COR167e Managing Your Personal Finances Assignment Solution

VerifiedAdded on 2023/06/08

|17

|3396

|211

Homework Assignment

AI Summary

This document presents a comprehensive solution to a financial planning assignment, likely for a course like SUSS COR167e. It addresses key aspects of personal finance, including wealth grounding, protection, and retirement planning. The assignment solution includes detailed answers to questions, financial ratio analysis (like debt-equity and acid-test ratios), tax calculations, and retirement benefit assessments. The solution also incorporates case studies and analysis of insurance policies, including critical illness coverage and life annuities. Furthermore, the document provides answers to multiple-choice questions related to retirement planning, CPF, and insurance, providing a well-rounded overview of personal finance concepts.

Running head: FINANCIAL PLANNING

Financial Planning

Name of the student:

Name of the University:

Authors Note:

Financial Planning

Name of the student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL PLANNING

Table of Contents

Assignment 1..............................................................................................................................3

Answer To Question 1:..............................................................................................................3

(a)(i):......................................................................................................................................3

(a)(ii):.....................................................................................................................................3

(b)(i):......................................................................................................................................4

(b)(ii):.....................................................................................................................................4

(c):..........................................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer to question 3:.................................................................................................................7

Answer questions 3b (i):........................................................................................................9

Answer questions 3b(ii):........................................................................................................9

Assignment 2............................................................................................................................10

Answer to Question 1...............................................................................................................10

Answer to Question 1(a):.....................................................................................................10

Answer to 1(b)(i):.................................................................................................................11

Answer to question 1(b)(ii):.................................................................................................11

Answer to question 1 C:.......................................................................................................12

Answer to question 1 (d):.....................................................................................................12

Question 2 (a):..........................................................................................................................13

Answer to Question 3:..............................................................................................................14

Table of Contents

Assignment 1..............................................................................................................................3

Answer To Question 1:..............................................................................................................3

(a)(i):......................................................................................................................................3

(a)(ii):.....................................................................................................................................3

(b)(i):......................................................................................................................................4

(b)(ii):.....................................................................................................................................4

(c):..........................................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer to question 3:.................................................................................................................7

Answer questions 3b (i):........................................................................................................9

Answer questions 3b(ii):........................................................................................................9

Assignment 2............................................................................................................................10

Answer to Question 1...............................................................................................................10

Answer to Question 1(a):.....................................................................................................10

Answer to 1(b)(i):.................................................................................................................11

Answer to question 1(b)(ii):.................................................................................................11

Answer to question 1 C:.......................................................................................................12

Answer to question 1 (d):.....................................................................................................12

Question 2 (a):..........................................................................................................................13

Answer to Question 3:..............................................................................................................14

2FINANCIAL PLANNING

Answer to question 3(a):.....................................................................................................14

Answer to question 3(b):......................................................................................................14

Answer to Question 3 C:......................................................................................................14

Answer to question 3 d:........................................................................................................15

Reference..................................................................................................................................16

Answer to question 3(a):.....................................................................................................14

Answer to question 3(b):......................................................................................................14

Answer to Question 3 C:......................................................................................................14

Answer to question 3 d:........................................................................................................15

Reference..................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL PLANNING

Assignment 1

Answer To Question 1:

(a)(i):

Mr T, a resident of Singapore, is engaged in the consultancy business. In addition to

that he has some other sources of income. All together the current investment and earning

capacity of the client is healthy. But the investment portfolios and the quantum of

expenditure are inadequate. The income form Royalty and Rental income are quite

substantial but the savings are not done properly, the budget is to be reviewed because to

increase the amount of savings (Kasuma et al., 2017). The potential needs of the asses to

review the budget as there are many deficiencies regarding the investment plan and the

margin or return. In the given case, Mr T has invested in much option from where income are

derived. However, the return in comparison of the investment are not adequate. The budget is

to review to diversify the investment and income generation.

(a)(ii):

Analysing the balance sheet of Mr T it is being identified that, major asset that Mr T

holds laid with the savings and retire fund. The other substantial portion of the assets are

located in two properties. For evaluating the position of the financial statement of an assesse

at first the liquidity is to be considered (Chwieroth, 2015). The liquidity is the ability to pay

certain debts or obligations. In the given case the Assesse liquidity is high as the investment

in the retirement fund and savings as well as fixed deposit investments are substantial to pay

the desired obligations.

Assignment 1

Answer To Question 1:

(a)(i):

Mr T, a resident of Singapore, is engaged in the consultancy business. In addition to

that he has some other sources of income. All together the current investment and earning

capacity of the client is healthy. But the investment portfolios and the quantum of

expenditure are inadequate. The income form Royalty and Rental income are quite

substantial but the savings are not done properly, the budget is to be reviewed because to

increase the amount of savings (Kasuma et al., 2017). The potential needs of the asses to

review the budget as there are many deficiencies regarding the investment plan and the

margin or return. In the given case, Mr T has invested in much option from where income are

derived. However, the return in comparison of the investment are not adequate. The budget is

to review to diversify the investment and income generation.

(a)(ii):

Analysing the balance sheet of Mr T it is being identified that, major asset that Mr T

holds laid with the savings and retire fund. The other substantial portion of the assets are

located in two properties. For evaluating the position of the financial statement of an assesse

at first the liquidity is to be considered (Chwieroth, 2015). The liquidity is the ability to pay

certain debts or obligations. In the given case the Assesse liquidity is high as the investment

in the retirement fund and savings as well as fixed deposit investments are substantial to pay

the desired obligations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL PLANNING

(b)(i):

___“FALSE”____ A person’s investment assets to net worth ratio should logically decrease,

as he/she grows older.

_____“FALSE”_____ Cash management helps you to manage your cash on a day-to-day

basis; hence, it has no relation with long-term financial goals.

_____“TRUE”_____ The rule of “72” says that, at 10% interest, it takes a little more than 7

years to double your money.

_______“TRUE”___ Liabilities are normally reported at their current fair market value.

_____“TRUE”_____ If you can cut your spending by 5% that would be equivalent to getting

a 5% raise.

______“FALSE”____ When budgeting monthly income, you should exclude one-off items

such as a 3- month year-end bonus.

______“FALSE”____ When a person’s cash-flow statement shows a surplus, this means that

funds are ready to be used.

_____“TRUE”_____ No one financial ratio tells the whole story; hence, we need to look at a

few ratios to get an overall picture of an individual’s financial health.

(b)(ii):

Mr T can state the funds are adequate by calculating some key financial ratios. The

ratios provide some key beneficial analysis of the financial statements such as debt coverage,

current ratio, acid test ration, and others. The ratios depicts the financial viability of the

client. In case of any sudden needs of the assesse or any investment requirement for

speculative income or sudden requirement to pay off any emergency cost such as medical

expense or any kinds of loss the ability of the assesse is determined by current ratios and the

(b)(i):

___“FALSE”____ A person’s investment assets to net worth ratio should logically decrease,

as he/she grows older.

_____“FALSE”_____ Cash management helps you to manage your cash on a day-to-day

basis; hence, it has no relation with long-term financial goals.

_____“TRUE”_____ The rule of “72” says that, at 10% interest, it takes a little more than 7

years to double your money.

_______“TRUE”___ Liabilities are normally reported at their current fair market value.

_____“TRUE”_____ If you can cut your spending by 5% that would be equivalent to getting

a 5% raise.

______“FALSE”____ When budgeting monthly income, you should exclude one-off items

such as a 3- month year-end bonus.

______“FALSE”____ When a person’s cash-flow statement shows a surplus, this means that

funds are ready to be used.

_____“TRUE”_____ No one financial ratio tells the whole story; hence, we need to look at a

few ratios to get an overall picture of an individual’s financial health.

(b)(ii):

Mr T can state the funds are adequate by calculating some key financial ratios. The

ratios provide some key beneficial analysis of the financial statements such as debt coverage,

current ratio, acid test ration, and others. The ratios depicts the financial viability of the

client. In case of any sudden needs of the assesse or any investment requirement for

speculative income or sudden requirement to pay off any emergency cost such as medical

expense or any kinds of loss the ability of the assesse is determined by current ratios and the

5FINANCIAL PLANNING

quick ratios. As this is the difference between the current assets and the current liabilities

(Deng, A., & Chen, 2017).

(c):

The two identified primary ratios are Debt Equity ratio, and Acid Test Ratio,

Debt equity ratio is the measure of the total debt of the assesse in comparison of the total

equity, this ratios shows the financial ability to repaid the dues and other obligations. The

Debt/ Equity will be favourable if it is more than 2. If is lower than 2, then the financial

viability will be considered as weak (Haldane, 2014).

Another key ratio is acid test ration, this is the measure of the short term loan or debt

payment ability. The Acid test ratio of quick ratio will be considered 3 to be good, higher will

be the value priories the financial position of the client.

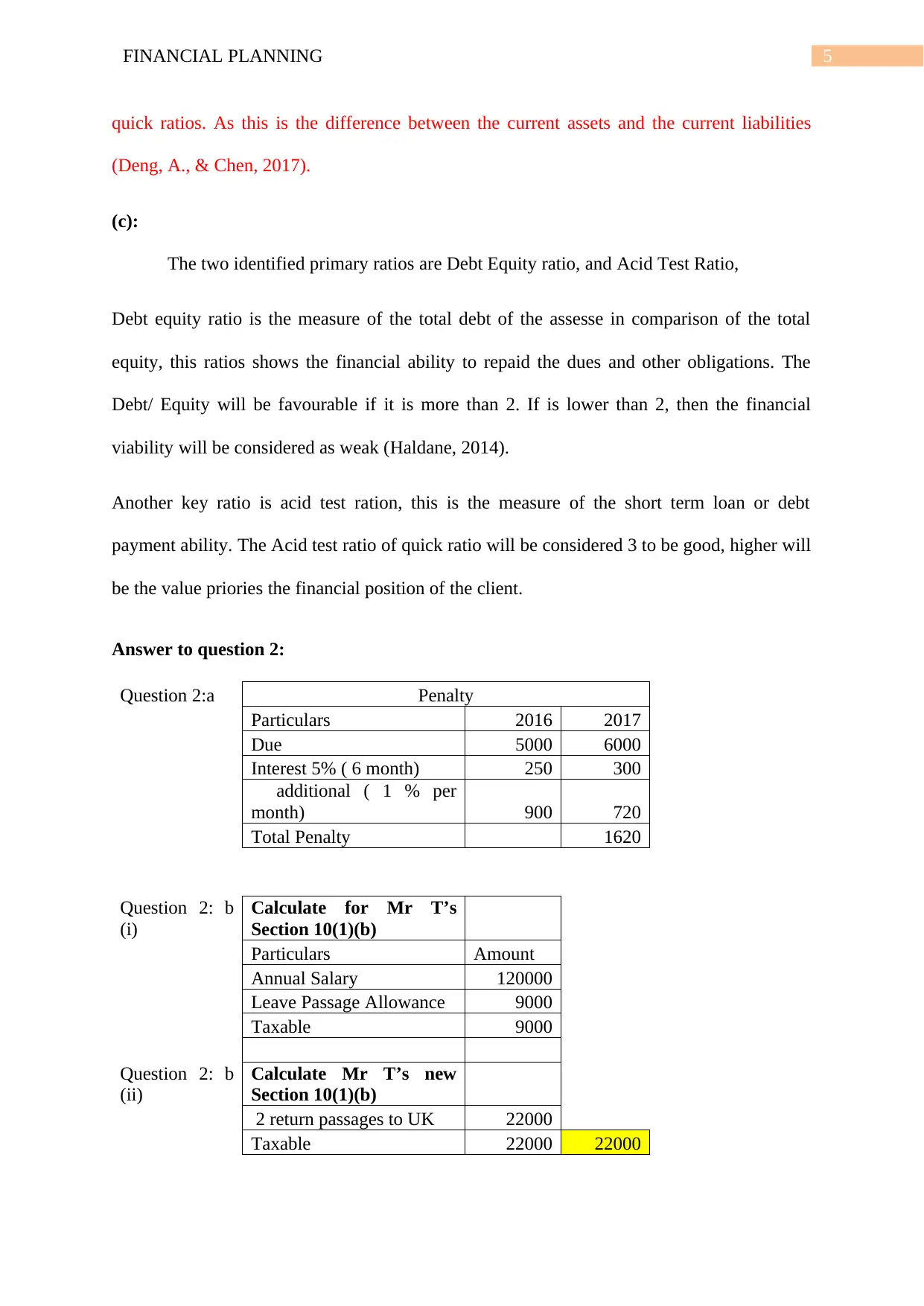

Answer to question 2:

Question 2:a Penalty

Particulars 2016 2017

Due 5000 6000

Interest 5% ( 6 month) 250 300

additional ( 1 % per

month) 900 720

Total Penalty 1620

Question 2: b

(i)

Calculate for Mr T’s

Section 10(1)(b)

Particulars Amount

Annual Salary 120000

Leave Passage Allowance 9000

Taxable 9000

Question 2: b

(ii)

Calculate Mr T’s new

Section 10(1)(b)

2 return passages to UK 22000

Taxable 22000 22000

quick ratios. As this is the difference between the current assets and the current liabilities

(Deng, A., & Chen, 2017).

(c):

The two identified primary ratios are Debt Equity ratio, and Acid Test Ratio,

Debt equity ratio is the measure of the total debt of the assesse in comparison of the total

equity, this ratios shows the financial ability to repaid the dues and other obligations. The

Debt/ Equity will be favourable if it is more than 2. If is lower than 2, then the financial

viability will be considered as weak (Haldane, 2014).

Another key ratio is acid test ration, this is the measure of the short term loan or debt

payment ability. The Acid test ratio of quick ratio will be considered 3 to be good, higher will

be the value priories the financial position of the client.

Answer to question 2:

Question 2:a Penalty

Particulars 2016 2017

Due 5000 6000

Interest 5% ( 6 month) 250 300

additional ( 1 % per

month) 900 720

Total Penalty 1620

Question 2: b

(i)

Calculate for Mr T’s

Section 10(1)(b)

Particulars Amount

Annual Salary 120000

Leave Passage Allowance 9000

Taxable 9000

Question 2: b

(ii)

Calculate Mr T’s new

Section 10(1)(b)

2 return passages to UK 22000

Taxable 22000 22000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL PLANNING

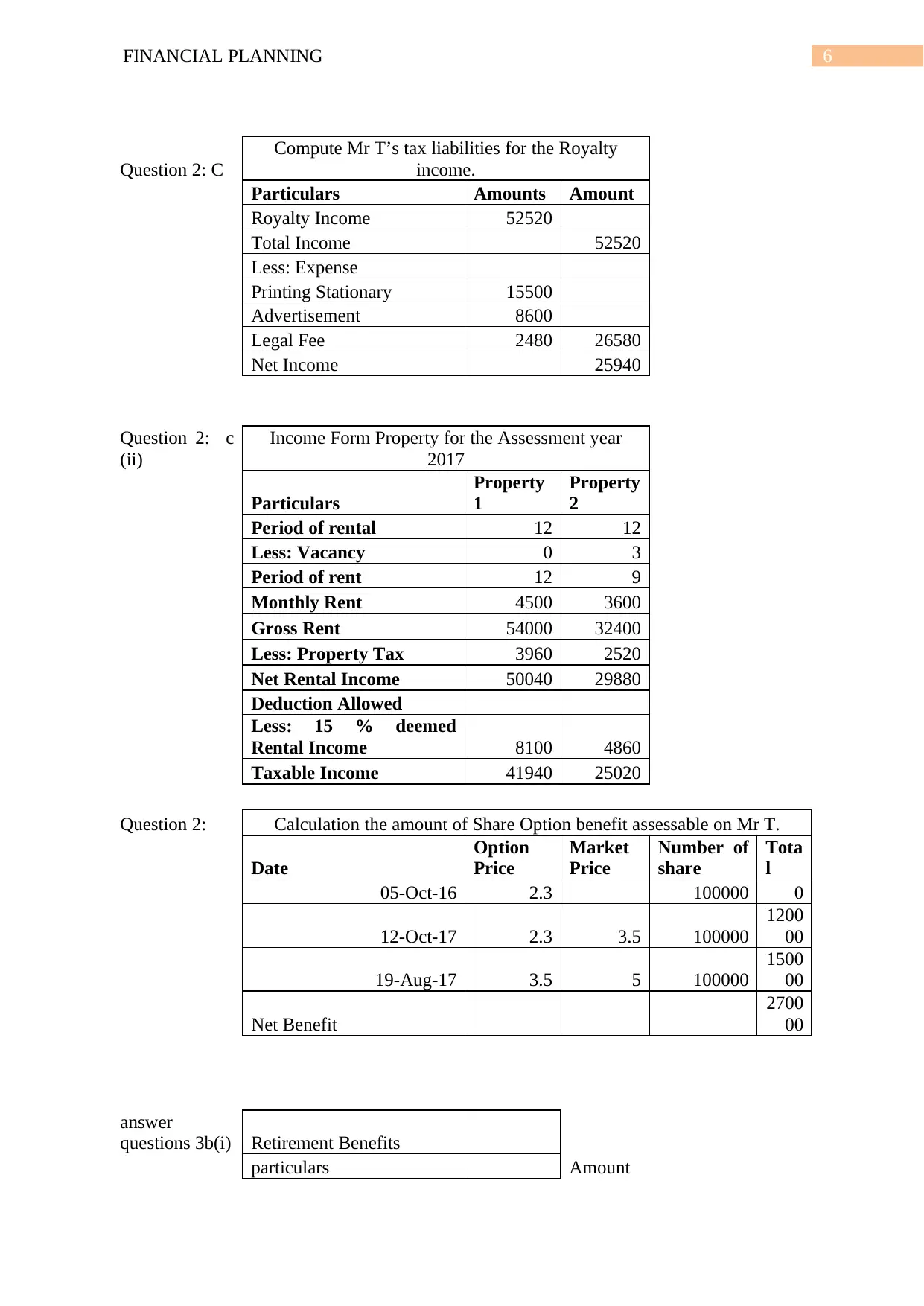

Question 2: C

Compute Mr T’s tax liabilities for the Royalty

income.

Particulars Amounts Amount

Royalty Income 52520

Total Income 52520

Less: Expense

Printing Stationary 15500

Advertisement 8600

Legal Fee 2480 26580

Net Income 25940

Question 2: c

(ii)

Income Form Property for the Assessment year

2017

Particulars

Property

1

Property

2

Period of rental 12 12

Less: Vacancy 0 3

Period of rent 12 9

Monthly Rent 4500 3600

Gross Rent 54000 32400

Less: Property Tax 3960 2520

Net Rental Income 50040 29880

Deduction Allowed

Less: 15 % deemed

Rental Income 8100 4860

Taxable Income 41940 25020

Question 2: Calculation the amount of Share Option benefit assessable on Mr T.

Date

Option

Price

Market

Price

Number of

share

Tota

l

05-Oct-16 2.3 100000 0

12-Oct-17 2.3 3.5 100000

1200

00

19-Aug-17 3.5 5 100000

1500

00

Net Benefit

2700

00

answer

questions 3b(i) Retirement Benefits

particulars Amount

Question 2: C

Compute Mr T’s tax liabilities for the Royalty

income.

Particulars Amounts Amount

Royalty Income 52520

Total Income 52520

Less: Expense

Printing Stationary 15500

Advertisement 8600

Legal Fee 2480 26580

Net Income 25940

Question 2: c

(ii)

Income Form Property for the Assessment year

2017

Particulars

Property

1

Property

2

Period of rental 12 12

Less: Vacancy 0 3

Period of rent 12 9

Monthly Rent 4500 3600

Gross Rent 54000 32400

Less: Property Tax 3960 2520

Net Rental Income 50040 29880

Deduction Allowed

Less: 15 % deemed

Rental Income 8100 4860

Taxable Income 41940 25020

Question 2: Calculation the amount of Share Option benefit assessable on Mr T.

Date

Option

Price

Market

Price

Number of

share

Tota

l

05-Oct-16 2.3 100000 0

12-Oct-17 2.3 3.5 100000

1200

00

19-Aug-17 3.5 5 100000

1500

00

Net Benefit

2700

00

answer

questions 3b(i) Retirement Benefits

particulars Amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL PLANNING

Requirement

$

2,354,000

.00

Current Value

$ -

350,000.0

0

Annuity

$ -

26,000.00

Interest rate 8%

Period 15.00

Future value

$

1,816,214

.15

Inflation

$

3,667,455

.30

Monthly Pension

receivable

investment value

$

1,816,214

.15

Period 30

Rate 8%

Pension

-

110.2576

714

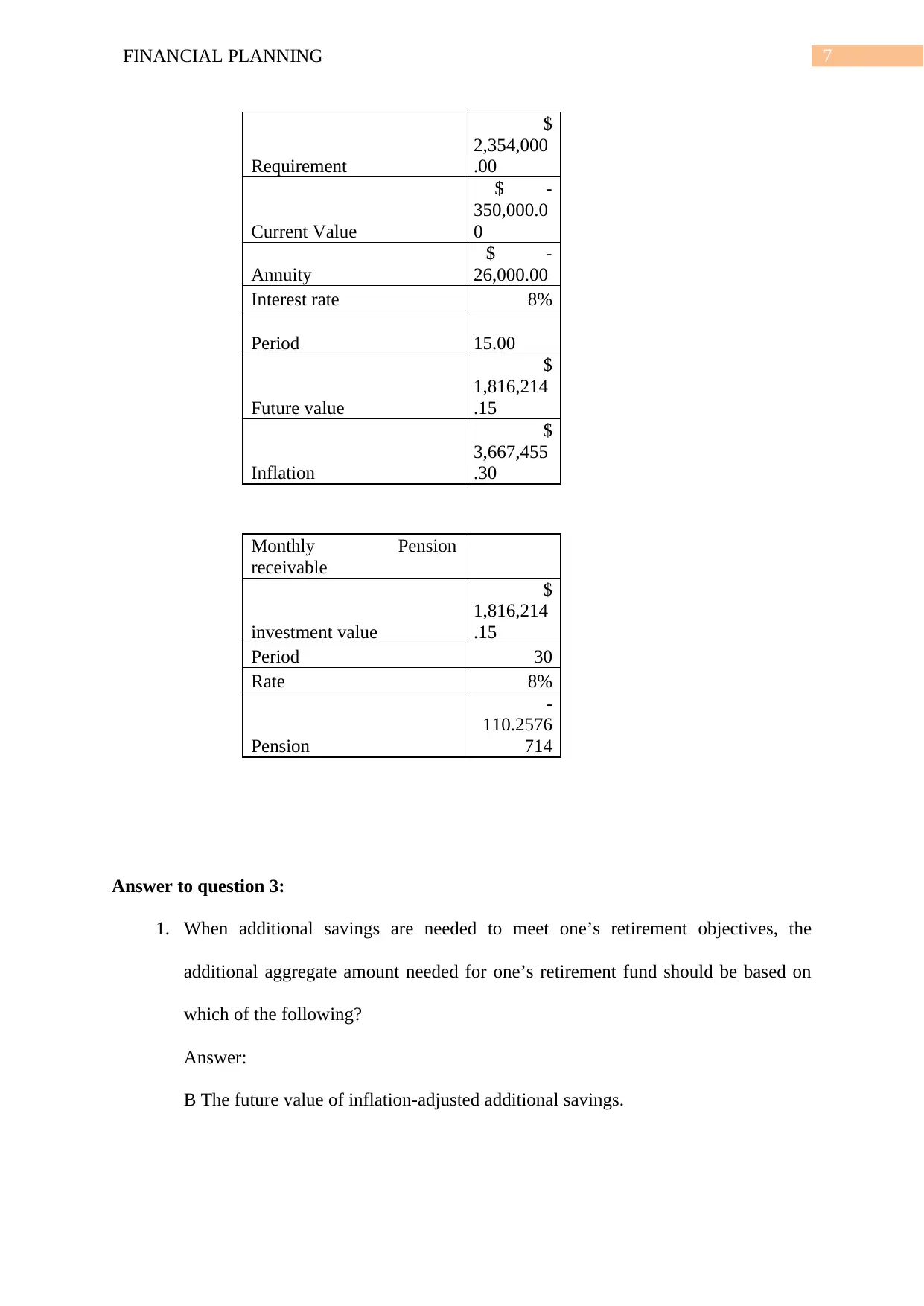

Answer to question 3:

1. When additional savings are needed to meet one’s retirement objectives, the

additional aggregate amount needed for one’s retirement fund should be based on

which of the following?

Answer:

B The future value of inflation-adjusted additional savings.

Requirement

$

2,354,000

.00

Current Value

$ -

350,000.0

0

Annuity

$ -

26,000.00

Interest rate 8%

Period 15.00

Future value

$

1,816,214

.15

Inflation

$

3,667,455

.30

Monthly Pension

receivable

investment value

$

1,816,214

.15

Period 30

Rate 8%

Pension

-

110.2576

714

Answer to question 3:

1. When additional savings are needed to meet one’s retirement objectives, the

additional aggregate amount needed for one’s retirement fund should be based on

which of the following?

Answer:

B The future value of inflation-adjusted additional savings.

8FINANCIAL PLANNING

2. The amount that must be saved annually for retirement would logically be reduced

by

Answer:

An increase in the rate of inflation

3. To calculate the future value of income-producing investments in the retirement

planning calculations, the most CORRECT interest factor to use is the

Answer:

Rate of return

4. Which of the following statements concerning inflation is/are CORRECT?

Answer:

C Both I and II

5. Which of the following are features of Supplementary Retirement Scheme?

Answer:

B I and II only.

6. The following statement(s) on the CPF is/are correct EXCEPT:

Answer:

A I only

7. Which of the following statement(s) about Eldershield and IDAPE is (are) TRUE?

Answer:

B I and III only.

8. When considering taking on an insurance policy for retirement purposes, which of

the following factors is most applicable?

Answer:

D All the above.

2. The amount that must be saved annually for retirement would logically be reduced

by

Answer:

An increase in the rate of inflation

3. To calculate the future value of income-producing investments in the retirement

planning calculations, the most CORRECT interest factor to use is the

Answer:

Rate of return

4. Which of the following statements concerning inflation is/are CORRECT?

Answer:

C Both I and II

5. Which of the following are features of Supplementary Retirement Scheme?

Answer:

B I and II only.

6. The following statement(s) on the CPF is/are correct EXCEPT:

Answer:

A I only

7. Which of the following statement(s) about Eldershield and IDAPE is (are) TRUE?

Answer:

B I and III only.

8. When considering taking on an insurance policy for retirement purposes, which of

the following factors is most applicable?

Answer:

D All the above.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL PLANNING

Answer questions 3b (i):

The return of ten retirement fund at the end of the term is less than the desirable

amount because of the rate of inflation that is expected to grow 3% per Annam respectively.

The major difference that has occurred only because of inflation. The rate of interest has

affected the desired sum (Li et al., 2016).

Answer questions 3b(ii):

The expected income that T will received after the retirement is

Retirement Benefits

particulars

Requirement $ 23,54,000.00

Current Value $ -3,50,000.00

Annuity $ -26,000.00

Interest rate 0.08

Period 15.00

Future value $ 18,16,214.15

(c ):

The rate of inflation is decided by having the higher value as the rate in cumulatively

increased , the Future Value of the retirement fund is expected at the rate of 8% per Annum.

As the return on investment are low might affect in the following:

1. Low return: because of the inflation the return will be inadequate to met.

Answer questions 3b (i):

The return of ten retirement fund at the end of the term is less than the desirable

amount because of the rate of inflation that is expected to grow 3% per Annam respectively.

The major difference that has occurred only because of inflation. The rate of interest has

affected the desired sum (Li et al., 2016).

Answer questions 3b(ii):

The expected income that T will received after the retirement is

Retirement Benefits

particulars

Requirement $ 23,54,000.00

Current Value $ -3,50,000.00

Annuity $ -26,000.00

Interest rate 0.08

Period 15.00

Future value $ 18,16,214.15

(c ):

The rate of inflation is decided by having the higher value as the rate in cumulatively

increased , the Future Value of the retirement fund is expected at the rate of 8% per Annum.

As the return on investment are low might affect in the following:

1. Low return: because of the inflation the return will be inadequate to met.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL PLANNING

2. Low Benefits: as the assured sum is assured and receivable at a future date then

the benefits that is desirable at the present time is higher than the future benefits.

3. Medical Allowance: as getting older attracts the medical expenses therefore the

future pensions are not considered to be effective to meet the medical cost.

4. The expectancy: the assesse expects to live for 90 years term and for that reason

Mr T is losing some substantial portion of the funds .

Assignment 2

Answer to Question 1

Answer to Question 1(a):

1. A I and II only.

2. C The insurer will reimburse the insured only to the extent of the insured’s financial

loss.

3. C Risk shifting or transfer

4. C They usually replace all of the disabled insured’s lost earnings

5. C Add an inflation protection rider.

2. Low Benefits: as the assured sum is assured and receivable at a future date then

the benefits that is desirable at the present time is higher than the future benefits.

3. Medical Allowance: as getting older attracts the medical expenses therefore the

future pensions are not considered to be effective to meet the medical cost.

4. The expectancy: the assesse expects to live for 90 years term and for that reason

Mr T is losing some substantial portion of the funds .

Assignment 2

Answer to Question 1

Answer to Question 1(a):

1. A I and II only.

2. C The insurer will reimburse the insured only to the extent of the insured’s financial

loss.

3. C Risk shifting or transfer

4. C They usually replace all of the disabled insured’s lost earnings

5. C Add an inflation protection rider.

11FINANCIAL PLANNING

6. B Life annuity with refund features

7. A Insureds who discontinue their insurance contribute to a surplus fund

8. B Retiring an instalment debt obligation at death.

Answer to 1(b)(i):

Uberimmae Fidei: It as a legal agreement of the parties to the contract with the obligation to

perform the duties in good faith.

Uberimmae Fidei, is a Latin fords which signifies the ‘Utmost Good Faith’. the insurance

contracts are the example of the Uberimmae Fidei, contracts as the policy holder pays

insurance premium to the insurer for availing the risk share agreement among them self’s.

In insurance sector, the policyholder or the policy applicant knows more therefore the

policyholder must voluntarily disclose all the relevant facts for fixation of the premium by the

insurer. It is necessary for both the parities to the contract to provide the benefits and fulfilled

the desired obligations (Epstein, 2018).

Answer to question 1(b)(ii):

The main features of the Uberimmae Fidei are that all the parties to the contacts must

have initiated all the material facts that are require to be disclosed in good faith. This contract

bounds both the parties to the contract to perform the duties such as notifying the condition

and the profanities of the risk insured and the chances of getting affected reasons and others.

6. B Life annuity with refund features

7. A Insureds who discontinue their insurance contribute to a surplus fund

8. B Retiring an instalment debt obligation at death.

Answer to 1(b)(i):

Uberimmae Fidei: It as a legal agreement of the parties to the contract with the obligation to

perform the duties in good faith.

Uberimmae Fidei, is a Latin fords which signifies the ‘Utmost Good Faith’. the insurance

contracts are the example of the Uberimmae Fidei, contracts as the policy holder pays

insurance premium to the insurer for availing the risk share agreement among them self’s.

In insurance sector, the policyholder or the policy applicant knows more therefore the

policyholder must voluntarily disclose all the relevant facts for fixation of the premium by the

insurer. It is necessary for both the parities to the contract to provide the benefits and fulfilled

the desired obligations (Epstein, 2018).

Answer to question 1(b)(ii):

The main features of the Uberimmae Fidei are that all the parties to the contacts must

have initiated all the material facts that are require to be disclosed in good faith. This contract

bounds both the parties to the contract to perform the duties such as notifying the condition

and the profanities of the risk insured and the chances of getting affected reasons and others.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.