Financial Planning Report: Brendon McDougall's Financial Future

VerifiedAdded on 2022/11/13

|10

|1878

|194

Report

AI Summary

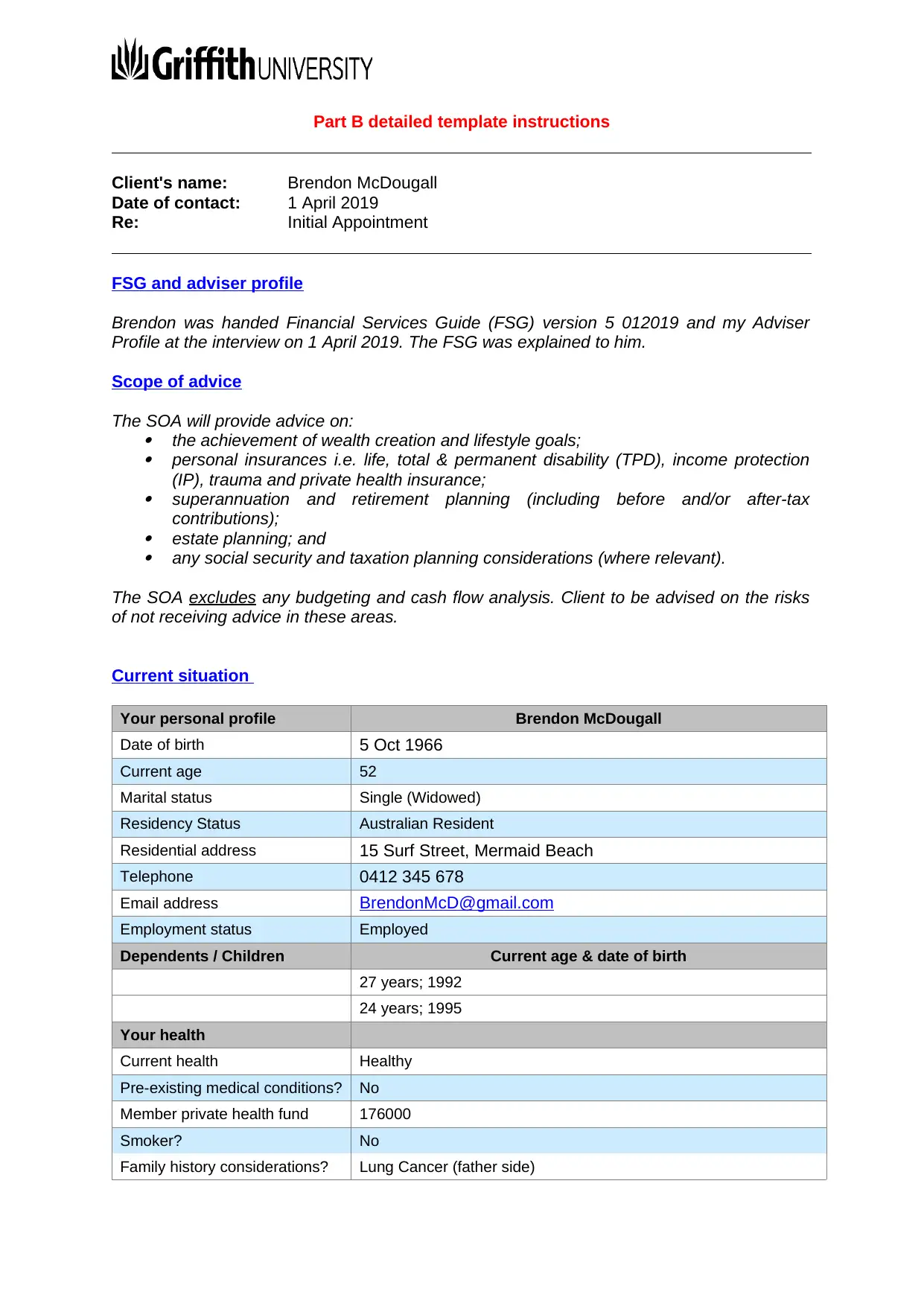

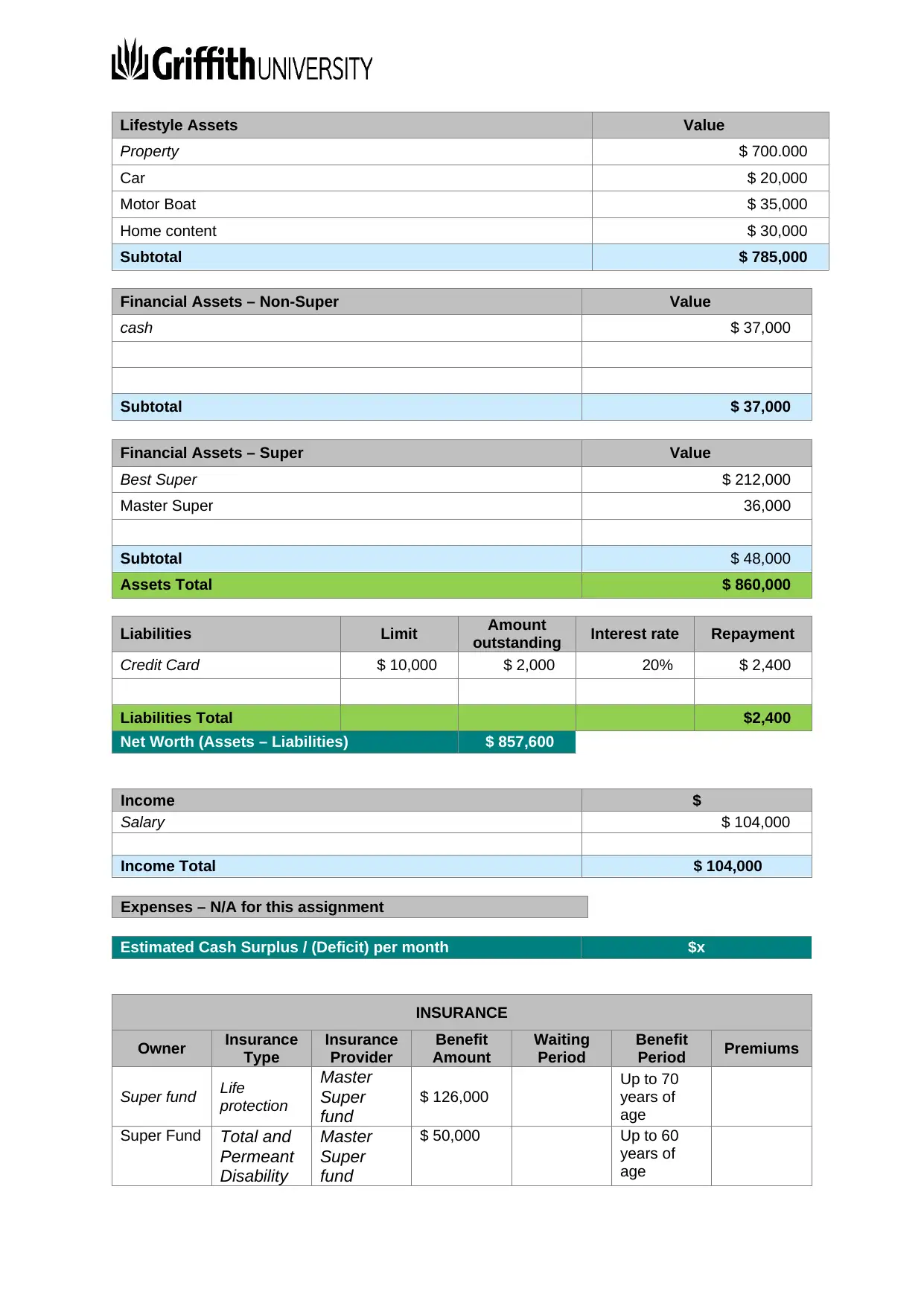

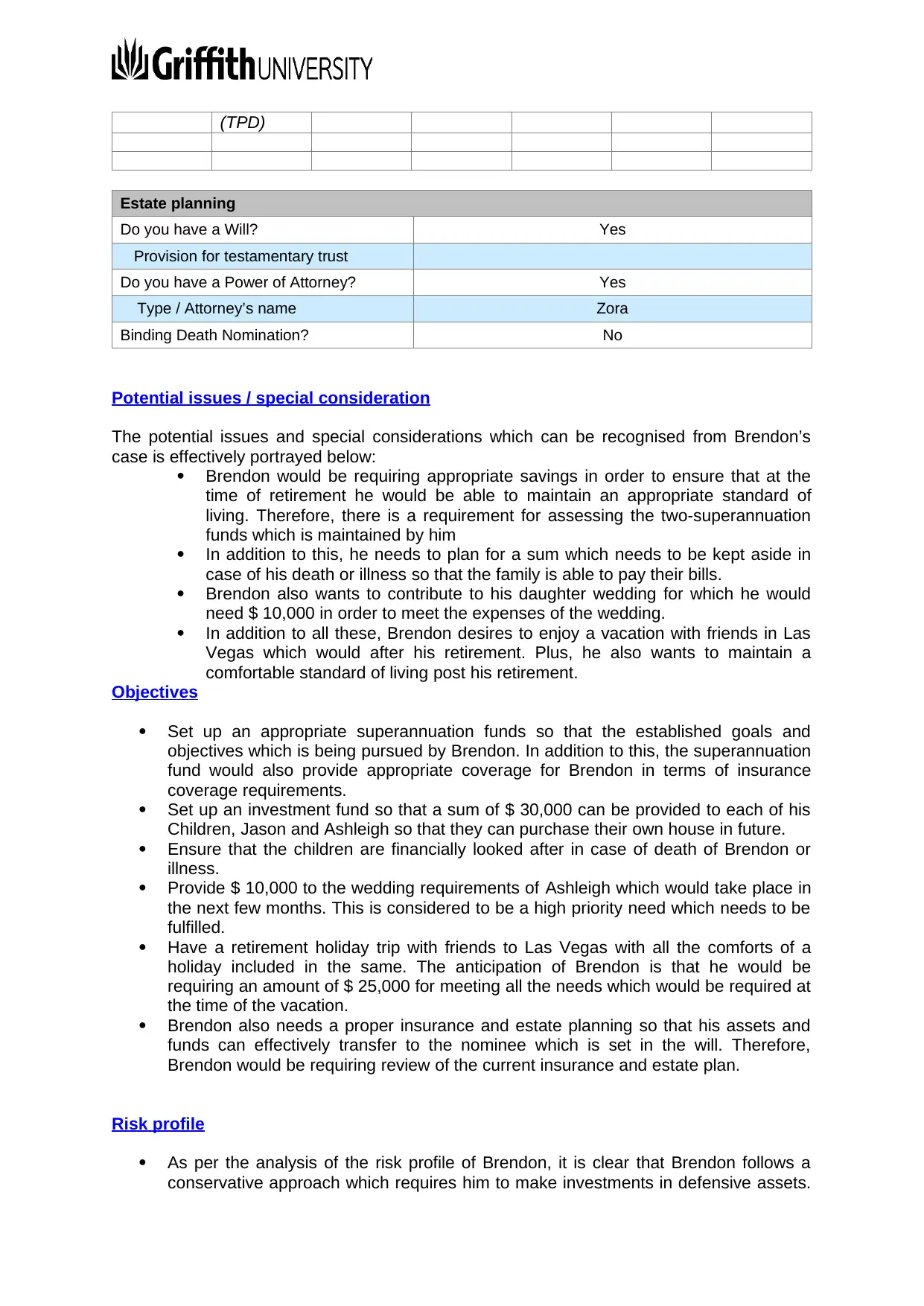

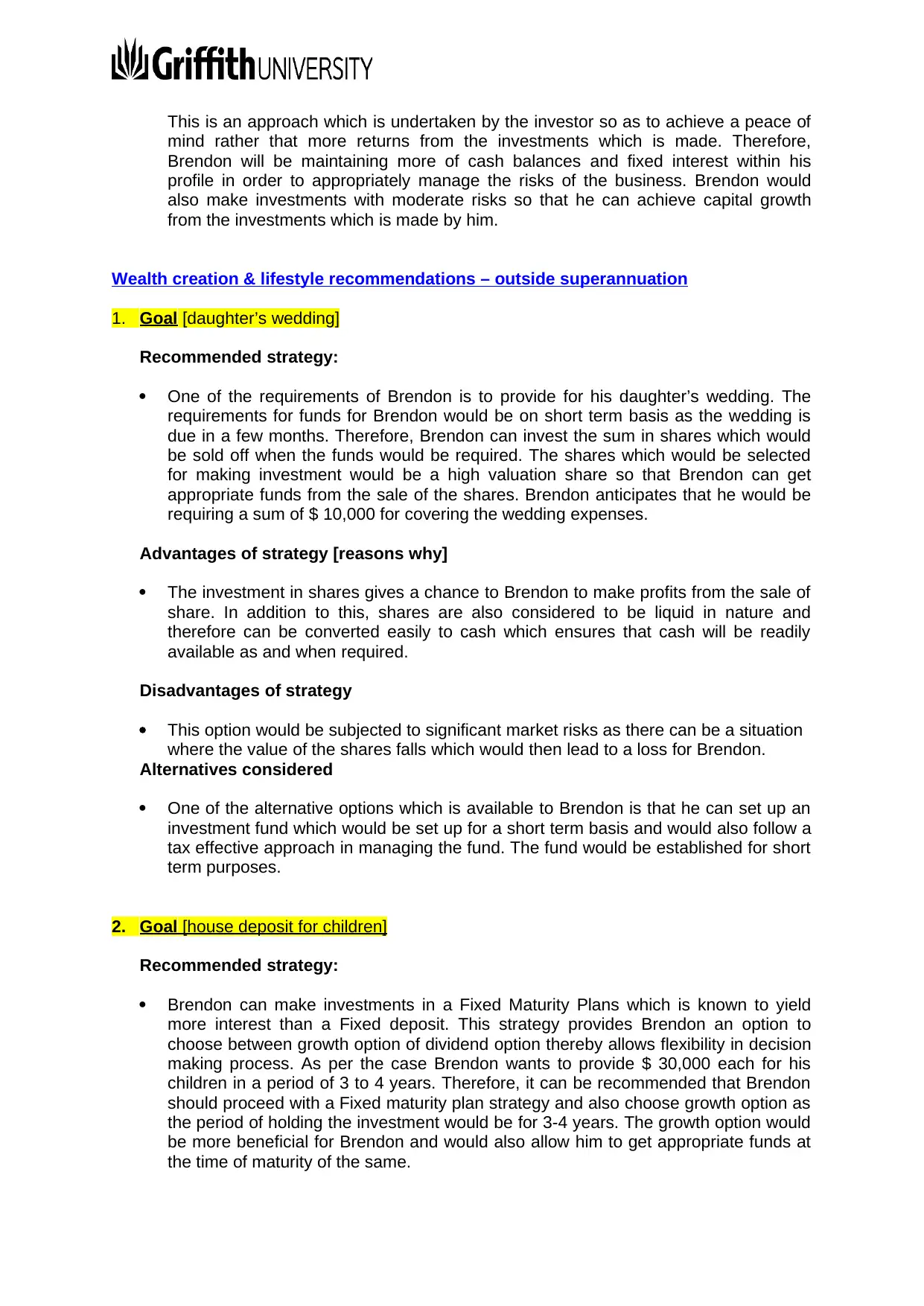

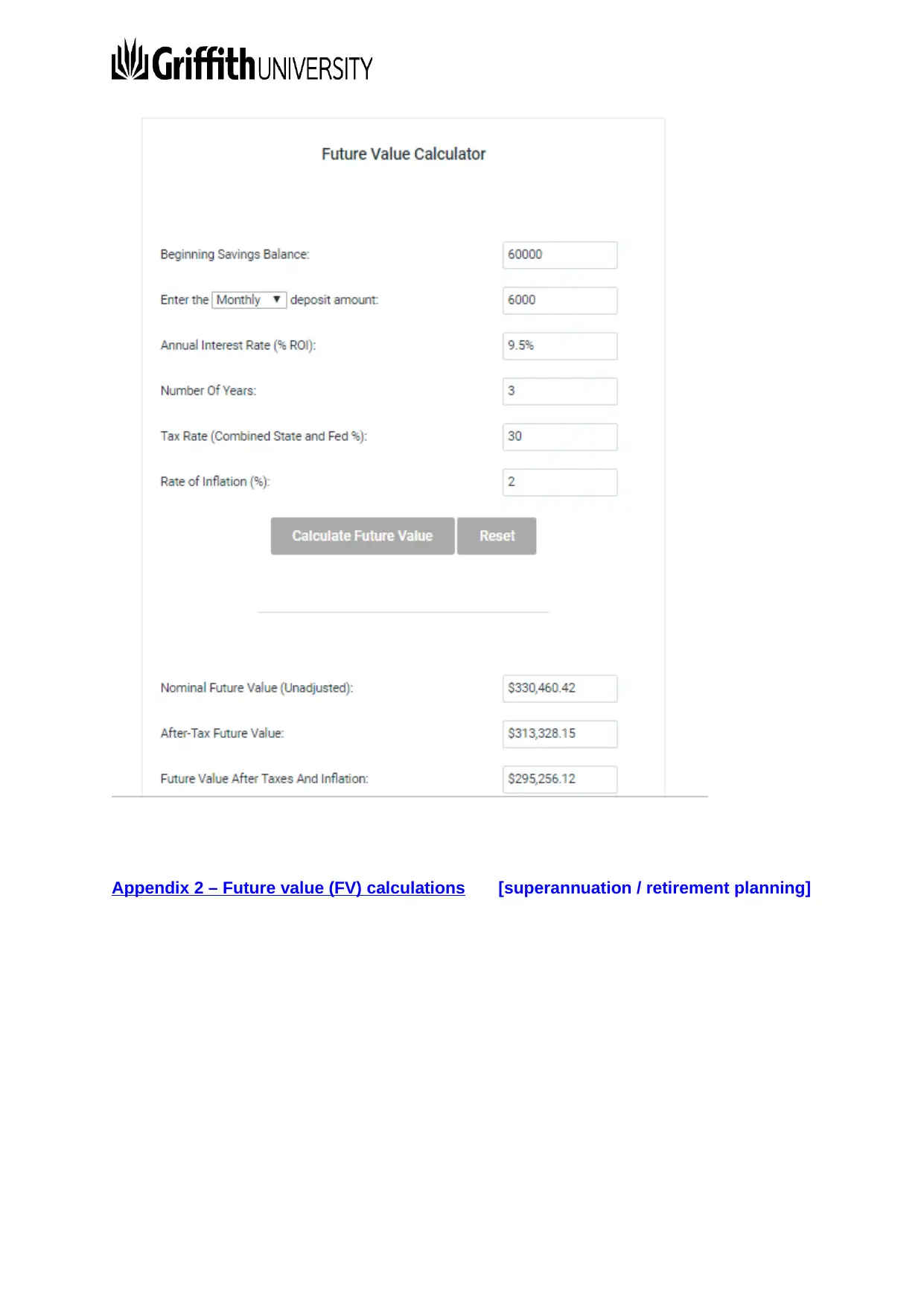

This report is a detailed financial plan for Brendon McDougall, a 52-year-old single (widowed) Australian resident. It outlines his current financial situation, including assets, liabilities, income, and existing insurance coverage. The report assesses his risk profile, which is conservative, and identifies his financial objectives: securing retirement, providing for his children's future home deposits, funding his daughter's wedding, planning a retirement holiday, and ensuring adequate insurance and estate planning. The recommendations include investment strategies for the daughter's wedding (shares), children's house deposits (Fixed Maturity Plans), and the retirement holiday (Bank Fixed deposits). It also suggests establishing a SMSF for superannuation and recommends specific insurance providers for life, TPD, income protection, trauma, and private health insurance. The report emphasizes the importance of estate planning and recommends formulating a will to ensure the appropriate transfer of assets. Appendices provide future value calculations for both outside and within superannuation investments.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.