Retirement and Estate Planning Report for Mark and Susan Saunders

VerifiedAdded on 2021/05/31

|12

|2423

|16

Report

AI Summary

This report provides a detailed financial analysis and planning for retirement and estate, focusing on a couple's financial situation. It includes a projected cash flow statement, wealth accumulation models for superannuation, shares, and property, along with detailed assumptions. The report calculates income needs during retirement, assesses the longevity of account-based pensions, and recommends strategies to increase wealth within superannuation accounts, such as utilizing account-based pensions and self-managed super funds (SMSF). Furthermore, it addresses socially responsible investing, exploring its meaning, different approaches, and a discussion on whether it leads to lower returns. The report also reviews relevant literature and provides recommendations for the couple's financial planning needs.

Running Head: RETIREMENT AND ESTATE PLANNING ASSIGNMENT 1

Retirement and Estate Planning Assignment

Student Name

Institution

Course Code

Retirement and Estate Planning Assignment

Student Name

Institution

Course Code

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

RETIREMENT AND ESTATE PLANNING ASSIGNMENT 2

Table of Contents

Cover Letter.................................................................................................................................................2

Projected Cash flow.....................................................................................................................................4

Wealth Accumulation template...................................................................................................................5

Assumptions............................................................................................................................................5

Income of the couple...................................................................................................................................7

Assumptions............................................................................................................................................7

Strategies Advised.......................................................................................................................................8

Investing in a socially responsible manner................................................................................................10

References.................................................................................................................................................12

Table of Contents

Cover Letter.................................................................................................................................................2

Projected Cash flow.....................................................................................................................................4

Wealth Accumulation template...................................................................................................................5

Assumptions............................................................................................................................................5

Income of the couple...................................................................................................................................7

Assumptions............................................................................................................................................7

Strategies Advised.......................................................................................................................................8

Investing in a socially responsible manner................................................................................................10

References.................................................................................................................................................12

RETIREMENT AND ESTATE PLANNING ASSIGNMENT 3

Cover Letter

Mark and Susan Saunders,

41 Super Street,

Diamond Creek, 3089

Australia

Dear Mr and Mrs Saunders,

Re: RETIREMENT AND ESTATE PLANNING REPORT

It was a pleasure to meet you on 15 July 2018 at 3.00 pm regarding your retirement and estate

planning.

As agreed in our meeting there are certain aspects that you wanted us to look into your financials

and come up with a plan for you. I am delighted to announce that we looked into your personal

financial profile and came up with a report touching on all your concerns. The report is hereby

attached for your perusal. Please look at it and do not hesitate to contact us in case you have any

queries.

Thank you for considering our company for your retirement and estate planning needs. We hope

to hear from you in the near future.

Yours very truly,

Financial analyst

Cover Letter

Mark and Susan Saunders,

41 Super Street,

Diamond Creek, 3089

Australia

Dear Mr and Mrs Saunders,

Re: RETIREMENT AND ESTATE PLANNING REPORT

It was a pleasure to meet you on 15 July 2018 at 3.00 pm regarding your retirement and estate

planning.

As agreed in our meeting there are certain aspects that you wanted us to look into your financials

and come up with a plan for you. I am delighted to announce that we looked into your personal

financial profile and came up with a report touching on all your concerns. The report is hereby

attached for your perusal. Please look at it and do not hesitate to contact us in case you have any

queries.

Thank you for considering our company for your retirement and estate planning needs. We hope

to hear from you in the near future.

Yours very truly,

Financial analyst

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

RETIREMENT AND ESTATE PLANNING ASSIGNMENT 4

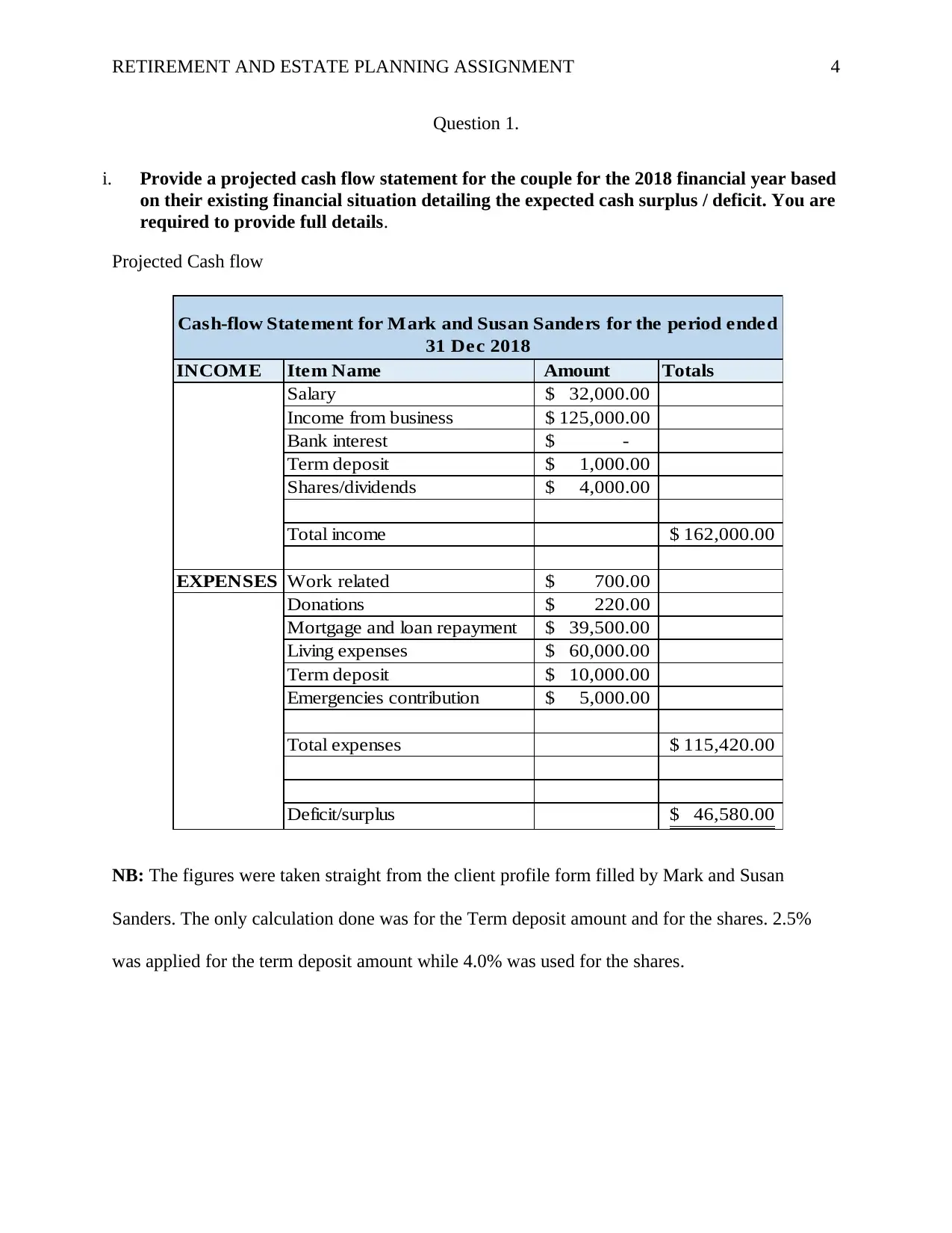

Question 1.

i. Provide a projected cash flow statement for the couple for the 2018 financial year based

on their existing financial situation detailing the expected cash surplus / deficit. You are

required to provide full details.

Projected Cash flow

INCOME Item Name Amount Totals

Salary 32,000.00$

Income from business 125,000.00$

Bank interest -$

Term deposit 1,000.00$

Shares/dividends 4,000.00$

Total income 162,000.00$

EXPENSES Work related 700.00$

Donations 220.00$

Mortgage and loan repayment 39,500.00$

Living expenses 60,000.00$

Term deposit 10,000.00$

Emergencies contribution 5,000.00$

Total expenses 115,420.00$

Deficit/surplus 46,580.00$

Cash-flow Statement for Mark and Susan Sanders for the period ended

31 Dec 2018

NB: The figures were taken straight from the client profile form filled by Mark and Susan

Sanders. The only calculation done was for the Term deposit amount and for the shares. 2.5%

was applied for the term deposit amount while 4.0% was used for the shares.

Question 1.

i. Provide a projected cash flow statement for the couple for the 2018 financial year based

on their existing financial situation detailing the expected cash surplus / deficit. You are

required to provide full details.

Projected Cash flow

INCOME Item Name Amount Totals

Salary 32,000.00$

Income from business 125,000.00$

Bank interest -$

Term deposit 1,000.00$

Shares/dividends 4,000.00$

Total income 162,000.00$

EXPENSES Work related 700.00$

Donations 220.00$

Mortgage and loan repayment 39,500.00$

Living expenses 60,000.00$

Term deposit 10,000.00$

Emergencies contribution 5,000.00$

Total expenses 115,420.00$

Deficit/surplus 46,580.00$

Cash-flow Statement for Mark and Susan Sanders for the period ended

31 Dec 2018

NB: The figures were taken straight from the client profile form filled by Mark and Susan

Sanders. The only calculation done was for the Term deposit amount and for the shares. 2.5%

was applied for the term deposit amount while 4.0% was used for the shares.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

RETIREMENT AND ESTATE PLANNING ASSIGNMENT 5

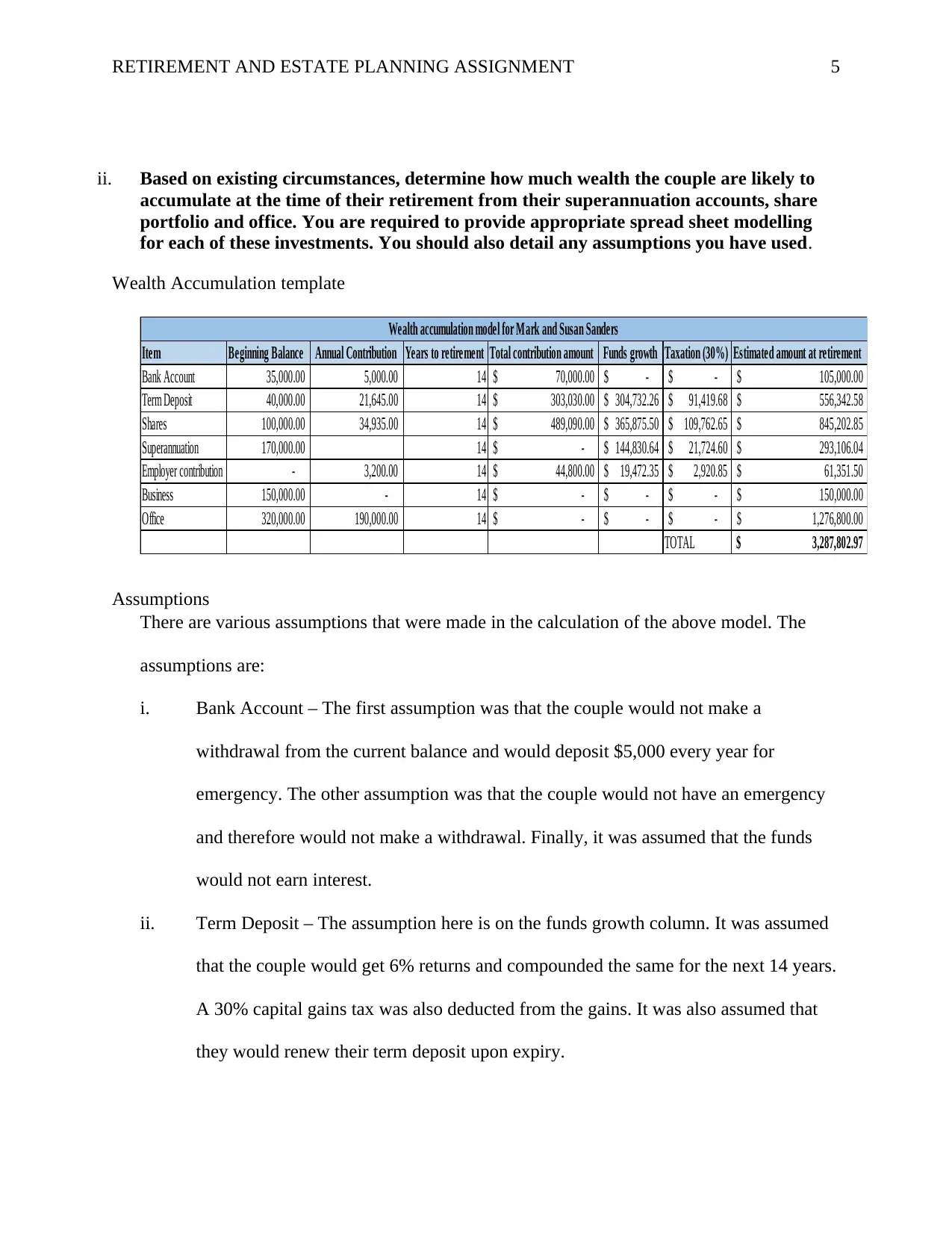

ii. Based on existing circumstances, determine how much wealth the couple are likely to

accumulate at the time of their retirement from their superannuation accounts, share

portfolio and office. You are required to provide appropriate spread sheet modelling

for each of these investments. You should also detail any assumptions you have used.

Wealth Accumulation template

Item Beginning Balance Annual Contribution Years to retirement Total contribution amount Funds growth Taxation (30%) Estimated amount at retirement

Bank Account 35,000.00 5,000.00 14 70,000.00$ -$ -$ 105,000.00$

Term Deposit 40,000.00 21,645.00 14 303,030.00$ 304,732.26$ 91,419.68$ 556,342.58$

Shares 100,000.00 34,935.00 14 489,090.00$ 365,875.50$ 109,762.65$ 845,202.85$

Superannuation 170,000.00 14 -$ 144,830.64$ 21,724.60$ 293,106.04$

Employer contribution - 3,200.00 14 44,800.00$ 19,472.35$ 2,920.85$ 61,351.50$

Business 150,000.00 - 14 -$ -$ -$ 150,000.00$

Office 320,000.00 190,000.00 14 -$ -$ -$ 1,276,800.00$

TOTAL 3,287,802.97$

Wealth accumulation model for Mark and Susan Sanders

Assumptions

There are various assumptions that were made in the calculation of the above model. The

assumptions are:

i. Bank Account – The first assumption was that the couple would not make a

withdrawal from the current balance and would deposit $5,000 every year for

emergency. The other assumption was that the couple would not have an emergency

and therefore would not make a withdrawal. Finally, it was assumed that the funds

would not earn interest.

ii. Term Deposit – The assumption here is on the funds growth column. It was assumed

that the couple would get 6% returns and compounded the same for the next 14 years.

A 30% capital gains tax was also deducted from the gains. It was also assumed that

they would renew their term deposit upon expiry.

ii. Based on existing circumstances, determine how much wealth the couple are likely to

accumulate at the time of their retirement from their superannuation accounts, share

portfolio and office. You are required to provide appropriate spread sheet modelling

for each of these investments. You should also detail any assumptions you have used.

Wealth Accumulation template

Item Beginning Balance Annual Contribution Years to retirement Total contribution amount Funds growth Taxation (30%) Estimated amount at retirement

Bank Account 35,000.00 5,000.00 14 70,000.00$ -$ -$ 105,000.00$

Term Deposit 40,000.00 21,645.00 14 303,030.00$ 304,732.26$ 91,419.68$ 556,342.58$

Shares 100,000.00 34,935.00 14 489,090.00$ 365,875.50$ 109,762.65$ 845,202.85$

Superannuation 170,000.00 14 -$ 144,830.64$ 21,724.60$ 293,106.04$

Employer contribution - 3,200.00 14 44,800.00$ 19,472.35$ 2,920.85$ 61,351.50$

Business 150,000.00 - 14 -$ -$ -$ 150,000.00$

Office 320,000.00 190,000.00 14 -$ -$ -$ 1,276,800.00$

TOTAL 3,287,802.97$

Wealth accumulation model for Mark and Susan Sanders

Assumptions

There are various assumptions that were made in the calculation of the above model. The

assumptions are:

i. Bank Account – The first assumption was that the couple would not make a

withdrawal from the current balance and would deposit $5,000 every year for

emergency. The other assumption was that the couple would not have an emergency

and therefore would not make a withdrawal. Finally, it was assumed that the funds

would not earn interest.

ii. Term Deposit – The assumption here is on the funds growth column. It was assumed

that the couple would get 6% returns and compounded the same for the next 14 years.

A 30% capital gains tax was also deducted from the gains. It was also assumed that

they would renew their term deposit upon expiry.

RETIREMENT AND ESTATE PLANNING ASSIGNMENT 6

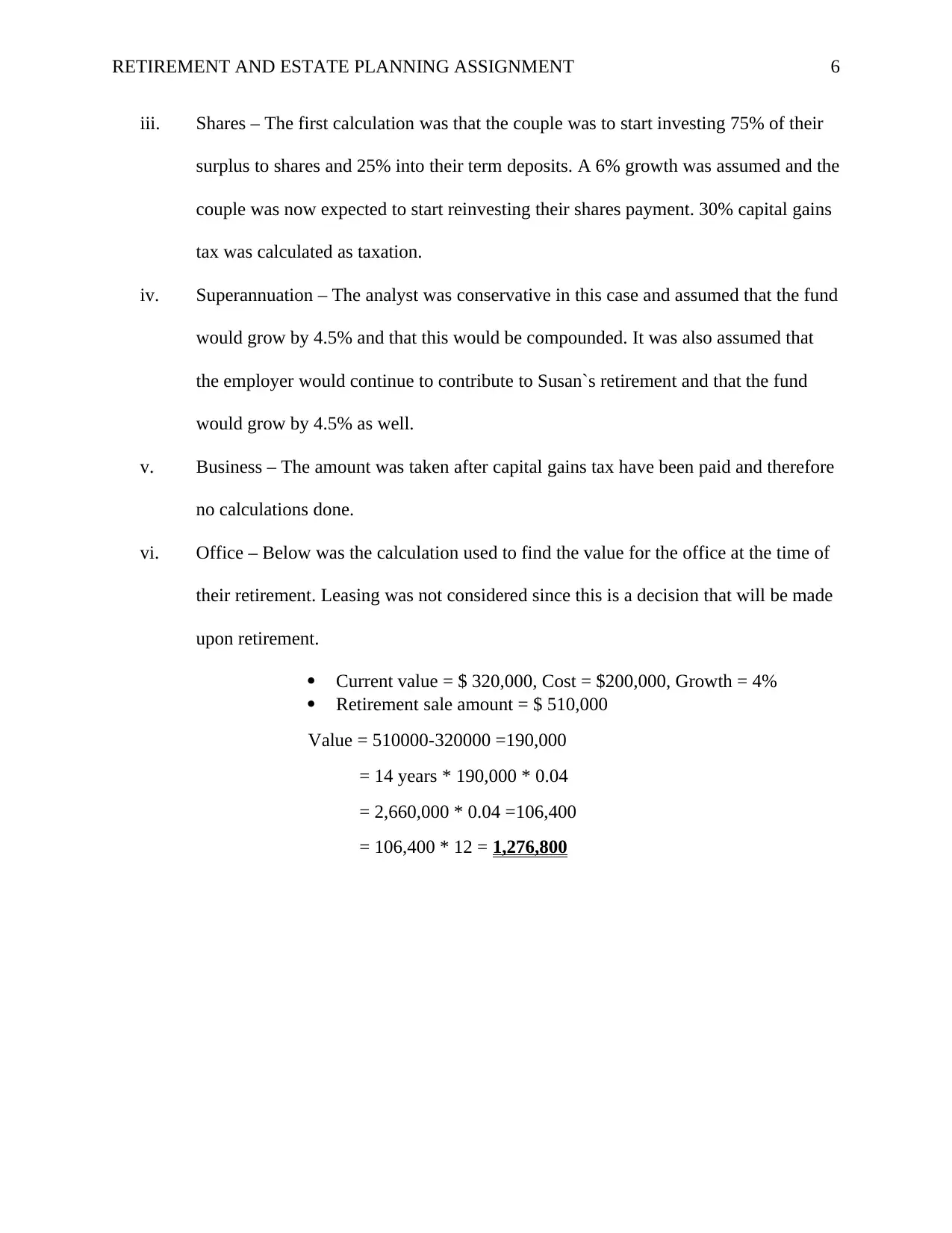

iii. Shares – The first calculation was that the couple was to start investing 75% of their

surplus to shares and 25% into their term deposits. A 6% growth was assumed and the

couple was now expected to start reinvesting their shares payment. 30% capital gains

tax was calculated as taxation.

iv. Superannuation – The analyst was conservative in this case and assumed that the fund

would grow by 4.5% and that this would be compounded. It was also assumed that

the employer would continue to contribute to Susan`s retirement and that the fund

would grow by 4.5% as well.

v. Business – The amount was taken after capital gains tax have been paid and therefore

no calculations done.

vi. Office – Below was the calculation used to find the value for the office at the time of

their retirement. Leasing was not considered since this is a decision that will be made

upon retirement.

Current value = $ 320,000, Cost = $200,000, Growth = 4%

Retirement sale amount = $ 510,000

Value = 510000-320000 =190,000

= 14 years * 190,000 * 0.04

= 2,660,000 * 0.04 =106,400

= 106,400 * 12 = 1,276,800

iii. Shares – The first calculation was that the couple was to start investing 75% of their

surplus to shares and 25% into their term deposits. A 6% growth was assumed and the

couple was now expected to start reinvesting their shares payment. 30% capital gains

tax was calculated as taxation.

iv. Superannuation – The analyst was conservative in this case and assumed that the fund

would grow by 4.5% and that this would be compounded. It was also assumed that

the employer would continue to contribute to Susan`s retirement and that the fund

would grow by 4.5% as well.

v. Business – The amount was taken after capital gains tax have been paid and therefore

no calculations done.

vi. Office – Below was the calculation used to find the value for the office at the time of

their retirement. Leasing was not considered since this is a decision that will be made

upon retirement.

Current value = $ 320,000, Cost = $200,000, Growth = 4%

Retirement sale amount = $ 510,000

Value = 510000-320000 =190,000

= 14 years * 190,000 * 0.04

= 2,660,000 * 0.04 =106,400

= 106,400 * 12 = 1,276,800

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

RETIREMENT AND ESTATE PLANNING ASSIGNMENT 7

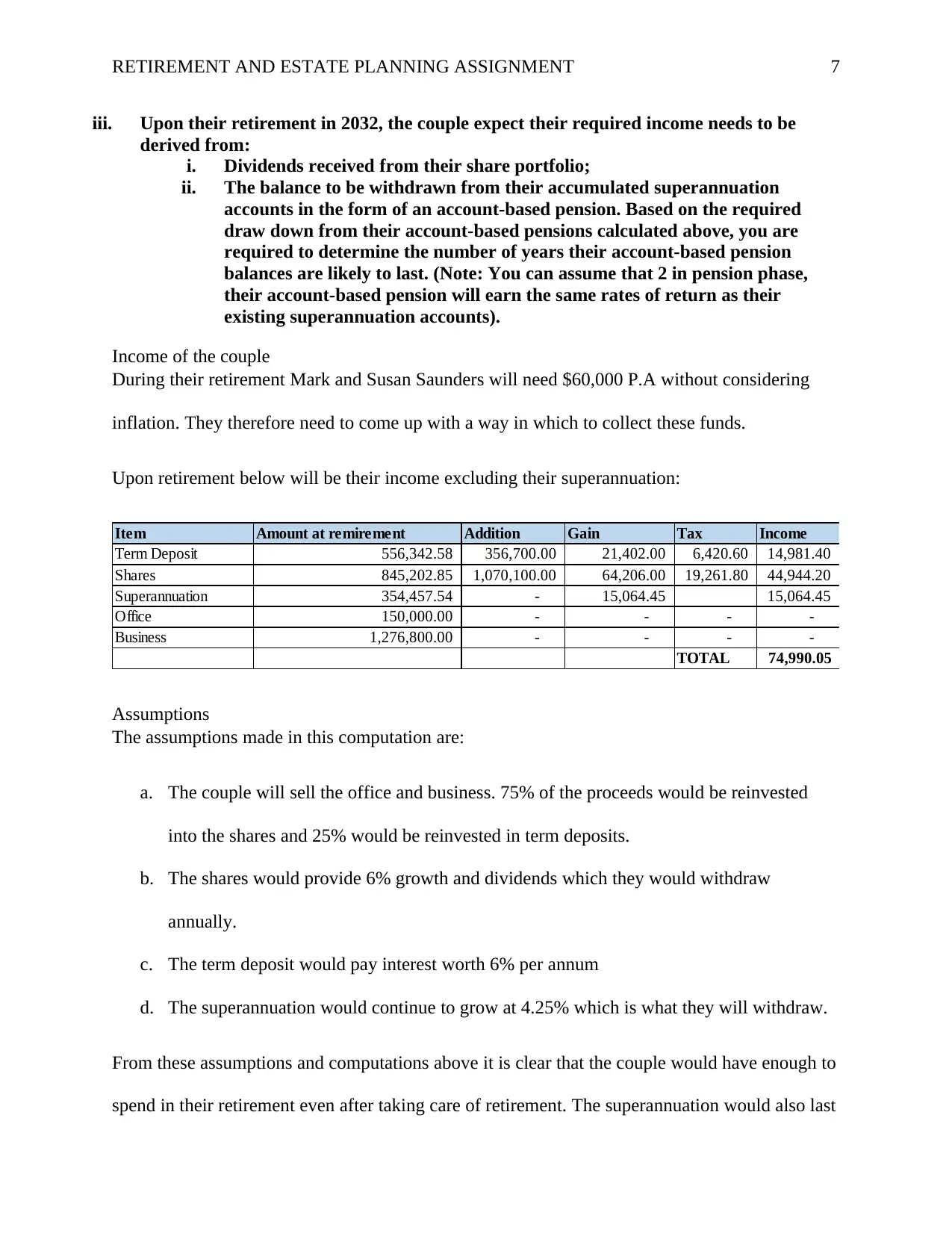

iii. Upon their retirement in 2032, the couple expect their required income needs to be

derived from:

i. Dividends received from their share portfolio;

ii. The balance to be withdrawn from their accumulated superannuation

accounts in the form of an account-based pension. Based on the required

draw down from their account-based pensions calculated above, you are

required to determine the number of years their account-based pension

balances are likely to last. (Note: You can assume that 2 in pension phase,

their account-based pension will earn the same rates of return as their

existing superannuation accounts).

Income of the couple

During their retirement Mark and Susan Saunders will need $60,000 P.A without considering

inflation. They therefore need to come up with a way in which to collect these funds.

Upon retirement below will be their income excluding their superannuation:

Item Amount at remirement Addition Gain Tax Income

Term Deposit 556,342.58 356,700.00 21,402.00 6,420.60 14,981.40

Shares 845,202.85 1,070,100.00 64,206.00 19,261.80 44,944.20

Superannuation 354,457.54 - 15,064.45 15,064.45

Office 150,000.00 - - - -

Business 1,276,800.00 - - - -

TOTAL 74,990.05

Assumptions

The assumptions made in this computation are:

a. The couple will sell the office and business. 75% of the proceeds would be reinvested

into the shares and 25% would be reinvested in term deposits.

b. The shares would provide 6% growth and dividends which they would withdraw

annually.

c. The term deposit would pay interest worth 6% per annum

d. The superannuation would continue to grow at 4.25% which is what they will withdraw.

From these assumptions and computations above it is clear that the couple would have enough to

spend in their retirement even after taking care of retirement. The superannuation would also last

iii. Upon their retirement in 2032, the couple expect their required income needs to be

derived from:

i. Dividends received from their share portfolio;

ii. The balance to be withdrawn from their accumulated superannuation

accounts in the form of an account-based pension. Based on the required

draw down from their account-based pensions calculated above, you are

required to determine the number of years their account-based pension

balances are likely to last. (Note: You can assume that 2 in pension phase,

their account-based pension will earn the same rates of return as their

existing superannuation accounts).

Income of the couple

During their retirement Mark and Susan Saunders will need $60,000 P.A without considering

inflation. They therefore need to come up with a way in which to collect these funds.

Upon retirement below will be their income excluding their superannuation:

Item Amount at remirement Addition Gain Tax Income

Term Deposit 556,342.58 356,700.00 21,402.00 6,420.60 14,981.40

Shares 845,202.85 1,070,100.00 64,206.00 19,261.80 44,944.20

Superannuation 354,457.54 - 15,064.45 15,064.45

Office 150,000.00 - - - -

Business 1,276,800.00 - - - -

TOTAL 74,990.05

Assumptions

The assumptions made in this computation are:

a. The couple will sell the office and business. 75% of the proceeds would be reinvested

into the shares and 25% would be reinvested in term deposits.

b. The shares would provide 6% growth and dividends which they would withdraw

annually.

c. The term deposit would pay interest worth 6% per annum

d. The superannuation would continue to grow at 4.25% which is what they will withdraw.

From these assumptions and computations above it is clear that the couple would have enough to

spend in their retirement even after taking care of retirement. The superannuation would also last

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

RETIREMENT AND ESTATE PLANNING ASSIGNMENT 8

them a lifetime unless where they have to withdraw the lump-sum. However, if they treat it as an

annuity and the shares continue performing they will use their dividends for a lifetime.

iv. Explain fully what strategies you would recommend to assist Susan and Mark increase

wealth within their superannuation accounts and their overall wealth position upon

retirement. As previously noted, the couple’s objective is to maximize wealth within

their SMSF for retirement.

Note: You are required to explain each strategy, provide a rationale for its

recommendation and discuss benefits and risks. (You are to base your strategies on

existing legislation. You should not consider any form of transition to retirement

strategy. The couple do not wish to borrow any further funds).

Strategies Advised

As seen in previous answers it’s clear that Mark and Susan Saunders have enough cash to

invest and make enough returns to enable them continue living the same lifestyle they are living

now. They can however employ several strategies to increase their savings and revenue. These

strategies will basically help the couple to reduce the amount of taxes they pay. Some of these

strategies include:

i. Commence on account based pension

This is one of the most effective strategies during the reduction of tax in retirement

(Diamond, 2011). Fund earnings are branded free from the time of the commencement of

pension from the super fund since the 15% instilled tax is no longer part of the fund earnings.

Anybody above the age of 60 years, it does not matter income amount drawn but the pension

income automatically becomes tax free

Fund earnings for people aged between the ages of 55-59 could also be tax free but a

small amount of payable tax on pension before turning 60 years. It is always wise to specify a

certain minimum percentage to be drawn as income from the fund balance for the year since as

one gets older, their minimum percentage increases. This strategy requires enough knowledge on

them a lifetime unless where they have to withdraw the lump-sum. However, if they treat it as an

annuity and the shares continue performing they will use their dividends for a lifetime.

iv. Explain fully what strategies you would recommend to assist Susan and Mark increase

wealth within their superannuation accounts and their overall wealth position upon

retirement. As previously noted, the couple’s objective is to maximize wealth within

their SMSF for retirement.

Note: You are required to explain each strategy, provide a rationale for its

recommendation and discuss benefits and risks. (You are to base your strategies on

existing legislation. You should not consider any form of transition to retirement

strategy. The couple do not wish to borrow any further funds).

Strategies Advised

As seen in previous answers it’s clear that Mark and Susan Saunders have enough cash to

invest and make enough returns to enable them continue living the same lifestyle they are living

now. They can however employ several strategies to increase their savings and revenue. These

strategies will basically help the couple to reduce the amount of taxes they pay. Some of these

strategies include:

i. Commence on account based pension

This is one of the most effective strategies during the reduction of tax in retirement

(Diamond, 2011). Fund earnings are branded free from the time of the commencement of

pension from the super fund since the 15% instilled tax is no longer part of the fund earnings.

Anybody above the age of 60 years, it does not matter income amount drawn but the pension

income automatically becomes tax free

Fund earnings for people aged between the ages of 55-59 could also be tax free but a

small amount of payable tax on pension before turning 60 years. It is always wise to specify a

certain minimum percentage to be drawn as income from the fund balance for the year since as

one gets older, their minimum percentage increases. This strategy requires enough knowledge on

RETIREMENT AND ESTATE PLANNING ASSIGNMENT 9

annual pension factors that affect payment. If one has other sources of income, definitely they

are most likely to have more income than exactly what they require.

ii. Consider using a self-managed super fund (SMSF)

Other super funds don’t match the SMSF strategy since it provides flexibility and greater

scope for tax planning. The application of the self-managed super fund leads to the availability of

more avenues up to retirement. People with no SMSF always find themselves trying to eliminate

the 15% tax by commencing an account-based pension (Phillips, Cathcart, & Teale, 2007). The

pension income is not necessary since it is drawn with respect to the factors of payment thus the

forceful withdrawal of funds from superannuation before the removal of the 15% earnings tax.

The SMSF can afford the flexibility of increased tax planning therefore the situation is oftently

avoided.

The key to SMSFs tax planning strategies is taking complete control over the investments

of funds and the ability to buy time and sell decisions. The 15% tax earnings can be offloaded

from the franking credits got from the Australian share dividends when tax returns are lodged at

the end of the year. The company’s already paid tax paid to shareholders before dividends is

represented by franking credits also known as imputation credits

Question 2

The couple have a strong interest to ensure that they invest in a socially responsible

manner. They want to ensure that they do not invest into any companies that negatively

impact upon the environment, health (eg tobacco) or society. However, they are also

concerned that if they do invest in a socially responsible manner, whether the return

generated within their super fund is likely to be lower.

Discuss what investing in a social responsible manner means and the different

approaches available that they couple might consider. You are also required to

examine the the literature to determine whether investing in a socially responsible

manner does tend to lead to lower returns being generated.

annual pension factors that affect payment. If one has other sources of income, definitely they

are most likely to have more income than exactly what they require.

ii. Consider using a self-managed super fund (SMSF)

Other super funds don’t match the SMSF strategy since it provides flexibility and greater

scope for tax planning. The application of the self-managed super fund leads to the availability of

more avenues up to retirement. People with no SMSF always find themselves trying to eliminate

the 15% tax by commencing an account-based pension (Phillips, Cathcart, & Teale, 2007). The

pension income is not necessary since it is drawn with respect to the factors of payment thus the

forceful withdrawal of funds from superannuation before the removal of the 15% earnings tax.

The SMSF can afford the flexibility of increased tax planning therefore the situation is oftently

avoided.

The key to SMSFs tax planning strategies is taking complete control over the investments

of funds and the ability to buy time and sell decisions. The 15% tax earnings can be offloaded

from the franking credits got from the Australian share dividends when tax returns are lodged at

the end of the year. The company’s already paid tax paid to shareholders before dividends is

represented by franking credits also known as imputation credits

Question 2

The couple have a strong interest to ensure that they invest in a socially responsible

manner. They want to ensure that they do not invest into any companies that negatively

impact upon the environment, health (eg tobacco) or society. However, they are also

concerned that if they do invest in a socially responsible manner, whether the return

generated within their super fund is likely to be lower.

Discuss what investing in a social responsible manner means and the different

approaches available that they couple might consider. You are also required to

examine the the literature to determine whether investing in a socially responsible

manner does tend to lead to lower returns being generated.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

RETIREMENT AND ESTATE PLANNING ASSIGNMENT 10

Investing in a socially responsible manner

It is crucial that one plans for retirement especially in Australia (O’Brien-Pallas, Duffield,

& Alksnis, 2004). Investing in a socially responsible manner is one way of planning for

retirement and it refers to the art of investing in businesses that operate in an ethical manner

following a certain code that does not harm the environment nor their clients (Schueth, 2003).

The companies in this category do not create profits through the use of less desirable actions or

even placement of items. The personal values of an investor need to be in-line with the company

that they are investing in for it to be considered value investing. One key misconception with this

type of investing is whether it leads to reduced returns. It is crucial to note that what this kind of

investing does is, it reduces the amount of companies that one can invest in.

Socially investing has grown over the ages. At the beginning, it comprised of just not

investing in a company that deals in drugs, alcohol and gambling. This scope has however grown

to include other matters including environmental friendliness (Dahlsrud, 2009). Investors doing

social investing now have to consider other factors commonly referred to as ESG or Economic,

Social and Governance factors.

Authors, researchers and scholars are divided on the topic of investing in a socially

responsible manner especially on returns. People who want to invest in a socially responsible

manner are those who are attached to their finances and want to invest in a cause (Friedman, &

Miles, 2001). In most cases they are willing to forego profits so as to maintain their values while

supporting their cause. It is expected that business which are socially responsible will give

returns that are comparable to the market. It is however important to note that these businesses

also experience the same ups and downs just like other businesses in the market. When

opportunities arise a socially responsible investor will have few choices with one who really

Investing in a socially responsible manner

It is crucial that one plans for retirement especially in Australia (O’Brien-Pallas, Duffield,

& Alksnis, 2004). Investing in a socially responsible manner is one way of planning for

retirement and it refers to the art of investing in businesses that operate in an ethical manner

following a certain code that does not harm the environment nor their clients (Schueth, 2003).

The companies in this category do not create profits through the use of less desirable actions or

even placement of items. The personal values of an investor need to be in-line with the company

that they are investing in for it to be considered value investing. One key misconception with this

type of investing is whether it leads to reduced returns. It is crucial to note that what this kind of

investing does is, it reduces the amount of companies that one can invest in.

Socially investing has grown over the ages. At the beginning, it comprised of just not

investing in a company that deals in drugs, alcohol and gambling. This scope has however grown

to include other matters including environmental friendliness (Dahlsrud, 2009). Investors doing

social investing now have to consider other factors commonly referred to as ESG or Economic,

Social and Governance factors.

Authors, researchers and scholars are divided on the topic of investing in a socially

responsible manner especially on returns. People who want to invest in a socially responsible

manner are those who are attached to their finances and want to invest in a cause (Friedman, &

Miles, 2001). In most cases they are willing to forego profits so as to maintain their values while

supporting their cause. It is expected that business which are socially responsible will give

returns that are comparable to the market. It is however important to note that these businesses

also experience the same ups and downs just like other businesses in the market. When

opportunities arise a socially responsible investor will have few choices with one who really

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

RETIREMENT AND ESTATE PLANNING ASSIGNMENT 11

doesn’t care about the company business. This is likely to be the key difference between the

returns for these two businesses.

An investor interested in socially responsible investing needs to consider their hunger for

returns (Friedman, & Miles, 2001). Are they willing to accept low returns due to their values and

CSR support is the question they need to answer when making the decision. If they choose to

proceed they should then scan the CSR activities of a company, its business model and possible

effects to its customers as the first step of analyzing a company. Once all these factors have been

considered the analysis should now look at the fundamentals and technicalities of the stock

before investing.

doesn’t care about the company business. This is likely to be the key difference between the

returns for these two businesses.

An investor interested in socially responsible investing needs to consider their hunger for

returns (Friedman, & Miles, 2001). Are they willing to accept low returns due to their values and

CSR support is the question they need to answer when making the decision. If they choose to

proceed they should then scan the CSR activities of a company, its business model and possible

effects to its customers as the first step of analyzing a company. Once all these factors have been

considered the analysis should now look at the fundamentals and technicalities of the stock

before investing.

RETIREMENT AND ESTATE PLANNING ASSIGNMENT 12

References

Dahlsrud, A. (2009). How corporate social responsibility is defined: an analysis of 37

definitions. Corporate social responsibility and environmental management, 15(1), 1-13.

Diamond, P. (2011). Economic theory and tax and pension policies. Economic Record, 87, 2-22.

Friedman, A. L., & Miles, S. (2001). Socially responsible investment and corporate social and

environmental reporting in the UK: an exploratory study. The British Accounting

Review, 33(4), 523-548.

O’Brien-Pallas, L., Duffield, C., & Alksnis, C. (2004). Who will be there to nurse?: Retention of

nurses nearing retirement. Journal of Nursing Administration, 34(6), 298-302.

Phillips, P. J., Cathcart, A., & Teale, J. (2007). The Diversification and Performance of Self‐

Managed Superannuation Funds. Australian Economic Review, 40(4), 339-352.

Schueth, S. (2003). Socially responsible investing in the United States. Journal of business

ethics, 43(3), 189-194.

References

Dahlsrud, A. (2009). How corporate social responsibility is defined: an analysis of 37

definitions. Corporate social responsibility and environmental management, 15(1), 1-13.

Diamond, P. (2011). Economic theory and tax and pension policies. Economic Record, 87, 2-22.

Friedman, A. L., & Miles, S. (2001). Socially responsible investment and corporate social and

environmental reporting in the UK: an exploratory study. The British Accounting

Review, 33(4), 523-548.

O’Brien-Pallas, L., Duffield, C., & Alksnis, C. (2004). Who will be there to nurse?: Retention of

nurses nearing retirement. Journal of Nursing Administration, 34(6), 298-302.

Phillips, P. J., Cathcart, A., & Teale, J. (2007). The Diversification and Performance of Self‐

Managed Superannuation Funds. Australian Economic Review, 40(4), 339-352.

Schueth, S. (2003). Socially responsible investing in the United States. Journal of business

ethics, 43(3), 189-194.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.