Management Accounting Report: Planning and Financial Problem Solving

VerifiedAdded on 2020/11/12

|16

|3904

|366

Report

AI Summary

This report examines the application of management accounting principles within the context of Tech Ltd, a company involved in manufacturing and selling mobile chargers and electronic gadgets. The report begins by differentiating management accounting from financial accounting, highlighting its role in internal decision-making, and then delves into the importance of management accounting for effective business decisions, including forecasting, investment analysis, and make-or-buy decisions. It explores various management accounting systems such as cost accounting, inventory management, and job costing, detailing their advantages and disadvantages. The report also discusses the role of managerial reporting systems, including budget reports, job cost reports, receivable reports, and inventory reports, in facilitating informed decision-making. Furthermore, the report analyzes the use of absorption and marginal costing methods, demonstrating their impact on profit calculations and decision-making. It also presents the application of managerial accounting techniques in planning, including the use of different types of budgets, and their advantages and disadvantages. Finally, the report explains how managerial accounting tools can aid in responding to financial problems, offering a comprehensive overview of management accounting's role in achieving financial goals and optimal resource utilization.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

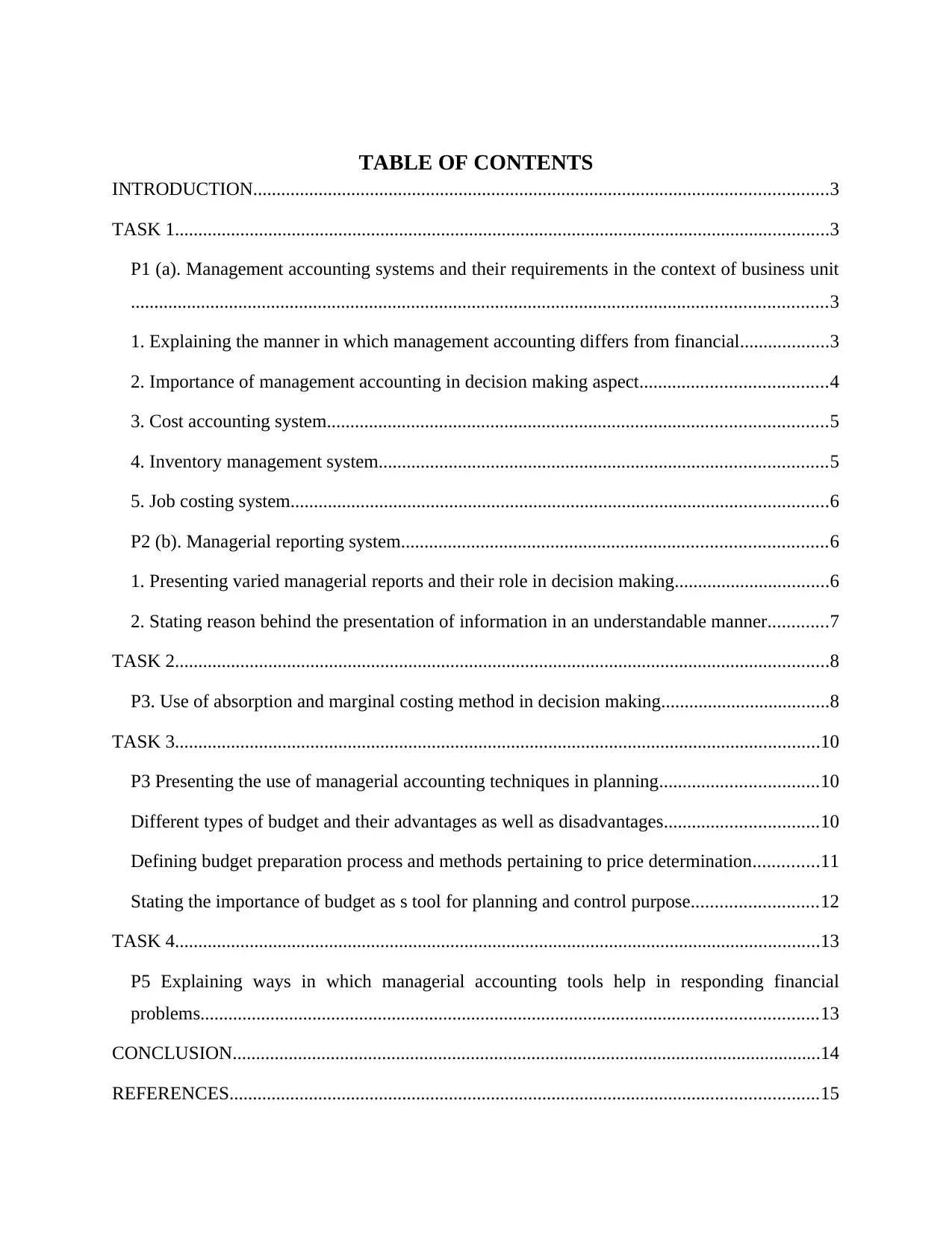

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 (a). Management accounting systems and their requirements in the context of business unit

.....................................................................................................................................................3

1. Explaining the manner in which management accounting differs from financial...................3

2. Importance of management accounting in decision making aspect........................................4

3. Cost accounting system...........................................................................................................5

4. Inventory management system................................................................................................5

5. Job costing system...................................................................................................................6

P2 (b). Managerial reporting system...........................................................................................6

1. Presenting varied managerial reports and their role in decision making.................................6

2. Stating reason behind the presentation of information in an understandable manner.............7

TASK 2............................................................................................................................................8

P3. Use of absorption and marginal costing method in decision making....................................8

TASK 3..........................................................................................................................................10

P3 Presenting the use of managerial accounting techniques in planning..................................10

Different types of budget and their advantages as well as disadvantages.................................10

Defining budget preparation process and methods pertaining to price determination..............11

Stating the importance of budget as s tool for planning and control purpose...........................12

TASK 4..........................................................................................................................................13

P5 Explaining ways in which managerial accounting tools help in responding financial

problems....................................................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 (a). Management accounting systems and their requirements in the context of business unit

.....................................................................................................................................................3

1. Explaining the manner in which management accounting differs from financial...................3

2. Importance of management accounting in decision making aspect........................................4

3. Cost accounting system...........................................................................................................5

4. Inventory management system................................................................................................5

5. Job costing system...................................................................................................................6

P2 (b). Managerial reporting system...........................................................................................6

1. Presenting varied managerial reports and their role in decision making.................................6

2. Stating reason behind the presentation of information in an understandable manner.............7

TASK 2............................................................................................................................................8

P3. Use of absorption and marginal costing method in decision making....................................8

TASK 3..........................................................................................................................................10

P3 Presenting the use of managerial accounting techniques in planning..................................10

Different types of budget and their advantages as well as disadvantages.................................10

Defining budget preparation process and methods pertaining to price determination..............11

Stating the importance of budget as s tool for planning and control purpose...........................12

TASK 4..........................................................................................................................................13

P5 Explaining ways in which managerial accounting tools help in responding financial

problems....................................................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

In the recent times, business units prefer to employ management accounting tool with the

motive to make optimum use of financial resources. Moreover, MA field of finance furnishes

information about cost and thereby helps in taking decision about future aspects. By using

management accounting techniques firm can do effectual financial planning which in turn makes

significant contribution in the attainment of goals. This report is based on the case scenario of

Tech Ltd which manufactures and offers mobile chargers as well as electronic gazettes to the

customers. In this, essential requirements of management accounting in the context of Tech Ltd

will be described. Further, report also depicts the role of managerial report indecision making.

Besides this, report will provide deeper insight about the use of marginal and absorption costing

in decision making. It also exhibits the manner in which MA techniques help in planning and

responding financial problems.

TASK 1

P1 (a). Management accounting systems and their requirements in the context of business unit

1. Explaining the manner in which management accounting differs from financial

Management accounting is the process of preparing managerial reports and accounts

which aid in the long & short decision making aspect of business organization. It lays high level

of emphasis on identifying, measuring, analyzing, interpreting and communication information

that contributes in the goal attainment (Mondal and Percival, 2010).

Management and financial accounting can be distinguished in the following manner:

Basis of difference Management accounting Financial accounting

Meaning It focuses on providing

managers with suitable

information about internal

operations so they become able

FA is concerned with the

recording of business

transactions and providing

stakeholders with the

In the recent times, business units prefer to employ management accounting tool with the

motive to make optimum use of financial resources. Moreover, MA field of finance furnishes

information about cost and thereby helps in taking decision about future aspects. By using

management accounting techniques firm can do effectual financial planning which in turn makes

significant contribution in the attainment of goals. This report is based on the case scenario of

Tech Ltd which manufactures and offers mobile chargers as well as electronic gazettes to the

customers. In this, essential requirements of management accounting in the context of Tech Ltd

will be described. Further, report also depicts the role of managerial report indecision making.

Besides this, report will provide deeper insight about the use of marginal and absorption costing

in decision making. It also exhibits the manner in which MA techniques help in planning and

responding financial problems.

TASK 1

P1 (a). Management accounting systems and their requirements in the context of business unit

1. Explaining the manner in which management accounting differs from financial

Management accounting is the process of preparing managerial reports and accounts

which aid in the long & short decision making aspect of business organization. It lays high level

of emphasis on identifying, measuring, analyzing, interpreting and communication information

that contributes in the goal attainment (Mondal and Percival, 2010).

Management and financial accounting can be distinguished in the following manner:

Basis of difference Management accounting Financial accounting

Meaning It focuses on providing

managers with suitable

information about internal

operations so they become able

FA is concerned with the

recording of business

transactions and providing

stakeholders with the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to take prominent decisions. framework for decision

making.

Use Give input to the internal

management team for taking

decision about budget etc.

Enables both internal and

external stakeholders in

analyzing the financial

performance of firm (Financial

Accounting vs. Management

Accounting, 2018).

Form of reporting In this, no prescribed or specific

format is following for

reporting purpose.

Financial reports are prepared

by taking into account

standardized format.

Frequency or time duration As per the requirements of

management team managerial

reports are prepared.

On statutory basis, financial

accounting report are drafted

and presented on annually and

semi-annually basis.

Statutory compliance No Yes or mandatory

Rules Under MA, no need to follow

specific rules while preparing

reports

IFRS, GAAP, IAS

2. Importance of management accounting in decision making aspect

Manager of Tech Ltd can take suitable business decisions considering management

accounting aspects about following matters:

Management team can make proper forecast about future aspects. Such field of finance

enables manager in deciding whether more funds should be invested in equipments or

not.

It facilitates appropriate decision making at both strategic and operational level. Tech

Ltd’s manager can assess whether firm should purchase product from third party or

manufacture them in house (Lukka and Modell, 2010). Thus, management accounting

tools help company in taking the most important decision pertaining to make or buy.

Variance analysis technique of management accounting enables manager to build on

positive results and make efforts to manage the negative aspects.

making.

Use Give input to the internal

management team for taking

decision about budget etc.

Enables both internal and

external stakeholders in

analyzing the financial

performance of firm (Financial

Accounting vs. Management

Accounting, 2018).

Form of reporting In this, no prescribed or specific

format is following for

reporting purpose.

Financial reports are prepared

by taking into account

standardized format.

Frequency or time duration As per the requirements of

management team managerial

reports are prepared.

On statutory basis, financial

accounting report are drafted

and presented on annually and

semi-annually basis.

Statutory compliance No Yes or mandatory

Rules Under MA, no need to follow

specific rules while preparing

reports

IFRS, GAAP, IAS

2. Importance of management accounting in decision making aspect

Manager of Tech Ltd can take suitable business decisions considering management

accounting aspects about following matters:

Management team can make proper forecast about future aspects. Such field of finance

enables manager in deciding whether more funds should be invested in equipments or

not.

It facilitates appropriate decision making at both strategic and operational level. Tech

Ltd’s manager can assess whether firm should purchase product from third party or

manufacture them in house (Lukka and Modell, 2010). Thus, management accounting

tools help company in taking the most important decision pertaining to make or buy.

Variance analysis technique of management accounting enables manager to build on

positive results and make efforts to manage the negative aspects.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Facilitates appropriate forecasting of cash flows through budgeting and helps in making

suitable estimation about the rate of return.

3. Cost accounting system

Management team of Tech Ltd can capture or assess the cost of production by using cost

accounting system. It lays focus on recording input cost associated with each step of production.

Cost accounting system offers opportunity in relation to doing comparison of actual performance

in against to the budgeted figures (Modell, 2010). Hence, by assessing deviations or variances

firm would become able to take corrective measure for improvement within the suitable time

frame.

Advantages

CA system enables management team of Tech Ltd to detect loss and assess reason

behind the same

Provides assistance in formulating future production policies

Gives input for setting suitable prices of the products or services offered

Disadvantages

Aspects regarding under or over overhead absorption leads problem

In the case of partial capacity utilization, such system is not considered as useful

This system presents past information, whereas management is taking decision about

future

4. Inventory management system

By employing inventory management tool manager of Tech ltd can maintain suitable stock

and thereby would become able to carry out operations without any difficulty. Through

undertaking economic quantity method Tech Ltd can decide the level to which they need o

maintain raw material within the business unit. This in turn helps in making control on ordering

and holding cost (Baldvinsdottir, Mitchell and Nørreklit, 2010). Further, FIFO method is highly

effectual which contributes in effective stock management and reduces risk level associated with

the introduction or use of new technological aspects.

Advantages Disadvantages

suitable estimation about the rate of return.

3. Cost accounting system

Management team of Tech Ltd can capture or assess the cost of production by using cost

accounting system. It lays focus on recording input cost associated with each step of production.

Cost accounting system offers opportunity in relation to doing comparison of actual performance

in against to the budgeted figures (Modell, 2010). Hence, by assessing deviations or variances

firm would become able to take corrective measure for improvement within the suitable time

frame.

Advantages

CA system enables management team of Tech Ltd to detect loss and assess reason

behind the same

Provides assistance in formulating future production policies

Gives input for setting suitable prices of the products or services offered

Disadvantages

Aspects regarding under or over overhead absorption leads problem

In the case of partial capacity utilization, such system is not considered as useful

This system presents past information, whereas management is taking decision about

future

4. Inventory management system

By employing inventory management tool manager of Tech ltd can maintain suitable stock

and thereby would become able to carry out operations without any difficulty. Through

undertaking economic quantity method Tech Ltd can decide the level to which they need o

maintain raw material within the business unit. This in turn helps in making control on ordering

and holding cost (Baldvinsdottir, Mitchell and Nørreklit, 2010). Further, FIFO method is highly

effectual which contributes in effective stock management and reduces risk level associated with

the introduction or use of new technological aspects.

Advantages Disadvantages

Leads cost reduction

Maximizes profit level

Avoids bottlenecks in the production

activities

For determining optimal inventory

level or value manager has to devote

more time.

Training needs to be organized for

developing familiarity of personnel

regarding inventory software.

5. Job costing system

This system assists business unit in allocating manufacturing product to an individual or

batches of products. By using this, Tech Ltd can assess cost of material, labour as well as

overhead and thereby would become able to identify cost per unit (What is Job Costing?, 2018).

Considering unit cost such manufacturing firm can set suitable prices of the products or services

offered.

Advantages Disadvantages

High flexible and provides assistance

in calculating indirect cost

Offers opportunity in relation to

making assessment of expenses

incurred

Enables to assign cost to the

individual product and thereby helps

in assessing profit margin

It includes more clerical work in

relations to the recording of business

transactions.

Includes measurement difficulties

Maximizes profit level

Avoids bottlenecks in the production

activities

For determining optimal inventory

level or value manager has to devote

more time.

Training needs to be organized for

developing familiarity of personnel

regarding inventory software.

5. Job costing system

This system assists business unit in allocating manufacturing product to an individual or

batches of products. By using this, Tech Ltd can assess cost of material, labour as well as

overhead and thereby would become able to identify cost per unit (What is Job Costing?, 2018).

Considering unit cost such manufacturing firm can set suitable prices of the products or services

offered.

Advantages Disadvantages

High flexible and provides assistance

in calculating indirect cost

Offers opportunity in relation to

making assessment of expenses

incurred

Enables to assign cost to the

individual product and thereby helps

in assessing profit margin

It includes more clerical work in

relations to the recording of business

transactions.

Includes measurement difficulties

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

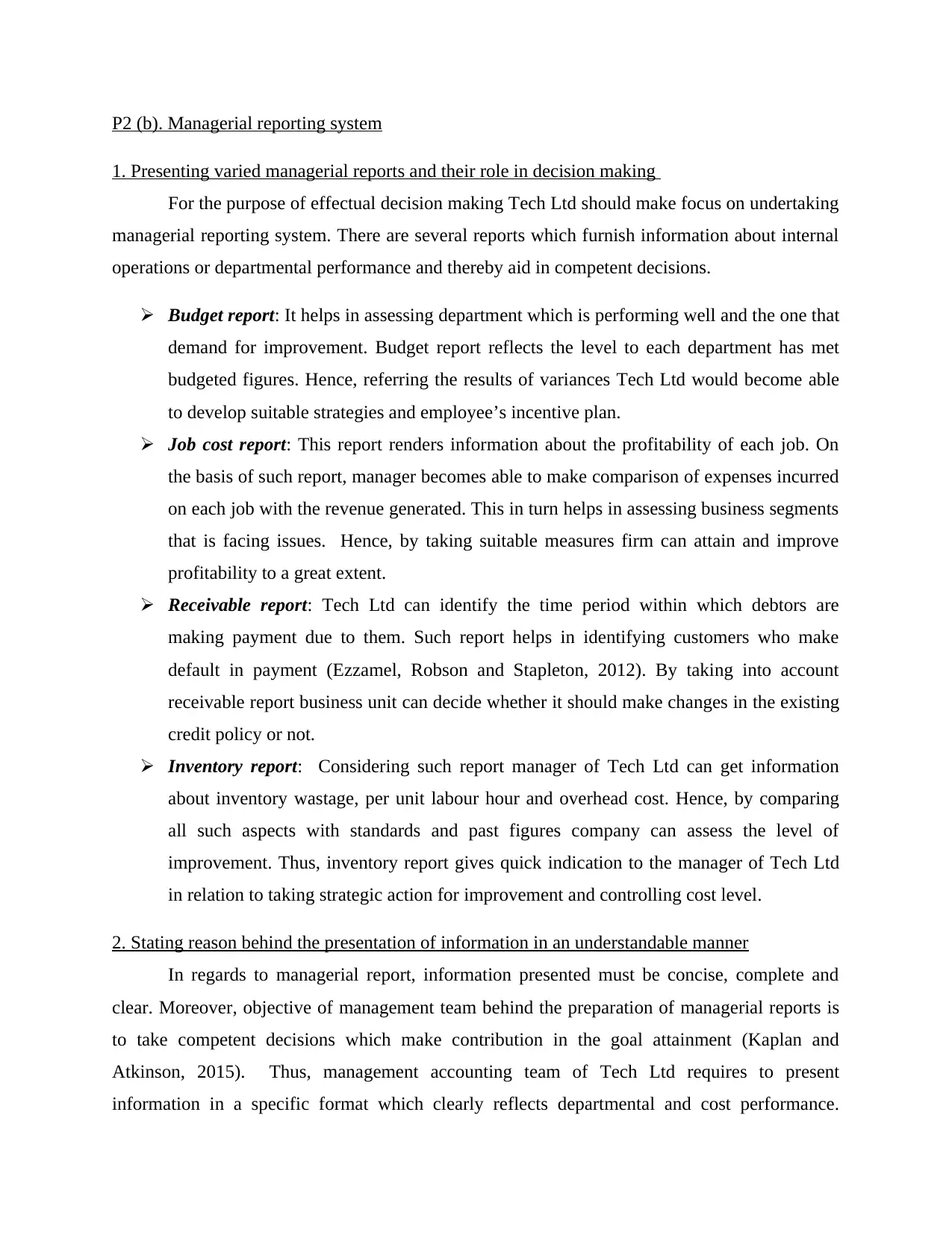

P2 (b). Managerial reporting system

1. Presenting varied managerial reports and their role in decision making

For the purpose of effectual decision making Tech Ltd should make focus on undertaking

managerial reporting system. There are several reports which furnish information about internal

operations or departmental performance and thereby aid in competent decisions.

Budget report: It helps in assessing department which is performing well and the one that

demand for improvement. Budget report reflects the level to each department has met

budgeted figures. Hence, referring the results of variances Tech Ltd would become able

to develop suitable strategies and employee’s incentive plan.

Job cost report: This report renders information about the profitability of each job. On

the basis of such report, manager becomes able to make comparison of expenses incurred

on each job with the revenue generated. This in turn helps in assessing business segments

that is facing issues. Hence, by taking suitable measures firm can attain and improve

profitability to a great extent.

Receivable report: Tech Ltd can identify the time period within which debtors are

making payment due to them. Such report helps in identifying customers who make

default in payment (Ezzamel, Robson and Stapleton, 2012). By taking into account

receivable report business unit can decide whether it should make changes in the existing

credit policy or not.

Inventory report: Considering such report manager of Tech Ltd can get information

about inventory wastage, per unit labour hour and overhead cost. Hence, by comparing

all such aspects with standards and past figures company can assess the level of

improvement. Thus, inventory report gives quick indication to the manager of Tech Ltd

in relation to taking strategic action for improvement and controlling cost level.

2. Stating reason behind the presentation of information in an understandable manner

In regards to managerial report, information presented must be concise, complete and

clear. Moreover, objective of management team behind the preparation of managerial reports is

to take competent decisions which make contribution in the goal attainment (Kaplan and

Atkinson, 2015). Thus, management accounting team of Tech Ltd requires to present

information in a specific format which clearly reflects departmental and cost performance.

1. Presenting varied managerial reports and their role in decision making

For the purpose of effectual decision making Tech Ltd should make focus on undertaking

managerial reporting system. There are several reports which furnish information about internal

operations or departmental performance and thereby aid in competent decisions.

Budget report: It helps in assessing department which is performing well and the one that

demand for improvement. Budget report reflects the level to each department has met

budgeted figures. Hence, referring the results of variances Tech Ltd would become able

to develop suitable strategies and employee’s incentive plan.

Job cost report: This report renders information about the profitability of each job. On

the basis of such report, manager becomes able to make comparison of expenses incurred

on each job with the revenue generated. This in turn helps in assessing business segments

that is facing issues. Hence, by taking suitable measures firm can attain and improve

profitability to a great extent.

Receivable report: Tech Ltd can identify the time period within which debtors are

making payment due to them. Such report helps in identifying customers who make

default in payment (Ezzamel, Robson and Stapleton, 2012). By taking into account

receivable report business unit can decide whether it should make changes in the existing

credit policy or not.

Inventory report: Considering such report manager of Tech Ltd can get information

about inventory wastage, per unit labour hour and overhead cost. Hence, by comparing

all such aspects with standards and past figures company can assess the level of

improvement. Thus, inventory report gives quick indication to the manager of Tech Ltd

in relation to taking strategic action for improvement and controlling cost level.

2. Stating reason behind the presentation of information in an understandable manner

In regards to managerial report, information presented must be concise, complete and

clear. Moreover, objective of management team behind the preparation of managerial reports is

to take competent decisions which make contribution in the goal attainment (Kaplan and

Atkinson, 2015). Thus, management accounting team of Tech Ltd requires to present

information in a specific format which clearly reflects departmental and cost performance.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Hence, emphasis should be placed on presenting information systematically rather than

haphazardly.

TASK 2

P3. Use of absorption and marginal costing method in decision making

Marginal costing: It may be served as a decision making technique which assists in

ascertaining or assessing the total cost of production. Under this costing method, variable cost is

recognized as product cost, whereas fixed terns as periodical (Nawaz, 2013). In this, PV ratio

presents profitability associated with the operations.

Profitability statement as per marginal costing

Particulars

Figures

(in £)

Figures

(in £)

Turnover 52500

Less: Variable expenses

Direct labour 10000

Material 16000

Variable production overhead 4000

Less: Ending inventory 7500 22500

Contribution (sales – variable cost) 30000

Variable selling & dist expenses (52500 * 15%) 7875

Net contribution 22125

Less fixed cost:

Fixed Production Overhead 15000

Fixed Selling, dist and administration expenses 10000 25000

Net loss -2875

Absorption costing: In this, total cost of production is determined through the means of

expenses apportionment as per respective centre. This is also known as full costing method

because it considers both fixed and variable expenses for the assessment of manufacturing cost

(Absorption Costing, 2018). It presents cost data in a conventional way and helps in highlighting

net profit per unit.

haphazardly.

TASK 2

P3. Use of absorption and marginal costing method in decision making

Marginal costing: It may be served as a decision making technique which assists in

ascertaining or assessing the total cost of production. Under this costing method, variable cost is

recognized as product cost, whereas fixed terns as periodical (Nawaz, 2013). In this, PV ratio

presents profitability associated with the operations.

Profitability statement as per marginal costing

Particulars

Figures

(in £)

Figures

(in £)

Turnover 52500

Less: Variable expenses

Direct labour 10000

Material 16000

Variable production overhead 4000

Less: Ending inventory 7500 22500

Contribution (sales – variable cost) 30000

Variable selling & dist expenses (52500 * 15%) 7875

Net contribution 22125

Less fixed cost:

Fixed Production Overhead 15000

Fixed Selling, dist and administration expenses 10000 25000

Net loss -2875

Absorption costing: In this, total cost of production is determined through the means of

expenses apportionment as per respective centre. This is also known as full costing method

because it considers both fixed and variable expenses for the assessment of manufacturing cost

(Absorption Costing, 2018). It presents cost data in a conventional way and helps in highlighting

net profit per unit.

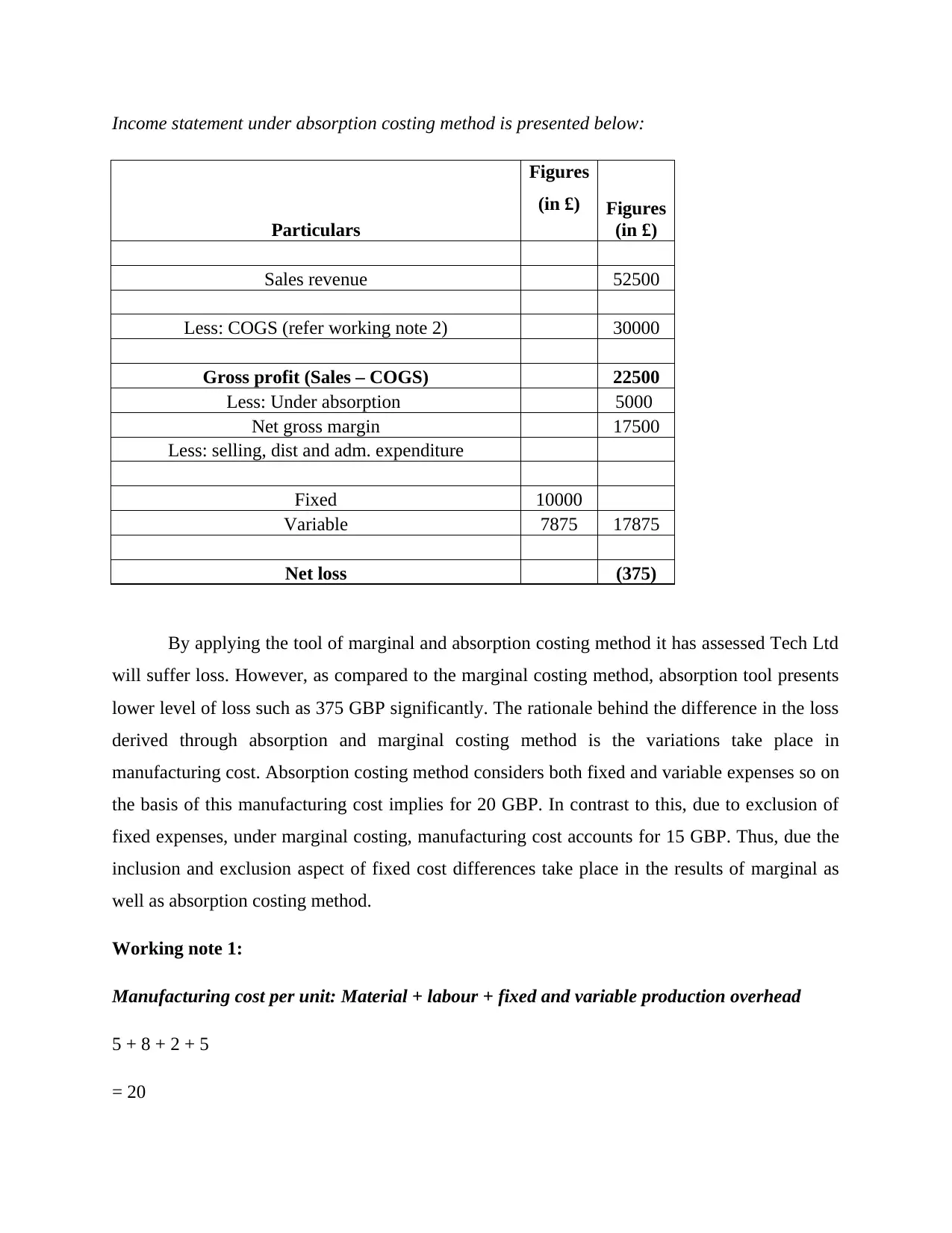

Income statement under absorption costing method is presented below:

Particulars

Figures

(in £) Figures

(in £)

Sales revenue 52500

Less: COGS (refer working note 2) 30000

Gross profit (Sales – COGS) 22500

Less: Under absorption 5000

Net gross margin 17500

Less: selling, dist and adm. expenditure

Fixed 10000

Variable 7875 17875

Net loss (375)

By applying the tool of marginal and absorption costing method it has assessed Tech Ltd

will suffer loss. However, as compared to the marginal costing method, absorption tool presents

lower level of loss such as 375 GBP significantly. The rationale behind the difference in the loss

derived through absorption and marginal costing method is the variations take place in

manufacturing cost. Absorption costing method considers both fixed and variable expenses so on

the basis of this manufacturing cost implies for 20 GBP. In contrast to this, due to exclusion of

fixed expenses, under marginal costing, manufacturing cost accounts for 15 GBP. Thus, due the

inclusion and exclusion aspect of fixed cost differences take place in the results of marginal as

well as absorption costing method.

Working note 1:

Manufacturing cost per unit: Material + labour + fixed and variable production overhead

5 + 8 + 2 + 5

= 20

Particulars

Figures

(in £) Figures

(in £)

Sales revenue 52500

Less: COGS (refer working note 2) 30000

Gross profit (Sales – COGS) 22500

Less: Under absorption 5000

Net gross margin 17500

Less: selling, dist and adm. expenditure

Fixed 10000

Variable 7875 17875

Net loss (375)

By applying the tool of marginal and absorption costing method it has assessed Tech Ltd

will suffer loss. However, as compared to the marginal costing method, absorption tool presents

lower level of loss such as 375 GBP significantly. The rationale behind the difference in the loss

derived through absorption and marginal costing method is the variations take place in

manufacturing cost. Absorption costing method considers both fixed and variable expenses so on

the basis of this manufacturing cost implies for 20 GBP. In contrast to this, due to exclusion of

fixed expenses, under marginal costing, manufacturing cost accounts for 15 GBP. Thus, due the

inclusion and exclusion aspect of fixed cost differences take place in the results of marginal as

well as absorption costing method.

Working note 1:

Manufacturing cost per unit: Material + labour + fixed and variable production overhead

5 + 8 + 2 + 5

= 20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

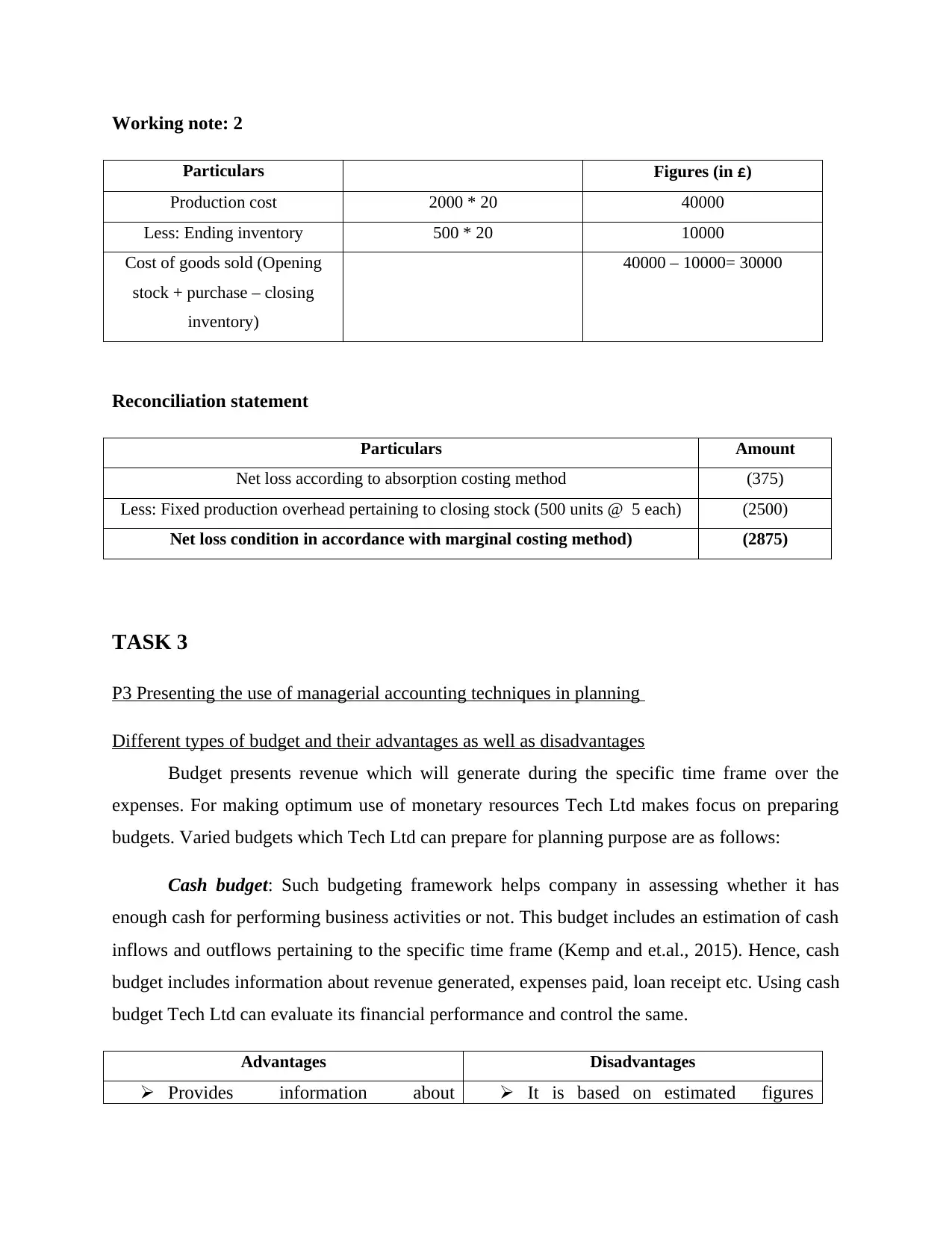

Working note: 2

Particulars Figures (in £)

Production cost 2000 * 20 40000

Less: Ending inventory 500 * 20 10000

Cost of goods sold (Opening

stock + purchase – closing

inventory)

40000 – 10000= 30000

Reconciliation statement

Particulars Amount

Net loss according to absorption costing method (375)

Less: Fixed production overhead pertaining to closing stock (500 units @ 5 each) (2500)

Net loss condition in accordance with marginal costing method) (2875)

TASK 3

P3 Presenting the use of managerial accounting techniques in planning

Different types of budget and their advantages as well as disadvantages

Budget presents revenue which will generate during the specific time frame over the

expenses. For making optimum use of monetary resources Tech Ltd makes focus on preparing

budgets. Varied budgets which Tech Ltd can prepare for planning purpose are as follows:

Cash budget: Such budgeting framework helps company in assessing whether it has

enough cash for performing business activities or not. This budget includes an estimation of cash

inflows and outflows pertaining to the specific time frame (Kemp and et.al., 2015). Hence, cash

budget includes information about revenue generated, expenses paid, loan receipt etc. Using cash

budget Tech Ltd can evaluate its financial performance and control the same.

Advantages Disadvantages

Provides information about It is based on estimated figures

Particulars Figures (in £)

Production cost 2000 * 20 40000

Less: Ending inventory 500 * 20 10000

Cost of goods sold (Opening

stock + purchase – closing

inventory)

40000 – 10000= 30000

Reconciliation statement

Particulars Amount

Net loss according to absorption costing method (375)

Less: Fixed production overhead pertaining to closing stock (500 units @ 5 each) (2500)

Net loss condition in accordance with marginal costing method) (2875)

TASK 3

P3 Presenting the use of managerial accounting techniques in planning

Different types of budget and their advantages as well as disadvantages

Budget presents revenue which will generate during the specific time frame over the

expenses. For making optimum use of monetary resources Tech Ltd makes focus on preparing

budgets. Varied budgets which Tech Ltd can prepare for planning purpose are as follows:

Cash budget: Such budgeting framework helps company in assessing whether it has

enough cash for performing business activities or not. This budget includes an estimation of cash

inflows and outflows pertaining to the specific time frame (Kemp and et.al., 2015). Hence, cash

budget includes information about revenue generated, expenses paid, loan receipt etc. Using cash

budget Tech Ltd can evaluate its financial performance and control the same.

Advantages Disadvantages

Provides information about It is based on estimated figures

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company’s cash position

Helps in identifying the amount of

cash needed for fulfilling short term

obligations without overdraft

which in turn limits its significance

level

Lack of flexibility

Includes manipulation

Capital expenses budget: This financial plan presents amount and time when fixed assets

will be purchased by the business unit. Capital expenditure budget provides high level of

assistance in organizing activities for the upcoming time period.

Advantages Disadvantages

Ensures appropriate planning

Facilitates appropriate investments on

time

Time intensive activity

Static budget: This budgeting framework remains same at each level of activity or output.

In other words, such budget is not affected from the changes take place in the number of

production units (Drury, 2013).

Advantages Disadvantages

Facilitates prioritization of activities

No need to update on continuous

basis

Helps in performing budgetary

control

Inflexibility

Static budget does not facilitate

allocation of additional resources

Defining budget preparation process and methods pertaining to price determination

By using below mentioned process manager of Tech Ltd can draft suitable budgeting

framework such as:

Assessment of cash inflow and outflow by taking into account activities which need to be

performed during the specific time frame.

Helps in identifying the amount of

cash needed for fulfilling short term

obligations without overdraft

which in turn limits its significance

level

Lack of flexibility

Includes manipulation

Capital expenses budget: This financial plan presents amount and time when fixed assets

will be purchased by the business unit. Capital expenditure budget provides high level of

assistance in organizing activities for the upcoming time period.

Advantages Disadvantages

Ensures appropriate planning

Facilitates appropriate investments on

time

Time intensive activity

Static budget: This budgeting framework remains same at each level of activity or output.

In other words, such budget is not affected from the changes take place in the number of

production units (Drury, 2013).

Advantages Disadvantages

Facilitates prioritization of activities

No need to update on continuous

basis

Helps in performing budgetary

control

Inflexibility

Static budget does not facilitate

allocation of additional resources

Defining budget preparation process and methods pertaining to price determination

By using below mentioned process manager of Tech Ltd can draft suitable budgeting

framework such as:

Assessment of cash inflow and outflow by taking into account activities which need to be

performed during the specific time frame.

In the next stage, manager also takes input from the managers of each department for

developing appropriate plan

Presenting financial estimation to the budget committee for getting approval

Circulating final budget at all respective or concerned department

Execution of budget

Matching actual income and expenses with the budgeted figures

Assessing deviations and taking measures for performance enhancement

Price can be determined by Tech Ltd through doing demand and supply analysis. In the

case of more demand and low supply firm can set high prices of the offerings. Further, by

making evaluation of competitors policy manager of the business unit determine the prices of its

own offerings (Ellul and et.al., 2015). In addition to this, by adding margin, which firm wishes to

attain, in per unit cost company can set appropriate prices of the mobile chargers and electronic

gazettes offered by it.

Stating the importance of budget as s tool for planning and control purpose

Significance of budget as a planning and controlling tool can be presented in the

following manner:

Budget provides manager with the standards and helps in comparing the same with actual

financial performance. Through this, Tech Ltd can assess the extent to which budgeted

figures are met. Budget or budgetary control tools offer opportunity to the manager to

identify reasons take place behind deviations. Hence, considering deviations firm can

take corrective measure on time and thereby becomes able to improve or control

performance.

In addition to this, deviations assessed through budgetary control help in setting suitable

standards for the upcoming time period (Otley and Emmanuel, 2013). By taking into

account reasons take place behind deficiency Tech Ltd can set realistic and achievable

budgeting plan.

Thus, by taking into account above depicted aspects it can be mentioned that Tech Ltd can

develop suitable financial plan and control performance by taking into account budgeting or

budgetary control tool.

developing appropriate plan

Presenting financial estimation to the budget committee for getting approval

Circulating final budget at all respective or concerned department

Execution of budget

Matching actual income and expenses with the budgeted figures

Assessing deviations and taking measures for performance enhancement

Price can be determined by Tech Ltd through doing demand and supply analysis. In the

case of more demand and low supply firm can set high prices of the offerings. Further, by

making evaluation of competitors policy manager of the business unit determine the prices of its

own offerings (Ellul and et.al., 2015). In addition to this, by adding margin, which firm wishes to

attain, in per unit cost company can set appropriate prices of the mobile chargers and electronic

gazettes offered by it.

Stating the importance of budget as s tool for planning and control purpose

Significance of budget as a planning and controlling tool can be presented in the

following manner:

Budget provides manager with the standards and helps in comparing the same with actual

financial performance. Through this, Tech Ltd can assess the extent to which budgeted

figures are met. Budget or budgetary control tools offer opportunity to the manager to

identify reasons take place behind deviations. Hence, considering deviations firm can

take corrective measure on time and thereby becomes able to improve or control

performance.

In addition to this, deviations assessed through budgetary control help in setting suitable

standards for the upcoming time period (Otley and Emmanuel, 2013). By taking into

account reasons take place behind deficiency Tech Ltd can set realistic and achievable

budgeting plan.

Thus, by taking into account above depicted aspects it can be mentioned that Tech Ltd can

develop suitable financial plan and control performance by taking into account budgeting or

budgetary control tool.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.