RMIT Financial Planning: Research and Application Assignment - Task 1

VerifiedAdded on 2022/11/28

|10

|2075

|356

Report

AI Summary

This report presents a comprehensive analysis of a financial planning assignment, covering key aspects of the financial services industry. It begins with an examination of the Financial Planning Association's (FPA) code of ethics, outlining its purpose, core principles, and methods for ensuring adherence. The report then explores the financial planning process, including budgeting and debt management strategies, and the advantages and risks associated with managed funds and share investments. It also delves into economic indicators impacting investments, client rapport-building techniques, and schedules for ongoing client services. The assignment draws on the provided materials, including the Swanston Banking Group Ltd. case study and relevant course modules, to provide practical insights and recommendations for financial planning practices. The report is structured around answering a series of questions related to financial planning concepts.

Running head: RESEARCH AND APPLICATION ASSIGNMENT

Research and Application Assignment

Name of the Student

Name of the University

Author’s note

Student name, student number, task 1, unit code, Research and Application assignment

Research and Application Assignment

Name of the Student

Name of the University

Author’s note

Student name, student number, task 1, unit code, Research and Application assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1RESEARCH AND APPLICATION ASSIGNMENT

Table of Contents

Question 1..................................................................................................................................2

Purpose of financial planning association’s code of ethics........................................................2

Main points stipulated by the code.............................................................................................2

Process to be put into place for ensuring adherence to the Code...............................................3

Question 2..................................................................................................................................4

Chart explaining the steps of financial planning process...........................................................4

Question 3..................................................................................................................................5

Advantages and risks associated with managed funds and share investments..........................5

Outline two economic indicators having impact on managed funds and share investments.....5

Recommendations for the consideration of the clients for investment opportunities................6

Question 4..................................................................................................................................6

Importance of budgeting and debt management in the financial planning process...................6

Three key strategies for utilising budget and debt management................................................6

Two tools for clients in managing budgets and cash flow.........................................................7

Question 5..................................................................................................................................7

Three to five strategies for building rapport with clients...........................................................7

Question 6..................................................................................................................................8

Schedule of services for prospective clients for ongoing services as a part of financial

planning process.........................................................................................................................8

References..................................................................................................................................9

Student name, student number, task 1, unit code, Research and Application assignment

Page 1 of 10

Table of Contents

Question 1..................................................................................................................................2

Purpose of financial planning association’s code of ethics........................................................2

Main points stipulated by the code.............................................................................................2

Process to be put into place for ensuring adherence to the Code...............................................3

Question 2..................................................................................................................................4

Chart explaining the steps of financial planning process...........................................................4

Question 3..................................................................................................................................5

Advantages and risks associated with managed funds and share investments..........................5

Outline two economic indicators having impact on managed funds and share investments.....5

Recommendations for the consideration of the clients for investment opportunities................6

Question 4..................................................................................................................................6

Importance of budgeting and debt management in the financial planning process...................6

Three key strategies for utilising budget and debt management................................................6

Two tools for clients in managing budgets and cash flow.........................................................7

Question 5..................................................................................................................................7

Three to five strategies for building rapport with clients...........................................................7

Question 6..................................................................................................................................8

Schedule of services for prospective clients for ongoing services as a part of financial

planning process.........................................................................................................................8

References..................................................................................................................................9

Student name, student number, task 1, unit code, Research and Application assignment

Page 1 of 10

2RESEARCH AND APPLICATION ASSIGNMENT

Question 1

Purpose of financial planning association’s code of ethics

The code of ethics that has been formulated by the Financial planning association is

situated at the top layer of the professional regulation. Barrett, C., 2018. The main function of

the code of ethics is to establish an ethical foundation for the other standards which are built

by FPA. These standards include Practice Standards as well as Rules of Professional Conduct

(Barrett 2018). The code of ethics has been constructed to follow eight principles which are

important for setting a minimum benchmark of professional behaviour that is applicable to all

the stakeholders, members, financial planning services users and government. These

principles are required to be followed in order to ensure good ethical practices within the

participant of Australian industries.

Main points stipulated by the code

The code of ethics as designed by the Financial planning association takes into

account the eight important principles of business ethics.

The interests of the clients should be the top priority of the employers

1) The industries should provide professional services with honesty and integrity

2) The professional services should be provided following the principles of objectivity,

that is, intellectual honesty and impartiality (Menzel 2017).

3) The principle also follows fairness and reasonableness in the professional

relationships with the clients.

4) The industries are required to act in a way that would demonstrate exemplary

professional conduct (Menzel 2017).

Student name, student number, task 1, unit code, Research and Application assignment

Page 2 of 10

Question 1

Purpose of financial planning association’s code of ethics

The code of ethics that has been formulated by the Financial planning association is

situated at the top layer of the professional regulation. Barrett, C., 2018. The main function of

the code of ethics is to establish an ethical foundation for the other standards which are built

by FPA. These standards include Practice Standards as well as Rules of Professional Conduct

(Barrett 2018). The code of ethics has been constructed to follow eight principles which are

important for setting a minimum benchmark of professional behaviour that is applicable to all

the stakeholders, members, financial planning services users and government. These

principles are required to be followed in order to ensure good ethical practices within the

participant of Australian industries.

Main points stipulated by the code

The code of ethics as designed by the Financial planning association takes into

account the eight important principles of business ethics.

The interests of the clients should be the top priority of the employers

1) The industries should provide professional services with honesty and integrity

2) The professional services should be provided following the principles of objectivity,

that is, intellectual honesty and impartiality (Menzel 2017).

3) The principle also follows fairness and reasonableness in the professional

relationships with the clients.

4) The industries are required to act in a way that would demonstrate exemplary

professional conduct (Menzel 2017).

Student name, student number, task 1, unit code, Research and Application assignment

Page 2 of 10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3RESEARCH AND APPLICATION ASSIGNMENT

5) The industries are obliged to maintain their skills, knowledge as well as abilities for

providing competent professional services

6) The employers should maintain the confidentiality of the client information and

should not disclose the information with a third party (Menzel 2017).

7) The final principle states about being diligence while performing the professional

services.

Process to be put into place for ensuring adherence to the Code

Adherence to the first principle can be done through serving the interests of the clients

above all the competing demands. Adherence to the principle of integrity can be fairly and

consistently performed by doing the right thing for catering to the best interests of the clients.

This can even be done while the others are not watching or noticing. Taking note of the

principle of objectivity, the adherence can be done through the demonstration of the ability to

evaluate information or circumstances (Board 2015). The members should not involve their

own emotions or priorities into this process. While ensuring fairness, the members should be

able to communicate their information responsibly to the clients bridging the gap between the

client’s needs and the information they have committed to provide.

Competence in the knowledge and skills can be maintained through coping up with

the changes that are taking place in the economic, regulatory environment and also with other

changes of financial services industry and areas of specific technical knowledge. Principle of

confidentiality can be adhered through taking all the reasonable steps for protecting and

storing all the important client documents as well as the communications (Board 2015).

Diligence can be adhered through following a proper process of management with the clients.

Professionalism is marked through the maintenance of proper ethics, behaviour and service

which are of high standards.

Student name, student number, task 1, unit code, Research and Application assignment

Page 3 of 10

5) The industries are obliged to maintain their skills, knowledge as well as abilities for

providing competent professional services

6) The employers should maintain the confidentiality of the client information and

should not disclose the information with a third party (Menzel 2017).

7) The final principle states about being diligence while performing the professional

services.

Process to be put into place for ensuring adherence to the Code

Adherence to the first principle can be done through serving the interests of the clients

above all the competing demands. Adherence to the principle of integrity can be fairly and

consistently performed by doing the right thing for catering to the best interests of the clients.

This can even be done while the others are not watching or noticing. Taking note of the

principle of objectivity, the adherence can be done through the demonstration of the ability to

evaluate information or circumstances (Board 2015). The members should not involve their

own emotions or priorities into this process. While ensuring fairness, the members should be

able to communicate their information responsibly to the clients bridging the gap between the

client’s needs and the information they have committed to provide.

Competence in the knowledge and skills can be maintained through coping up with

the changes that are taking place in the economic, regulatory environment and also with other

changes of financial services industry and areas of specific technical knowledge. Principle of

confidentiality can be adhered through taking all the reasonable steps for protecting and

storing all the important client documents as well as the communications (Board 2015).

Diligence can be adhered through following a proper process of management with the clients.

Professionalism is marked through the maintenance of proper ethics, behaviour and service

which are of high standards.

Student name, student number, task 1, unit code, Research and Application assignment

Page 3 of 10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4RESEARCH AND APPLICATION ASSIGNMENT

Question 2

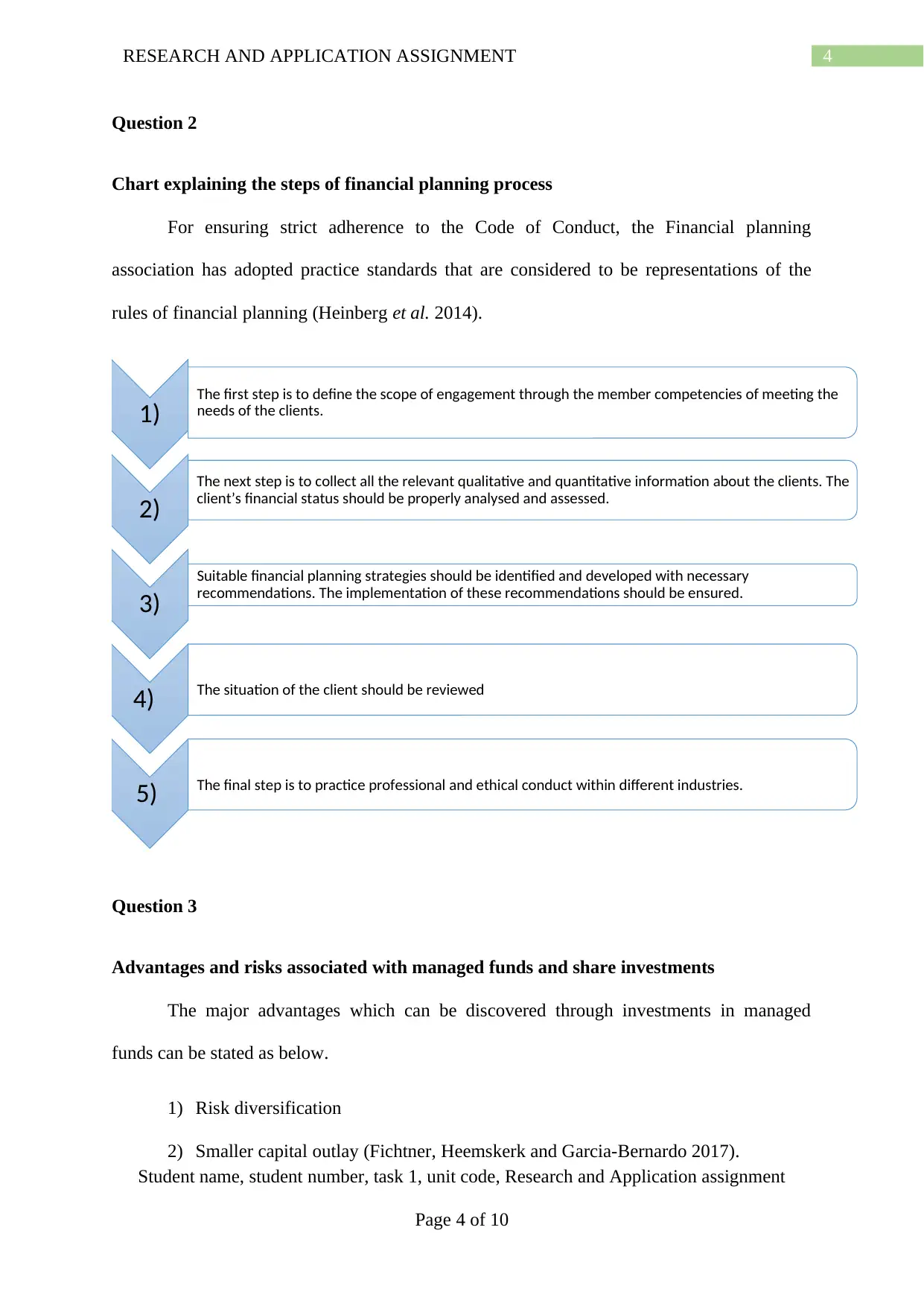

Chart explaining the steps of financial planning process

For ensuring strict adherence to the Code of Conduct, the Financial planning

association has adopted practice standards that are considered to be representations of the

rules of financial planning (Heinberg et al. 2014).

Question 3

Advantages and risks associated with managed funds and share investments

The major advantages which can be discovered through investments in managed

funds can be stated as below.

1) Risk diversification

2) Smaller capital outlay (Fichtner, Heemskerk and Garcia-Bernardo 2017).

Student name, student number, task 1, unit code, Research and Application assignment

Page 4 of 10

1) The first step is to define the scope of engagement through the member competencies of meeting the

needs of the clients.

2)

The next step is to collect all the relevant qualitative and quantitative information about the clients. The

client’s financial status should be properly analysed and assessed.

3)

Suitable financial planning strategies should be identified and developed with necessary

recommendations. The implementation of these recommendations should be ensured.

4) The situation of the client should be reviewed

5) The final step is to practice professional and ethical conduct within different industries.

Question 2

Chart explaining the steps of financial planning process

For ensuring strict adherence to the Code of Conduct, the Financial planning

association has adopted practice standards that are considered to be representations of the

rules of financial planning (Heinberg et al. 2014).

Question 3

Advantages and risks associated with managed funds and share investments

The major advantages which can be discovered through investments in managed

funds can be stated as below.

1) Risk diversification

2) Smaller capital outlay (Fichtner, Heemskerk and Garcia-Bernardo 2017).

Student name, student number, task 1, unit code, Research and Application assignment

Page 4 of 10

1) The first step is to define the scope of engagement through the member competencies of meeting the

needs of the clients.

2)

The next step is to collect all the relevant qualitative and quantitative information about the clients. The

client’s financial status should be properly analysed and assessed.

3)

Suitable financial planning strategies should be identified and developed with necessary

recommendations. The implementation of these recommendations should be ensured.

4) The situation of the client should be reviewed

5) The final step is to practice professional and ethical conduct within different industries.

5RESEARCH AND APPLICATION ASSIGNMENT

3) Variety of products

4) Investment in a disciplined manner

5) Professional management of funds

6) Access to the international markets of investments (Fichtner, Heemskerk and

Garcia-Bernardo 2017).

The different risks which are associated with the managed funds can be stated below.

1) Risk of the market

2) Risk occurring due to inflation

3) Risk of changes in the interest rates

4) Currency risks (Fichtner, Heemskerk and Garcia-Bernardo 2017).

5) Credit risks

Outline two economic indicators having impact on managed funds and share

investments

Two economic indicators that can have direct impact on managed funds and share

investments are growth of the GDP and Industrial production which is also regarded as

factory output (Tosun 2014).

Recommendations for the consideration of the clients for investment opportunities

Suitable inquiry of the prospective client’s investment experience, risk and return

objectives. Determination of the suitability of the investment with the financial situation of

the client. Judgement about the suitability of the investments with respect to the client’s total

portfolio.

Student name, student number, task 1, unit code, Research and Application assignment

Page 5 of 10

3) Variety of products

4) Investment in a disciplined manner

5) Professional management of funds

6) Access to the international markets of investments (Fichtner, Heemskerk and

Garcia-Bernardo 2017).

The different risks which are associated with the managed funds can be stated below.

1) Risk of the market

2) Risk occurring due to inflation

3) Risk of changes in the interest rates

4) Currency risks (Fichtner, Heemskerk and Garcia-Bernardo 2017).

5) Credit risks

Outline two economic indicators having impact on managed funds and share

investments

Two economic indicators that can have direct impact on managed funds and share

investments are growth of the GDP and Industrial production which is also regarded as

factory output (Tosun 2014).

Recommendations for the consideration of the clients for investment opportunities

Suitable inquiry of the prospective client’s investment experience, risk and return

objectives. Determination of the suitability of the investment with the financial situation of

the client. Judgement about the suitability of the investments with respect to the client’s total

portfolio.

Student name, student number, task 1, unit code, Research and Application assignment

Page 5 of 10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6RESEARCH AND APPLICATION ASSIGNMENT

Question 4

Importance of budgeting and debt management in the financial planning process

Budgeting is a very important process through which a plan is created for expenditure

of money. A budget ensures that the person has enough money for the desired things and also

for the important things. A budget can be used for properly forecasting the spending for the

upcoming financial year and thus, can serve as an efficient tool for long-term financial

planning (Navickas Gudaitis and Krajnakova 2014). Through a budget, realistic assumptions

can be made on elements such as annual income, buying of investment, expenditure for

business goals and many others.

A financial planner plans a budget and also sets up a debt repayment plan that reflects

the time period within which the debt can be fully repaid. The extra money to be paid for the

debt is highlighted properly in the budget prepared by the financial planner.

Three key strategies for utilising budget and debt management

The spending plan that is required for the preparation of a budget generally tracks two

important things. One of such things is the after-tax income of the client and the amount that

is getting shelled out each month. One of the key strategies to this can be taking inventory of

the finances or the expenses. The next strategy can be awareness about legitimate financial

goals of the year (Navickas Gudaitis and Krajnakova 2014). The final strategy can be

understanding the two sides of the budget, that Is, both income and expenditure.

A client who is already burdened with debt can seek the help of a financial advisor.

Through a financial planning procedure, a client’s cash flow and areas of existing and

potential problems can be identified. After this process, a new and balanced budget can be

Student name, student number, task 1, unit code, Research and Application assignment

Page 6 of 10

Question 4

Importance of budgeting and debt management in the financial planning process

Budgeting is a very important process through which a plan is created for expenditure

of money. A budget ensures that the person has enough money for the desired things and also

for the important things. A budget can be used for properly forecasting the spending for the

upcoming financial year and thus, can serve as an efficient tool for long-term financial

planning (Navickas Gudaitis and Krajnakova 2014). Through a budget, realistic assumptions

can be made on elements such as annual income, buying of investment, expenditure for

business goals and many others.

A financial planner plans a budget and also sets up a debt repayment plan that reflects

the time period within which the debt can be fully repaid. The extra money to be paid for the

debt is highlighted properly in the budget prepared by the financial planner.

Three key strategies for utilising budget and debt management

The spending plan that is required for the preparation of a budget generally tracks two

important things. One of such things is the after-tax income of the client and the amount that

is getting shelled out each month. One of the key strategies to this can be taking inventory of

the finances or the expenses. The next strategy can be awareness about legitimate financial

goals of the year (Navickas Gudaitis and Krajnakova 2014). The final strategy can be

understanding the two sides of the budget, that Is, both income and expenditure.

A client who is already burdened with debt can seek the help of a financial advisor.

Through a financial planning procedure, a client’s cash flow and areas of existing and

potential problems can be identified. After this process, a new and balanced budget can be

Student name, student number, task 1, unit code, Research and Application assignment

Page 6 of 10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7RESEARCH AND APPLICATION ASSIGNMENT

prepared by the financial advisor in such a way that there is no existence of debt in the

picture.

Two tools for clients in managing budgets and cash flow

There can be number of tools required for the management of budget as well as the

cash flow.

1) Worksheets

The budgeting worksheets are free online tools for managing budgets. These tools are

required for household budgeting, expense tracking and budgeting for specific needs.

2) Banking tools

The banking tools are primarily required for developing a workable spending plan that would

be useful for managing the cash flow (Maskell, Baggaley and Grasso 2017).

Question 5

Three to five strategies for building rapport with clients

The perfect rapport with the clients can be built through five important elements.

Ensuring effective communication with the clients through the usage of proper words.

There should be simple sentences in communication without much use of the jargons (Swift

and Littlechild 2015). The other important tips of communication would be eye contact, slow

speaking, asking right questions and many others.

Another way to build a good rapport with the client is to listen actively to the wants

and needs of the clients from the beginning (Swift and Littlechild 2015). Another strategy

could be a proper personal presentation. The person should be well dressed in order to build

Student name, student number, task 1, unit code, Research and Application assignment

Page 7 of 10

prepared by the financial advisor in such a way that there is no existence of debt in the

picture.

Two tools for clients in managing budgets and cash flow

There can be number of tools required for the management of budget as well as the

cash flow.

1) Worksheets

The budgeting worksheets are free online tools for managing budgets. These tools are

required for household budgeting, expense tracking and budgeting for specific needs.

2) Banking tools

The banking tools are primarily required for developing a workable spending plan that would

be useful for managing the cash flow (Maskell, Baggaley and Grasso 2017).

Question 5

Three to five strategies for building rapport with clients

The perfect rapport with the clients can be built through five important elements.

Ensuring effective communication with the clients through the usage of proper words.

There should be simple sentences in communication without much use of the jargons (Swift

and Littlechild 2015). The other important tips of communication would be eye contact, slow

speaking, asking right questions and many others.

Another way to build a good rapport with the client is to listen actively to the wants

and needs of the clients from the beginning (Swift and Littlechild 2015). Another strategy

could be a proper personal presentation. The person should be well dressed in order to build

Student name, student number, task 1, unit code, Research and Application assignment

Page 7 of 10

8RESEARCH AND APPLICATION ASSIGNMENT

trust among the clients. The person should have a positive as well as an optimistic mental

attitude. The person should understand importance of acknowledgement and respect.

Question 6

Schedule of services for prospective clients for ongoing services as a part of financial

planning process

The schedule of services which are required to be followed while making the clients

aware of the ongoing services are listed as follows.

Initial meeting with the clients. Advice process which allows the Industries to

consider the relevant matters of the clients. Ongoing services that focusses on the changes of

personal situations, financial markets, legislations and many other services over time (Baker

and Dellaert 2017). These services ensure that the plans remain appropriate and the

investments are well managed. Accessing the financial adviser after the proper

implementation of the plan.

Student name, student number, task 1, unit code, Research and Application assignment

Page 8 of 10

trust among the clients. The person should have a positive as well as an optimistic mental

attitude. The person should understand importance of acknowledgement and respect.

Question 6

Schedule of services for prospective clients for ongoing services as a part of financial

planning process

The schedule of services which are required to be followed while making the clients

aware of the ongoing services are listed as follows.

Initial meeting with the clients. Advice process which allows the Industries to

consider the relevant matters of the clients. Ongoing services that focusses on the changes of

personal situations, financial markets, legislations and many other services over time (Baker

and Dellaert 2017). These services ensure that the plans remain appropriate and the

investments are well managed. Accessing the financial adviser after the proper

implementation of the plan.

Student name, student number, task 1, unit code, Research and Application assignment

Page 8 of 10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9RESEARCH AND APPLICATION ASSIGNMENT

References

Baker, T. and Dellaert, B., 2017. Regulating robo advice across the financial services

industry. Iowa L. Rev., 103, p.713.

Barrett, C., 2018. Everyday ethics for practicing planners. Routledge.

Board, C.F.P., 2015. Financial planning competency handbook. John Wiley & Sons.

Fichtner, J., Heemskerk, E.M. and Garcia-Bernardo, J., 2017. Hidden power of the Big

Three? Passive index funds, re-concentration of corporate ownership, and new financial

risk. Business and Politics, 19(2), pp.298-326.

Heinberg, A., Hung, A., Kapteyn, A., Lusardi, A., Samek, A.S. and Yoong, J., 2014. Five

steps to planning success: experimental evidence from US households. Oxford Review of

Economic Policy, 30(4), pp.697-724.

Maskell, B.H., Baggaley, B. and Grasso, L., 2017. Practical lean accounting: a proven

system for measuring and managing the lean enterprise. Productivity Press.

Menzel, D.C., 2017. Ethics moments in government: Cases and controversies. Routledge.

Navickas, M., Gudaitis, T. and Krajnakova, E., 2014. Influence of financial literacy on

management of personal finances in a young household. Business: theory and practice, 15(1),

pp.32-40.

Swift, M. and Littlechild, J., 2015. Building trust through communication. Journal of

Financial Planning, 28(11), p.28.

Tosun, J., 2014. Absorption of regional funds: A comparative analysis. JCMS: Journal of

Common Market Studies, 52(2), pp.371-387.

Student name, student number, task 1, unit code, Research and Application assignment

Page 9 of 10

References

Baker, T. and Dellaert, B., 2017. Regulating robo advice across the financial services

industry. Iowa L. Rev., 103, p.713.

Barrett, C., 2018. Everyday ethics for practicing planners. Routledge.

Board, C.F.P., 2015. Financial planning competency handbook. John Wiley & Sons.

Fichtner, J., Heemskerk, E.M. and Garcia-Bernardo, J., 2017. Hidden power of the Big

Three? Passive index funds, re-concentration of corporate ownership, and new financial

risk. Business and Politics, 19(2), pp.298-326.

Heinberg, A., Hung, A., Kapteyn, A., Lusardi, A., Samek, A.S. and Yoong, J., 2014. Five

steps to planning success: experimental evidence from US households. Oxford Review of

Economic Policy, 30(4), pp.697-724.

Maskell, B.H., Baggaley, B. and Grasso, L., 2017. Practical lean accounting: a proven

system for measuring and managing the lean enterprise. Productivity Press.

Menzel, D.C., 2017. Ethics moments in government: Cases and controversies. Routledge.

Navickas, M., Gudaitis, T. and Krajnakova, E., 2014. Influence of financial literacy on

management of personal finances in a young household. Business: theory and practice, 15(1),

pp.32-40.

Swift, M. and Littlechild, J., 2015. Building trust through communication. Journal of

Financial Planning, 28(11), p.28.

Tosun, J., 2014. Absorption of regional funds: A comparative analysis. JCMS: Journal of

Common Market Studies, 52(2), pp.371-387.

Student name, student number, task 1, unit code, Research and Application assignment

Page 9 of 10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.