University Finance: Managing Budgets and Financial Plans Report

VerifiedAdded on 2022/08/14

|21

|4329

|19

Report

AI Summary

This report provides a comprehensive analysis of budgeting and financial planning practices within the context of a business, specifically Big Red Bicycles Pty Ltd. It begins by outlining the importance of budgeting for achieving financial goals, including revenue enhancement and cost control. The report identifies key issues such as excessive advertising costs and higher-than-expected wages, proposing strategies for improvement like reducing advertising budgets and controlling labor costs through skilled recruitment and training programs. It emphasizes the application of accounting principles, such as the money measurement and cost concepts, and their relevance in budget preparation and issue identification. The report also delves into relevant legislations and ATO requirements, including payroll reporting, monthly organizational activity statements, and financial year reporting. It then explores various techniques for managing budgets, highlighting the importance of market trend information, error recognition, and resource estimation. The report includes contingency plans to address potential risks, such as variances between budgeted and actual profits, and discrepancies in commission structures. It further discusses financial policies, including the use of spreadsheets for tracking expenses and the implementation of reimbursement policies. The report also presents a training plan to enhance employee skills in areas such as spreadsheet application, expense tracking, and sales operations. Finally, the report includes a variance report for the fiscal year 2011/2012, comparing the master budget with actual figures to identify areas of deviation and assess the effectiveness of financial planning and management strategies.

Running head: MANAGE BUDGETS AND FINANCIAL PLANS

Manage Budgets and Financial Plans

Name of the Student:

Name of the University:

Author’s Note

Manage Budgets and Financial Plans

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MANAGE BUDGETS AND FINANCIAL PLANS

Table of Contents

Assessment Task 1.....................................................................................................................2

Budgeting Practices and Negotiating Changes......................................................................2

Identification of Issues and Negotiating Changes..................................................................2

Basic Accounting Principles..................................................................................................3

Relevant Legislations and ATO Requirements......................................................................4

Techniques for Managing Budgets........................................................................................5

Contingency plan...................................................................................................................5

Assessment 2..............................................................................................................................7

Financial Policies of the business..........................................................................................7

Training plan..........................................................................................................................8

Assessment 3..............................................................................................................................9

Implementing contingency plan...............................................................................................13

Activity 1..............................................................................................................................14

Activity 2..............................................................................................................................15

Activity 3..............................................................................................................................15

Activity 4..............................................................................................................................16

Management Accounting and Planning Principle................................................................17

Reflections................................................................................................................................18

Reference..................................................................................................................................20

MANAGE BUDGETS AND FINANCIAL PLANS

Table of Contents

Assessment Task 1.....................................................................................................................2

Budgeting Practices and Negotiating Changes......................................................................2

Identification of Issues and Negotiating Changes..................................................................2

Basic Accounting Principles..................................................................................................3

Relevant Legislations and ATO Requirements......................................................................4

Techniques for Managing Budgets........................................................................................5

Contingency plan...................................................................................................................5

Assessment 2..............................................................................................................................7

Financial Policies of the business..........................................................................................7

Training plan..........................................................................................................................8

Assessment 3..............................................................................................................................9

Implementing contingency plan...............................................................................................13

Activity 1..............................................................................................................................14

Activity 2..............................................................................................................................15

Activity 3..............................................................................................................................15

Activity 4..............................................................................................................................16

Management Accounting and Planning Principle................................................................17

Reflections................................................................................................................................18

Reference..................................................................................................................................20

2

MANAGE BUDGETS AND FINANCIAL PLANS

Assessment Task 1

Budgeting Practices and Negotiating Changes

The practice of budgeting is closely followed in a business for the purpose of

effectively listing the financial goals of the business and ensuring that the same are achieved.

Budgets allow a business to estimate the costs and revenue which is associated with a

business and it can also be used for allocation of resources and evaluation of performance of

the business1. It is also to be noted that the tool is also used for the purpose of formulating

financial plans for a business. In this case the business of Big Red Bicycles is considered

which is aiming to achieve a net profit before tax of $1,000,000. In order to achieve this goal,

the management needs to control the expenses and at the same time also enhance the revenue

which is generated by the business.

The analysis of the budget shows that the business is focusing more on advertisement

and promotion so that more awareness can be achieved. Further, a major portion of the

expenses is due to the wages which needs to be controlled in order to achieve the objective of

the business.

Identification of Issues and Negotiating Changes

One of the main changes which is required to be made by the management is related

to reducing the budget for advertisement so that the total costs of operations can be improved.

The company mainly engages in production of bicycles which is quite a regular good and

therefore such extensive advertisement is not required. The management of the company

needs to control such expenses in order to enhance the profits of the business2. In order to

control the expenses, proper quality measures can be introduced and unnecessary costs can be

avoided. Big Red Bicycle Pty Ltd needs to maintain a good relation with retailers, so that the

1 Lauth, T.P., 2014. Zero‐Base Budgeting Redux in Georgia: Efficiency or Ideology?. Public Budgeting &

Finance, 34(1), pp.1-17.

2 Needles, B.E., Powers, M. and Crosson, S.V., 2013. Principles of accounting. Cengage Learning.

MANAGE BUDGETS AND FINANCIAL PLANS

Assessment Task 1

Budgeting Practices and Negotiating Changes

The practice of budgeting is closely followed in a business for the purpose of

effectively listing the financial goals of the business and ensuring that the same are achieved.

Budgets allow a business to estimate the costs and revenue which is associated with a

business and it can also be used for allocation of resources and evaluation of performance of

the business1. It is also to be noted that the tool is also used for the purpose of formulating

financial plans for a business. In this case the business of Big Red Bicycles is considered

which is aiming to achieve a net profit before tax of $1,000,000. In order to achieve this goal,

the management needs to control the expenses and at the same time also enhance the revenue

which is generated by the business.

The analysis of the budget shows that the business is focusing more on advertisement

and promotion so that more awareness can be achieved. Further, a major portion of the

expenses is due to the wages which needs to be controlled in order to achieve the objective of

the business.

Identification of Issues and Negotiating Changes

One of the main changes which is required to be made by the management is related

to reducing the budget for advertisement so that the total costs of operations can be improved.

The company mainly engages in production of bicycles which is quite a regular good and

therefore such extensive advertisement is not required. The management of the company

needs to control such expenses in order to enhance the profits of the business2. In order to

control the expenses, proper quality measures can be introduced and unnecessary costs can be

avoided. Big Red Bicycle Pty Ltd needs to maintain a good relation with retailers, so that the

1 Lauth, T.P., 2014. Zero‐Base Budgeting Redux in Georgia: Efficiency or Ideology?. Public Budgeting &

Finance, 34(1), pp.1-17.

2 Needles, B.E., Powers, M. and Crosson, S.V., 2013. Principles of accounting. Cengage Learning.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MANAGE BUDGETS AND FINANCIAL PLANS

distribution of the products can be done freely. The expenses which is incurred by the Big

Red Bicycle Pty Ltd needs to be minimized which would also ensure that the cash outflows

for the business is kept at a minimum. The business also has sponsorship for which huge

amount of cash outflow is shown and therefore, it can be said that such expenses can be

reduced by the business.

The variable costs of the business which includes wages and salaries are shown to be

slightly higher and therefore the same can be controlled by the business. In order to achieve

this, the management needs to recruit skilled employees and labors according to their skills so

that a level of productivity can be maintained. If the efficiency level of the employees can be

enhanced than labour costs can be reduced significantly. The management of the company

needs to initiate training programs in order to enhance the efficiency level of the staff

members.

Basic Accounting Principles

The accounting concepts and principles are important for formulating an accounting

report so that proper information is included and quality of disclosures can be maintained. In

the case of Big Red Bicycle Pty Ltd, the accounting concepts and principles which are

applicable are Money Measurement Concept and Cost Concept. The concept which is stated

is considered to be important for the purpose of preparing the budget and also for identifying

the issues3. In the money measurement concept, all the transactions which are related to

money are recorded here. The business can appropriately measure the cash outflows of a

business with the help of this concept. It is the responsibility for the Senior Accountant, Pat

Roberts to monitor the cash inflows and outflows of the business. This would help the

management of the company to control the costs which is related to advertisement as well

wages and salaries of the business.

3 Schläfke, M., Silvi, R. and Möller, K., 2013. A framework for business analytics in performance

management. International Journal of Productivity and Performance Management.

MANAGE BUDGETS AND FINANCIAL PLANS

distribution of the products can be done freely. The expenses which is incurred by the Big

Red Bicycle Pty Ltd needs to be minimized which would also ensure that the cash outflows

for the business is kept at a minimum. The business also has sponsorship for which huge

amount of cash outflow is shown and therefore, it can be said that such expenses can be

reduced by the business.

The variable costs of the business which includes wages and salaries are shown to be

slightly higher and therefore the same can be controlled by the business. In order to achieve

this, the management needs to recruit skilled employees and labors according to their skills so

that a level of productivity can be maintained. If the efficiency level of the employees can be

enhanced than labour costs can be reduced significantly. The management of the company

needs to initiate training programs in order to enhance the efficiency level of the staff

members.

Basic Accounting Principles

The accounting concepts and principles are important for formulating an accounting

report so that proper information is included and quality of disclosures can be maintained. In

the case of Big Red Bicycle Pty Ltd, the accounting concepts and principles which are

applicable are Money Measurement Concept and Cost Concept. The concept which is stated

is considered to be important for the purpose of preparing the budget and also for identifying

the issues3. In the money measurement concept, all the transactions which are related to

money are recorded here. The business can appropriately measure the cash outflows of a

business with the help of this concept. It is the responsibility for the Senior Accountant, Pat

Roberts to monitor the cash inflows and outflows of the business. This would help the

management of the company to control the costs which is related to advertisement as well

wages and salaries of the business.

3 Schläfke, M., Silvi, R. and Möller, K., 2013. A framework for business analytics in performance

management. International Journal of Productivity and Performance Management.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MANAGE BUDGETS AND FINANCIAL PLANS

As per the cost concept, the management needs to measure the assets on the basis of

original costs of the business. The business needs to identify the assets such as machineries

which are used for the manufacture bicycles and therefore the cost concept is considered to

be important4. The management needs to ensure that proper monitoring of the activities needs

to be done so that the activities of the business can be executed efficiently. The management

would be benefitting greatly by following this concept and the same also helps in controlling

the costs of the business.

Relevant Legislations and ATO Requirements

The Australian Tax Office implements the tax regulations and ensures that the same

are adhered to by businesses while conducting their operations. In addition to this, ATO also

makes changes to the law as and when required for effective tax compliance5. Some of the

important regulations which are administered by ATO are superannuation, payroll, income

taxes regulations.

The requirements which is needed for the reporting includes:

Payroll reporting

Monthly organizational activity statements

Financial year reporting

In case of payroll reporting, one of the major requirements is to lodge report in respect

with Australian Tax Office (ATO) with the application of Single Touch Payroll Software.

There is also a need for proper reporting of transactions and appropriate maintenance of the

same so that it complies with the new process of reporting.

In case of monthly organizational activity statements, the concerned entity needs to

submit report which comprises of activities of the business that can be of monthly, quarterly

4 Renz, D. O. (2016). The Jossey-Bass handbook of nonprofit leadership and management. John Wiley & Sons.

5 Pettigrew, A.M., 2014. The politics of organizational decision-making. Routledge

MANAGE BUDGETS AND FINANCIAL PLANS

As per the cost concept, the management needs to measure the assets on the basis of

original costs of the business. The business needs to identify the assets such as machineries

which are used for the manufacture bicycles and therefore the cost concept is considered to

be important4. The management needs to ensure that proper monitoring of the activities needs

to be done so that the activities of the business can be executed efficiently. The management

would be benefitting greatly by following this concept and the same also helps in controlling

the costs of the business.

Relevant Legislations and ATO Requirements

The Australian Tax Office implements the tax regulations and ensures that the same

are adhered to by businesses while conducting their operations. In addition to this, ATO also

makes changes to the law as and when required for effective tax compliance5. Some of the

important regulations which are administered by ATO are superannuation, payroll, income

taxes regulations.

The requirements which is needed for the reporting includes:

Payroll reporting

Monthly organizational activity statements

Financial year reporting

In case of payroll reporting, one of the major requirements is to lodge report in respect

with Australian Tax Office (ATO) with the application of Single Touch Payroll Software.

There is also a need for proper reporting of transactions and appropriate maintenance of the

same so that it complies with the new process of reporting.

In case of monthly organizational activity statements, the concerned entity needs to

submit report which comprises of activities of the business that can be of monthly, quarterly

4 Renz, D. O. (2016). The Jossey-Bass handbook of nonprofit leadership and management. John Wiley & Sons.

5 Pettigrew, A.M., 2014. The politics of organizational decision-making. Routledge

5

MANAGE BUDGETS AND FINANCIAL PLANS

or annually.

In case of financial year reporting, entities are required to prepare financial report for

estimating the taxes from 1St July to 30Th June. This will help the organization in lodging the

income tax return for that period. This is important for maintaining transparency in the

operations of the business.

Techniques for Managing Budgets

The purpose of formulating a budget is to formulate a guideline for managing the

revenue and expenses associated with the business. It is one of the valuable tools which can

play a vital role in planning process and also for implementing a plan. The key principles

which should adhere to while preparing a budget are:

It should be prepared considering the most recent market trend information for

accuracy.

It must be capable of recognizing errors in transactions.

The changes which are made in an organization should be detectable.

It should give a correct estimation of the resources which the business.

Contingency plan

Contingency plan 1

Contingency Plan

Company name: Big Red Bicycle Pty Ltd

Person developing the plan: Sales Manager of Sales Centre A

Name: John Marks

Position Sales Manager

Risk identified: Variance among the budgeted profit and actual profit by 20%

MANAGE BUDGETS AND FINANCIAL PLANS

or annually.

In case of financial year reporting, entities are required to prepare financial report for

estimating the taxes from 1St July to 30Th June. This will help the organization in lodging the

income tax return for that period. This is important for maintaining transparency in the

operations of the business.

Techniques for Managing Budgets

The purpose of formulating a budget is to formulate a guideline for managing the

revenue and expenses associated with the business. It is one of the valuable tools which can

play a vital role in planning process and also for implementing a plan. The key principles

which should adhere to while preparing a budget are:

It should be prepared considering the most recent market trend information for

accuracy.

It must be capable of recognizing errors in transactions.

The changes which are made in an organization should be detectable.

It should give a correct estimation of the resources which the business.

Contingency plan

Contingency plan 1

Contingency Plan

Company name: Big Red Bicycle Pty Ltd

Person developing the plan: Sales Manager of Sales Centre A

Name: John Marks

Position Sales Manager

Risk identified: Variance among the budgeted profit and actual profit by 20%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MANAGE BUDGETS AND FINANCIAL PLANS

Strategies/activities to minimise the risk By when By whom

Implementation of Innovative practices for generating

competitive advantage over the competitors which can

enhance the sales

10th January Sales Manager

Expanding the scope of the business in the overseas market so

that it will have a secondary market to generate sales.

28th February Production

Manager

Contingency plan 2

Contingency Plan

Company name: Big Red Bicycle Pty Ltd

Person developing the plan: Sales Manager of Sales Centre A

Name: John Marks

Position: Sales Manager

Risk identified: Discrepancies in commission with the Budgeted Figure.

Strategies/activities to minimise the risk By when By whom

Implementing the commission based on progressive charge that

will also provide rewards based on the performance

28th

December

Operational

Manager

Motivating the employees with new commission system for

motivating the employees

10th January Top level

Management

and CEO

MANAGE BUDGETS AND FINANCIAL PLANS

Strategies/activities to minimise the risk By when By whom

Implementation of Innovative practices for generating

competitive advantage over the competitors which can

enhance the sales

10th January Sales Manager

Expanding the scope of the business in the overseas market so

that it will have a secondary market to generate sales.

28th February Production

Manager

Contingency plan 2

Contingency Plan

Company name: Big Red Bicycle Pty Ltd

Person developing the plan: Sales Manager of Sales Centre A

Name: John Marks

Position: Sales Manager

Risk identified: Discrepancies in commission with the Budgeted Figure.

Strategies/activities to minimise the risk By when By whom

Implementing the commission based on progressive charge that

will also provide rewards based on the performance

28th

December

Operational

Manager

Motivating the employees with new commission system for

motivating the employees

10th January Top level

Management

and CEO

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGE BUDGETS AND FINANCIAL PLANS

Assessment 2

The senior executives of the company would be informing the sales executives

regarding the targets which are presented in the budget. In such an instance, the employee

would be clear regarding the sales target and aims of the business. In addition to this, the

budget should also portray the expenses which is anticipated and on the basis of the same

appropriate changes needs to be incorporated. Further, it was clear from the budget that 2nd

quarter’s sales are more as compared to other 3 quarters. It is found that the allocated wages

to each of the sales centres is $ 1,00,000 under budget. Similarly the other costs which is

related to the business is also shown to be on the rise which is a matter of concern for the

management and appropriate steps needs to be taken in this regard. The management of Big

Red Bicycles Ltd needs to take steps for ensuring that costs are reduced for enhancing the

profits of the business.

Financial Policies of the business

In order to achieve success and the goals of the business, the senior officials of Big

Red Bicycles Ltd needs to formulate strategies so that proper utilization is done for all the

resources and cost is managed to the best of interest6. The business would be utilizing excel

spread sheets and software programs for tracking expenses and recording the same. As per

the given case study individual bill will be selected for petty cash handling. Further, the bills

are required to be maintained in spreadsheet for keeping track for which there will be

training. In addition to this, the business also has a reimbursement policy for employees so

that they can recover any amount which is spent for the benefit of the company. The expenses

6 Morgan, D., Robinson, K. S., Strachota, D., & Hough, J. A. (2017). The Budget Cycle: Characteristics and

Consequences. In Budgeting for Local Governments and Communities (pp. 135-164). Routledge.

MANAGE BUDGETS AND FINANCIAL PLANS

Assessment 2

The senior executives of the company would be informing the sales executives

regarding the targets which are presented in the budget. In such an instance, the employee

would be clear regarding the sales target and aims of the business. In addition to this, the

budget should also portray the expenses which is anticipated and on the basis of the same

appropriate changes needs to be incorporated. Further, it was clear from the budget that 2nd

quarter’s sales are more as compared to other 3 quarters. It is found that the allocated wages

to each of the sales centres is $ 1,00,000 under budget. Similarly the other costs which is

related to the business is also shown to be on the rise which is a matter of concern for the

management and appropriate steps needs to be taken in this regard. The management of Big

Red Bicycles Ltd needs to take steps for ensuring that costs are reduced for enhancing the

profits of the business.

Financial Policies of the business

In order to achieve success and the goals of the business, the senior officials of Big

Red Bicycles Ltd needs to formulate strategies so that proper utilization is done for all the

resources and cost is managed to the best of interest6. The business would be utilizing excel

spread sheets and software programs for tracking expenses and recording the same. As per

the given case study individual bill will be selected for petty cash handling. Further, the bills

are required to be maintained in spreadsheet for keeping track for which there will be

training. In addition to this, the business also has a reimbursement policy for employees so

that they can recover any amount which is spent for the benefit of the company. The expenses

6 Morgan, D., Robinson, K. S., Strachota, D., & Hough, J. A. (2017). The Budget Cycle: Characteristics and

Consequences. In Budgeting for Local Governments and Communities (pp. 135-164). Routledge.

8

MANAGE BUDGETS AND FINANCIAL PLANS

which are genuine in nature are applicable for reimbursement. In addition to this, the

company also takes its petty cash and tracking of expenses policy quite seriously so that

adequate cash flow can be maintained. The petty cash needs to be maintained properly by a

person who can be held accountable for the same. The petty cash provides appropriate funds

in the hand of management so that they can meet some urgent obligation which might come

up. The business also aims to make use of spreadsheet for managing the expenses and also

for properly recording the same. It is also to be noted that maintenance of petty cash ledger

should be maintained by two or more person so that if person falls sick, the recording process

is not hampered in any manner7. The petty cash which is maintained by the business is used

for reimbursement for the employees in regards to some expenses undertaken.

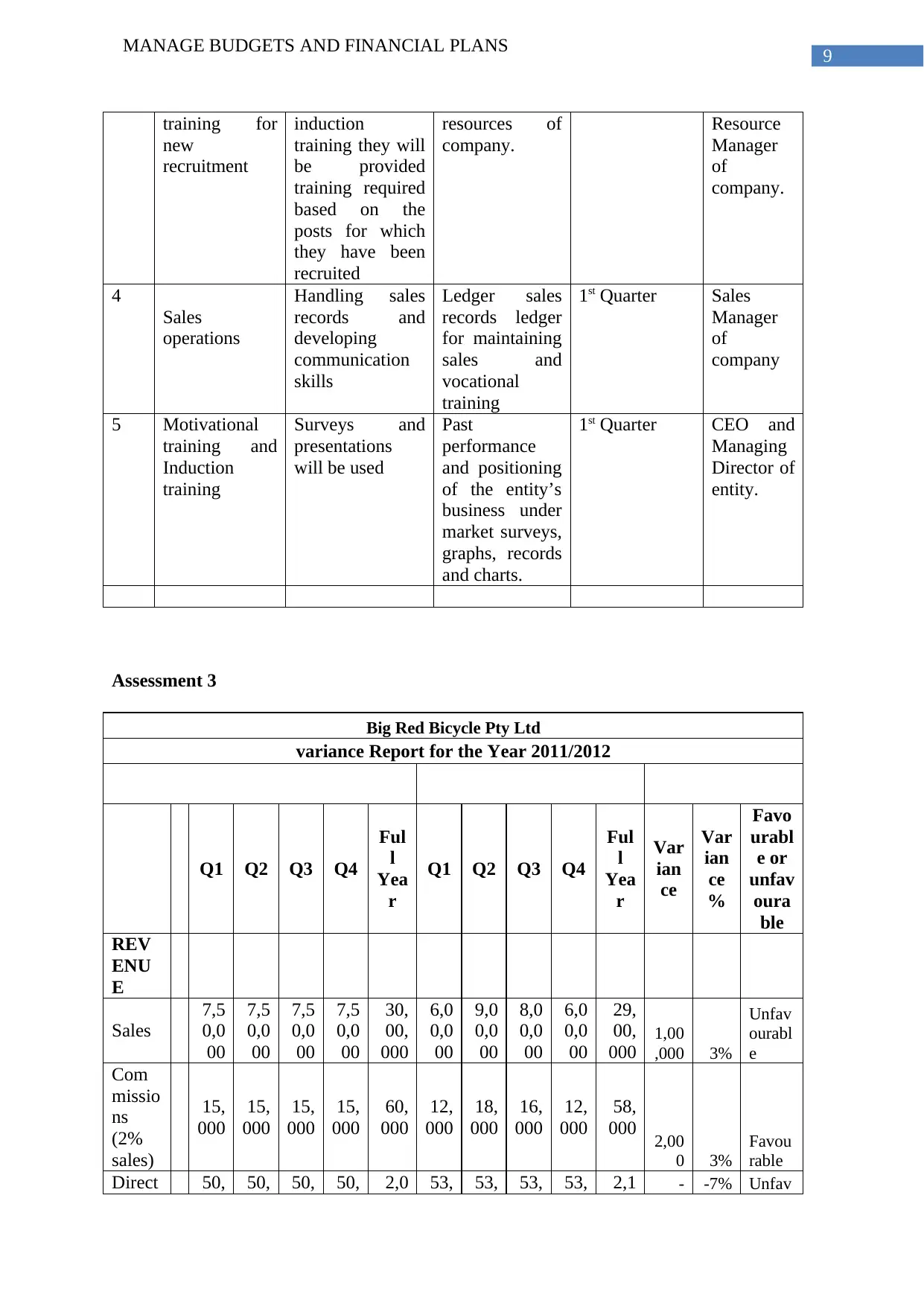

Training plan

# Skills/

knowledge to

be developed

Training

method

Resources

Required

Timeframe Review

date and

by whom?Start Finish

1 Application of

Spreadsheet

and use of

formulas

Training will be

provided through

practical use of

spreadsheet with

required formula

and functions

Computer

Software

2nd Quarter Operations

Manager.

2 Tracking the

company’s

Expenses

Spreadsheet

application will

be used for

tracking and

maintaining the

details of

business

expenses.

Further, budgets

will be used for

comparing the

actual expenses

with the

budgeted one.

Budgeting

Techniques and

MS Excel

Software

2nd Quarter Senior

Accountan

t and

Operation

Manager

of

company.

3 General Apart from General 1st Quarter Human

7 Morden, T. (2016). Principles of strategic management. Routledge

MANAGE BUDGETS AND FINANCIAL PLANS

which are genuine in nature are applicable for reimbursement. In addition to this, the

company also takes its petty cash and tracking of expenses policy quite seriously so that

adequate cash flow can be maintained. The petty cash needs to be maintained properly by a

person who can be held accountable for the same. The petty cash provides appropriate funds

in the hand of management so that they can meet some urgent obligation which might come

up. The business also aims to make use of spreadsheet for managing the expenses and also

for properly recording the same. It is also to be noted that maintenance of petty cash ledger

should be maintained by two or more person so that if person falls sick, the recording process

is not hampered in any manner7. The petty cash which is maintained by the business is used

for reimbursement for the employees in regards to some expenses undertaken.

Training plan

# Skills/

knowledge to

be developed

Training

method

Resources

Required

Timeframe Review

date and

by whom?Start Finish

1 Application of

Spreadsheet

and use of

formulas

Training will be

provided through

practical use of

spreadsheet with

required formula

and functions

Computer

Software

2nd Quarter Operations

Manager.

2 Tracking the

company’s

Expenses

Spreadsheet

application will

be used for

tracking and

maintaining the

details of

business

expenses.

Further, budgets

will be used for

comparing the

actual expenses

with the

budgeted one.

Budgeting

Techniques and

MS Excel

Software

2nd Quarter Senior

Accountan

t and

Operation

Manager

of

company.

3 General Apart from General 1st Quarter Human

7 Morden, T. (2016). Principles of strategic management. Routledge

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

MANAGE BUDGETS AND FINANCIAL PLANS

training for

new

recruitment

induction

training they will

be provided

training required

based on the

posts for which

they have been

recruited

resources of

company.

Resource

Manager

of

company.

4

Sales

operations

Handling sales

records and

developing

communication

skills

Ledger sales

records ledger

for maintaining

sales and

vocational

training

1st Quarter Sales

Manager

of

company

5 Motivational

training and

Induction

training

Surveys and

presentations

will be used

Past

performance

and positioning

of the entity’s

business under

market surveys,

graphs, records

and charts.

1st Quarter CEO and

Managing

Director of

entity.

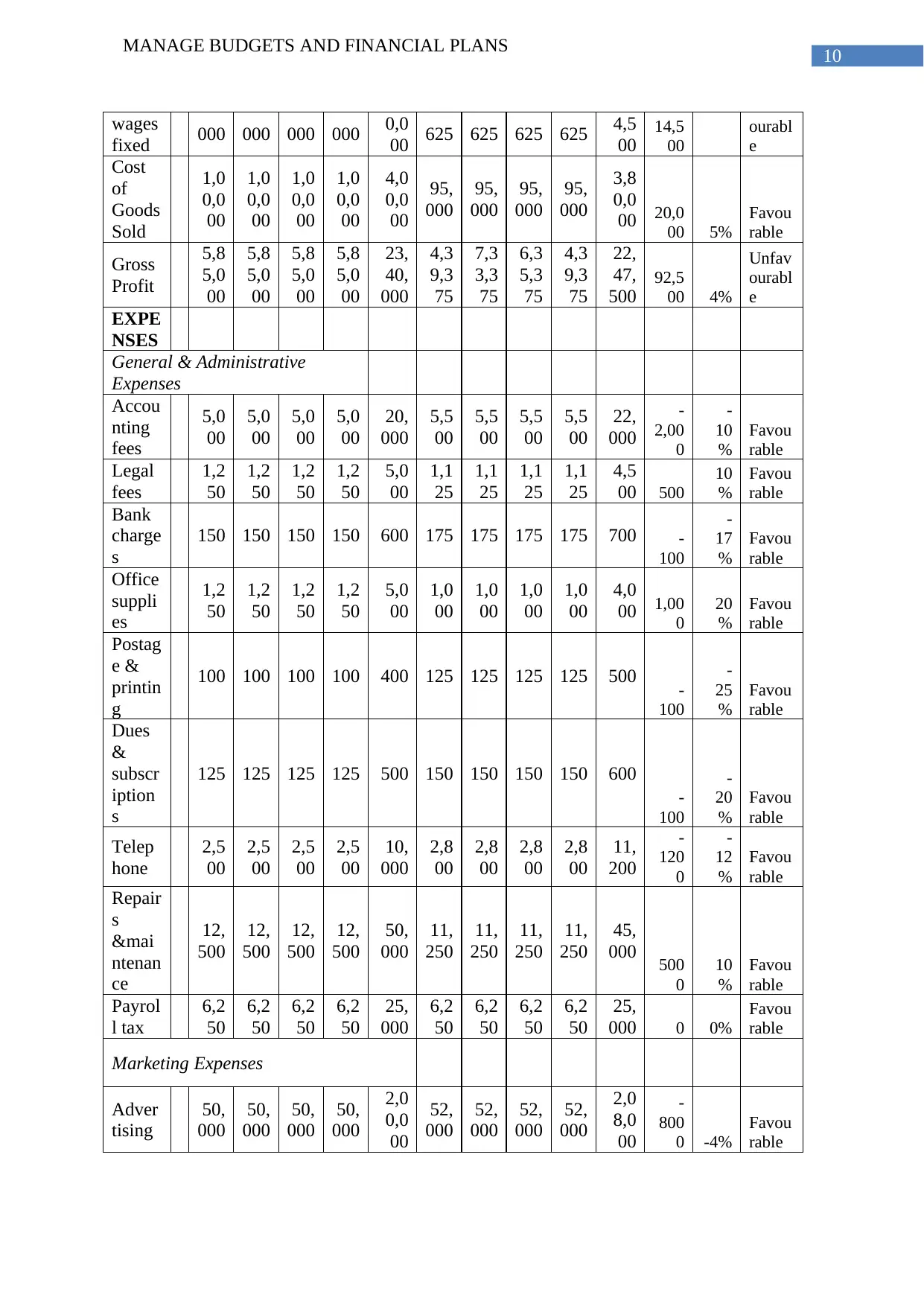

Assessment 3

Big Red Bicycle Pty Ltd

variance Report for the Year 2011/2012

Master Budget FY 2011/2012 Actual FY 2011/2012

Variance FY

2011/2012

Q1 Q2 Q3 Q4

Ful

l

Yea

r

Q1 Q2 Q3 Q4

Ful

l

Yea

r

Var

ian

ce

Var

ian

ce

%

Favo

urabl

e or

unfav

oura

ble

REV

ENU

E

Sales

7,5

0,0

00

7,5

0,0

00

7,5

0,0

00

7,5

0,0

00

30,

00,

000

6,0

0,0

00

9,0

0,0

00

8,0

0,0

00

6,0

0,0

00

29,

00,

000

1,00

,000 3%

Unfav

ourabl

e

Com

missio

ns

(2%

sales)

15,

000

15,

000

15,

000

15,

000

60,

000

12,

000

18,

000

16,

000

12,

000

58,

000 2,00

0 3%

Favou

rable

Direct 50, 50, 50, 50, 2,0 53, 53, 53, 53, 2,1 - -7% Unfav

MANAGE BUDGETS AND FINANCIAL PLANS

training for

new

recruitment

induction

training they will

be provided

training required

based on the

posts for which

they have been

recruited

resources of

company.

Resource

Manager

of

company.

4

Sales

operations

Handling sales

records and

developing

communication

skills

Ledger sales

records ledger

for maintaining

sales and

vocational

training

1st Quarter Sales

Manager

of

company

5 Motivational

training and

Induction

training

Surveys and

presentations

will be used

Past

performance

and positioning

of the entity’s

business under

market surveys,

graphs, records

and charts.

1st Quarter CEO and

Managing

Director of

entity.

Assessment 3

Big Red Bicycle Pty Ltd

variance Report for the Year 2011/2012

Master Budget FY 2011/2012 Actual FY 2011/2012

Variance FY

2011/2012

Q1 Q2 Q3 Q4

Ful

l

Yea

r

Q1 Q2 Q3 Q4

Ful

l

Yea

r

Var

ian

ce

Var

ian

ce

%

Favo

urabl

e or

unfav

oura

ble

REV

ENU

E

Sales

7,5

0,0

00

7,5

0,0

00

7,5

0,0

00

7,5

0,0

00

30,

00,

000

6,0

0,0

00

9,0

0,0

00

8,0

0,0

00

6,0

0,0

00

29,

00,

000

1,00

,000 3%

Unfav

ourabl

e

Com

missio

ns

(2%

sales)

15,

000

15,

000

15,

000

15,

000

60,

000

12,

000

18,

000

16,

000

12,

000

58,

000 2,00

0 3%

Favou

rable

Direct 50, 50, 50, 50, 2,0 53, 53, 53, 53, 2,1 - -7% Unfav

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

MANAGE BUDGETS AND FINANCIAL PLANS

wages

fixed 000 000 000 000 0,0

00 625 625 625 625 4,5

00

14,5

00

ourabl

e

Cost

of

Goods

Sold

1,0

0,0

00

1,0

0,0

00

1,0

0,0

00

1,0

0,0

00

4,0

0,0

00

95,

000

95,

000

95,

000

95,

000

3,8

0,0

00 20,0

00 5%

Favou

rable

Gross

Profit

5,8

5,0

00

5,8

5,0

00

5,8

5,0

00

5,8

5,0

00

23,

40,

000

4,3

9,3

75

7,3

3,3

75

6,3

5,3

75

4,3

9,3

75

22,

47,

500

92,5

00 4%

Unfav

ourabl

e

EXPE

NSES

General & Administrative

Expenses

Accou

nting

fees

5,0

00

5,0

00

5,0

00

5,0

00

20,

000

5,5

00

5,5

00

5,5

00

5,5

00

22,

000

-

2,00

0

-

10

%

Favou

rable

Legal

fees

1,2

50

1,2

50

1,2

50

1,2

50

5,0

00

1,1

25

1,1

25

1,1

25

1,1

25

4,5

00 500

10

%

Favou

rable

Bank

charge

s

150 150 150 150 600 175 175 175 175 700 -

100

-

17

%

Favou

rable

Office

suppli

es

1,2

50

1,2

50

1,2

50

1,2

50

5,0

00

1,0

00

1,0

00

1,0

00

1,0

00

4,0

00 1,00

0

20

%

Favou

rable

Postag

e &

printin

g

100 100 100 100 400 125 125 125 125 500 -

100

-

25

%

Favou

rable

Dues

&

subscr

iption

s

125 125 125 125 500 150 150 150 150 600

-

100

-

20

%

Favou

rable

Telep

hone

2,5

00

2,5

00

2,5

00

2,5

00

10,

000

2,8

00

2,8

00

2,8

00

2,8

00

11,

200

-

120

0

-

12

%

Favou

rable

Repair

s

&mai

ntenan

ce

12,

500

12,

500

12,

500

12,

500

50,

000

11,

250

11,

250

11,

250

11,

250

45,

000 500

0

10

%

Favou

rable

Payrol

l tax

6,2

50

6,2

50

6,2

50

6,2

50

25,

000

6,2

50

6,2

50

6,2

50

6,2

50

25,

000 0 0%

Favou

rable

Marketing Expenses

Adver

tising

50,

000

50,

000

50,

000

50,

000

2,0

0,0

00

52,

000

52,

000

52,

000

52,

000

2,0

8,0

00

-

800

0 -4%

Favou

rable

MANAGE BUDGETS AND FINANCIAL PLANS

wages

fixed 000 000 000 000 0,0

00 625 625 625 625 4,5

00

14,5

00

ourabl

e

Cost

of

Goods

Sold

1,0

0,0

00

1,0

0,0

00

1,0

0,0

00

1,0

0,0

00

4,0

0,0

00

95,

000

95,

000

95,

000

95,

000

3,8

0,0

00 20,0

00 5%

Favou

rable

Gross

Profit

5,8

5,0

00

5,8

5,0

00

5,8

5,0

00

5,8

5,0

00

23,

40,

000

4,3

9,3

75

7,3

3,3

75

6,3

5,3

75

4,3

9,3

75

22,

47,

500

92,5

00 4%

Unfav

ourabl

e

EXPE

NSES

General & Administrative

Expenses

Accou

nting

fees

5,0

00

5,0

00

5,0

00

5,0

00

20,

000

5,5

00

5,5

00

5,5

00

5,5

00

22,

000

-

2,00

0

-

10

%

Favou

rable

Legal

fees

1,2

50

1,2

50

1,2

50

1,2

50

5,0

00

1,1

25

1,1

25

1,1

25

1,1

25

4,5

00 500

10

%

Favou

rable

Bank

charge

s

150 150 150 150 600 175 175 175 175 700 -

100

-

17

%

Favou

rable

Office

suppli

es

1,2

50

1,2

50

1,2

50

1,2

50

5,0

00

1,0

00

1,0

00

1,0

00

1,0

00

4,0

00 1,00

0

20

%

Favou

rable

Postag

e &

printin

g

100 100 100 100 400 125 125 125 125 500 -

100

-

25

%

Favou

rable

Dues

&

subscr

iption

s

125 125 125 125 500 150 150 150 150 600

-

100

-

20

%

Favou

rable

Telep

hone

2,5

00

2,5

00

2,5

00

2,5

00

10,

000

2,8

00

2,8

00

2,8

00

2,8

00

11,

200

-

120

0

-

12

%

Favou

rable

Repair

s

&mai

ntenan

ce

12,

500

12,

500

12,

500

12,

500

50,

000

11,

250

11,

250

11,

250

11,

250

45,

000 500

0

10

%

Favou

rable

Payrol

l tax

6,2

50

6,2

50

6,2

50

6,2

50

25,

000

6,2

50

6,2

50

6,2

50

6,2

50

25,

000 0 0%

Favou

rable

Marketing Expenses

Adver

tising

50,

000

50,

000

50,

000

50,

000

2,0

0,0

00

52,

000

52,

000

52,

000

52,

000

2,0

8,0

00

-

800

0 -4%

Favou

rable

11

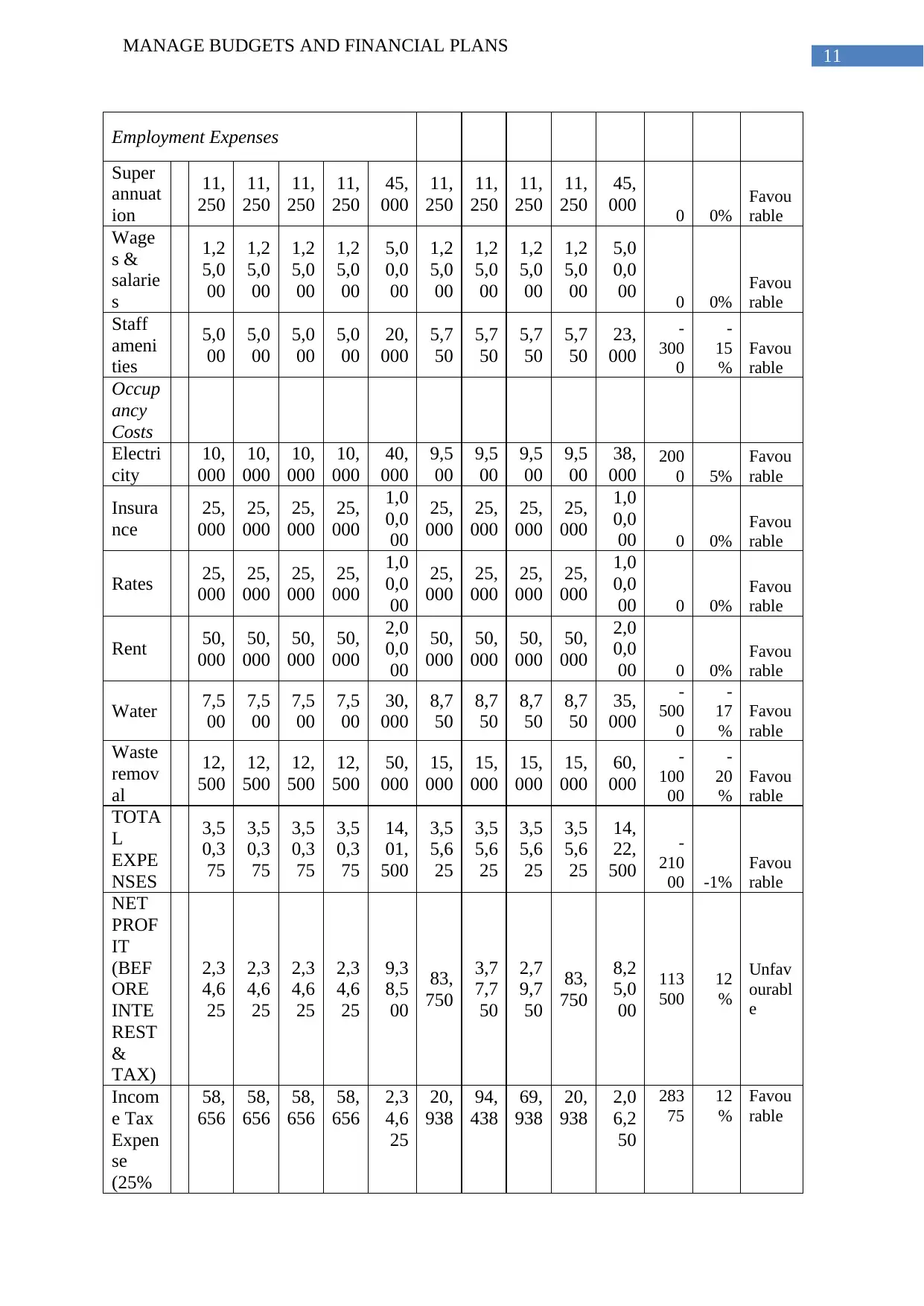

MANAGE BUDGETS AND FINANCIAL PLANS

Employment Expenses

Super

annuat

ion

11,

250

11,

250

11,

250

11,

250

45,

000

11,

250

11,

250

11,

250

11,

250

45,

000 0 0%

Favou

rable

Wage

s &

salarie

s

1,2

5,0

00

1,2

5,0

00

1,2

5,0

00

1,2

5,0

00

5,0

0,0

00

1,2

5,0

00

1,2

5,0

00

1,2

5,0

00

1,2

5,0

00

5,0

0,0

00 0 0%

Favou

rable

Staff

ameni

ties

5,0

00

5,0

00

5,0

00

5,0

00

20,

000

5,7

50

5,7

50

5,7

50

5,7

50

23,

000

-

300

0

-

15

%

Favou

rable

Occup

ancy

Costs

Electri

city

10,

000

10,

000

10,

000

10,

000

40,

000

9,5

00

9,5

00

9,5

00

9,5

00

38,

000

200

0 5%

Favou

rable

Insura

nce

25,

000

25,

000

25,

000

25,

000

1,0

0,0

00

25,

000

25,

000

25,

000

25,

000

1,0

0,0

00 0 0%

Favou

rable

Rates 25,

000

25,

000

25,

000

25,

000

1,0

0,0

00

25,

000

25,

000

25,

000

25,

000

1,0

0,0

00 0 0%

Favou

rable

Rent 50,

000

50,

000

50,

000

50,

000

2,0

0,0

00

50,

000

50,

000

50,

000

50,

000

2,0

0,0

00 0 0%

Favou

rable

Water 7,5

00

7,5

00

7,5

00

7,5

00

30,

000

8,7

50

8,7

50

8,7

50

8,7

50

35,

000

-

500

0

-

17

%

Favou

rable

Waste

remov

al

12,

500

12,

500

12,

500

12,

500

50,

000

15,

000

15,

000

15,

000

15,

000

60,

000

-

100

00

-

20

%

Favou

rable

TOTA

L

EXPE

NSES

3,5

0,3

75

3,5

0,3

75

3,5

0,3

75

3,5

0,3

75

14,

01,

500

3,5

5,6

25

3,5

5,6

25

3,5

5,6

25

3,5

5,6

25

14,

22,

500

-

210

00 -1%

Favou

rable

NET

PROF

IT

(BEF

ORE

INTE

REST

&

TAX)

2,3

4,6

25

2,3

4,6

25

2,3

4,6

25

2,3

4,6

25

9,3

8,5

00

83,

750

3,7

7,7

50

2,7

9,7

50

83,

750

8,2

5,0

00

113

500

12

%

Unfav

ourabl

e

Incom

e Tax

Expen

se

(25%

58,

656

58,

656

58,

656

58,

656

2,3

4,6

25

20,

938

94,

438

69,

938

20,

938

2,0

6,2

50

283

75

12

%

Favou

rable

MANAGE BUDGETS AND FINANCIAL PLANS

Employment Expenses

Super

annuat

ion

11,

250

11,

250

11,

250

11,

250

45,

000

11,

250

11,

250

11,

250

11,

250

45,

000 0 0%

Favou

rable

Wage

s &

salarie

s

1,2

5,0

00

1,2

5,0

00

1,2

5,0

00

1,2

5,0

00

5,0

0,0

00

1,2

5,0

00

1,2

5,0

00

1,2

5,0

00

1,2

5,0

00

5,0

0,0

00 0 0%

Favou

rable

Staff

ameni

ties

5,0

00

5,0

00

5,0

00

5,0

00

20,

000

5,7

50

5,7

50

5,7

50

5,7

50

23,

000

-

300

0

-

15

%

Favou

rable

Occup

ancy

Costs

Electri

city

10,

000

10,

000

10,

000

10,

000

40,

000

9,5

00

9,5

00

9,5

00

9,5

00

38,

000

200

0 5%

Favou

rable

Insura

nce

25,

000

25,

000

25,

000

25,

000

1,0

0,0

00

25,

000

25,

000

25,

000

25,

000

1,0

0,0

00 0 0%

Favou

rable

Rates 25,

000

25,

000

25,

000

25,

000

1,0

0,0

00

25,

000

25,

000

25,

000

25,

000

1,0

0,0

00 0 0%

Favou

rable

Rent 50,

000

50,

000

50,

000

50,

000

2,0

0,0

00

50,

000

50,

000

50,

000

50,

000

2,0

0,0

00 0 0%

Favou

rable

Water 7,5

00

7,5

00

7,5

00

7,5

00

30,

000

8,7

50

8,7

50

8,7

50

8,7

50

35,

000

-

500

0

-

17

%

Favou

rable

Waste

remov

al

12,

500

12,

500

12,

500

12,

500

50,

000

15,

000

15,

000

15,

000

15,

000

60,

000

-

100

00

-

20

%

Favou

rable

TOTA

L

EXPE

NSES

3,5

0,3

75

3,5

0,3

75

3,5

0,3

75

3,5

0,3

75

14,

01,

500

3,5

5,6

25

3,5

5,6

25

3,5

5,6

25

3,5

5,6

25

14,

22,

500

-

210

00 -1%

Favou

rable

NET

PROF

IT

(BEF

ORE

INTE

REST

&

TAX)

2,3

4,6

25

2,3

4,6

25

2,3

4,6

25

2,3

4,6

25

9,3

8,5

00

83,

750

3,7

7,7

50

2,7

9,7

50

83,

750

8,2

5,0

00

113

500

12

%

Unfav

ourabl

e

Incom

e Tax

Expen

se

(25%

58,

656

58,

656

58,

656

58,

656

2,3

4,6

25

20,

938

94,

438

69,

938

20,

938

2,0

6,2

50

283

75

12

%

Favou

rable

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.