to

improve.

(5 points)

Invest more funds to lower your average investment price. (7 points)

(If you have experienced a fall like this, choose the answer that corresponds to your actual behaviour.)

7. If your investments fell by more than 6% over a short period, would you:

Units: FNSCUS505, FNSCUS506, FNSFPL501, FNSIAD501, FNSFPL505

3. How long have you been investing, not counting your own home or bank type deposits?

a) 3 years or more. (5 points)

Up to 3 years. (2 points)

c) This is my/our first investment. (1 point)

4. How long would you invest the majority of your money before you think you would need

access to it? (Assuming you already have plans in place to meet short term cash flow and/or

emergencies).

a) In 2 years or less. (1 point)

b) Within 3 – 5 years. (3 points)

c) Within 6 – 10 years. (7 points)

Not for 10+ years. (10 points)

5. Once you start using your invested money how long would you need it to last?

a) Over a period of 2 years or less. (0 points)

b) Over a period of 3 – 5 years. (1 point)

c) Over a period of 6 – 10 years. (3 points)

More than10 years/Retirement. (5 points)

6. In October 1987, the Australian share market fell more than 40% during the month. If the

share component of your portfolio fell by 40% over a short period, such as a month, would you:

Sell all of the investments. You do not intend to take risks. (1 point)

Sell a portion of your portfolio to cut your losses and reinvest into

more secure investment sectors.

(3 points)

Hold the investment and sell nothing, expecting performance to

improve.

(5 points)

Invest more funds to lower your average investment price. (7 points)

(If you have experienced a fall like this, choose the answer that corresponds to your actual behaviour.)

7. If your investments fell by more than 6% over a short period, would you:

Units: FNSCUS505, FNSCUS506, FNSFPL501, FNSIAD501, FNSFPL505

DFP Module 1 Assignment 1509

Sell all of the remaining investment. (1 point)

Sell a portion of the remaining investment. (3 points)

Hold your investments and sell nothing. (5 points)

Invest more funds. You can tolerate short term losses in expectation of

future growth.

(6 points)

(If your portfolio has experienced a drop like this, choose the answer that corresponds to your actual

behaviour.)

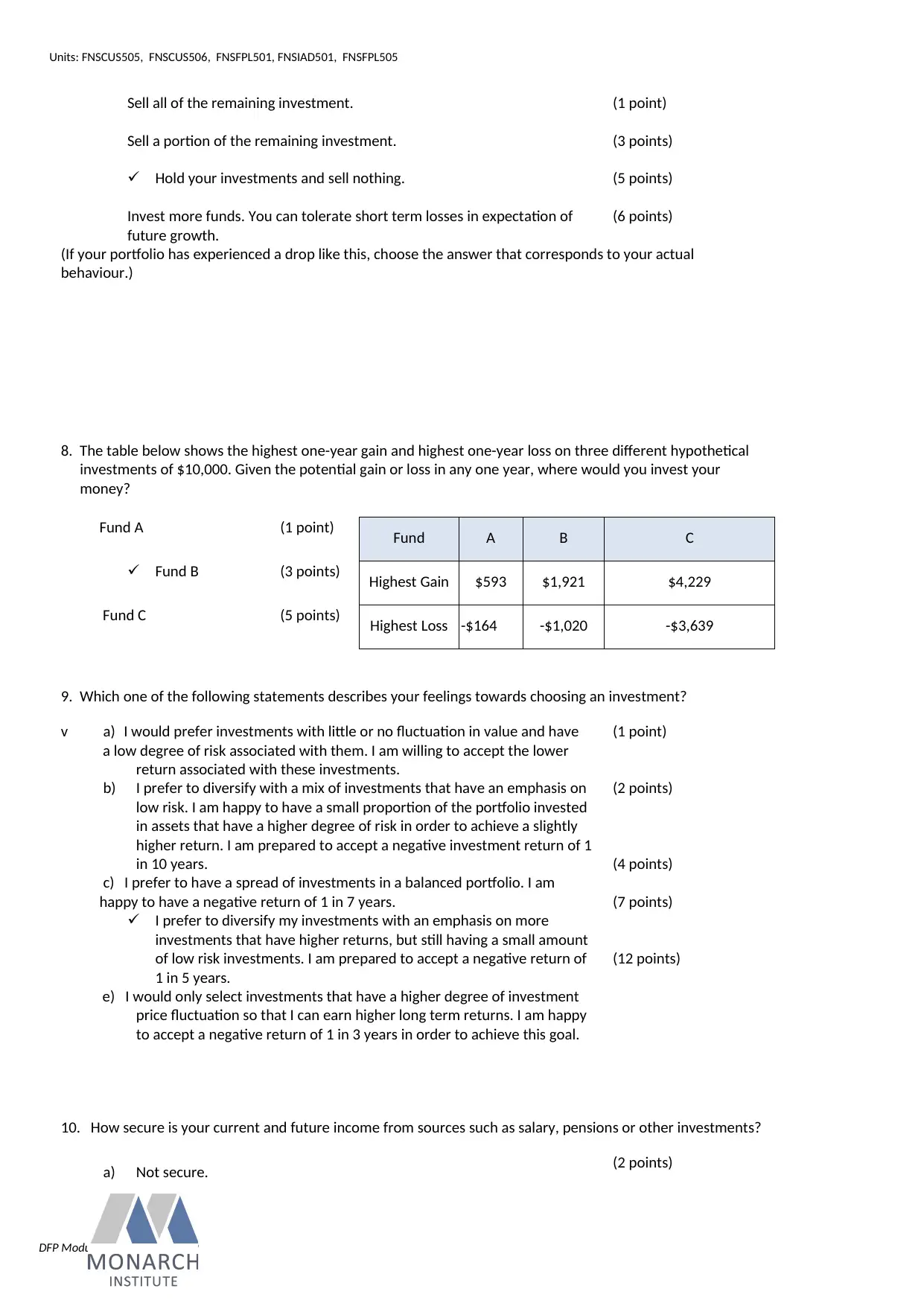

8. The table below shows the highest one-year gain and highest one-year loss on three different hypothetical

investments of $10,000. Given the potential gain or loss in any one year, where would you invest your

money?

Fund A (1 point) Fund A B C

Fund B (3 points) Highest Gain $593 $1,921 $4,229

Fund C (5 points) Highest Loss -$164 -$1,020 -$3,639

9. Which one of the following statements describes your feelings towards choosing an investment?

v a) I would prefer investments with little or no fluctuation in value and have

a low degree of risk associated with them. I am willing to accept the lower

return associated with these investments.

b) I prefer to diversify with a mix of investments that have an emphasis on

low risk. I am happy to have a small proportion of the portfolio invested

in assets that have a higher degree of risk in order to achieve a slightly

higher return. I am prepared to accept a negative investment return of 1

in 10 years.

c) I prefer to have a spread of investments in a balanced portfolio. I am

happy to have a negative return of 1 in 7 years.

I prefer to diversify my investments with an emphasis on more

investments that have higher returns, but still having a small amount

of low risk investments. I am prepared to accept a negative return of

1 in 5 years.

e) I would only select investments that have a higher degree of investment

price fluctuation so that I can earn higher long term returns. I am happy

to accept a negative return of 1 in 3 years in order to achieve this goal.

(1 point)

(2 points)

(4 points)

(7 points)

(12 points)

10. How secure is your current and future income from sources such as salary, pensions or other investments?

a) Not secure. (2 points)

Units: FNSCUS505, FNSCUS506, FNSFPL501, FNSIAD501, FNSFPL505

Sell all of the remaining investment. (1 point)

Sell a portion of the remaining investment. (3 points)

Hold your investments and sell nothing. (5 points)

Invest more funds. You can tolerate short term losses in expectation of

future growth.

(6 points)

(If your portfolio has experienced a drop like this, choose the answer that corresponds to your actual

behaviour.)

8. The table below shows the highest one-year gain and highest one-year loss on three different hypothetical

investments of $10,000. Given the potential gain or loss in any one year, where would you invest your

money?

Fund A (1 point) Fund A B C

Fund B (3 points) Highest Gain $593 $1,921 $4,229

Fund C (5 points) Highest Loss -$164 -$1,020 -$3,639

9. Which one of the following statements describes your feelings towards choosing an investment?

v a) I would prefer investments with little or no fluctuation in value and have

a low degree of risk associated with them. I am willing to accept the lower

return associated with these investments.

b) I prefer to diversify with a mix of investments that have an emphasis on

low risk. I am happy to have a small proportion of the portfolio invested

in assets that have a higher degree of risk in order to achieve a slightly

higher return. I am prepared to accept a negative investment return of 1

in 10 years.

c) I prefer to have a spread of investments in a balanced portfolio. I am

happy to have a negative return of 1 in 7 years.

I prefer to diversify my investments with an emphasis on more

investments that have higher returns, but still having a small amount

of low risk investments. I am prepared to accept a negative return of

1 in 5 years.

e) I would only select investments that have a higher degree of investment

price fluctuation so that I can earn higher long term returns. I am happy

to accept a negative return of 1 in 3 years in order to achieve this goal.

(1 point)

(2 points)

(4 points)

(7 points)

(12 points)

10. How secure is your current and future income from sources such as salary, pensions or other investments?

a) Not secure. (2 points)

Units: FNSCUS505, FNSCUS506, FNSFPL501, FNSIAD501, FNSFPL505

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DFP Module 1 Assignment 1509

b) Somewhat secure. (3 points)

Fairly secure.

d) Very secure

(4 points)

(5 points)

Units: FNSCUS505, FNSCUS506, FNSFPL501, FNSIAD501, FNSFPL505

b) Somewhat secure. (3 points)

Fairly secure.

d) Very secure

(4 points)

(5 points)

Units: FNSCUS505, FNSCUS506, FNSFPL501, FNSIAD501, FNSFPL505

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DFP Module 1 Assignment 1509

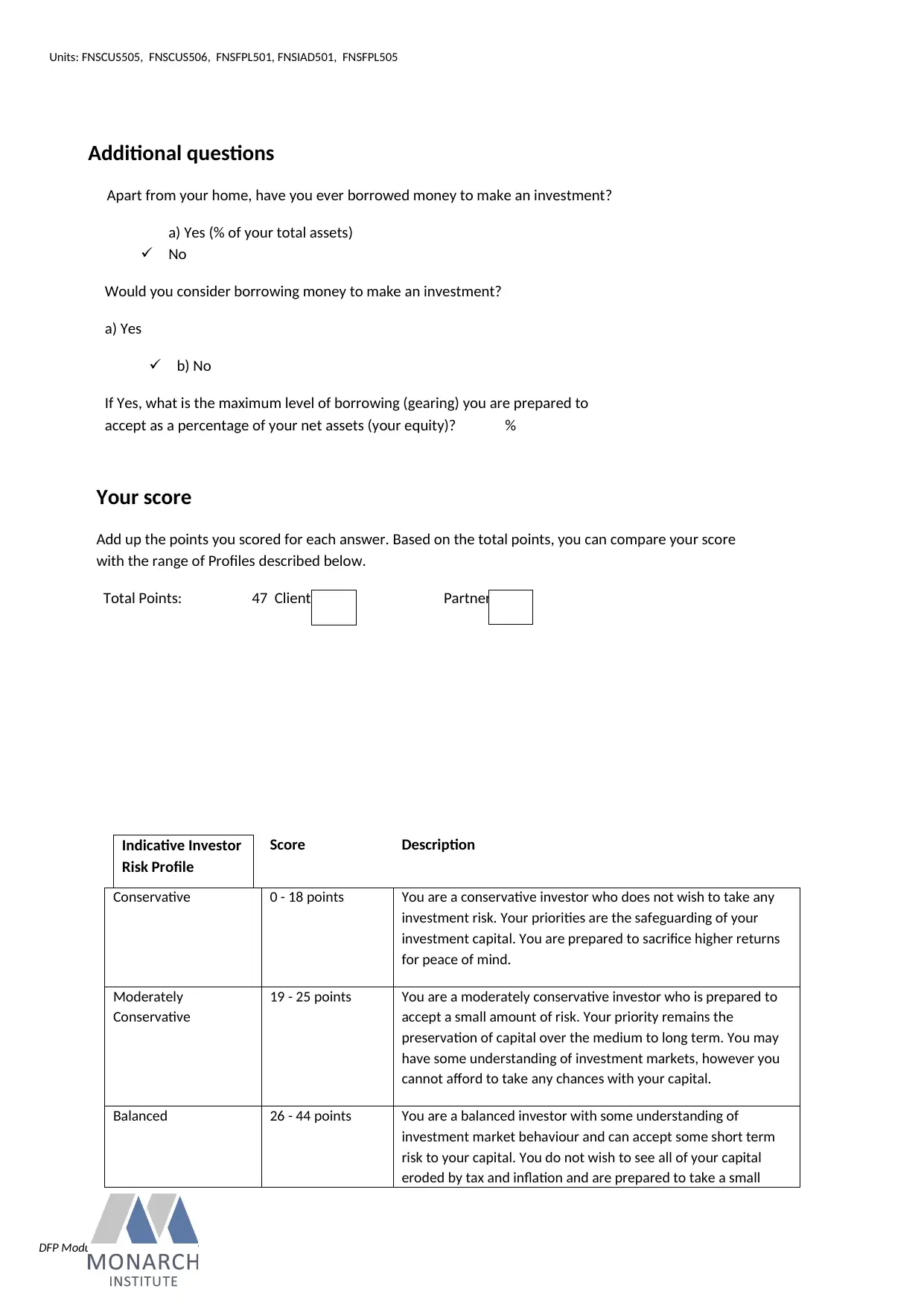

Additional questions

Apart from your home, have you ever borrowed money to make an investment?

a) Yes (% of your total assets)

No

Would you consider borrowing money to make an investment?

a) Yes

b) No

If Yes, what is the maximum level of borrowing (gearing) you are prepared to

accept as a percentage of your net assets (your equity)? %

Your score

Add up the points you scored for each answer. Based on the total points, you can compare your score

with the range of Profiles described below.

Total Points: 47 Client Partner

Indicative Investor

Risk Profile

Score Description

Conservative 0 - 18 points You are a conservative investor who does not wish to take any

investment risk. Your priorities are the safeguarding of your

investment capital. You are prepared to sacrifice higher returns

for peace of mind.

Moderately

Conservative

19 - 25 points You are a moderately conservative investor who is prepared to

accept a small amount of risk. Your priority remains the

preservation of capital over the medium to long term. You may

have some understanding of investment markets, however you

cannot afford to take any chances with your capital.

Balanced 26 - 44 points You are a balanced investor with some understanding of

investment market behaviour and can accept some short term

risk to your capital. You do not wish to see all of your capital

eroded by tax and inflation and are prepared to take a small

Units: FNSCUS505, FNSCUS506, FNSFPL501, FNSIAD501, FNSFPL505

Additional questions

Apart from your home, have you ever borrowed money to make an investment?

a) Yes (% of your total assets)

No

Would you consider borrowing money to make an investment?

a) Yes

b) No

If Yes, what is the maximum level of borrowing (gearing) you are prepared to

accept as a percentage of your net assets (your equity)? %

Your score

Add up the points you scored for each answer. Based on the total points, you can compare your score

with the range of Profiles described below.

Total Points: 47 Client Partner

Indicative Investor

Risk Profile

Score Description

Conservative 0 - 18 points You are a conservative investor who does not wish to take any

investment risk. Your priorities are the safeguarding of your

investment capital. You are prepared to sacrifice higher returns

for peace of mind.

Moderately

Conservative

19 - 25 points You are a moderately conservative investor who is prepared to

accept a small amount of risk. Your priority remains the

preservation of capital over the medium to long term. You may

have some understanding of investment markets, however you

cannot afford to take any chances with your capital.

Balanced 26 - 44 points You are a balanced investor with some understanding of

investment market behaviour and can accept some short term

risk to your capital. You do not wish to see all of your capital

eroded by tax and inflation and are prepared to take a small

Units: FNSCUS505, FNSCUS506, FNSFPL501, FNSIAD501, FNSFPL505

DFP Module 1 Assignment 1509

short term risk in order to gain longer term capital growth.

Assertive 45 - 55 points You are an assertive investor who understands the movement of

investment markets. You are most interested in maximising long

term capital growth, although you do not wish to make

unbalanced investment decisions. You are happy to sacrifice

short term safety in order to maximise long term capital growth.

Aggressive 56+ points You are an aggressive investor. You are prepared to sacrifice

your investment capital in pursuit of the highest long term

capital growth investment. You are most interested in reducing

your taxable income and have an understanding of the

behaviour of investment markets.

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all 5 questions that follow.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the front of this assessment

Estimated time for completion of this assessment activity: 1 hour

Units: FNSCUS505, FNSCUS506, FNSFPL501, FNSIAD501, FNSFPL505

Assessment Activity 2

Simulation Exercise

Regulations & Legislation

short term risk in order to gain longer term capital growth.

Assertive 45 - 55 points You are an assertive investor who understands the movement of

investment markets. You are most interested in maximising long

term capital growth, although you do not wish to make

unbalanced investment decisions. You are happy to sacrifice

short term safety in order to maximise long term capital growth.

Aggressive 56+ points You are an aggressive investor. You are prepared to sacrifice

your investment capital in pursuit of the highest long term

capital growth investment. You are most interested in reducing

your taxable income and have an understanding of the

behaviour of investment markets.

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all 5 questions that follow.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the front of this assessment

Estimated time for completion of this assessment activity: 1 hour

Units: FNSCUS505, FNSCUS506, FNSFPL501, FNSIAD501, FNSFPL505

Assessment Activity 2

Simulation Exercise

Regulations & Legislation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 40

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.