Financial Planning 1: Wealth Creation Working Paper - Tristen & Zoey

VerifiedAdded on 2022/11/30

|7

|1524

|203

Report

AI Summary

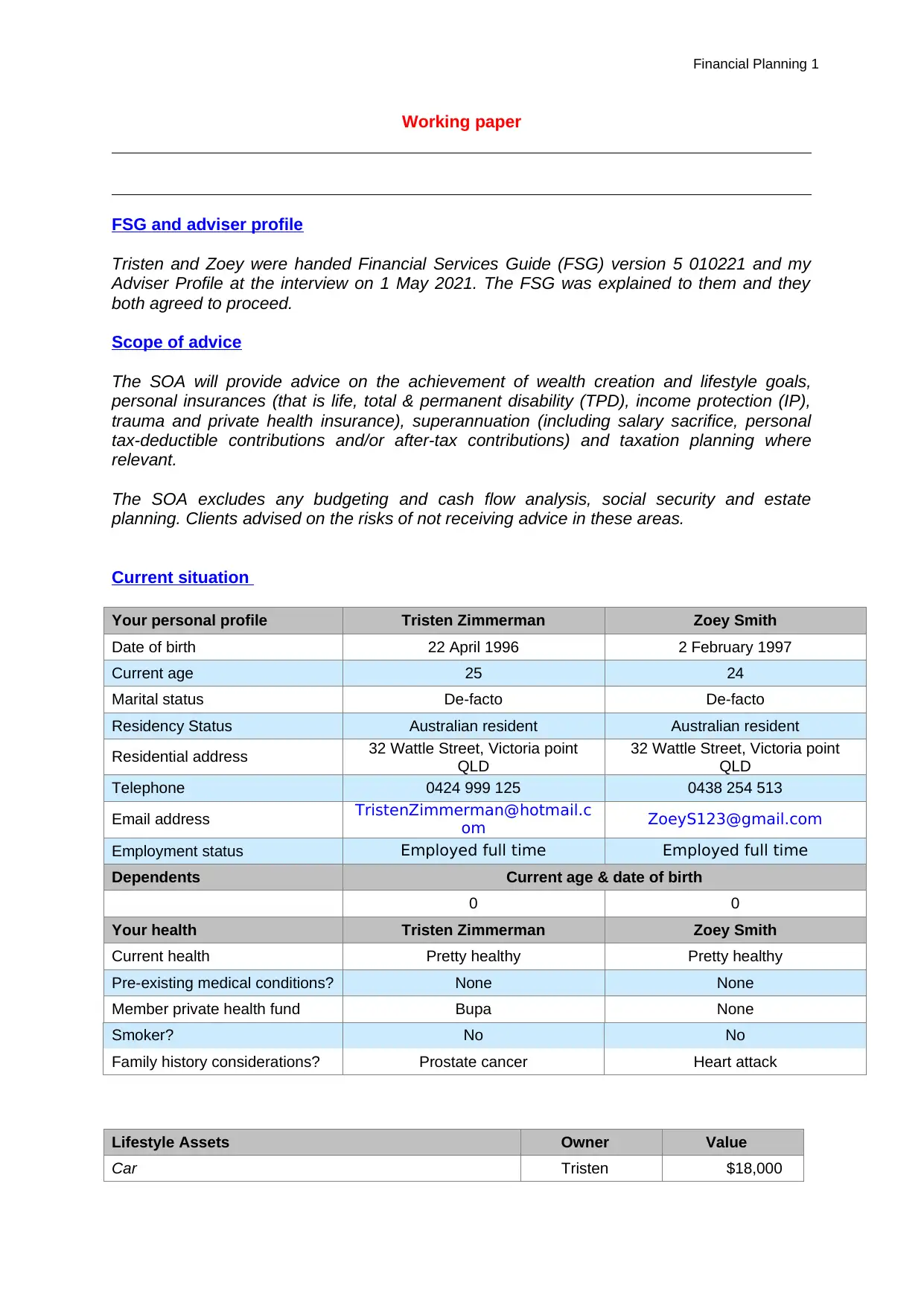

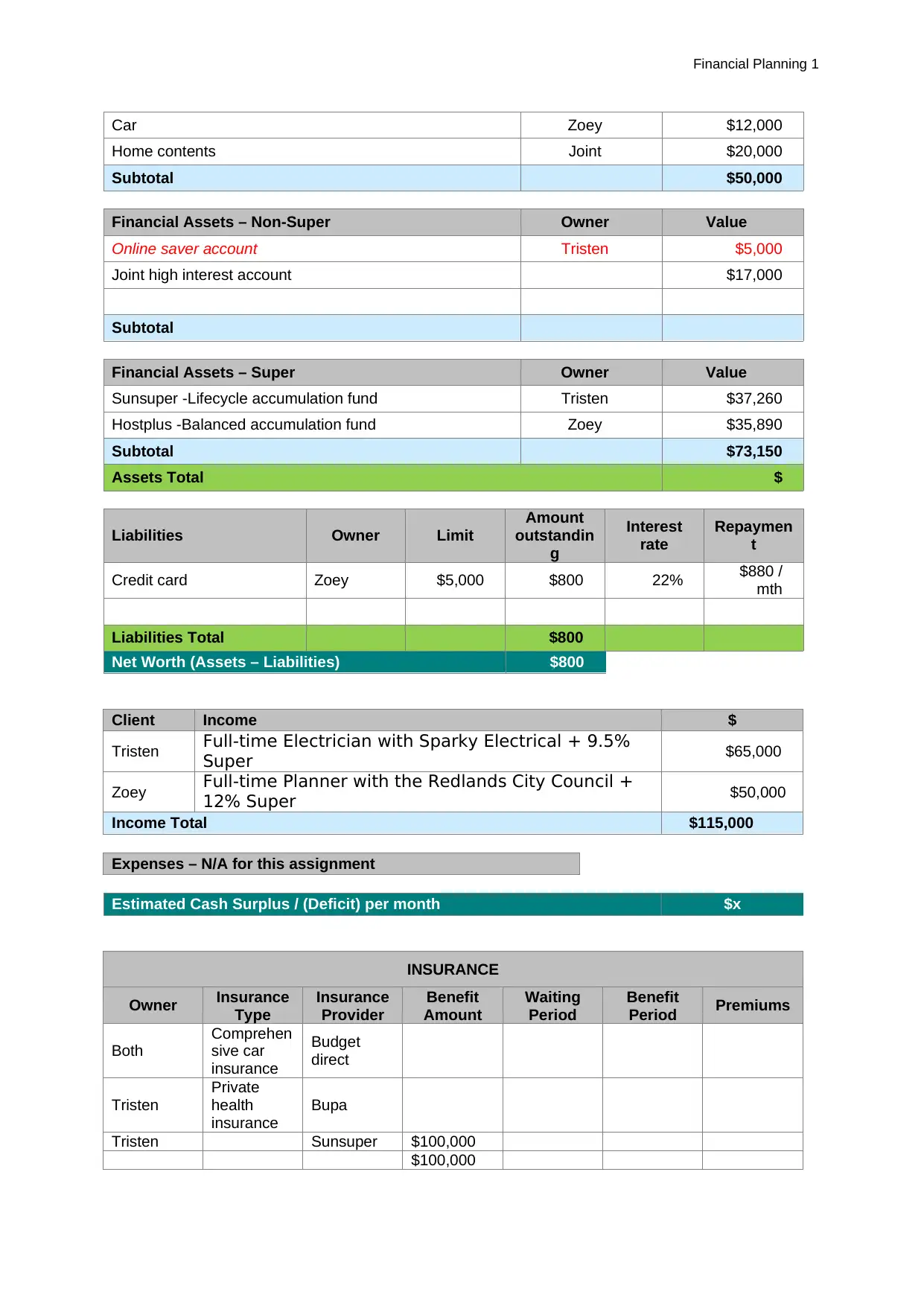

This financial planning working paper presents a comprehensive analysis of Tristen Zimmerman and Zoey Smith's financial situation, goals, and objectives based on their initial interview. The paper outlines the scope of advice, including wealth creation, insurance, superannuation, and tax planning, while excluding areas like budgeting and estate planning. It details their current assets, liabilities, income, and expenses, along with their risk profile. The core of the paper focuses on strategic recommendations for achieving their goals, which include wealth creation (through SIPs and recurring deposits), home deposit savings, and superannuation optimization. It also covers wealth protection strategies like life, TPD, income protection, trauma, and private health insurance. The paper analyzes the advantages, disadvantages, and alternatives for each strategy, supported by future value calculations, and provides a clear roadmap for Tristen and Zoey to achieve their financial aspirations.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.