Kaplan DFP1 Financial Planning Fundamentals Assignment Solution

VerifiedAdded on 2020/05/04

|34

|9817

|173

Homework Assignment

AI Summary

This document presents a comprehensive solution to a Financial Planning Fundamentals (DFP1) assignment, focusing on the case study of Joe and Natalie Olden. The assignment requires an analysis of their financial situation, based on the provided fact find, including their assets, liabilities, income, and expenses. The solution likely involves determining their investment objectives, risk profile, and providing financial advice related to their goal of purchasing a house, considering their income, debts, and available savings. The solution will likely include calculations, recommendations, and a discussion of relevant financial planning principles and regulations. The assignment covers units of competency such as financial planning analysis, ethical guidelines, client needs, and financial product knowledge.

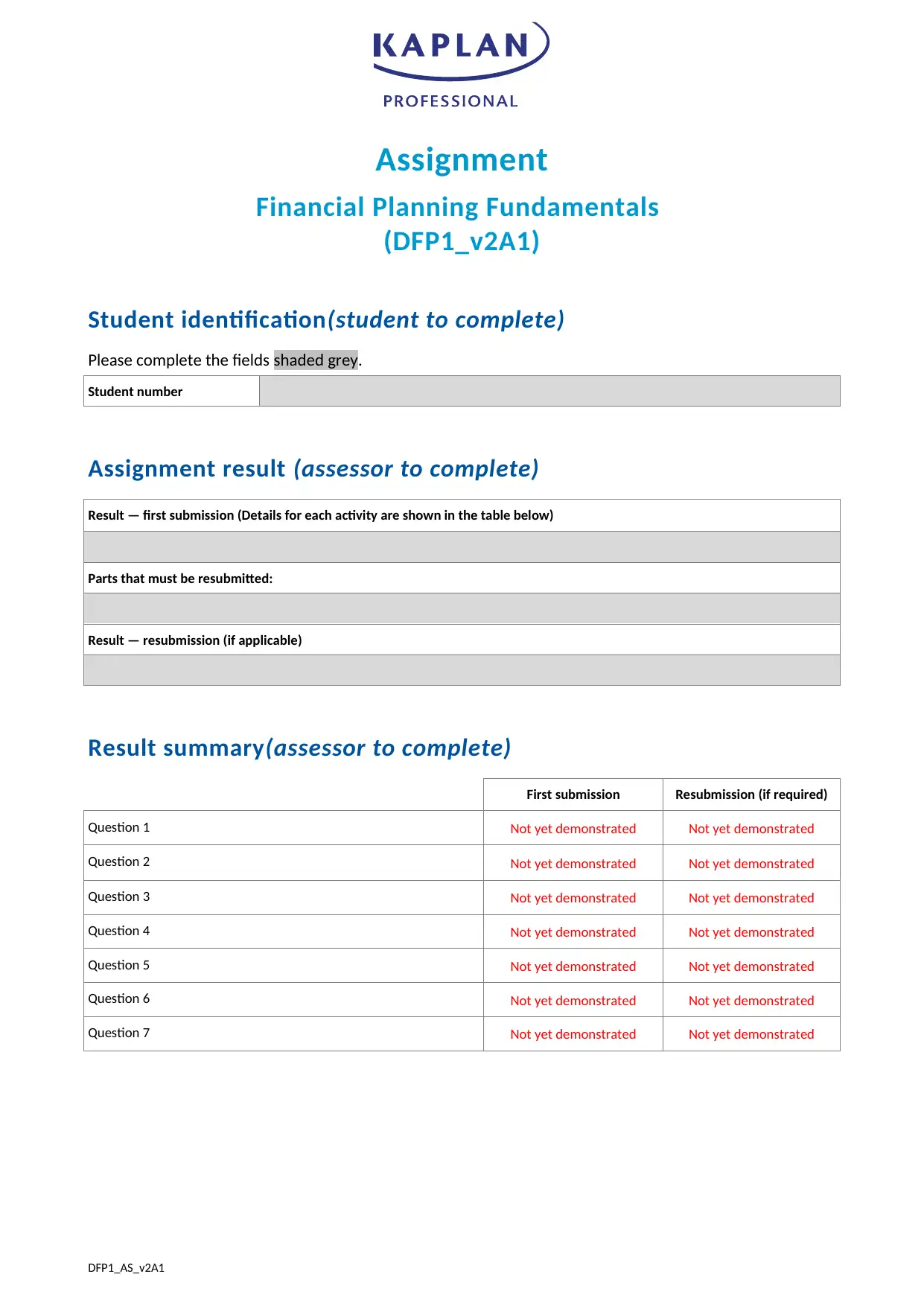

Assignment

Financial Planning Fundamentals

(DFP1_v2A1)

Student identification(student to complete)

Please complete the fields shaded grey.

Student number

Assignment result (assessor to complete)

Result — first submission (Details for each activity are shown in the table below)

Parts that must be resubmitted:

Result — resubmission (if applicable)

Result summary(assessor to complete)

First submission Resubmission (if required)

Question 1 Not yet demonstrated Not yet demonstrated

Question 2 Not yet demonstrated Not yet demonstrated

Question 3 Not yet demonstrated Not yet demonstrated

Question 4 Not yet demonstrated Not yet demonstrated

Question 5 Not yet demonstrated Not yet demonstrated

Question 6 Not yet demonstrated Not yet demonstrated

Question 7 Not yet demonstrated Not yet demonstrated

DFP1_AS_v2A1

Financial Planning Fundamentals

(DFP1_v2A1)

Student identification(student to complete)

Please complete the fields shaded grey.

Student number

Assignment result (assessor to complete)

Result — first submission (Details for each activity are shown in the table below)

Parts that must be resubmitted:

Result — resubmission (if applicable)

Result summary(assessor to complete)

First submission Resubmission (if required)

Question 1 Not yet demonstrated Not yet demonstrated

Question 2 Not yet demonstrated Not yet demonstrated

Question 3 Not yet demonstrated Not yet demonstrated

Question 4 Not yet demonstrated Not yet demonstrated

Question 5 Not yet demonstrated Not yet demonstrated

Question 6 Not yet demonstrated Not yet demonstrated

Question 7 Not yet demonstrated Not yet demonstrated

DFP1_AS_v2A1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Feedback (assessor to complete)

[insert assessor feedback]

Page 2 of 34

[insert assessor feedback]

Page 2 of 34

Before you begin

Read everything in this document before you start your assignment for Financial Planning Fundamentals

(DFP1v2).

About this document

This document includes the following parts:

• Part 1: Instructions for completing and submitting this assignment

• Part 2: Case study

• Part 3: Assignment questions.

How to use the study plan

We recommend that you use the study plan for this subject to help you manage your time to complete

the assignment within your enrolment period. Your study plan is in the KapLearn Financial Planning

Fundamentals (DFP1v2) subject room.

Part 1: Instructions for completing and submitting this

assignment

Word count

The word count shown with each question is indicative only. You will not be penalised for exceeding the

suggested word count. Please do not include additional information which is outside the scope of the

question.

Additional research

You will be required to complete additional research to answer the assignment questions.

Page 3 of 34

Read everything in this document before you start your assignment for Financial Planning Fundamentals

(DFP1v2).

About this document

This document includes the following parts:

• Part 1: Instructions for completing and submitting this assignment

• Part 2: Case study

• Part 3: Assignment questions.

How to use the study plan

We recommend that you use the study plan for this subject to help you manage your time to complete

the assignment within your enrolment period. Your study plan is in the KapLearn Financial Planning

Fundamentals (DFP1v2) subject room.

Part 1: Instructions for completing and submitting this

assignment

Word count

The word count shown with each question is indicative only. You will not be penalised for exceeding the

suggested word count. Please do not include additional information which is outside the scope of the

question.

Additional research

You will be required to complete additional research to answer the assignment questions.

Page 3 of 34

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Saving your work

Download this document to your desktop, type your answers in the spaces provided and save your

work regularly.

• Use the template provided, as other formats will not be accepted for this assignment.

• Name your file as follows: Studentnumber_SubjectCode_Submissionnumber

(e.g. 12345678_DFP1_Submission1).

• Include your student ID on the first page of the assignment.

Before you submit your work, please do a spell check and proofread your work to ensure that everything is

clear and unambiguous.

Submitting the assignment

You must submit your completed assignment in a compatible Microsoft Word document.

You need to save and submit this entire document.

Do not remove any sections of the document.

Do not save your completed assignment as a PDF.

The assignment must be completed before submitting it to Kaplan Professional. Incomplete assignments

will be returned to you unmarked.

The maximum file size is 5MB. Once you submit your assignment for marking you will be unable to make

any further changes to it.

You are able to submit your assignment earlier than the deadline if you are confident you have completed

all parts and have prepared a quality submission.

The assignment marking process

You have 12 weeks from the date of your enrolment in this subject to submit your completed assignment.

Should your assignment be deemed ‘not yet competent’ you will be give an additional four (4) weeks to

resubmit your assignment.

Your assessor will mark your assignment and return it to you in the Financial Planning Fundamentals

(DFP1v2) subject room in KapLearn under the ‘Assessment’ tab.

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all of the questions in

your assignment. Failure to do so will mean that your assignment will not be accepted for marking;

therefore you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your

submission deadline to submit your completed assignment.

Page 4 of 34

Download this document to your desktop, type your answers in the spaces provided and save your

work regularly.

• Use the template provided, as other formats will not be accepted for this assignment.

• Name your file as follows: Studentnumber_SubjectCode_Submissionnumber

(e.g. 12345678_DFP1_Submission1).

• Include your student ID on the first page of the assignment.

Before you submit your work, please do a spell check and proofread your work to ensure that everything is

clear and unambiguous.

Submitting the assignment

You must submit your completed assignment in a compatible Microsoft Word document.

You need to save and submit this entire document.

Do not remove any sections of the document.

Do not save your completed assignment as a PDF.

The assignment must be completed before submitting it to Kaplan Professional. Incomplete assignments

will be returned to you unmarked.

The maximum file size is 5MB. Once you submit your assignment for marking you will be unable to make

any further changes to it.

You are able to submit your assignment earlier than the deadline if you are confident you have completed

all parts and have prepared a quality submission.

The assignment marking process

You have 12 weeks from the date of your enrolment in this subject to submit your completed assignment.

Should your assignment be deemed ‘not yet competent’ you will be give an additional four (4) weeks to

resubmit your assignment.

Your assessor will mark your assignment and return it to you in the Financial Planning Fundamentals

(DFP1v2) subject room in KapLearn under the ‘Assessment’ tab.

Make a reasonable attempt

You must demonstrate that you have made a reasonable attempt to answer all of the questions in

your assignment. Failure to do so will mean that your assignment will not be accepted for marking;

therefore you will not receive the benefit of feedback on your submission.

If you do not meet these requirements, you will be notified. You will then have until your

submission deadline to submit your completed assignment.

Page 4 of 34

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

How your assignment is graded

Assignment tasks are used to determine your ‘competence’ in demonstrating the required knowledge

and/or skills for each subject. As a result, you will be graded as either competent or not yet competent.

Your assessor will follow the below process when marking your assignment:

• Assess your responses to each question, and sub-parts if applicable, and then determine whether you

have demonstrated competence in each question.

• Determine if, on a holistic basis, your responses to the questions have demonstrated overall competence.

‘Not yet competent’ and resubmissions

Should sections of your assignment be marked as ‘not yet competent’ you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the required level.

You must address the assessor’s feedback in your amended responses. You only need amend those sections

where the assessor has determined you are ‘not yet competent’.

Make changes to your original submission. Use a different text colour for your resubmission. Your assessor

will be in a better position to gauge the quality and nature of your changes. Ensure you leave your first

assessor’s comments in your assignment, so your second assessor can see the instructions that were

originally provided for you. Do not change any comments made by a Kaplan assessor.

Units of competency

This assignment is your opportunity to demonstrate your competency against these units:

FNSFPL502 Conduct financial planning analysis and research

FNSFPL501 Comply with financial planning practice ethical and operational guidelines and regulations

FNSFPL506 Determine client financial requirements and expectations

FNSINC401 Apply principles of professional practice to work in the financial services industry

BSBITU402 Develop and use complex spreadsheets

FNSASIC301 Establish client relationship and analyse needs

FNSASIC302 Develop, present and negotiate client solutions

FNSIAD301 Provide general advice on financial products and services

We are here to help

If you have any questions about this assignment you can post your query at the ‘Ask your Tutor’ forum in

your subject room. You can expect an answer within 24 hours of your posting from one of our technical

advisers or student support staff.

Page 5 of 34

Assignment tasks are used to determine your ‘competence’ in demonstrating the required knowledge

and/or skills for each subject. As a result, you will be graded as either competent or not yet competent.

Your assessor will follow the below process when marking your assignment:

• Assess your responses to each question, and sub-parts if applicable, and then determine whether you

have demonstrated competence in each question.

• Determine if, on a holistic basis, your responses to the questions have demonstrated overall competence.

‘Not yet competent’ and resubmissions

Should sections of your assignment be marked as ‘not yet competent’ you will be given an additional

opportunity to amend your responses so that you can demonstrate your competency to the required level.

You must address the assessor’s feedback in your amended responses. You only need amend those sections

where the assessor has determined you are ‘not yet competent’.

Make changes to your original submission. Use a different text colour for your resubmission. Your assessor

will be in a better position to gauge the quality and nature of your changes. Ensure you leave your first

assessor’s comments in your assignment, so your second assessor can see the instructions that were

originally provided for you. Do not change any comments made by a Kaplan assessor.

Units of competency

This assignment is your opportunity to demonstrate your competency against these units:

FNSFPL502 Conduct financial planning analysis and research

FNSFPL501 Comply with financial planning practice ethical and operational guidelines and regulations

FNSFPL506 Determine client financial requirements and expectations

FNSINC401 Apply principles of professional practice to work in the financial services industry

BSBITU402 Develop and use complex spreadsheets

FNSASIC301 Establish client relationship and analyse needs

FNSASIC302 Develop, present and negotiate client solutions

FNSIAD301 Provide general advice on financial products and services

We are here to help

If you have any questions about this assignment you can post your query at the ‘Ask your Tutor’ forum in

your subject room. You can expect an answer within 24 hours of your posting from one of our technical

advisers or student support staff.

Page 5 of 34

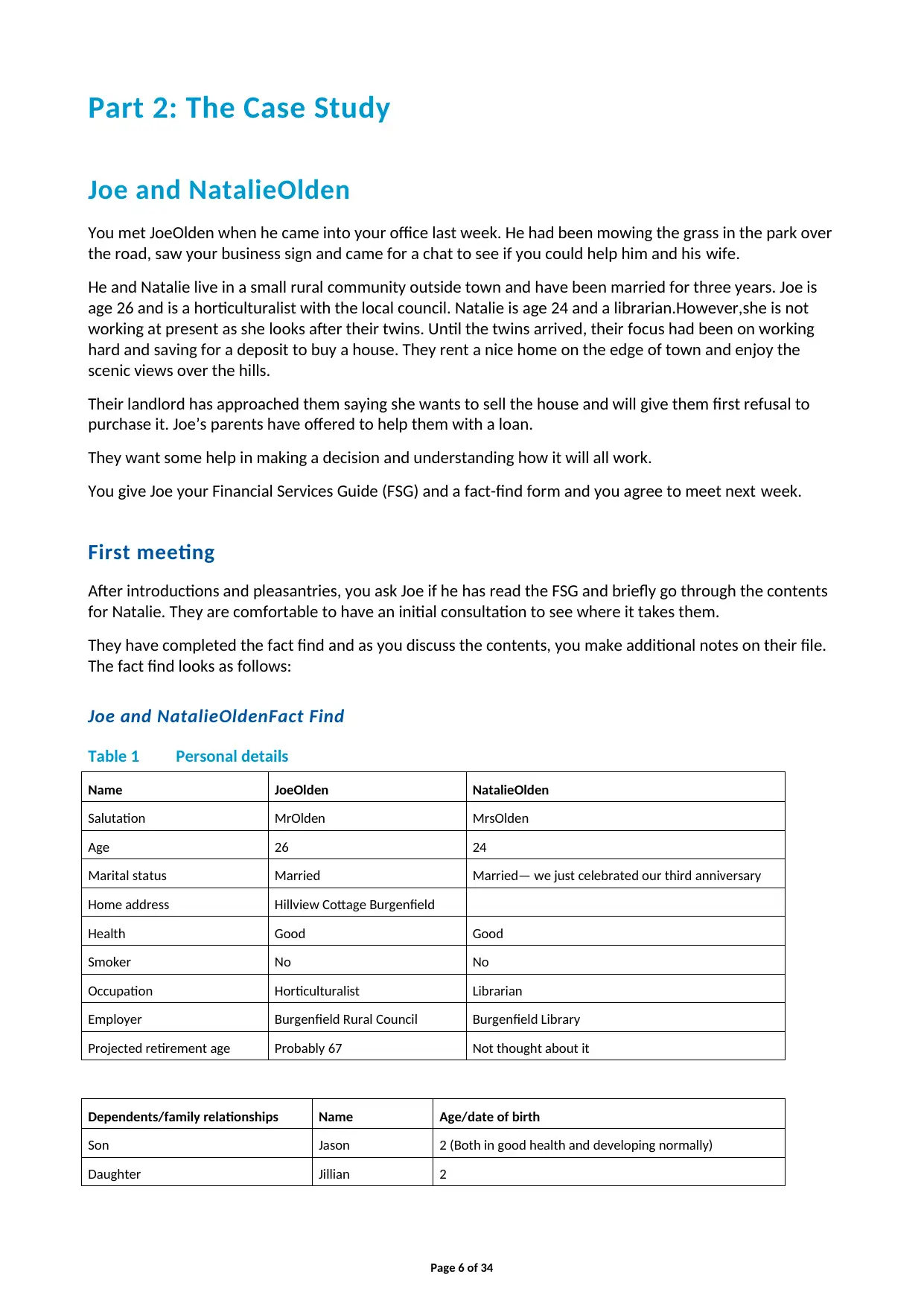

Part 2: The Case Study

Joe and NatalieOlden

You met JoeOlden when he came into your office last week. He had been mowing the grass in the park over

the road, saw your business sign and came for a chat to see if you could help him and his wife.

He and Natalie live in a small rural community outside town and have been married for three years. Joe is

age 26 and is a horticulturalist with the local council. Natalie is age 24 and a librarian.However,she is not

working at present as she looks after their twins. Until the twins arrived, their focus had been on working

hard and saving for a deposit to buy a house. They rent a nice home on the edge of town and enjoy the

scenic views over the hills.

Their landlord has approached them saying she wants to sell the house and will give them first refusal to

purchase it. Joe’s parents have offered to help them with a loan.

They want some help in making a decision and understanding how it will all work.

You give Joe your Financial Services Guide (FSG) and a fact-find form and you agree to meet next week.

First meeting

After introductions and pleasantries, you ask Joe if he has read the FSG and briefly go through the contents

for Natalie. They are comfortable to have an initial consultation to see where it takes them.

They have completed the fact find and as you discuss the contents, you make additional notes on their file.

The fact find looks as follows:

Joe and NatalieOldenFact Find

Table 1 Personal details

Name JoeOlden NatalieOlden

Salutation MrOlden MrsOlden

Age 26 24

Marital status Married Married— we just celebrated our third anniversary

Home address Hillview Cottage Burgenfield

Health Good Good

Smoker No No

Occupation Horticulturalist Librarian

Employer Burgenfield Rural Council Burgenfield Library

Projected retirement age Probably 67 Not thought about it

Dependents/family relationships Name Age/date of birth

Son Jason 2 (Both in good health and developing normally)

Daughter Jillian 2

Page 6 of 34

Joe and NatalieOlden

You met JoeOlden when he came into your office last week. He had been mowing the grass in the park over

the road, saw your business sign and came for a chat to see if you could help him and his wife.

He and Natalie live in a small rural community outside town and have been married for three years. Joe is

age 26 and is a horticulturalist with the local council. Natalie is age 24 and a librarian.However,she is not

working at present as she looks after their twins. Until the twins arrived, their focus had been on working

hard and saving for a deposit to buy a house. They rent a nice home on the edge of town and enjoy the

scenic views over the hills.

Their landlord has approached them saying she wants to sell the house and will give them first refusal to

purchase it. Joe’s parents have offered to help them with a loan.

They want some help in making a decision and understanding how it will all work.

You give Joe your Financial Services Guide (FSG) and a fact-find form and you agree to meet next week.

First meeting

After introductions and pleasantries, you ask Joe if he has read the FSG and briefly go through the contents

for Natalie. They are comfortable to have an initial consultation to see where it takes them.

They have completed the fact find and as you discuss the contents, you make additional notes on their file.

The fact find looks as follows:

Joe and NatalieOldenFact Find

Table 1 Personal details

Name JoeOlden NatalieOlden

Salutation MrOlden MrsOlden

Age 26 24

Marital status Married Married— we just celebrated our third anniversary

Home address Hillview Cottage Burgenfield

Health Good Good

Smoker No No

Occupation Horticulturalist Librarian

Employer Burgenfield Rural Council Burgenfield Library

Projected retirement age Probably 67 Not thought about it

Dependents/family relationships Name Age/date of birth

Son Jason 2 (Both in good health and developing normally)

Daughter Jillian 2

Page 6 of 34

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

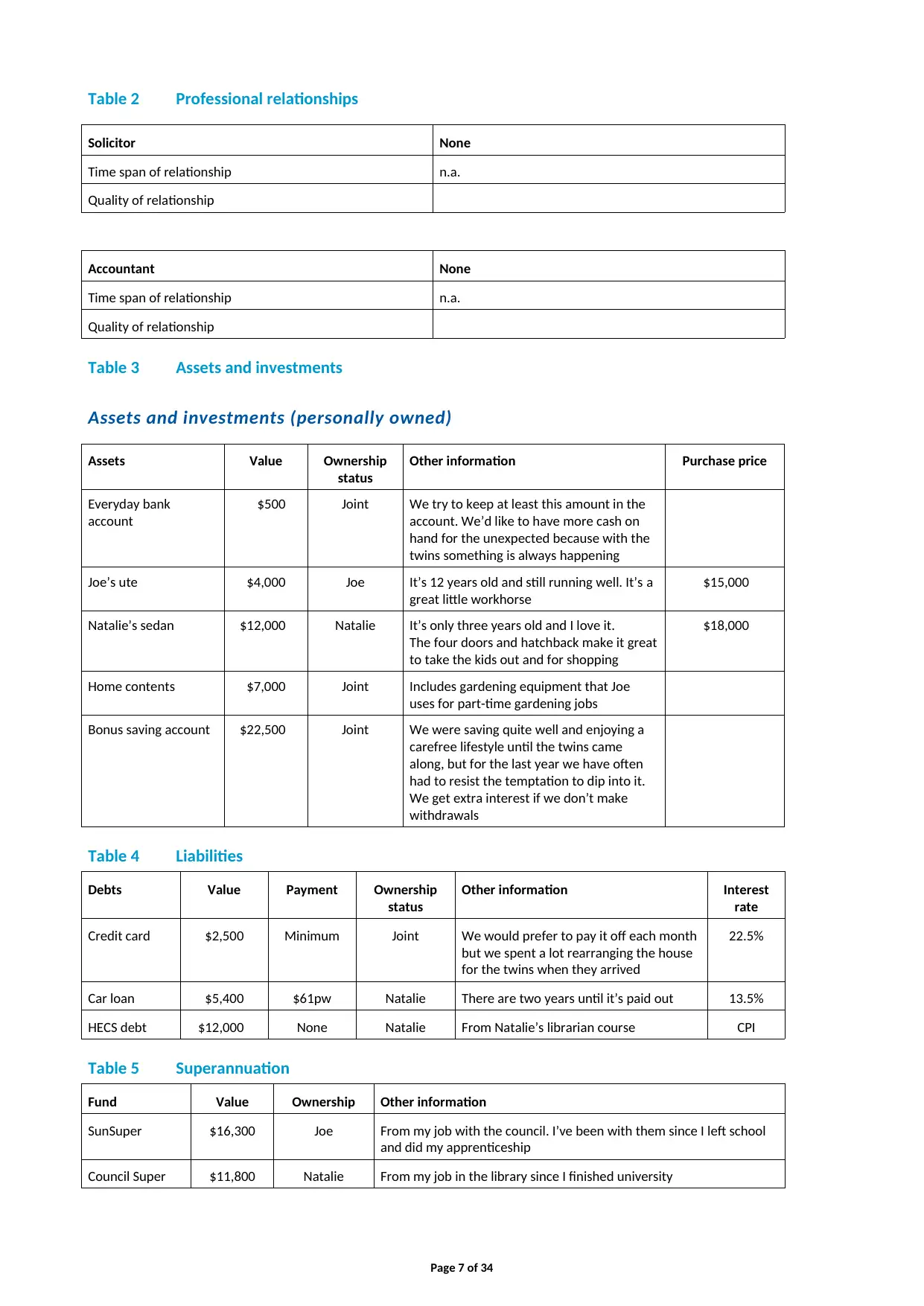

Table 2 Professional relationships

Solicitor None

Time span of relationship n.a.

Quality of relationship

Accountant None

Time span of relationship n.a.

Quality of relationship

Table 3 Assets and investments

Assets and investments (personally owned)

Assets Value Ownership

status

Other information Purchase price

Everyday bank

account

$500 Joint We try to keep at least this amount in the

account. We’d like to have more cash on

hand for the unexpected because with the

twins something is always happening

Joe’s ute $4,000 Joe It’s 12 years old and still running well. It’s a

great little workhorse

$15,000

Natalie’s sedan $12,000 Natalie It’s only three years old and I love it.

The four doors and hatchback make it great

to take the kids out and for shopping

$18,000

Home contents $7,000 Joint Includes gardening equipment that Joe

uses for part-time gardening jobs

Bonus saving account $22,500 Joint We were saving quite well and enjoying a

carefree lifestyle until the twins came

along, but for the last year we have often

had to resist the temptation to dip into it.

We get extra interest if we don’t make

withdrawals

Table 4 Liabilities

Debts Value Payment Ownership

status

Other information Interest

rate

Credit card $2,500 Minimum Joint We would prefer to pay it off each month

but we spent a lot rearranging the house

for the twins when they arrived

22.5%

Car loan $5,400 $61pw Natalie There are two years until it’s paid out 13.5%

HECS debt $12,000 None Natalie From Natalie’s librarian course CPI

Table 5 Superannuation

Fund Value Ownership Other information

SunSuper $16,300 Joe From my job with the council. I’ve been with them since I left school

and did my apprenticeship

Council Super $11,800 Natalie From my job in the library since I finished university

Page 7 of 34

Solicitor None

Time span of relationship n.a.

Quality of relationship

Accountant None

Time span of relationship n.a.

Quality of relationship

Table 3 Assets and investments

Assets and investments (personally owned)

Assets Value Ownership

status

Other information Purchase price

Everyday bank

account

$500 Joint We try to keep at least this amount in the

account. We’d like to have more cash on

hand for the unexpected because with the

twins something is always happening

Joe’s ute $4,000 Joe It’s 12 years old and still running well. It’s a

great little workhorse

$15,000

Natalie’s sedan $12,000 Natalie It’s only three years old and I love it.

The four doors and hatchback make it great

to take the kids out and for shopping

$18,000

Home contents $7,000 Joint Includes gardening equipment that Joe

uses for part-time gardening jobs

Bonus saving account $22,500 Joint We were saving quite well and enjoying a

carefree lifestyle until the twins came

along, but for the last year we have often

had to resist the temptation to dip into it.

We get extra interest if we don’t make

withdrawals

Table 4 Liabilities

Debts Value Payment Ownership

status

Other information Interest

rate

Credit card $2,500 Minimum Joint We would prefer to pay it off each month

but we spent a lot rearranging the house

for the twins when they arrived

22.5%

Car loan $5,400 $61pw Natalie There are two years until it’s paid out 13.5%

HECS debt $12,000 None Natalie From Natalie’s librarian course CPI

Table 5 Superannuation

Fund Value Ownership Other information

SunSuper $16,300 Joe From my job with the council. I’ve been with them since I left school

and did my apprenticeship

Council Super $11,800 Natalie From my job in the library since I finished university

Page 7 of 34

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

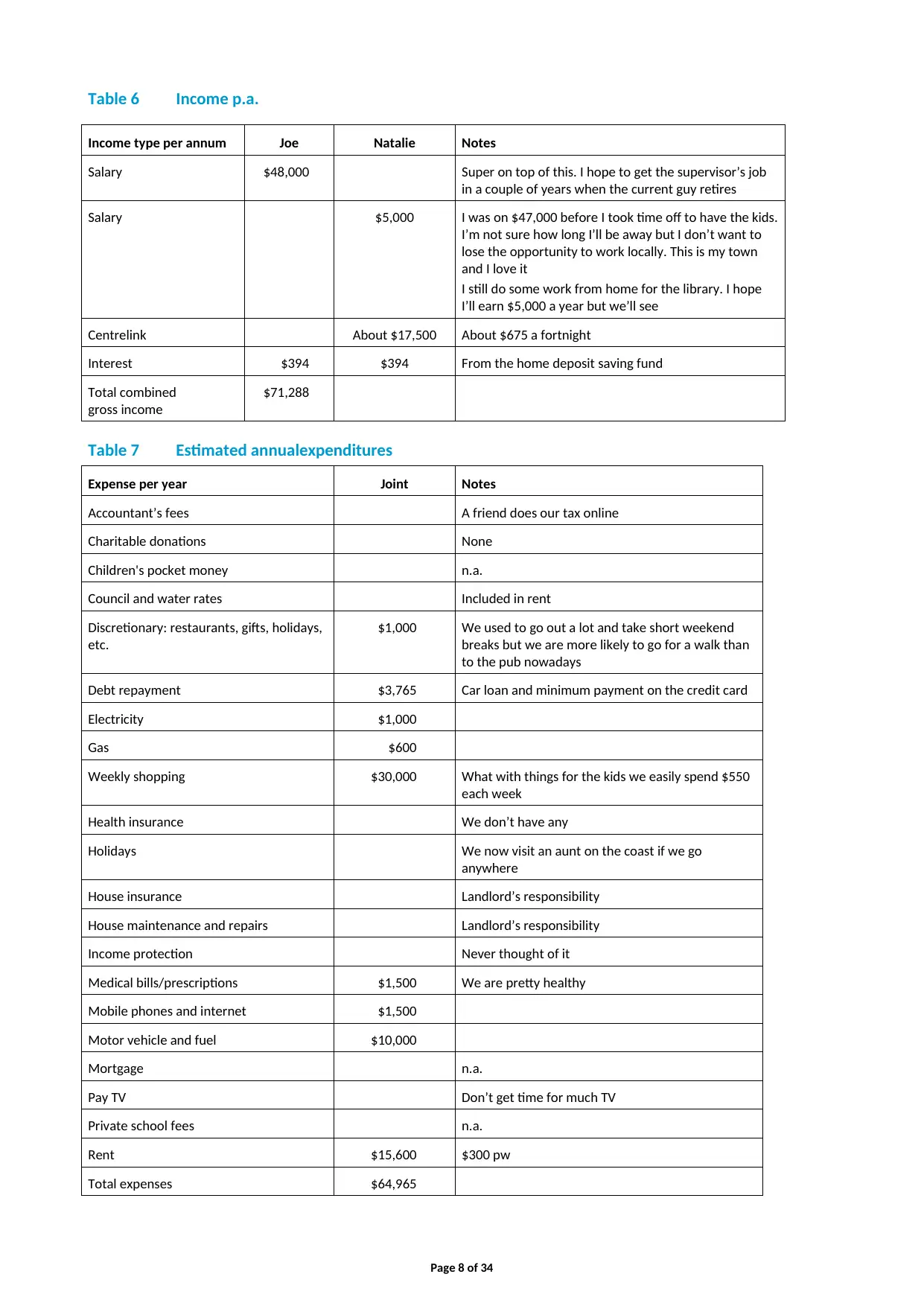

Table 6 Income p.a.

Income type per annum Joe Natalie Notes

Salary $48,000 Super on top of this. I hope to get the supervisor’s job

in a couple of years when the current guy retires

Salary $5,000 I was on $47,000 before I took time off to have the kids.

I’m not sure how long I’ll be away but I don’t want to

lose the opportunity to work locally. This is my town

and I love it

I still do some work from home for the library. I hope

I’ll earn $5,000 a year but we’ll see

Centrelink About $17,500 About $675 a fortnight

Interest $394 $394 From the home deposit saving fund

Total combined

gross income

$71,288

Table 7 Estimated annualexpenditures

Expense per year Joint Notes

Accountant’s fees A friend does our tax online

Charitable donations None

Children's pocket money n.a.

Council and water rates Included in rent

Discretionary: restaurants, gifts, holidays,

etc.

$1,000 We used to go out a lot and take short weekend

breaks but we are more likely to go for a walk than

to the pub nowadays

Debt repayment $3,765 Car loan and minimum payment on the credit card

Electricity $1,000

Gas $600

Weekly shopping $30,000 What with things for the kids we easily spend $550

each week

Health insurance We don’t have any

Holidays We now visit an aunt on the coast if we go

anywhere

House insurance Landlord’s responsibility

House maintenance and repairs Landlord’s responsibility

Income protection Never thought of it

Medical bills/prescriptions $1,500 We are pretty healthy

Mobile phones and internet $1,500

Motor vehicle and fuel $10,000

Mortgage n.a.

Pay TV Don’t get time for much TV

Private school fees n.a.

Rent $15,600 $300 pw

Total expenses $64,965

Page 8 of 34

Income type per annum Joe Natalie Notes

Salary $48,000 Super on top of this. I hope to get the supervisor’s job

in a couple of years when the current guy retires

Salary $5,000 I was on $47,000 before I took time off to have the kids.

I’m not sure how long I’ll be away but I don’t want to

lose the opportunity to work locally. This is my town

and I love it

I still do some work from home for the library. I hope

I’ll earn $5,000 a year but we’ll see

Centrelink About $17,500 About $675 a fortnight

Interest $394 $394 From the home deposit saving fund

Total combined

gross income

$71,288

Table 7 Estimated annualexpenditures

Expense per year Joint Notes

Accountant’s fees A friend does our tax online

Charitable donations None

Children's pocket money n.a.

Council and water rates Included in rent

Discretionary: restaurants, gifts, holidays,

etc.

$1,000 We used to go out a lot and take short weekend

breaks but we are more likely to go for a walk than

to the pub nowadays

Debt repayment $3,765 Car loan and minimum payment on the credit card

Electricity $1,000

Gas $600

Weekly shopping $30,000 What with things for the kids we easily spend $550

each week

Health insurance We don’t have any

Holidays We now visit an aunt on the coast if we go

anywhere

House insurance Landlord’s responsibility

House maintenance and repairs Landlord’s responsibility

Income protection Never thought of it

Medical bills/prescriptions $1,500 We are pretty healthy

Mobile phones and internet $1,500

Motor vehicle and fuel $10,000

Mortgage n.a.

Pay TV Don’t get time for much TV

Private school fees n.a.

Rent $15,600 $300 pw

Total expenses $64,965

Page 8 of 34

Not

applicable

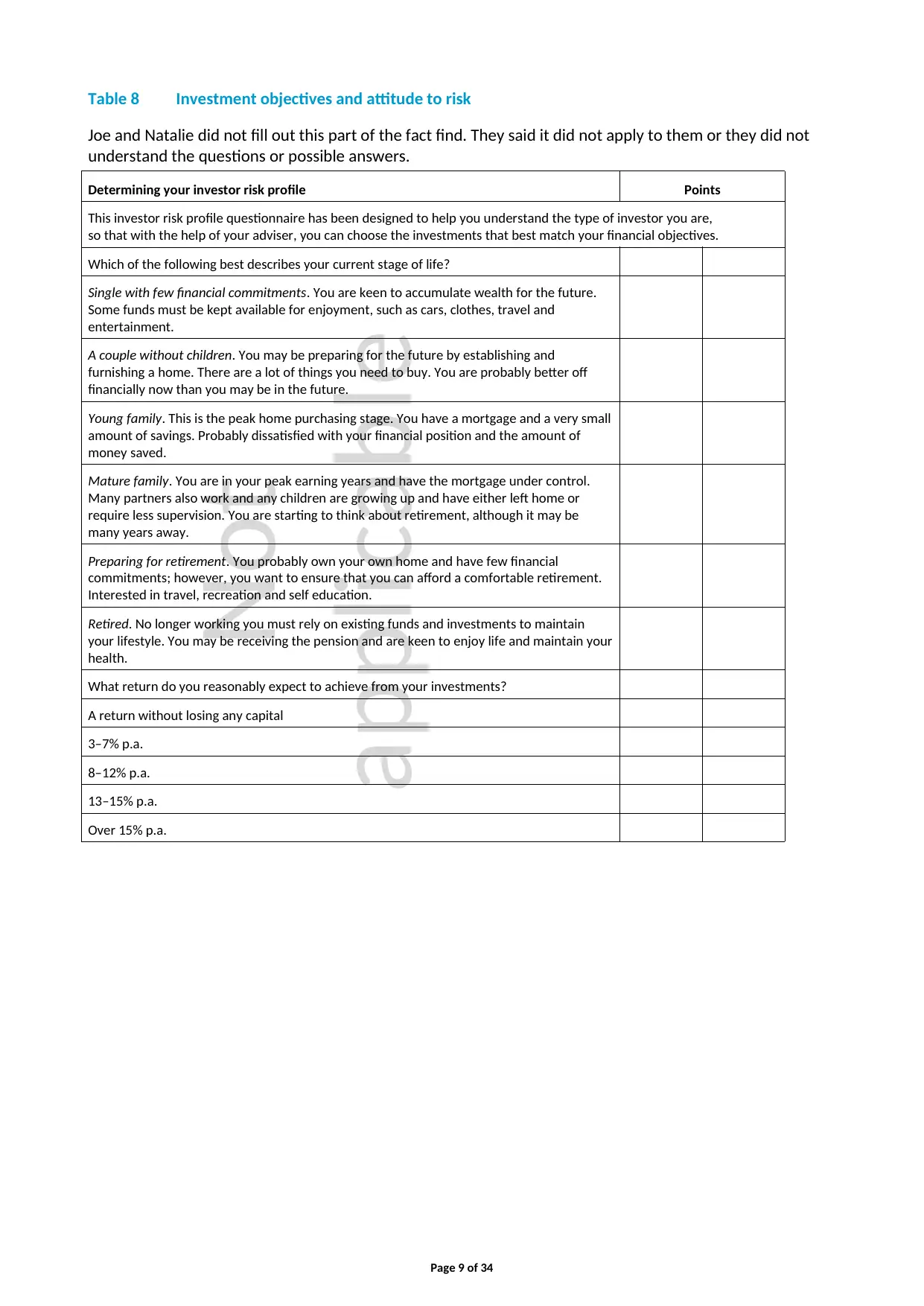

Table 8 Investment objectives and attitude to risk

Joe and Natalie did not fill out this part of the fact find. They said it did not apply to them or they did not

understand the questions or possible answers.

Determining your investor risk profile Points

This investor risk profile questionnaire has been designed to help you understand the type of investor you are,

so that with the help of your adviser, you can choose the investments that best match your financial objectives.

Which of the following best describes your current stage of life?

Single with few financial commitments. You are keen to accumulate wealth for the future.

Some funds must be kept available for enjoyment, such as cars, clothes, travel and

entertainment.

A couple without children. You may be preparing for the future by establishing and

furnishing a home. There are a lot of things you need to buy. You are probably better off

financially now than you may be in the future.

Young family. This is the peak home purchasing stage. You have a mortgage and a very small

amount of savings. Probably dissatisfied with your financial position and the amount of

money saved.

Mature family. You are in your peak earning years and have the mortgage under control.

Many partners also work and any children are growing up and have either left home or

require less supervision. You are starting to think about retirement, although it may be

many years away.

Preparing for retirement. You probably own your own home and have few financial

commitments; however, you want to ensure that you can afford a comfortable retirement.

Interested in travel, recreation and self education.

Retired. No longer working you must rely on existing funds and investments to maintain

your lifestyle. You may be receiving the pension and are keen to enjoy life and maintain your

health.

What return do you reasonably expect to achieve from your investments?

A return without losing any capital

3–7% p.a.

8–12% p.a.

13–15% p.a.

Over 15% p.a.

Page 9 of 34

applicable

Table 8 Investment objectives and attitude to risk

Joe and Natalie did not fill out this part of the fact find. They said it did not apply to them or they did not

understand the questions or possible answers.

Determining your investor risk profile Points

This investor risk profile questionnaire has been designed to help you understand the type of investor you are,

so that with the help of your adviser, you can choose the investments that best match your financial objectives.

Which of the following best describes your current stage of life?

Single with few financial commitments. You are keen to accumulate wealth for the future.

Some funds must be kept available for enjoyment, such as cars, clothes, travel and

entertainment.

A couple without children. You may be preparing for the future by establishing and

furnishing a home. There are a lot of things you need to buy. You are probably better off

financially now than you may be in the future.

Young family. This is the peak home purchasing stage. You have a mortgage and a very small

amount of savings. Probably dissatisfied with your financial position and the amount of

money saved.

Mature family. You are in your peak earning years and have the mortgage under control.

Many partners also work and any children are growing up and have either left home or

require less supervision. You are starting to think about retirement, although it may be

many years away.

Preparing for retirement. You probably own your own home and have few financial

commitments; however, you want to ensure that you can afford a comfortable retirement.

Interested in travel, recreation and self education.

Retired. No longer working you must rely on existing funds and investments to maintain

your lifestyle. You may be receiving the pension and are keen to enjoy life and maintain your

health.

What return do you reasonably expect to achieve from your investments?

A return without losing any capital

3–7% p.a.

8–12% p.a.

13–15% p.a.

Over 15% p.a.

Page 9 of 34

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Not

applicable

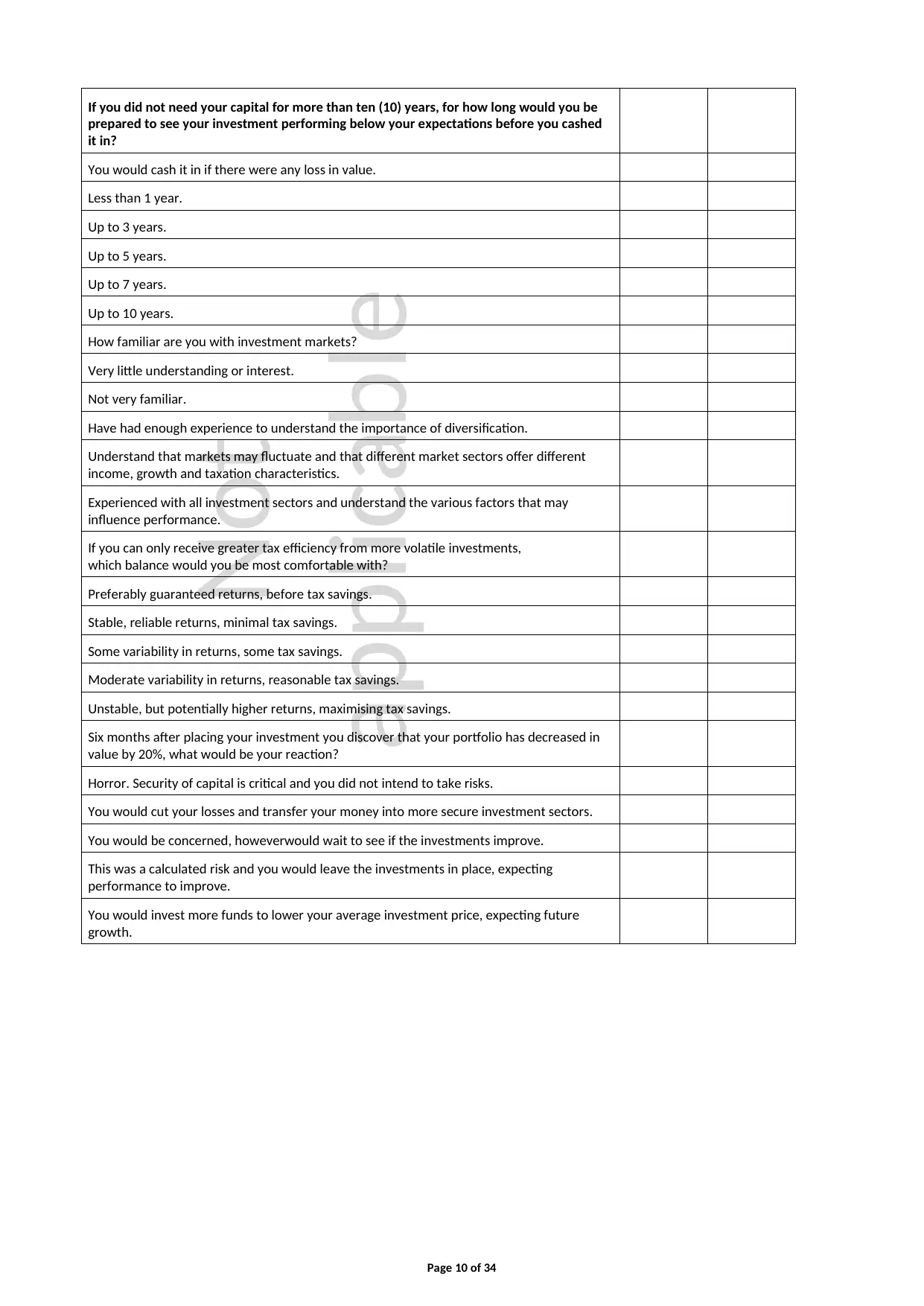

If you did not need your capital for more than ten (10) years, for how long would you be

prepared to see your investment performing below your expectations before you cashed

it in?

You would cash it in if there were any loss in value.

Less than 1 year.

Up to 3 years.

Up to 5 years.

Up to 7 years.

Up to 10 years.

How familiar are you with investment markets?

Very little understanding or interest.

Not very familiar.

Have had enough experience to understand the importance of diversification.

Understand that markets may fluctuate and that different market sectors offer different

income, growth and taxation characteristics.

Experienced with all investment sectors and understand the various factors that may

influence performance.

If you can only receive greater tax efficiency from more volatile investments,

which balance would you be most comfortable with?

Preferably guaranteed returns, before tax savings.

Stable, reliable returns, minimal tax savings.

Some variability in returns, some tax savings.

Moderate variability in returns, reasonable tax savings.

Unstable, but potentially higher returns, maximising tax savings.

Six months after placing your investment you discover that your portfolio has decreased in

value by 20%, what would be your reaction?

Horror. Security of capital is critical and you did not intend to take risks.

You would cut your losses and transfer your money into more secure investment sectors.

You would be concerned, howeverwould wait to see if the investments improve.

This was a calculated risk and you would leave the investments in place, expecting

performance to improve.

You would invest more funds to lower your average investment price, expecting future

growth.

Page 10 of 34

applicable

If you did not need your capital for more than ten (10) years, for how long would you be

prepared to see your investment performing below your expectations before you cashed

it in?

You would cash it in if there were any loss in value.

Less than 1 year.

Up to 3 years.

Up to 5 years.

Up to 7 years.

Up to 10 years.

How familiar are you with investment markets?

Very little understanding or interest.

Not very familiar.

Have had enough experience to understand the importance of diversification.

Understand that markets may fluctuate and that different market sectors offer different

income, growth and taxation characteristics.

Experienced with all investment sectors and understand the various factors that may

influence performance.

If you can only receive greater tax efficiency from more volatile investments,

which balance would you be most comfortable with?

Preferably guaranteed returns, before tax savings.

Stable, reliable returns, minimal tax savings.

Some variability in returns, some tax savings.

Moderate variability in returns, reasonable tax savings.

Unstable, but potentially higher returns, maximising tax savings.

Six months after placing your investment you discover that your portfolio has decreased in

value by 20%, what would be your reaction?

Horror. Security of capital is critical and you did not intend to take risks.

You would cut your losses and transfer your money into more secure investment sectors.

You would be concerned, howeverwould wait to see if the investments improve.

This was a calculated risk and you would leave the investments in place, expecting

performance to improve.

You would invest more funds to lower your average investment price, expecting future

growth.

Page 10 of 34

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Not applicable

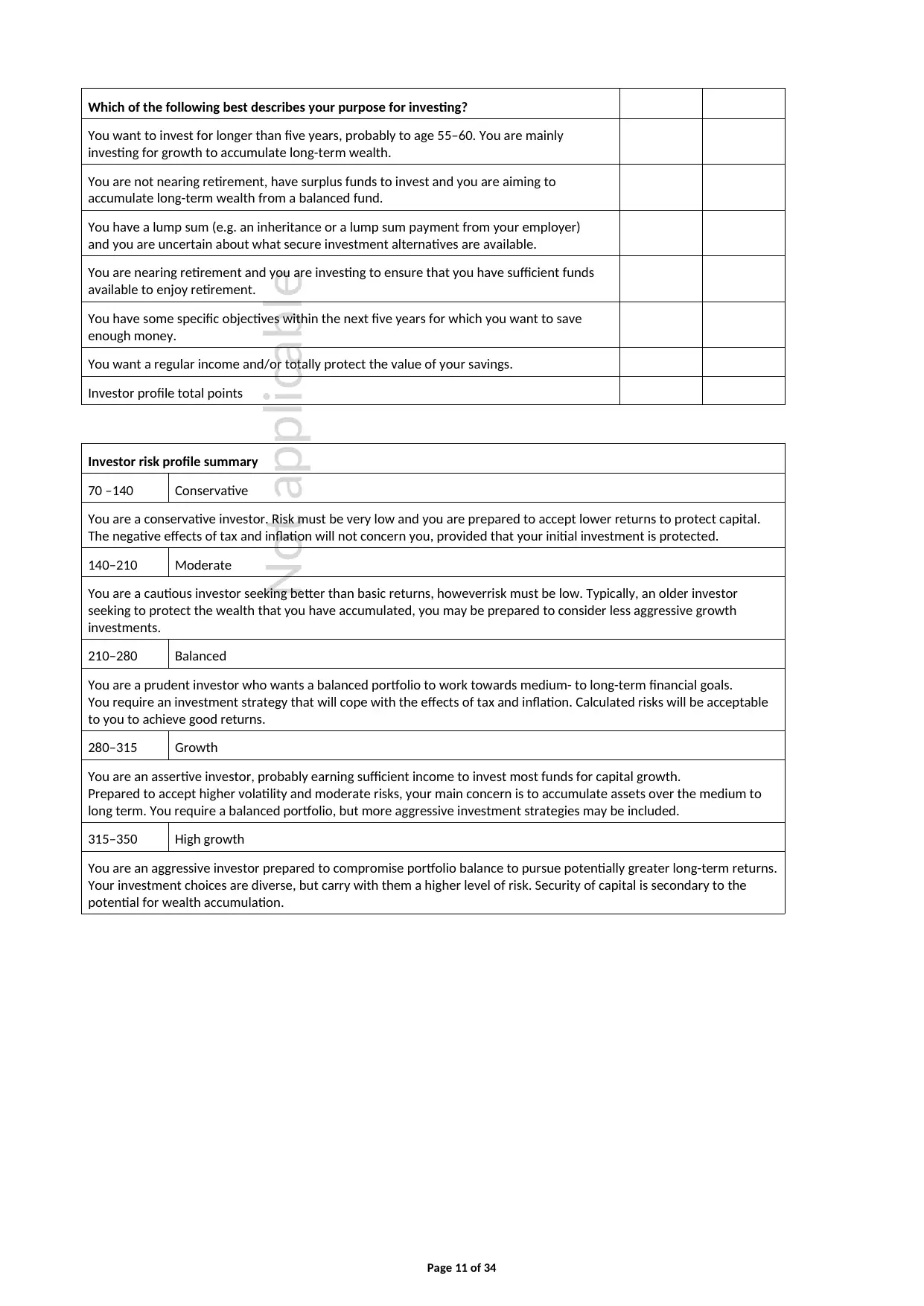

Which of the following best describes your purpose for investing?

You want to invest for longer than five years, probably to age 55–60. You are mainly

investing for growth to accumulate long-term wealth.

You are not nearing retirement, have surplus funds to invest and you are aiming to

accumulate long-term wealth from a balanced fund.

You have a lump sum (e.g. an inheritance or a lump sum payment from your employer)

and you are uncertain about what secure investment alternatives are available.

You are nearing retirement and you are investing to ensure that you have sufficient funds

available to enjoy retirement.

You have some specific objectives within the next five years for which you want to save

enough money.

You want a regular income and/or totally protect the value of your savings.

Investor profile total points

Investor risk profile summary

70 –140 Conservative

You are a conservative investor. Risk must be very low and you are prepared to accept lower returns to protect capital.

The negative effects of tax and inflation will not concern you, provided that your initial investment is protected.

140–210 Moderate

You are a cautious investor seeking better than basic returns, howeverrisk must be low. Typically, an older investor

seeking to protect the wealth that you have accumulated, you may be prepared to consider less aggressive growth

investments.

210–280 Balanced

You are a prudent investor who wants a balanced portfolio to work towards medium- to long-term financial goals.

You require an investment strategy that will cope with the effects of tax and inflation. Calculated risks will be acceptable

to you to achieve good returns.

280–315 Growth

You are an assertive investor, probably earning sufficient income to invest most funds for capital growth.

Prepared to accept higher volatility and moderate risks, your main concern is to accumulate assets over the medium to

long term. You require a balanced portfolio, but more aggressive investment strategies may be included.

315–350 High growth

You are an aggressive investor prepared to compromise portfolio balance to pursue potentially greater long-term returns.

Your investment choices are diverse, but carry with them a higher level of risk. Security of capital is secondary to the

potential for wealth accumulation.

Page 11 of 34

Which of the following best describes your purpose for investing?

You want to invest for longer than five years, probably to age 55–60. You are mainly

investing for growth to accumulate long-term wealth.

You are not nearing retirement, have surplus funds to invest and you are aiming to

accumulate long-term wealth from a balanced fund.

You have a lump sum (e.g. an inheritance or a lump sum payment from your employer)

and you are uncertain about what secure investment alternatives are available.

You are nearing retirement and you are investing to ensure that you have sufficient funds

available to enjoy retirement.

You have some specific objectives within the next five years for which you want to save

enough money.

You want a regular income and/or totally protect the value of your savings.

Investor profile total points

Investor risk profile summary

70 –140 Conservative

You are a conservative investor. Risk must be very low and you are prepared to accept lower returns to protect capital.

The negative effects of tax and inflation will not concern you, provided that your initial investment is protected.

140–210 Moderate

You are a cautious investor seeking better than basic returns, howeverrisk must be low. Typically, an older investor

seeking to protect the wealth that you have accumulated, you may be prepared to consider less aggressive growth

investments.

210–280 Balanced

You are a prudent investor who wants a balanced portfolio to work towards medium- to long-term financial goals.

You require an investment strategy that will cope with the effects of tax and inflation. Calculated risks will be acceptable

to you to achieve good returns.

280–315 Growth

You are an assertive investor, probably earning sufficient income to invest most funds for capital growth.

Prepared to accept higher volatility and moderate risks, your main concern is to accumulate assets over the medium to

long term. You require a balanced portfolio, but more aggressive investment strategies may be included.

315–350 High growth

You are an aggressive investor prepared to compromise portfolio balance to pursue potentially greater long-term returns.

Your investment choices are diverse, but carry with them a higher level of risk. Security of capital is secondary to the

potential for wealth accumulation.

Page 11 of 34

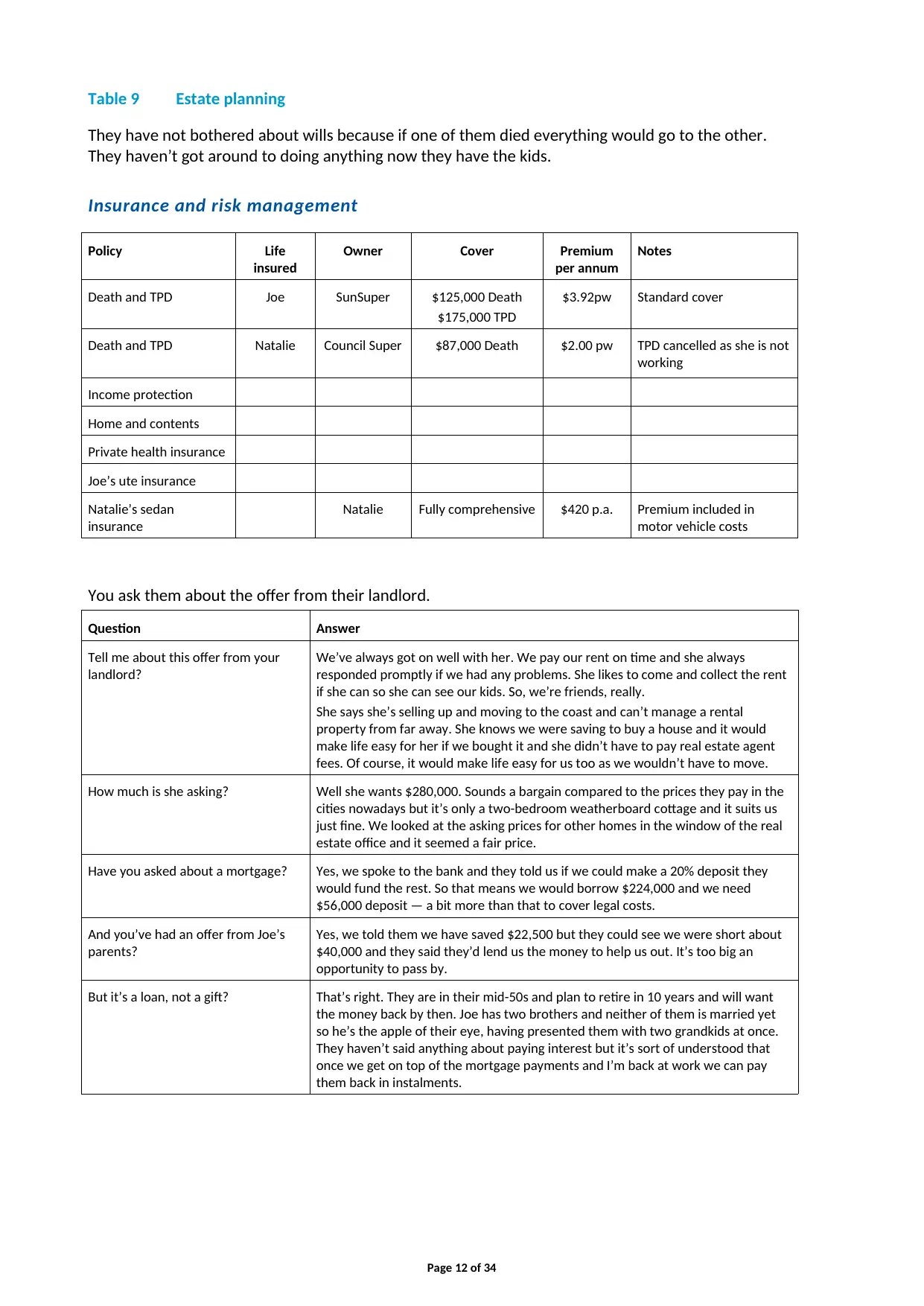

Table 9 Estate planning

They have not bothered about wills because if one of them died everything would go to the other.

They haven’t got around to doing anything now they have the kids.

Insurance and risk management

Policy Life

insured

Owner Cover Premium

per annum

Notes

Death and TPD Joe SunSuper $125,000 Death

$175,000 TPD

$3.92pw Standard cover

Death and TPD Natalie Council Super $87,000 Death $2.00 pw TPD cancelled as she is not

working

Income protection

Home and contents

Private health insurance

Joe’s ute insurance

Natalie’s sedan

insurance

Natalie Fully comprehensive $420 p.a. Premium included in

motor vehicle costs

You ask them about the offer from their landlord.

Question Answer

Tell me about this offer from your

landlord?

We’ve always got on well with her. We pay our rent on time and she always

responded promptly if we had any problems. She likes to come and collect the rent

if she can so she can see our kids. So, we’re friends, really.

She says she’s selling up and moving to the coast and can’t manage a rental

property from far away. She knows we were saving to buy a house and it would

make life easy for her if we bought it and she didn’t have to pay real estate agent

fees. Of course, it would make life easy for us too as we wouldn’t have to move.

How much is she asking? Well she wants $280,000. Sounds a bargain compared to the prices they pay in the

cities nowadays but it’s only a two-bedroom weatherboard cottage and it suits us

just fine. We looked at the asking prices for other homes in the window of the real

estate office and it seemed a fair price.

Have you asked about a mortgage? Yes, we spoke to the bank and they told us if we could make a 20% deposit they

would fund the rest. So that means we would borrow $224,000 and we need

$56,000 deposit — a bit more than that to cover legal costs.

And you’ve had an offer from Joe’s

parents?

Yes, we told them we have saved $22,500 but they could see we were short about

$40,000 and they said they’d lend us the money to help us out. It’s too big an

opportunity to pass by.

But it’s a loan, not a gift? That’s right. They are in their mid-50s and plan to retire in 10 years and will want

the money back by then. Joe has two brothers and neither of them is married yet

so he’s the apple of their eye, having presented them with two grandkids at once.

They haven’t said anything about paying interest but it’s sort of understood that

once we get on top of the mortgage payments and I’m back at work we can pay

them back in instalments.

Page 12 of 34

They have not bothered about wills because if one of them died everything would go to the other.

They haven’t got around to doing anything now they have the kids.

Insurance and risk management

Policy Life

insured

Owner Cover Premium

per annum

Notes

Death and TPD Joe SunSuper $125,000 Death

$175,000 TPD

$3.92pw Standard cover

Death and TPD Natalie Council Super $87,000 Death $2.00 pw TPD cancelled as she is not

working

Income protection

Home and contents

Private health insurance

Joe’s ute insurance

Natalie’s sedan

insurance

Natalie Fully comprehensive $420 p.a. Premium included in

motor vehicle costs

You ask them about the offer from their landlord.

Question Answer

Tell me about this offer from your

landlord?

We’ve always got on well with her. We pay our rent on time and she always

responded promptly if we had any problems. She likes to come and collect the rent

if she can so she can see our kids. So, we’re friends, really.

She says she’s selling up and moving to the coast and can’t manage a rental

property from far away. She knows we were saving to buy a house and it would

make life easy for her if we bought it and she didn’t have to pay real estate agent

fees. Of course, it would make life easy for us too as we wouldn’t have to move.

How much is she asking? Well she wants $280,000. Sounds a bargain compared to the prices they pay in the

cities nowadays but it’s only a two-bedroom weatherboard cottage and it suits us

just fine. We looked at the asking prices for other homes in the window of the real

estate office and it seemed a fair price.

Have you asked about a mortgage? Yes, we spoke to the bank and they told us if we could make a 20% deposit they

would fund the rest. So that means we would borrow $224,000 and we need

$56,000 deposit — a bit more than that to cover legal costs.

And you’ve had an offer from Joe’s

parents?

Yes, we told them we have saved $22,500 but they could see we were short about

$40,000 and they said they’d lend us the money to help us out. It’s too big an

opportunity to pass by.

But it’s a loan, not a gift? That’s right. They are in their mid-50s and plan to retire in 10 years and will want

the money back by then. Joe has two brothers and neither of them is married yet

so he’s the apple of their eye, having presented them with two grandkids at once.

They haven’t said anything about paying interest but it’s sort of understood that

once we get on top of the mortgage payments and I’m back at work we can pay

them back in instalments.

Page 12 of 34

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 34

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.