Detailed Financial Plan for Alastair and Wendy Windsor's Future

VerifiedAdded on 2022/11/26

|24

|1145

|371

Report

AI Summary

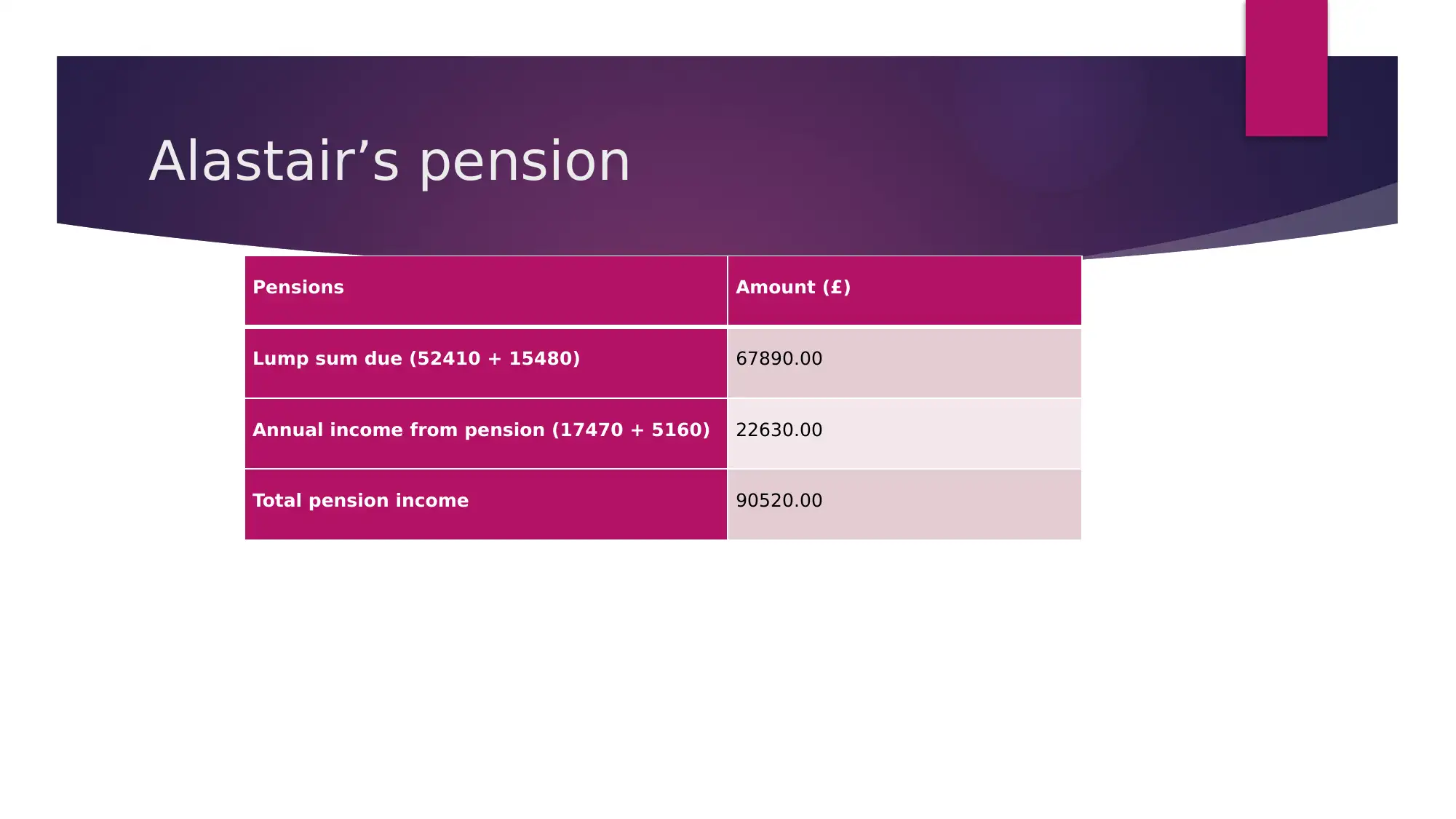

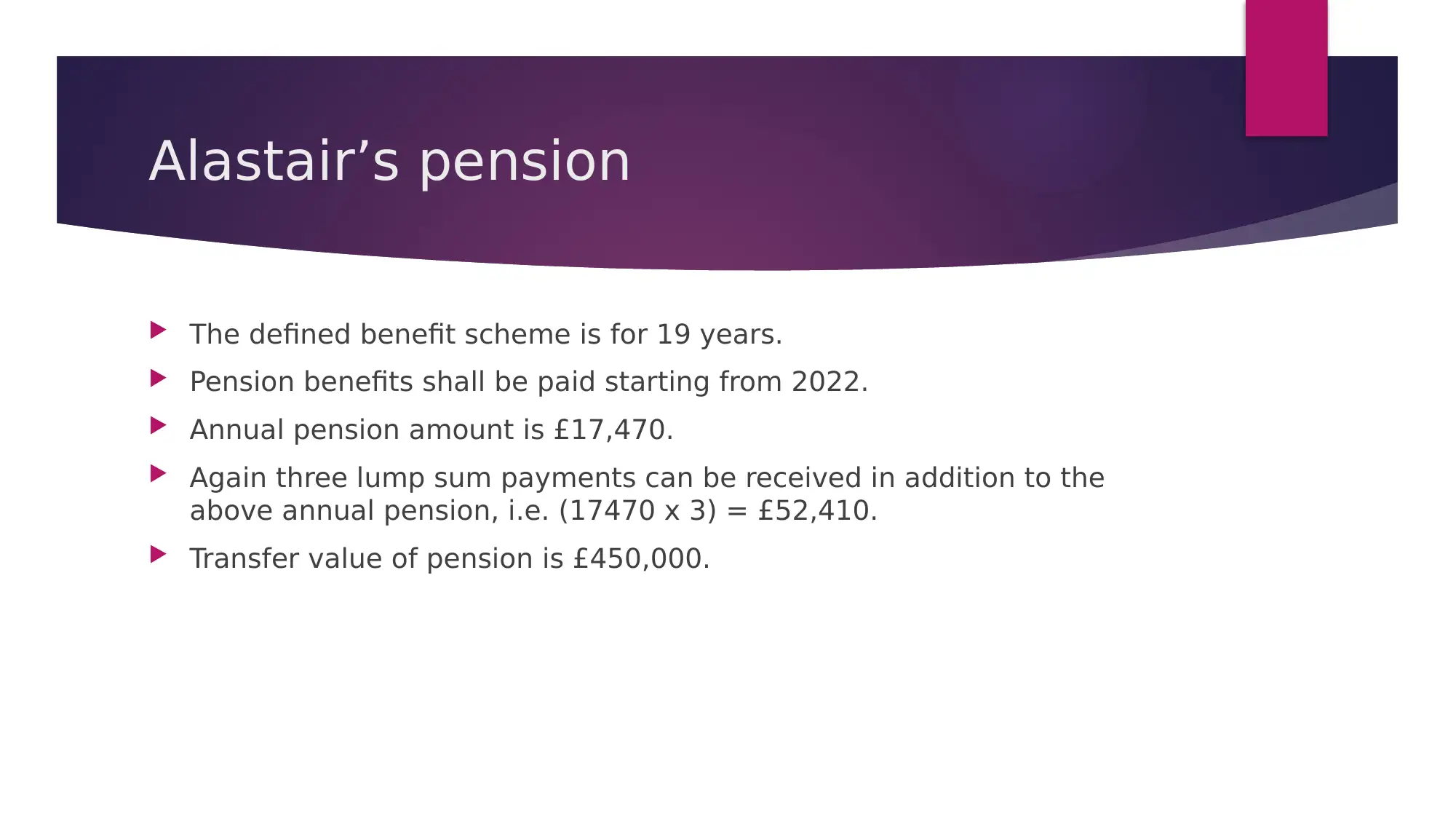

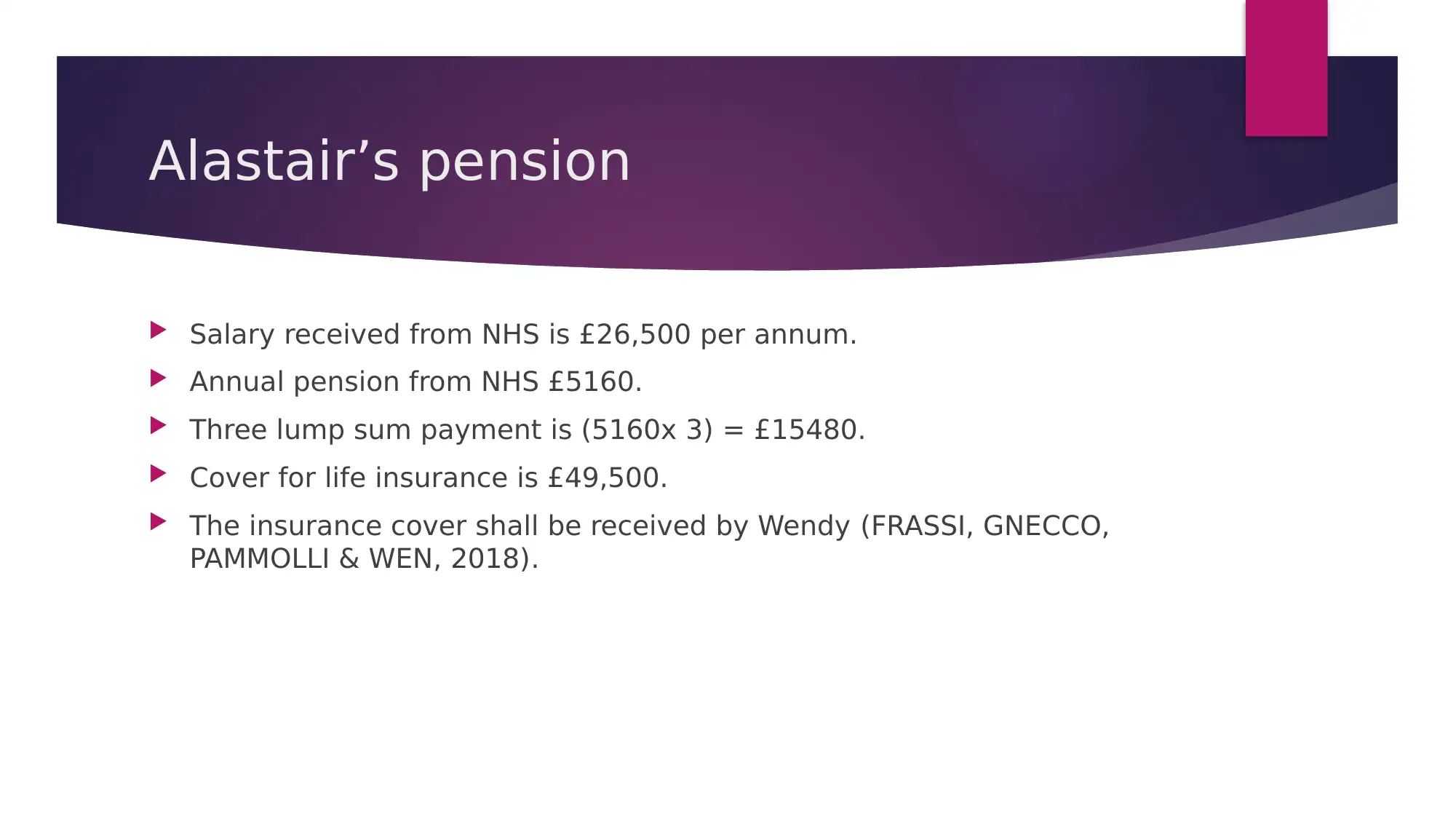

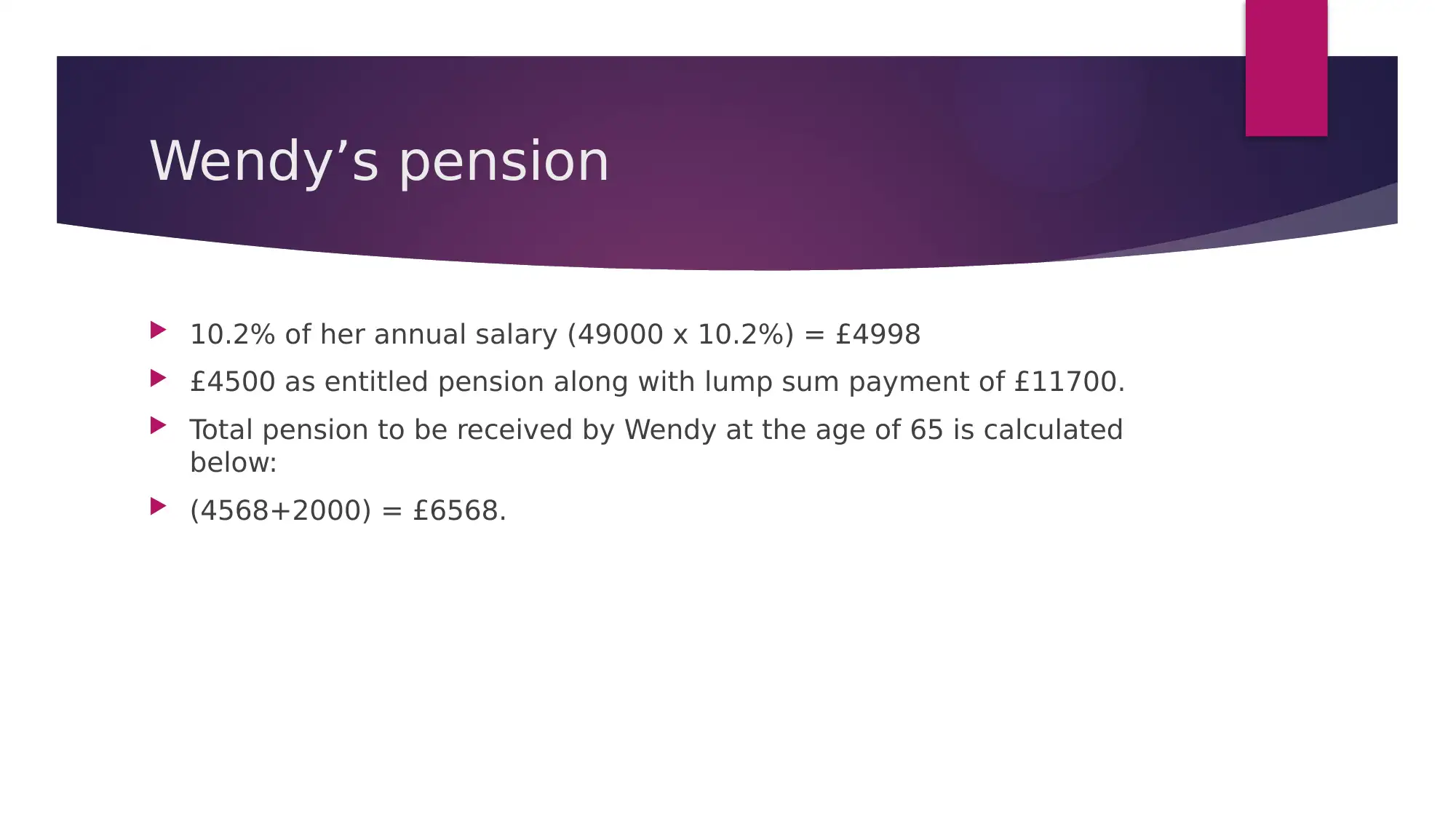

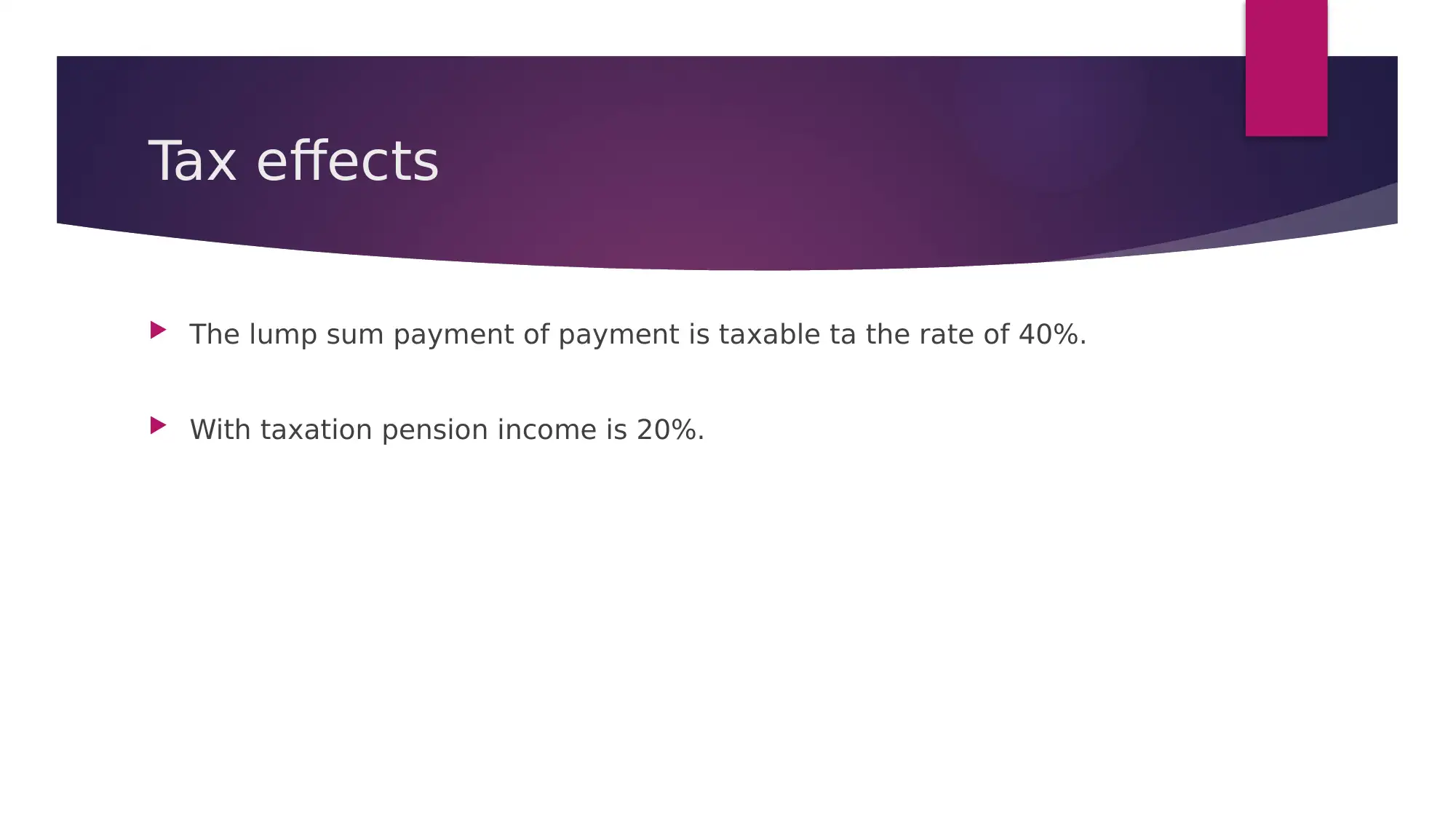

This financial plan addresses the retirement and investment needs of Alastair and Wendy Windsor, a couple nearing retirement. The report analyzes their current financial situation, including income, pensions from various sources, and existing assets. It explores suitable pension schemes, considering the 2014/15 pension reforms, and evaluates the tax implications of lump-sum payments and inheritance. The plan outlines investment options, such as government bonds and mutual funds, aligning with the couple's risk tolerance and financial objectives. Additionally, it provides mortgage advice to their son, Harry, and emphasizes the importance of will creation for estate planning. The report includes detailed calculations, assumptions, and references to support its recommendations, aiming to secure a stable financial future for Alastair and Wendy.

1 out of 24

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.