Financial Planning Diploma: Superannuation Technical Issues Assessment

VerifiedAdded on 2020/03/01

|33

|7261

|310

Homework Assignment

AI Summary

This document is a comprehensive solution to a superannuation technical issues assignment, addressing various aspects of financial planning and retirement strategies. The assignment covers topics such as Superannuation Guarantee contributions, salary sacrifice calculations, non-concessional contributions, contribution splitting, and the impact of age and account balances on contribution eligibility. It also explores case studies involving inheritance, retirement income streams, and the benefits of transferring funds to a retirement phase. The assignment delves into the advantages of investing in a retirement income stream phase, the potential downsides of such transfers, and the implications of SMSFs. The answers provided demonstrate an understanding of relevant legislation and regulations, offering practical insights for financial advisors and students alike. This resource is designed to assist students in understanding complex superannuation concepts and preparing for financial planning assessments.

DFP+SMSF Module 3Wkplace Simulation1707

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Diploma of Financial Planning + SMSF

Module 3 Workplace Simulation

Submission Instructions:

Key steps that must be followed:

Please complete the Declaration of Authenticity at the bottom of this page.

Once you have completed all parts of the assessment and saved it (e.g. to your

desktop computer), login to the Monarch Learning Management System (LMS) to

submit your assessment.

In the LMS, click on the file ”Submit DFP+SMSF Module 3 workplace simulation” in the

Module 3 section of your course and upload your assessment file/s by following the

prompts.

Please be sure to click “Continue” after clicking “submit”.This ensures your assessor

receives notification – very important!

Click here to go to the Monarch LMS

Declaration of Authenticity*

I certify that the attached material is my original work. No other person’s work hasbeen used without due

acknowledgement. I understandthat the work submitted may be reproduced and/or communicated for the purposeof

detecting plagiarism.

Student Name*: Date:

* I understand that by typing my name or inserting a digital signature into this box that I agree and am bound

by the above student declaration.

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Diploma of Financial Planning + SMSF

Module 3 Workplace Simulation

Submission Instructions:

Key steps that must be followed:

Please complete the Declaration of Authenticity at the bottom of this page.

Once you have completed all parts of the assessment and saved it (e.g. to your

desktop computer), login to the Monarch Learning Management System (LMS) to

submit your assessment.

In the LMS, click on the file ”Submit DFP+SMSF Module 3 workplace simulation” in the

Module 3 section of your course and upload your assessment file/s by following the

prompts.

Please be sure to click “Continue” after clicking “submit”.This ensures your assessor

receives notification – very important!

Click here to go to the Monarch LMS

Declaration of Authenticity*

I certify that the attached material is my original work. No other person’s work hasbeen used without due

acknowledgement. I understandthat the work submitted may be reproduced and/or communicated for the purposeof

detecting plagiarism.

Student Name*: Date:

* I understand that by typing my name or inserting a digital signature into this box that I agree and am bound

by the above student declaration.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DFP+SMSF Module 3Wkplace Simulation1707

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Important assessment information

Aims of this assessment

This assessment covers the fundamentals of superannuation. It covers spouse contribution rules

and strategies. It explores the making of non-concessional contribution strategies including

addressing the ‘bring-forward’ rule. The tax consequences on concessional and non-concessional

‘caps’ is explored, as are the tax consequences on superannuation contributions and withdrawals.

The differentiation between employer and membercontributions (i.e. different contribution types)

is explored. Transition-to-retirement strategies are covered as are the tax implications of taxable

versus tax-free superannuation benefits paid out to members or their beneficiaries. SMSF’s are

addressed in the context of using limited recourse borrowing arrangements. Bare Trusts are

explored as the holding mechanism for SMSF assets that are used as security in the borrowing

arrangement. The rules regarding business real property are explored in the context of making

concessional or non-concessional in-specie contributions into a SMSF. Rules on trusteeship of

SMSF’s are covered including differences between individual and corporate trustee arrangements.

Membership rules around an SMSF are covered including familial rules and employer/employee

rules. Rules on investment strategies within SMSF’s are explored. Death benefits paid from

SMSF’s are also addressed, including estate planning issues and re-contribution strategies.

Marking and feedback

This assignment contains 5 assessment activities each containing specific instructions.

This particular assessment forms part of your overall assessment for the following units of

competency:

FNSASICU503

FNSFPL502

FNSFPL503

FNSSMS501

FNSSMS505

FNSSMS601

FNSSMS602

FNSSMS603

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Important assessment information

Aims of this assessment

This assessment covers the fundamentals of superannuation. It covers spouse contribution rules

and strategies. It explores the making of non-concessional contribution strategies including

addressing the ‘bring-forward’ rule. The tax consequences on concessional and non-concessional

‘caps’ is explored, as are the tax consequences on superannuation contributions and withdrawals.

The differentiation between employer and membercontributions (i.e. different contribution types)

is explored. Transition-to-retirement strategies are covered as are the tax implications of taxable

versus tax-free superannuation benefits paid out to members or their beneficiaries. SMSF’s are

addressed in the context of using limited recourse borrowing arrangements. Bare Trusts are

explored as the holding mechanism for SMSF assets that are used as security in the borrowing

arrangement. The rules regarding business real property are explored in the context of making

concessional or non-concessional in-specie contributions into a SMSF. Rules on trusteeship of

SMSF’s are covered including differences between individual and corporate trustee arrangements.

Membership rules around an SMSF are covered including familial rules and employer/employee

rules. Rules on investment strategies within SMSF’s are explored. Death benefits paid from

SMSF’s are also addressed, including estate planning issues and re-contribution strategies.

Marking and feedback

This assignment contains 5 assessment activities each containing specific instructions.

This particular assessment forms part of your overall assessment for the following units of

competency:

FNSASICU503

FNSFPL502

FNSFPL503

FNSSMS501

FNSSMS505

FNSSMS601

FNSSMS602

FNSSMS603

DFP+SMSF Module 3Wkplace Simulation1707

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Grading for this assessment will be deemed “competent” or “not-yet-competent” in line with

specified educational standards under the Australian Qualifications Framework.

What does “competent” mean?

These answers contain relevant and accurate information in response to the question/s with

limited serious errors in fact or application. If incorrect information is contained in an answer, it

must be fundamentally outweighed by the accurate information provided. This will be assessed

against a marking guide provided to assessors for their determination.

What does “not-yet-competent” mean?

This occurs when an assessment does not meet the marking guide standards provided to

assessors. These answers either do not address the question specifically, or are wrong from a

legislative perspective, or are incorrectly applied. Answers that omit to provide a response to any

significant issue (where multiple issues must be addressed in a question) may also be deemed

not-yet-competent. Answers that have faulty reasoning, a poor standard of expression or include

plagiarism may also be deemed not-yet-competent. Please note, additional information regarding

Monarch’s plagiarism policy is contained in the Student Information Guide which can be found

here: http://www.monarch.edu.au/student-info/

What happens if you are deemed not-yet-competent?

In the event you do not achieve competency by your assessor on this assessment, you will be

given one more opportunity to re-submit the assessment after consultation with your Trainer/

Assessor. You will know your assessment is deemed ‘not-yet-competent’ if your grade book in the

Monarch LMS says “NYC” after you have received an email from your assessor advising your

assessment has been graded.

Important: It is your responsibility to ensure your assessment resubmission addresses all areas

deemed unsatisfactory by your assessor. Please note, if you are still unsuccessful in meeting

competency after resubmitting your assessment, you will be required to repeat those units.

In the event that you have concerns about the assessment decision then you can refer to our

Complaints & Appeals process also contained within the Student Information Guide.

Expectations from your assessor when answering different types of assessment questions

Knowledge based questions:

A knowledge based question requires you to clearly identify and cover the key subject matter

areas raised in the question in full as part of the response.

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Grading for this assessment will be deemed “competent” or “not-yet-competent” in line with

specified educational standards under the Australian Qualifications Framework.

What does “competent” mean?

These answers contain relevant and accurate information in response to the question/s with

limited serious errors in fact or application. If incorrect information is contained in an answer, it

must be fundamentally outweighed by the accurate information provided. This will be assessed

against a marking guide provided to assessors for their determination.

What does “not-yet-competent” mean?

This occurs when an assessment does not meet the marking guide standards provided to

assessors. These answers either do not address the question specifically, or are wrong from a

legislative perspective, or are incorrectly applied. Answers that omit to provide a response to any

significant issue (where multiple issues must be addressed in a question) may also be deemed

not-yet-competent. Answers that have faulty reasoning, a poor standard of expression or include

plagiarism may also be deemed not-yet-competent. Please note, additional information regarding

Monarch’s plagiarism policy is contained in the Student Information Guide which can be found

here: http://www.monarch.edu.au/student-info/

What happens if you are deemed not-yet-competent?

In the event you do not achieve competency by your assessor on this assessment, you will be

given one more opportunity to re-submit the assessment after consultation with your Trainer/

Assessor. You will know your assessment is deemed ‘not-yet-competent’ if your grade book in the

Monarch LMS says “NYC” after you have received an email from your assessor advising your

assessment has been graded.

Important: It is your responsibility to ensure your assessment resubmission addresses all areas

deemed unsatisfactory by your assessor. Please note, if you are still unsuccessful in meeting

competency after resubmitting your assessment, you will be required to repeat those units.

In the event that you have concerns about the assessment decision then you can refer to our

Complaints & Appeals process also contained within the Student Information Guide.

Expectations from your assessor when answering different types of assessment questions

Knowledge based questions:

A knowledge based question requires you to clearly identify and cover the key subject matter

areas raised in the question in full as part of the response.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DFP+SMSF Module 3Wkplace Simulation1707

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Skill based questions:

Where you are asked to write as though you are speaking to a client, your answers must show

your ability to:

understand your client’s concerns/perspective/views

show empathy

display a professional response

explain ideas clearly and simply so your client can understand the issues

Good luck

Finally, good luck with your learning and assessments and remember your trainers are here to

assist you

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Skill based questions:

Where you are asked to write as though you are speaking to a client, your answers must show

your ability to:

understand your client’s concerns/perspective/views

show empathy

display a professional response

explain ideas clearly and simply so your client can understand the issues

Good luck

Finally, good luck with your learning and assessments and remember your trainers are here to

assist you

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DFP+SMSF Module 3Wkplace Simulation1707

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all10 questions that follow.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the front of this assessment

Estimated time for completion of this assessment activity: 1-2 hours

Assessment Activity 1

Technical Issues

Superannuation

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all10 questions that follow.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the front of this assessment

Estimated time for completion of this assessment activity: 1-2 hours

Assessment Activity 1

Technical Issues

Superannuation

DFP+SMSF Module 3Wkplace Simulation1707

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

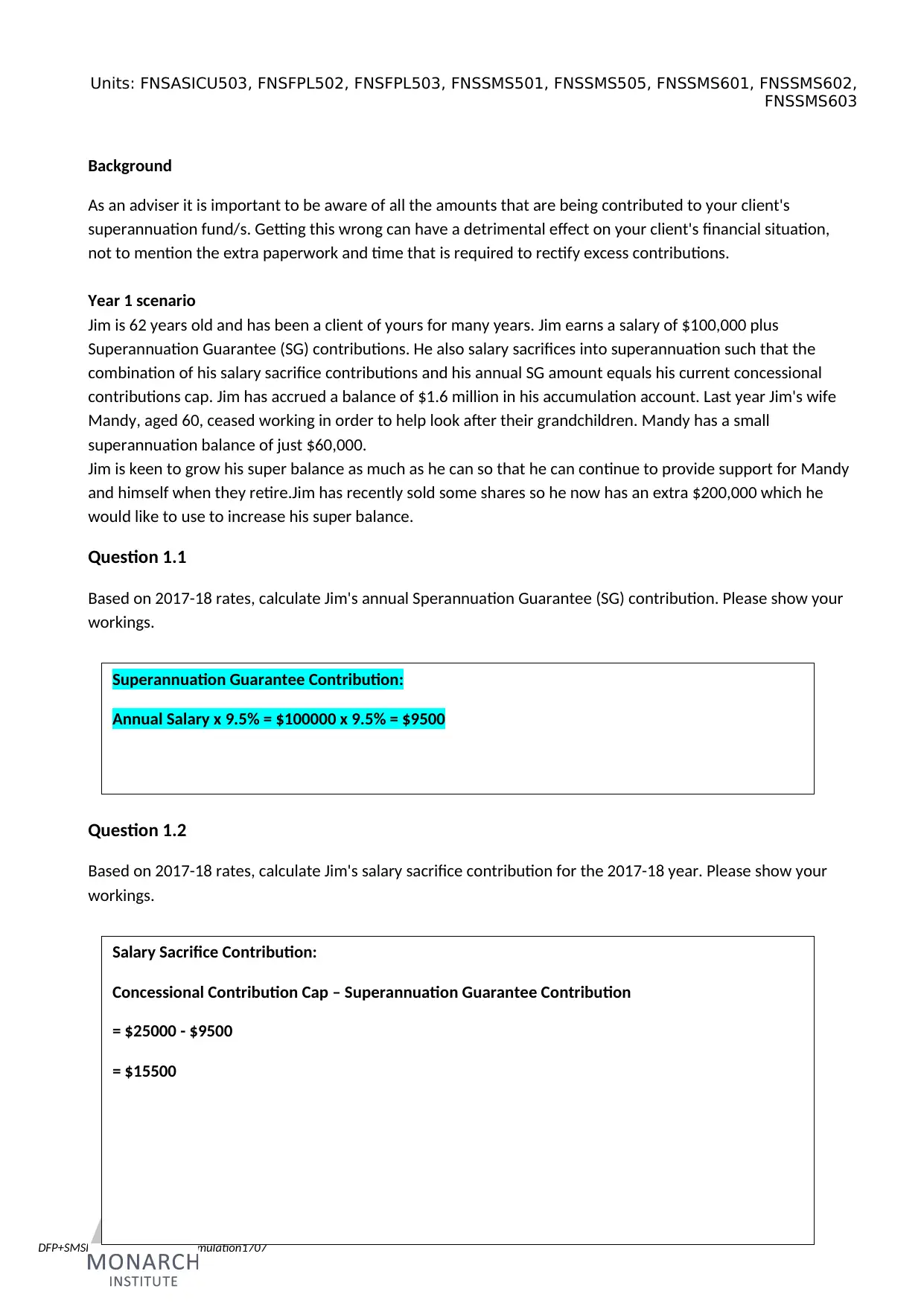

Background

As an adviser it is important to be aware of all the amounts that are being contributed to your client's

superannuation fund/s. Getting this wrong can have a detrimental effect on your client's financial situation,

not to mention the extra paperwork and time that is required to rectify excess contributions.

Year 1 scenario

Jim is 62 years old and has been a client of yours for many years. Jim earns a salary of $100,000 plus

Superannuation Guarantee (SG) contributions. He also salary sacrifices into superannuation such that the

combination of his salary sacrifice contributions and his annual SG amount equals his current concessional

contributions cap. Jim has accrued a balance of $1.6 million in his accumulation account. Last year Jim's wife

Mandy, aged 60, ceased working in order to help look after their grandchildren. Mandy has a small

superannuation balance of just $60,000.

Jim is keen to grow his super balance as much as he can so that he can continue to provide support for Mandy

and himself when they retire.Jim has recently sold some shares so he now has an extra $200,000 which he

would like to use to increase his super balance.

Question 1.1

Based on 2017-18 rates, calculate Jim's annual Sperannuation Guarantee (SG) contribution. Please show your

workings.

Question 1.2

Based on 2017-18 rates, calculate Jim's salary sacrifice contribution for the 2017-18 year. Please show your

workings.

Superannuation Guarantee Contribution:

Annual Salary x 9.5% = $100000 x 9.5% = $9500

Salary Sacrifice Contribution:

Concessional Contribution Cap – Superannuation Guarantee Contribution

= $25000 - $9500

= $15500

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Background

As an adviser it is important to be aware of all the amounts that are being contributed to your client's

superannuation fund/s. Getting this wrong can have a detrimental effect on your client's financial situation,

not to mention the extra paperwork and time that is required to rectify excess contributions.

Year 1 scenario

Jim is 62 years old and has been a client of yours for many years. Jim earns a salary of $100,000 plus

Superannuation Guarantee (SG) contributions. He also salary sacrifices into superannuation such that the

combination of his salary sacrifice contributions and his annual SG amount equals his current concessional

contributions cap. Jim has accrued a balance of $1.6 million in his accumulation account. Last year Jim's wife

Mandy, aged 60, ceased working in order to help look after their grandchildren. Mandy has a small

superannuation balance of just $60,000.

Jim is keen to grow his super balance as much as he can so that he can continue to provide support for Mandy

and himself when they retire.Jim has recently sold some shares so he now has an extra $200,000 which he

would like to use to increase his super balance.

Question 1.1

Based on 2017-18 rates, calculate Jim's annual Sperannuation Guarantee (SG) contribution. Please show your

workings.

Question 1.2

Based on 2017-18 rates, calculate Jim's salary sacrifice contribution for the 2017-18 year. Please show your

workings.

Superannuation Guarantee Contribution:

Annual Salary x 9.5% = $100000 x 9.5% = $9500

Salary Sacrifice Contribution:

Concessional Contribution Cap – Superannuation Guarantee Contribution

= $25000 - $9500

= $15500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DFP+SMSF Module 3Wkplace Simulation1707

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

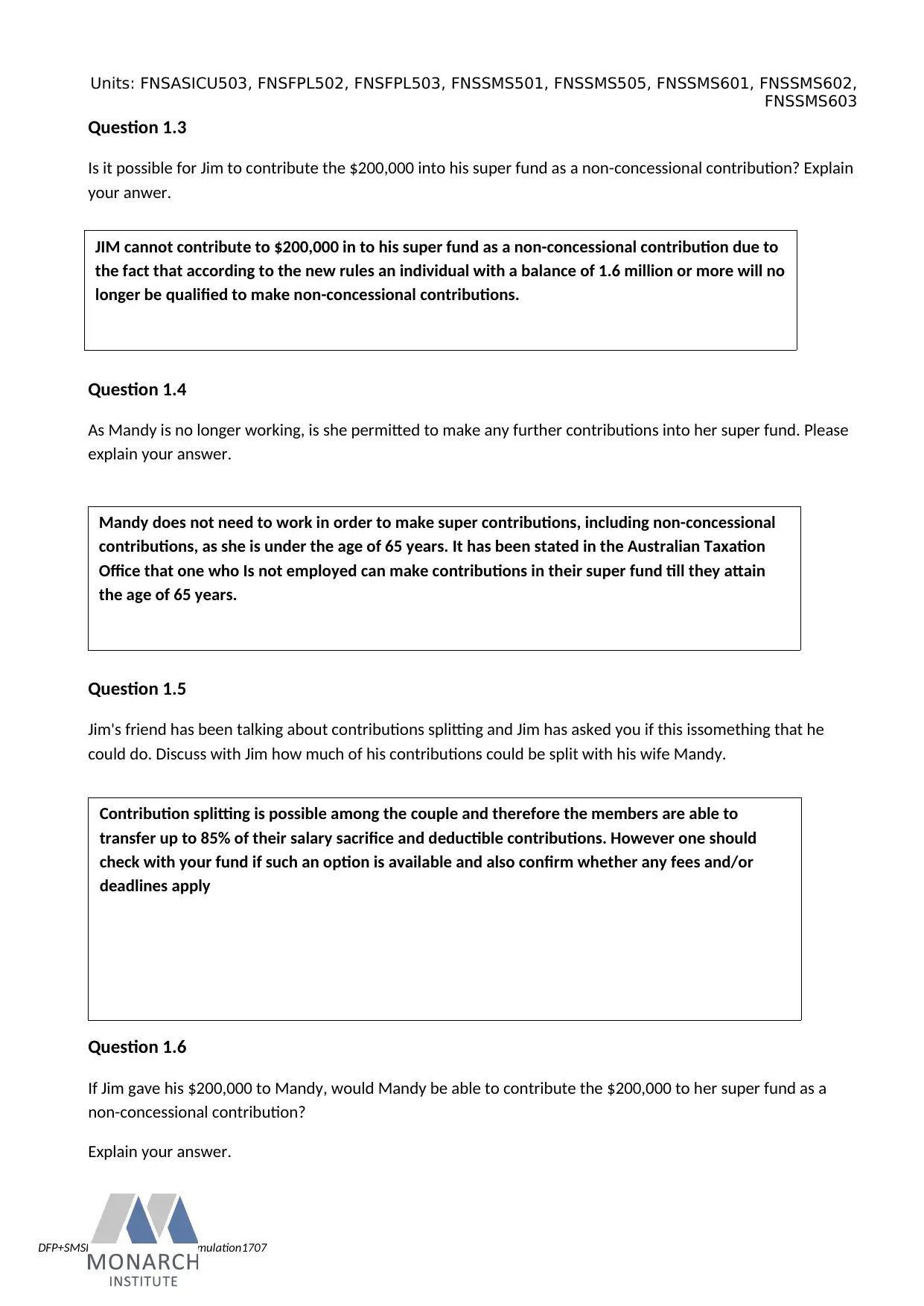

Question 1.3

Is it possible for Jim to contribute the $200,000 into his super fund as a non-concessional contribution? Explain

your anwer.

Question 1.4

As Mandy is no longer working, is she permitted to make any further contributions into her super fund. Please

explain your answer.

Question 1.5

Jim's friend has been talking about contributions splitting and Jim has asked you if this issomething that he

could do. Discuss with Jim how much of his contributions could be split with his wife Mandy.

Question 1.6

If Jim gave his $200,000 to Mandy, would Mandy be able to contribute the $200,000 to her super fund as a

non-concessional contribution?

Explain your answer.

JIM cannot contribute to $200,000 in to his super fund as a non-concessional contribution due to

the fact that according to the new rules an individual with a balance of 1.6 million or more will no

longer be qualified to make non-concessional contributions.

Contribution splitting is possible among the couple and therefore the members are able to

transfer up to 85% of their salary sacrifice and deductible contributions. However one should

check with your fund if such an option is available and also confirm whether any fees and/or

deadlines apply

Mandy does not need to work in order to make super contributions, including non-concessional

contributions, as she is under the age of 65 years. It has been stated in the Australian Taxation

Office that one who Is not employed can make contributions in their super fund till they attain

the age of 65 years.

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Question 1.3

Is it possible for Jim to contribute the $200,000 into his super fund as a non-concessional contribution? Explain

your anwer.

Question 1.4

As Mandy is no longer working, is she permitted to make any further contributions into her super fund. Please

explain your answer.

Question 1.5

Jim's friend has been talking about contributions splitting and Jim has asked you if this issomething that he

could do. Discuss with Jim how much of his contributions could be split with his wife Mandy.

Question 1.6

If Jim gave his $200,000 to Mandy, would Mandy be able to contribute the $200,000 to her super fund as a

non-concessional contribution?

Explain your answer.

JIM cannot contribute to $200,000 in to his super fund as a non-concessional contribution due to

the fact that according to the new rules an individual with a balance of 1.6 million or more will no

longer be qualified to make non-concessional contributions.

Contribution splitting is possible among the couple and therefore the members are able to

transfer up to 85% of their salary sacrifice and deductible contributions. However one should

check with your fund if such an option is available and also confirm whether any fees and/or

deadlines apply

Mandy does not need to work in order to make super contributions, including non-concessional

contributions, as she is under the age of 65 years. It has been stated in the Australian Taxation

Office that one who Is not employed can make contributions in their super fund till they attain

the age of 65 years.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DFP+SMSF Module 3Wkplace Simulation1707

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

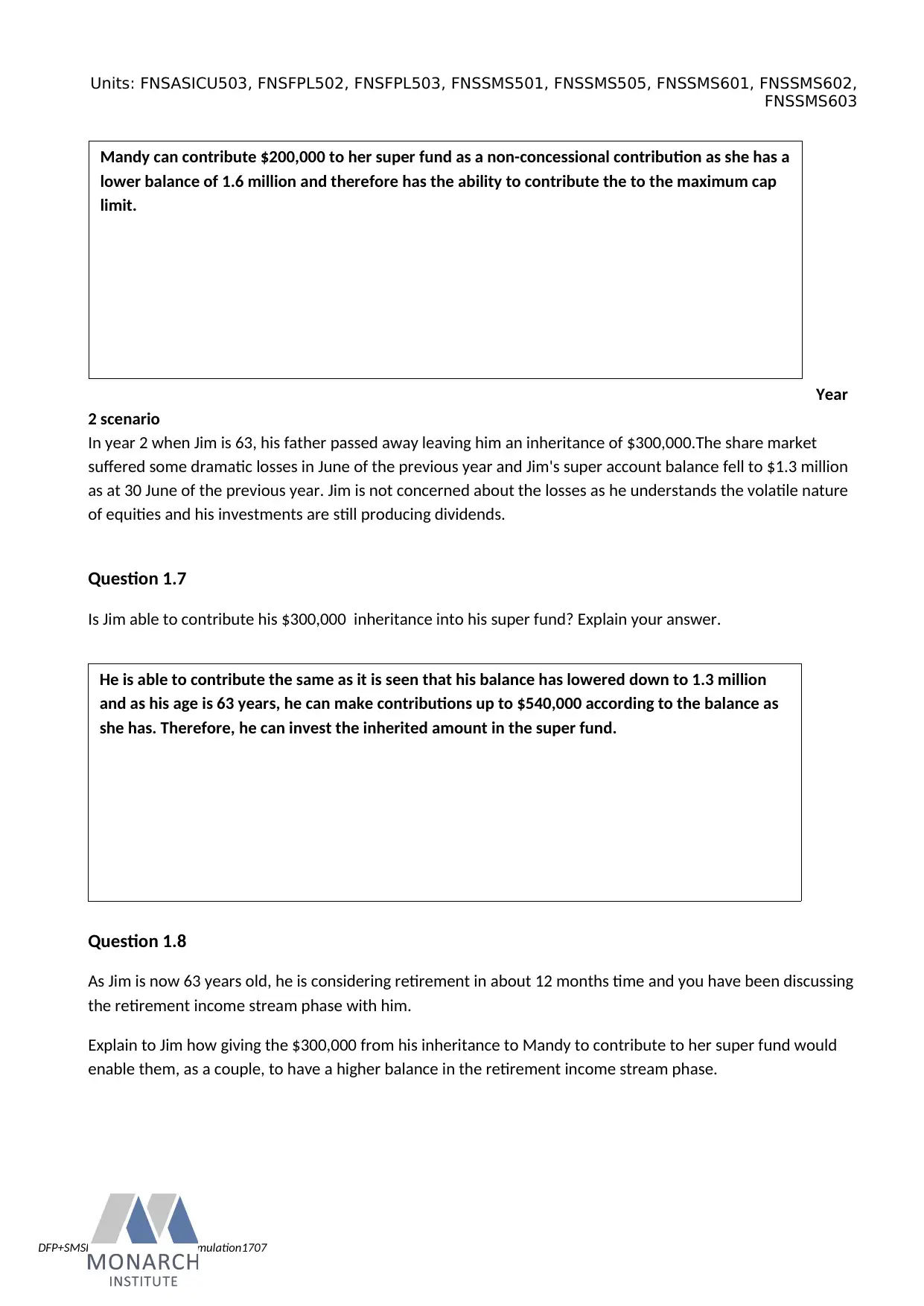

Year

2 scenario

In year 2 when Jim is 63, his father passed away leaving him an inheritance of $300,000.The share market

suffered some dramatic losses in June of the previous year and Jim's super account balance fell to $1.3 million

as at 30 June of the previous year. Jim is not concerned about the losses as he understands the volatile nature

of equities and his investments are still producing dividends.

Question 1.7

Is Jim able to contribute his $300,000 inheritance into his super fund? Explain your answer.

Question 1.8

As Jim is now 63 years old, he is considering retirement in about 12 months time and you have been discussing

the retirement income stream phase with him.

Explain to Jim how giving the $300,000 from his inheritance to Mandy to contribute to her super fund would

enable them, as a couple, to have a higher balance in the retirement income stream phase.

Mandy can contribute $200,000 to her super fund as a non-concessional contribution as she has a

lower balance of 1.6 million and therefore has the ability to contribute the to the maximum cap

limit.

He is able to contribute the same as it is seen that his balance has lowered down to 1.3 million

and as his age is 63 years, he can make contributions up to $540,000 according to the balance as

she has. Therefore, he can invest the inherited amount in the super fund.

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Year

2 scenario

In year 2 when Jim is 63, his father passed away leaving him an inheritance of $300,000.The share market

suffered some dramatic losses in June of the previous year and Jim's super account balance fell to $1.3 million

as at 30 June of the previous year. Jim is not concerned about the losses as he understands the volatile nature

of equities and his investments are still producing dividends.

Question 1.7

Is Jim able to contribute his $300,000 inheritance into his super fund? Explain your answer.

Question 1.8

As Jim is now 63 years old, he is considering retirement in about 12 months time and you have been discussing

the retirement income stream phase with him.

Explain to Jim how giving the $300,000 from his inheritance to Mandy to contribute to her super fund would

enable them, as a couple, to have a higher balance in the retirement income stream phase.

Mandy can contribute $200,000 to her super fund as a non-concessional contribution as she has a

lower balance of 1.6 million and therefore has the ability to contribute the to the maximum cap

limit.

He is able to contribute the same as it is seen that his balance has lowered down to 1.3 million

and as his age is 63 years, he can make contributions up to $540,000 according to the balance as

she has. Therefore, he can invest the inherited amount in the super fund.

DFP+SMSF Module 3Wkplace Simulation1707

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Question 1.9

Why may it bemore beneficial to have as much money invested in the retirement income stream phase as

possible compared with leaving it in the accumulation phase?

Jim giving the $300,000 from his inheritance to Mandy to contribute to her super fund would

enable them, as a couple, to have a higher balance in the retirement income stream phase because

it is seen that Mandy is not working and has a super fund of $60,000. In this scenario, tranferring

the fund to the balance of Mandy would mean paying lower level of tax rate and thereby increasing

the retirement income scheme for the couple.

It is beneficial to have as much money invested in the retirement income stream phase as

possible compared with leaving it in the accumulation phase because it is seen that retirement

income stream phase provides a tax free component and therefore the money invested in this

scheme would be tax free. However, keeping the balance in the accumulation phase would mean

that one has not started a pension with the value available in the superannuation account and

therefore this amount us liable for tax and will be subject up to 15% earnings tax.

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Question 1.9

Why may it bemore beneficial to have as much money invested in the retirement income stream phase as

possible compared with leaving it in the accumulation phase?

Jim giving the $300,000 from his inheritance to Mandy to contribute to her super fund would

enable them, as a couple, to have a higher balance in the retirement income stream phase because

it is seen that Mandy is not working and has a super fund of $60,000. In this scenario, tranferring

the fund to the balance of Mandy would mean paying lower level of tax rate and thereby increasing

the retirement income scheme for the couple.

It is beneficial to have as much money invested in the retirement income stream phase as

possible compared with leaving it in the accumulation phase because it is seen that retirement

income stream phase provides a tax free component and therefore the money invested in this

scheme would be tax free. However, keeping the balance in the accumulation phase would mean

that one has not started a pension with the value available in the superannuation account and

therefore this amount us liable for tax and will be subject up to 15% earnings tax.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DFP+SMSF Module 3Wkplace Simulation1707

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Question 1.10

If a client already has sufficient cashflow from other investments outside of superannuation, what is a potentia

l downside to transferring money to a retirement phase income stream?

Assessment Activity 2

Case Study

Superannuation

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all10 questions that follow.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the front of this assessment

Estimated time for completion of this assessment activity: 2-3 hours

It is seen that the downside of transferring money to a retirement phase income stream would

mean that the level of returns from the income would become lower and it is even seen that

many individuals in order to evade tax try to do the same but the ATO has restricted individuals

from transferring the amount from the cash flow up to a certain limit.

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Question 1.10

If a client already has sufficient cashflow from other investments outside of superannuation, what is a potentia

l downside to transferring money to a retirement phase income stream?

Assessment Activity 2

Case Study

Superannuation

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all10 questions that follow.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the front of this assessment

Estimated time for completion of this assessment activity: 2-3 hours

It is seen that the downside of transferring money to a retirement phase income stream would

mean that the level of returns from the income would become lower and it is even seen that

many individuals in order to evade tax try to do the same but the ATO has restricted individuals

from transferring the amount from the cash flow up to a certain limit.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DFP+SMSF Module 3Wkplace Simulation1707

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

DFP+SMSF Module 3Wkplace Simulation1707

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Scenario 1 - Background

Genevieve is age 62 and is considering retiring permanently from the workforce however she is concerned that

she may become bored in retirement. She has come in to discuss issues around taking a pension from her

superannuation account which is currently in accumulation phase.

She has sought your advice regarding some superannuation issues she is unsure about.

Required:

Answer Genevieve’s queries in a way that will be both clear to her and also comprehensive.

Question 2.1

If Genevieve commences a transition to retirement (TTR) income stream (pension)after 1 July 2017 while she

continues to work, explain how the earnings on her superannuation investments will be taxed.

Question 2.2

Explain to Genevieve how the tax treatment of her super investments will be different if she retires

permanently from the workforce and then commences a retirement phase income stream (pension).

Question 2.3

While the current tax treatment of income received from a TTR pension will not change, the tax

treatment of investment earnings on super fund assets that support it will change from1 July this

year. Earnings on fund assets supporting a TTR income stream will be subject to the same

maximum 15% tax rate that applies to super accumulation funds. This is the amount that would

be charged.

As she retires permanently, the tax structure would change and as she is retired her income

would become tax free and therefore she can gain more from the retirement phase income

steam. On the other hand, it can be stated that if she still continues and has attained the

preservation age then her rate of tax would reduce by a certain percentage.

Units: FNSASICU503, FNSFPL502, FNSFPL503, FNSSMS501, FNSSMS505, FNSSMS601, FNSSMS602,

FNSSMS603

Scenario 1 - Background

Genevieve is age 62 and is considering retiring permanently from the workforce however she is concerned that

she may become bored in retirement. She has come in to discuss issues around taking a pension from her

superannuation account which is currently in accumulation phase.

She has sought your advice regarding some superannuation issues she is unsure about.

Required:

Answer Genevieve’s queries in a way that will be both clear to her and also comprehensive.

Question 2.1

If Genevieve commences a transition to retirement (TTR) income stream (pension)after 1 July 2017 while she

continues to work, explain how the earnings on her superannuation investments will be taxed.

Question 2.2

Explain to Genevieve how the tax treatment of her super investments will be different if she retires

permanently from the workforce and then commences a retirement phase income stream (pension).

Question 2.3

While the current tax treatment of income received from a TTR pension will not change, the tax

treatment of investment earnings on super fund assets that support it will change from1 July this

year. Earnings on fund assets supporting a TTR income stream will be subject to the same

maximum 15% tax rate that applies to super accumulation funds. This is the amount that would

be charged.

As she retires permanently, the tax structure would change and as she is retired her income

would become tax free and therefore she can gain more from the retirement phase income

steam. On the other hand, it can be stated that if she still continues and has attained the

preservation age then her rate of tax would reduce by a certain percentage.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 33

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.