DFP Module 2 Assignment: Financial Planning and Investment Analysis

VerifiedAdded on 2023/06/11

|26

|5678

|159

Homework Assignment

AI Summary

This assignment focuses on investment analysis and financial planning principles within the context of Diploma of Financial Planning Module 2. It involves analyzing investment options, constructing portfolio asset allocations using Excel, and calculating weighted returns for different investment funds. The assignment requires the application of time value of money concepts to mortgage affordability scenarios, including calculating loan amounts and assessing financial feasibility. Students are expected to demonstrate proficiency in using Excel for financial modeling, including creating pie charts to visualize asset allocations and applying formulas for calculating totals and weighted returns. Additionally, the assignment explores the differences between relative and absolute cell references in Excel and their appropriate use in financial calculations. The assignment also touches upon understanding weighted returns and the factors influencing investment decisions. Desklib provides students with access to this solved assignment and a variety of other resources, including past papers and study tools, to support their learning and academic success.

DFP Module 2 Assignment 1505

Diploma of Financial Planning

Module 2 Assignment

Submission Instructions:

Key steps that must be followed:

1. Please complete the Declaration of Authenticity at the bottom of this page.

2. Once you have completed all parts of the assessment and saved it (eg. to your

desktop computer), login to the Monarch Learning Management System (LMS) to

submit your assessment.

3. In the LMS, click on the file ”Submit DFP Module 2 Assignment” in the Module 2

section of your course and upload your assessment file/s by following the

prompts.

4. Please be sure to click “Continue” after clicking “submit”. This ensures your

assessor receives notification – very important!

Declaration of Understanding and Authenticity *

I have read and understood the assessment instructions provided to me in the Learning Management System.

I certify that the attached material is my original work. No other person’s work has been used without due

acknowledgement. I understand that the work submitted may be reproduced and/or communicated for the purpose

of detecting plagiarism.

.

Student Name*: Date:

* I understand that by typing my name or inserting a digital signature into this box that I agree and am bound by the

above student declaration.

Diploma of Financial Planning

Module 2 Assignment

Submission Instructions:

Key steps that must be followed:

1. Please complete the Declaration of Authenticity at the bottom of this page.

2. Once you have completed all parts of the assessment and saved it (eg. to your

desktop computer), login to the Monarch Learning Management System (LMS) to

submit your assessment.

3. In the LMS, click on the file ”Submit DFP Module 2 Assignment” in the Module 2

section of your course and upload your assessment file/s by following the

prompts.

4. Please be sure to click “Continue” after clicking “submit”. This ensures your

assessor receives notification – very important!

Declaration of Understanding and Authenticity *

I have read and understood the assessment instructions provided to me in the Learning Management System.

I certify that the attached material is my original work. No other person’s work has been used without due

acknowledgement. I understand that the work submitted may be reproduced and/or communicated for the purpose

of detecting plagiarism.

.

Student Name*: Date:

* I understand that by typing my name or inserting a digital signature into this box that I agree and am bound by the

above student declaration.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DFP Module 2 Assignment 1505

Units: FNSINC401, FNSINC501, FNSASICT503, FNSASICW503, FNSASICV503, FNSFMK502, FNSFMK503, BSBITU402, FNSFPL506

Important assessment information

Aims of this assessment

This assessment covers the fundamentals of investment theory and application. The use of

excel spreadsheets is required to express an asset allocation in a pie chart context, with

inclusion of labels and percentages. Excel is also used to calculate a portfolio’s weighted

return. Relative and absolute cell references are also addressed. The time value of money

is covered, with specific reference to how the concepts are applied in a financial planning

modelling context. Different modelling scenarios cover the use of a present value of a lump

sum, the future value of a lump sum, the present value of an annuity and future value of

annuity to model certain advice scenarios. Loan affordability ratios and mortgage stress

are explored using time value of money methodologies. Analysing and valuing investments

using ratio analysis such as earnings per share is covered. Different types of research and

valuation methodology for investments including bottom up and top down analysis is also

addressed. Income and growth oriented investment options are canvassed, as are the use

of derivative contracts in order to manage risks. Futures and options contracts are explored

in this regard.

Marking and feedback

This assignment contains 5 assessment activities each containing specific instructions.

This particular assessment forms part of your overall assessment for the following units of

competency:

FNSINC401

FNSINC501

FNSASICT503

FNSASICW503

FNSASICV503

FNSFMK502

FNSFMK503

BSBITU402

FNSFPL506

Grading for this assessment will be deemed “competent” or “not-yet-competent” in line

with specified educational standards under the Australian Qualifications Framework.

Units: FNSINC401, FNSINC501, FNSASICT503, FNSASICW503, FNSASICV503, FNSFMK502, FNSFMK503, BSBITU402, FNSFPL506

Important assessment information

Aims of this assessment

This assessment covers the fundamentals of investment theory and application. The use of

excel spreadsheets is required to express an asset allocation in a pie chart context, with

inclusion of labels and percentages. Excel is also used to calculate a portfolio’s weighted

return. Relative and absolute cell references are also addressed. The time value of money

is covered, with specific reference to how the concepts are applied in a financial planning

modelling context. Different modelling scenarios cover the use of a present value of a lump

sum, the future value of a lump sum, the present value of an annuity and future value of

annuity to model certain advice scenarios. Loan affordability ratios and mortgage stress

are explored using time value of money methodologies. Analysing and valuing investments

using ratio analysis such as earnings per share is covered. Different types of research and

valuation methodology for investments including bottom up and top down analysis is also

addressed. Income and growth oriented investment options are canvassed, as are the use

of derivative contracts in order to manage risks. Futures and options contracts are explored

in this regard.

Marking and feedback

This assignment contains 5 assessment activities each containing specific instructions.

This particular assessment forms part of your overall assessment for the following units of

competency:

FNSINC401

FNSINC501

FNSASICT503

FNSASICW503

FNSASICV503

FNSFMK502

FNSFMK503

BSBITU402

FNSFPL506

Grading for this assessment will be deemed “competent” or “not-yet-competent” in line

with specified educational standards under the Australian Qualifications Framework.

DFP Module 2 Assignment 1505

Units: FNSINC401, FNSINC501, FNSASICT503, FNSASICW503, FNSASICV503, FNSFMK502, FNSFMK503, BSBITU402, FNSFPL506

What does “competent” mean?

These answers contain relevant and accurate information in response to the question/s

with limited serious errors in fact or application. If incorrect information is contained in an

answer, it must be fundamentally outweighed by the accurate information provided. This

will be assessed against a marking guide provided to assessors for their determination.

What does “not-yet-competent” mean?

This occurs when an assessment does not meet the marking guide standards provided to

assessors. These answers either do not address the question specifically, or are wrong from

a legislative perspective, or are incorrectly applied. Answers that omit to provide a

response to any significant issue (where multiple issues must be addressed in a question)

may also be deemed not-yet-competent. Answers that have faulty reasoning, a poor

standard of expression or include plagiarism may also be deemed not-yet-competent.

Please note, additional information regarding Monarch’s plagiarism policy is contained in

the Student Information Guide which can be found here:

http://www.monarch.edu.au/student-info/

What happens if you are deemed not-yet-competent?

In the event you do not achieve competency by your assessor on this assessment, you will

be given one more opportunity to re-submit the assessment after consultation with your

Trainer/ Assessor. You will know your assessment is deemed ‘not-yet-competent’ if your

grade book in the Monarch LMS says “NYC” after you have received an email from your

assessor advising your assessment has been graded.

Important: It is your responsibility to ensure your assessment resubmission addresses all

areas deemed unsatisfactory by your assessor. Please note, if you are still unsuccessful in

meeting competency after resubmitting your assessment, you will be required to repeat

those units.

In the event that you have concerns about the assessment decision then you can refer to

our Complaints & Appeals process also contained within the Student Information Guide.

Expectations from your assessor when answering different types of assessment questions

Knowledge based questions:

A knowledge based question requires you to clearly identify and cover the key subject

matter areas raised in the question in full as part of the response.

Units: FNSINC401, FNSINC501, FNSASICT503, FNSASICW503, FNSASICV503, FNSFMK502, FNSFMK503, BSBITU402, FNSFPL506

What does “competent” mean?

These answers contain relevant and accurate information in response to the question/s

with limited serious errors in fact or application. If incorrect information is contained in an

answer, it must be fundamentally outweighed by the accurate information provided. This

will be assessed against a marking guide provided to assessors for their determination.

What does “not-yet-competent” mean?

This occurs when an assessment does not meet the marking guide standards provided to

assessors. These answers either do not address the question specifically, or are wrong from

a legislative perspective, or are incorrectly applied. Answers that omit to provide a

response to any significant issue (where multiple issues must be addressed in a question)

may also be deemed not-yet-competent. Answers that have faulty reasoning, a poor

standard of expression or include plagiarism may also be deemed not-yet-competent.

Please note, additional information regarding Monarch’s plagiarism policy is contained in

the Student Information Guide which can be found here:

http://www.monarch.edu.au/student-info/

What happens if you are deemed not-yet-competent?

In the event you do not achieve competency by your assessor on this assessment, you will

be given one more opportunity to re-submit the assessment after consultation with your

Trainer/ Assessor. You will know your assessment is deemed ‘not-yet-competent’ if your

grade book in the Monarch LMS says “NYC” after you have received an email from your

assessor advising your assessment has been graded.

Important: It is your responsibility to ensure your assessment resubmission addresses all

areas deemed unsatisfactory by your assessor. Please note, if you are still unsuccessful in

meeting competency after resubmitting your assessment, you will be required to repeat

those units.

In the event that you have concerns about the assessment decision then you can refer to

our Complaints & Appeals process also contained within the Student Information Guide.

Expectations from your assessor when answering different types of assessment questions

Knowledge based questions:

A knowledge based question requires you to clearly identify and cover the key subject

matter areas raised in the question in full as part of the response.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DFP Module 2 Assignment 1505

Units: FNSINC401, FNSINC501, FNSASICT503, FNSASICW503, FNSASICV503, FNSFMK502, FNSFMK503, BSBITU402, FNSFPL506

Skill based questions:

Where you are asked to write as though you are speaking to a client, your answers must

show your ability to:

understand your client’s concerns/perspective/views

show empathy

display a professional response

explain ideas clearly and simply so your client can understand the issues

Good luck

Finally, good luck with your learning and assessments and remember your trainers are here

to assist you

Units: FNSINC401, FNSINC501, FNSASICT503, FNSASICW503, FNSASICV503, FNSFMK502, FNSFMK503, BSBITU402, FNSFPL506

Skill based questions:

Where you are asked to write as though you are speaking to a client, your answers must

show your ability to:

understand your client’s concerns/perspective/views

show empathy

display a professional response

explain ideas clearly and simply so your client can understand the issues

Good luck

Finally, good luck with your learning and assessments and remember your trainers are here

to assist you

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DFP Module 2 Assignment 1505

Units: FNSINC401, FNSINC501, FNSASICT503, FNSASICW503, FNSASICV503, FNSFMK502, FNSFMK503, BSBITU402, FNSFPL506

Assessment Activity 1

Project

Balanced Funds Comparison

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all 10 questions that follow.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the front of this

assessment

Estimated time for completion of this assessment activity: 3 hours

Units: FNSINC401, FNSINC501, FNSASICT503, FNSASICW503, FNSASICV503, FNSFMK502, FNSFMK503, BSBITU402, FNSFPL506

Assessment Activity 1

Project

Balanced Funds Comparison

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all 10 questions that follow.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the front of this

assessment

Estimated time for completion of this assessment activity: 3 hours

DFP Module 2 Assignment 1505

Units: FNSINC401, FNSINC501, FNSASICT503, FNSASICW503, FNSASICV503, FNSFMK502, FNSFMK503, BSBITU402, FNSFPL506

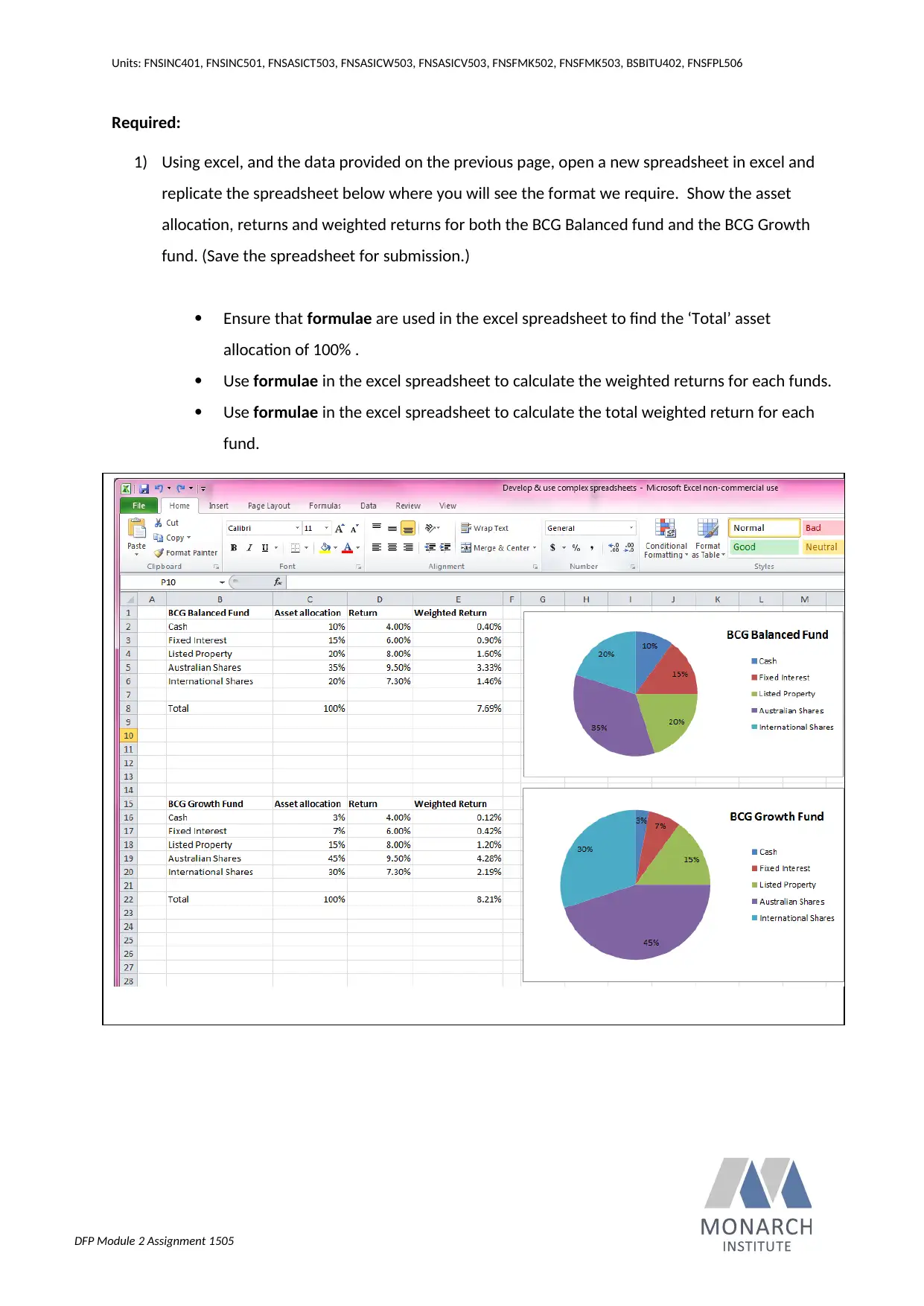

Background

Your client is considering investing $50,000 in one of 2 funds offered through BCG, a notable investment

fund manager. One fund under consideration is the BCG Balanced Fund which has the following asset

allocation.

Cash 10%

Fixed Interest 15%

Listed Property 20%

Australian Shares 35%

International Shares 20%

The alternative fund is the BCG Growth fund which has the following asset allocation:

Cash 3%

Fixed Interest 7%

Listed Property 15%

Australian Shares 45%

International Shares 30%

From your research you have also been able to determine the average returns that these funds have

generated in the past three years for each asset class. The returns have been:

Cash 4.00%

Fixed Interest 6.00%

Listed Property 8.00%

Australian Shares 9.50%

International Shares 7.30%

At your next client meeting you have decided to present to your client an excel spreadsheet that shows

the overall weighted return that would have been received by investors in the BCG Balanced Fund

compared to returns that would have been received by investors in the BCG Growth Fund, over the

previous three years. You will also show a visual representation of the asset allocation by including a pie

chart for each fund. (In Appendix 5 of Module 2 are tips to help you with excel.)

Please save all parts to this assessment activity and upload these to the LMS when submitting your

assignment for grading.

Units: FNSINC401, FNSINC501, FNSASICT503, FNSASICW503, FNSASICV503, FNSFMK502, FNSFMK503, BSBITU402, FNSFPL506

Background

Your client is considering investing $50,000 in one of 2 funds offered through BCG, a notable investment

fund manager. One fund under consideration is the BCG Balanced Fund which has the following asset

allocation.

Cash 10%

Fixed Interest 15%

Listed Property 20%

Australian Shares 35%

International Shares 20%

The alternative fund is the BCG Growth fund which has the following asset allocation:

Cash 3%

Fixed Interest 7%

Listed Property 15%

Australian Shares 45%

International Shares 30%

From your research you have also been able to determine the average returns that these funds have

generated in the past three years for each asset class. The returns have been:

Cash 4.00%

Fixed Interest 6.00%

Listed Property 8.00%

Australian Shares 9.50%

International Shares 7.30%

At your next client meeting you have decided to present to your client an excel spreadsheet that shows

the overall weighted return that would have been received by investors in the BCG Balanced Fund

compared to returns that would have been received by investors in the BCG Growth Fund, over the

previous three years. You will also show a visual representation of the asset allocation by including a pie

chart for each fund. (In Appendix 5 of Module 2 are tips to help you with excel.)

Please save all parts to this assessment activity and upload these to the LMS when submitting your

assignment for grading.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DFP Module 2 Assignment 1505

Units: FNSINC401, FNSINC501, FNSASICT503, FNSASICW503, FNSASICV503, FNSFMK502, FNSFMK503, BSBITU402, FNSFPL506

Required:

1) Using excel, and the data provided on the previous page, open a new spreadsheet in excel and

replicate the spreadsheet below where you will see the format we require. Show the asset

allocation, returns and weighted returns for both the BCG Balanced fund and the BCG Growth

fund. (Save the spreadsheet for submission.)

Ensure that formulae are used in the excel spreadsheet to find the ‘Total’ asset

allocation of 100% .

Use formulae in the excel spreadsheet to calculate the weighted returns for each funds.

Use formulae in the excel spreadsheet to calculate the total weighted return for each

fund.

Units: FNSINC401, FNSINC501, FNSASICT503, FNSASICW503, FNSASICV503, FNSFMK502, FNSFMK503, BSBITU402, FNSFPL506

Required:

1) Using excel, and the data provided on the previous page, open a new spreadsheet in excel and

replicate the spreadsheet below where you will see the format we require. Show the asset

allocation, returns and weighted returns for both the BCG Balanced fund and the BCG Growth

fund. (Save the spreadsheet for submission.)

Ensure that formulae are used in the excel spreadsheet to find the ‘Total’ asset

allocation of 100% .

Use formulae in the excel spreadsheet to calculate the weighted returns for each funds.

Use formulae in the excel spreadsheet to calculate the total weighted return for each

fund.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DFP Module 2 Assignment 1505

Units: FNSINC401, FNSINC501, FNSASICT503, FNSASICW503, FNSASICV503, FNSFMK502, FNSFMK503, BSBITU402, FNSFPL506

2) Create a pie chart for each fund showing the asset allocation of each fund.

Include a legend showing which asset class each colour represents

Include data labels on the pie charts to show the actual percentages allocated to each

asset class

Include a title for each fund

3) Write the formula in the box below that you used in the cell that gives the Total as being 100%

(cell C8)

C3+C4+C5+C6+C7

4) Write the formula in the box below that you used in the cell that gives the weighted return for

Cash in the BCG Balanced Fund (cell E2)

SUMPRODUCT(C4,D4)/C8

5) Write the formula in the box below that you used in the cell that gives the Total weighted return

for the BCG Growth Fund (cell E22)

SUM(E3:E7)

6) When looking at a cell reference, how do you know if the cell is a “relative” cell reference in

excel or an ‘’absolute” cell reference in excel? Remember, you can google or youtube this, in

addition to the notes we have provided in Appendix 5 if you need additional help.

There are two sorts of cell references and they are absolute and relative. Absolute and relative

references perform in a different manner when they are copied to any other cell. Relative

references on the other hand change when any formula is copied to any other different cell. It is

seen that absolute references remain unchanged even when they are copied.

Units: FNSINC401, FNSINC501, FNSASICT503, FNSASICW503, FNSASICV503, FNSFMK502, FNSFMK503, BSBITU402, FNSFPL506

2) Create a pie chart for each fund showing the asset allocation of each fund.

Include a legend showing which asset class each colour represents

Include data labels on the pie charts to show the actual percentages allocated to each

asset class

Include a title for each fund

3) Write the formula in the box below that you used in the cell that gives the Total as being 100%

(cell C8)

C3+C4+C5+C6+C7

4) Write the formula in the box below that you used in the cell that gives the weighted return for

Cash in the BCG Balanced Fund (cell E2)

SUMPRODUCT(C4,D4)/C8

5) Write the formula in the box below that you used in the cell that gives the Total weighted return

for the BCG Growth Fund (cell E22)

SUM(E3:E7)

6) When looking at a cell reference, how do you know if the cell is a “relative” cell reference in

excel or an ‘’absolute” cell reference in excel? Remember, you can google or youtube this, in

addition to the notes we have provided in Appendix 5 if you need additional help.

There are two sorts of cell references and they are absolute and relative. Absolute and relative

references perform in a different manner when they are copied to any other cell. Relative

references on the other hand change when any formula is copied to any other different cell. It is

seen that absolute references remain unchanged even when they are copied.

DFP Module 2 Assignment 1505

Units: FNSINC401, FNSINC501, FNSASICT503, FNSASICW503, FNSASICV503, FNSFMK502, FNSFMK503, BSBITU402, FNSFPL506

7) Provide an example of when you might use a relative cell reference in excel. Remember, you can

google or youtube this, in addition to the notes we have provided if you need additional help.

Relative cell reference is taken into consideration when any kind of value is copied among

multiple cells and this becomes the scenario that can be used at the time of auto filling.

8) Provide an example of when you might use an absolute cell reference in excel. Remember, you

can google or youtube this, in addition to the notes we have provided if you need additional

help.

An instance can be provided in accordance to the fact that in order to keep the sign of dollar in

all the cells, it is seen that absolute references are done.

9) Explain what is meant by a weighted return.

It looks to address the process with the assistance of which the present value of the cash flows

and the value that is terminal in nature becomes equal to the investment value that was made

primarily.

Units: FNSINC401, FNSINC501, FNSASICT503, FNSASICW503, FNSASICV503, FNSFMK502, FNSFMK503, BSBITU402, FNSFPL506

7) Provide an example of when you might use a relative cell reference in excel. Remember, you can

google or youtube this, in addition to the notes we have provided if you need additional help.

Relative cell reference is taken into consideration when any kind of value is copied among

multiple cells and this becomes the scenario that can be used at the time of auto filling.

8) Provide an example of when you might use an absolute cell reference in excel. Remember, you

can google or youtube this, in addition to the notes we have provided if you need additional

help.

An instance can be provided in accordance to the fact that in order to keep the sign of dollar in

all the cells, it is seen that absolute references are done.

9) Explain what is meant by a weighted return.

It looks to address the process with the assistance of which the present value of the cash flows

and the value that is terminal in nature becomes equal to the investment value that was made

primarily.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DFP Module 2 Assignment 1505

Units: FNSINC401, FNSINC501, FNSASICT503, FNSASICW503, FNSASICV503, FNSFMK502, FNSFMK503, BSBITU402, FNSFPL506

10) Ensure you submit your excel spreadsheet including the pie chart when you submit your

assignment.

Assessment Activity 2

Calculation Exercise

Time Value of money - Mortgage

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all 7 questions that follow.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the front of this

assessment

Estimated time for completion of this assessment activity: 1-2 hours

Units: FNSINC401, FNSINC501, FNSASICT503, FNSASICW503, FNSASICV503, FNSFMK502, FNSFMK503, BSBITU402, FNSFPL506

10) Ensure you submit your excel spreadsheet including the pie chart when you submit your

assignment.

Assessment Activity 2

Calculation Exercise

Time Value of money - Mortgage

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all 7 questions that follow.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the front of this

assessment

Estimated time for completion of this assessment activity: 1-2 hours

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DFP Module 2 Assignment 1505

Units: FNSINC401, FNSINC501, FNSASICT503, FNSASICW503, FNSASICV503, FNSFMK502, FNSFMK503, BSBITU402, FNSFPL506

Tip: Appendix 4 of Module 2 has a similar question with workings.

Background

Kyle and Julia are considering whether or not to buy a particular property valued at $720,000. They

have $200,000 of their own funds to commit towards the purchase and they expect to incur an

additional $50,000 in fees and taxes on the purchase itself. They are able to borrow at an interest rate

of 7.20 per cent per annum with interest compounded monthly. Loan repayments would be monthly

with the first payment due at the end of the first month after purchasing the property. The term of the

home loan is 30 years. They both work full-time earning a combined after-tax salary of $12,000 per

month.

1. How much is the monthly mortgage payment Kyle and Julia will be required to pay for their loan?

Hint: because the interest is compounded monthly, we need to use the number of months for the

mortgage loan, not the number of years in determining the regular payments to be made. We also

need to use the monthly interest rate (7.2% /12 = 0.6%)

Using the present value of an annuity formula we can rearrange the following formula to obtain the

regular monthly mortgage payment PMT.

PV = PMT

[1−( 1+r )−n

]

r

PMT = PV /

[1−( 1+r )−n

]

r

Alternatively, you can use a financial calculator to determine PMT.

PV = amountborrowed from the bank

r = interest rate per month

n = number of months over the entire loan period

If we select the payment key (PMT) on the financial calculator, we will know the amount of

the regular monthly mortgage payments the bank requires us to pay.

If you prefer to use an online mortgage calculator, you can choose one of hundreds

available. An example of one such mortgage calculator is:

http://www.nab.com.au/personal/loans/home-loans/loan-calculators/loan-repayments-

calculator

Units: FNSINC401, FNSINC501, FNSASICT503, FNSASICW503, FNSASICV503, FNSFMK502, FNSFMK503, BSBITU402, FNSFPL506

Tip: Appendix 4 of Module 2 has a similar question with workings.

Background

Kyle and Julia are considering whether or not to buy a particular property valued at $720,000. They

have $200,000 of their own funds to commit towards the purchase and they expect to incur an

additional $50,000 in fees and taxes on the purchase itself. They are able to borrow at an interest rate

of 7.20 per cent per annum with interest compounded monthly. Loan repayments would be monthly

with the first payment due at the end of the first month after purchasing the property. The term of the

home loan is 30 years. They both work full-time earning a combined after-tax salary of $12,000 per

month.

1. How much is the monthly mortgage payment Kyle and Julia will be required to pay for their loan?

Hint: because the interest is compounded monthly, we need to use the number of months for the

mortgage loan, not the number of years in determining the regular payments to be made. We also

need to use the monthly interest rate (7.2% /12 = 0.6%)

Using the present value of an annuity formula we can rearrange the following formula to obtain the

regular monthly mortgage payment PMT.

PV = PMT

[1−( 1+r )−n

]

r

PMT = PV /

[1−( 1+r )−n

]

r

Alternatively, you can use a financial calculator to determine PMT.

PV = amountborrowed from the bank

r = interest rate per month

n = number of months over the entire loan period

If we select the payment key (PMT) on the financial calculator, we will know the amount of

the regular monthly mortgage payments the bank requires us to pay.

If you prefer to use an online mortgage calculator, you can choose one of hundreds

available. An example of one such mortgage calculator is:

http://www.nab.com.au/personal/loans/home-loans/loan-calculators/loan-repayments-

calculator

DFP Module 2 Assignment 1505

Units: FNSINC401, FNSINC501, FNSASICT503, FNSASICW503, FNSASICV503, FNSFMK502, FNSFMK503, BSBITU402, FNSFPL506

Provide your answer here

$3869

2. A loan affordability ratio is equal to the monthly home loan repayment divided by a couple’s

household after-tax monthly income. A key threshold for ‘mortgage stress’ is when the loan

affordability ratio reaches 35%. Will Kyle and Julia face mortgage stress at current interest rates.

Provide your answer here

$3869/$12,000* 100= 32%.

It is seen that the loan affordability percentage has been 32% and this explains that they are closer to

the stress limit of 35%.

3. After 1 year, the bank informs Kyle and Julia that $564,429 is still owing on their loan. How much

in total have Kyle and Julia paid in mortgage payments during the first year?

Provide your answer here

$3,869* 12= $46,428

Units: FNSINC401, FNSINC501, FNSASICT503, FNSASICW503, FNSASICV503, FNSFMK502, FNSFMK503, BSBITU402, FNSFPL506

Provide your answer here

$3869

2. A loan affordability ratio is equal to the monthly home loan repayment divided by a couple’s

household after-tax monthly income. A key threshold for ‘mortgage stress’ is when the loan

affordability ratio reaches 35%. Will Kyle and Julia face mortgage stress at current interest rates.

Provide your answer here

$3869/$12,000* 100= 32%.

It is seen that the loan affordability percentage has been 32% and this explains that they are closer to

the stress limit of 35%.

3. After 1 year, the bank informs Kyle and Julia that $564,429 is still owing on their loan. How much

in total have Kyle and Julia paid in mortgage payments during the first year?

Provide your answer here

$3,869* 12= $46,428

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.