Financial Economics Project: Portfolio Analysis and Efficient Frontier

VerifiedAdded on 2023/01/23

|10

|1669

|384

Project

AI Summary

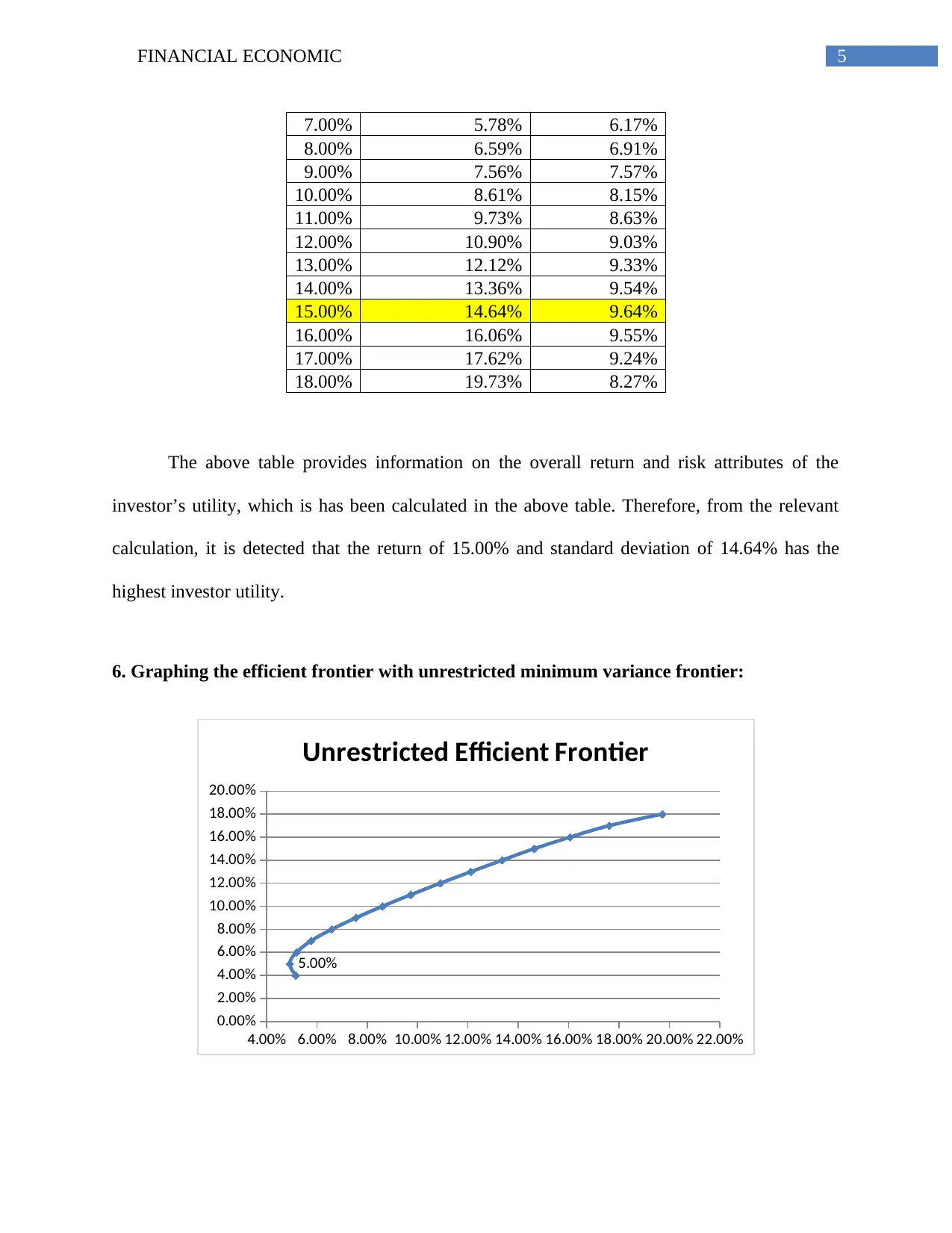

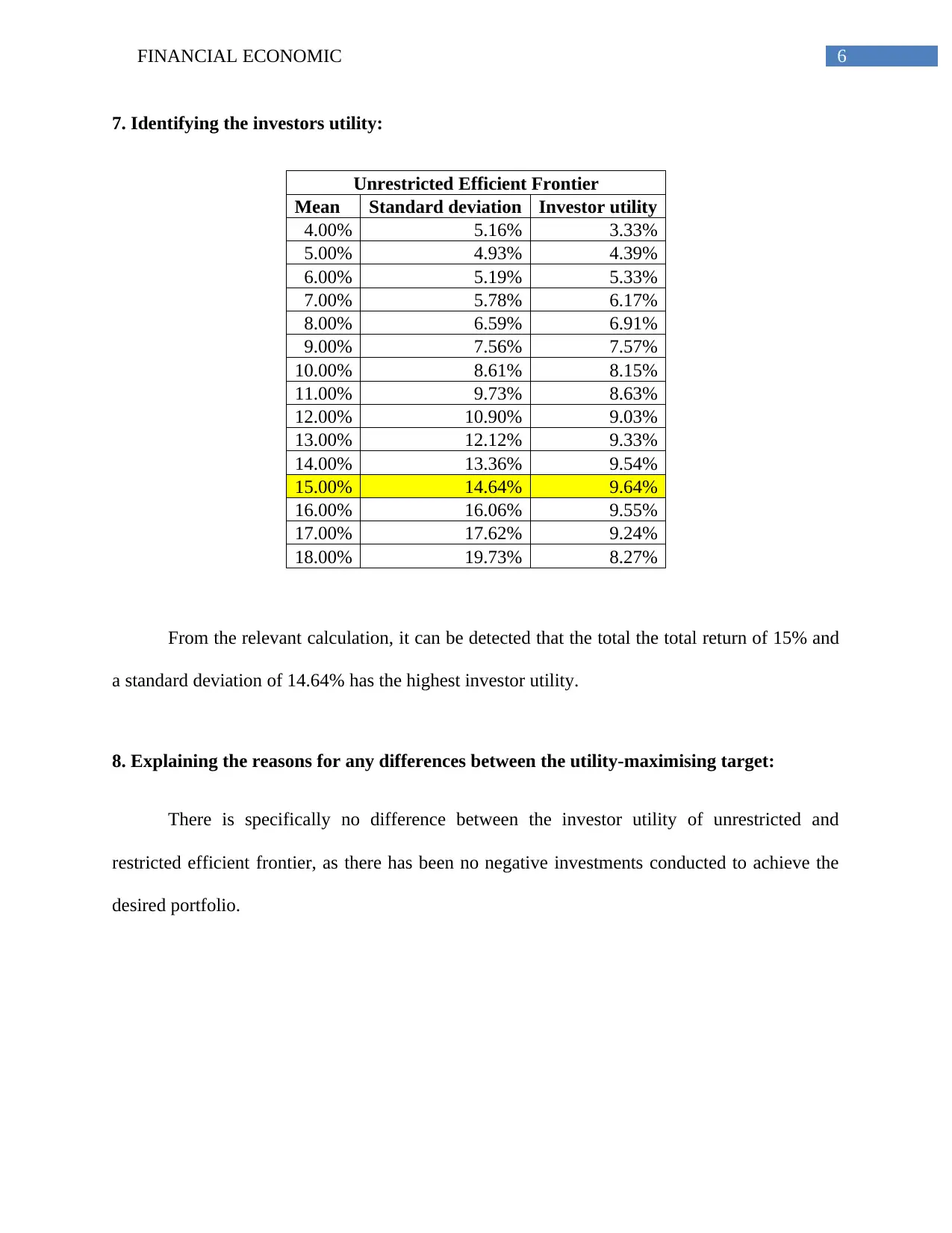

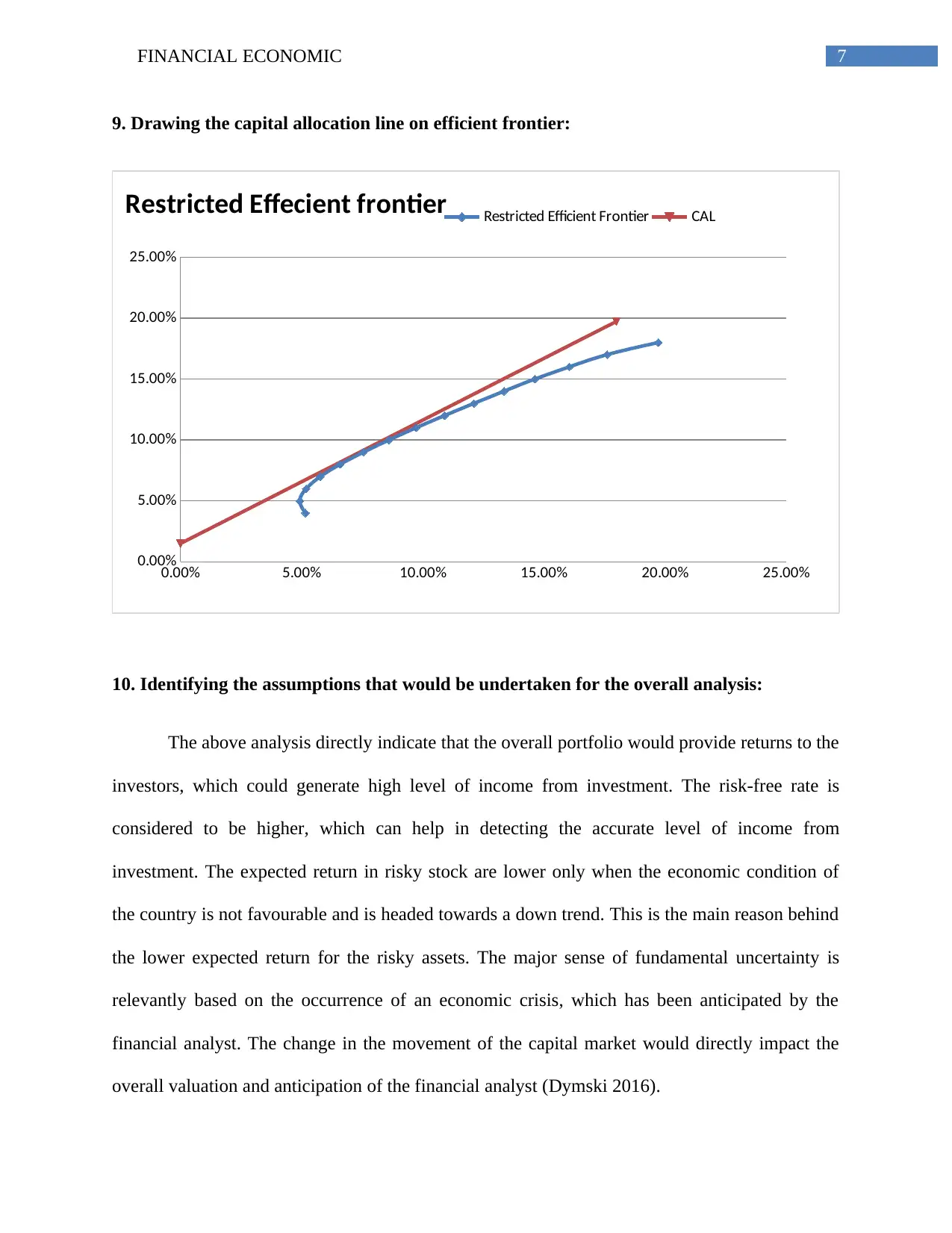

This financial economics project undertakes a comprehensive analysis of portfolio optimization. It begins by calculating the expected return, standard deviation, and geometric mean for various assets. The project then proceeds to compute the correlation and covariance matrices, providing insights into the relationships between different assets. Utilizing these calculations, the project graphs both restricted and unrestricted efficient frontiers, demonstrating the trade-off between risk and return. Investor utility is identified for different points on the efficient frontier. The project also draws the capital allocation line to illustrate the optimal allocation of capital. Finally, the analysis identifies the assumptions underlying the entire process and provides a detailed explanation of the factors influencing investor utility maximization and identifies the differences between the utility-maximizing targets. The project incorporates relevant references to support its findings.

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.