Financial Planning Report: Financial Planning for Retirement ACCT 2264

VerifiedAdded on 2022/11/24

|24

|5058

|394

Report

AI Summary

This financial planning report presents a Statement of Advice (SOA) developed for a married couple, Sean and Lydia Salter, who are seeking pre-retirement planning guidance. The report begins with an executive summary, outlining the clients' personal and financial situations, including their goals to retire by 2025, pay off their mortgage, and maintain their current standard of living. It details their combined gross income, assets, and liabilities, as well as their objectives such as minimizing taxes, providing for their children, and ensuring a comfortable retirement income. The report assesses the clients' balanced risk profile and scope of advice, which focuses on establishing a realistic retirement plan and advising on financial products to minimize tax expenses. It includes detailed personal information, a risk profile assessment, and a discussion of potential risks associated with the advice. The report then evaluates the viability of the recommendations, including strategies for superannuation, estate planning, and investment properties, along with an ongoing service review and authority to proceed. Finally, it provides a detailed financial position analysis, including cash flow projections, and offers specific recommendations to achieve the clients' financial goals, such as paying off the mortgage, purchasing a car, taking a holiday, and providing for their children. The report aims to provide a comprehensive and compliant financial plan for a secure retirement.

Running head: FINANCIAL PLANNING

Statement of Advice

Confidential

Prepared for

(Mr Sean and Lydia Slatar)

Client Address Line 1)

(Client Address Line 2)

Prepared By

(Insert Adviser Name)

(Adviser Address here)

Authorised Representative of

Mentor Financial Planning Pty Ltd ABN 61 094 529 987

Australian Financial Services Licensee

Australian Financial Services License number xxxxx

Level 18, 28 Bligh Street,

Sydney NSW 2000

Statement of Advice

Confidential

Prepared for

(Mr Sean and Lydia Slatar)

Client Address Line 1)

(Client Address Line 2)

Prepared By

(Insert Adviser Name)

(Adviser Address here)

Authorised Representative of

Mentor Financial Planning Pty Ltd ABN 61 094 529 987

Australian Financial Services Licensee

Australian Financial Services License number xxxxx

Level 18, 28 Bligh Street,

Sydney NSW 2000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

FINANCIAL PLANNING

Table of Contents

Executive Summary.........................................................................................................................2

Personal Situation of the Client...................................................................................................2

Financial Situation.......................................................................................................................2

Goals and Objectives...................................................................................................................3

Risk Profile..................................................................................................................................3

Scope of Advice...............................................................................................................................3

Personal Information of the Client..............................................................................................4

Goals and Objectives of the Clients.................................................................................................5

Risk Profile Assessment..................................................................................................................6

Risks Associated with the Advice...................................................................................................6

Viability of the Recommendations..................................................................................................7

Financial Position of the client........................................................................................................8

Recommendations..........................................................................................................................10

Superannuation Fund.....................................................................................................................16

Estate Planning..............................................................................................................................18

Investment Property.......................................................................................................................18

Ongoing Service Review...............................................................................................................19

Authority to Proceed......................................................................................................................20

FINANCIAL PLANNING

Table of Contents

Executive Summary.........................................................................................................................2

Personal Situation of the Client...................................................................................................2

Financial Situation.......................................................................................................................2

Goals and Objectives...................................................................................................................3

Risk Profile..................................................................................................................................3

Scope of Advice...............................................................................................................................3

Personal Information of the Client..............................................................................................4

Goals and Objectives of the Clients.................................................................................................5

Risk Profile Assessment..................................................................................................................6

Risks Associated with the Advice...................................................................................................6

Viability of the Recommendations..................................................................................................7

Financial Position of the client........................................................................................................8

Recommendations..........................................................................................................................10

Superannuation Fund.....................................................................................................................16

Estate Planning..............................................................................................................................18

Investment Property.......................................................................................................................18

Ongoing Service Review...............................................................................................................19

Authority to Proceed......................................................................................................................20

2

FINANCIAL PLANNING

Executive Summary

Personal Situation of the Client

As per the information which is provided, the clients are Sean and Lydia Salter who are a

married couple. The information which is provided in the fact sheet shows that Sean works as an

electrician while Lydia works as a Florist. Both the clients want to retire by 2025 and by the time

needs to have proper and quite retirement life with no burden of any mortgage. The annual salary

of Sean is $ 140,000 while Lydia earns around $ 30,000. The couple wants to ensure that their

standard of living to be appropriate and also wishes that they can purchase a car and go on a

holiday trip after retirement. As per the information, they hold a property which is used for

residential purposes but after retirement, they want to use the property for generating rental

income.

Financial Situation

As the client fact sheet highlights, Sean is able to generate a gross income of $ 140,000

from his work while Lydia is able to generate $ 30,000 from her florist job. In total, the gross

income of the family is $ 170,000. The couple also owns a property which has a market value of

$ 550,000 and the same is under mortgage. The mortgage interest amounts to $ 175,000 which

also needs to covered by the time of their retirement. I also noticed that Lydia would be getting a

inheritance to her aunts property which is worth $ 200,000. In addition to this, the client has a

superannuation of $ 270,000 while client’s partner has a superannuation of $ 100,000.

Goals and Objectives

The goals and objectives which the clients would be looking forward to fulfill are listed

below in details:

FINANCIAL PLANNING

Executive Summary

Personal Situation of the Client

As per the information which is provided, the clients are Sean and Lydia Salter who are a

married couple. The information which is provided in the fact sheet shows that Sean works as an

electrician while Lydia works as a Florist. Both the clients want to retire by 2025 and by the time

needs to have proper and quite retirement life with no burden of any mortgage. The annual salary

of Sean is $ 140,000 while Lydia earns around $ 30,000. The couple wants to ensure that their

standard of living to be appropriate and also wishes that they can purchase a car and go on a

holiday trip after retirement. As per the information, they hold a property which is used for

residential purposes but after retirement, they want to use the property for generating rental

income.

Financial Situation

As the client fact sheet highlights, Sean is able to generate a gross income of $ 140,000

from his work while Lydia is able to generate $ 30,000 from her florist job. In total, the gross

income of the family is $ 170,000. The couple also owns a property which has a market value of

$ 550,000 and the same is under mortgage. The mortgage interest amounts to $ 175,000 which

also needs to covered by the time of their retirement. I also noticed that Lydia would be getting a

inheritance to her aunts property which is worth $ 200,000. In addition to this, the client has a

superannuation of $ 270,000 while client’s partner has a superannuation of $ 100,000.

Goals and Objectives

The goals and objectives which the clients would be looking forward to fulfill are listed

below in details:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

FINANCIAL PLANNING

To pay off their mortgages at retirement and have sufficient funds to purchase a new car

($40,000) and take a holiday ($25,000).

To restructure their affairs with a view to having $52,000pa in retirement.

To give the two children $40,000 each to start their savings plans.

To minimize tax, if possible, both now and in retirement

To maintain their current standard of living while conducting the operations of the

business.

Risk Profile

The client fact sheet which is available shows that the client is a balanced investor as the

investment objective of the client is to maintain appropriate funding after their retirement so that

they can maintain an appropriate standard of living for themselves. The income that would be

attained requires to satisfy the need of income and the fair rate of return.

Scope of Advice

As per the information which is available to me from the client fact sheet is that the

clients need financial advice regarding establishing a realistic future plan for setting up

retirement plan for themselves. My role would be to advise the clients about the entire financial

product available in the market that can be beneficial for the client. The different products which

are available in the market would help the client in minimizing the tax expenses which is

associated with the business. I would be suggesting some of the strategies which can be followed

by the client for the purpose of ensuring that the clients are satisfied with the services which is

followed by the business.

FINANCIAL PLANNING

To pay off their mortgages at retirement and have sufficient funds to purchase a new car

($40,000) and take a holiday ($25,000).

To restructure their affairs with a view to having $52,000pa in retirement.

To give the two children $40,000 each to start their savings plans.

To minimize tax, if possible, both now and in retirement

To maintain their current standard of living while conducting the operations of the

business.

Risk Profile

The client fact sheet which is available shows that the client is a balanced investor as the

investment objective of the client is to maintain appropriate funding after their retirement so that

they can maintain an appropriate standard of living for themselves. The income that would be

attained requires to satisfy the need of income and the fair rate of return.

Scope of Advice

As per the information which is available to me from the client fact sheet is that the

clients need financial advice regarding establishing a realistic future plan for setting up

retirement plan for themselves. My role would be to advise the clients about the entire financial

product available in the market that can be beneficial for the client. The different products which

are available in the market would help the client in minimizing the tax expenses which is

associated with the business. I would be suggesting some of the strategies which can be followed

by the client for the purpose of ensuring that the clients are satisfied with the services which is

followed by the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

FINANCIAL PLANNING

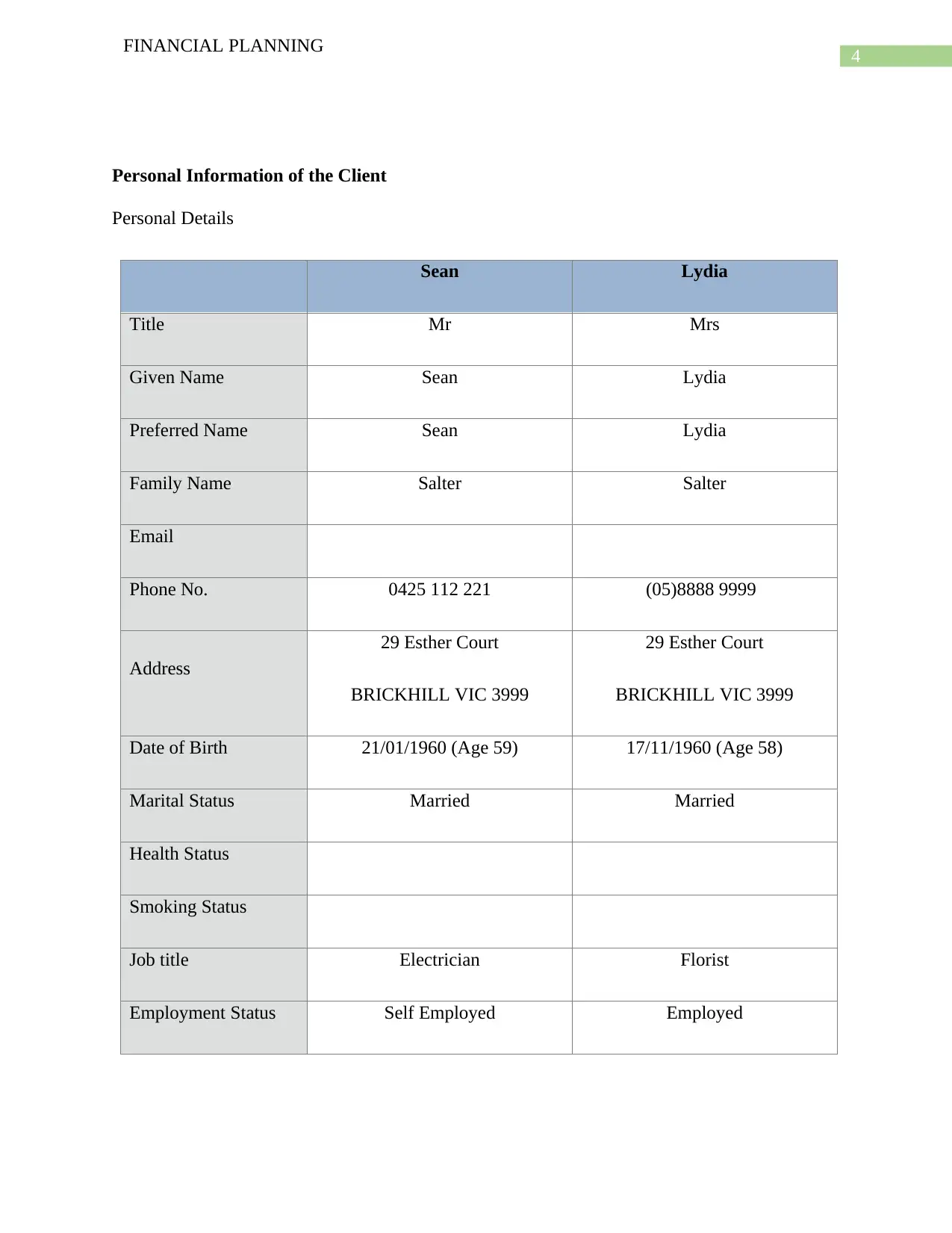

Personal Information of the Client

Personal Details

Sean Lydia

Title Mr Mrs

Given Name Sean Lydia

Preferred Name Sean Lydia

Family Name Salter Salter

Email

Phone No. 0425 112 221 (05)8888 9999

Address

29 Esther Court

BRICKHILL VIC 3999

29 Esther Court

BRICKHILL VIC 3999

Date of Birth 21/01/1960 (Age 59) 17/11/1960 (Age 58)

Marital Status Married Married

Health Status

Smoking Status

Job title Electrician Florist

Employment Status Self Employed Employed

FINANCIAL PLANNING

Personal Information of the Client

Personal Details

Sean Lydia

Title Mr Mrs

Given Name Sean Lydia

Preferred Name Sean Lydia

Family Name Salter Salter

Phone No. 0425 112 221 (05)8888 9999

Address

29 Esther Court

BRICKHILL VIC 3999

29 Esther Court

BRICKHILL VIC 3999

Date of Birth 21/01/1960 (Age 59) 17/11/1960 (Age 58)

Marital Status Married Married

Health Status

Smoking Status

Job title Electrician Florist

Employment Status Self Employed Employed

5

FINANCIAL PLANNING

Number of

Dependants

0

Goals and Objectives of the Clients

In order to ensure that the investment strategies are properly followed and implemented,

it is imperative that the goals and objectives of the business are properly managed and the same

should also be the basis on which the recommendation would be framed. In case of any change

in the scenario of the client or market condition, the recommendation would also change. From

which I have understood from the fact sheet of the client is that the goals and objectives of the

client can be divided into three categories:

Short Term: The short-term goals of the clients is to enhance their current standards of

living and also minimize their taxes. This would be providing supporting finance to the

clients for meeting their standard of living.

Medium Term Goals: The clients intend to give each of their children a sum of $ 40,000

for their better future. The clients want to pay off their mortgage loans by the time they

are fully into retirement.

Long term: The long-term objectives of the clients is to ensure that they have an

appropriate fund on per annum basis of about $ 52,000 so that they can meet their

standards of living after retirement. In addition to this, the client also wants to purchase a

new car for a value of $ 25,000 and also go on a holiday trip which would costs $ 40,000.

Risk Profile Assessment

FINANCIAL PLANNING

Number of

Dependants

0

Goals and Objectives of the Clients

In order to ensure that the investment strategies are properly followed and implemented,

it is imperative that the goals and objectives of the business are properly managed and the same

should also be the basis on which the recommendation would be framed. In case of any change

in the scenario of the client or market condition, the recommendation would also change. From

which I have understood from the fact sheet of the client is that the goals and objectives of the

client can be divided into three categories:

Short Term: The short-term goals of the clients is to enhance their current standards of

living and also minimize their taxes. This would be providing supporting finance to the

clients for meeting their standard of living.

Medium Term Goals: The clients intend to give each of their children a sum of $ 40,000

for their better future. The clients want to pay off their mortgage loans by the time they

are fully into retirement.

Long term: The long-term objectives of the clients is to ensure that they have an

appropriate fund on per annum basis of about $ 52,000 so that they can meet their

standards of living after retirement. In addition to this, the client also wants to purchase a

new car for a value of $ 25,000 and also go on a holiday trip which would costs $ 40,000.

Risk Profile Assessment

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

FINANCIAL PLANNING

The fact sheet which is provided to me shows that the client wants to take a less risky

approach in managing their financials while at the same time ensuring that the goals and

objectives of the client are fulfilled. During our meetings we also discussed: your reasons for

seeking advice; what sort of returns you are expecting; how you would like to manage your

investments; what your short, medium and long-term goals are; and how you feel about potential

capital growth and investment security. On the basis of our meetings I can assess that your risk

type is balanced. I would assess that you want a 60% growth while 40% would be on secured

income. This percentage makes you a balanced risk taker. The risk management policies which

needs to be followed in the business would be appropriately managing the operations. The

investment objective of the client is to maintain a stable return over the medium term, whereby

security of capital is of major importance. The clients want a stable life after retirement and

therefore needs to plan properly for meeting their current standard of living even after retirement.

Risks Associated with the Advice

The advice which I would be giving would be based on the current market situation and

the fact sheet which is provided by the client. On the basis of the information which is reflected

in the client fact sheet and considering the goals and objectives of the client, I would be

preparing my statement of advice for the clients. The risks which are associated with the advice

are listed below in point form:

The advices or recommendation which I would be giving would be based on current

situation of the market. The market is always subjected to change and therefore if a major

change occurs than the advice would not be applicable.

FINANCIAL PLANNING

The fact sheet which is provided to me shows that the client wants to take a less risky

approach in managing their financials while at the same time ensuring that the goals and

objectives of the client are fulfilled. During our meetings we also discussed: your reasons for

seeking advice; what sort of returns you are expecting; how you would like to manage your

investments; what your short, medium and long-term goals are; and how you feel about potential

capital growth and investment security. On the basis of our meetings I can assess that your risk

type is balanced. I would assess that you want a 60% growth while 40% would be on secured

income. This percentage makes you a balanced risk taker. The risk management policies which

needs to be followed in the business would be appropriately managing the operations. The

investment objective of the client is to maintain a stable return over the medium term, whereby

security of capital is of major importance. The clients want a stable life after retirement and

therefore needs to plan properly for meeting their current standard of living even after retirement.

Risks Associated with the Advice

The advice which I would be giving would be based on the current market situation and

the fact sheet which is provided by the client. On the basis of the information which is reflected

in the client fact sheet and considering the goals and objectives of the client, I would be

preparing my statement of advice for the clients. The risks which are associated with the advice

are listed below in point form:

The advices or recommendation which I would be giving would be based on current

situation of the market. The market is always subjected to change and therefore if a major

change occurs than the advice would not be applicable.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FINANCIAL PLANNING

In case there is a change in the goals and objectives of the client that the advice which is

provided by me would also change and I would have to review the statement of advice

again.

It is quite possible that an investment product supposes a superannuation product which I

have suggest to be the best and tax effective can still be not the best option. This is

because the market is changing and new companies are brining in better options.

Therefore, there will always be an option available in the market which would be better

than what I have suggested.

The above-mentioned risks are some of the risks which are likely to arise which I am

disclosing fully. I would also to highlight that I have provided the recommendations to the best

of knowledge and believe that the same would be in the best interest of the clients.

Viability of the Recommendations

The recommendation which I have suggested is based on the fact sheet which was

provided to us by the client and after a detailed analysis of the market situation and also

identification of the best product which is available in the market. I would like to assure you that

the recommendation which I have provided is in the best interest of both of you and it would

effectively help you to meet long term objectives and goals. The recommendations if

implemented would help to minimize your tax expenses thereby enhance the savings which is

generated by you and your partner along with ensuring that the mortgage is paid off along with

the interest amount which is associated with the same. In addition to this, you would also be able

to keep aside a sum of money which can then be used by both of you for providing a gift to your

children of $ 40,000. In addition to this, after retirement you would be able to maintain your

FINANCIAL PLANNING

In case there is a change in the goals and objectives of the client that the advice which is

provided by me would also change and I would have to review the statement of advice

again.

It is quite possible that an investment product supposes a superannuation product which I

have suggest to be the best and tax effective can still be not the best option. This is

because the market is changing and new companies are brining in better options.

Therefore, there will always be an option available in the market which would be better

than what I have suggested.

The above-mentioned risks are some of the risks which are likely to arise which I am

disclosing fully. I would also to highlight that I have provided the recommendations to the best

of knowledge and believe that the same would be in the best interest of the clients.

Viability of the Recommendations

The recommendation which I have suggested is based on the fact sheet which was

provided to us by the client and after a detailed analysis of the market situation and also

identification of the best product which is available in the market. I would like to assure you that

the recommendation which I have provided is in the best interest of both of you and it would

effectively help you to meet long term objectives and goals. The recommendations if

implemented would help to minimize your tax expenses thereby enhance the savings which is

generated by you and your partner along with ensuring that the mortgage is paid off along with

the interest amount which is associated with the same. In addition to this, you would also be able

to keep aside a sum of money which can then be used by both of you for providing a gift to your

children of $ 40,000. In addition to this, after retirement you would be able to maintain your

8

FINANCIAL PLANNING

current standards of living as well purchase the car which you are intending to buy and also go

on the holiday trip which is one of your objectives.

The recommendation would serve in the best interest of the client as the same is provided

to the client considering all risks which are applicable to the client and I have selected the best

possible course of action which can be taken in such a situation. The main objective on my part

is to ensure that the goals and objectives of the client are fulfilled. There are also some other

goals and objectives which needs to be fulfilled and the same would also be considered in my

statement of advice.

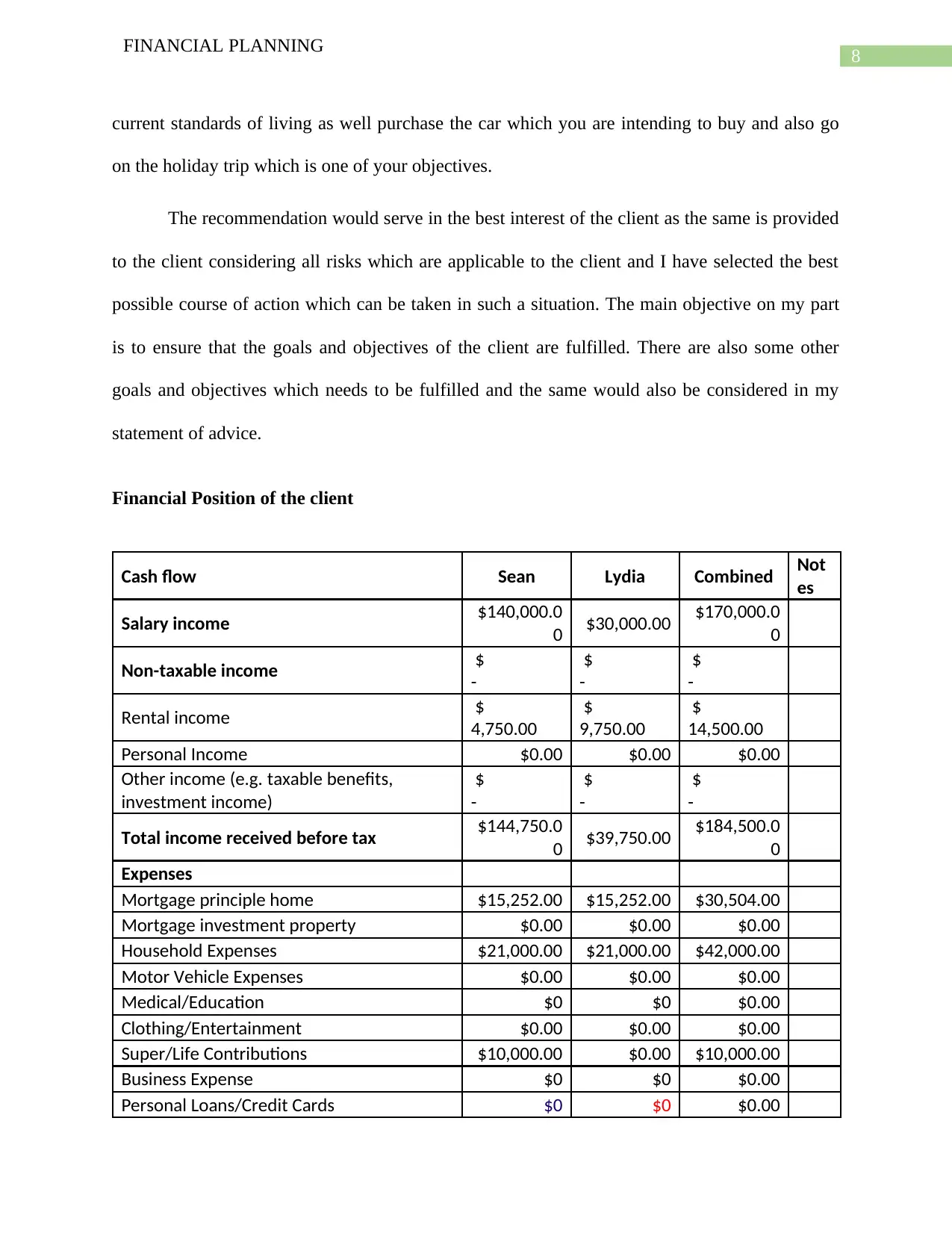

Financial Position of the client

Cash flow Sean Lydia Combined Not

es

Salary income $140,000.0

0 $30,000.00 $170,000.0

0

Non-taxable income $

-

$

-

$

-

Rental income $

4,750.00

$

9,750.00

$

14,500.00

Personal Income $0.00 $0.00 $0.00

Other income (e.g. taxable benefits,

investment income)

$

-

$

-

$

-

Total income received before tax $144,750.0

0 $39,750.00 $184,500.0

0

Expenses

Mortgage principle home $15,252.00 $15,252.00 $30,504.00

Mortgage investment property $0.00 $0.00 $0.00

Household Expenses $21,000.00 $21,000.00 $42,000.00

Motor Vehicle Expenses $0.00 $0.00 $0.00

Medical/Education $0 $0 $0.00

Clothing/Entertainment $0.00 $0.00 $0.00

Super/Life Contributions $10,000.00 $0.00 $10,000.00

Business Expense $0 $0 $0.00

Personal Loans/Credit Cards $0 $0 $0.00

FINANCIAL PLANNING

current standards of living as well purchase the car which you are intending to buy and also go

on the holiday trip which is one of your objectives.

The recommendation would serve in the best interest of the client as the same is provided

to the client considering all risks which are applicable to the client and I have selected the best

possible course of action which can be taken in such a situation. The main objective on my part

is to ensure that the goals and objectives of the client are fulfilled. There are also some other

goals and objectives which needs to be fulfilled and the same would also be considered in my

statement of advice.

Financial Position of the client

Cash flow Sean Lydia Combined Not

es

Salary income $140,000.0

0 $30,000.00 $170,000.0

0

Non-taxable income $

-

$

-

$

-

Rental income $

4,750.00

$

9,750.00

$

14,500.00

Personal Income $0.00 $0.00 $0.00

Other income (e.g. taxable benefits,

investment income)

$

-

$

-

$

-

Total income received before tax $144,750.0

0 $39,750.00 $184,500.0

0

Expenses

Mortgage principle home $15,252.00 $15,252.00 $30,504.00

Mortgage investment property $0.00 $0.00 $0.00

Household Expenses $21,000.00 $21,000.00 $42,000.00

Motor Vehicle Expenses $0.00 $0.00 $0.00

Medical/Education $0 $0 $0.00

Clothing/Entertainment $0.00 $0.00 $0.00

Super/Life Contributions $10,000.00 $0.00 $10,000.00

Business Expense $0 $0 $0.00

Personal Loans/Credit Cards $0 $0 $0.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

FINANCIAL PLANNING

Other Expenses $0.00 $0.00 $0.00

Total expenses $46,252.00 $36,252.00 $82,504.00

Total income received before tax less total

expenses $98,498.00 $3,498.00 $101,996.0

0

Total tax payable from tax table above $41,850.00 $2,750.00 $44,600.00

Total net cash flow $56,648.00 $748.00 $57,396.00

The above table effectively shows the income and expenses of the clients and how the

same affect the ultimate savings of the client. The above table shows financial projection of Sean

and Lydia in separate manner as well as combined manner. This is the income statement for the

client in current scenario and the shows that the expenses for Sean and Lydia is extremely high.

In addition to this, the tax expenses which is represented for Sean and Lydia is also shown to be

significantly high. The client is not able to maintain a savings of $ 82,000 for meeting their

expenses and therefore, it is imperative that a proper plan is formulated for minimising the taxes

of the clients. In addition to this, the cash flow statement provides an idea regarding the major

expenses which is incurred by the client and also the ultimate savings which is made by the

client in current scenario.

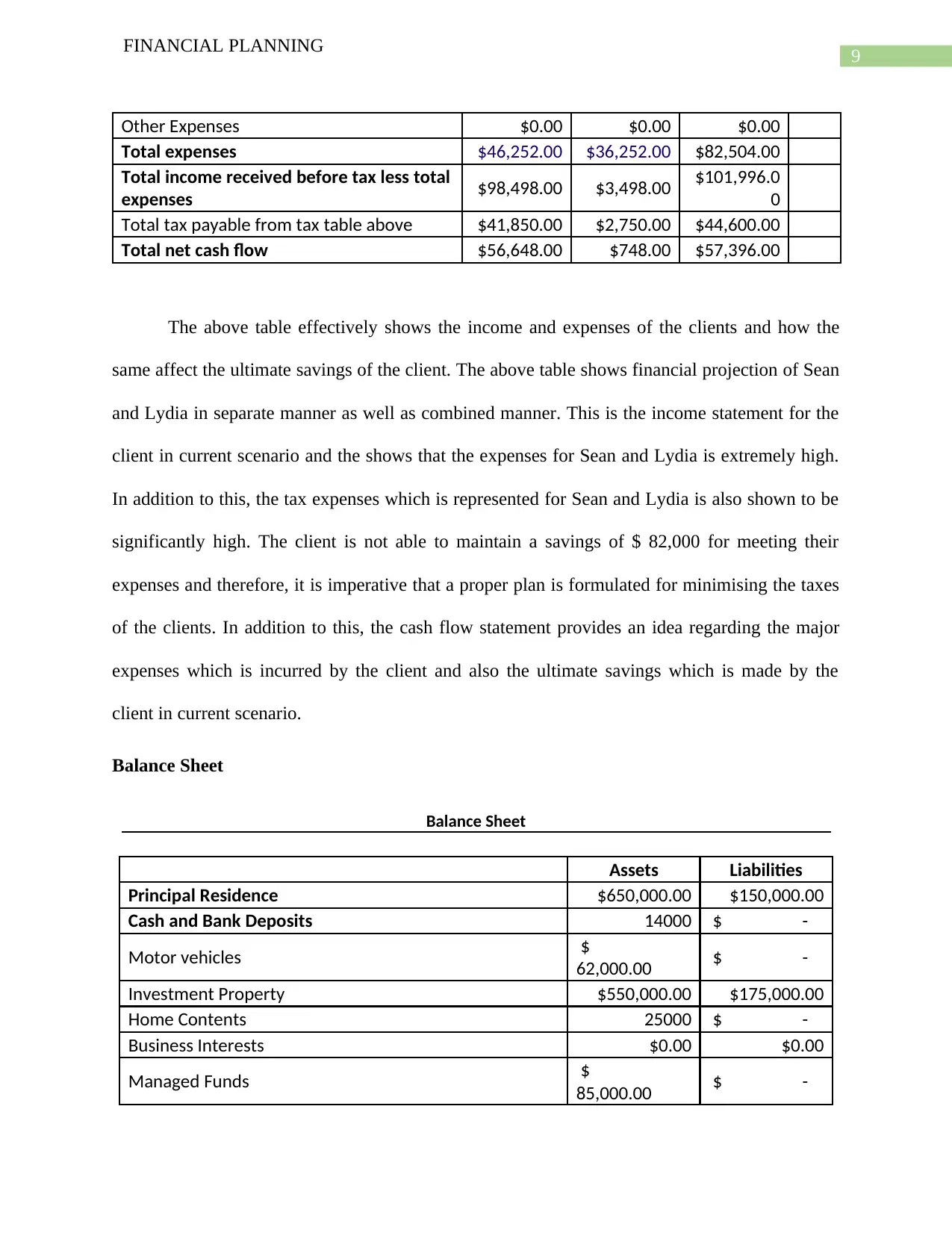

Balance Sheet

Balance Sheet

Assets Liabilities

Principal Residence $650,000.00 $150,000.00

Cash and Bank Deposits 14000 $ -

Motor vehicles $

62,000.00 $ -

Investment Property $550,000.00 $175,000.00

Home Contents 25000 $ -

Business Interests $0.00 $0.00

Managed Funds $

85,000.00 $ -

FINANCIAL PLANNING

Other Expenses $0.00 $0.00 $0.00

Total expenses $46,252.00 $36,252.00 $82,504.00

Total income received before tax less total

expenses $98,498.00 $3,498.00 $101,996.0

0

Total tax payable from tax table above $41,850.00 $2,750.00 $44,600.00

Total net cash flow $56,648.00 $748.00 $57,396.00

The above table effectively shows the income and expenses of the clients and how the

same affect the ultimate savings of the client. The above table shows financial projection of Sean

and Lydia in separate manner as well as combined manner. This is the income statement for the

client in current scenario and the shows that the expenses for Sean and Lydia is extremely high.

In addition to this, the tax expenses which is represented for Sean and Lydia is also shown to be

significantly high. The client is not able to maintain a savings of $ 82,000 for meeting their

expenses and therefore, it is imperative that a proper plan is formulated for minimising the taxes

of the clients. In addition to this, the cash flow statement provides an idea regarding the major

expenses which is incurred by the client and also the ultimate savings which is made by the

client in current scenario.

Balance Sheet

Balance Sheet

Assets Liabilities

Principal Residence $650,000.00 $150,000.00

Cash and Bank Deposits 14000 $ -

Motor vehicles $

62,000.00 $ -

Investment Property $550,000.00 $175,000.00

Home Contents 25000 $ -

Business Interests $0.00 $0.00

Managed Funds $

85,000.00 $ -

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

FINANCIAL PLANNING

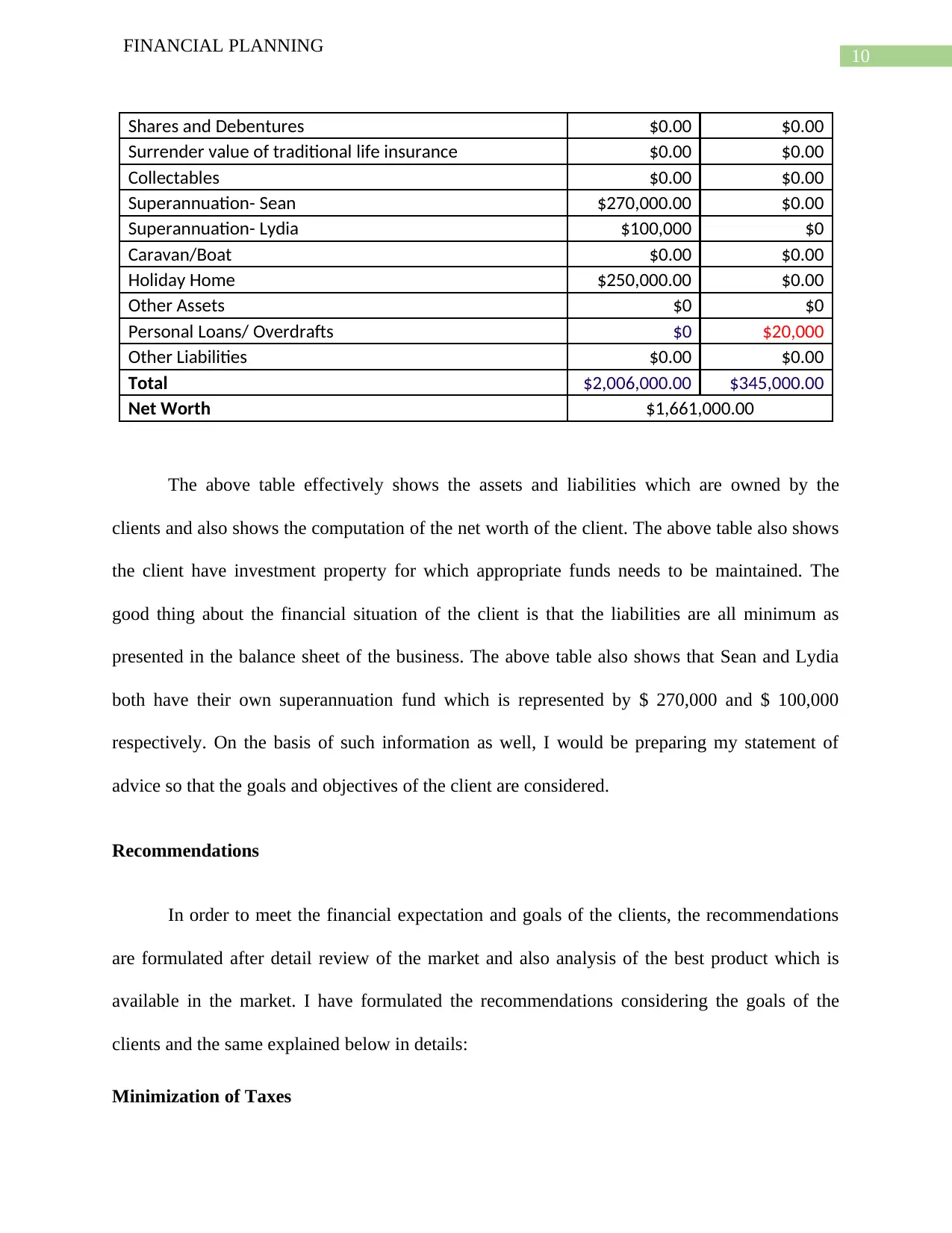

Shares and Debentures $0.00 $0.00

Surrender value of traditional life insurance $0.00 $0.00

Collectables $0.00 $0.00

Superannuation- Sean $270,000.00 $0.00

Superannuation- Lydia $100,000 $0

Caravan/Boat $0.00 $0.00

Holiday Home $250,000.00 $0.00

Other Assets $0 $0

Personal Loans/ Overdrafts $0 $20,000

Other Liabilities $0.00 $0.00

Total $2,006,000.00 $345,000.00

Net Worth $1,661,000.00

The above table effectively shows the assets and liabilities which are owned by the

clients and also shows the computation of the net worth of the client. The above table also shows

the client have investment property for which appropriate funds needs to be maintained. The

good thing about the financial situation of the client is that the liabilities are all minimum as

presented in the balance sheet of the business. The above table also shows that Sean and Lydia

both have their own superannuation fund which is represented by $ 270,000 and $ 100,000

respectively. On the basis of such information as well, I would be preparing my statement of

advice so that the goals and objectives of the client are considered.

Recommendations

In order to meet the financial expectation and goals of the clients, the recommendations

are formulated after detail review of the market and also analysis of the best product which is

available in the market. I have formulated the recommendations considering the goals of the

clients and the same explained below in details:

Minimization of Taxes

FINANCIAL PLANNING

Shares and Debentures $0.00 $0.00

Surrender value of traditional life insurance $0.00 $0.00

Collectables $0.00 $0.00

Superannuation- Sean $270,000.00 $0.00

Superannuation- Lydia $100,000 $0

Caravan/Boat $0.00 $0.00

Holiday Home $250,000.00 $0.00

Other Assets $0 $0

Personal Loans/ Overdrafts $0 $20,000

Other Liabilities $0.00 $0.00

Total $2,006,000.00 $345,000.00

Net Worth $1,661,000.00

The above table effectively shows the assets and liabilities which are owned by the

clients and also shows the computation of the net worth of the client. The above table also shows

the client have investment property for which appropriate funds needs to be maintained. The

good thing about the financial situation of the client is that the liabilities are all minimum as

presented in the balance sheet of the business. The above table also shows that Sean and Lydia

both have their own superannuation fund which is represented by $ 270,000 and $ 100,000

respectively. On the basis of such information as well, I would be preparing my statement of

advice so that the goals and objectives of the client are considered.

Recommendations

In order to meet the financial expectation and goals of the clients, the recommendations

are formulated after detail review of the market and also analysis of the best product which is

available in the market. I have formulated the recommendations considering the goals of the

clients and the same explained below in details:

Minimization of Taxes

11

FINANCIAL PLANNING

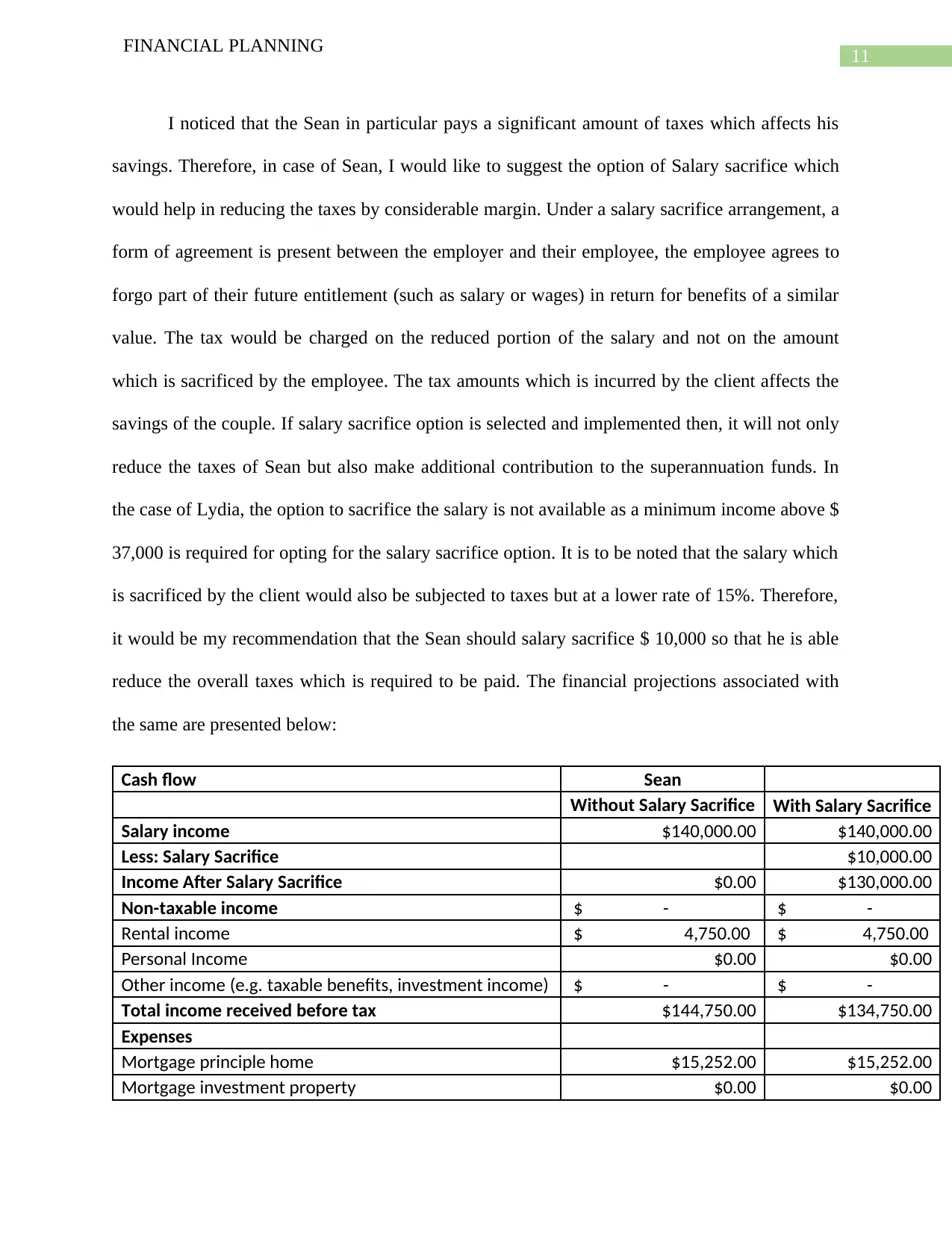

I noticed that the Sean in particular pays a significant amount of taxes which affects his

savings. Therefore, in case of Sean, I would like to suggest the option of Salary sacrifice which

would help in reducing the taxes by considerable margin. Under a salary sacrifice arrangement, a

form of agreement is present between the employer and their employee, the employee agrees to

forgo part of their future entitlement (such as salary or wages) in return for benefits of a similar

value. The tax would be charged on the reduced portion of the salary and not on the amount

which is sacrificed by the employee. The tax amounts which is incurred by the client affects the

savings of the couple. If salary sacrifice option is selected and implemented then, it will not only

reduce the taxes of Sean but also make additional contribution to the superannuation funds. In

the case of Lydia, the option to sacrifice the salary is not available as a minimum income above $

37,000 is required for opting for the salary sacrifice option. It is to be noted that the salary which

is sacrificed by the client would also be subjected to taxes but at a lower rate of 15%. Therefore,

it would be my recommendation that the Sean should salary sacrifice $ 10,000 so that he is able

reduce the overall taxes which is required to be paid. The financial projections associated with

the same are presented below:

Cash flow Sean

Without Salary Sacrifice With Salary Sacrifice

Salary income $140,000.00 $140,000.00

Less: Salary Sacrifice $10,000.00

Income After Salary Sacrifice $0.00 $130,000.00

Non-taxable income $ - $ -

Rental income $ 4,750.00 $ 4,750.00

Personal Income $0.00 $0.00

Other income (e.g. taxable benefits, investment income) $ - $ -

Total income received before tax $144,750.00 $134,750.00

Expenses

Mortgage principle home $15,252.00 $15,252.00

Mortgage investment property $0.00 $0.00

FINANCIAL PLANNING

I noticed that the Sean in particular pays a significant amount of taxes which affects his

savings. Therefore, in case of Sean, I would like to suggest the option of Salary sacrifice which

would help in reducing the taxes by considerable margin. Under a salary sacrifice arrangement, a

form of agreement is present between the employer and their employee, the employee agrees to

forgo part of their future entitlement (such as salary or wages) in return for benefits of a similar

value. The tax would be charged on the reduced portion of the salary and not on the amount

which is sacrificed by the employee. The tax amounts which is incurred by the client affects the

savings of the couple. If salary sacrifice option is selected and implemented then, it will not only

reduce the taxes of Sean but also make additional contribution to the superannuation funds. In

the case of Lydia, the option to sacrifice the salary is not available as a minimum income above $

37,000 is required for opting for the salary sacrifice option. It is to be noted that the salary which

is sacrificed by the client would also be subjected to taxes but at a lower rate of 15%. Therefore,

it would be my recommendation that the Sean should salary sacrifice $ 10,000 so that he is able

reduce the overall taxes which is required to be paid. The financial projections associated with

the same are presented below:

Cash flow Sean

Without Salary Sacrifice With Salary Sacrifice

Salary income $140,000.00 $140,000.00

Less: Salary Sacrifice $10,000.00

Income After Salary Sacrifice $0.00 $130,000.00

Non-taxable income $ - $ -

Rental income $ 4,750.00 $ 4,750.00

Personal Income $0.00 $0.00

Other income (e.g. taxable benefits, investment income) $ - $ -

Total income received before tax $144,750.00 $134,750.00

Expenses

Mortgage principle home $15,252.00 $15,252.00

Mortgage investment property $0.00 $0.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.