Analysis of Management Accounting & Financial Planning - BETA IT

VerifiedAdded on 2023/06/17

|10

|3068

|321

Report

AI Summary

This report provides an analysis of management accounting and financial planning strategies within the context of BETA IT, a Dubai-based IT company. It covers various aspects of standard costing, including its types and limitations, and compares it with target costing. The report also examines the role of the contribution technique in decision-making, highlighting its use in determining minimum sale prices, analyzing profit, calculating break-even points, and deciding the margin of safety. Furthermore, it interprets how the transfer pricing approach can improve business gains by optimizing tax deductions and employing methods like the comparable uncontrolled price method. The analysis uses examples to illustrate the practical application of these techniques, emphasizing their importance in cost control, performance analysis, and profitability enhancement for BETA IT.

Management

Accounting and

Financial Planning

Accounting and

Financial Planning

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

MAIN BODY...................................................................................................................................3

Describe standard costing in addition to its types. Also specify its limitations.....................3

Discuss about Target costing and how it differs with Standard costing.................................4

Describe the role of contribution technique for making decisions.........................................6

Interpret the manner in which transfer pricing approach helps in improving the gains of

business...................................................................................................................................7

CONCLUSION ...............................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION ..........................................................................................................................3

MAIN BODY...................................................................................................................................3

Describe standard costing in addition to its types. Also specify its limitations.....................3

Discuss about Target costing and how it differs with Standard costing.................................4

Describe the role of contribution technique for making decisions.........................................6

Interpret the manner in which transfer pricing approach helps in improving the gains of

business...................................................................................................................................7

CONCLUSION ...............................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION

Management accounting refers to the process of identifying, analysing and interpreting

the financial data of organisation for the purpose of taking various monetary as well as non-

monetary decisions. It prepares various types of statements and tries to find out the weaknesses

of firm so that its profitability could be increased (Tsai and Jhong, 2019). The report is based on

BETA IT company. It is a Dubai based business dealing in developing apps, software

consultancy, support and maintenance of application, IOT services ans many more. The report

discusses about various types and limitations of standard costing along with its compression with

target costing. It further provides the role of contribution technique in decision making, in

addition to analyse the approaches of transfer of price to improve the profitability of firm.

MAIN BODY

Describe standard costing in addition to its types. Also specify its limitations.

It is a process of estimating the amount of expenses that can be incurred during

production. The cost estimated in this system is then compared with the actual results to know

the difference about them and collect information about the reason behind this variation. Its

objective is to implement estimated budget correctly and examine the performance of that

operation, so that BETA can control the extra cost incurred on it. They are generally prepared

periodically and work on the previous experience of the firm. It takes advance search and finding

for determining the base for coming year.

Kinds

Normally, it has four types

Ideal standard- These are measures which are very easy to obtained in normal

conditions. It requires BETA to adopt the most favourable cost for its labour and

material along with maximum attainable output that can be produced amid of showing

highest level of efficiency. There is no space for any sort of spoilage or inefficiency in

these types of measures (Bradley and et. al., 2018).

Normal standards- They are the estimated level which are anticipated to be achieved in

future, generally for the duration of single business cycle. BETA frame these standards

while looking at its average capacity that can help it in boom and regression. The cost

recognised in this method is not revised ans remains same for the whole cycle.

Management accounting refers to the process of identifying, analysing and interpreting

the financial data of organisation for the purpose of taking various monetary as well as non-

monetary decisions. It prepares various types of statements and tries to find out the weaknesses

of firm so that its profitability could be increased (Tsai and Jhong, 2019). The report is based on

BETA IT company. It is a Dubai based business dealing in developing apps, software

consultancy, support and maintenance of application, IOT services ans many more. The report

discusses about various types and limitations of standard costing along with its compression with

target costing. It further provides the role of contribution technique in decision making, in

addition to analyse the approaches of transfer of price to improve the profitability of firm.

MAIN BODY

Describe standard costing in addition to its types. Also specify its limitations.

It is a process of estimating the amount of expenses that can be incurred during

production. The cost estimated in this system is then compared with the actual results to know

the difference about them and collect information about the reason behind this variation. Its

objective is to implement estimated budget correctly and examine the performance of that

operation, so that BETA can control the extra cost incurred on it. They are generally prepared

periodically and work on the previous experience of the firm. It takes advance search and finding

for determining the base for coming year.

Kinds

Normally, it has four types

Ideal standard- These are measures which are very easy to obtained in normal

conditions. It requires BETA to adopt the most favourable cost for its labour and

material along with maximum attainable output that can be produced amid of showing

highest level of efficiency. There is no space for any sort of spoilage or inefficiency in

these types of measures (Bradley and et. al., 2018).

Normal standards- They are the estimated level which are anticipated to be achieved in

future, generally for the duration of single business cycle. BETA frame these standards

while looking at its average capacity that can help it in boom and regression. The cost

recognised in this method is not revised ans remains same for the whole cycle.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Basic standards- These are measures which are established by firm for an undefined

period of time. These measures normally remains unaltered, but are sometimes revised

according to the fluctuation in price level. These are not used by BETA, only for the

evaluation of actual results, but also for the expected results. In other words, basic

standards work as a measure for other grades (Johnsen and Hvam, 2019).

Currently attainable standards- These measures are usually for short time period and

are related to present conditions of work. BETA follows these standards to bring

efficiency in their operations. The levels formed in them are generally very hard, but are

attainable and demands proper focus. They gives allowance for a particular level of

spoilage, wastage and breakdowns along with idle time.

Shortcomings of standard costing

Costly tool - It requires expert understanding for setting up fixed values and evaluating

them from the actual performance. This type of learning is acquired by professionals and

BETA have to spend lot of money in hiring such persons.

Demands regular revision- Due to frequent fluctuations in market, price and inflation

levels, it is very much important to update these measures from time-to-time. It is very

complicated and slow process, thus consumes a lot of time of BETA company.

Effects employee Psychology- The management has to keep in mind that the level set by

it must be attainable and in the reach of their employees. Unattainable or high measures

can make the employees of BETA dissatisfied instead of motivating them to work more.

So, standard costing guides the firm about the limit of expenses it can incur in its

operations. Though there are various drawbacks related to this technique, still this tool is very

helpful in analysing the performance and controlling the cost of various operations (Fuss, Barros

and Poganietz, 2018).

Discuss about Target costing and how it differs with Standard costing.

In this system , company pre-defines its cost, price and revenue associated with a new product or

service. If the firm feels that the good could not be prepared at planned level, then the idea of

manufacturing is dropped. These pre-set value are based on the deep deep research done by the

BETA on that product in market, on the basis of profits earned by competitors, demand of

customers and many more. Then the designed team determines the minimum and maximum cost

that would be spend for producing that material. Then, that product is created by making sure

period of time. These measures normally remains unaltered, but are sometimes revised

according to the fluctuation in price level. These are not used by BETA, only for the

evaluation of actual results, but also for the expected results. In other words, basic

standards work as a measure for other grades (Johnsen and Hvam, 2019).

Currently attainable standards- These measures are usually for short time period and

are related to present conditions of work. BETA follows these standards to bring

efficiency in their operations. The levels formed in them are generally very hard, but are

attainable and demands proper focus. They gives allowance for a particular level of

spoilage, wastage and breakdowns along with idle time.

Shortcomings of standard costing

Costly tool - It requires expert understanding for setting up fixed values and evaluating

them from the actual performance. This type of learning is acquired by professionals and

BETA have to spend lot of money in hiring such persons.

Demands regular revision- Due to frequent fluctuations in market, price and inflation

levels, it is very much important to update these measures from time-to-time. It is very

complicated and slow process, thus consumes a lot of time of BETA company.

Effects employee Psychology- The management has to keep in mind that the level set by

it must be attainable and in the reach of their employees. Unattainable or high measures

can make the employees of BETA dissatisfied instead of motivating them to work more.

So, standard costing guides the firm about the limit of expenses it can incur in its

operations. Though there are various drawbacks related to this technique, still this tool is very

helpful in analysing the performance and controlling the cost of various operations (Fuss, Barros

and Poganietz, 2018).

Discuss about Target costing and how it differs with Standard costing.

In this system , company pre-defines its cost, price and revenue associated with a new product or

service. If the firm feels that the good could not be prepared at planned level, then the idea of

manufacturing is dropped. These pre-set value are based on the deep deep research done by the

BETA on that product in market, on the basis of profits earned by competitors, demand of

customers and many more. Then the designed team determines the minimum and maximum cost

that would be spend for producing that material. Then, that product is created by making sure

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

quality material, timely transportation of inputs, adequate number with minimum price. The

main aim is to provide a tool for planning and managing the cost. This technique makes BETA

price taker instead of making it price maker. In simple words, contribution analysis determines

the extent to which the payment received from individual goods helps in recovering the fixed

cost and at which unit, the product will start earning profit for it (Petrovich, Hille and

Wüstenhagen, 2019).

Advantages of Target costing

It makes sure that the desired profit can be achieved as they are framed by the conducting

research of that product. This makes the employees confident that that set target is in their

reach and they should put efforts to attain that.

The cost of product is pre-defined which helps BETA in controlling the cost of

production at every step.

It provides a proper and formal process according to which the whole operation of

production is carried on. This ultimately, helps BETA in eliminating all the wasteful

activities that can increase the amount of cost.

Target costing demands the integration of all the employees of every department. It

works with the coordination of all of them. This results in bringing efficiency in the

organisational environment (Warren, Reeve and Duchac, 2017).

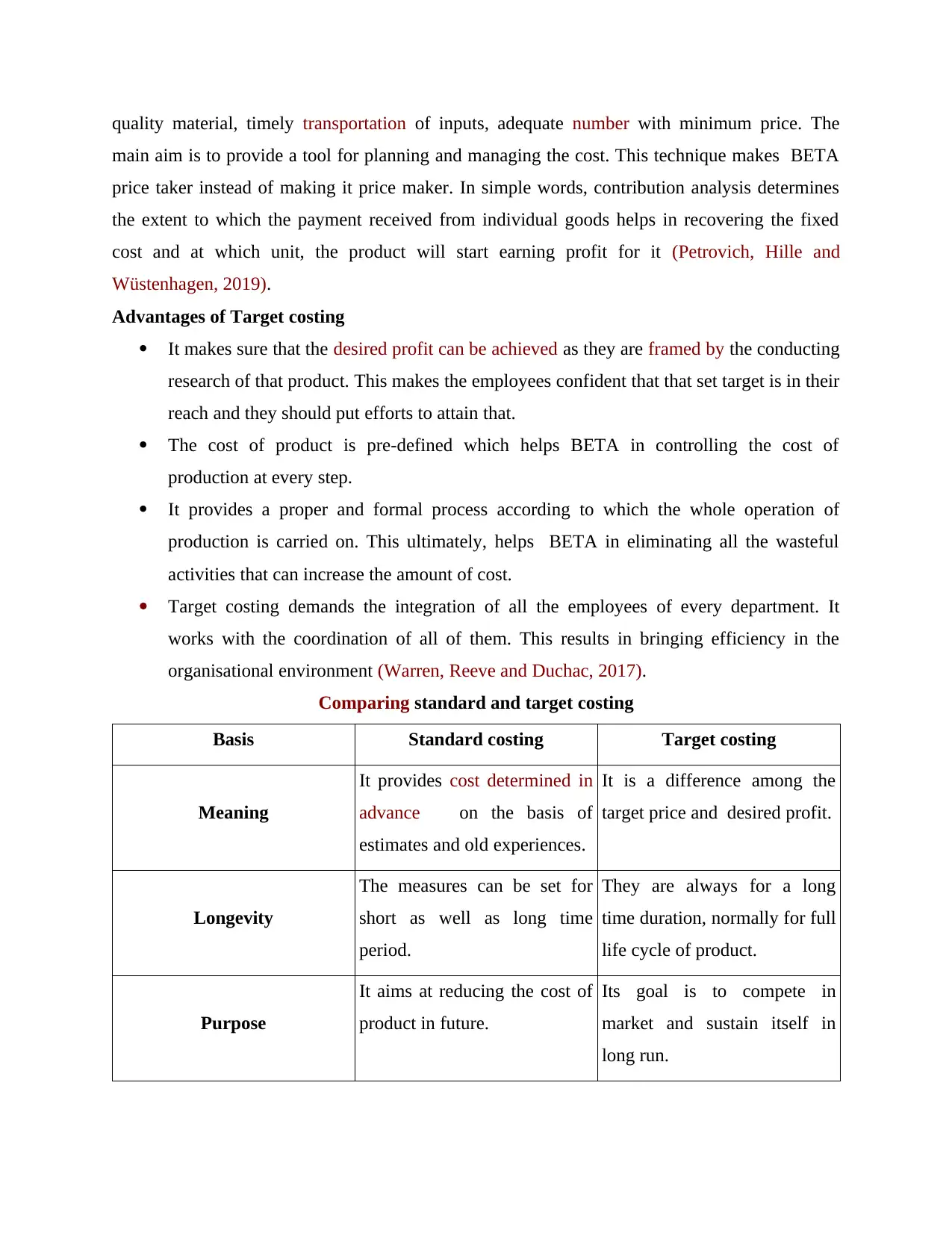

Comparing standard and target costing

Basis Standard costing Target costing

Meaning

It provides cost determined in

advance on the basis of

estimates and old experiences.

It is a difference among the

target price and desired profit.

Longevity

The measures can be set for

short as well as long time

period.

They are always for a long

time duration, normally for full

life cycle of product.

Purpose

It aims at reducing the cost of

product in future.

Its goal is to compete in

market and sustain itself in

long run.

main aim is to provide a tool for planning and managing the cost. This technique makes BETA

price taker instead of making it price maker. In simple words, contribution analysis determines

the extent to which the payment received from individual goods helps in recovering the fixed

cost and at which unit, the product will start earning profit for it (Petrovich, Hille and

Wüstenhagen, 2019).

Advantages of Target costing

It makes sure that the desired profit can be achieved as they are framed by the conducting

research of that product. This makes the employees confident that that set target is in their

reach and they should put efforts to attain that.

The cost of product is pre-defined which helps BETA in controlling the cost of

production at every step.

It provides a proper and formal process according to which the whole operation of

production is carried on. This ultimately, helps BETA in eliminating all the wasteful

activities that can increase the amount of cost.

Target costing demands the integration of all the employees of every department. It

works with the coordination of all of them. This results in bringing efficiency in the

organisational environment (Warren, Reeve and Duchac, 2017).

Comparing standard and target costing

Basis Standard costing Target costing

Meaning

It provides cost determined in

advance on the basis of

estimates and old experiences.

It is a difference among the

target price and desired profit.

Longevity

The measures can be set for

short as well as long time

period.

They are always for a long

time duration, normally for full

life cycle of product.

Purpose

It aims at reducing the cost of

product in future.

Its goal is to compete in

market and sustain itself in

long run.

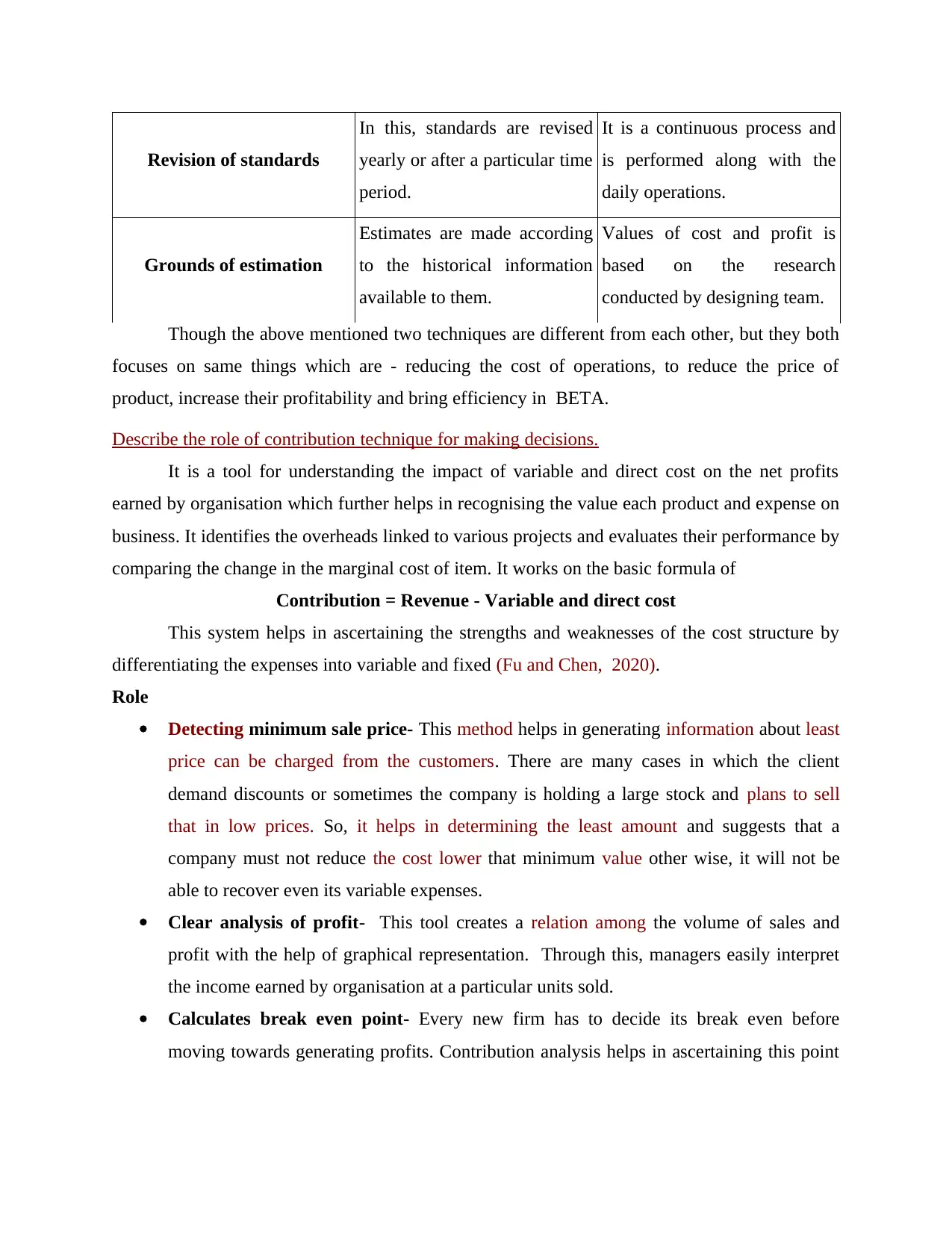

Revision of standards

In this, standards are revised

yearly or after a particular time

period.

It is a continuous process and

is performed along with the

daily operations.

Grounds of estimation

Estimates are made according

to the historical information

available to them.

Values of cost and profit is

based on the research

conducted by designing team.

Though the above mentioned two techniques are different from each other, but they both

focuses on same things which are - reducing the cost of operations, to reduce the price of

product, increase their profitability and bring efficiency in BETA.

Describe the role of contribution technique for making decisions.

It is a tool for understanding the impact of variable and direct cost on the net profits

earned by organisation which further helps in recognising the value each product and expense on

business. It identifies the overheads linked to various projects and evaluates their performance by

comparing the change in the marginal cost of item. It works on the basic formula of

Contribution = Revenue - Variable and direct cost

This system helps in ascertaining the strengths and weaknesses of the cost structure by

differentiating the expenses into variable and fixed (Fu and Chen, 2020).

Role

Detecting minimum sale price- This method helps in generating information about least

price can be charged from the customers. There are many cases in which the client

demand discounts or sometimes the company is holding a large stock and plans to sell

that in low prices. So, it helps in determining the least amount and suggests that a

company must not reduce the cost lower that minimum value other wise, it will not be

able to recover even its variable expenses.

Clear analysis of profit- This tool creates a relation among the volume of sales and

profit with the help of graphical representation. Through this, managers easily interpret

the income earned by organisation at a particular units sold.

Calculates break even point- Every new firm has to decide its break even before

moving towards generating profits. Contribution analysis helps in ascertaining this point

In this, standards are revised

yearly or after a particular time

period.

It is a continuous process and

is performed along with the

daily operations.

Grounds of estimation

Estimates are made according

to the historical information

available to them.

Values of cost and profit is

based on the research

conducted by designing team.

Though the above mentioned two techniques are different from each other, but they both

focuses on same things which are - reducing the cost of operations, to reduce the price of

product, increase their profitability and bring efficiency in BETA.

Describe the role of contribution technique for making decisions.

It is a tool for understanding the impact of variable and direct cost on the net profits

earned by organisation which further helps in recognising the value each product and expense on

business. It identifies the overheads linked to various projects and evaluates their performance by

comparing the change in the marginal cost of item. It works on the basic formula of

Contribution = Revenue - Variable and direct cost

This system helps in ascertaining the strengths and weaknesses of the cost structure by

differentiating the expenses into variable and fixed (Fu and Chen, 2020).

Role

Detecting minimum sale price- This method helps in generating information about least

price can be charged from the customers. There are many cases in which the client

demand discounts or sometimes the company is holding a large stock and plans to sell

that in low prices. So, it helps in determining the least amount and suggests that a

company must not reduce the cost lower that minimum value other wise, it will not be

able to recover even its variable expenses.

Clear analysis of profit- This tool creates a relation among the volume of sales and

profit with the help of graphical representation. Through this, managers easily interpret

the income earned by organisation at a particular units sold.

Calculates break even point- Every new firm has to decide its break even before

moving towards generating profits. Contribution analysis helps in ascertaining this point

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

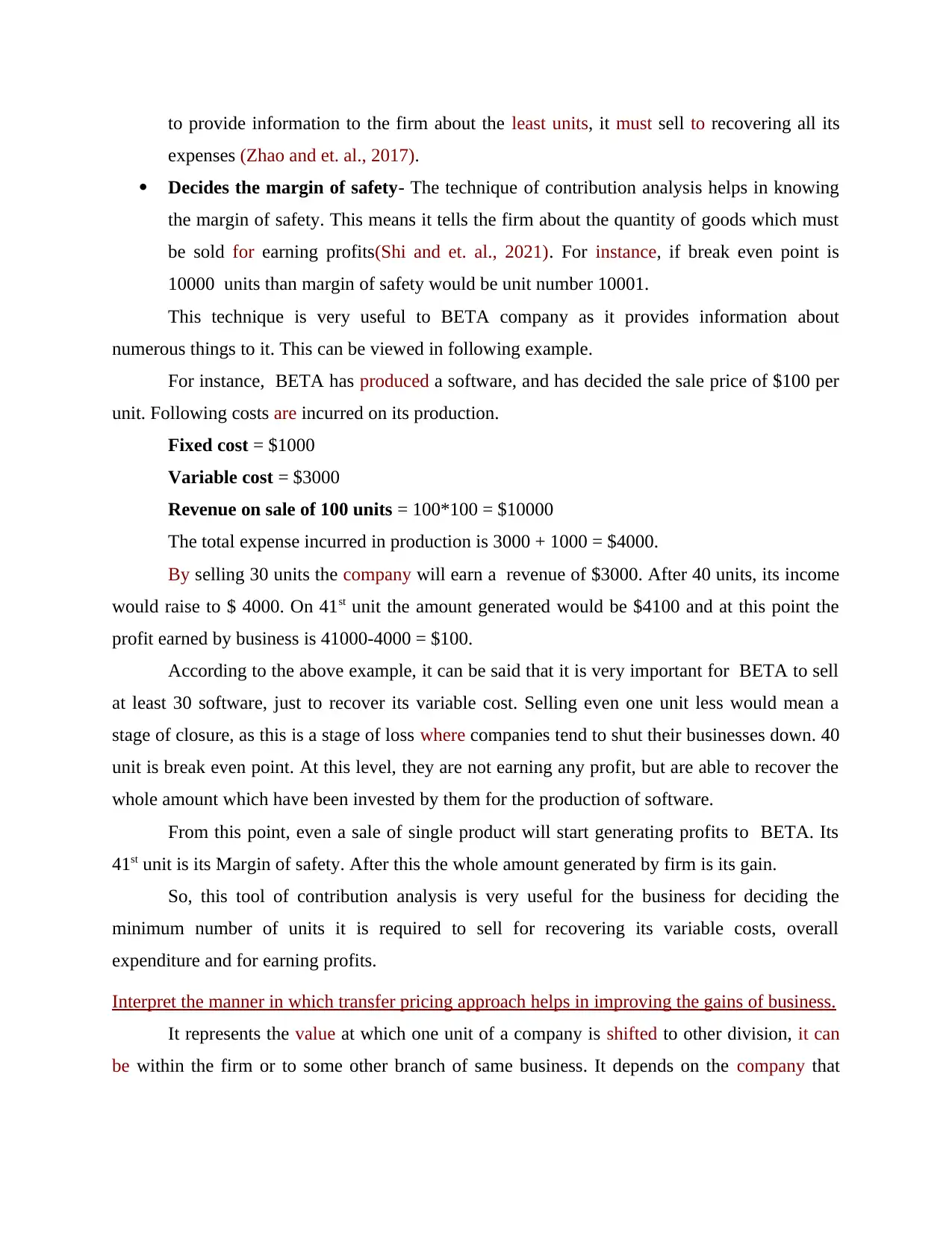

to provide information to the firm about the least units, it must sell to recovering all its

expenses (Zhao and et. al., 2017).

Decides the margin of safety- The technique of contribution analysis helps in knowing

the margin of safety. This means it tells the firm about the quantity of goods which must

be sold for earning profits(Shi and et. al., 2021). For instance, if break even point is

10000 units than margin of safety would be unit number 10001.

This technique is very useful to BETA company as it provides information about

numerous things to it. This can be viewed in following example.

For instance, BETA has produced a software, and has decided the sale price of $100 per

unit. Following costs are incurred on its production.

Fixed cost = $1000

Variable cost = $3000

Revenue on sale of 100 units = 100*100 = $10000

The total expense incurred in production is 3000 + 1000 = $4000.

By selling 30 units the company will earn a revenue of $3000. After 40 units, its income

would raise to $ 4000. On 41st unit the amount generated would be $4100 and at this point the

profit earned by business is 41000-4000 = $100.

According to the above example, it can be said that it is very important for BETA to sell

at least 30 software, just to recover its variable cost. Selling even one unit less would mean a

stage of closure, as this is a stage of loss where companies tend to shut their businesses down. 40

unit is break even point. At this level, they are not earning any profit, but are able to recover the

whole amount which have been invested by them for the production of software.

From this point, even a sale of single product will start generating profits to BETA. Its

41st unit is its Margin of safety. After this the whole amount generated by firm is its gain.

So, this tool of contribution analysis is very useful for the business for deciding the

minimum number of units it is required to sell for recovering its variable costs, overall

expenditure and for earning profits.

Interpret the manner in which transfer pricing approach helps in improving the gains of business.

It represents the value at which one unit of a company is shifted to other division, it can

be within the firm or to some other branch of same business. It depends on the company that

expenses (Zhao and et. al., 2017).

Decides the margin of safety- The technique of contribution analysis helps in knowing

the margin of safety. This means it tells the firm about the quantity of goods which must

be sold for earning profits(Shi and et. al., 2021). For instance, if break even point is

10000 units than margin of safety would be unit number 10001.

This technique is very useful to BETA company as it provides information about

numerous things to it. This can be viewed in following example.

For instance, BETA has produced a software, and has decided the sale price of $100 per

unit. Following costs are incurred on its production.

Fixed cost = $1000

Variable cost = $3000

Revenue on sale of 100 units = 100*100 = $10000

The total expense incurred in production is 3000 + 1000 = $4000.

By selling 30 units the company will earn a revenue of $3000. After 40 units, its income

would raise to $ 4000. On 41st unit the amount generated would be $4100 and at this point the

profit earned by business is 41000-4000 = $100.

According to the above example, it can be said that it is very important for BETA to sell

at least 30 software, just to recover its variable cost. Selling even one unit less would mean a

stage of closure, as this is a stage of loss where companies tend to shut their businesses down. 40

unit is break even point. At this level, they are not earning any profit, but are able to recover the

whole amount which have been invested by them for the production of software.

From this point, even a sale of single product will start generating profits to BETA. Its

41st unit is its Margin of safety. After this the whole amount generated by firm is its gain.

So, this tool of contribution analysis is very useful for the business for deciding the

minimum number of units it is required to sell for recovering its variable costs, overall

expenditure and for earning profits.

Interpret the manner in which transfer pricing approach helps in improving the gains of business.

It represents the value at which one unit of a company is shifted to other division, it can

be within the firm or to some other branch of same business. It depends on the company that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

whether the firm delivers the product at cost or profits. The main aim behind charging this profit

is to take advantage of tax deduction for the purchasing subsidiary (Buchholz and et. al., 2020).

Different approaches

Comparable uncontrolled price method- This tool creates a relation among the

controlled and uncontrolled transaction among two unrelated parties by comparing their

price and circumstances. This helps BETA in determining the price it can charge for its

product, so that the cost remains acceptable for the buyers and business can also earn

profits from it. So, it provides a strategic price through which profitability of organisation

can be increased (van Walbeek and van der Zee, 2018).

Cost Plus method- It is normally castes by the parties dealing in semi- finished products.

Here, the seller of goods demands a markup price added in the cost of goods sold to

buyer, so that it can earn enough amount that its direct as well as indirect expenses can

be recovered out of it. It helps the BETA in estimating the value it must charge while

transferring the goods so that its profitability is maximized.

Transactional net margin method- This mode ascertains the profit through the net

profit of controlled transactions. This value is further used for the comparison with

uncontrolled affairs. It helps BETA in recognising the profit that can be generated form

the manufacturing, sales and distribution activities, so that it can increase the level of

profit by improving its cost maintenance techniques.

Profit split method- This method is used when the two parties are involved in any such

transaction whose impact cannot be separated. It examines the way third parties divide

the profits linked with similar transactions. The technique is normally applied in

intangible assets which are difficult to get apart. This could help BETA in understanding

the prices in more holistic way by determining the accurate value of their asset. With the

help of this technique the firm can decide the part of tax it needs to pay related to

particular transaction, so that it can prevents itself form paying extra tax on that and

decrease its losses. In this way, company can improve its profitability.

CONCLUSION

It can be concluded from the above report that various techniques of management

accounting helps in controlling the cost and revenues of business. It provides standards which

further helps in determining the variations between the budgeted value and the actual results, so

is to take advantage of tax deduction for the purchasing subsidiary (Buchholz and et. al., 2020).

Different approaches

Comparable uncontrolled price method- This tool creates a relation among the

controlled and uncontrolled transaction among two unrelated parties by comparing their

price and circumstances. This helps BETA in determining the price it can charge for its

product, so that the cost remains acceptable for the buyers and business can also earn

profits from it. So, it provides a strategic price through which profitability of organisation

can be increased (van Walbeek and van der Zee, 2018).

Cost Plus method- It is normally castes by the parties dealing in semi- finished products.

Here, the seller of goods demands a markup price added in the cost of goods sold to

buyer, so that it can earn enough amount that its direct as well as indirect expenses can

be recovered out of it. It helps the BETA in estimating the value it must charge while

transferring the goods so that its profitability is maximized.

Transactional net margin method- This mode ascertains the profit through the net

profit of controlled transactions. This value is further used for the comparison with

uncontrolled affairs. It helps BETA in recognising the profit that can be generated form

the manufacturing, sales and distribution activities, so that it can increase the level of

profit by improving its cost maintenance techniques.

Profit split method- This method is used when the two parties are involved in any such

transaction whose impact cannot be separated. It examines the way third parties divide

the profits linked with similar transactions. The technique is normally applied in

intangible assets which are difficult to get apart. This could help BETA in understanding

the prices in more holistic way by determining the accurate value of their asset. With the

help of this technique the firm can decide the part of tax it needs to pay related to

particular transaction, so that it can prevents itself form paying extra tax on that and

decrease its losses. In this way, company can improve its profitability.

CONCLUSION

It can be concluded from the above report that various techniques of management

accounting helps in controlling the cost and revenues of business. It provides standards which

further helps in determining the variations between the budgeted value and the actual results, so

that corrective measures could be taken in time. The other technique of target costing also helps

in controlling cost but it estimates all the figures in advance and tries to work within that limit

only. Further, the contribution analysis helps in ascertaining level the product can recover its

variable and fixed cost and the point at which it will start bringing profit for firm. Some firms do

sell their goods to its own branch after adding some gain it. So, this transfer price can be can be

known by implementing its approaches. All these mode from one way or the other helps in

improving the profitability and performance of business.

in controlling cost but it estimates all the figures in advance and tries to work within that limit

only. Further, the contribution analysis helps in ascertaining level the product can recover its

variable and fixed cost and the point at which it will start bringing profit for firm. Some firms do

sell their goods to its own branch after adding some gain it. So, this transfer price can be can be

known by implementing its approaches. All these mode from one way or the other helps in

improving the profitability and performance of business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Tsai, W.H. and Jhong, S.Y., 2019. Production decision model with carbon tax for the knitted

footwear industry under activity-based costing. Journal of cleaner production. 207.

pp.1150-1162.

Bradley, R. and et. al., 2018. A total life cycle cost model (TLCCM) for the circular economy

and its application to post-recovery resource allocation. Resources, Conservation and

Recycling. 135. pp.141-149.

Johnsen, S.M. and Hvam, L., 2019. Understanding the impact of non-standard customisations in

an engineer-to-order context: A case study. International Journal of Production

Research. 57(21). pp.6780-6794.

Fuss, M., Barros, R.T.V. and Poganietz, W.R., 2018. Designing a framework for municipal solid

waste management towards sustainability in emerging economy countries-An

application to a case study in Belo Horizonte (Brazil). Journal of Cleaner

Production. 178. pp.655-664.

Petrovich, B., Hille, S.L. and Wüstenhagen, R., 2019. Beauty and the budget: A segmentation of

residential solar adopters. Ecological Economics. 164. p.106353.

Warren, C.S., Reeve, J.M. and Duchac, J., 2017. Accounting. Cengage Learning.

Fu, X. and Chen, S., 2020. Geochemical characteristics and sources of Chang 8 crude oil from

Xiaoxian area, Southwest margin of the Ordos Basin, China. Energy Sources, Part A:

Recovery, Utilization, and Environmental Effects, pp.1-12.

Zhao, Y. and et. al., 2017. Grain price forecasting using a hybrid stochastic method. Asia-Pacific

Journal of Operational Research. 34(05). p.1750020.

Shi, W. and et. al., 2021. An effective Two-Stage Electricity Price forecasting scheme. Electric

Power Systems Research. 199. p.107416.

Buchholz, P. and et. al., 2020. Leaning against the wind: low-price benchmarks for acting

anticyclically in the metal markets. Mineral Economics. 33(1). pp.81-100.

van Walbeek, C. and van der Zee, K., 2018. Collecting cigarette price data on a limited

budget. Tobacco Induced Diseases. 16(1).

Books and Journals

Tsai, W.H. and Jhong, S.Y., 2019. Production decision model with carbon tax for the knitted

footwear industry under activity-based costing. Journal of cleaner production. 207.

pp.1150-1162.

Bradley, R. and et. al., 2018. A total life cycle cost model (TLCCM) for the circular economy

and its application to post-recovery resource allocation. Resources, Conservation and

Recycling. 135. pp.141-149.

Johnsen, S.M. and Hvam, L., 2019. Understanding the impact of non-standard customisations in

an engineer-to-order context: A case study. International Journal of Production

Research. 57(21). pp.6780-6794.

Fuss, M., Barros, R.T.V. and Poganietz, W.R., 2018. Designing a framework for municipal solid

waste management towards sustainability in emerging economy countries-An

application to a case study in Belo Horizonte (Brazil). Journal of Cleaner

Production. 178. pp.655-664.

Petrovich, B., Hille, S.L. and Wüstenhagen, R., 2019. Beauty and the budget: A segmentation of

residential solar adopters. Ecological Economics. 164. p.106353.

Warren, C.S., Reeve, J.M. and Duchac, J., 2017. Accounting. Cengage Learning.

Fu, X. and Chen, S., 2020. Geochemical characteristics and sources of Chang 8 crude oil from

Xiaoxian area, Southwest margin of the Ordos Basin, China. Energy Sources, Part A:

Recovery, Utilization, and Environmental Effects, pp.1-12.

Zhao, Y. and et. al., 2017. Grain price forecasting using a hybrid stochastic method. Asia-Pacific

Journal of Operational Research. 34(05). p.1750020.

Shi, W. and et. al., 2021. An effective Two-Stage Electricity Price forecasting scheme. Electric

Power Systems Research. 199. p.107416.

Buchholz, P. and et. al., 2020. Leaning against the wind: low-price benchmarks for acting

anticyclically in the metal markets. Mineral Economics. 33(1). pp.81-100.

van Walbeek, C. and van der Zee, K., 2018. Collecting cigarette price data on a limited

budget. Tobacco Induced Diseases. 16(1).

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.