1202AFE Financial Planning 1 Trimester 1, 2018: Statement of Advice

VerifiedAdded on 2023/06/12

|5

|1285

|186

Report

AI Summary

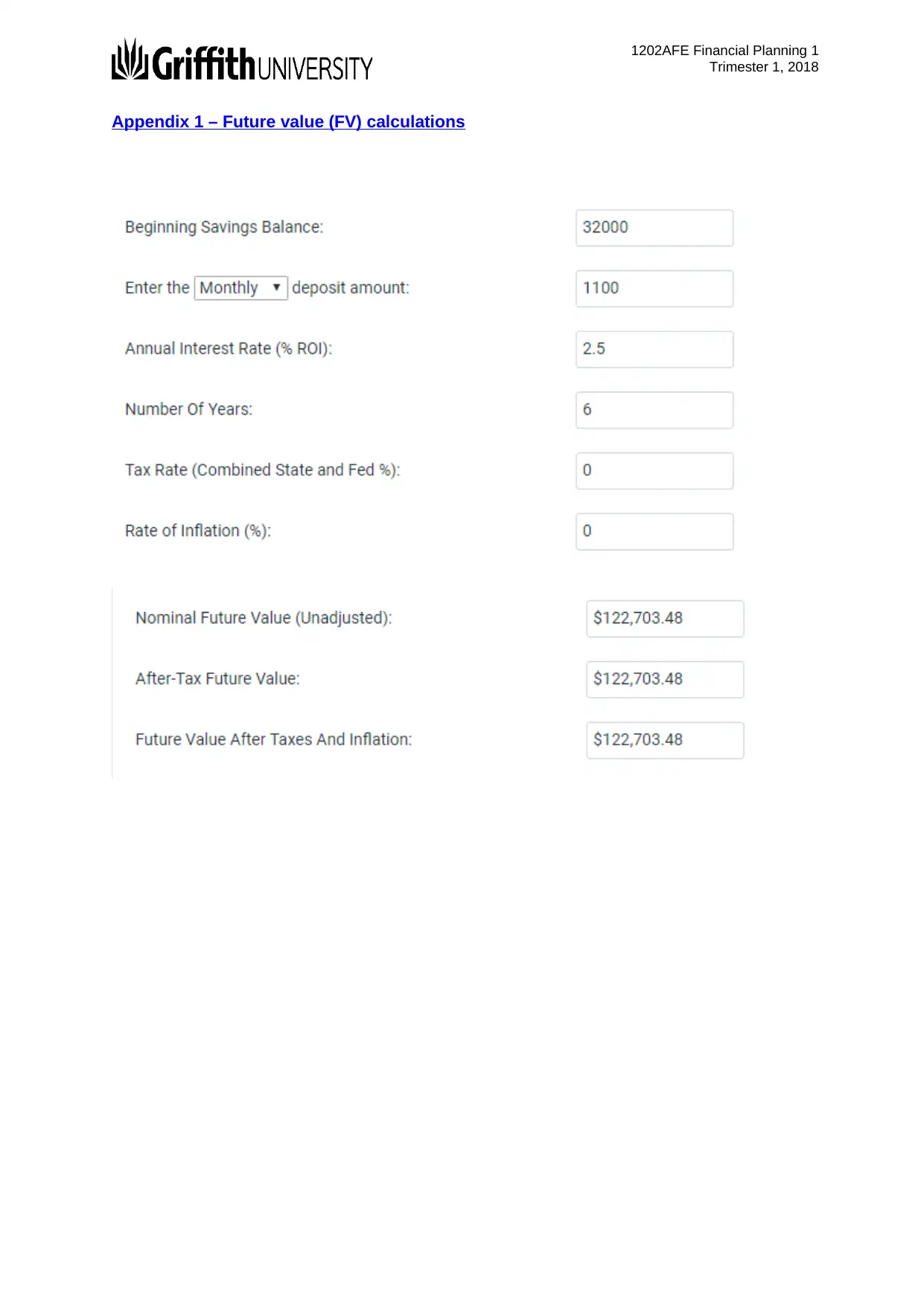

This document presents a financial planning file note for Pete Molloy, a 28-year-old electrician, created on April 9, 2018. The statement of advice (SOA) covers wealth creation, lifestyle goals, personal insurances (life, TPD, income protection, trauma, and private health), superannuation, and taxation planning. Pete's current situation, including his income, assets, and objectives like purchasing a house, securing his daughter's future, and planning for retirement, are outlined. The analysis includes recommendations for wealth creation outside superannuation (house deposit), lifestyle (holiday planning), and superannuation strategies, along with insurance advice. The file note also assesses Pete's risk profile as a growth investor and provides detailed future value calculations in the appendix. Desklib provides access to this and other solved assignments.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.