Financial Planning Assignment: RESP, TFSA, and Retirement

VerifiedAdded on 2022/09/26

|3

|1067

|17

Project

AI Summary

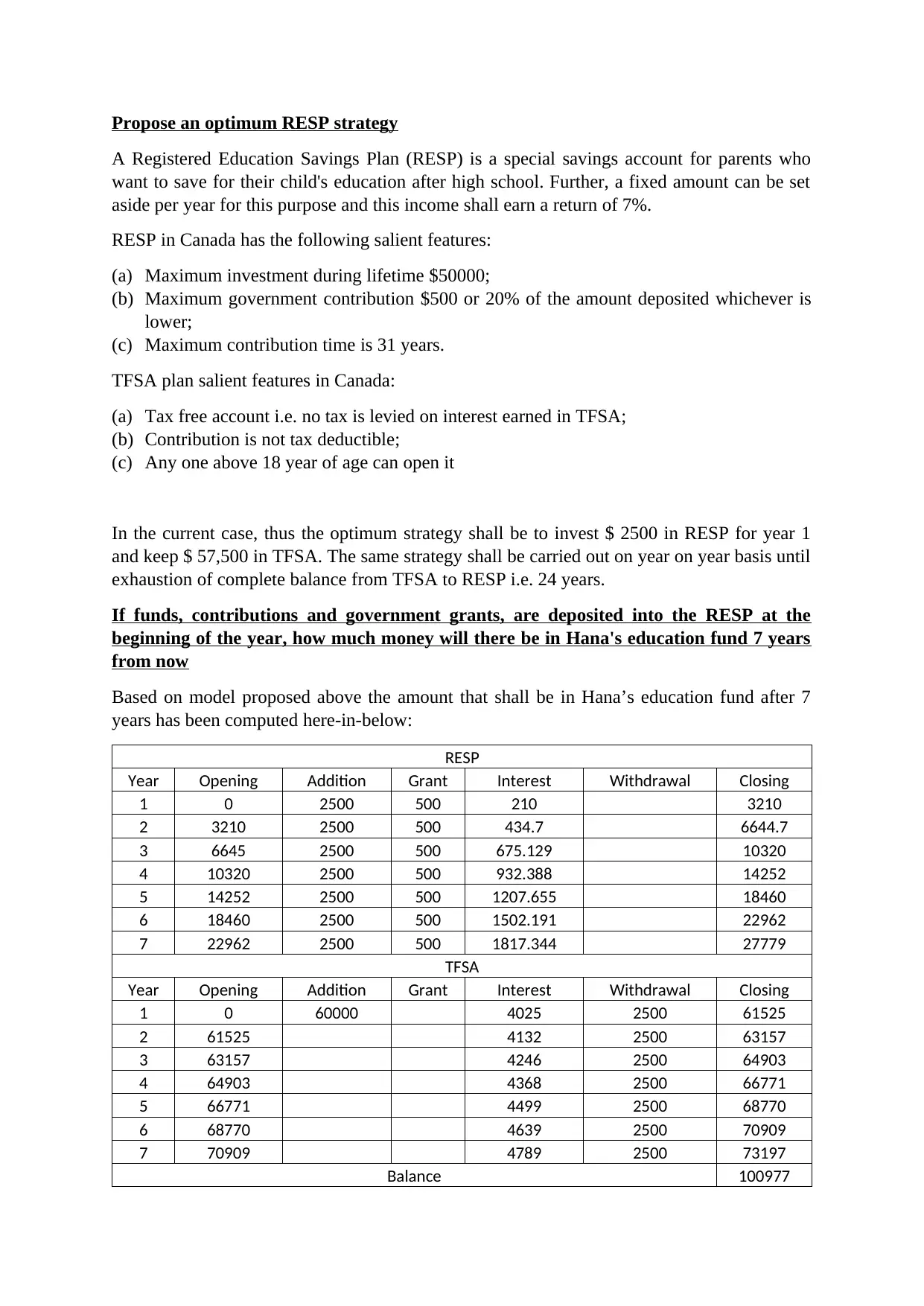

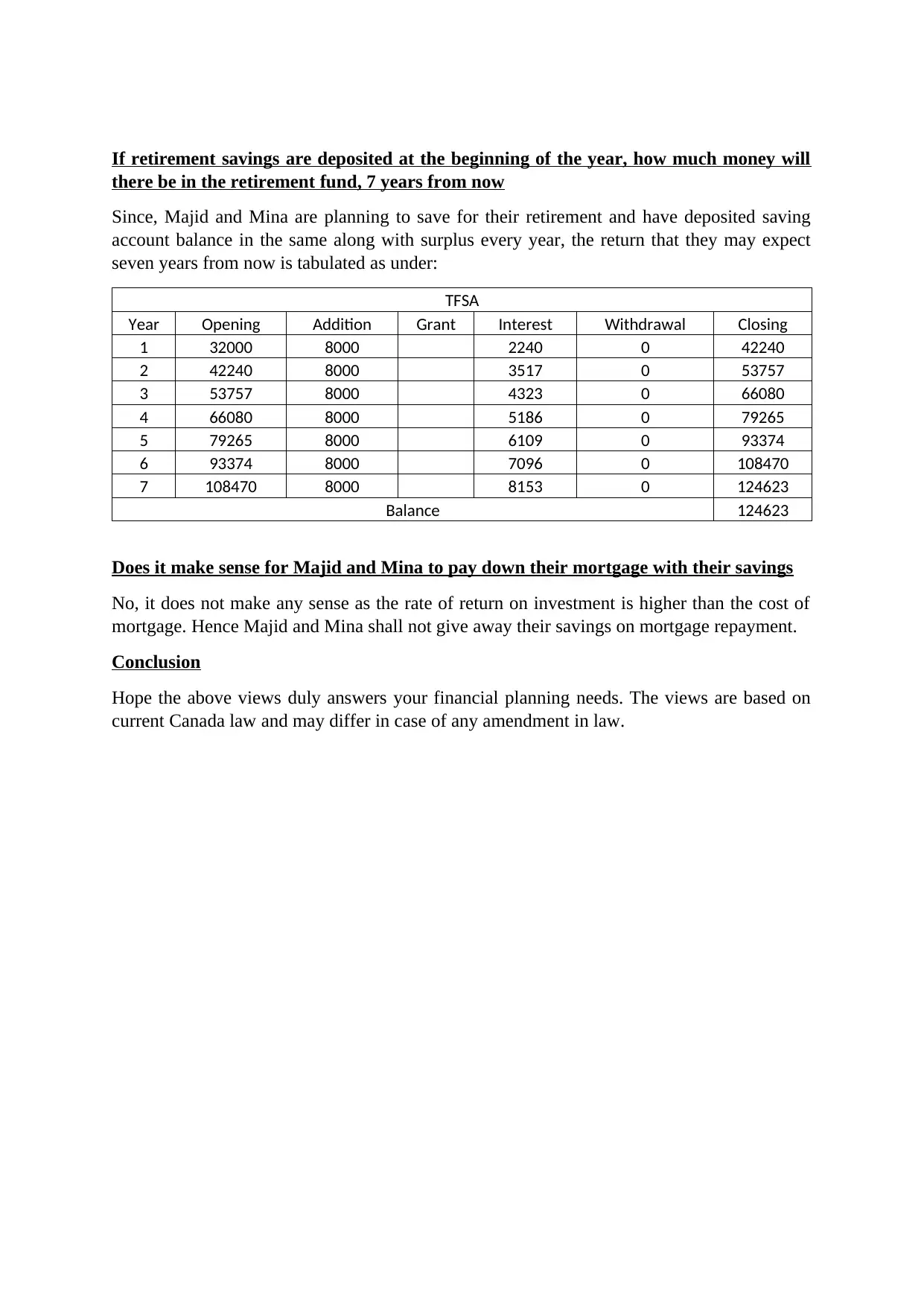

This financial planning assignment focuses on developing an optimal investment strategy for Majid and Mina, a couple with a daughter, Hana, residing in Ontario. The assignment addresses the family's financial goals, including funding Hana's post-secondary education and their retirement. It explores the use of Registered Education Savings Plans (RESPs) and Tax-Free Savings Accounts (TFSAs), evaluating contribution strategies and potential returns. The analysis includes calculating the future value of RESP and retirement funds over a seven-year period, considering government grants and interest rates. Furthermore, the assignment assesses the financial prudence of paying down their mortgage using their savings, comparing the benefits of investment returns versus mortgage interest rates. The solution provides a detailed breakdown of the proposed investment allocation, offering insights into maximizing financial benefits based on current Canadian financial regulations.

1 out of 3

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.