LSBM203 Managerial Finance Portfolio: Financial Statement Analysis

VerifiedAdded on 2023/01/03

|19

|3919

|55

Portfolio

AI Summary

This finance portfolio delves into the analysis of financial statements, focusing on two key areas: ratio analysis and investment appraisal techniques. The portfolio examines the financial data of Tesco and Sainsbury, utilizing various ratio analysis methods such as current ratio, quick ratio, net profit margin, gearing ratio, price to earnings ratio, and return on capital employed to evaluate their financial performance. Furthermore, the report explores investment appraisal techniques, specifically the net present value method, to assess different investment options. The analysis includes interpretations of the ratios and their implications for the companies' financial health and investment decisions, providing a comprehensive overview of financial statement analysis and capital budgeting processes within a business context. The portfolio is structured into two main sections, covering the analysis of financial statements and evaluation of investment options through the net present value method.

Portfolio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION.....................................................................3

PORTFOLIO 1...........................................................................3

Ratio analysis..........................................................................3

Limitations of ratio analysis:................................................14

PORTFOLIO 2.........................................................................14

Investment appraisal techniques...........................................14

Limitation of using investment appraisal techniques in long term decision making 16

CONCLUSION........................................................................17

REFERENCES........................................................................18

INTRODUCTION.....................................................................3

PORTFOLIO 1...........................................................................3

Ratio analysis..........................................................................3

Limitations of ratio analysis:................................................14

PORTFOLIO 2.........................................................................14

Investment appraisal techniques...........................................14

Limitation of using investment appraisal techniques in long term decision making 16

CONCLUSION........................................................................17

REFERENCES........................................................................18

INTRODUCTION

In a business firm, the most important thing that is required for taking on the business

operations further is money and finance. Another look aspect in this category is that company

should properly analyse the financial statements. To analyse financial statements, there are

various methods, through which these reports can be monitored and evaluated. To investigate

into financial statements, there are various forms of tests, some of main are ratio analysis, trend

analysis, cash flow statement, etc. The major objective behind this investigation into financial

statements of the company is that it will assist in planning for future course of action. To produce

an efficient strategic planning for future prospects of business, it is essential to look into every

small aspect of financial statements. After inspecting into financial statements, next step is to

look into the process of application of funds and financial resources. The main element in this

aspect is that resources should be allocated in such a way that; they are generating maximum

possible benefits. This process of analysis is called as capital budgeting process. This report is

divided in two segments, first is discussing about analysing financial statements and second part

is focusing on evaluation of various investment options through method of net present value

method. This report will be focusing of financial information of Tesco and Sainsbury, which are

extracted from their financial reports.

PORTFOLIO 1

Ratio analysis

Tesco plc

Name of ratio Calculation Result

2018 2019

Current ratio Current assets/ current

liabilities

13,726 / 19,238

= 0.713484

12668/2

0680

=

0.61257

3

In a business firm, the most important thing that is required for taking on the business

operations further is money and finance. Another look aspect in this category is that company

should properly analyse the financial statements. To analyse financial statements, there are

various methods, through which these reports can be monitored and evaluated. To investigate

into financial statements, there are various forms of tests, some of main are ratio analysis, trend

analysis, cash flow statement, etc. The major objective behind this investigation into financial

statements of the company is that it will assist in planning for future course of action. To produce

an efficient strategic planning for future prospects of business, it is essential to look into every

small aspect of financial statements. After inspecting into financial statements, next step is to

look into the process of application of funds and financial resources. The main element in this

aspect is that resources should be allocated in such a way that; they are generating maximum

possible benefits. This process of analysis is called as capital budgeting process. This report is

divided in two segments, first is discussing about analysing financial statements and second part

is focusing on evaluation of various investment options through method of net present value

method. This report will be focusing of financial information of Tesco and Sainsbury, which are

extracted from their financial reports.

PORTFOLIO 1

Ratio analysis

Tesco plc

Name of ratio Calculation Result

2018 2019

Current ratio Current assets/ current

liabilities

13,726 / 19,238

= 0.713484

12668/2

0680

=

0.61257

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Quick ratio Quick assets/ current

liabilities

4379/ 19238

= 0.227622

3373/ 20680

= 0.163104

Net profit margin Net profit/ total sales (1206/57491)*100

=2.097%

(1322/63911)*100

= 2.068%

Gross profit margin Gross profit/ total sales (3350/57491)*100

= 5.827%

(4144/63911)*100

= 6.484%

Gearing ratio

(Debt to Equity Ratio)

Total debt/ total equity 44862/10480

= 4.280%

49047 / 14858

= 3.301%

P/E ratio Market value per share/

Earnings per share

229/ 9.35

=24.49

213.6/13.65

= 16.97

Earnings per share Income available/ total

number of shares

outstanding

9.35 13.65

Return on capital

employed

Operating profit/ capital

employed

5.13 6.86

Average inventories

turnover period

Net sales/ average

inventory

57491/2282.5

= 25.91 days

63911/2240.5

= 28.52 days.

Dividend pay-out ratio Dividend paid/ net

income

82/1206

= 0.68.

357/1322

= 0.27

Sainsbury plc

Name of ratio Calculation Result

2018 2019

Current ratio Current assets/ current

liabilities

7857/10302

=0.73

7550/11849

=0.63

Quick ratio Quick assets/ current1933/10302 1283/11849

liabilities

4379/ 19238

= 0.227622

3373/ 20680

= 0.163104

Net profit margin Net profit/ total sales (1206/57491)*100

=2.097%

(1322/63911)*100

= 2.068%

Gross profit margin Gross profit/ total sales (3350/57491)*100

= 5.827%

(4144/63911)*100

= 6.484%

Gearing ratio

(Debt to Equity Ratio)

Total debt/ total equity 44862/10480

= 4.280%

49047 / 14858

= 3.301%

P/E ratio Market value per share/

Earnings per share

229/ 9.35

=24.49

213.6/13.65

= 16.97

Earnings per share Income available/ total

number of shares

outstanding

9.35 13.65

Return on capital

employed

Operating profit/ capital

employed

5.13 6.86

Average inventories

turnover period

Net sales/ average

inventory

57491/2282.5

= 25.91 days

63911/2240.5

= 28.52 days.

Dividend pay-out ratio Dividend paid/ net

income

82/1206

= 0.68.

357/1322

= 0.27

Sainsbury plc

Name of ratio Calculation Result

2018 2019

Current ratio Current assets/ current

liabilities

7857/10302

=0.73

7550/11849

=0.63

Quick ratio Quick assets/ current1933/10302 1283/11849

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

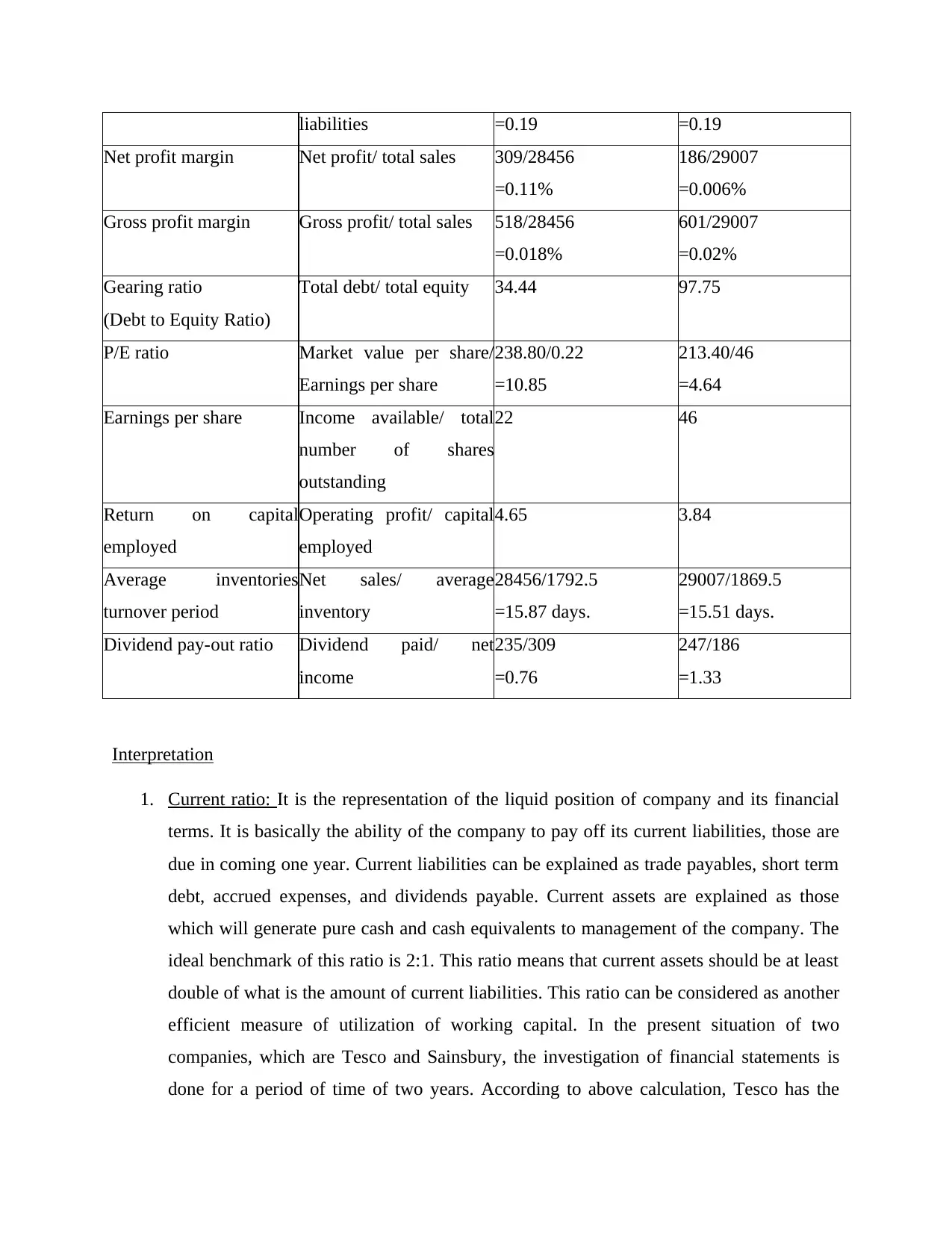

liabilities =0.19 =0.19

Net profit margin Net profit/ total sales 309/28456

=0.11%

186/29007

=0.006%

Gross profit margin Gross profit/ total sales 518/28456

=0.018%

601/29007

=0.02%

Gearing ratio

(Debt to Equity Ratio)

Total debt/ total equity 34.44 97.75

P/E ratio Market value per share/

Earnings per share

238.80/0.22

=10.85

213.40/46

=4.64

Earnings per share Income available/ total

number of shares

outstanding

22 46

Return on capital

employed

Operating profit/ capital

employed

4.65 3.84

Average inventories

turnover period

Net sales/ average

inventory

28456/1792.5

=15.87 days.

29007/1869.5

=15.51 days.

Dividend pay-out ratio Dividend paid/ net

income

235/309

=0.76

247/186

=1.33

Interpretation

1. Current ratio: It is the representation of the liquid position of company and its financial

terms. It is basically the ability of the company to pay off its current liabilities, those are

due in coming one year. Current liabilities can be explained as trade payables, short term

debt, accrued expenses, and dividends payable. Current assets are explained as those

which will generate pure cash and cash equivalents to management of the company. The

ideal benchmark of this ratio is 2:1. This ratio means that current assets should be at least

double of what is the amount of current liabilities. This ratio can be considered as another

efficient measure of utilization of working capital. In the present situation of two

companies, which are Tesco and Sainsbury, the investigation of financial statements is

done for a period of time of two years. According to above calculation, Tesco has the

Net profit margin Net profit/ total sales 309/28456

=0.11%

186/29007

=0.006%

Gross profit margin Gross profit/ total sales 518/28456

=0.018%

601/29007

=0.02%

Gearing ratio

(Debt to Equity Ratio)

Total debt/ total equity 34.44 97.75

P/E ratio Market value per share/

Earnings per share

238.80/0.22

=10.85

213.40/46

=4.64

Earnings per share Income available/ total

number of shares

outstanding

22 46

Return on capital

employed

Operating profit/ capital

employed

4.65 3.84

Average inventories

turnover period

Net sales/ average

inventory

28456/1792.5

=15.87 days.

29007/1869.5

=15.51 days.

Dividend pay-out ratio Dividend paid/ net

income

235/309

=0.76

247/186

=1.33

Interpretation

1. Current ratio: It is the representation of the liquid position of company and its financial

terms. It is basically the ability of the company to pay off its current liabilities, those are

due in coming one year. Current liabilities can be explained as trade payables, short term

debt, accrued expenses, and dividends payable. Current assets are explained as those

which will generate pure cash and cash equivalents to management of the company. The

ideal benchmark of this ratio is 2:1. This ratio means that current assets should be at least

double of what is the amount of current liabilities. This ratio can be considered as another

efficient measure of utilization of working capital. In the present situation of two

companies, which are Tesco and Sainsbury, the investigation of financial statements is

done for a period of time of two years. According to above calculation, Tesco has the

current ratio of 0.71 and 0.61 in year 2018 and 2019. On the other hand, Sainsbury has

the current ratio of 0.73 and 0.63, respectively in same span of time. The position of

liquidity is almost indistinguishable in both the companies. This means they both are

using their working capital according to same policies of working capital. Ratio is not

matching the mark of ideal ratio, as in accordance of ideal ratio current assets should be

twice of what is the volume of current liabilities. The ratio of chosen companies’ low,

hence, it is advisable that company should take care of this fact.

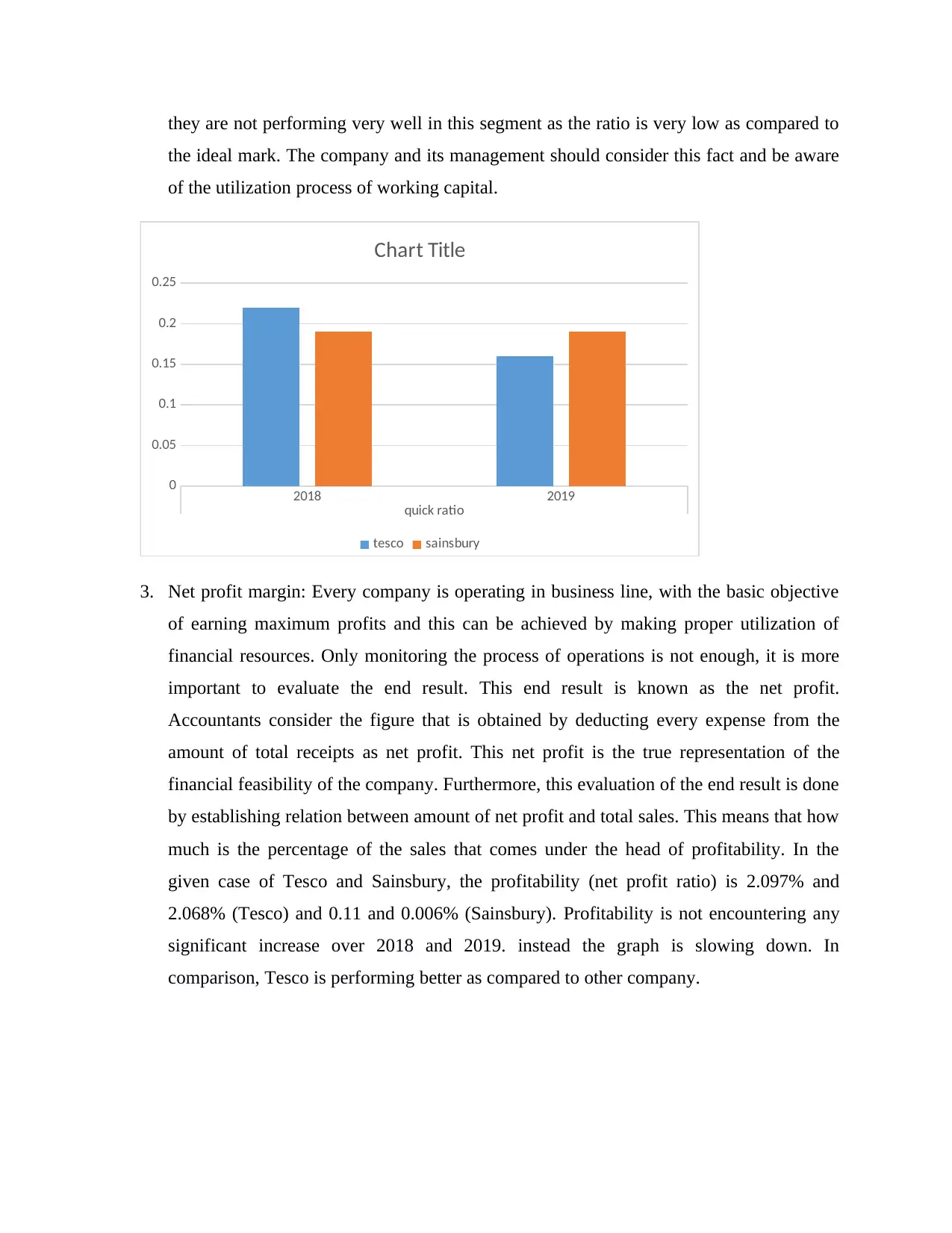

2. Quick ratio: This ratio comes under the category of same liquidity ratio. This is also

making an attempt to develop an understanding of the operational feasibility of the quick

assets or almost liquid assets. This means that is determining the relation of quick assets

and current liabilities. Quick assets are defined as those assets which are almost

equivalent to cash and cash equivalents. This means that they can be easily converted into

cash or are already in cash. Examples of quick assets are cash, marketable securities,

trade receivables, etc. These assets are used to pay off current liabilities. In accordance of

what famous theorists has recognized, the ideal mark for quick ratio is 1:1. This means

that quick assets should be at least equal to current liabilities. This will represent the

situation of perfect liquidity as, if there is some emergency, where immediate cash is

required, then company is in a position to confront that situation with ease. In the present

situation of Tesco and Sainsbury, the quick ratio comes out to be (Tesco- 0.22 and 0.16)

and (Sainsbury-0.19 and 0.19), respectively in year of 2018 and 2019. This means that

the current ratio of 0.73 and 0.63, respectively in same span of time. The position of

liquidity is almost indistinguishable in both the companies. This means they both are

using their working capital according to same policies of working capital. Ratio is not

matching the mark of ideal ratio, as in accordance of ideal ratio current assets should be

twice of what is the volume of current liabilities. The ratio of chosen companies’ low,

hence, it is advisable that company should take care of this fact.

2. Quick ratio: This ratio comes under the category of same liquidity ratio. This is also

making an attempt to develop an understanding of the operational feasibility of the quick

assets or almost liquid assets. This means that is determining the relation of quick assets

and current liabilities. Quick assets are defined as those assets which are almost

equivalent to cash and cash equivalents. This means that they can be easily converted into

cash or are already in cash. Examples of quick assets are cash, marketable securities,

trade receivables, etc. These assets are used to pay off current liabilities. In accordance of

what famous theorists has recognized, the ideal mark for quick ratio is 1:1. This means

that quick assets should be at least equal to current liabilities. This will represent the

situation of perfect liquidity as, if there is some emergency, where immediate cash is

required, then company is in a position to confront that situation with ease. In the present

situation of Tesco and Sainsbury, the quick ratio comes out to be (Tesco- 0.22 and 0.16)

and (Sainsbury-0.19 and 0.19), respectively in year of 2018 and 2019. This means that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

they are not performing very well in this segment as the ratio is very low as compared to

the ideal mark. The company and its management should consider this fact and be aware

of the utilization process of working capital.

2018 2019

quick ratio

0

0.05

0.1

0.15

0.2

0.25

Chart Title

tesco sainsbury

3. Net profit margin: Every company is operating in business line, with the basic objective

of earning maximum profits and this can be achieved by making proper utilization of

financial resources. Only monitoring the process of operations is not enough, it is more

important to evaluate the end result. This end result is known as the net profit.

Accountants consider the figure that is obtained by deducting every expense from the

amount of total receipts as net profit. This net profit is the true representation of the

financial feasibility of the company. Furthermore, this evaluation of the end result is done

by establishing relation between amount of net profit and total sales. This means that how

much is the percentage of the sales that comes under the head of profitability. In the

given case of Tesco and Sainsbury, the profitability (net profit ratio) is 2.097% and

2.068% (Tesco) and 0.11 and 0.006% (Sainsbury). Profitability is not encountering any

significant increase over 2018 and 2019. instead the graph is slowing down. In

comparison, Tesco is performing better as compared to other company.

the ideal mark. The company and its management should consider this fact and be aware

of the utilization process of working capital.

2018 2019

quick ratio

0

0.05

0.1

0.15

0.2

0.25

Chart Title

tesco sainsbury

3. Net profit margin: Every company is operating in business line, with the basic objective

of earning maximum profits and this can be achieved by making proper utilization of

financial resources. Only monitoring the process of operations is not enough, it is more

important to evaluate the end result. This end result is known as the net profit.

Accountants consider the figure that is obtained by deducting every expense from the

amount of total receipts as net profit. This net profit is the true representation of the

financial feasibility of the company. Furthermore, this evaluation of the end result is done

by establishing relation between amount of net profit and total sales. This means that how

much is the percentage of the sales that comes under the head of profitability. In the

given case of Tesco and Sainsbury, the profitability (net profit ratio) is 2.097% and

2.068% (Tesco) and 0.11 and 0.006% (Sainsbury). Profitability is not encountering any

significant increase over 2018 and 2019. instead the graph is slowing down. In

comparison, Tesco is performing better as compared to other company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

tesco sainsbury

0

0.5

1

1.5

2

2.5

Chart Title

net profit ratio 2018 net profit ratio 2019

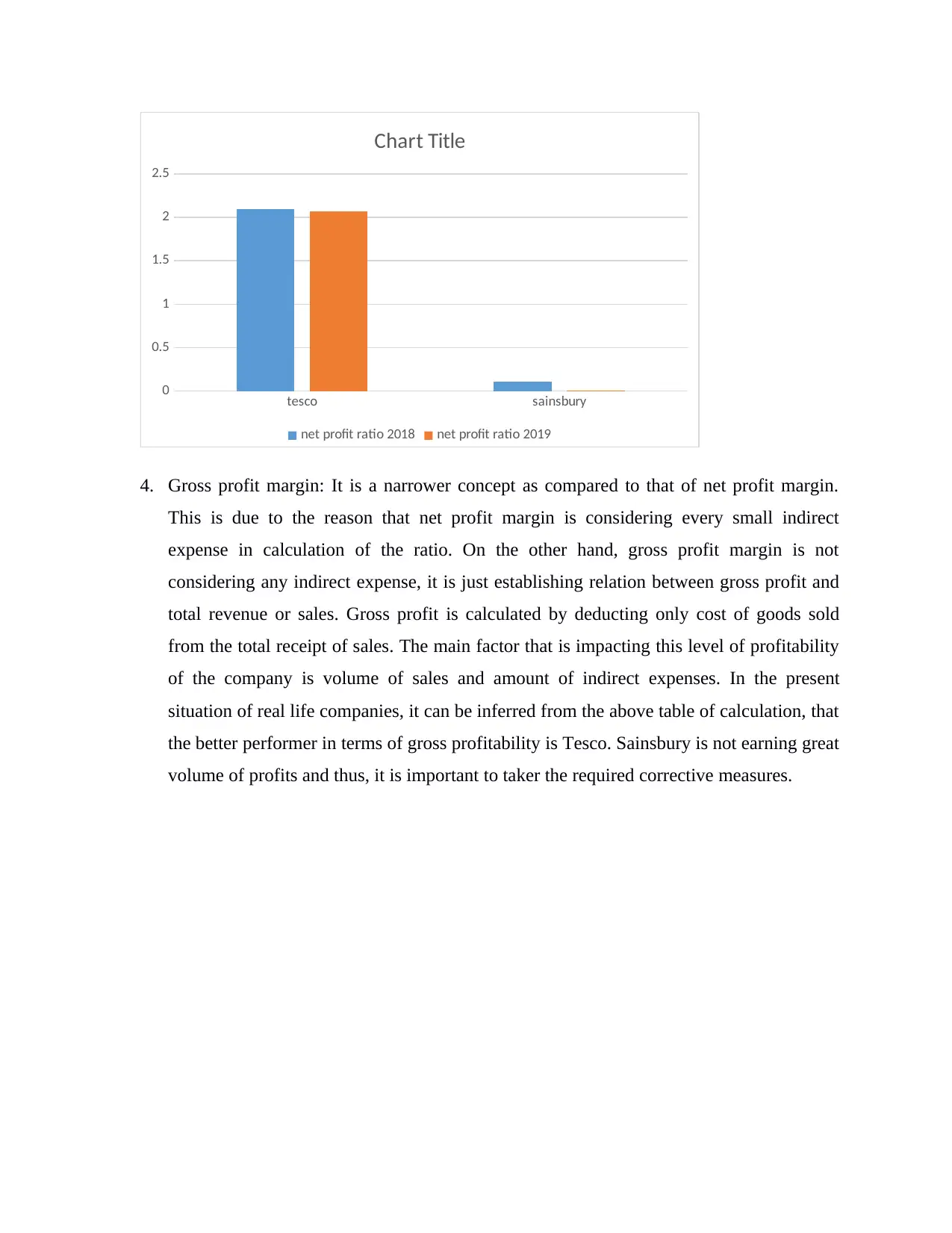

4. Gross profit margin: It is a narrower concept as compared to that of net profit margin.

This is due to the reason that net profit margin is considering every small indirect

expense in calculation of the ratio. On the other hand, gross profit margin is not

considering any indirect expense, it is just establishing relation between gross profit and

total revenue or sales. Gross profit is calculated by deducting only cost of goods sold

from the total receipt of sales. The main factor that is impacting this level of profitability

of the company is volume of sales and amount of indirect expenses. In the present

situation of real life companies, it can be inferred from the above table of calculation, that

the better performer in terms of gross profitability is Tesco. Sainsbury is not earning great

volume of profits and thus, it is important to taker the required corrective measures.

0

0.5

1

1.5

2

2.5

Chart Title

net profit ratio 2018 net profit ratio 2019

4. Gross profit margin: It is a narrower concept as compared to that of net profit margin.

This is due to the reason that net profit margin is considering every small indirect

expense in calculation of the ratio. On the other hand, gross profit margin is not

considering any indirect expense, it is just establishing relation between gross profit and

total revenue or sales. Gross profit is calculated by deducting only cost of goods sold

from the total receipt of sales. The main factor that is impacting this level of profitability

of the company is volume of sales and amount of indirect expenses. In the present

situation of real life companies, it can be inferred from the above table of calculation, that

the better performer in terms of gross profitability is Tesco. Sainsbury is not earning great

volume of profits and thus, it is important to taker the required corrective measures.

tesco sainsbury

0

0.5

1

1.5

2

2.5

Chart Title

gross profit ratio 2018 gross profit ratio 2019

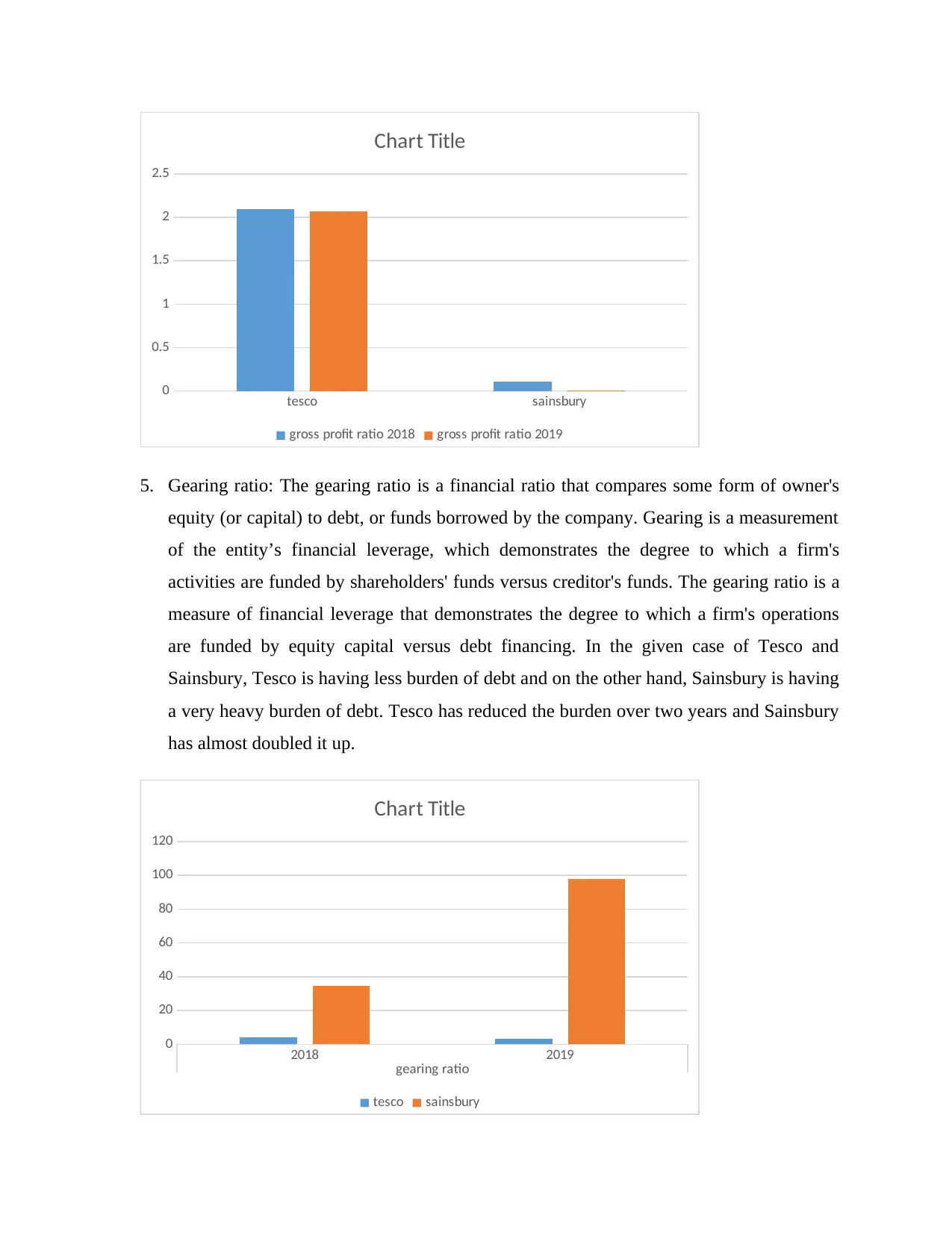

5. Gearing ratio: The gearing ratio is a financial ratio that compares some form of owner's

equity (or capital) to debt, or funds borrowed by the company. Gearing is a measurement

of the entity’s financial leverage, which demonstrates the degree to which a firm's

activities are funded by shareholders' funds versus creditor's funds. The gearing ratio is a

measure of financial leverage that demonstrates the degree to which a firm's operations

are funded by equity capital versus debt financing. In the given case of Tesco and

Sainsbury, Tesco is having less burden of debt and on the other hand, Sainsbury is having

a very heavy burden of debt. Tesco has reduced the burden over two years and Sainsbury

has almost doubled it up.

2018 2019

gearing ratio

0

20

40

60

80

100

120

Chart Title

tesco sainsbury

0

0.5

1

1.5

2

2.5

Chart Title

gross profit ratio 2018 gross profit ratio 2019

5. Gearing ratio: The gearing ratio is a financial ratio that compares some form of owner's

equity (or capital) to debt, or funds borrowed by the company. Gearing is a measurement

of the entity’s financial leverage, which demonstrates the degree to which a firm's

activities are funded by shareholders' funds versus creditor's funds. The gearing ratio is a

measure of financial leverage that demonstrates the degree to which a firm's operations

are funded by equity capital versus debt financing. In the given case of Tesco and

Sainsbury, Tesco is having less burden of debt and on the other hand, Sainsbury is having

a very heavy burden of debt. Tesco has reduced the burden over two years and Sainsbury

has almost doubled it up.

2018 2019

gearing ratio

0

20

40

60

80

100

120

Chart Title

tesco sainsbury

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

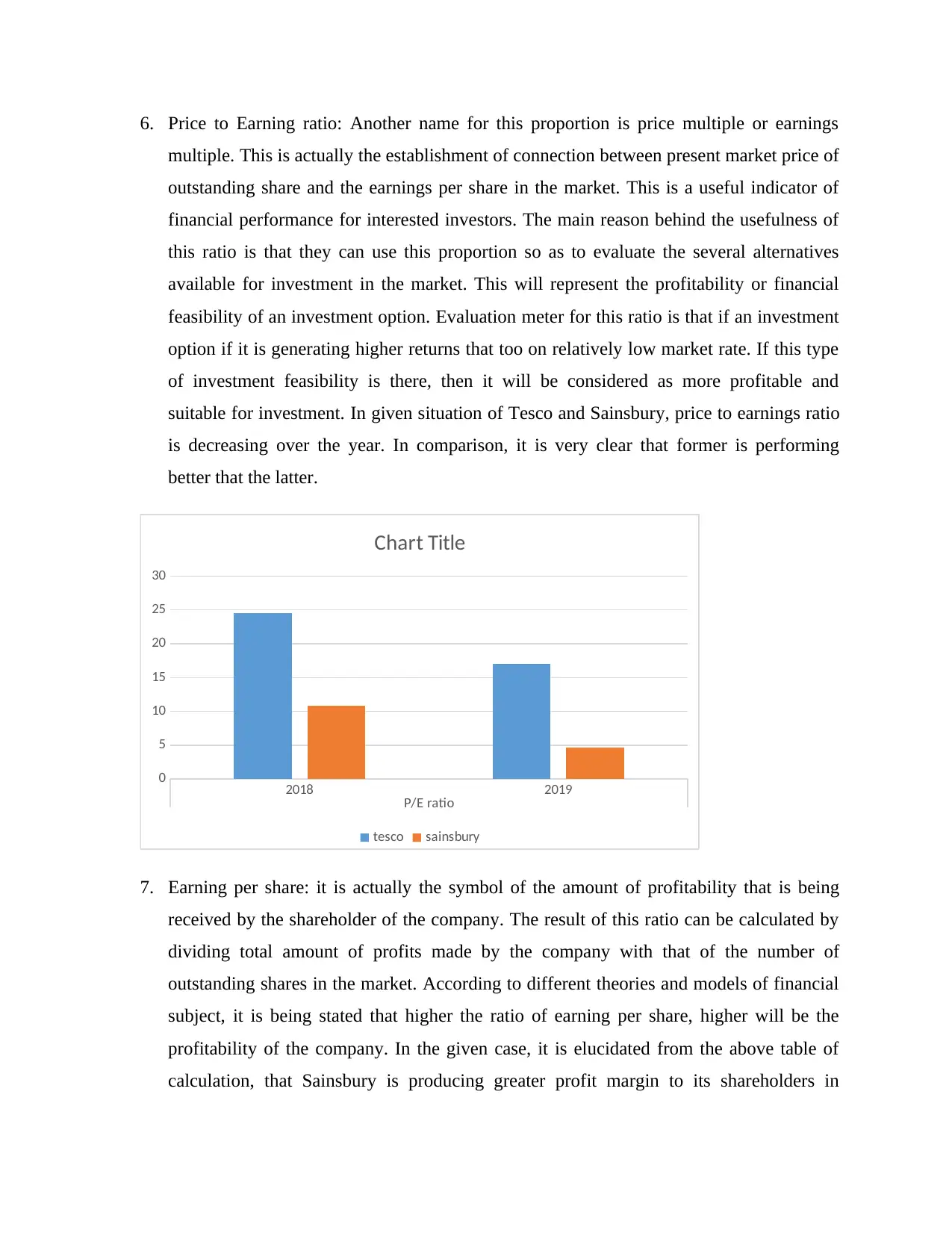

6. Price to Earning ratio: Another name for this proportion is price multiple or earnings

multiple. This is actually the establishment of connection between present market price of

outstanding share and the earnings per share in the market. This is a useful indicator of

financial performance for interested investors. The main reason behind the usefulness of

this ratio is that they can use this proportion so as to evaluate the several alternatives

available for investment in the market. This will represent the profitability or financial

feasibility of an investment option. Evaluation meter for this ratio is that if an investment

option if it is generating higher returns that too on relatively low market rate. If this type

of investment feasibility is there, then it will be considered as more profitable and

suitable for investment. In given situation of Tesco and Sainsbury, price to earnings ratio

is decreasing over the year. In comparison, it is very clear that former is performing

better that the latter.

2018 2019

P/E ratio

0

5

10

15

20

25

30

Chart Title

tesco sainsbury

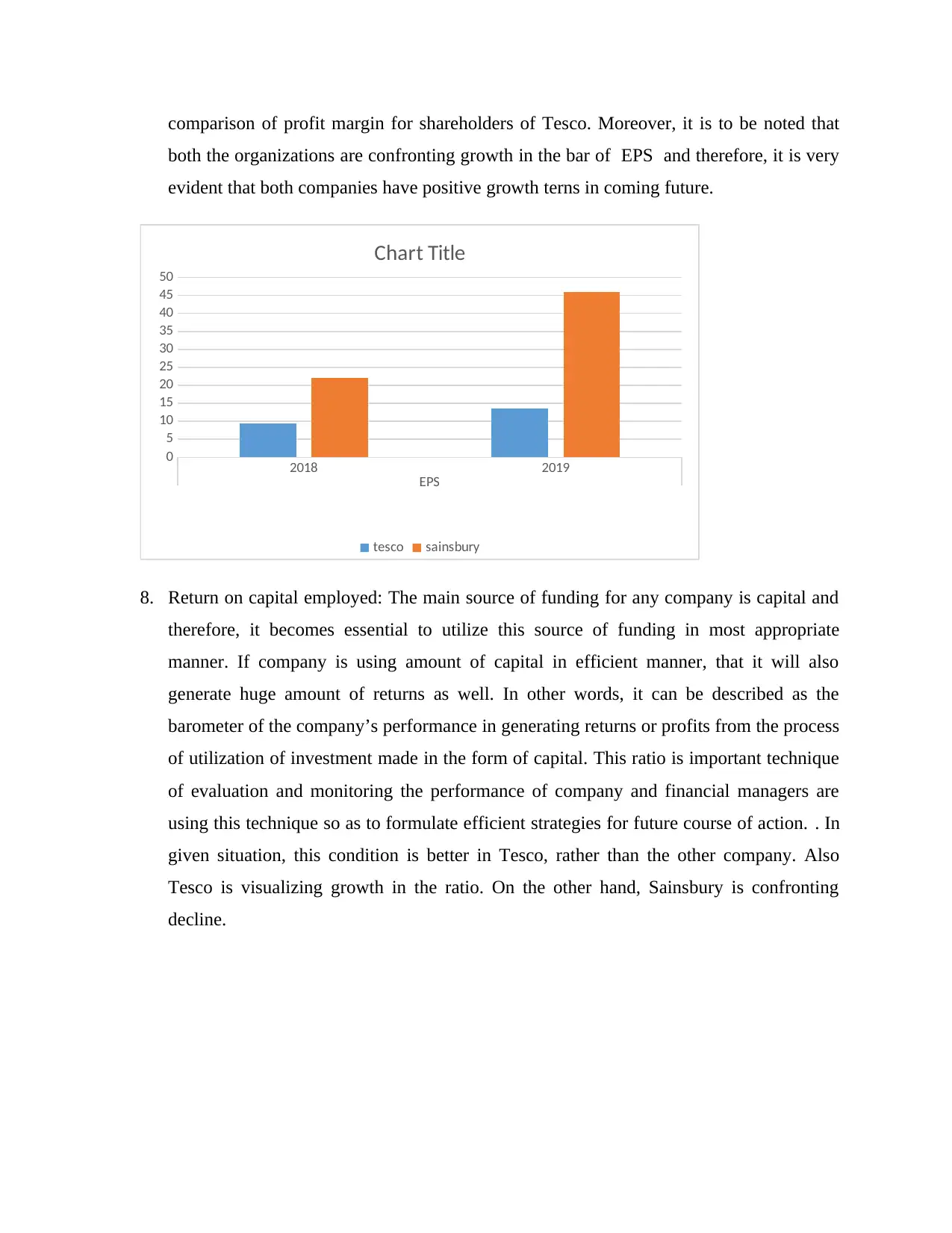

7. Earning per share: it is actually the symbol of the amount of profitability that is being

received by the shareholder of the company. The result of this ratio can be calculated by

dividing total amount of profits made by the company with that of the number of

outstanding shares in the market. According to different theories and models of financial

subject, it is being stated that higher the ratio of earning per share, higher will be the

profitability of the company. In the given case, it is elucidated from the above table of

calculation, that Sainsbury is producing greater profit margin to its shareholders in

multiple. This is actually the establishment of connection between present market price of

outstanding share and the earnings per share in the market. This is a useful indicator of

financial performance for interested investors. The main reason behind the usefulness of

this ratio is that they can use this proportion so as to evaluate the several alternatives

available for investment in the market. This will represent the profitability or financial

feasibility of an investment option. Evaluation meter for this ratio is that if an investment

option if it is generating higher returns that too on relatively low market rate. If this type

of investment feasibility is there, then it will be considered as more profitable and

suitable for investment. In given situation of Tesco and Sainsbury, price to earnings ratio

is decreasing over the year. In comparison, it is very clear that former is performing

better that the latter.

2018 2019

P/E ratio

0

5

10

15

20

25

30

Chart Title

tesco sainsbury

7. Earning per share: it is actually the symbol of the amount of profitability that is being

received by the shareholder of the company. The result of this ratio can be calculated by

dividing total amount of profits made by the company with that of the number of

outstanding shares in the market. According to different theories and models of financial

subject, it is being stated that higher the ratio of earning per share, higher will be the

profitability of the company. In the given case, it is elucidated from the above table of

calculation, that Sainsbury is producing greater profit margin to its shareholders in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

comparison of profit margin for shareholders of Tesco. Moreover, it is to be noted that

both the organizations are confronting growth in the bar of EPS and therefore, it is very

evident that both companies have positive growth terns in coming future.

2018 2019

EPS

0

5

10

15

20

25

30

35

40

45

50

Chart Title

tesco sainsbury

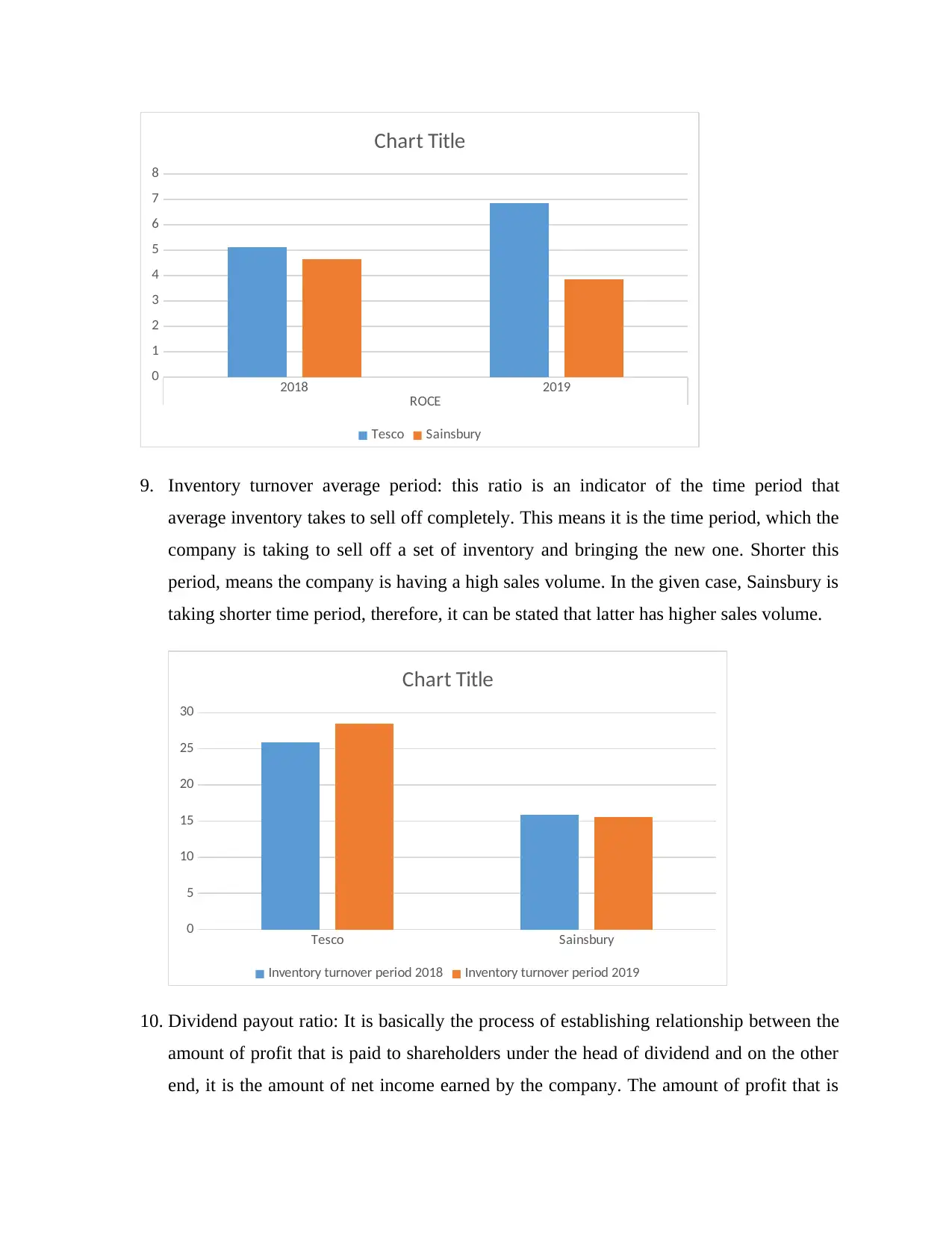

8. Return on capital employed: The main source of funding for any company is capital and

therefore, it becomes essential to utilize this source of funding in most appropriate

manner. If company is using amount of capital in efficient manner, that it will also

generate huge amount of returns as well. In other words, it can be described as the

barometer of the company’s performance in generating returns or profits from the process

of utilization of investment made in the form of capital. This ratio is important technique

of evaluation and monitoring the performance of company and financial managers are

using this technique so as to formulate efficient strategies for future course of action. . In

given situation, this condition is better in Tesco, rather than the other company. Also

Tesco is visualizing growth in the ratio. On the other hand, Sainsbury is confronting

decline.

both the organizations are confronting growth in the bar of EPS and therefore, it is very

evident that both companies have positive growth terns in coming future.

2018 2019

EPS

0

5

10

15

20

25

30

35

40

45

50

Chart Title

tesco sainsbury

8. Return on capital employed: The main source of funding for any company is capital and

therefore, it becomes essential to utilize this source of funding in most appropriate

manner. If company is using amount of capital in efficient manner, that it will also

generate huge amount of returns as well. In other words, it can be described as the

barometer of the company’s performance in generating returns or profits from the process

of utilization of investment made in the form of capital. This ratio is important technique

of evaluation and monitoring the performance of company and financial managers are

using this technique so as to formulate efficient strategies for future course of action. . In

given situation, this condition is better in Tesco, rather than the other company. Also

Tesco is visualizing growth in the ratio. On the other hand, Sainsbury is confronting

decline.

2018 2019

ROCE

0

1

2

3

4

5

6

7

8

Chart Title

Tesco Sainsbury

9. Inventory turnover average period: this ratio is an indicator of the time period that

average inventory takes to sell off completely. This means it is the time period, which the

company is taking to sell off a set of inventory and bringing the new one. Shorter this

period, means the company is having a high sales volume. In the given case, Sainsbury is

taking shorter time period, therefore, it can be stated that latter has higher sales volume.

Tesco Sainsbury

0

5

10

15

20

25

30

Chart Title

Inventory turnover period 2018 Inventory turnover period 2019

10. Dividend payout ratio: It is basically the process of establishing relationship between the

amount of profit that is paid to shareholders under the head of dividend and on the other

end, it is the amount of net income earned by the company. The amount of profit that is

ROCE

0

1

2

3

4

5

6

7

8

Chart Title

Tesco Sainsbury

9. Inventory turnover average period: this ratio is an indicator of the time period that

average inventory takes to sell off completely. This means it is the time period, which the

company is taking to sell off a set of inventory and bringing the new one. Shorter this

period, means the company is having a high sales volume. In the given case, Sainsbury is

taking shorter time period, therefore, it can be stated that latter has higher sales volume.

Tesco Sainsbury

0

5

10

15

20

25

30

Chart Title

Inventory turnover period 2018 Inventory turnover period 2019

10. Dividend payout ratio: It is basically the process of establishing relationship between the

amount of profit that is paid to shareholders under the head of dividend and on the other

end, it is the amount of net income earned by the company. The amount of profit that is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.