Financial Planning: Wealth Creation and Lifestyle Strategies

VerifiedAdded on 2023/01/18

|3

|851

|37

Homework Assignment

AI Summary

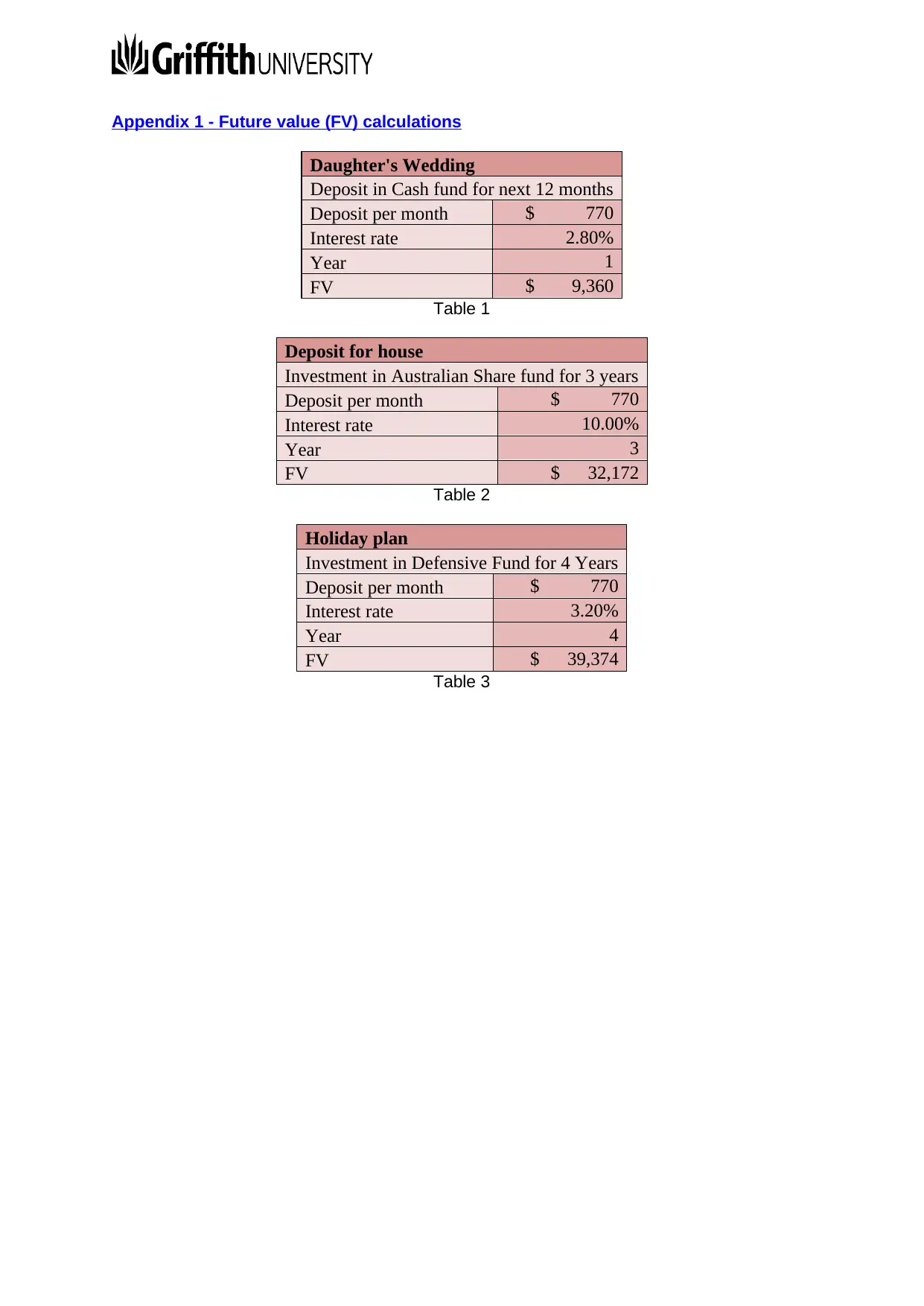

This assignment presents a financial plan tailored to an individual's goals, encompassing wealth creation and lifestyle recommendations. The plan outlines strategies for three key objectives: funding a daughter's wedding, accumulating a house deposit for children, and planning for a holiday. For the wedding, the plan suggests a cash fund investment, detailing the monthly deposit, interest rate, and projected returns. The house deposit strategy involves investing in an Australian share fund, considering the potential high yields and associated risks. Finally, the holiday plan recommends investing in a defensive fund to achieve the savings target while mitigating risk. Each strategy includes advantages, disadvantages, and alternative investment options, along with future value calculations to support the recommendations.

1 out of 3

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.