FNSFPL502 & FNSFPL508: Complex Financial Planning Research - Case

VerifiedAdded on 2023/04/19

|50

|11396

|430

Case Study

AI Summary

This assignment presents a financial planning research report based on a case study involving clients Dennis and Donna Barker. The study evaluates their current financial situation, including income, expenses, assets, and liabilities. It identifies key issues and objectives related to cash flow management, tax minimization, wealth creation through superannuation and investments, debt reduction, and wealth protection via insurance and estate planning. The research involves analyzing the integrity of client-provided information, calculating investment income, superannuation contributions, and surplus income after tax. Client objectives are quantified in present value terms and verified for viability. The assessment includes reviewing relevant documents such as pay slips, tax returns, bank statements, and insurance policies to ensure the accuracy of the financial data used for planning.

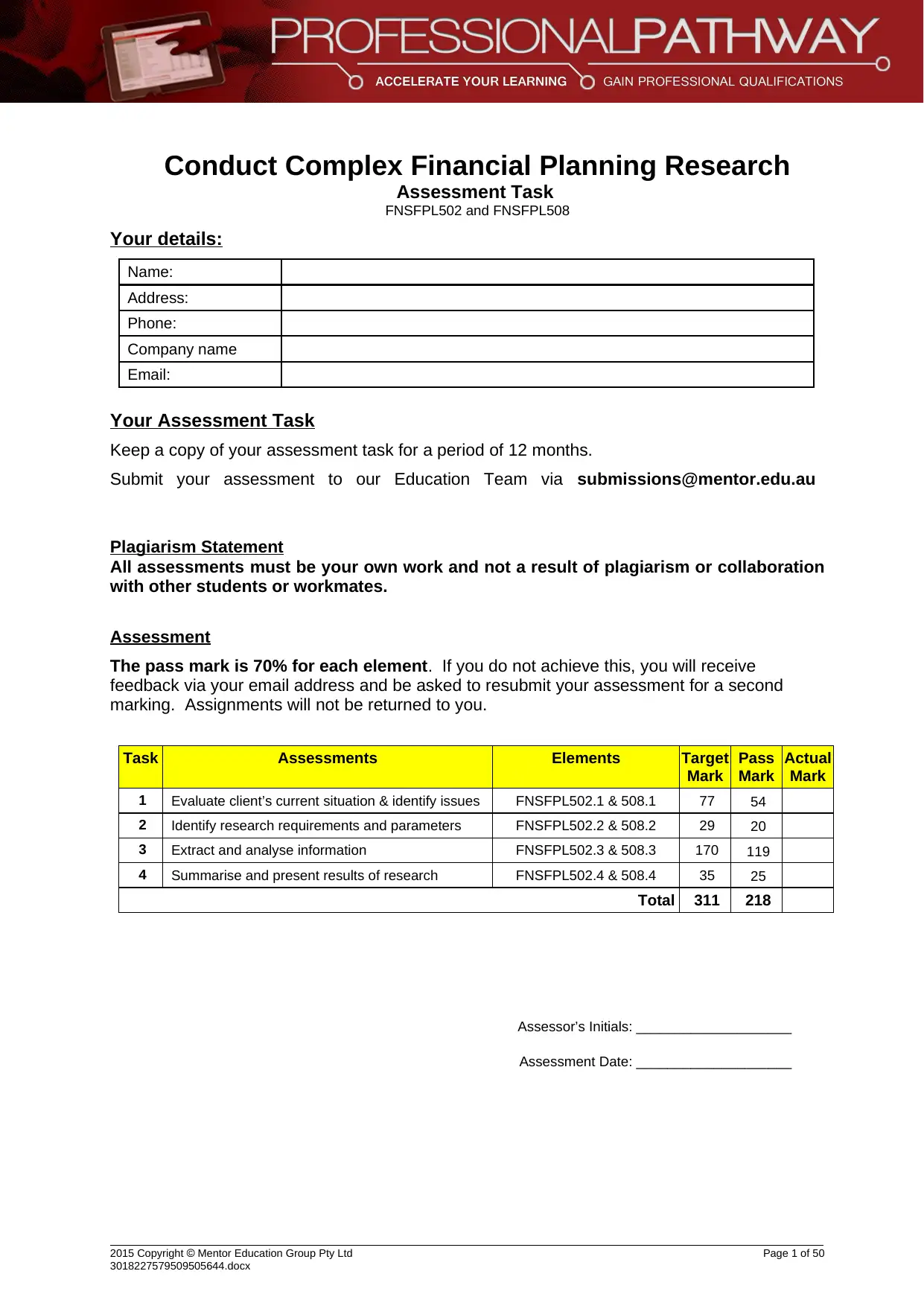

Conduct Complex Financial Planning Research

Assessment Task

FNSFPL502 and FNSFPL508

Your details:

Name:

Address:

Phone:

Company name

Email:

Your Assessment Task

Keep a copy of your assessment task for a period of 12 months.

Submit your assessment to our Education Team via submissions@mentor.edu.au

Plagiarism Statement

All assessments must be your own work and not a result of plagiarism or collaboration

with other students or workmates.

Assessment

The pass mark is 70% for each element. If you do not achieve this, you will receive

feedback via your email address and be asked to resubmit your assessment for a second

marking. Assignments will not be returned to you.

Task Assessments Elements Target

Mark

Pass

Mark

Actual

Mark

1 Evaluate client’s current situation & identify issues FNSFPL502.1 & 508.1 77 54

2 Identify research requirements and parameters FNSFPL502.2 & 508.2 29 20

3 Extract and analyse information FNSFPL502.3 & 508.3 170 119

4 Summarise and present results of research FNSFPL502.4 & 508.4 35 25

Total 311 218

Assessor’s Initials: ____________________

Assessment Date: ____________________

2015 Copyright Mentor Education Group Pty Ltd Page 1 of 50

3018227579509505644.docx

Assessment Task

FNSFPL502 and FNSFPL508

Your details:

Name:

Address:

Phone:

Company name

Email:

Your Assessment Task

Keep a copy of your assessment task for a period of 12 months.

Submit your assessment to our Education Team via submissions@mentor.edu.au

Plagiarism Statement

All assessments must be your own work and not a result of plagiarism or collaboration

with other students or workmates.

Assessment

The pass mark is 70% for each element. If you do not achieve this, you will receive

feedback via your email address and be asked to resubmit your assessment for a second

marking. Assignments will not be returned to you.

Task Assessments Elements Target

Mark

Pass

Mark

Actual

Mark

1 Evaluate client’s current situation & identify issues FNSFPL502.1 & 508.1 77 54

2 Identify research requirements and parameters FNSFPL502.2 & 508.2 29 20

3 Extract and analyse information FNSFPL502.3 & 508.3 170 119

4 Summarise and present results of research FNSFPL502.4 & 508.4 35 25

Total 311 218

Assessor’s Initials: ____________________

Assessment Date: ____________________

2015 Copyright Mentor Education Group Pty Ltd Page 1 of 50

3018227579509505644.docx

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction

Objective The objective of this first assessment is to develop a Research Report for

the practical client situation described in the case study assigned to you.

Scope To achieve this objective, you will need to:

Evaluate client’s current situation and identify issues,

Identify research requirements and parameters,

Extract and analyse information, and

Summarise and present results of research.

The assessment tasks in this assessment will allow you to demonstrate

your knowledge and skills in these elements

Assessment

process

Start by:

1. Reading the Assessment Task and case study.

2. Type your answers to the assessment tasks into this template

document (hand-written answers are not accepted)

3. Submit your completed document by emailing it to

submissions@mentor.edu.au

Don’t forget to keep a copy and retain it for 12 months

Need help? If you have any questions, please email the Mentor Support Team at

service@mentor.edu.au

Related

Assessments

When you have completed all written assessment tasks in this program of

study (Statement of Advice series), you will then need to undertake one

other related assessment:

Skills Assessment (telephone simulation) to assess your

communication and interpersonal skills in relation to presenting your

research findings to the financial planner. FNSFPL508A.4.4

This assessment will be conducted together with the presentation

requirements in relation to preparing a financial plan, FNSFPL503A

implementation FNSFPL504A and ongoing service FNSFPL505A

Units of

competency

Upon successful completion of these assessments, you will be awarded

two units of competency for:

1. FNSFPL502: Conduct financial planning analysis and research,

and

2. FNSFPL508: Conduct complex financial planning research.

Copyright Mentor Education Group Pty Ltd Page 2 of 50

3018227579509505644.docx

Objective The objective of this first assessment is to develop a Research Report for

the practical client situation described in the case study assigned to you.

Scope To achieve this objective, you will need to:

Evaluate client’s current situation and identify issues,

Identify research requirements and parameters,

Extract and analyse information, and

Summarise and present results of research.

The assessment tasks in this assessment will allow you to demonstrate

your knowledge and skills in these elements

Assessment

process

Start by:

1. Reading the Assessment Task and case study.

2. Type your answers to the assessment tasks into this template

document (hand-written answers are not accepted)

3. Submit your completed document by emailing it to

submissions@mentor.edu.au

Don’t forget to keep a copy and retain it for 12 months

Need help? If you have any questions, please email the Mentor Support Team at

service@mentor.edu.au

Related

Assessments

When you have completed all written assessment tasks in this program of

study (Statement of Advice series), you will then need to undertake one

other related assessment:

Skills Assessment (telephone simulation) to assess your

communication and interpersonal skills in relation to presenting your

research findings to the financial planner. FNSFPL508A.4.4

This assessment will be conducted together with the presentation

requirements in relation to preparing a financial plan, FNSFPL503A

implementation FNSFPL504A and ongoing service FNSFPL505A

Units of

competency

Upon successful completion of these assessments, you will be awarded

two units of competency for:

1. FNSFPL502: Conduct financial planning analysis and research,

and

2. FNSFPL508: Conduct complex financial planning research.

Copyright Mentor Education Group Pty Ltd Page 2 of 50

3018227579509505644.docx

Assessment Task 1

1.0 Evaluate

the client's

current

situation and

identify the

issues

FNSFPLN502.1

FNSFPL508.1

The first assessment involves the evaluation of the case study allocated

to you, to assess the client's current situation and identify the issues.

This requires that you:

undertake an analysis of the integrity of information provided by the

client,

identify and quantify the client objectives and expectations and test

them for viability, and

establish the basis for strategy development based on confirmed

objectives.

For this activity, refer to the case study and complete your answers to

these assessment tasks in the space provided in the following pages.

Marks / 77

Copyright Mentor Education Group Pty Ltd Page 3 of 50

3018227579509505644.docx

1.0 Evaluate

the client's

current

situation and

identify the

issues

FNSFPLN502.1

FNSFPL508.1

The first assessment involves the evaluation of the case study allocated

to you, to assess the client's current situation and identify the issues.

This requires that you:

undertake an analysis of the integrity of information provided by the

client,

identify and quantify the client objectives and expectations and test

them for viability, and

establish the basis for strategy development based on confirmed

objectives.

For this activity, refer to the case study and complete your answers to

these assessment tasks in the space provided in the following pages.

Marks / 77

Copyright Mentor Education Group Pty Ltd Page 3 of 50

3018227579509505644.docx

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

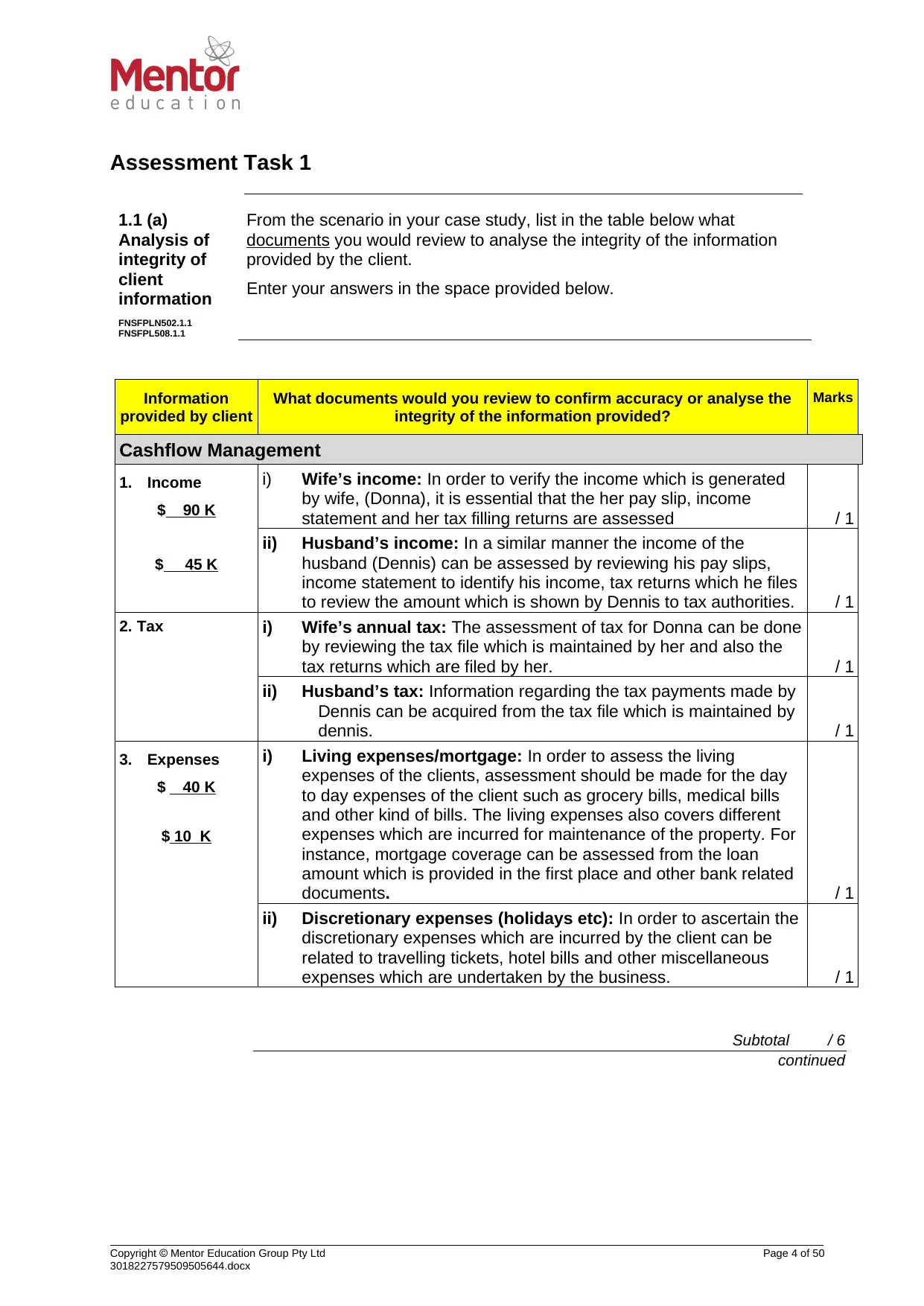

Assessment Task 1

1.1 (a)

Analysis of

integrity of

client

information

FNSFPLN502.1.1

FNSFPL508.1.1

From the scenario in your case study, list in the table below what

documents you would review to analyse the integrity of the information

provided by the client.

Enter your answers in the space provided below.

Information

provided by client

What documents would you review to confirm accuracy or analyse the

integrity of the information provided?

Marks

Cashflow Management

1. Income

$ 90 K

$ 45 K

i) Wife’s income: In order to verify the income which is generated

by wife, (Donna), it is essential that the her pay slip, income

statement and her tax filling returns are assessed / 1

ii) Husband’s income: In a similar manner the income of the

husband (Dennis) can be assessed by reviewing his pay slips,

income statement to identify his income, tax returns which he files

to review the amount which is shown by Dennis to tax authorities. / 1

2. Tax i) Wife’s annual tax: The assessment of tax for Donna can be done

by reviewing the tax file which is maintained by her and also the

tax returns which are filed by her. / 1

ii) Husband’s tax: Information regarding the tax payments made by

Dennis can be acquired from the tax file which is maintained by

dennis. / 1

3. Expenses

$ 40 K

$ 10 K

i) Living expenses/mortgage: In order to assess the living

expenses of the clients, assessment should be made for the day

to day expenses of the client such as grocery bills, medical bills

and other kind of bills. The living expenses also covers different

expenses which are incurred for maintenance of the property. For

instance, mortgage coverage can be assessed from the loan

amount which is provided in the first place and other bank related

documents. / 1

ii) Discretionary expenses (holidays etc): In order to ascertain the

discretionary expenses which are incurred by the client can be

related to travelling tickets, hotel bills and other miscellaneous

expenses which are undertaken by the business. / 1

Subtotal / 6

continued

Copyright Mentor Education Group Pty Ltd Page 4 of 50

3018227579509505644.docx

1.1 (a)

Analysis of

integrity of

client

information

FNSFPLN502.1.1

FNSFPL508.1.1

From the scenario in your case study, list in the table below what

documents you would review to analyse the integrity of the information

provided by the client.

Enter your answers in the space provided below.

Information

provided by client

What documents would you review to confirm accuracy or analyse the

integrity of the information provided?

Marks

Cashflow Management

1. Income

$ 90 K

$ 45 K

i) Wife’s income: In order to verify the income which is generated

by wife, (Donna), it is essential that the her pay slip, income

statement and her tax filling returns are assessed / 1

ii) Husband’s income: In a similar manner the income of the

husband (Dennis) can be assessed by reviewing his pay slips,

income statement to identify his income, tax returns which he files

to review the amount which is shown by Dennis to tax authorities. / 1

2. Tax i) Wife’s annual tax: The assessment of tax for Donna can be done

by reviewing the tax file which is maintained by her and also the

tax returns which are filed by her. / 1

ii) Husband’s tax: Information regarding the tax payments made by

Dennis can be acquired from the tax file which is maintained by

dennis. / 1

3. Expenses

$ 40 K

$ 10 K

i) Living expenses/mortgage: In order to assess the living

expenses of the clients, assessment should be made for the day

to day expenses of the client such as grocery bills, medical bills

and other kind of bills. The living expenses also covers different

expenses which are incurred for maintenance of the property. For

instance, mortgage coverage can be assessed from the loan

amount which is provided in the first place and other bank related

documents. / 1

ii) Discretionary expenses (holidays etc): In order to ascertain the

discretionary expenses which are incurred by the client can be

related to travelling tickets, hotel bills and other miscellaneous

expenses which are undertaken by the business. / 1

Subtotal / 6

continued

Copyright Mentor Education Group Pty Ltd Page 4 of 50

3018227579509505644.docx

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

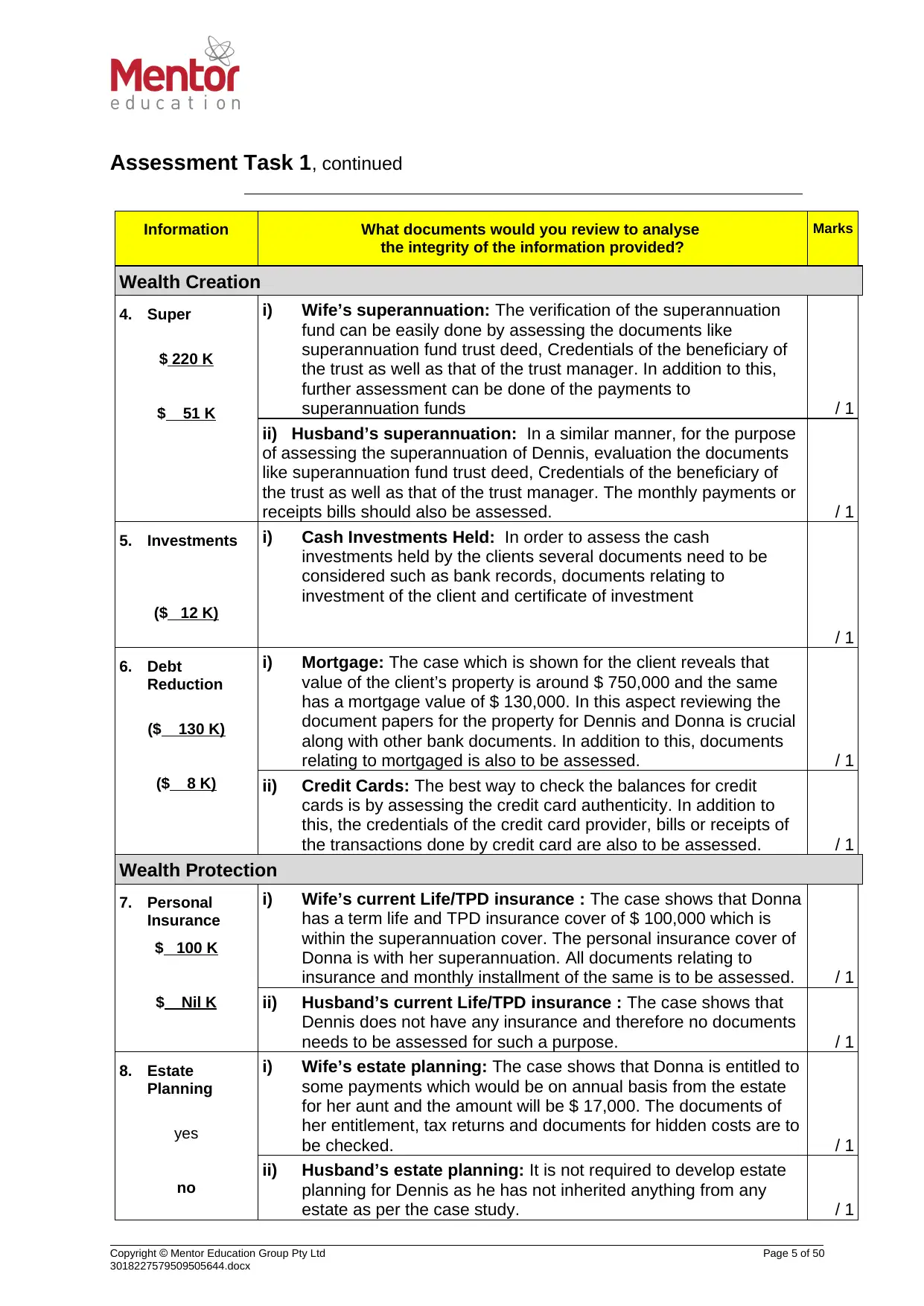

Assessment Task 1, continued

Information What documents would you review to analyse

the integrity of the information provided?

Marks

Wealth Creation

4. Super

$ 220 K

$ 51 K

i) Wife’s superannuation: The verification of the superannuation

fund can be easily done by assessing the documents like

superannuation fund trust deed, Credentials of the beneficiary of

the trust as well as that of the trust manager. In addition to this,

further assessment can be done of the payments to

superannuation funds / 1

ii) Husband’s superannuation: In a similar manner, for the purpose

of assessing the superannuation of Dennis, evaluation the documents

like superannuation fund trust deed, Credentials of the beneficiary of

the trust as well as that of the trust manager. The monthly payments or

receipts bills should also be assessed. / 1

5. Investments

($ 12 K)

i) Cash Investments Held: In order to assess the cash

investments held by the clients several documents need to be

considered such as bank records, documents relating to

investment of the client and certificate of investment

/ 1

6. Debt

Reduction

($ 130 K)

($ 8 K)

i) Mortgage: The case which is shown for the client reveals that

value of the client’s property is around $ 750,000 and the same

has a mortgage value of $ 130,000. In this aspect reviewing the

document papers for the property for Dennis and Donna is crucial

along with other bank documents. In addition to this, documents

relating to mortgaged is also to be assessed. / 1

ii) Credit Cards: The best way to check the balances for credit

cards is by assessing the credit card authenticity. In addition to

this, the credentials of the credit card provider, bills or receipts of

the transactions done by credit card are also to be assessed. / 1

Wealth Protection

7. Personal

Insurance

$ 100 K

$ Nil K

i) Wife’s current Life/TPD insurance : The case shows that Donna

has a term life and TPD insurance cover of $ 100,000 which is

within the superannuation cover. The personal insurance cover of

Donna is with her superannuation. All documents relating to

insurance and monthly installment of the same is to be assessed. / 1

ii) Husband’s current Life/TPD insurance : The case shows that

Dennis does not have any insurance and therefore no documents

needs to be assessed for such a purpose. / 1

8. Estate

Planning

yes

no

i) Wife’s estate planning: The case shows that Donna is entitled to

some payments which would be on annual basis from the estate

for her aunt and the amount will be $ 17,000. The documents of

her entitlement, tax returns and documents for hidden costs are to

be checked. / 1

ii) Husband’s estate planning: It is not required to develop estate

planning for Dennis as he has not inherited anything from any

estate as per the case study. / 1

Copyright Mentor Education Group Pty Ltd Page 5 of 50

3018227579509505644.docx

Information What documents would you review to analyse

the integrity of the information provided?

Marks

Wealth Creation

4. Super

$ 220 K

$ 51 K

i) Wife’s superannuation: The verification of the superannuation

fund can be easily done by assessing the documents like

superannuation fund trust deed, Credentials of the beneficiary of

the trust as well as that of the trust manager. In addition to this,

further assessment can be done of the payments to

superannuation funds / 1

ii) Husband’s superannuation: In a similar manner, for the purpose

of assessing the superannuation of Dennis, evaluation the documents

like superannuation fund trust deed, Credentials of the beneficiary of

the trust as well as that of the trust manager. The monthly payments or

receipts bills should also be assessed. / 1

5. Investments

($ 12 K)

i) Cash Investments Held: In order to assess the cash

investments held by the clients several documents need to be

considered such as bank records, documents relating to

investment of the client and certificate of investment

/ 1

6. Debt

Reduction

($ 130 K)

($ 8 K)

i) Mortgage: The case which is shown for the client reveals that

value of the client’s property is around $ 750,000 and the same

has a mortgage value of $ 130,000. In this aspect reviewing the

document papers for the property for Dennis and Donna is crucial

along with other bank documents. In addition to this, documents

relating to mortgaged is also to be assessed. / 1

ii) Credit Cards: The best way to check the balances for credit

cards is by assessing the credit card authenticity. In addition to

this, the credentials of the credit card provider, bills or receipts of

the transactions done by credit card are also to be assessed. / 1

Wealth Protection

7. Personal

Insurance

$ 100 K

$ Nil K

i) Wife’s current Life/TPD insurance : The case shows that Donna

has a term life and TPD insurance cover of $ 100,000 which is

within the superannuation cover. The personal insurance cover of

Donna is with her superannuation. All documents relating to

insurance and monthly installment of the same is to be assessed. / 1

ii) Husband’s current Life/TPD insurance : The case shows that

Dennis does not have any insurance and therefore no documents

needs to be assessed for such a purpose. / 1

8. Estate

Planning

yes

no

i) Wife’s estate planning: The case shows that Donna is entitled to

some payments which would be on annual basis from the estate

for her aunt and the amount will be $ 17,000. The documents of

her entitlement, tax returns and documents for hidden costs are to

be checked. / 1

ii) Husband’s estate planning: It is not required to develop estate

planning for Dennis as he has not inherited anything from any

estate as per the case study. / 1

Copyright Mentor Education Group Pty Ltd Page 5 of 50

3018227579509505644.docx

/9

continued

Copyright Mentor Education Group Pty Ltd Page 6 of 50

3018227579509505644.docx

continued

Copyright Mentor Education Group Pty Ltd Page 6 of 50

3018227579509505644.docx

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

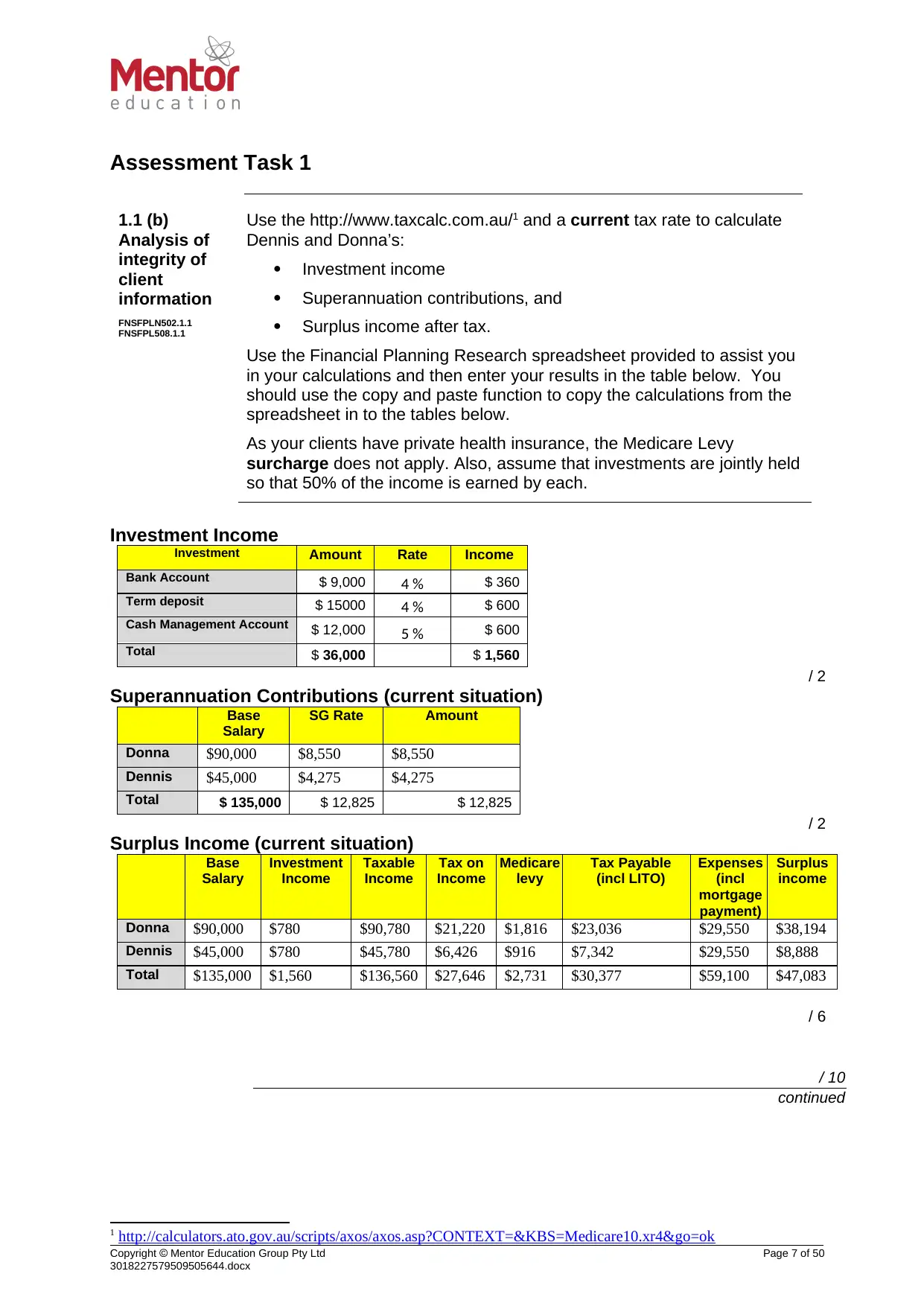

Assessment Task 1

1.1 (b)

Analysis of

integrity of

client

information

FNSFPLN502.1.1

FNSFPL508.1.1

Use the http://www.taxcalc.com.au/1 and a current tax rate to calculate

Dennis and Donna’s:

Investment income

Superannuation contributions, and

Surplus income after tax.

Use the Financial Planning Research spreadsheet provided to assist you

in your calculations and then enter your results in the table below. You

should use the copy and paste function to copy the calculations from the

spreadsheet in to the tables below.

As your clients have private health insurance, the Medicare Levy

surcharge does not apply. Also, assume that investments are jointly held

so that 50% of the income is earned by each.

Investment Income

Investment Amount Rate Income

Bank Account $ 9,000 4 % $ 360

Term deposit $ 15000 4 % $ 600

Cash Management Account $ 12,000 5 % $ 600

Total $ 36,000 $ 1,560

/ 2

Superannuation Contributions (current situation)

Base

Salary

SG Rate Amount

Donna $90,000 $8,550 $8,550

Dennis $45,000 $4,275 $4,275

Total $ 135,000 $ 12,825 $ 12,825

/ 2

Surplus Income (current situation)

Base

Salary

Investment

Income

Taxable

Income

Tax on

Income

Medicare

levy

Tax Payable

(incl LITO)

Expenses

(incl

mortgage

payment)

Surplus

income

Donna $90,000 $780 $90,780 $21,220 $1,816 $23,036 $29,550 $38,194

Dennis $45,000 $780 $45,780 $6,426 $916 $7,342 $29,550 $8,888

Total $135,000 $1,560 $136,560 $27,646 $2,731 $30,377 $59,100 $47,083

/ 6

/ 10

continued

1 http://calculators.ato.gov.au/scripts/axos/axos.asp?CONTEXT=&KBS=Medicare10.xr4&go=ok

Copyright Mentor Education Group Pty Ltd Page 7 of 50

3018227579509505644.docx

1.1 (b)

Analysis of

integrity of

client

information

FNSFPLN502.1.1

FNSFPL508.1.1

Use the http://www.taxcalc.com.au/1 and a current tax rate to calculate

Dennis and Donna’s:

Investment income

Superannuation contributions, and

Surplus income after tax.

Use the Financial Planning Research spreadsheet provided to assist you

in your calculations and then enter your results in the table below. You

should use the copy and paste function to copy the calculations from the

spreadsheet in to the tables below.

As your clients have private health insurance, the Medicare Levy

surcharge does not apply. Also, assume that investments are jointly held

so that 50% of the income is earned by each.

Investment Income

Investment Amount Rate Income

Bank Account $ 9,000 4 % $ 360

Term deposit $ 15000 4 % $ 600

Cash Management Account $ 12,000 5 % $ 600

Total $ 36,000 $ 1,560

/ 2

Superannuation Contributions (current situation)

Base

Salary

SG Rate Amount

Donna $90,000 $8,550 $8,550

Dennis $45,000 $4,275 $4,275

Total $ 135,000 $ 12,825 $ 12,825

/ 2

Surplus Income (current situation)

Base

Salary

Investment

Income

Taxable

Income

Tax on

Income

Medicare

levy

Tax Payable

(incl LITO)

Expenses

(incl

mortgage

payment)

Surplus

income

Donna $90,000 $780 $90,780 $21,220 $1,816 $23,036 $29,550 $38,194

Dennis $45,000 $780 $45,780 $6,426 $916 $7,342 $29,550 $8,888

Total $135,000 $1,560 $136,560 $27,646 $2,731 $30,377 $59,100 $47,083

/ 6

/ 10

continued

1 http://calculators.ato.gov.au/scripts/axos/axos.asp?CONTEXT=&KBS=Medicare10.xr4&go=ok

Copyright Mentor Education Group Pty Ltd Page 7 of 50

3018227579509505644.docx

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

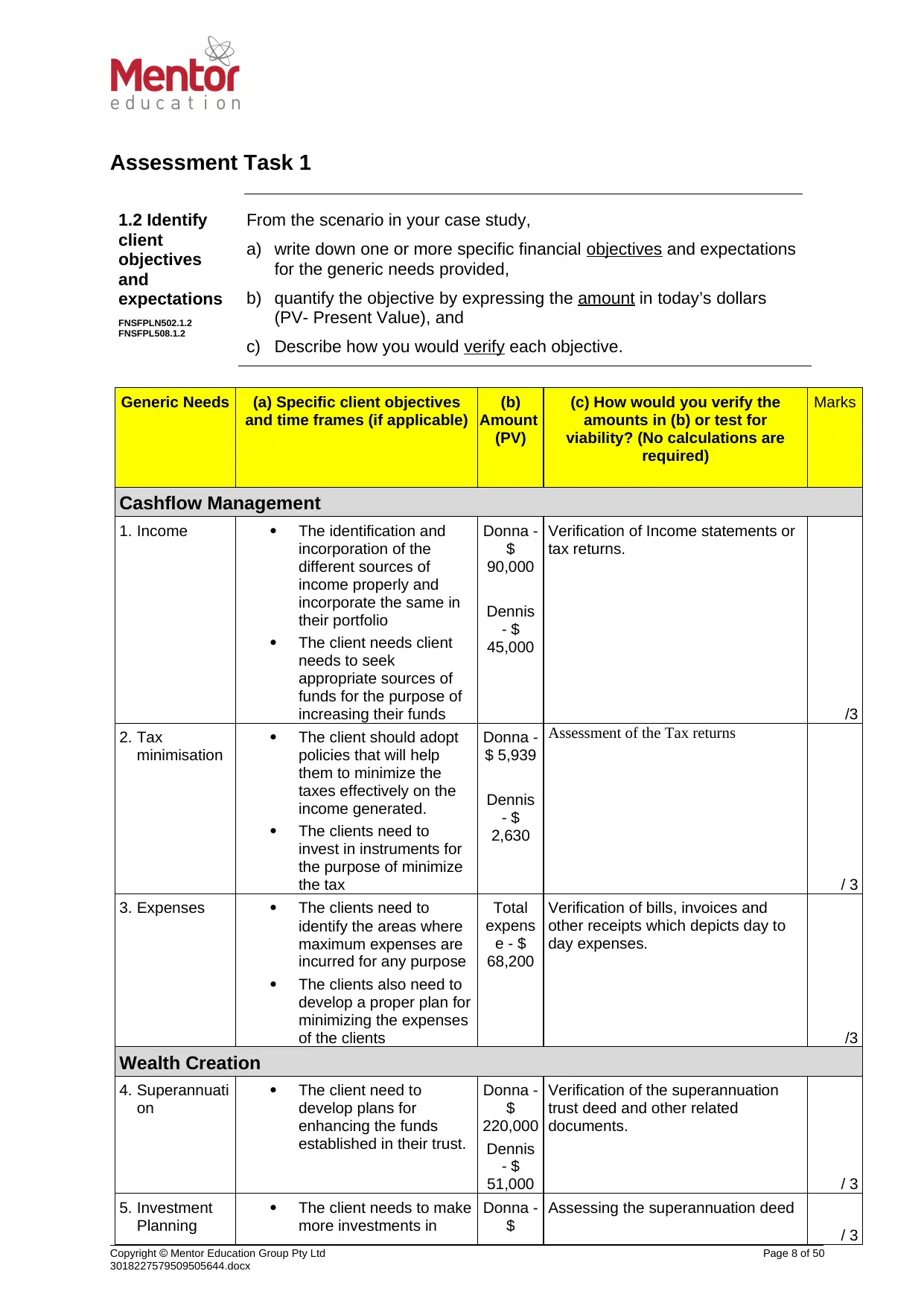

Assessment Task 1

1.2 Identify

client

objectives

and

expectations

FNSFPLN502.1.2

FNSFPL508.1.2

From the scenario in your case study,

a) write down one or more specific financial objectives and expectations

for the generic needs provided,

b) quantify the objective by expressing the amount in today’s dollars

(PV- Present Value), and

c) Describe how you would verify each objective.

Generic Needs (a) Specific client objectives

and time frames (if applicable)

(b)

Amount

(PV)

(c) How would you verify the

amounts in (b) or test for

viability? (No calculations are

required)

Marks

Cashflow Management

1. Income The identification and

incorporation of the

different sources of

income properly and

incorporate the same in

their portfolio

The client needs client

needs to seek

appropriate sources of

funds for the purpose of

increasing their funds

Donna -

$

90,000

Dennis

- $

45,000

Verification of Income statements or

tax returns.

/3

2. Tax

minimisation

The client should adopt

policies that will help

them to minimize the

taxes effectively on the

income generated.

The clients need to

invest in instruments for

the purpose of minimize

the tax

Donna -

$ 5,939

Dennis

- $

2,630

Assessment of the Tax returns

/ 3

3. Expenses The clients need to

identify the areas where

maximum expenses are

incurred for any purpose

The clients also need to

develop a proper plan for

minimizing the expenses

of the clients

Total

expens

e - $

68,200

Verification of bills, invoices and

other receipts which depicts day to

day expenses.

/3

Wealth Creation

4. Superannuati

on

The client need to

develop plans for

enhancing the funds

established in their trust.

Donna -

$

220,000

Dennis

- $

51,000

Verification of the superannuation

trust deed and other related

documents.

/ 3

5. Investment

Planning

The client needs to make

more investments in

Donna -

$

Assessing the superannuation deed

/ 3

Copyright Mentor Education Group Pty Ltd Page 8 of 50

3018227579509505644.docx

1.2 Identify

client

objectives

and

expectations

FNSFPLN502.1.2

FNSFPL508.1.2

From the scenario in your case study,

a) write down one or more specific financial objectives and expectations

for the generic needs provided,

b) quantify the objective by expressing the amount in today’s dollars

(PV- Present Value), and

c) Describe how you would verify each objective.

Generic Needs (a) Specific client objectives

and time frames (if applicable)

(b)

Amount

(PV)

(c) How would you verify the

amounts in (b) or test for

viability? (No calculations are

required)

Marks

Cashflow Management

1. Income The identification and

incorporation of the

different sources of

income properly and

incorporate the same in

their portfolio

The client needs client

needs to seek

appropriate sources of

funds for the purpose of

increasing their funds

Donna -

$

90,000

Dennis

- $

45,000

Verification of Income statements or

tax returns.

/3

2. Tax

minimisation

The client should adopt

policies that will help

them to minimize the

taxes effectively on the

income generated.

The clients need to

invest in instruments for

the purpose of minimize

the tax

Donna -

$ 5,939

Dennis

- $

2,630

Assessment of the Tax returns

/ 3

3. Expenses The clients need to

identify the areas where

maximum expenses are

incurred for any purpose

The clients also need to

develop a proper plan for

minimizing the expenses

of the clients

Total

expens

e - $

68,200

Verification of bills, invoices and

other receipts which depicts day to

day expenses.

/3

Wealth Creation

4. Superannuati

on

The client need to

develop plans for

enhancing the funds

established in their trust.

Donna -

$

220,000

Dennis

- $

51,000

Verification of the superannuation

trust deed and other related

documents.

/ 3

5. Investment

Planning

The client needs to make

more investments in

Donna -

$

Assessing the superannuation deed

/ 3

Copyright Mentor Education Group Pty Ltd Page 8 of 50

3018227579509505644.docx

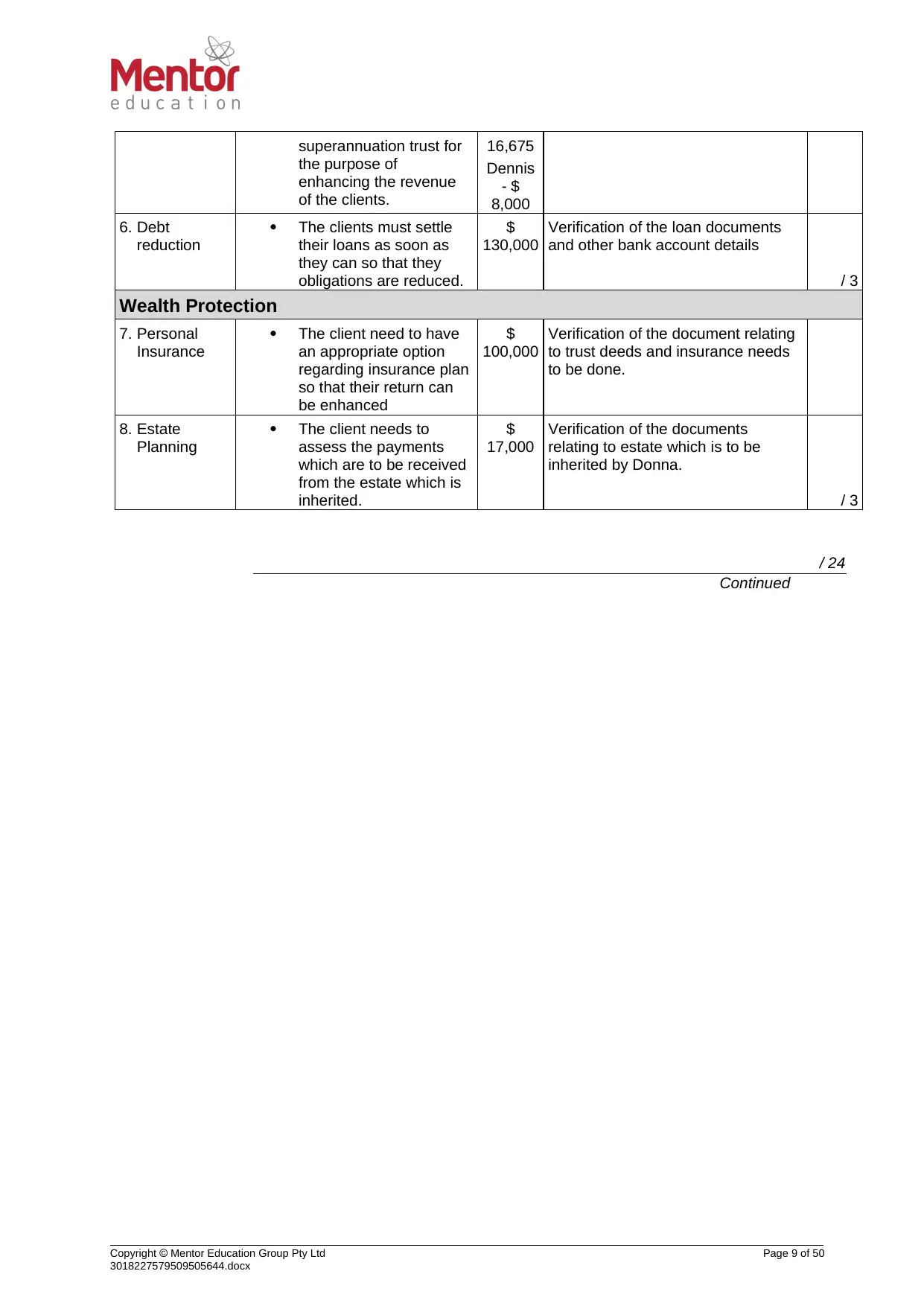

superannuation trust for

the purpose of

enhancing the revenue

of the clients.

16,675

Dennis

- $

8,000

6. Debt

reduction

The clients must settle

their loans as soon as

they can so that they

obligations are reduced.

$

130,000

Verification of the loan documents

and other bank account details

/ 3

Wealth Protection

7. Personal

Insurance

The client need to have

an appropriate option

regarding insurance plan

so that their return can

be enhanced

$

100,000

Verification of the document relating

to trust deeds and insurance needs

to be done.

8. Estate

Planning

The client needs to

assess the payments

which are to be received

from the estate which is

inherited.

$

17,000

Verification of the documents

relating to estate which is to be

inherited by Donna.

/ 3

/ 24

Continued

Copyright Mentor Education Group Pty Ltd Page 9 of 50

3018227579509505644.docx

the purpose of

enhancing the revenue

of the clients.

16,675

Dennis

- $

8,000

6. Debt

reduction

The clients must settle

their loans as soon as

they can so that they

obligations are reduced.

$

130,000

Verification of the loan documents

and other bank account details

/ 3

Wealth Protection

7. Personal

Insurance

The client need to have

an appropriate option

regarding insurance plan

so that their return can

be enhanced

$

100,000

Verification of the document relating

to trust deeds and insurance needs

to be done.

8. Estate

Planning

The client needs to

assess the payments

which are to be received

from the estate which is

inherited.

$

17,000

Verification of the documents

relating to estate which is to be

inherited by Donna.

/ 3

/ 24

Continued

Copyright Mentor Education Group Pty Ltd Page 9 of 50

3018227579509505644.docx

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

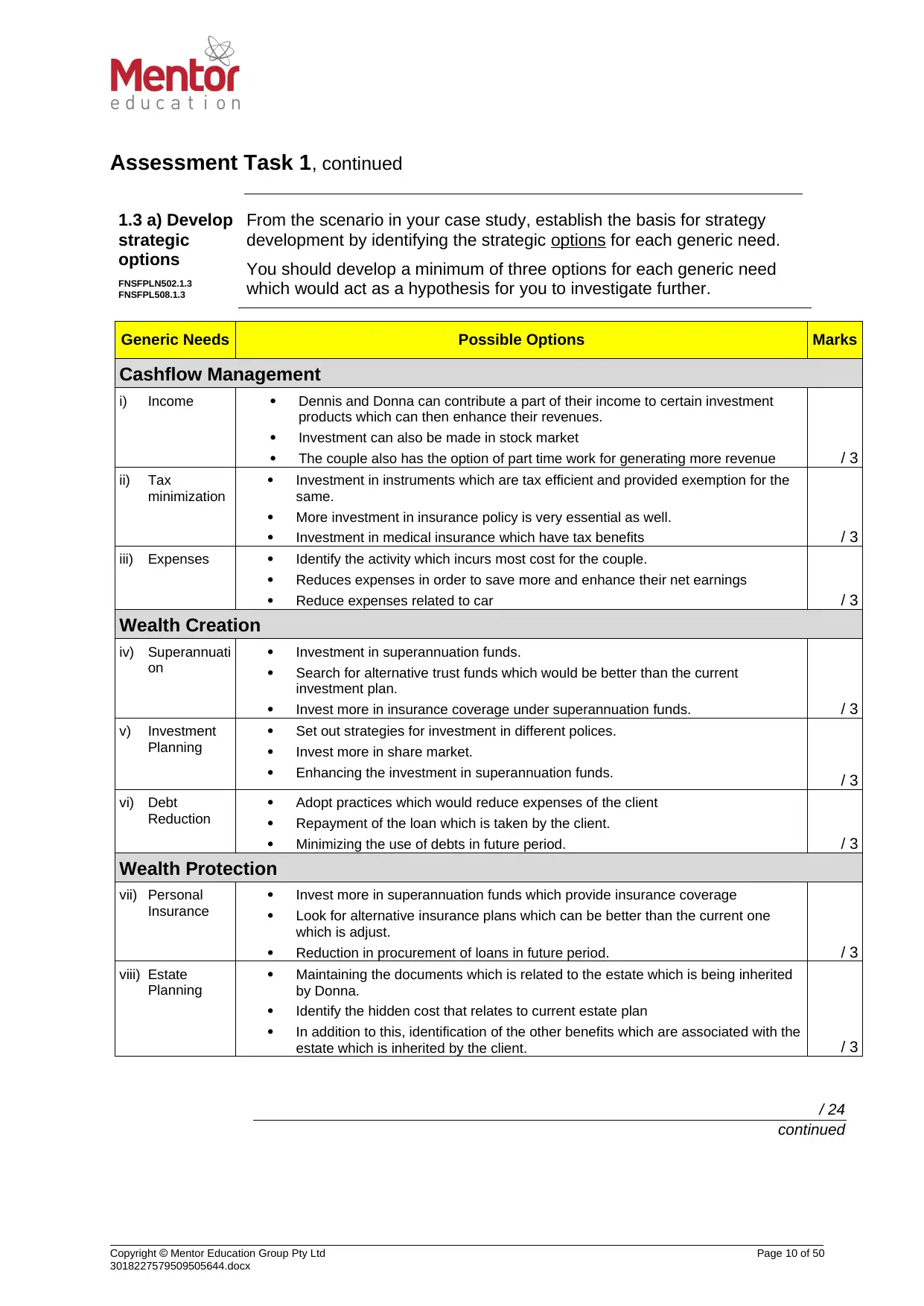

Assessment Task 1, continued

1.3 a) Develop

strategic

options

FNSFPLN502.1.3

FNSFPL508.1.3

From the scenario in your case study, establish the basis for strategy

development by identifying the strategic options for each generic need.

You should develop a minimum of three options for each generic need

which would act as a hypothesis for you to investigate further.

Generic Needs Possible Options Marks

Cashflow Management

i) Income Dennis and Donna can contribute a part of their income to certain investment

products which can then enhance their revenues.

Investment can also be made in stock market

The couple also has the option of part time work for generating more revenue / 3

ii) Tax

minimization

Investment in instruments which are tax efficient and provided exemption for the

same.

More investment in insurance policy is very essential as well.

Investment in medical insurance which have tax benefits / 3

iii) Expenses Identify the activity which incurs most cost for the couple.

Reduces expenses in order to save more and enhance their net earnings

Reduce expenses related to car / 3

Wealth Creation

iv) Superannuati

on

Investment in superannuation funds.

Search for alternative trust funds which would be better than the current

investment plan.

Invest more in insurance coverage under superannuation funds. / 3

v) Investment

Planning

Set out strategies for investment in different polices.

Invest more in share market.

Enhancing the investment in superannuation funds. / 3

vi) Debt

Reduction

Adopt practices which would reduce expenses of the client

Repayment of the loan which is taken by the client.

Minimizing the use of debts in future period. / 3

Wealth Protection

vii) Personal

Insurance

Invest more in superannuation funds which provide insurance coverage

Look for alternative insurance plans which can be better than the current one

which is adjust.

Reduction in procurement of loans in future period. / 3

viii) Estate

Planning

Maintaining the documents which is related to the estate which is being inherited

by Donna.

Identify the hidden cost that relates to current estate plan

In addition to this, identification of the other benefits which are associated with the

estate which is inherited by the client. / 3

/ 24

continued

Copyright Mentor Education Group Pty Ltd Page 10 of 50

3018227579509505644.docx

1.3 a) Develop

strategic

options

FNSFPLN502.1.3

FNSFPL508.1.3

From the scenario in your case study, establish the basis for strategy

development by identifying the strategic options for each generic need.

You should develop a minimum of three options for each generic need

which would act as a hypothesis for you to investigate further.

Generic Needs Possible Options Marks

Cashflow Management

i) Income Dennis and Donna can contribute a part of their income to certain investment

products which can then enhance their revenues.

Investment can also be made in stock market

The couple also has the option of part time work for generating more revenue / 3

ii) Tax

minimization

Investment in instruments which are tax efficient and provided exemption for the

same.

More investment in insurance policy is very essential as well.

Investment in medical insurance which have tax benefits / 3

iii) Expenses Identify the activity which incurs most cost for the couple.

Reduces expenses in order to save more and enhance their net earnings

Reduce expenses related to car / 3

Wealth Creation

iv) Superannuati

on

Investment in superannuation funds.

Search for alternative trust funds which would be better than the current

investment plan.

Invest more in insurance coverage under superannuation funds. / 3

v) Investment

Planning

Set out strategies for investment in different polices.

Invest more in share market.

Enhancing the investment in superannuation funds. / 3

vi) Debt

Reduction

Adopt practices which would reduce expenses of the client

Repayment of the loan which is taken by the client.

Minimizing the use of debts in future period. / 3

Wealth Protection

vii) Personal

Insurance

Invest more in superannuation funds which provide insurance coverage

Look for alternative insurance plans which can be better than the current one

which is adjust.

Reduction in procurement of loans in future period. / 3

viii) Estate

Planning

Maintaining the documents which is related to the estate which is being inherited

by Donna.

Identify the hidden cost that relates to current estate plan

In addition to this, identification of the other benefits which are associated with the

estate which is inherited by the client. / 3

/ 24

continued

Copyright Mentor Education Group Pty Ltd Page 10 of 50

3018227579509505644.docx

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assessment Task 1, continued

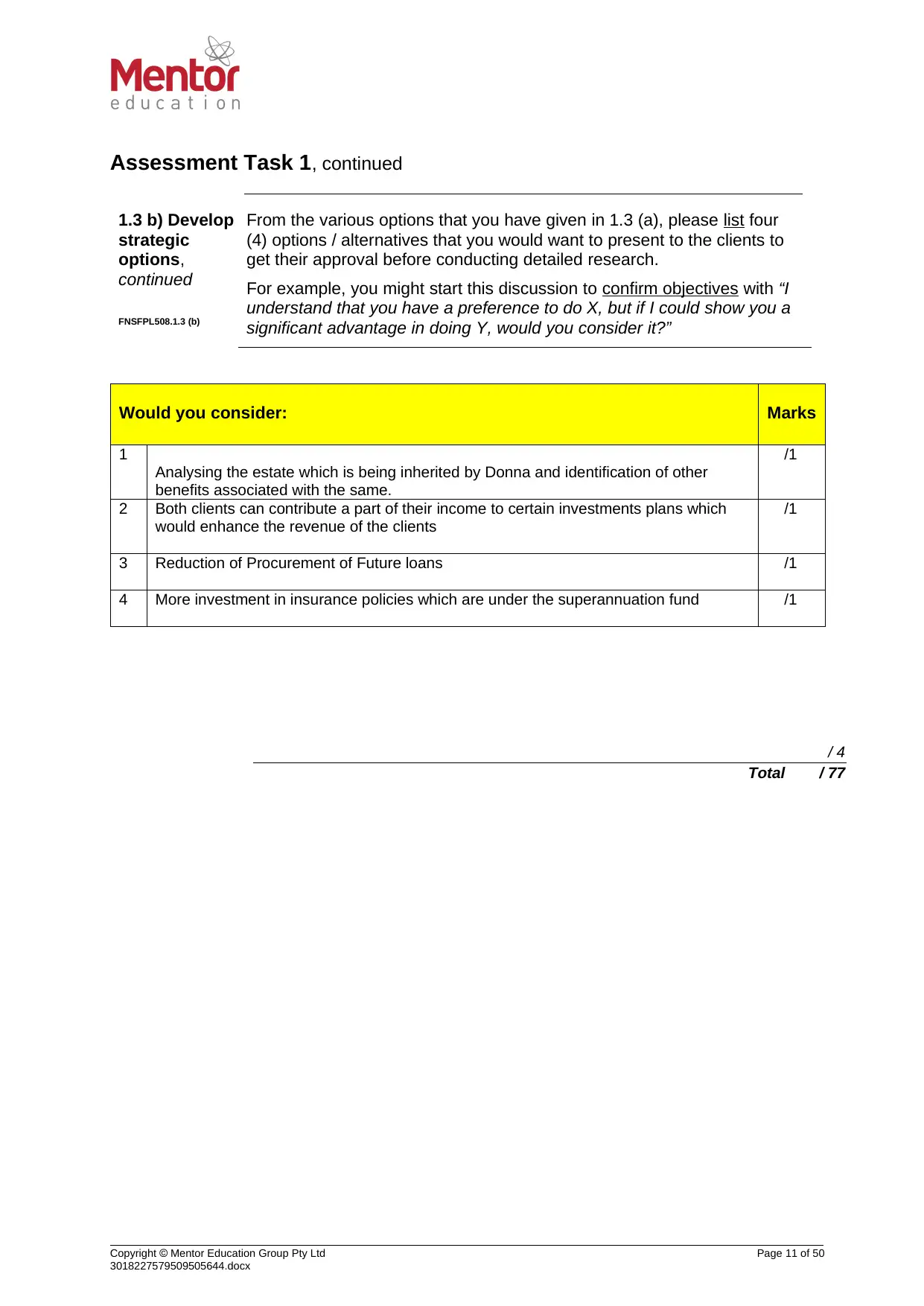

1.3 b) Develop

strategic

options,

continued

FNSFPL508.1.3 (b)

From the various options that you have given in 1.3 (a), please list four

(4) options / alternatives that you would want to present to the clients to

get their approval before conducting detailed research.

For example, you might start this discussion to confirm objectives with “I

understand that you have a preference to do X, but if I could show you a

significant advantage in doing Y, would you consider it?”

Would you consider: Marks

1

Analysing the estate which is being inherited by Donna and identification of other

benefits associated with the same.

/1

2 Both clients can contribute a part of their income to certain investments plans which

would enhance the revenue of the clients

/1

3 Reduction of Procurement of Future loans /1

4 More investment in insurance policies which are under the superannuation fund /1

/ 4

Total / 77

Copyright Mentor Education Group Pty Ltd Page 11 of 50

3018227579509505644.docx

1.3 b) Develop

strategic

options,

continued

FNSFPL508.1.3 (b)

From the various options that you have given in 1.3 (a), please list four

(4) options / alternatives that you would want to present to the clients to

get their approval before conducting detailed research.

For example, you might start this discussion to confirm objectives with “I

understand that you have a preference to do X, but if I could show you a

significant advantage in doing Y, would you consider it?”

Would you consider: Marks

1

Analysing the estate which is being inherited by Donna and identification of other

benefits associated with the same.

/1

2 Both clients can contribute a part of their income to certain investments plans which

would enhance the revenue of the clients

/1

3 Reduction of Procurement of Future loans /1

4 More investment in insurance policies which are under the superannuation fund /1

/ 4

Total / 77

Copyright Mentor Education Group Pty Ltd Page 11 of 50

3018227579509505644.docx

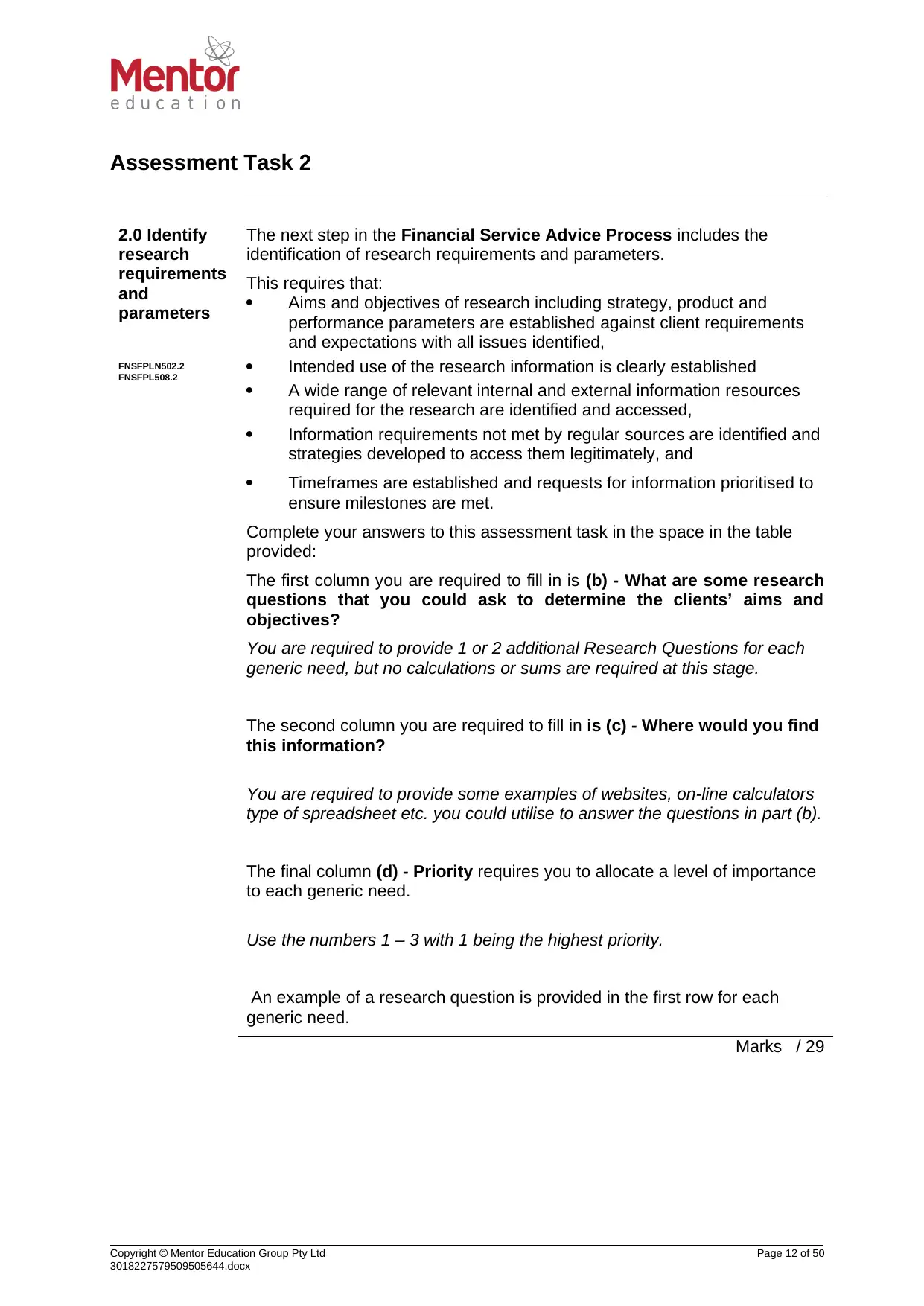

Assessment Task 2

2.0 Identify

research

requirements

and

parameters

FNSFPLN502.2

FNSFPL508.2

The next step in the Financial Service Advice Process includes the

identification of research requirements and parameters.

This requires that:

Aims and objectives of research including strategy, product and

performance parameters are established against client requirements

and expectations with all issues identified,

Intended use of the research information is clearly established

A wide range of relevant internal and external information resources

required for the research are identified and accessed,

Information requirements not met by regular sources are identified and

strategies developed to access them legitimately, and

Timeframes are established and requests for information prioritised to

ensure milestones are met.

Complete your answers to this assessment task in the space in the table

provided:

The first column you are required to fill in is (b) - What are some research

questions that you could ask to determine the clients’ aims and

objectives?

You are required to provide 1 or 2 additional Research Questions for each

generic need, but no calculations or sums are required at this stage.

The second column you are required to fill in is (c) - Where would you find

this information?

You are required to provide some examples of websites, on-line calculators

type of spreadsheet etc. you could utilise to answer the questions in part (b).

The final column (d) - Priority requires you to allocate a level of importance

to each generic need.

Use the numbers 1 – 3 with 1 being the highest priority.

An example of a research question is provided in the first row for each

generic need.

Marks / 29

Copyright Mentor Education Group Pty Ltd Page 12 of 50

3018227579509505644.docx

2.0 Identify

research

requirements

and

parameters

FNSFPLN502.2

FNSFPL508.2

The next step in the Financial Service Advice Process includes the

identification of research requirements and parameters.

This requires that:

Aims and objectives of research including strategy, product and

performance parameters are established against client requirements

and expectations with all issues identified,

Intended use of the research information is clearly established

A wide range of relevant internal and external information resources

required for the research are identified and accessed,

Information requirements not met by regular sources are identified and

strategies developed to access them legitimately, and

Timeframes are established and requests for information prioritised to

ensure milestones are met.

Complete your answers to this assessment task in the space in the table

provided:

The first column you are required to fill in is (b) - What are some research

questions that you could ask to determine the clients’ aims and

objectives?

You are required to provide 1 or 2 additional Research Questions for each

generic need, but no calculations or sums are required at this stage.

The second column you are required to fill in is (c) - Where would you find

this information?

You are required to provide some examples of websites, on-line calculators

type of spreadsheet etc. you could utilise to answer the questions in part (b).

The final column (d) - Priority requires you to allocate a level of importance

to each generic need.

Use the numbers 1 – 3 with 1 being the highest priority.

An example of a research question is provided in the first row for each

generic need.

Marks / 29

Copyright Mentor Education Group Pty Ltd Page 12 of 50

3018227579509505644.docx

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 50

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.