FIN200: Financial Accounting Report - Portfolio Analysis & CAPM

VerifiedAdded on 2022/08/23

|13

|2882

|31

Report

AI Summary

This financial accounting report delves into portfolio theory, exploring concepts such as the Security Market Line (SML) and Capital Market Line (CML), and their graphical depictions. It identifies and discusses the importance of minimum variance portfolios in risk management and diversification. The report then examines the Capital Asset Pricing Model (CAPM), justifying its relevance in calculating the required rate of return compared to other methods. It covers how CAPM helps in estimating expected returns and managing systematic risks, making it a vital tool in investment management. The report also emphasizes the importance of diversification and efficient portfolios, providing a comprehensive understanding of financial accounting and investment strategies, as well as the importance of beta values and the assumptions underlying the CAPM model, and its limitations.

Running head: FINANCIAL ACCOUNTING

Financial Accounting

Name of the Student

Name of the University

Author Note

Financial Accounting

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL ACCOUNTING

Table of Contents

Introduction................................................................................................................................2

Discussion..................................................................................................................................2

Security Market Line versus Capital Market Line.................................................................2

Importance of Minimum Variance Portfolios........................................................................5

CAPM Relevance for Required Rate of Return.....................................................................7

Conclusion..................................................................................................................................9

References................................................................................................................................10

Table of Contents

Introduction................................................................................................................................2

Discussion..................................................................................................................................2

Security Market Line versus Capital Market Line.................................................................2

Importance of Minimum Variance Portfolios........................................................................5

CAPM Relevance for Required Rate of Return.....................................................................7

Conclusion..................................................................................................................................9

References................................................................................................................................10

2FINANCIAL ACCOUNTING

Introduction

Company uses several management techniques in financial management. Financial

management is not complete without the reference of modern portfolio theory that efficiently

constructs the investor’s portfolio (Elterich 2014). The report aims to underline portfolio

theories through the theory of CAPM and its related concepts. The theory manages the risk

and returns factors related to the portfolio as per the scenario of the market. Capital Asset

Pricing Model (CAPM) is a model that is highly used in the field of investment management.

The report has discussed regarding the efficient portfolios in which Minimum Variance

Portfolios determines to provide with an expected level of return through minimum risk that

is positioned through the diversified portfolio (Rutterford and Sotiropoulos 2016). Markowitz

suggests the investor that they can reduce the risk of loss by diversifying and allocating their

assets of investment with a proper quantitative technique (Chen 2016). The discussion cannot

be completed without the reference of the Security market line, which represents CAPM

graphically, and Capital market line that reflects a proficient portfolio and Minimum variance

portfolios graphically. All of these form a pillar of financial and investment management in

which it embraces major importance in making decisions related to the investment.

Discussion

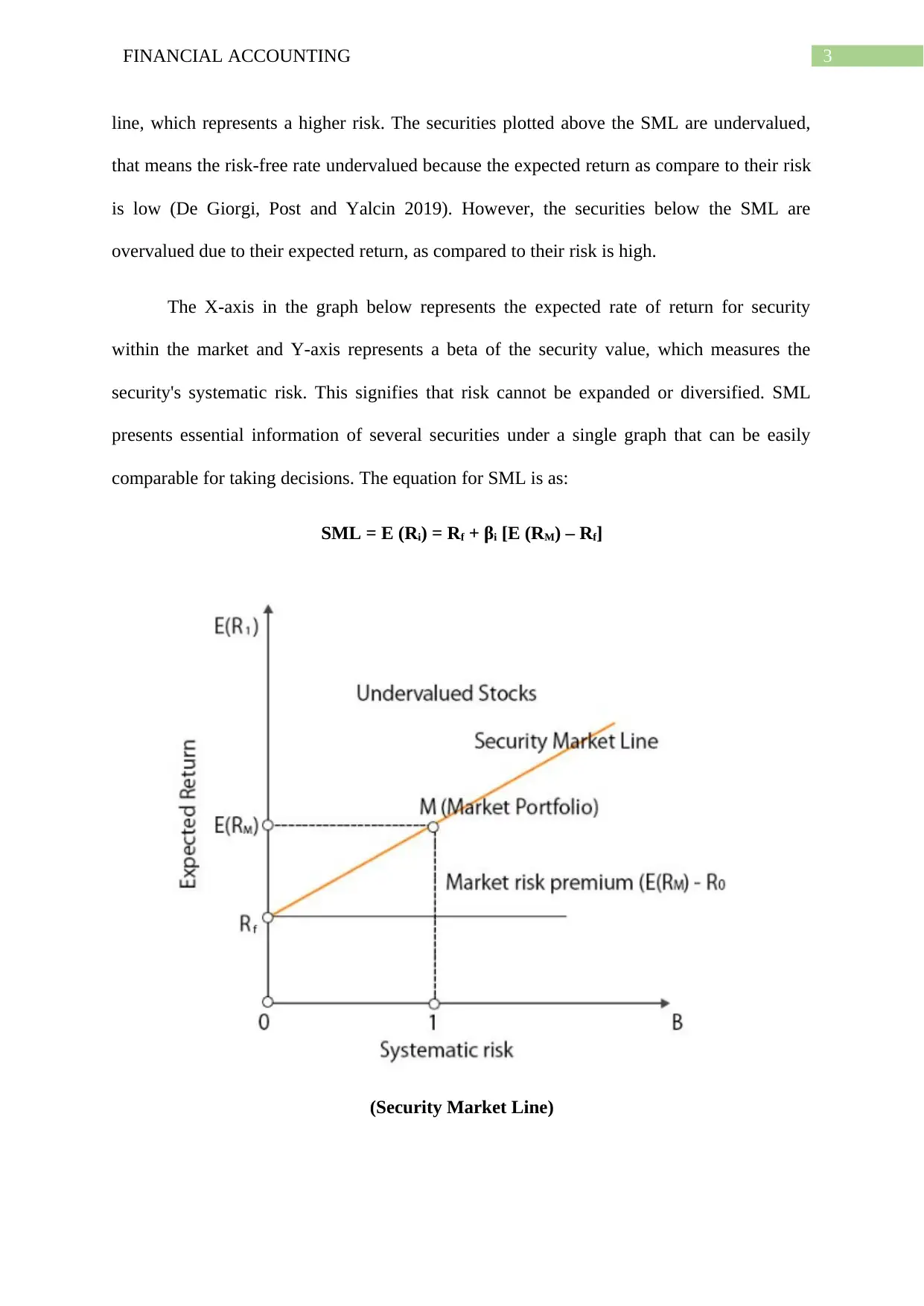

Security Market Line versus Capital Market Line

SML or Security Market Line is the graphical demonstration of CAPM that seeks to

present the level of market risk based on an assumption of a perfect market. SML estimates

the expected return by assuming that risk and return are proceeding in the same direction

(Jylha 2014). Thus, the investors who prefer a risk-averse condition used to choose the

investment nearby to the start of the line where the risk seems to be zero. On the other hand,

the investors who are risk-takers used to choose the investment to the uppermost point of the

Introduction

Company uses several management techniques in financial management. Financial

management is not complete without the reference of modern portfolio theory that efficiently

constructs the investor’s portfolio (Elterich 2014). The report aims to underline portfolio

theories through the theory of CAPM and its related concepts. The theory manages the risk

and returns factors related to the portfolio as per the scenario of the market. Capital Asset

Pricing Model (CAPM) is a model that is highly used in the field of investment management.

The report has discussed regarding the efficient portfolios in which Minimum Variance

Portfolios determines to provide with an expected level of return through minimum risk that

is positioned through the diversified portfolio (Rutterford and Sotiropoulos 2016). Markowitz

suggests the investor that they can reduce the risk of loss by diversifying and allocating their

assets of investment with a proper quantitative technique (Chen 2016). The discussion cannot

be completed without the reference of the Security market line, which represents CAPM

graphically, and Capital market line that reflects a proficient portfolio and Minimum variance

portfolios graphically. All of these form a pillar of financial and investment management in

which it embraces major importance in making decisions related to the investment.

Discussion

Security Market Line versus Capital Market Line

SML or Security Market Line is the graphical demonstration of CAPM that seeks to

present the level of market risk based on an assumption of a perfect market. SML estimates

the expected return by assuming that risk and return are proceeding in the same direction

(Jylha 2014). Thus, the investors who prefer a risk-averse condition used to choose the

investment nearby to the start of the line where the risk seems to be zero. On the other hand,

the investors who are risk-takers used to choose the investment to the uppermost point of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL ACCOUNTING

line, which represents a higher risk. The securities plotted above the SML are undervalued,

that means the risk-free rate undervalued because the expected return as compare to their risk

is low (De Giorgi, Post and Yalcin 2019). However, the securities below the SML are

overvalued due to their expected return, as compared to their risk is high.

The X-axis in the graph below represents the expected rate of return for security

within the market and Y-axis represents a beta of the security value, which measures the

security's systematic risk. This signifies that risk cannot be expanded or diversified. SML

presents essential information of several securities under a single graph that can be easily

comparable for taking decisions. The equation for SML is as:

SML = E (Ri) = Rf + βi [E (RM) – Rf]

(Security Market Line)

line, which represents a higher risk. The securities plotted above the SML are undervalued,

that means the risk-free rate undervalued because the expected return as compare to their risk

is low (De Giorgi, Post and Yalcin 2019). However, the securities below the SML are

overvalued due to their expected return, as compared to their risk is high.

The X-axis in the graph below represents the expected rate of return for security

within the market and Y-axis represents a beta of the security value, which measures the

security's systematic risk. This signifies that risk cannot be expanded or diversified. SML

presents essential information of several securities under a single graph that can be easily

comparable for taking decisions. The equation for SML is as:

SML = E (Ri) = Rf + βi [E (RM) – Rf]

(Security Market Line)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL ACCOUNTING

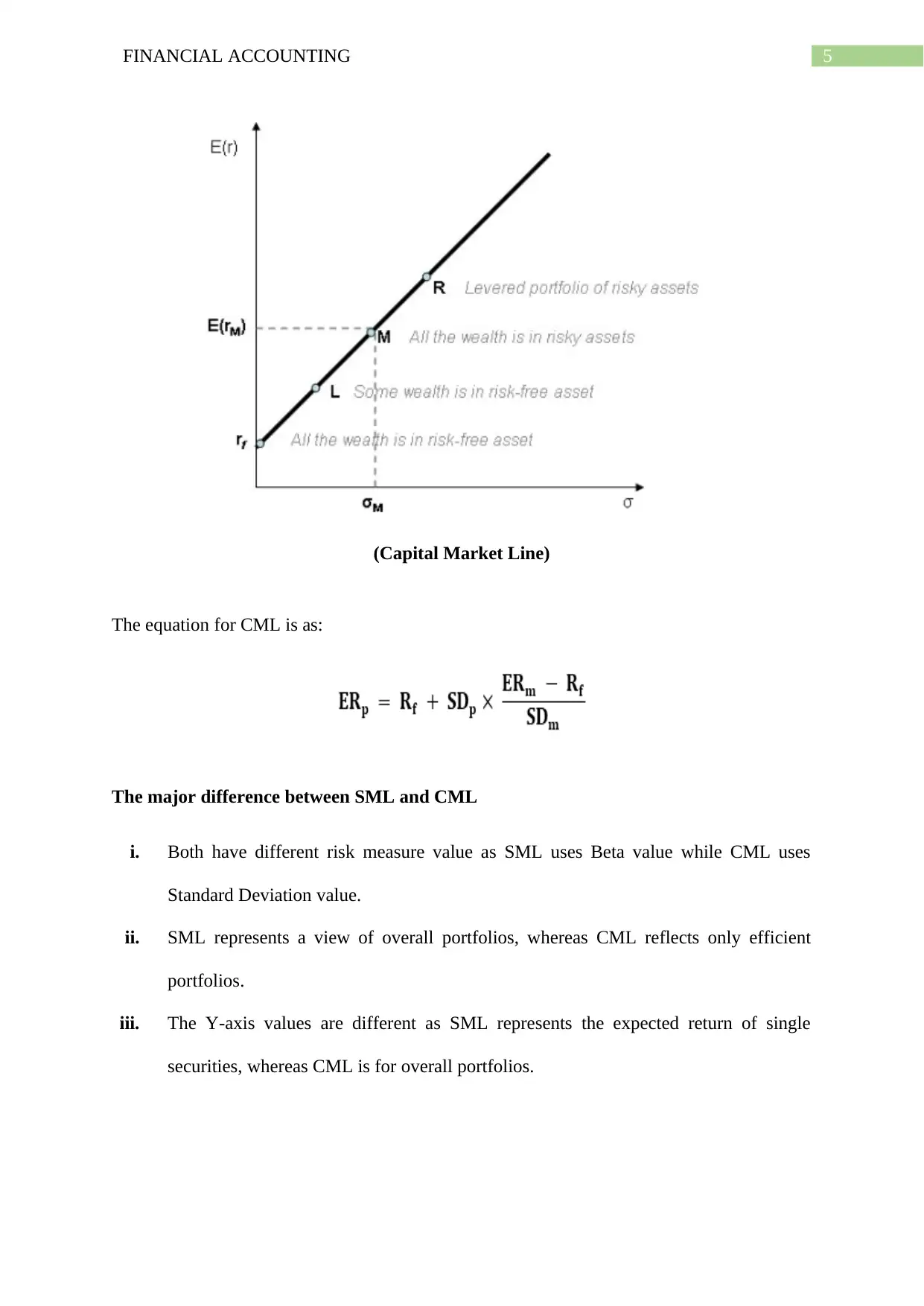

In compare, Capital Market Line is a graphical representation that reflects tradeoff

amongst risk and returns within well-organized portfolios. CML is a concept that provides

optimum mixtures of a risk-free asset as well as the market portfolio. The investors will

prefer to choose the market portfolio as same as the risk associated with them (Ibbotson and

Kim 2014). The line represents the earning of the investor as a premium risk in return of

taking additional risk within its portfolio. Rational investors tend to go for higher returns

from the assets, which is riskier.

It can be seen in the below graph that X-axis denotes the risk value or the standard

deviation value and Y-axis denotes the expected rate of return from the portfolio. Portfolio M

is comprised of risky assets and the market. There is not any risk-free asset, which means that

the money can neither invested in nor borrowed. The characteristics of risk-return for the

potential portfolio of risk asset can be strategized to create Markowitz efficient frontier (Lee

and Su 2014). The line from where the risk-return touches to the Markowitz portfolio then it

is called a market portfolio. The point joining the Risk-free asset with the market portfolio

signifies Capital market line.

In compare, Capital Market Line is a graphical representation that reflects tradeoff

amongst risk and returns within well-organized portfolios. CML is a concept that provides

optimum mixtures of a risk-free asset as well as the market portfolio. The investors will

prefer to choose the market portfolio as same as the risk associated with them (Ibbotson and

Kim 2014). The line represents the earning of the investor as a premium risk in return of

taking additional risk within its portfolio. Rational investors tend to go for higher returns

from the assets, which is riskier.

It can be seen in the below graph that X-axis denotes the risk value or the standard

deviation value and Y-axis denotes the expected rate of return from the portfolio. Portfolio M

is comprised of risky assets and the market. There is not any risk-free asset, which means that

the money can neither invested in nor borrowed. The characteristics of risk-return for the

potential portfolio of risk asset can be strategized to create Markowitz efficient frontier (Lee

and Su 2014). The line from where the risk-return touches to the Markowitz portfolio then it

is called a market portfolio. The point joining the Risk-free asset with the market portfolio

signifies Capital market line.

5FINANCIAL ACCOUNTING

(Capital Market Line)

The equation for CML is as:

The major difference between SML and CML

i. Both have different risk measure value as SML uses Beta value while CML uses

Standard Deviation value.

ii. SML represents a view of overall portfolios, whereas CML reflects only efficient

portfolios.

iii. The Y-axis values are different as SML represents the expected return of single

securities, whereas CML is for overall portfolios.

(Capital Market Line)

The equation for CML is as:

The major difference between SML and CML

i. Both have different risk measure value as SML uses Beta value while CML uses

Standard Deviation value.

ii. SML represents a view of overall portfolios, whereas CML reflects only efficient

portfolios.

iii. The Y-axis values are different as SML represents the expected return of single

securities, whereas CML is for overall portfolios.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL ACCOUNTING

Importance of Minimum Variance Portfolios

A minimum Variance Portfolio reflects a well-diversified securities portfolio that

comes together to reduce the volatility in the price for the entire portfolio. The impulsiveness

in the investments is substitutable in terms with the market risk. Hence, the higher the

investment’s volatility, the higher will be the market risk. (Levy and Levy 2014) The

investor's willingness to minimize the risk also affect the minimizations of volatility.

Diversification

The modern portfolio theory supposed to minimize the risk that is related to the

portfolio of an asset, although maintaining the same returns. Investments that have relatively

low correlation can be stated as those that are not too similar or performing differently within

the similar market and economic environment. The focus is about ‘not to put all the eggs in

the single basket’. The diversification can result in a lower risk (Fragkiskos 2014). When an

stakeholder diversifies its portfolio, then they are basically looking for for less volatility, and

this is the base of minimum variance portfolio, which is a diversified portfolio of assets or

securities. Addition to this, the risk can be increased or decreased by adjusting the amount

that is allocated to individual security. It can be done through make certain that the securities

that have been selected have a lesser correlation (Dewandaru et al. 2017). This can be

explained as if the price of one security increases, then it is not possible to increase of other

security is within the same degree. This is the safe and secure effect of diversification.

Mean-Variance Efficient Frontier

The efficient frontier is the group of an investment portfolio that offers the maximum

expected return for a lowest risk for a well-defined level of expected return. In theoretical

terms, a portfolio of securities can be attained to the risk at lowest level for a stated level of

expected returns. As no other grouping of the securities, yield a minimum level of risk for the

Importance of Minimum Variance Portfolios

A minimum Variance Portfolio reflects a well-diversified securities portfolio that

comes together to reduce the volatility in the price for the entire portfolio. The impulsiveness

in the investments is substitutable in terms with the market risk. Hence, the higher the

investment’s volatility, the higher will be the market risk. (Levy and Levy 2014) The

investor's willingness to minimize the risk also affect the minimizations of volatility.

Diversification

The modern portfolio theory supposed to minimize the risk that is related to the

portfolio of an asset, although maintaining the same returns. Investments that have relatively

low correlation can be stated as those that are not too similar or performing differently within

the similar market and economic environment. The focus is about ‘not to put all the eggs in

the single basket’. The diversification can result in a lower risk (Fragkiskos 2014). When an

stakeholder diversifies its portfolio, then they are basically looking for for less volatility, and

this is the base of minimum variance portfolio, which is a diversified portfolio of assets or

securities. Addition to this, the risk can be increased or decreased by adjusting the amount

that is allocated to individual security. It can be done through make certain that the securities

that have been selected have a lesser correlation (Dewandaru et al. 2017). This can be

explained as if the price of one security increases, then it is not possible to increase of other

security is within the same degree. This is the safe and secure effect of diversification.

Mean-Variance Efficient Frontier

The efficient frontier is the group of an investment portfolio that offers the maximum

expected return for a lowest risk for a well-defined level of expected return. In theoretical

terms, a portfolio of securities can be attained to the risk at lowest level for a stated level of

expected returns. As no other grouping of the securities, yield a minimum level of risk for the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL ACCOUNTING

stated level of expected returns. This is a unique nature of the portfolio, which is also known

as mean-variance efficient. Portfolio existing below the efficient frontier is considered as sub-

optimal as it does not deliver sufficient return for the level of risk (Bodnar, Parolya and

Schmid 2018). Portfolios to the right of the efficient frontier have a high level of risk for a

specified rate of return.

A graphical representation of mean-variance efficient portfolios forms a curve. A

rational investor tends to invest that falls on the efficient frontier as it entails lower risk with

an expected rate of return (Simaan, Simaan and Tang 2018). Above the frontier will pride the

same level of return with higher risk. The frontier technique is essential for creating strategies

for investment, which is also known as the Minimum Variance Portfolio (MVP).

The formation of Minimum Variance Portfolio includes allocation of weightage of

several securities within portfolio so that to attain a lower level of risk. The optimization of

MVP technique helps to achieve an expected rate of return with an appropriate standard

deviation (Yao, Li and Chen 2014). The use of MVP is very useful in the creation of

investment fund and equity strategies and many other similar uses.

CAPM Relevance for Required Rate of Return

The above discussion of the theory of modern portfolio is somehow depended on a pillar of

expected return. Thus, it becomes essential to guess the expected returns acceptably and

accurately to an extent which is more challenging. There are several techniques which is

available to assess an expected rate of return. However, all give a result that is not accurate

and reliable. CAPM is one of the traditional method to estimate the expected rate of return.

The economists have formed this theory as an extension of Markowitz diversification theory.

Capital Asset Pricing Model (CAPM) is an important theory of financial management

that defines the connection amongst the expected return for stocks and systematic risk

stated level of expected returns. This is a unique nature of the portfolio, which is also known

as mean-variance efficient. Portfolio existing below the efficient frontier is considered as sub-

optimal as it does not deliver sufficient return for the level of risk (Bodnar, Parolya and

Schmid 2018). Portfolios to the right of the efficient frontier have a high level of risk for a

specified rate of return.

A graphical representation of mean-variance efficient portfolios forms a curve. A

rational investor tends to invest that falls on the efficient frontier as it entails lower risk with

an expected rate of return (Simaan, Simaan and Tang 2018). Above the frontier will pride the

same level of return with higher risk. The frontier technique is essential for creating strategies

for investment, which is also known as the Minimum Variance Portfolio (MVP).

The formation of Minimum Variance Portfolio includes allocation of weightage of

several securities within portfolio so that to attain a lower level of risk. The optimization of

MVP technique helps to achieve an expected rate of return with an appropriate standard

deviation (Yao, Li and Chen 2014). The use of MVP is very useful in the creation of

investment fund and equity strategies and many other similar uses.

CAPM Relevance for Required Rate of Return

The above discussion of the theory of modern portfolio is somehow depended on a pillar of

expected return. Thus, it becomes essential to guess the expected returns acceptably and

accurately to an extent which is more challenging. There are several techniques which is

available to assess an expected rate of return. However, all give a result that is not accurate

and reliable. CAPM is one of the traditional method to estimate the expected rate of return.

The economists have formed this theory as an extension of Markowitz diversification theory.

Capital Asset Pricing Model (CAPM) is an important theory of financial management

that defines the connection amongst the expected return for stocks and systematic risk

8FINANCIAL ACCOUNTING

(Mehrara, Falahati and Zahiri 2014). The pricing of the risky securities is supported through

the CAPM so that to generate an expected return for stocks or assets. The CAPM is stated in

the equation as:

E(ri) = Rf + βi (E(rm) – Rf)

Whereas, ri = required rate of return on the asset,

Rf = risk-free rate of return,

βi = beta value for the asset, and

E(rm) = average market return.

Investors feel and expect to be reimbursed for the risk as well as the time value of

money. In the equation, the risk-free rate refers to the time value of money, and other

components consider the investor's additional risk. The Beta measures the level of risk added

to a portfolio that is similar to the market (Novak 2015). If a stock seems to be riskier than

the market, then it will be supposed to have Beta greater than one the equation is assumed to

reduce the risk of a portfolio, if the Beta of a stock is less than one. In other words, Beta

value is a correlation of the securities or asset with the market (Elbannan 2015). Therefore,

the equation of CAPM is able to consider equity risk premium effectively.

There are few assumptions used for CAPM. First, is the unsystematic risk can be

wholly removed by maintaining diversification in the portfolio. Addition to this, it assumes

that the investor holds a diversified portfolio. Secondly, the CPM model assumes single

period horizon for entire transactions so that to get comparable data for the risk-free and

average rate of return in the market and a beta value (Blitz, Falkenstein and Van Vliet 2014).

Further, the model assumes that the investors have access as well as understanding of the risk

free rate of return obtainable in the market, which they use in making risk free by lending and

(Mehrara, Falahati and Zahiri 2014). The pricing of the risky securities is supported through

the CAPM so that to generate an expected return for stocks or assets. The CAPM is stated in

the equation as:

E(ri) = Rf + βi (E(rm) – Rf)

Whereas, ri = required rate of return on the asset,

Rf = risk-free rate of return,

βi = beta value for the asset, and

E(rm) = average market return.

Investors feel and expect to be reimbursed for the risk as well as the time value of

money. In the equation, the risk-free rate refers to the time value of money, and other

components consider the investor's additional risk. The Beta measures the level of risk added

to a portfolio that is similar to the market (Novak 2015). If a stock seems to be riskier than

the market, then it will be supposed to have Beta greater than one the equation is assumed to

reduce the risk of a portfolio, if the Beta of a stock is less than one. In other words, Beta

value is a correlation of the securities or asset with the market (Elbannan 2015). Therefore,

the equation of CAPM is able to consider equity risk premium effectively.

There are few assumptions used for CAPM. First, is the unsystematic risk can be

wholly removed by maintaining diversification in the portfolio. Addition to this, it assumes

that the investor holds a diversified portfolio. Secondly, the CPM model assumes single

period horizon for entire transactions so that to get comparable data for the risk-free and

average rate of return in the market and a beta value (Blitz, Falkenstein and Van Vliet 2014).

Further, the model assumes that the investors have access as well as understanding of the risk

free rate of return obtainable in the market, which they use in making risk free by lending and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL ACCOUNTING

borrowing. At last, the CAPM model has an assumption of a perfect capital market, which

means there is not any cost involved, and data can be easily accessible by the investors.

The above assumption also leads to several criticisms for the CAPM model. As in the

real world, there are several included costs like taxes and transaction costs. It is also not

possible that each investor willing to replicate the whole market in his/her asset portfolio and

not all investor can take or offer amount at the risk-free rate of return.

In spite of several criticisms, CAPM still is considered as one of the important

techniques for calculating the expected rate of return. In the industry related to investment

management and a world of corporate finance, the use of CAPM is advanced and erudite

(Mota 2015). The CAPM model used parallel in respect with the other methods so that there

can be the validation of results, identification and rectification of outliers.

CAPM model accounts only for the systematic risks which cannot be diversified. It also

provides the data in a standard format and with clarity. From the last several years, the

CAPM model is subjected to be stood with frequent empirical testing. The method is also

well known to calculate the cost of equity as it is related to the systematic risk. Therefore, it is

superior to the dividend growth model. Thus, the CAPM model is still preferable to be

chosen by the financial managers instead to go for other techniques.

Conclusion

The Diversification, efficient portfolios, Security market line, Capital market line and CAPM

model are some of the methods that are widely used in the concept of financial management.

They are held as a pillar of the financial management that keeps importance while taking any

financial or investment related decisions. The techniques further used to minimize the

estimation error and used with the other techniques. Thus, these techniques help out in

borrowing. At last, the CAPM model has an assumption of a perfect capital market, which

means there is not any cost involved, and data can be easily accessible by the investors.

The above assumption also leads to several criticisms for the CAPM model. As in the

real world, there are several included costs like taxes and transaction costs. It is also not

possible that each investor willing to replicate the whole market in his/her asset portfolio and

not all investor can take or offer amount at the risk-free rate of return.

In spite of several criticisms, CAPM still is considered as one of the important

techniques for calculating the expected rate of return. In the industry related to investment

management and a world of corporate finance, the use of CAPM is advanced and erudite

(Mota 2015). The CAPM model used parallel in respect with the other methods so that there

can be the validation of results, identification and rectification of outliers.

CAPM model accounts only for the systematic risks which cannot be diversified. It also

provides the data in a standard format and with clarity. From the last several years, the

CAPM model is subjected to be stood with frequent empirical testing. The method is also

well known to calculate the cost of equity as it is related to the systematic risk. Therefore, it is

superior to the dividend growth model. Thus, the CAPM model is still preferable to be

chosen by the financial managers instead to go for other techniques.

Conclusion

The Diversification, efficient portfolios, Security market line, Capital market line and CAPM

model are some of the methods that are widely used in the concept of financial management.

They are held as a pillar of the financial management that keeps importance while taking any

financial or investment related decisions. The techniques further used to minimize the

estimation error and used with the other techniques. Thus, these techniques help out in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL ACCOUNTING

several situations such as difficulty regarding the investment-related decision and while

maintaining an efficient portfolio.

several situations such as difficulty regarding the investment-related decision and while

maintaining an efficient portfolio.

11FINANCIAL ACCOUNTING

References

Blitz, D., Falkenstein, E. and Van Vliet, P., 2014. Explanations for the volatility effect: An

overview based on the CAPM assumptions. The Journal of Portfolio Management, 40(3),

pp.61-76.

Bodnar, T., Parolya, N. and Schmid, W., 2018. Estimation of the global minimum variance

portfolio in high dimensions. European Journal of Operational Research, 266(1), pp.371-

390.

Chen, J.M., 2016. Modern portfolio theory. In Postmodern Portfolio Theory (pp. 5-25).

Palgrave Macmillan, New York.

De Giorgi, E.G., Post, T. and Yalçın, A., 2019. A concave security market line. Journal of

Banking & Finance, 106, pp.65-81.

Dewandaru, G., Masih, R., Bacha, O.I. and Masih, A.M.M., 2017. The role of Islamic asset

classes in the diversified portfolios: Mean variance spanning test. Emerging Markets

Review, 30, pp.66-95.

Elbannan, M.A., 2015. The capital asset pricing model: an overview of the

theory. International Journal of Economics and Finance, 7(1), pp.216-228.

Elterich, S., FMR LLC, 2014. Financial Account Management. U.S. Patent Application

14/164,558.

Fragkiskos, A., 2014. What is Portfolio Diversification?. Available at SSRN 2331475.

Ibbotson, R.G. and Kim, D.Y., 2014. Risk and return within the stock market: what works

best?. Working Paper, Zebra Capital.

References

Blitz, D., Falkenstein, E. and Van Vliet, P., 2014. Explanations for the volatility effect: An

overview based on the CAPM assumptions. The Journal of Portfolio Management, 40(3),

pp.61-76.

Bodnar, T., Parolya, N. and Schmid, W., 2018. Estimation of the global minimum variance

portfolio in high dimensions. European Journal of Operational Research, 266(1), pp.371-

390.

Chen, J.M., 2016. Modern portfolio theory. In Postmodern Portfolio Theory (pp. 5-25).

Palgrave Macmillan, New York.

De Giorgi, E.G., Post, T. and Yalçın, A., 2019. A concave security market line. Journal of

Banking & Finance, 106, pp.65-81.

Dewandaru, G., Masih, R., Bacha, O.I. and Masih, A.M.M., 2017. The role of Islamic asset

classes in the diversified portfolios: Mean variance spanning test. Emerging Markets

Review, 30, pp.66-95.

Elbannan, M.A., 2015. The capital asset pricing model: an overview of the

theory. International Journal of Economics and Finance, 7(1), pp.216-228.

Elterich, S., FMR LLC, 2014. Financial Account Management. U.S. Patent Application

14/164,558.

Fragkiskos, A., 2014. What is Portfolio Diversification?. Available at SSRN 2331475.

Ibbotson, R.G. and Kim, D.Y., 2014. Risk and return within the stock market: what works

best?. Working Paper, Zebra Capital.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.