Financial Planning Report: Analysis of Jake Mackenzie's Finances

VerifiedAdded on 2020/02/05

|9

|2602

|46

Report

AI Summary

This financial planning report analyzes the current financial circumstances of Jake Mackenzie, a 57-year-old architect with a strong financial standing, including a high salary, significant savings, and substantial property and superannuation assets. The report identifies potential future issues, such as retirement funding and investment avenues, and outlines Jake's objectives, including early retirement, share portfolio growth, and lifestyle enhancements. It assesses his risk profile and provides detailed recommendations for wealth creation, including diversification of investments beyond shares. The report also covers insurance needs, including life, income protection, and medical insurance, along with the advantages and disadvantages of each. It explores superannuation and retirement planning, suggesting the Transition to Retirement strategy, and discusses estate planning considerations, including wills and inheritance. Finally, the report touches on social security benefits and concludes with a marking rubric for assessment.

FINANCIAL PLANNING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

CURRENT CIRCUMSTANCES....................................................................................................1

Current wealth condition of Jake............................................................................................1

Potential issues.......................................................................................................................1

Objectives...............................................................................................................................1

Risk Profile.............................................................................................................................1

WEALTH CREATION / LIFESTYLE RECOMMENDATIONS..................................................2

INSURANCE...................................................................................................................................2

SUPERANNUATION / RETIREMENT PLANNING...................................................................3

ESTATE PLANNING.....................................................................................................................4

SOCIAL SECURITY.......................................................................................................................4

MARKING RUBRIC.......................................................................................................................4

REFERENCES................................................................................................................................7

CURRENT CIRCUMSTANCES....................................................................................................1

Current wealth condition of Jake............................................................................................1

Potential issues.......................................................................................................................1

Objectives...............................................................................................................................1

Risk Profile.............................................................................................................................1

WEALTH CREATION / LIFESTYLE RECOMMENDATIONS..................................................2

INSURANCE...................................................................................................................................2

SUPERANNUATION / RETIREMENT PLANNING...................................................................3

ESTATE PLANNING.....................................................................................................................4

SOCIAL SECURITY.......................................................................................................................4

MARKING RUBRIC.......................................................................................................................4

REFERENCES................................................................................................................................7

CURRENT CIRCUMSTANCES

Current wealth condition of Jake

In the current case study there is a client Jake Mackenzie who was born on 12/02/1960

and in the current year he is 57 years old. He is Australian citizen and working in Grand Designs

Pty Limited company on the profile of Architect and his current economic condition or financial

health is better. Salary of Jake is worth of $140,000 per annum excluding the superannuation and

the excluded amount will be return to him after retirement. Saving of Jake per month is worth of

$2500, value of his house and motor vehicle is worth of $850,000 and $40,000 respectively.

Along with this his home contents of approximately worth of $75,000. The superannuation

amount of the Jake is also high and due to which he has two superannuation accounts in the

Bank. The taxable amount of the client is worth of $492,500 which is lower as compare to his

balance like $532,500. Apart from this, after the retirement he will get huge amount and in short

it can be said that economic condition of Jake is healthier and strong.

Potential issues

The issues and problems of the Jake are for the future that after age of retirement how

much fund he will require for spending further life. Other issue is related to avenue of investment

that which one will be beneficial like insurance, shares or any other. Moreover, he needs to keep

some fund for the superannuation or not etc. Apart from this, main concern of the Jake is for

need of money as well as selection of fruitful investment avenue. Another issue is regarding to

salary that employer of Jake allow his to sacrifice salary.

Objectives

Key objective related to non financial of Jake for short term (8 years) is to take self

retirement at the age of 63 years instead of 65 years. Medium term goal of the client is to

improve the money of share portfolio from $40,000 to $100,000 within upcoming 5 years.

Moreover, he needs to build swimming pool, raise fund for holiday, estate planning as well as

get the appropriate insurance. Second last and last options and objectives having the higher

priority as compare to others.

Risk Profile

The Jake having time frame to raise the amount of shares portfolio within 5 years in

which he has risk of 1 year. It may be possible that balanced amount can be delay for 1 year in

1

Current wealth condition of Jake

In the current case study there is a client Jake Mackenzie who was born on 12/02/1960

and in the current year he is 57 years old. He is Australian citizen and working in Grand Designs

Pty Limited company on the profile of Architect and his current economic condition or financial

health is better. Salary of Jake is worth of $140,000 per annum excluding the superannuation and

the excluded amount will be return to him after retirement. Saving of Jake per month is worth of

$2500, value of his house and motor vehicle is worth of $850,000 and $40,000 respectively.

Along with this his home contents of approximately worth of $75,000. The superannuation

amount of the Jake is also high and due to which he has two superannuation accounts in the

Bank. The taxable amount of the client is worth of $492,500 which is lower as compare to his

balance like $532,500. Apart from this, after the retirement he will get huge amount and in short

it can be said that economic condition of Jake is healthier and strong.

Potential issues

The issues and problems of the Jake are for the future that after age of retirement how

much fund he will require for spending further life. Other issue is related to avenue of investment

that which one will be beneficial like insurance, shares or any other. Moreover, he needs to keep

some fund for the superannuation or not etc. Apart from this, main concern of the Jake is for

need of money as well as selection of fruitful investment avenue. Another issue is regarding to

salary that employer of Jake allow his to sacrifice salary.

Objectives

Key objective related to non financial of Jake for short term (8 years) is to take self

retirement at the age of 63 years instead of 65 years. Medium term goal of the client is to

improve the money of share portfolio from $40,000 to $100,000 within upcoming 5 years.

Moreover, he needs to build swimming pool, raise fund for holiday, estate planning as well as

get the appropriate insurance. Second last and last options and objectives having the higher

priority as compare to others.

Risk Profile

The Jake having time frame to raise the amount of shares portfolio within 5 years in

which he has risk of 1 year. It may be possible that balanced amount can be delay for 1 year in

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

case the conditions of stock market reduce. Apart from this, Jake not consider any other kind of

investment criteria because he has faith on the stock investment rather than other available

options to invest money. Due to this, the risk profile of Jake is regarding to the time-frame for

meet with the balance of share portfolio as well as delaying the retirement years.

WEALTH CREATION / LIFESTYLE RECOMMENDATIONS

The Jake wants to improve his level of wealth and economic conditions and for which he

makes several kinds of objectives as well as plan along with the time frame. As per the financial

adviser there are several kinds of ways and methods through which the client Jake can make

investment and then create or improve his wealth up to the higher condition. At the current case

study Jake has various types of objectives and among all of them some relies under the financial

and some under the non financial aspect. For the financial aspect Jake always consider shares

portfolio as compare to another available investment categories. On the basis of this it can be

recommended to the Jake that he needs to consider other investment avenues also which help to

reduce the level of risk and enhance return of initial investment.

Advantage to make investment in other criteria is rather than considering only one, is

Jake able reduce risk because it diversifies in other aspects. Along with this, he able to generate

more amount in terms of return as compare to only shares.

Disadvantage of go for diversify portfolio is that Jake needs to consider and manage the

all investment avenues and look at all within specific time frame.

INSURANCE

The term which provide protection to living and non living aspects against to those events

which can be incurred is considered as insurance. There are various kinds of insurance which

will be suitable for the Jake in order to achieve different types of objectives in effective manner.

The Jake has specific objective is that use appropriate insurance which having the higher priority

which are like life, total and permanent disability, income protection, trauma and others. After

considering these all it can be suggested to the Jake that he needs to invest money in life

insurance, income protection as well as medical which provide safety and protection to him in

terms of profitability. The income protection allows to protect those amount which are generated

through different kinds of economic activities done by Jake. Life insurance helps to the Jake for

2

investment criteria because he has faith on the stock investment rather than other available

options to invest money. Due to this, the risk profile of Jake is regarding to the time-frame for

meet with the balance of share portfolio as well as delaying the retirement years.

WEALTH CREATION / LIFESTYLE RECOMMENDATIONS

The Jake wants to improve his level of wealth and economic conditions and for which he

makes several kinds of objectives as well as plan along with the time frame. As per the financial

adviser there are several kinds of ways and methods through which the client Jake can make

investment and then create or improve his wealth up to the higher condition. At the current case

study Jake has various types of objectives and among all of them some relies under the financial

and some under the non financial aspect. For the financial aspect Jake always consider shares

portfolio as compare to another available investment categories. On the basis of this it can be

recommended to the Jake that he needs to consider other investment avenues also which help to

reduce the level of risk and enhance return of initial investment.

Advantage to make investment in other criteria is rather than considering only one, is

Jake able reduce risk because it diversifies in other aspects. Along with this, he able to generate

more amount in terms of return as compare to only shares.

Disadvantage of go for diversify portfolio is that Jake needs to consider and manage the

all investment avenues and look at all within specific time frame.

INSURANCE

The term which provide protection to living and non living aspects against to those events

which can be incurred is considered as insurance. There are various kinds of insurance which

will be suitable for the Jake in order to achieve different types of objectives in effective manner.

The Jake has specific objective is that use appropriate insurance which having the higher priority

which are like life, total and permanent disability, income protection, trauma and others. After

considering these all it can be suggested to the Jake that he needs to invest money in life

insurance, income protection as well as medical which provide safety and protection to him in

terms of profitability. The income protection allows to protect those amount which are generated

through different kinds of economic activities done by Jake. Life insurance helps to the Jake for

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

recovering some of money in case he dies which is one of the highly prioritised insurance. Along

with this, through medical insurance Jake is beneficial in terms of taking money at the time of

arising diseases. There are some advantages and disadvantages of insurance which are such as

follows:

When the Jake go through insurance in order to make investment then able to protect

himself in terms of monetary which helps to enhance the lifestyle of his up to the higher level.

This kind of investment avenue allows to Jake for tax relief in which he not needs to pay any

kind of taxation amount. In case, the income of Jake scraped or stolen then insurance company

will provide to Jake which is also one kind of benefit for him. Apart from this, when he will ill

and for his treatment huge expenses are there, which will be provided by the insurance firm.

Hence, it can be said that insurance will be highly supportive for Jake in order manage wealth

and lifestyle both.

In contrary to this, disadvantage of insurance is that amount of superannuation is affected

in negative manner because the deductions of insurance amount will be from fund of the

superannuation. Apart from this, if the Jake not come under any disease and not arise any kind of

expenses related to treatment then any benefit will not be there. Along with this, whole

premiums or funds of medical insurance will not be provided return to Jake.

SUPERANNUATION / RETIREMENT PLANNING

Objective of the Jake regarding to the retirement planning as well as superannuation is to

take retirement before 2 years which is at the age of 63 years rather than standards age of

retirement 65 years. In this the Jake should adopt the Transition to Retirement (TTR) strategy in

which the benefits and allowances given by firm are to be sacrificed by the employee. The Jake's

employer allow to him for salary sacrifice worth of on which any kind of taxation not need to

pay as well as NIC is to be paid by company. Hence, it can be recommended that Jake needs to

adopt the strategy of Transition to Retirement and some advantages and drawbacks of it are such

as:

Very basic benefit of the TTR strategy is that it allows to Jake for supplement his level of

salary as well as boost up the lifestyle which is key objective of his. Along with this, through

suggested strategy Jake able to use tax which is saved and due to which his super or lifestyle

3

with this, through medical insurance Jake is beneficial in terms of taking money at the time of

arising diseases. There are some advantages and disadvantages of insurance which are such as

follows:

When the Jake go through insurance in order to make investment then able to protect

himself in terms of monetary which helps to enhance the lifestyle of his up to the higher level.

This kind of investment avenue allows to Jake for tax relief in which he not needs to pay any

kind of taxation amount. In case, the income of Jake scraped or stolen then insurance company

will provide to Jake which is also one kind of benefit for him. Apart from this, when he will ill

and for his treatment huge expenses are there, which will be provided by the insurance firm.

Hence, it can be said that insurance will be highly supportive for Jake in order manage wealth

and lifestyle both.

In contrary to this, disadvantage of insurance is that amount of superannuation is affected

in negative manner because the deductions of insurance amount will be from fund of the

superannuation. Apart from this, if the Jake not come under any disease and not arise any kind of

expenses related to treatment then any benefit will not be there. Along with this, whole

premiums or funds of medical insurance will not be provided return to Jake.

SUPERANNUATION / RETIREMENT PLANNING

Objective of the Jake regarding to the retirement planning as well as superannuation is to

take retirement before 2 years which is at the age of 63 years rather than standards age of

retirement 65 years. In this the Jake should adopt the Transition to Retirement (TTR) strategy in

which the benefits and allowances given by firm are to be sacrificed by the employee. The Jake's

employer allow to him for salary sacrifice worth of on which any kind of taxation not need to

pay as well as NIC is to be paid by company. Hence, it can be recommended that Jake needs to

adopt the strategy of Transition to Retirement and some advantages and drawbacks of it are such

as:

Very basic benefit of the TTR strategy is that it allows to Jake for supplement his level of

salary as well as boost up the lifestyle which is key objective of his. Along with this, through

suggested strategy Jake able to use tax which is saved and due to which his super or lifestyle

3

boost up or increase up to higher extent before the retirement or age of 65 years. In addition to

this, it is tax effective by which wealth improves ultimately.

All kinds of super fund not provide and allow to using the TTR strategy which is major

disadvantage for the Jake. Apart from this, there is specific time frame is available and within it

Jake able to take fund using TTR otherwise cannot withdraw money. In case the Jake not reaches

up to the age of preservation then unable to use this strategy in effectual manner which affects to

his lifestyle in negative manner.

ESTATE PLANNING

In the estate planning Jake wants to consider the will or inherent property which he gets

from his previous generation who are passed away. In addition to this, the will is specified and

give direction to the Jake that in which order he will deal with property which he got in the will.

Due to taking property of will Jake has various kinds of responsibilities which are necessary to

fulfil and complete by him. Through the estate planning Jake will be beneficial up to the higher

extent because it helps to improve level of property of his and make his lifestyle effectual. In

order to this, Jake needs to complete responsibilities like funeral of will givers, outstanding debt

which left by ancestors, defending those challenges which are included with the will property

etc. Hence, it can be said that estate planning is beneficial because these are inherent from

ancestors in free of costs which lead to improve the financial position and wealth up to the higher

extent. Along with this, responsibilities and other things which are ancestors left are to be

completed and fulfilled by Jake which is adverse condition of estate planning.

SOCIAL SECURITY

In the social security the government of country comes into picture where the employees

are in various kinds of beneficial situations. In the social security the government provides

assistance to the employees in terms of financial as well as monetary situations by which Jake

will be in the fruitful manner. Due to this kind of beneficial conditions Jake highly able to meet

with the objectives of wealth creation as well as enhancing the lifestyle. From the social security

Jake is in the protective and safely area which helps to reduce level of risk up to some level.

Along with this, chances of reduction in lifestyle and wealth creation will be reduce which is one

of the highly beneficial. In opposite to this, some amount from salary is needs to given to the

government which is negative aspect of social security.

4

this, it is tax effective by which wealth improves ultimately.

All kinds of super fund not provide and allow to using the TTR strategy which is major

disadvantage for the Jake. Apart from this, there is specific time frame is available and within it

Jake able to take fund using TTR otherwise cannot withdraw money. In case the Jake not reaches

up to the age of preservation then unable to use this strategy in effectual manner which affects to

his lifestyle in negative manner.

ESTATE PLANNING

In the estate planning Jake wants to consider the will or inherent property which he gets

from his previous generation who are passed away. In addition to this, the will is specified and

give direction to the Jake that in which order he will deal with property which he got in the will.

Due to taking property of will Jake has various kinds of responsibilities which are necessary to

fulfil and complete by him. Through the estate planning Jake will be beneficial up to the higher

extent because it helps to improve level of property of his and make his lifestyle effectual. In

order to this, Jake needs to complete responsibilities like funeral of will givers, outstanding debt

which left by ancestors, defending those challenges which are included with the will property

etc. Hence, it can be said that estate planning is beneficial because these are inherent from

ancestors in free of costs which lead to improve the financial position and wealth up to the higher

extent. Along with this, responsibilities and other things which are ancestors left are to be

completed and fulfilled by Jake which is adverse condition of estate planning.

SOCIAL SECURITY

In the social security the government of country comes into picture where the employees

are in various kinds of beneficial situations. In the social security the government provides

assistance to the employees in terms of financial as well as monetary situations by which Jake

will be in the fruitful manner. Due to this kind of beneficial conditions Jake highly able to meet

with the objectives of wealth creation as well as enhancing the lifestyle. From the social security

Jake is in the protective and safely area which helps to reduce level of risk up to some level.

Along with this, chances of reduction in lifestyle and wealth creation will be reduce which is one

of the highly beneficial. In opposite to this, some amount from salary is needs to given to the

government which is negative aspect of social security.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

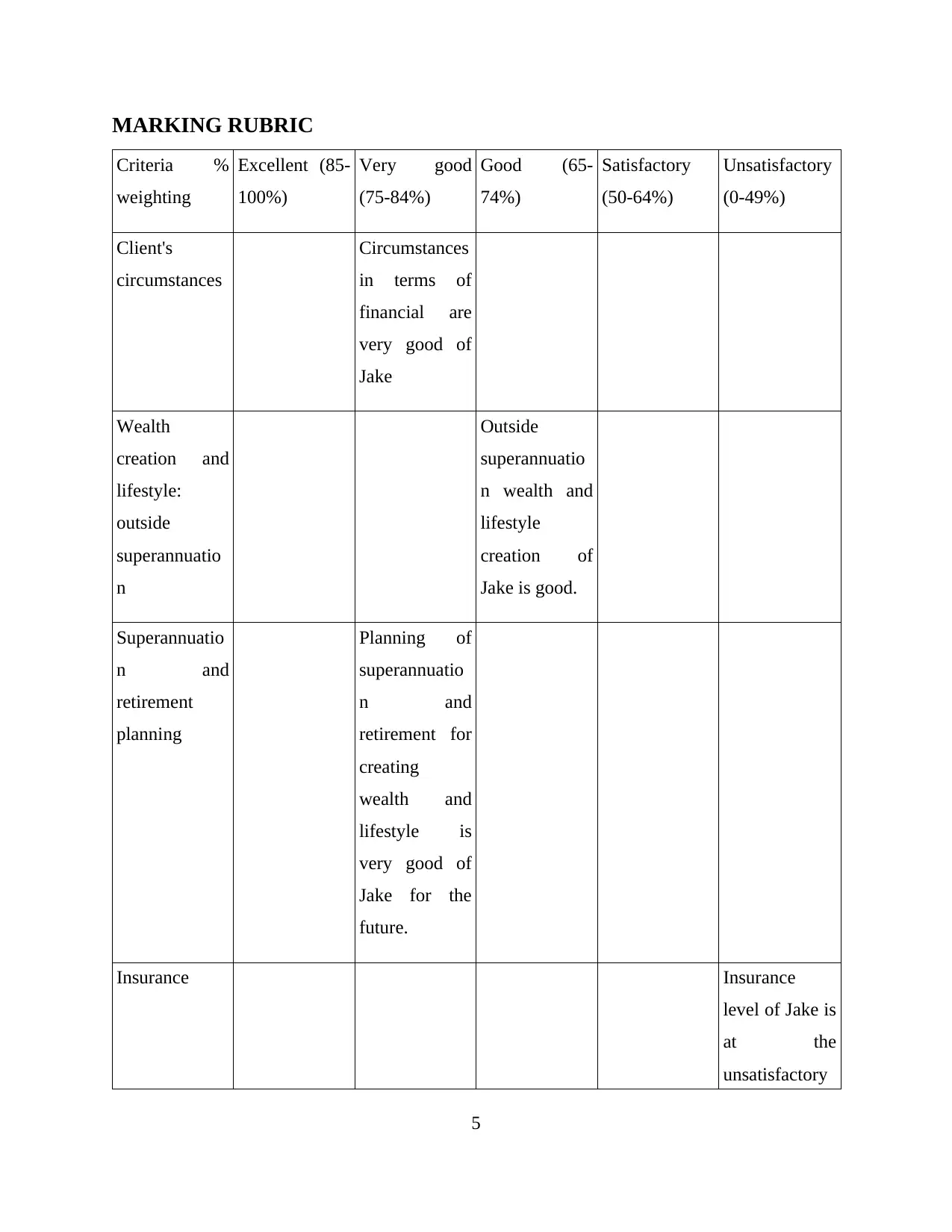

MARKING RUBRIC

Criteria %

weighting

Excellent (85-

100%)

Very good

(75-84%)

Good (65-

74%)

Satisfactory

(50-64%)

Unsatisfactory

(0-49%)

Client's

circumstances

Circumstances

in terms of

financial are

very good of

Jake

Wealth

creation and

lifestyle:

outside

superannuatio

n

Outside

superannuatio

n wealth and

lifestyle

creation of

Jake is good.

Superannuatio

n and

retirement

planning

Planning of

superannuatio

n and

retirement for

creating

wealth and

lifestyle is

very good of

Jake for the

future.

Insurance Insurance

level of Jake is

at the

unsatisfactory

5

Criteria %

weighting

Excellent (85-

100%)

Very good

(75-84%)

Good (65-

74%)

Satisfactory

(50-64%)

Unsatisfactory

(0-49%)

Client's

circumstances

Circumstances

in terms of

financial are

very good of

Jake

Wealth

creation and

lifestyle:

outside

superannuatio

n

Outside

superannuatio

n wealth and

lifestyle

creation of

Jake is good.

Superannuatio

n and

retirement

planning

Planning of

superannuatio

n and

retirement for

creating

wealth and

lifestyle is

very good of

Jake for the

future.

Insurance Insurance

level of Jake is

at the

unsatisfactory

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

level.

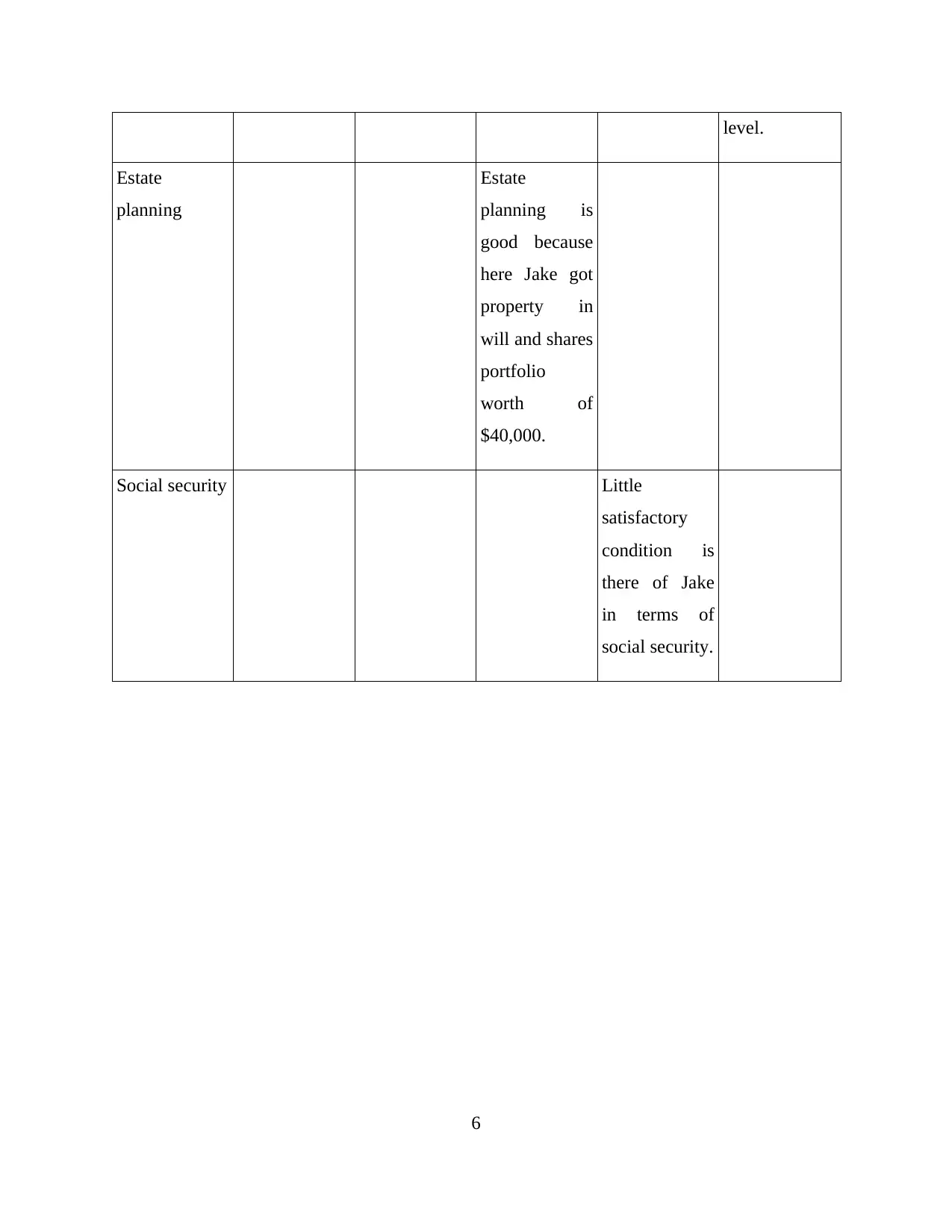

Estate

planning

Estate

planning is

good because

here Jake got

property in

will and shares

portfolio

worth of

$40,000.

Social security Little

satisfactory

condition is

there of Jake

in terms of

social security.

6

Estate

planning

Estate

planning is

good because

here Jake got

property in

will and shares

portfolio

worth of

$40,000.

Social security Little

satisfactory

condition is

there of Jake

in terms of

social security.

6

REFERENCES

Journals and Books

Baker, H. K. and Ricciardi, V., 2014. Investor behavior: The psychology of financial planning

and investing. John Wiley & Sons.

Boisclair, D., Lusardi, A. and Michaud, P.C., 2015. Financial literacy and retirement planning in

Canada. Journal of Pension Economics & Finance. pp. 1-20.

Delgadillo, L. M., 2014. Financial clarity: Education, literacy, capability, counseling, planning,

and coaching. Family and Consumer Sciences Research Journal. 43(1). pp. 18-28.

Hastings, J. S., Madrian, B. C. and Skimmyhorn, W. L., 2013. Financial literacy, financial

education, and economic outcomes. Annu. Rev. Econ. 5(1). pp. 347-373.

Jalil, M., Abdul Razak, D. and Azam, F., 2013. Exploring factors influencing financial planning

after retirement: structural equation modeling approach. American Journal of Applied

Sciences. 10(3). pp. 270-279.

Parks, B., Olson, P. D. and Bokor, D. W., 2015. Don't mistake business plans for planning (it

may be dangerous to your financial health). Journal of small business strategy. 2(1). pp.

15-24.

Serna, G. R., 2013. Understanding the effects of state oversight and fiscal policy on university

revenues: Considerations for financial planning. Planning for Higher Education. 41(2). p.

93.

Online

Power, T., 2017. TRIPs: 10 interesting facts about transition-to-retirement pensions. [Online].

Available through: <https://www.superguide.com.au/boost-your-superannuation/trips-

facts-about-transition-to-retirement-pensions> [Accessed on 1st June 2017].

7

Journals and Books

Baker, H. K. and Ricciardi, V., 2014. Investor behavior: The psychology of financial planning

and investing. John Wiley & Sons.

Boisclair, D., Lusardi, A. and Michaud, P.C., 2015. Financial literacy and retirement planning in

Canada. Journal of Pension Economics & Finance. pp. 1-20.

Delgadillo, L. M., 2014. Financial clarity: Education, literacy, capability, counseling, planning,

and coaching. Family and Consumer Sciences Research Journal. 43(1). pp. 18-28.

Hastings, J. S., Madrian, B. C. and Skimmyhorn, W. L., 2013. Financial literacy, financial

education, and economic outcomes. Annu. Rev. Econ. 5(1). pp. 347-373.

Jalil, M., Abdul Razak, D. and Azam, F., 2013. Exploring factors influencing financial planning

after retirement: structural equation modeling approach. American Journal of Applied

Sciences. 10(3). pp. 270-279.

Parks, B., Olson, P. D. and Bokor, D. W., 2015. Don't mistake business plans for planning (it

may be dangerous to your financial health). Journal of small business strategy. 2(1). pp.

15-24.

Serna, G. R., 2013. Understanding the effects of state oversight and fiscal policy on university

revenues: Considerations for financial planning. Planning for Higher Education. 41(2). p.

93.

Online

Power, T., 2017. TRIPs: 10 interesting facts about transition-to-retirement pensions. [Online].

Available through: <https://www.superguide.com.au/boost-your-superannuation/trips-

facts-about-transition-to-retirement-pensions> [Accessed on 1st June 2017].

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.