Management Accounting & Financial Planning: Pricing, Budgeting & Tax

VerifiedAdded on 2023/06/17

|12

|3932

|179

Report

AI Summary

This report provides a comprehensive analysis of management accounting and financial planning, covering various aspects crucial for informed decision-making in business. It begins with a critical discussion of utilizing relevant costs for short-term pricing decisions, highlighting its limitations for long-term strategies and potential conflicts with traditional absorption costing. The report then evaluates the usefulness and limitations of capital investment techniques, such as Accounting Rate of Return (ARR), Payback Period, Net Present Value (NPV), Profitability Index (PI), and Internal Rate of Return (IRR), in choosing between alternative investment opportunities. Furthermore, it explores the role of budgeting in supporting enterprises beyond the Covid-19 pandemic, emphasizing its importance in financial planning and control. Finally, the report delves into the various means taxing authorities use to determine the reasonableness of transfer prices, ensuring compliance and minimizing tax liabilities. The report concludes by reinforcing the significance of management accounting and financial planning in achieving organizational goals and maintaining financial stability.

Management

Accounting and

Financial Planning

Accounting and

Financial Planning

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

TASK 1............................................................................................................................................1

A. Critical discussion of utilising the relevant cost to set selling price that may be appropriate

for short-term pricing decisions & inappropriate for long-term pricing decisions as well as

conflicts between reporting profitability under traditional absorption costing system and

utilisation of relevant cost based pricing................................................................................1

B. Conflicts between reporting profitability within traditional absorption costing system and

using relevant cost based pricing............................................................................................2

TASK 2............................................................................................................................................3

C. Critical evaluation of usefulness and limitations of capital investment techniques to choose

between alternative investment opportunities........................................................................3

TASK 3............................................................................................................................................7

D. Critically discuss the role of budgeting to support enterprise beyond the Covid 19

pandemic.................................................................................................................................7

TASK 4............................................................................................................................................8

E. Critical discussion of various means of taxing authorities to determine if a transfer price is

reasonable...............................................................................................................................8

CONCLUSION................................................................................................................................9

References:.....................................................................................................................................10

Books and Journals...............................................................................................................10

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

TASK 1............................................................................................................................................1

A. Critical discussion of utilising the relevant cost to set selling price that may be appropriate

for short-term pricing decisions & inappropriate for long-term pricing decisions as well as

conflicts between reporting profitability under traditional absorption costing system and

utilisation of relevant cost based pricing................................................................................1

B. Conflicts between reporting profitability within traditional absorption costing system and

using relevant cost based pricing............................................................................................2

TASK 2............................................................................................................................................3

C. Critical evaluation of usefulness and limitations of capital investment techniques to choose

between alternative investment opportunities........................................................................3

TASK 3............................................................................................................................................7

D. Critically discuss the role of budgeting to support enterprise beyond the Covid 19

pandemic.................................................................................................................................7

TASK 4............................................................................................................................................8

E. Critical discussion of various means of taxing authorities to determine if a transfer price is

reasonable...............................................................................................................................8

CONCLUSION................................................................................................................................9

References:.....................................................................................................................................10

Books and Journals...............................................................................................................10

INTRODUCTION

Management accounting refers to preparation of reports about the operations of business,

this help the organisation in making short term and long term decisions. Goals are achieved in

the business by identification, measurement, analysing information to the managers (Marota and

et al., 2017). Financial planning refers to a systematic approach to manage and control the

income and expenses. This report covers the discussion of strategies of short term and long term

in the business which helps them in setting prices. Capital investment techniques are also

discussed below with their usefulness and limitations. Along with the role of budgeting

technique in supporting the business during the time of COVID 19.

MAIN BODY

TASK 1

A. Critical discussion of utilising the relevant cost to set selling price that may be appropriate for

short-term pricing decisions & inappropriate for long-term pricing decisions as well as

conflicts between reporting profitability under traditional absorption costing system and

utilisation of relevant cost based pricing.

Relevant cost is a term of management accounting that tells the cost that pertain to a specific

decisions. This type of cost helps in elimination of information that are inessential in course of

business (Gutsalenko and et al., 2018). The motive behind this cost is to measure the objectivity

in the business. This cost is divided into four types, these four types of cost are discussed below:

Avoidable costs- This cost refers to the expenses which occur due to a specific activity, this

respective activity can be avoided in the business. Decline in this cost helps the business in

decreasing overall cost and maximizing the revenue of the business (Bochulia and Melnychenko,

2019). Avoidable cost are generally treated in period of short term as the company don’t disturb

the operations that run on a long term basis.

Future cash flow- This type of costing helps in estimating the expense that may occur in the

future course of business (Darma, 2018). A decline in the day to day cost will help in reducing

the actual cost of the products. Maintaining a short term cash flow is essential as the business

can’t exactly predict the cash scenario in a long term due to fluctuations and volatility in the

market conditions.

1

Management accounting refers to preparation of reports about the operations of business,

this help the organisation in making short term and long term decisions. Goals are achieved in

the business by identification, measurement, analysing information to the managers (Marota and

et al., 2017). Financial planning refers to a systematic approach to manage and control the

income and expenses. This report covers the discussion of strategies of short term and long term

in the business which helps them in setting prices. Capital investment techniques are also

discussed below with their usefulness and limitations. Along with the role of budgeting

technique in supporting the business during the time of COVID 19.

MAIN BODY

TASK 1

A. Critical discussion of utilising the relevant cost to set selling price that may be appropriate for

short-term pricing decisions & inappropriate for long-term pricing decisions as well as

conflicts between reporting profitability under traditional absorption costing system and

utilisation of relevant cost based pricing.

Relevant cost is a term of management accounting that tells the cost that pertain to a specific

decisions. This type of cost helps in elimination of information that are inessential in course of

business (Gutsalenko and et al., 2018). The motive behind this cost is to measure the objectivity

in the business. This cost is divided into four types, these four types of cost are discussed below:

Avoidable costs- This cost refers to the expenses which occur due to a specific activity, this

respective activity can be avoided in the business. Decline in this cost helps the business in

decreasing overall cost and maximizing the revenue of the business (Bochulia and Melnychenko,

2019). Avoidable cost are generally treated in period of short term as the company don’t disturb

the operations that run on a long term basis.

Future cash flow- This type of costing helps in estimating the expense that may occur in the

future course of business (Darma, 2018). A decline in the day to day cost will help in reducing

the actual cost of the products. Maintaining a short term cash flow is essential as the business

can’t exactly predict the cash scenario in a long term due to fluctuations and volatility in the

market conditions.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

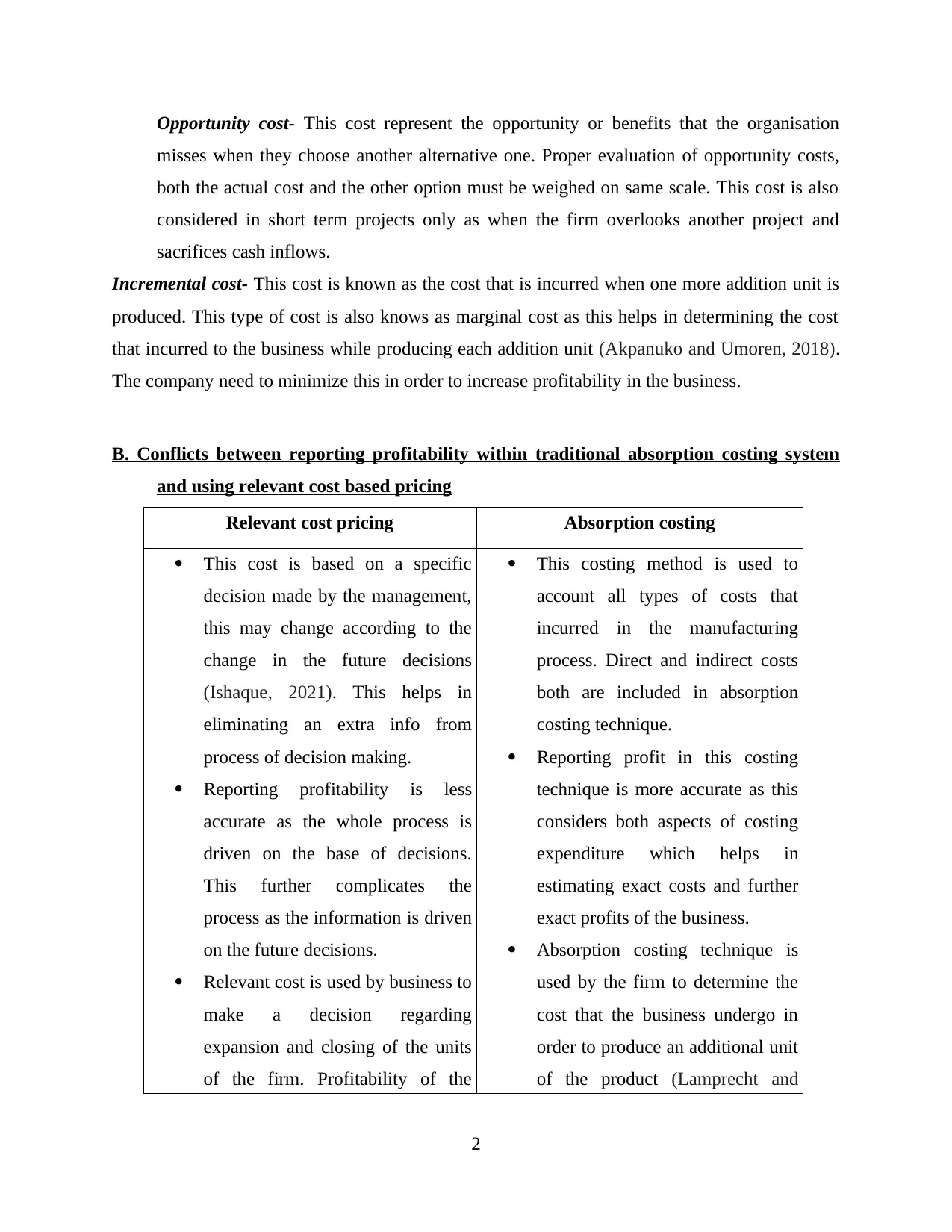

Opportunity cost- This cost represent the opportunity or benefits that the organisation

misses when they choose another alternative one. Proper evaluation of opportunity costs,

both the actual cost and the other option must be weighed on same scale. This cost is also

considered in short term projects only as when the firm overlooks another project and

sacrifices cash inflows.

Incremental cost- This cost is known as the cost that is incurred when one more addition unit is

produced. This type of cost is also knows as marginal cost as this helps in determining the cost

that incurred to the business while producing each addition unit (Akpanuko and Umoren, 2018).

The company need to minimize this in order to increase profitability in the business.

B. Conflicts between reporting profitability within traditional absorption costing system

and using relevant cost based pricing

Relevant cost pricing Absorption costing

This cost is based on a specific

decision made by the management,

this may change according to the

change in the future decisions

(Ishaque, 2021). This helps in

eliminating an extra info from

process of decision making.

Reporting profitability is less

accurate as the whole process is

driven on the base of decisions.

This further complicates the

process as the information is driven

on the future decisions.

Relevant cost is used by business to

make a decision regarding

expansion and closing of the units

of the firm. Profitability of the

This costing method is used to

account all types of costs that

incurred in the manufacturing

process. Direct and indirect costs

both are included in absorption

costing technique.

Reporting profit in this costing

technique is more accurate as this

considers both aspects of costing

expenditure which helps in

estimating exact costs and further

exact profits of the business.

Absorption costing technique is

used by the firm to determine the

cost that the business undergo in

order to produce an additional unit

of the product (Lamprecht and

2

misses when they choose another alternative one. Proper evaluation of opportunity costs,

both the actual cost and the other option must be weighed on same scale. This cost is also

considered in short term projects only as when the firm overlooks another project and

sacrifices cash inflows.

Incremental cost- This cost is known as the cost that is incurred when one more addition unit is

produced. This type of cost is also knows as marginal cost as this helps in determining the cost

that incurred to the business while producing each addition unit (Akpanuko and Umoren, 2018).

The company need to minimize this in order to increase profitability in the business.

B. Conflicts between reporting profitability within traditional absorption costing system

and using relevant cost based pricing

Relevant cost pricing Absorption costing

This cost is based on a specific

decision made by the management,

this may change according to the

change in the future decisions

(Ishaque, 2021). This helps in

eliminating an extra info from

process of decision making.

Reporting profitability is less

accurate as the whole process is

driven on the base of decisions.

This further complicates the

process as the information is driven

on the future decisions.

Relevant cost is used by business to

make a decision regarding

expansion and closing of the units

of the firm. Profitability of the

This costing method is used to

account all types of costs that

incurred in the manufacturing

process. Direct and indirect costs

both are included in absorption

costing technique.

Reporting profit in this costing

technique is more accurate as this

considers both aspects of costing

expenditure which helps in

estimating exact costs and further

exact profits of the business.

Absorption costing technique is

used by the firm to determine the

cost that the business undergo in

order to produce an additional unit

of the product (Lamprecht and

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company is maximized by closing a

dead unit of the business or

expanding in areas where there are

opportunities for business.

Guetterman, 2019).

TASK 2

C. Critical evaluation of usefulness and limitations of capital investment techniques to choose

between alternative investment opportunities

Capital investment techniques are considered in budgeting process that companies uses in

their projects in order to evaluate the profitability on that particular project over a certain

period of time. This technique is further applied on long term assets such as machinery,

equipment and real estate (Abad-Segura and et al., 2021). The ultimate objective of using

this process is to select the projects and assets which will yield maximum return to the

company over period of time. Businesses uses various techniques to do evaluate the capital

investment, few of them are discussed below:

Accounting Rate of Return (ARR): This refers to the percentage rate of return that the business

expect from its investment compared to the initial investment (Osadcha and et al., 2018). This

technique is used in firms to choose and evaluate different capital investments and further reach

on decision related to capital budgeting. This is calculated by a specific formula that is dividing

the average annual profits with the average investment. The formula is mentioned below:

ARR= Average annual profit/ average investment * 100

Usefulness of ARR: Using ARR technique in the business bring some major advantages,

few of them are discussed below:

Maximization of financial condition- Every business makes an investment in order

to gain some profit, the process of capital formation over the year could be difficult

to report. ARR helps in reporting exact percentage of return that the business has

earned or will earn in future from that particular project.

Helps in decision making process- ARR helps in comparing two projects based on

their potential to give return in the future. This helps the business in choosing one

3

dead unit of the business or

expanding in areas where there are

opportunities for business.

Guetterman, 2019).

TASK 2

C. Critical evaluation of usefulness and limitations of capital investment techniques to choose

between alternative investment opportunities

Capital investment techniques are considered in budgeting process that companies uses in

their projects in order to evaluate the profitability on that particular project over a certain

period of time. This technique is further applied on long term assets such as machinery,

equipment and real estate (Abad-Segura and et al., 2021). The ultimate objective of using

this process is to select the projects and assets which will yield maximum return to the

company over period of time. Businesses uses various techniques to do evaluate the capital

investment, few of them are discussed below:

Accounting Rate of Return (ARR): This refers to the percentage rate of return that the business

expect from its investment compared to the initial investment (Osadcha and et al., 2018). This

technique is used in firms to choose and evaluate different capital investments and further reach

on decision related to capital budgeting. This is calculated by a specific formula that is dividing

the average annual profits with the average investment. The formula is mentioned below:

ARR= Average annual profit/ average investment * 100

Usefulness of ARR: Using ARR technique in the business bring some major advantages,

few of them are discussed below:

Maximization of financial condition- Every business makes an investment in order

to gain some profit, the process of capital formation over the year could be difficult

to report. ARR helps in reporting exact percentage of return that the business has

earned or will earn in future from that particular project.

Helps in decision making process- ARR helps in comparing two projects based on

their potential to give return in the future. This helps the business in choosing one

3

project over another and making a rigid decision while acquiring new assets in the

company.

Limitations of ARR: This technique like any other techniques has some major

drawbacks, few of them are discussed below:

ARR is totally based on the net returns and profit and ignores the other aspects

of the investment process which sometimes makes the decision making process

more hectic and confusing.

ARR ignores the concept of discounting factor due to which exact estimation

of return is not done in this technique.

Payback period:

The technique is used by firm to determine the period of time that the project will take in

order to payback the business with initial amount of investment. The lower the payback period

means that the project has good potential and is able to recover the invested amount in a very

short period of time (Di Fabio and Avallone, 2018). Whereas a higher payback period tells that

the project won’t be able to generate returns for a longer period of time as it is taking a lot of

time in recovering the initial amount of investment. The calculation of payback period is

performed by dividing the initial investment in the asset or product divided by the cash flow per

year.

Payback period= Initial investment/ Annual cash flow

Usefulness of Payback period:

Prediction of exact period of time- This technique enables the firm to determine the

exact period of time in which the company can generate the cost that is initially invested

by them. With the help of this the business can know after what point of time the

company will start making profit out of it. Helps in making investment decision- This helps in choosing between several projects,

the company would pick the project whose payback period is the least and is generating

constant returns for the business.

Limitations of payback period:

Ignores the concept of discounted factor- It ignores the discounting factor which does

not help in getting the exact time. The payback period attained from this process is not

accurate.

4

company.

Limitations of ARR: This technique like any other techniques has some major

drawbacks, few of them are discussed below:

ARR is totally based on the net returns and profit and ignores the other aspects

of the investment process which sometimes makes the decision making process

more hectic and confusing.

ARR ignores the concept of discounting factor due to which exact estimation

of return is not done in this technique.

Payback period:

The technique is used by firm to determine the period of time that the project will take in

order to payback the business with initial amount of investment. The lower the payback period

means that the project has good potential and is able to recover the invested amount in a very

short period of time (Di Fabio and Avallone, 2018). Whereas a higher payback period tells that

the project won’t be able to generate returns for a longer period of time as it is taking a lot of

time in recovering the initial amount of investment. The calculation of payback period is

performed by dividing the initial investment in the asset or product divided by the cash flow per

year.

Payback period= Initial investment/ Annual cash flow

Usefulness of Payback period:

Prediction of exact period of time- This technique enables the firm to determine the

exact period of time in which the company can generate the cost that is initially invested

by them. With the help of this the business can know after what point of time the

company will start making profit out of it. Helps in making investment decision- This helps in choosing between several projects,

the company would pick the project whose payback period is the least and is generating

constant returns for the business.

Limitations of payback period:

Ignores the concept of discounted factor- It ignores the discounting factor which does

not help in getting the exact time. The payback period attained from this process is not

accurate.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Formula does not apply everywhere- The formula of payback period is only applicable

on the years in which inflow of cash is constant and same. If the inflow of cash is

variable and volatile then this formula of payback period won’t work.

Net present value: This tool is used to ascertain the value of the project after a certain period of

time and on a specific period. This helps in predicting the value that the project will generate and

will be worth off after a specific period of time. Net present value is used to analyse if a project

is profitable or not for the company. The formula of NPV is:

NPV = Rt / (1+i)t

Usefulness of NPV: NPV has a lot of applications in business, few of them are discussed below:

Risk and uncertainty: This technique helps in analysing the risk associated with the

business. This helps in choosing a project that optimise with the risk that he business is

willing to take in future course of business.

Complexities of investment decision making: Net present value considers factors such

as discounted factor to get an exact value of the project. It solves complexities that are

associated with the investment, the business owner can easily chose between different

projects with the help of this technique.

Limitations of NPV: NPV like any other technique has a few limitations that effects the

operations of business, few of them are discussed below:

Ignores qualitative aspects of the project: NPV only focuses on quantitative aspects

and ignores the quality and life of the project. Due to this, managers will make an

uniformed decision about the project.

Ignores the time constraint- One project after 3 years might generate better returns than

the other but ultimately the other project might have good potential to give more returns

over its life.

Profitability Index (PI):

This technique helps in determining the present value of the project along with the

benefits that the company may avail in future. This technique is directly in relation with the

NPV:

Usefulness of Profitability Index (PI):

5

on the years in which inflow of cash is constant and same. If the inflow of cash is

variable and volatile then this formula of payback period won’t work.

Net present value: This tool is used to ascertain the value of the project after a certain period of

time and on a specific period. This helps in predicting the value that the project will generate and

will be worth off after a specific period of time. Net present value is used to analyse if a project

is profitable or not for the company. The formula of NPV is:

NPV = Rt / (1+i)t

Usefulness of NPV: NPV has a lot of applications in business, few of them are discussed below:

Risk and uncertainty: This technique helps in analysing the risk associated with the

business. This helps in choosing a project that optimise with the risk that he business is

willing to take in future course of business.

Complexities of investment decision making: Net present value considers factors such

as discounted factor to get an exact value of the project. It solves complexities that are

associated with the investment, the business owner can easily chose between different

projects with the help of this technique.

Limitations of NPV: NPV like any other technique has a few limitations that effects the

operations of business, few of them are discussed below:

Ignores qualitative aspects of the project: NPV only focuses on quantitative aspects

and ignores the quality and life of the project. Due to this, managers will make an

uniformed decision about the project.

Ignores the time constraint- One project after 3 years might generate better returns than

the other but ultimately the other project might have good potential to give more returns

over its life.

Profitability Index (PI):

This technique helps in determining the present value of the project along with the

benefits that the company may avail in future. This technique is directly in relation with the

NPV:

Usefulness of Profitability Index (PI):

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Control on expenses: This technique helps in managing the expenses as the profitability

index is more concerned about the income of the business (Jovanović and Vašiček,

2021). This looks if an investment has enough potential to increase the value of firm or

not.

Helps in comparing the time value of cash flows, this helps in determining the exact

value that the investment could yield to business.

Limitations of Profitability Index (PI):

Sunk cost of the investment is generally ignored while using this technique therefore the

company is not able to estimate the exact value of return from the investment

(Ramachandran and Kakani, 2020).

The information that is generated in by using this technique is based just on estimates and

therefore has a chance that the decision making process in this criteria is not correct.

Internal Rate of Return (IRR): This calculation is used by businesses to determine if a

particular investment is worth investing or not (Stockenstrand and Nilsson, 2017). The

assessment of this factor is done on the basis of interest that is yielded over the years on the

capital investment. The ideal internal rate of return should sum up to greater than the cost of

capital invested in that.

Usefulness of Internal rate of return (IRR): Choosing a project: IRR is helpful in choosing between two or projects as the rate of

return tells which project will be beneficial for the company in long term aspects. A

project with higher ARR is chosen over the project with a lower one. Can be mix used: IRR can be used with other capital investment techniques in order to

gain a more real and correct insight on the investment. With the help of this managers can

make correct decisions on the basis of several techniques.

Limitations of Internal Rate of Return (IRR):

Ignores the duration of project: This techniques does not take the lifecycle and

duration of the project and only takes the value of project in consideration. If a company

has two projects with an IRR of 15% and 20% respectively then the company will chose

the second one, ignoring the fact that the first one is of a longer term and will be able to

generate more revenue for the company.

6

index is more concerned about the income of the business (Jovanović and Vašiček,

2021). This looks if an investment has enough potential to increase the value of firm or

not.

Helps in comparing the time value of cash flows, this helps in determining the exact

value that the investment could yield to business.

Limitations of Profitability Index (PI):

Sunk cost of the investment is generally ignored while using this technique therefore the

company is not able to estimate the exact value of return from the investment

(Ramachandran and Kakani, 2020).

The information that is generated in by using this technique is based just on estimates and

therefore has a chance that the decision making process in this criteria is not correct.

Internal Rate of Return (IRR): This calculation is used by businesses to determine if a

particular investment is worth investing or not (Stockenstrand and Nilsson, 2017). The

assessment of this factor is done on the basis of interest that is yielded over the years on the

capital investment. The ideal internal rate of return should sum up to greater than the cost of

capital invested in that.

Usefulness of Internal rate of return (IRR): Choosing a project: IRR is helpful in choosing between two or projects as the rate of

return tells which project will be beneficial for the company in long term aspects. A

project with higher ARR is chosen over the project with a lower one. Can be mix used: IRR can be used with other capital investment techniques in order to

gain a more real and correct insight on the investment. With the help of this managers can

make correct decisions on the basis of several techniques.

Limitations of Internal Rate of Return (IRR):

Ignores the duration of project: This techniques does not take the lifecycle and

duration of the project and only takes the value of project in consideration. If a company

has two projects with an IRR of 15% and 20% respectively then the company will chose

the second one, ignoring the fact that the first one is of a longer term and will be able to

generate more revenue for the company.

6

This technique assumes that total cash inflows are reinvested at the same rate as the

initially project was. It ignores the true picture and company might not be able to report

the exact amount of profit under this technique.

TASK 3

D. Critically discuss the role of budgeting to support enterprise beyond the Covid 19 pandemic

A budget refers to an estimated statement that outlines the cost of activities that may incur during

the course of business. A specific format of budget contains the estimated or predicted revenue

and expenditure of the business (Mahmud and et al., 2019). Budgeting helps the organisation in

many ways, there are certain roles of budget in business. Few of these importance and roles of

budget in an organisation beyond the period of COVID 19 is discussed below:

Managing the commitments of all the time frames- Budgeting helps in managing

the commitments that are to be dealt in a short term and long term. Budgeting help

in ignoring the aspects of uncertainty to some extent. In times like COVID 19, the

companies got a little bit prepared as they aside some funds to use for

unforeseeable situation like this. This helps them in managing the working capital

requirement of the business.

Controllability on the managerial functionality- Budgeting made the task of

managers easy as they were able to control the functions of the business. Budget

helps in managing every function in the department. This brings more of a direction

in the work of administration, research and development, marketing and finance.

This helps these department in following a pattern, which decreases the

unnecessary expenditure.

Involvement of uncertainty in the business: COVID 19 like situation was

uncertain which put business operations in jeopardy. Budget helps in maintaining

funds to deal with these situations. While the business operations were totally off

and the company was unable to make much sales. At times like these there are

some costs that still incur in the business, these extra funds helps in managing these

costs.

Profitability review: Budgeting helps in gaining insights on the overall revenue and

profits generated by the business in a particular period of time. A properly allotted

7

initially project was. It ignores the true picture and company might not be able to report

the exact amount of profit under this technique.

TASK 3

D. Critically discuss the role of budgeting to support enterprise beyond the Covid 19 pandemic

A budget refers to an estimated statement that outlines the cost of activities that may incur during

the course of business. A specific format of budget contains the estimated or predicted revenue

and expenditure of the business (Mahmud and et al., 2019). Budgeting helps the organisation in

many ways, there are certain roles of budget in business. Few of these importance and roles of

budget in an organisation beyond the period of COVID 19 is discussed below:

Managing the commitments of all the time frames- Budgeting helps in managing

the commitments that are to be dealt in a short term and long term. Budgeting help

in ignoring the aspects of uncertainty to some extent. In times like COVID 19, the

companies got a little bit prepared as they aside some funds to use for

unforeseeable situation like this. This helps them in managing the working capital

requirement of the business.

Controllability on the managerial functionality- Budgeting made the task of

managers easy as they were able to control the functions of the business. Budget

helps in managing every function in the department. This brings more of a direction

in the work of administration, research and development, marketing and finance.

This helps these department in following a pattern, which decreases the

unnecessary expenditure.

Involvement of uncertainty in the business: COVID 19 like situation was

uncertain which put business operations in jeopardy. Budget helps in maintaining

funds to deal with these situations. While the business operations were totally off

and the company was unable to make much sales. At times like these there are

some costs that still incur in the business, these extra funds helps in managing these

costs.

Profitability review: Budgeting helps in gaining insights on the overall revenue and

profits generated by the business in a particular period of time. A properly allotted

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

budget increases the efficiency and productivity of the organisation. Evaluation of

the operations also becomes easy due to budgeting, as management can make

informed decision on dropping some existing parts of the business or expanding

further.

Planning orientation: Planning the activities in business is most important aspect

as this leads the organisation to its desired goals and objectives. Budgeting helps in

planning the activities and finance of the business. During COVID 19, an effective

planning according to the finance and budget helped businesses in sustaining. The

companies can plan the financial expenses on different projects and can work

accordingly.

Facilitate solutions for management conflicts: Fund allocation and the operations

of business needs to be in smooth flow in order to bring productivity in the

business. Conflicts between the structure of working and finance gets settled by the

help of budgeting. Various and different kinds of outlooks of people are merged in

one place.

Budgeting helps the business in overcoming these problems of the organisation. These

certain roles are fulfilled by the budgeting technique which helps the entity in attaining

the goals and objectives.

TASK 4

E. Critical discussion of various means of taxing authorities to determine if a transfer price is

reasonable

Transfer pricing is a practice in accounting that represents that one division charges on another

division for services and goods. This is the legal framework that is essential in various

enterprises even the multi-national companies (Piersiala, 2017). Tax authorities are the authority

under the governance that hold documentation for evaluation, collection and imposition of

taxation on the businesses. Administrative section of UK is Her Majesty’s Revenue & Customs

(HMRC) which is responsible for the Inland revenues, customs and excise duties. The transferral

prices in UK works under two frameworks, which are discussed below:

Arm length principle: Relevance of this indicator is to fiscal indicator stating facts and

figures which is established with the help of unfavourable methods to the transactories

8

the operations also becomes easy due to budgeting, as management can make

informed decision on dropping some existing parts of the business or expanding

further.

Planning orientation: Planning the activities in business is most important aspect

as this leads the organisation to its desired goals and objectives. Budgeting helps in

planning the activities and finance of the business. During COVID 19, an effective

planning according to the finance and budget helped businesses in sustaining. The

companies can plan the financial expenses on different projects and can work

accordingly.

Facilitate solutions for management conflicts: Fund allocation and the operations

of business needs to be in smooth flow in order to bring productivity in the

business. Conflicts between the structure of working and finance gets settled by the

help of budgeting. Various and different kinds of outlooks of people are merged in

one place.

Budgeting helps the business in overcoming these problems of the organisation. These

certain roles are fulfilled by the budgeting technique which helps the entity in attaining

the goals and objectives.

TASK 4

E. Critical discussion of various means of taxing authorities to determine if a transfer price is

reasonable

Transfer pricing is a practice in accounting that represents that one division charges on another

division for services and goods. This is the legal framework that is essential in various

enterprises even the multi-national companies (Piersiala, 2017). Tax authorities are the authority

under the governance that hold documentation for evaluation, collection and imposition of

taxation on the businesses. Administrative section of UK is Her Majesty’s Revenue & Customs

(HMRC) which is responsible for the Inland revenues, customs and excise duties. The transferral

prices in UK works under two frameworks, which are discussed below:

Arm length principle: Relevance of this indicator is to fiscal indicator stating facts and

figures which is established with the help of unfavourable methods to the transactories

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

which are difficult to manage. Determining the formation on which the dependence is high

is part of this principle. The OECD programme is classified into five methods, that are,

Resale pricing, Transactional Net margin, Comparable Uncontrolled price, Cost plus

strategy and Transacted profit split.

Statistical techniques: This technique involves a degree of comparison between

controllable nature transactions with the each other. While paying tax to the government

committees, this technique is helpful in maintaining a positive and reasonable decision

within the structure.

CONCLUSION

From the above report it can be concluded that there are different types of costing techniques

which are used in the businesses to report the cost incurred in a specific project or during the

course of a particular year. For capital investment also there are various techniques which

help the business in estimating the returns that the project will be able to generate in the near

future. Every one of these capital investment technique has their advantages and limitations,

the company need to optimize and choose the best according to the need of firm. Budgeting

is a technique used in organisations to ascertain and estimate the expenditure and revenue

that will incur in the future run of the business. Budgeting technique is very beneficial for

the business as it helps in solving several issues in the business.

9

is part of this principle. The OECD programme is classified into five methods, that are,

Resale pricing, Transactional Net margin, Comparable Uncontrolled price, Cost plus

strategy and Transacted profit split.

Statistical techniques: This technique involves a degree of comparison between

controllable nature transactions with the each other. While paying tax to the government

committees, this technique is helpful in maintaining a positive and reasonable decision

within the structure.

CONCLUSION

From the above report it can be concluded that there are different types of costing techniques

which are used in the businesses to report the cost incurred in a specific project or during the

course of a particular year. For capital investment also there are various techniques which

help the business in estimating the returns that the project will be able to generate in the near

future. Every one of these capital investment technique has their advantages and limitations,

the company need to optimize and choose the best according to the need of firm. Budgeting

is a technique used in organisations to ascertain and estimate the expenditure and revenue

that will incur in the future run of the business. Budgeting technique is very beneficial for

the business as it helps in solving several issues in the business.

9

References:

Books and Journals

Marota, R., and et al., 2017. Material flow cost accounting approach for sustainable supply chain

management system. International Journal of Supply Chain Management. 6(2). pp. 33-37.

Gutsalenko, L., and et al., 2018. Accounting control of capital investment management: realities

of Ukraine and Poland. Economic annals-XXI. (170). pp.79-84.

Darma, J., 2018. The role of top management support in the quality of financial accounting

information systems. Journal of Applied Economic Sciences. 13(4). pp. 1009-1020.

Mahmud, N., and et al., 2019. Total quality management and SME performance: The mediating

effect of innovation in Malaysia. Asia-Pacific Management Accounting Journal. 14(1).

pp. 201-217.

Bochulia, T. and Melnychenko, O., 2019. Accounting and analytical provision of management in

the times of information thinking. European Cooperation. 1(41). pp. 52-64.

Akpanuko, E.E. and Umoren, N.J., 2018. The influence of creative accounting on the credibility

of accounting reports. Journal of Financial Reporting and Accounting.

Ishaque, M., 2021. Managing conflict of interests in professional accounting firms: a research

synthesis. Journal of Business Ethics, 169(3). pp. 537-555.

Piersiala, L., 2017. Cost accounting for management of health services in a hospital. Acta

Universitatis Lodziensis. Folia Oeconomica, 3(329).

Abad-Segura, E., and et al., 2021. Blockchain Technology for Secure Accounting Management:

Research Trends Analysis. Mathematics, 9(14), p.1631.

Lamprecht, C. and Guetterman, T.C., 2019. Mixed methods in accounting: a field based

analysis. Meditari Accountancy Research.

Jovanović, T. and Vašiček, V., 2021. The role and application of accounting and budgeting

information in government financial management process—a qualitative study in

Slovenia. Public Money & Management, 41(2), pp.99-106.

Osadcha, O.O., and et al., 2018. Implementation of accounting processes as an alternative

method for organizing accounting. Financial and credit activity: problems of theory and

practice, 4(27), pp.193-200.

Ramachandran, N. and Kakani, R.K., 2020. Financial Accounting For Management|. McGraw-

Hill Education.

Di Fabio, C. and Avallone, F., 2018. Business model in accounting: An overview. Journal of

Business Models, 6(2), pp.25-31.

Stockenstrand, A.K. and Nilsson, F. eds., 2017. Bank Regulation: Effects on Strategy, Financial

Accounting and Management Control. Taylor & Francis.

10

Books and Journals

Marota, R., and et al., 2017. Material flow cost accounting approach for sustainable supply chain

management system. International Journal of Supply Chain Management. 6(2). pp. 33-37.

Gutsalenko, L., and et al., 2018. Accounting control of capital investment management: realities

of Ukraine and Poland. Economic annals-XXI. (170). pp.79-84.

Darma, J., 2018. The role of top management support in the quality of financial accounting

information systems. Journal of Applied Economic Sciences. 13(4). pp. 1009-1020.

Mahmud, N., and et al., 2019. Total quality management and SME performance: The mediating

effect of innovation in Malaysia. Asia-Pacific Management Accounting Journal. 14(1).

pp. 201-217.

Bochulia, T. and Melnychenko, O., 2019. Accounting and analytical provision of management in

the times of information thinking. European Cooperation. 1(41). pp. 52-64.

Akpanuko, E.E. and Umoren, N.J., 2018. The influence of creative accounting on the credibility

of accounting reports. Journal of Financial Reporting and Accounting.

Ishaque, M., 2021. Managing conflict of interests in professional accounting firms: a research

synthesis. Journal of Business Ethics, 169(3). pp. 537-555.

Piersiala, L., 2017. Cost accounting for management of health services in a hospital. Acta

Universitatis Lodziensis. Folia Oeconomica, 3(329).

Abad-Segura, E., and et al., 2021. Blockchain Technology for Secure Accounting Management:

Research Trends Analysis. Mathematics, 9(14), p.1631.

Lamprecht, C. and Guetterman, T.C., 2019. Mixed methods in accounting: a field based

analysis. Meditari Accountancy Research.

Jovanović, T. and Vašiček, V., 2021. The role and application of accounting and budgeting

information in government financial management process—a qualitative study in

Slovenia. Public Money & Management, 41(2), pp.99-106.

Osadcha, O.O., and et al., 2018. Implementation of accounting processes as an alternative

method for organizing accounting. Financial and credit activity: problems of theory and

practice, 4(27), pp.193-200.

Ramachandran, N. and Kakani, R.K., 2020. Financial Accounting For Management|. McGraw-

Hill Education.

Di Fabio, C. and Avallone, F., 2018. Business model in accounting: An overview. Journal of

Business Models, 6(2), pp.25-31.

Stockenstrand, A.K. and Nilsson, F. eds., 2017. Bank Regulation: Effects on Strategy, Financial

Accounting and Management Control. Taylor & Francis.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.