Financial Analysis and Planning for Melbourne Property Purchase

VerifiedAdded on 2021/05/27

|12

|2059

|33

Report

AI Summary

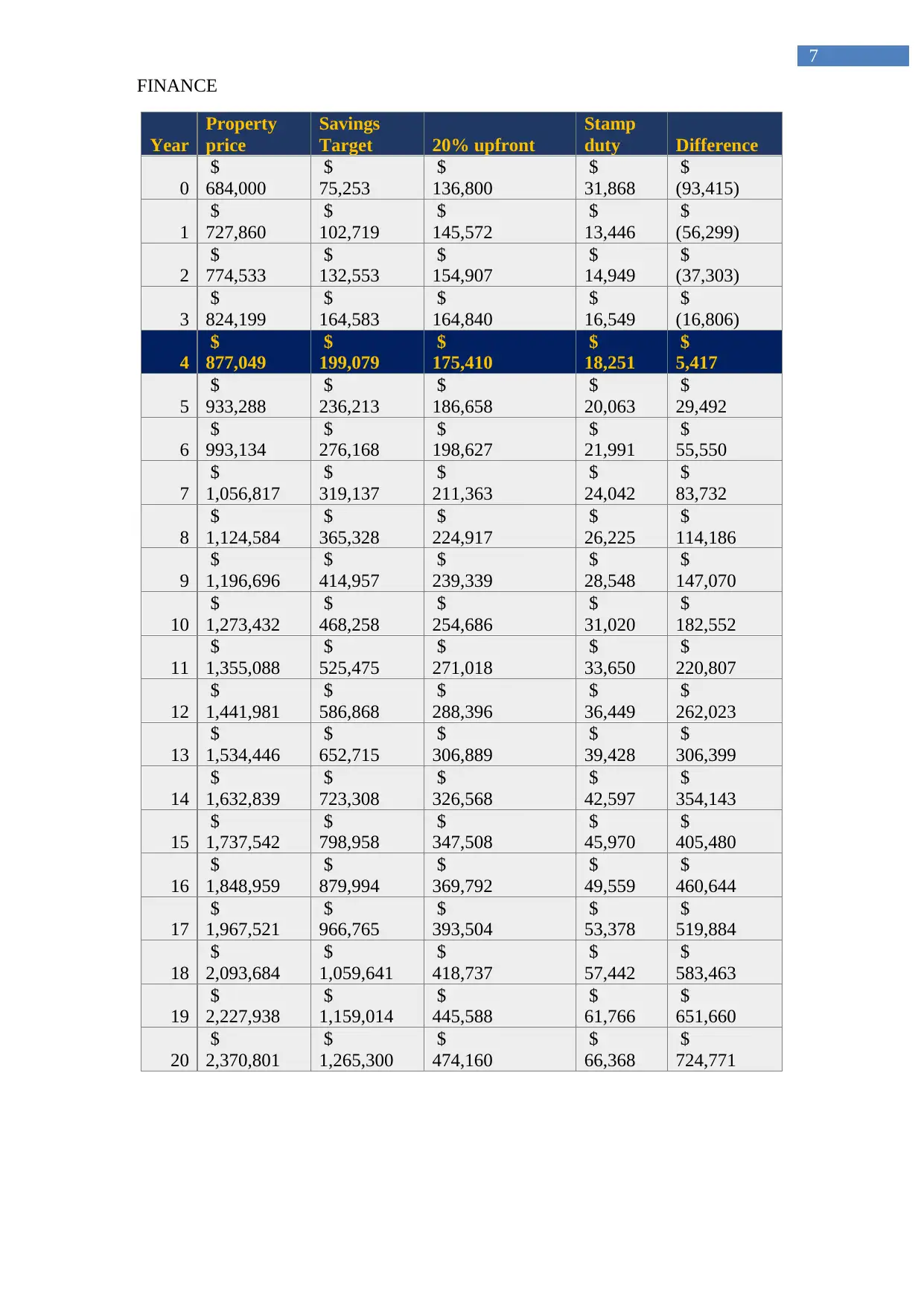

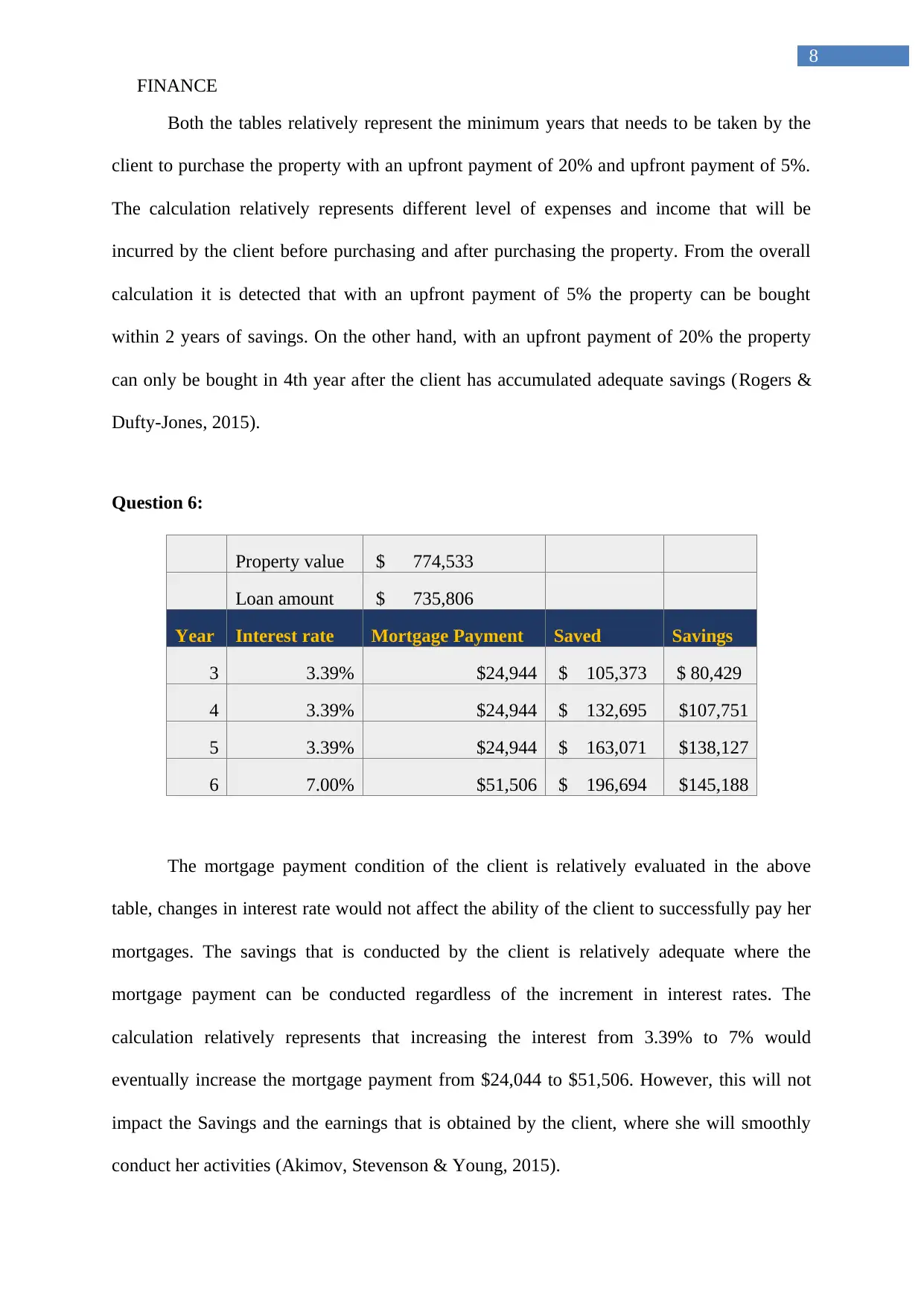

This finance report provides a comprehensive financial analysis for a client aiming to purchase property in Melbourne, Australia. It begins by examining historical property price trends to project future growth and investment needs, utilizing calculations to determine the potential increase in property value over 20 years. The report includes an analysis of income data, inflation rates, and average income increments to forecast the client's savings potential. Detailed calculations are presented to assess the client's monthly and yearly income, expenses, and savings, which are then used to evaluate mortgage options with and without insurance premiums. The report explores different loan scenarios, considering factors such as LVR, deposit amounts, stamp duty, and insurance costs. Furthermore, it analyzes the time required to accumulate sufficient funds for a property purchase under different upfront payment conditions (5% and 20%). Finally, the report assesses the impact of interest rate changes on mortgage payments and identifies potential risks that could affect the financial plan's success, such as job loss or economic downturns. The report concludes by referencing relevant financial and economic literature.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.