Managing Financial Principles and Techniques for Miramar Hotel

VerifiedAdded on 2020/01/28

|17

|5926

|61

Report

AI Summary

This report provides a comprehensive analysis of financial principles and techniques, focusing on their application within a business context, specifically using the Miramar Hotel as a case study. The report begins by categorizing costs and exploring various costing systems, including job order, process, and activity-based costing, and their relevance to pricing decisions. It then delves into budgeting, including the moving average methodology, master budget construction, and variance analysis. Furthermore, the report examines project evaluation techniques, such as payback period, net present value, and internal rate of return, alongside sources of finance and post-appraisal audits. Finally, the report includes an analysis of profitability ratios and provides recommendations for improving financial performance. The report concludes with a comparative analysis of investment appraisal techniques in the public and private sectors.

MANAGING FINANCIAL

PRINCIPLES AND

TECHNQUES

PRINCIPLES AND

TECHNQUES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

(a) Different means of categorizing cost and their applications to products and services..........3

(B) Costing system for an organization......................................................................................4

(c) Role of cost in organization pricing decisions and improvements in the costing and pricing

systems........................................................................................................................................5

(d) Process that can reduce cost .................................................................................................6

(e) Appropriateness of activity based costing for identifying full cost.......................................6

TASK 2............................................................................................................................................7

(a) Moving average methodology...............................................................................................7

(b) Good practice to be considered in both construction of master budget and budgetary

monitoring and control ...............................................................................................................7

(c) Conformity of practices with the budget monitoring and control.........................................8

(d) Comparison of budget with actual figures.............................................................................8

TASK 3............................................................................................................................................9

(a) Project evaluation technique .................................................................................................9

(b) Strength and weakness of above appraisal techniques........................................................10

(c) Recommendation on selection of project............................................................................10

(e) Possible source of finance and its advantages as well as limitations..................................11

(f) Post appraisal audit and effectiveness of investment decision-making...............................11

(g) Main difference between investment appraisal techniques of public and private sector

...................................................................................................................................................12

TASK 4 .........................................................................................................................................12

(a) Profitability of company for two years................................................................................12

(b) Recommendation of the firm performance..........................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

APPENDIX....................................................................................................................................17

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

(a) Different means of categorizing cost and their applications to products and services..........3

(B) Costing system for an organization......................................................................................4

(c) Role of cost in organization pricing decisions and improvements in the costing and pricing

systems........................................................................................................................................5

(d) Process that can reduce cost .................................................................................................6

(e) Appropriateness of activity based costing for identifying full cost.......................................6

TASK 2............................................................................................................................................7

(a) Moving average methodology...............................................................................................7

(b) Good practice to be considered in both construction of master budget and budgetary

monitoring and control ...............................................................................................................7

(c) Conformity of practices with the budget monitoring and control.........................................8

(d) Comparison of budget with actual figures.............................................................................8

TASK 3............................................................................................................................................9

(a) Project evaluation technique .................................................................................................9

(b) Strength and weakness of above appraisal techniques........................................................10

(c) Recommendation on selection of project............................................................................10

(e) Possible source of finance and its advantages as well as limitations..................................11

(f) Post appraisal audit and effectiveness of investment decision-making...............................11

(g) Main difference between investment appraisal techniques of public and private sector

...................................................................................................................................................12

TASK 4 .........................................................................................................................................12

(a) Profitability of company for two years................................................................................12

(b) Recommendation of the firm performance..........................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

APPENDIX....................................................................................................................................17

INTRODUCTION

Finance is a considered as life blood for every organization and with out it, it business

can notcannot survive in the industry. In the report, financial isuesissues are discussed in detail.

Miramar hotel is located in the Hong Kong and it is a well establishedwell-established hotel in

the mentioned region. It also have has some of the restaurants in specific locations. Finance and

cost both play an important role in the success and failure of an organization. In the present

report, sources of finance are recommended to the firm for the project finance. Along with this,

project evaluation techniques are also applied on the firm cash flows. Apart from this, costs are

classified and there categories are explained in detail in the report. Along with this, costCost

systems are also explained and same for the firm is designed. Relevant to this, cost and price

systems are explained in the report. After that, moving average is calculated and budget is

prepared. By comparing actual figures with budget, variance is identified and possible reasons

for the variance of in results are identified. At the end of the report, gross profit and net profit

ratio is are also calculated and comments on the same is are done.

TASK 1

(a) Different means of categorizing cost and their applications to products and services

Following are the different means of categorizing cost. Some of them are as follows. Fixed cost- It refers to the cost that never gets changed and remains fix during whole life

time of the firm. Miramar ltd is a hotel and restaurant chain in the Hong Kong and it have

has huge facility. Investment that it made makes in for the establishment of machinery in

its plant is the best example of the fixed cost. The cost of same cannot be changed until

the time up to which they are infixed cost is used in the firm. With passage of time, fixed

cost of the firm gets increased. This is because as with passage of time firm increased

increases its production capacity (Zimmerman and Yahya-Zadeh, 2011). In order to

increase production capacity, it is necessary to purchase machines. Hence, fixed cost of

machine remains same but with purchase of new machines, fixed cost of the firms gets

increased and it also applied applies on the firm’s product and services. Variable cost- Variable cost is a cost that keeps on changing continuously. If, production

gets increased then per unit variable cost gets declined. Miramar group is operating as a

Finance is a considered as life blood for every organization and with out it, it business

can notcannot survive in the industry. In the report, financial isuesissues are discussed in detail.

Miramar hotel is located in the Hong Kong and it is a well establishedwell-established hotel in

the mentioned region. It also have has some of the restaurants in specific locations. Finance and

cost both play an important role in the success and failure of an organization. In the present

report, sources of finance are recommended to the firm for the project finance. Along with this,

project evaluation techniques are also applied on the firm cash flows. Apart from this, costs are

classified and there categories are explained in detail in the report. Along with this, costCost

systems are also explained and same for the firm is designed. Relevant to this, cost and price

systems are explained in the report. After that, moving average is calculated and budget is

prepared. By comparing actual figures with budget, variance is identified and possible reasons

for the variance of in results are identified. At the end of the report, gross profit and net profit

ratio is are also calculated and comments on the same is are done.

TASK 1

(a) Different means of categorizing cost and their applications to products and services

Following are the different means of categorizing cost. Some of them are as follows. Fixed cost- It refers to the cost that never gets changed and remains fix during whole life

time of the firm. Miramar ltd is a hotel and restaurant chain in the Hong Kong and it have

has huge facility. Investment that it made makes in for the establishment of machinery in

its plant is the best example of the fixed cost. The cost of same cannot be changed until

the time up to which they are infixed cost is used in the firm. With passage of time, fixed

cost of the firm gets increased. This is because as with passage of time firm increased

increases its production capacity (Zimmerman and Yahya-Zadeh, 2011). In order to

increase production capacity, it is necessary to purchase machines. Hence, fixed cost of

machine remains same but with purchase of new machines, fixed cost of the firms gets

increased and it also applied applies on the firm’s product and services. Variable cost- Variable cost is a cost that keeps on changing continuously. If, production

gets increased then per unit variable cost gets declined. Miramar group is operating as a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

restaurant chain in which it provides Chinese, Japanese and South East Asia food items.

Therefore, it needs to import some of the items and need requires to purchase food items

from domestic people. Cost of food items keeps on changing steadily and in recession,

their price is increasing increases continuously. Hence Thus, variable cost of the firm is

changing with passage of time. Hence, this cost apply applies to firm’s product or

services.

Semi variable cost- Semi variable cost refers to the cost who’s whose some part is fixed

and some part is variable. Part that is fixed always remains same and part that is variable

is vary from time to time (Qian, Burritt and Monroe, 2011). In Miramar group, specific

number of employees are employed and it is a fixed cost. But if, firm employee employs

people above this limit then it will become variable cost because number of labor are

changed in the an organzationorganization. Hence, employee labor cost at Miramar hotel

is a semi variable in nature.

(B) Costing system for an organization

Following are the costing system that can be used in an organization. Job order costing- In job order costing, cost for all the products is measures measured

and recorded separately. This method is employed by the firm when it is producing

multiple products that are different from each other. If, we look at the Miramar group

products then it can be seen that its products are not different and it is providing same

services in its to all its customersbusiness. Hence, this costing system is not appropriate

for the firm. Process costing- Process costing is different from job order costing because in process

costing, the cost for entire process is recorded step by step (Tayler, 2010). For producing

food items, firm is purchasing products from domestic and foreign people. After

purchasing raw products, it process them starts processing and produces finished items.

In this entire process, it uses electricity and performs many steps. Under this costing

system, firm will measure cost for each and every step separately. These costs will also

be recorded separately. After the end of the process, finally entire cost is computed and in

this way, this cost system is used by the Miramar hotel to measure and record cost.

Therefore, it needs to import some of the items and need requires to purchase food items

from domestic people. Cost of food items keeps on changing steadily and in recession,

their price is increasing increases continuously. Hence Thus, variable cost of the firm is

changing with passage of time. Hence, this cost apply applies to firm’s product or

services.

Semi variable cost- Semi variable cost refers to the cost who’s whose some part is fixed

and some part is variable. Part that is fixed always remains same and part that is variable

is vary from time to time (Qian, Burritt and Monroe, 2011). In Miramar group, specific

number of employees are employed and it is a fixed cost. But if, firm employee employs

people above this limit then it will become variable cost because number of labor are

changed in the an organzationorganization. Hence, employee labor cost at Miramar hotel

is a semi variable in nature.

(B) Costing system for an organization

Following are the costing system that can be used in an organization. Job order costing- In job order costing, cost for all the products is measures measured

and recorded separately. This method is employed by the firm when it is producing

multiple products that are different from each other. If, we look at the Miramar group

products then it can be seen that its products are not different and it is providing same

services in its to all its customersbusiness. Hence, this costing system is not appropriate

for the firm. Process costing- Process costing is different from job order costing because in process

costing, the cost for entire process is recorded step by step (Tayler, 2010). For producing

food items, firm is purchasing products from domestic and foreign people. After

purchasing raw products, it process them starts processing and produces finished items.

In this entire process, it uses electricity and performs many steps. Under this costing

system, firm will measure cost for each and every step separately. These costs will also

be recorded separately. After the end of the process, finally entire cost is computed and in

this way, this cost system is used by the Miramar hotel to measure and record cost.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity based costing- In activity based costing, all activities that are performed in

production are identified and cost of these activities is identified also calculated. Finally,

cost of these activities are added in order to find out the final cost of the product.

Miramar hotel can either use process system or it can design a new system under which process

costing and activity based costing system will be added (Scapens and Bromwich, 2010). Under

this new system, all the activities that are performed in the under =process of specific product

production producing specific product will be identified and costing of same will be done. By

adding costs of all the activities of a single process, cost of each and every process will be

identified. After that, costs of these process will be added to find out the entire cost of

production. In this way, new costing system will bring efficiency in the costing operations of the

Miramar hotel.

(c) Role of cost in organization pricing decisions and improvements in the costing and pricing

systems

Cost plays an very important role in the organization’s cost and pricing decisions. This is

because the cost acts as a foundation for the determination of price in case of every firm. With

change in cost, price of the product also gets changed. As per the economics concepts, variable

cost is a cost that keeps on changing continuously. With increase in production, costits of per

unit gets reduced per unit. In the today era, firms are competing with each other on the basis of

price. Hence, in order to win a competition competitive advantage, firms take certain measures to

reduce their cost and to generate economies of scale. Miramar hotel can purchase raw material in

bulk in order to reduce the production cost. Due to purchase in bulk, firm will get discount. This

will generate economies of scale. Hence, cost of production for the firm will be reduced to a

larger extent (Van Helden and Northcott, 2010). Due to reduction in cost, Miramar hotel can

reduce the price of its products. From this, it is clear that cost plays an important role in the

firm’s pricing decisions.

Costing system is an essential system that is used to monitor expenses and to control the

same. It may can be considered as a form of spreadsheet or paper table in which all the costs are

recorded. In order to improve costing system, it is necessary to evaluate complexity of the in the

company’s operations. Along with this, spreadsheet that is used to record expenses also needs to

be evaluated. If, spreadsheet is not as per the complexity of operations then it is possible that all

expenses are not recorded. It may be possible that they are have recorded but not in a proper

production are identified and cost of these activities is identified also calculated. Finally,

cost of these activities are added in order to find out the final cost of the product.

Miramar hotel can either use process system or it can design a new system under which process

costing and activity based costing system will be added (Scapens and Bromwich, 2010). Under

this new system, all the activities that are performed in the under =process of specific product

production producing specific product will be identified and costing of same will be done. By

adding costs of all the activities of a single process, cost of each and every process will be

identified. After that, costs of these process will be added to find out the entire cost of

production. In this way, new costing system will bring efficiency in the costing operations of the

Miramar hotel.

(c) Role of cost in organization pricing decisions and improvements in the costing and pricing

systems

Cost plays an very important role in the organization’s cost and pricing decisions. This is

because the cost acts as a foundation for the determination of price in case of every firm. With

change in cost, price of the product also gets changed. As per the economics concepts, variable

cost is a cost that keeps on changing continuously. With increase in production, costits of per

unit gets reduced per unit. In the today era, firms are competing with each other on the basis of

price. Hence, in order to win a competition competitive advantage, firms take certain measures to

reduce their cost and to generate economies of scale. Miramar hotel can purchase raw material in

bulk in order to reduce the production cost. Due to purchase in bulk, firm will get discount. This

will generate economies of scale. Hence, cost of production for the firm will be reduced to a

larger extent (Van Helden and Northcott, 2010). Due to reduction in cost, Miramar hotel can

reduce the price of its products. From this, it is clear that cost plays an important role in the

firm’s pricing decisions.

Costing system is an essential system that is used to monitor expenses and to control the

same. It may can be considered as a form of spreadsheet or paper table in which all the costs are

recorded. In order to improve costing system, it is necessary to evaluate complexity of the in the

company’s operations. Along with this, spreadsheet that is used to record expenses also needs to

be evaluated. If, spreadsheet is not as per the complexity of operations then it is possible that all

expenses are not recorded. It may be possible that they are have recorded but not in a proper

manner. Hence, spreadsheet can be modified and under different process, specific expenses can

be recorded. This will help in the segregation of expenses and will also play a supportive role to

process the cost accounting system (Pipan and Czarniawska, 2010). Hence, it can be said that

above mentioned changesthis change in the cost system will play a supportive role to the process

costing system of Miramar hotel.

(d) Process that can reduce cost

There is a concept of economies of scale that is widely used in economics as a discipline.

As per this concept, firms can take many steps that will lead to the reduction in its cost. In this

regard, firm can increase its production capacity. Entire cost of production has two components;

one is fixed and one is variable. When, production gets increased the then proportion of both the

components of cost get reduced as per the unit produced. Hence, Miramar can increase its

productivity in terms of services and food items. In respect to this, it can launch new food items.

Due to all these efforts, people consumption level of service will be increased at Miramar hotel

and economies of scale will be generated. Hence, per unit cost will be reduced reduce and

profitability of the Miramar hotel will get increased. Food production includes purchase

purchasing of raw items and its processing at the workplace. Hence, purchase can be divided in

to these two parts (Merchant, 2010). In the first stage of process, Miramar hotel can purchase

raw items in large quantity and at different rates. This will lead to adjustment in cost. Besides

this, due to purchase in bulk, firm will get discount. This will lead to savings in save cost. Thus,

by doing this, cost of process food production can be reduced by the Miramar.

(e) Appropriateness of activity based costing for identifying full cost

Activity based costing is an appropriate method for identifying full cost. This is because

in this method, cost is computed by calculating cost of each and every activity. After doing so,

all these costs are added back in order to compute final cost of the product. This method is

appropriate for identifying full cost because in this, all the activities that are performed to

produce a product are considered in calculation. Thus, by employing this method, cost can be

calculated in an accurate manner (Lambert and Sponem, 2012). Due to this reason, activity based

costing system is widely used by the business firms in comparison to the other tool of cost

computation. The main benefit of this method is that in this technique, all the activities that firm

is performed performs to prepare a product are identified. Hence, by using this technique, cost

accountant comes to know about the expenses which are made in with a large amount. By

be recorded. This will help in the segregation of expenses and will also play a supportive role to

process the cost accounting system (Pipan and Czarniawska, 2010). Hence, it can be said that

above mentioned changesthis change in the cost system will play a supportive role to the process

costing system of Miramar hotel.

(d) Process that can reduce cost

There is a concept of economies of scale that is widely used in economics as a discipline.

As per this concept, firms can take many steps that will lead to the reduction in its cost. In this

regard, firm can increase its production capacity. Entire cost of production has two components;

one is fixed and one is variable. When, production gets increased the then proportion of both the

components of cost get reduced as per the unit produced. Hence, Miramar can increase its

productivity in terms of services and food items. In respect to this, it can launch new food items.

Due to all these efforts, people consumption level of service will be increased at Miramar hotel

and economies of scale will be generated. Hence, per unit cost will be reduced reduce and

profitability of the Miramar hotel will get increased. Food production includes purchase

purchasing of raw items and its processing at the workplace. Hence, purchase can be divided in

to these two parts (Merchant, 2010). In the first stage of process, Miramar hotel can purchase

raw items in large quantity and at different rates. This will lead to adjustment in cost. Besides

this, due to purchase in bulk, firm will get discount. This will lead to savings in save cost. Thus,

by doing this, cost of process food production can be reduced by the Miramar.

(e) Appropriateness of activity based costing for identifying full cost

Activity based costing is an appropriate method for identifying full cost. This is because

in this method, cost is computed by calculating cost of each and every activity. After doing so,

all these costs are added back in order to compute final cost of the product. This method is

appropriate for identifying full cost because in this, all the activities that are performed to

produce a product are considered in calculation. Thus, by employing this method, cost can be

calculated in an accurate manner (Lambert and Sponem, 2012). Due to this reason, activity based

costing system is widely used by the business firms in comparison to the other tool of cost

computation. The main benefit of this method is that in this technique, all the activities that firm

is performed performs to prepare a product are identified. Hence, by using this technique, cost

accountant comes to know about the expenses which are made in with a large amount. By

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

comparing with old data, cost accountant is able to identify activities in which it makes

extravagance. Hence, activity based costing method helps in the identification of full cost.

TASK 2

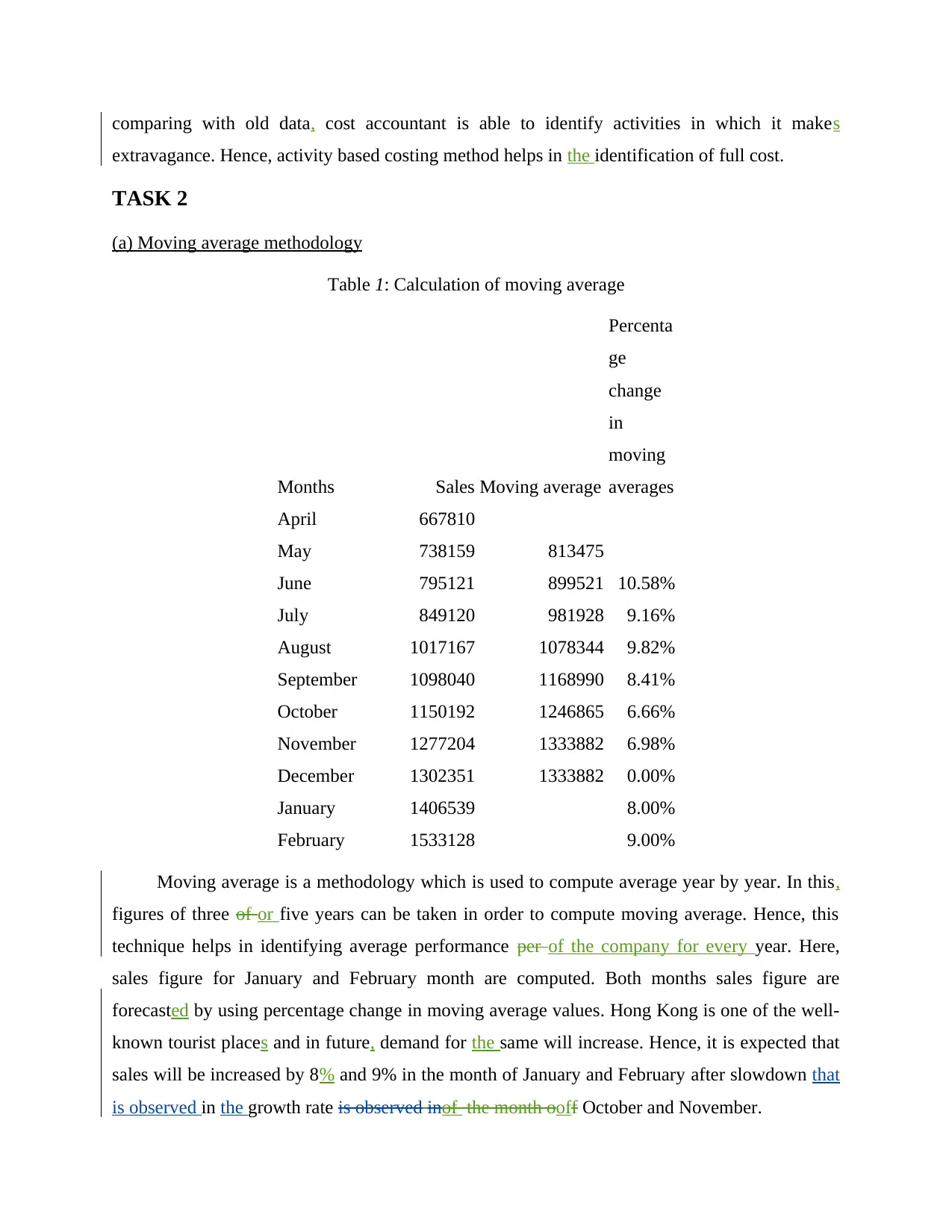

(a) Moving average methodology

Table 1: Calculation of moving average

Months Sales Moving average

Percenta

ge

change

in

moving

averages

April 667810

May 738159 813475

June 795121 899521 10.58%

July 849120 981928 9.16%

August 1017167 1078344 9.82%

September 1098040 1168990 8.41%

October 1150192 1246865 6.66%

November 1277204 1333882 6.98%

December 1302351 1333882 0.00%

January 1406539 8.00%

February 1533128 9.00%

Moving average is a methodology which is used to compute average year by year. In this,

figures of three of or five years can be taken in order to compute moving average. Hence, this

technique helps in identifying average performance per of the company for every year. Here,

sales figure for January and February month are computed. Both months sales figure are

forecasted by using percentage change in moving average values. Hong Kong is one of the well-

known tourist places and in future, demand for the same will increase. Hence, it is expected that

sales will be increased by 8% and 9% in the month of January and February after slowdown that

is observed in the growth rate is observed inof the month ooff October and November.

extravagance. Hence, activity based costing method helps in the identification of full cost.

TASK 2

(a) Moving average methodology

Table 1: Calculation of moving average

Months Sales Moving average

Percenta

ge

change

in

moving

averages

April 667810

May 738159 813475

June 795121 899521 10.58%

July 849120 981928 9.16%

August 1017167 1078344 9.82%

September 1098040 1168990 8.41%

October 1150192 1246865 6.66%

November 1277204 1333882 6.98%

December 1302351 1333882 0.00%

January 1406539 8.00%

February 1533128 9.00%

Moving average is a methodology which is used to compute average year by year. In this,

figures of three of or five years can be taken in order to compute moving average. Hence, this

technique helps in identifying average performance per of the company for every year. Here,

sales figure for January and February month are computed. Both months sales figure are

forecasted by using percentage change in moving average values. Hong Kong is one of the well-

known tourist places and in future, demand for the same will increase. Hence, it is expected that

sales will be increased by 8% and 9% in the month of January and February after slowdown that

is observed in the growth rate is observed inof the month ooff October and November.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(b) Good practice to be considered in both construction of master budget and budgetary

monitoring and control

In master budget, various types of budgets are prepared like sales and production budget

etc. Budget indicates the expectations of the top management or the target that they wants to

achieve in the specific duration. While preparing budget in order to make accurate estimates,

Miramar hotel can evaluate business environment and can identify performance that it gives has

given in the previous business environment conditions. By evaluating current business

environment, managers can identify the level up to which firm can give a its performance. Apart

from this, some of the forecasting techniques like moving average can be used by them in order

to project cash flows. By doing so, budget can be prepared in the a proper manner (Kotas, 2014).

In order to monitor budget in proper in an effective manner, managers must look out at the

duration for which budget is prepared. In Addition addition to this, managers can break down

this duration in some parts. At the end of the every sub duration, managers will need to evaluate

their performance in a proper manner. In this way, budget will be monitored time to time. In

order to perform control function in a proper manner, managers can decide control measures and

can discuss same with the employee’s. By arriving at consensus, proper corrective actions can be

taken by the managers.

(c) Conformity of practices with the budget monitoring and control

The practices mentioned above conform to the budget monitoring and control. This is

because if budget will be monitored at the end of time period. Then then variances will be always

always comes in existence and an organization will not get time to improve its performance. But,

if, time to time performance will evaluated evaluate then managers will come to know about the

fact that they are performing well or worst (Lukka, 2010). If, they are performing worst then they

will be able to improve performance by taking corrective actions on time. Moreover, budgets

will also be monitored time to time. Hence, it can be said that budget monitoring and control will

go hand in hand. Hence, it can be said that practices mentioned above conform to the budget

monitoring and control.

(d) Comparison of budget with actual figures

monitoring and control

In master budget, various types of budgets are prepared like sales and production budget

etc. Budget indicates the expectations of the top management or the target that they wants to

achieve in the specific duration. While preparing budget in order to make accurate estimates,

Miramar hotel can evaluate business environment and can identify performance that it gives has

given in the previous business environment conditions. By evaluating current business

environment, managers can identify the level up to which firm can give a its performance. Apart

from this, some of the forecasting techniques like moving average can be used by them in order

to project cash flows. By doing so, budget can be prepared in the a proper manner (Kotas, 2014).

In order to monitor budget in proper in an effective manner, managers must look out at the

duration for which budget is prepared. In Addition addition to this, managers can break down

this duration in some parts. At the end of the every sub duration, managers will need to evaluate

their performance in a proper manner. In this way, budget will be monitored time to time. In

order to perform control function in a proper manner, managers can decide control measures and

can discuss same with the employee’s. By arriving at consensus, proper corrective actions can be

taken by the managers.

(c) Conformity of practices with the budget monitoring and control

The practices mentioned above conform to the budget monitoring and control. This is

because if budget will be monitored at the end of time period. Then then variances will be always

always comes in existence and an organization will not get time to improve its performance. But,

if, time to time performance will evaluated evaluate then managers will come to know about the

fact that they are performing well or worst (Lukka, 2010). If, they are performing worst then they

will be able to improve performance by taking corrective actions on time. Moreover, budgets

will also be monitored time to time. Hence, it can be said that budget monitoring and control will

go hand in hand. Hence, it can be said that practices mentioned above conform to the budget

monitoring and control.

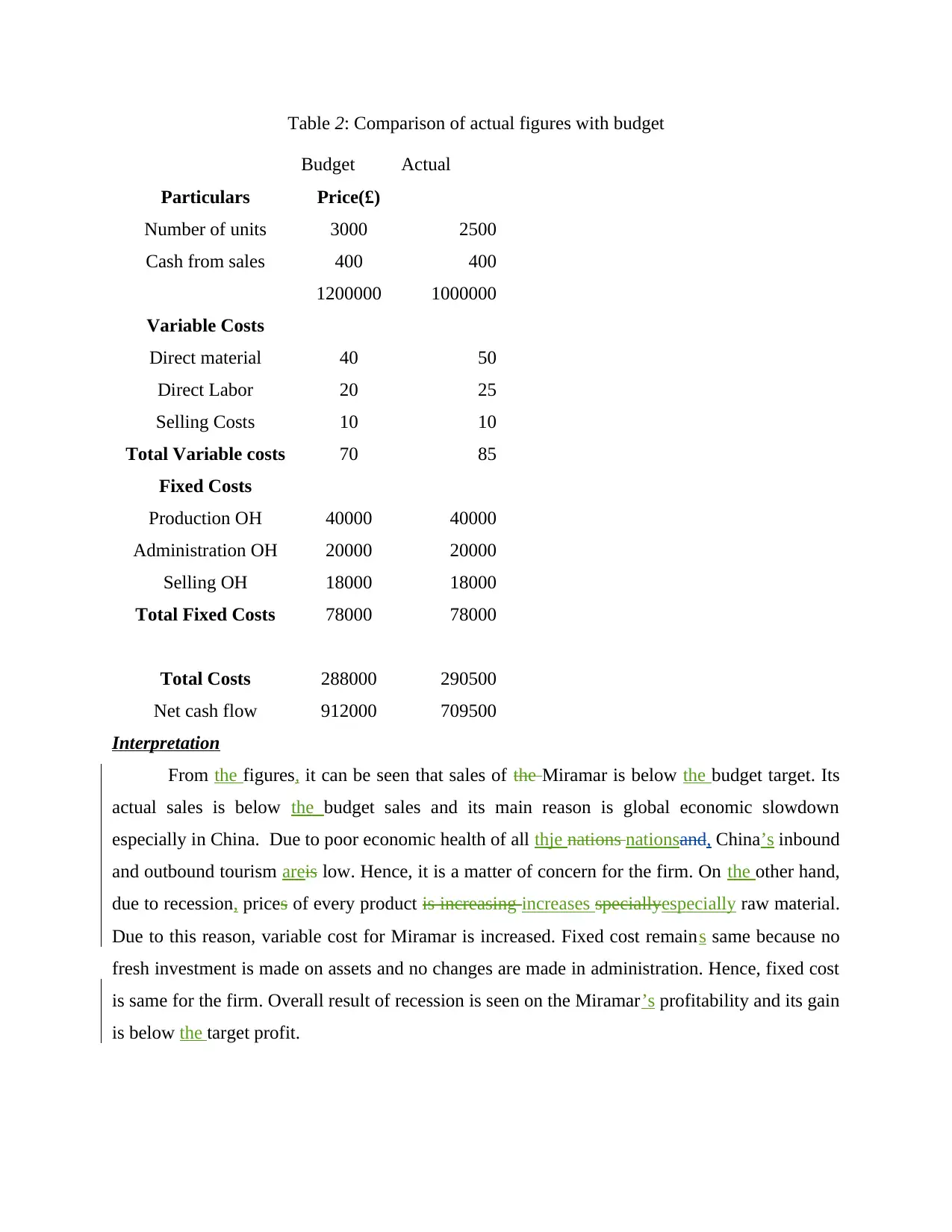

(d) Comparison of budget with actual figures

Table 2: Comparison of actual figures with budget

Budget Actual

Particulars Price(£)

Number of units 3000 2500

Cash from sales 400 400

1200000 1000000

Variable Costs

Direct material 40 50

Direct Labor 20 25

Selling Costs 10 10

Total Variable costs 70 85

Fixed Costs

Production OH 40000 40000

Administration OH 20000 20000

Selling OH 18000 18000

Total Fixed Costs 78000 78000

Total Costs 288000 290500

Net cash flow 912000 709500

Interpretation

From the figures, it can be seen that sales of the Miramar is below the budget target. Its

actual sales is below the budget sales and its main reason is global economic slowdown

especially in China. Due to poor economic health of all thje nations nationsand, China’s inbound

and outbound tourism areis low. Hence, it is a matter of concern for the firm. On the other hand,

due to recession, prices of every product is increasing increases speciallyespecially raw material.

Due to this reason, variable cost for Miramar is increased. Fixed cost remains same because no

fresh investment is made on assets and no changes are made in administration. Hence, fixed cost

is same for the firm. Overall result of recession is seen on the Miramar’s profitability and its gain

is below the target profit.

Budget Actual

Particulars Price(£)

Number of units 3000 2500

Cash from sales 400 400

1200000 1000000

Variable Costs

Direct material 40 50

Direct Labor 20 25

Selling Costs 10 10

Total Variable costs 70 85

Fixed Costs

Production OH 40000 40000

Administration OH 20000 20000

Selling OH 18000 18000

Total Fixed Costs 78000 78000

Total Costs 288000 290500

Net cash flow 912000 709500

Interpretation

From the figures, it can be seen that sales of the Miramar is below the budget target. Its

actual sales is below the budget sales and its main reason is global economic slowdown

especially in China. Due to poor economic health of all thje nations nationsand, China’s inbound

and outbound tourism areis low. Hence, it is a matter of concern for the firm. On the other hand,

due to recession, prices of every product is increasing increases speciallyespecially raw material.

Due to this reason, variable cost for Miramar is increased. Fixed cost remains same because no

fresh investment is made on assets and no changes are made in administration. Hence, fixed cost

is same for the firm. Overall result of recession is seen on the Miramar’s profitability and its gain

is below the target profit.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

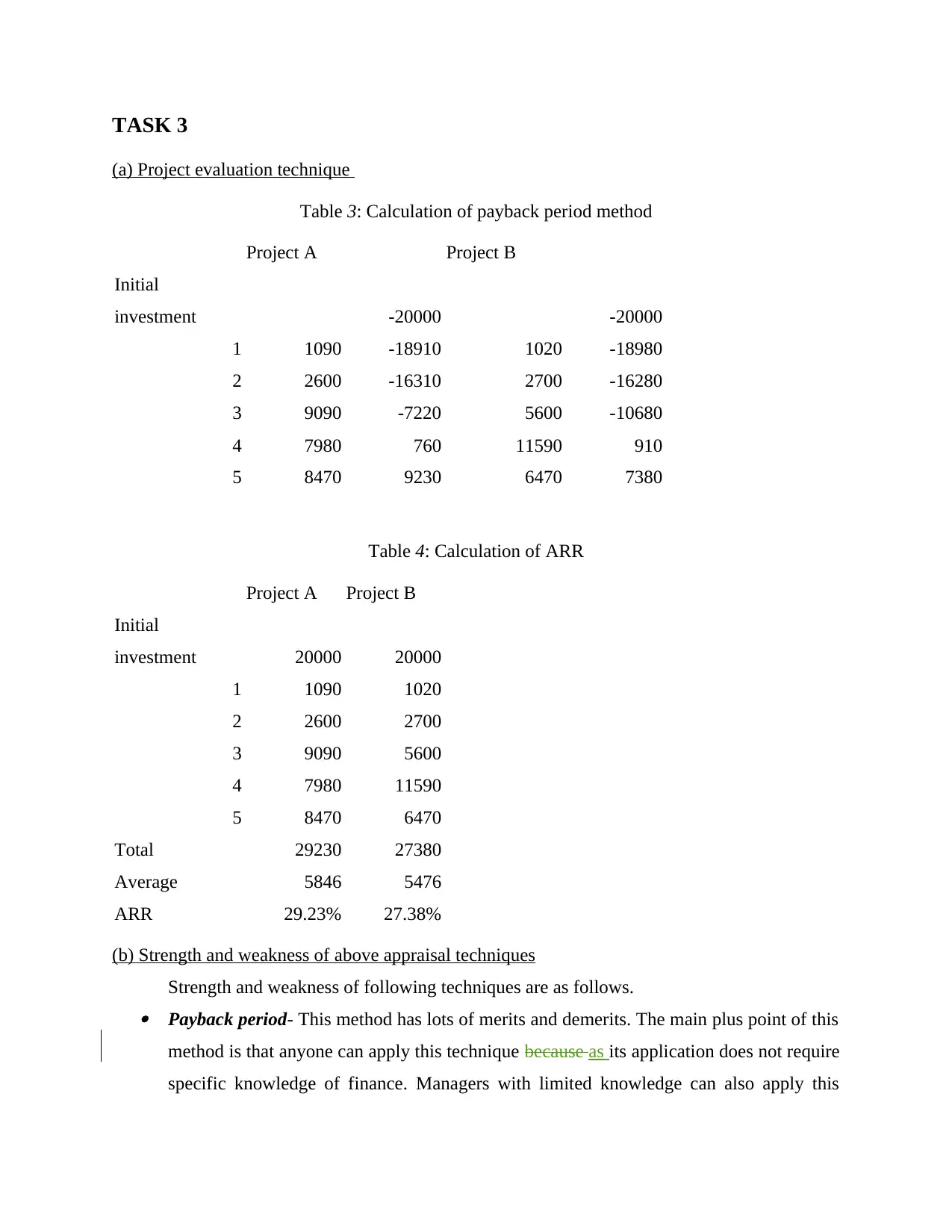

TASK 3

(a) Project evaluation technique

Table 3: Calculation of payback period method

Project A Project B

Initial

investment -20000 -20000

1 1090 -18910 1020 -18980

2 2600 -16310 2700 -16280

3 9090 -7220 5600 -10680

4 7980 760 11590 910

5 8470 9230 6470 7380

Table 4: Calculation of ARR

Project A Project B

Initial

investment 20000 20000

1 1090 1020

2 2600 2700

3 9090 5600

4 7980 11590

5 8470 6470

Total 29230 27380

Average 5846 5476

ARR 29.23% 27.38%

(b) Strength and weakness of above appraisal techniques

Strength and weakness of following techniques are as follows. Payback period- This method has lots of merits and demerits. The main plus point of this

method is that anyone can apply this technique because as its application does not require

specific knowledge of finance. Managers with limited knowledge can also apply this

(a) Project evaluation technique

Table 3: Calculation of payback period method

Project A Project B

Initial

investment -20000 -20000

1 1090 -18910 1020 -18980

2 2600 -16310 2700 -16280

3 9090 -7220 5600 -10680

4 7980 760 11590 910

5 8470 9230 6470 7380

Table 4: Calculation of ARR

Project A Project B

Initial

investment 20000 20000

1 1090 1020

2 2600 2700

3 9090 5600

4 7980 11590

5 8470 6470

Total 29230 27380

Average 5846 5476

ARR 29.23% 27.38%

(b) Strength and weakness of above appraisal techniques

Strength and weakness of following techniques are as follows. Payback period- This method has lots of merits and demerits. The main plus point of this

method is that anyone can apply this technique because as its application does not require

specific knowledge of finance. Managers with limited knowledge can also apply this

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

technique. The other main plus point of this method is that it is very easy to interpret

results of this technique. Due to this reason, this method is widely used in the project

management (Newcomer, Harry and Wholey, 2015). Pay backPayback period indicates

the time frame within which project can be completed. Hence, this provides information

about the time period up to which firm need has to wait for earning a profit. The only

limitation of this technique is that in this, present value is not used. Hence, present value

of the cash flows is not computed. This is a major weakness of this method.

Average rate of return- Average rate of return indicates the average return that a project

can earn on the invested value. This is the emainMain merit of this method because is

that through application of this technique, project managers comes to know about the

overall profit that on average basis, can be earned on by the project (Law, Qi and Buhalis,

2010). The main limitation of this method is that here also present value method is also

not used here, which while it is actively used in accounting for and computing the

impairment of asset. Hence, these are major benefits and limitations of ARR.

(c) Recommendation on selection of project

On the basis of comparison, of both projects project A is selected for the Miramar hotel.

This is because on pay back InOn the basis of calculation, it can be seen that both the projects

are recovering investment amount in 3 years. Hence, here both projects are equal ton each other.

On the other hand, there is an average rate of return method whose results shows that project A is

giving good return then than project B. Former project is giving return of 29.23%. Whereas,

latter project is giving return of 27.38%. On this basis, project A is considered viable for the

Miramar hotel relative to project B.

(e) Possible source of finance and its advantages as well as limitations

Sources of finance that are available to Miramar hotel to finance its projects are as

follows:

Equity- Miramar hotel can issue equity shares in the primary market. In this regard, it can

bring IPO or FPO in the primary market. Through this source of finance, it can raised

raise a its target amount. If, it failed fails to do so then underwriters will purchase

company’s shares. Hence, determined targeted amount will be surely raised from the

primary market by the mentioned firm.

results of this technique. Due to this reason, this method is widely used in the project

management (Newcomer, Harry and Wholey, 2015). Pay backPayback period indicates

the time frame within which project can be completed. Hence, this provides information

about the time period up to which firm need has to wait for earning a profit. The only

limitation of this technique is that in this, present value is not used. Hence, present value

of the cash flows is not computed. This is a major weakness of this method.

Average rate of return- Average rate of return indicates the average return that a project

can earn on the invested value. This is the emainMain merit of this method because is

that through application of this technique, project managers comes to know about the

overall profit that on average basis, can be earned on by the project (Law, Qi and Buhalis,

2010). The main limitation of this method is that here also present value method is also

not used here, which while it is actively used in accounting for and computing the

impairment of asset. Hence, these are major benefits and limitations of ARR.

(c) Recommendation on selection of project

On the basis of comparison, of both projects project A is selected for the Miramar hotel.

This is because on pay back InOn the basis of calculation, it can be seen that both the projects

are recovering investment amount in 3 years. Hence, here both projects are equal ton each other.

On the other hand, there is an average rate of return method whose results shows that project A is

giving good return then than project B. Former project is giving return of 29.23%. Whereas,

latter project is giving return of 27.38%. On this basis, project A is considered viable for the

Miramar hotel relative to project B.

(e) Possible source of finance and its advantages as well as limitations

Sources of finance that are available to Miramar hotel to finance its projects are as

follows:

Equity- Miramar hotel can issue equity shares in the primary market. In this regard, it can

bring IPO or FPO in the primary market. Through this source of finance, it can raised

raise a its target amount. If, it failed fails to do so then underwriters will purchase

company’s shares. Hence, determined targeted amount will be surely raised from the

primary market by the mentioned firm.

Debt – This is commonly available option and exercised by the most of the firms. Under

this, firm can take debt from the banks and financial institutions. In return, bank it will

need to pay interest to the bank. Loans are available at fixed and floating interest rates. If,

loan is taken at the floating interest rate then finance cost may be increased or decreased

(Brown and Petersen, 2011). If, interest rate is increased by the central bank then rate of

loan cost of the company will also be increased by bank. Hence, finance cost of the firm

will increased. Hence, companies must abstain from focus on taking loan at flexible

interest rates.

Venture capital- Under this, there is a firm that makes an investment in the company

equity. In return, they get shareholding in the firm business. This method is used by the

firms that cannot be listed in the stock market. Hence, Miramar can also use this option.

(f) Post appraisal audit and effectiveness of investment decision-making

Post appraisal audit may improve the effectiveness of investment decision-making. This

is because in calculation, cash flows are taken into account. These cash flows are estimated and

there is no technique that can perfectly give calculate the cash flows. Hence, there is a high

possibility of error in the estimation of the cash flow. If, cash flows are wrongly estimated then

wrong results will come in existence (Luft and Shields, 2010). Hence, decisions made on the

basis of same will also be wrong. This will lead to the selection of wrong project. Hence, if after

doing appraisal, post audit is done then errors that are done in calculation or estimation of cash

flows can be estimated will be easily identified. Corrections can be made on the errors and right

project can easily be selected by the firm. Selection of wrong project leads to heavy loss to the

firm. But, due to post appraisal, chances of such kind of mistakes will can be reduced to a large

extent. Hence, use of post appraisal audit helps in making sound investment decisions.

(g) Main difference between investment appraisal techniques of public and private sector

There is a large difference in between the investment appraisal technique used by the

public sector and private sector. In private sector, techniques like NPV, IRR, ARR and pay back

are used for project evaluation. But, in public sector organizations, cost volume profit analysis

technique is used. By using cost volume relationship, breakeven point is identified (DRURY,

2013). This is a point where cost is equal to the revenue. This is a sales level where in which

there is no profit and no loss. Hence, by using this technique, public organizations identify that

what amount of sales they need to generate in order to cover cost. On the basis of estimation of

this, firm can take debt from the banks and financial institutions. In return, bank it will

need to pay interest to the bank. Loans are available at fixed and floating interest rates. If,

loan is taken at the floating interest rate then finance cost may be increased or decreased

(Brown and Petersen, 2011). If, interest rate is increased by the central bank then rate of

loan cost of the company will also be increased by bank. Hence, finance cost of the firm

will increased. Hence, companies must abstain from focus on taking loan at flexible

interest rates.

Venture capital- Under this, there is a firm that makes an investment in the company

equity. In return, they get shareholding in the firm business. This method is used by the

firms that cannot be listed in the stock market. Hence, Miramar can also use this option.

(f) Post appraisal audit and effectiveness of investment decision-making

Post appraisal audit may improve the effectiveness of investment decision-making. This

is because in calculation, cash flows are taken into account. These cash flows are estimated and

there is no technique that can perfectly give calculate the cash flows. Hence, there is a high

possibility of error in the estimation of the cash flow. If, cash flows are wrongly estimated then

wrong results will come in existence (Luft and Shields, 2010). Hence, decisions made on the

basis of same will also be wrong. This will lead to the selection of wrong project. Hence, if after

doing appraisal, post audit is done then errors that are done in calculation or estimation of cash

flows can be estimated will be easily identified. Corrections can be made on the errors and right

project can easily be selected by the firm. Selection of wrong project leads to heavy loss to the

firm. But, due to post appraisal, chances of such kind of mistakes will can be reduced to a large

extent. Hence, use of post appraisal audit helps in making sound investment decisions.

(g) Main difference between investment appraisal techniques of public and private sector

There is a large difference in between the investment appraisal technique used by the

public sector and private sector. In private sector, techniques like NPV, IRR, ARR and pay back

are used for project evaluation. But, in public sector organizations, cost volume profit analysis

technique is used. By using cost volume relationship, breakeven point is identified (DRURY,

2013). This is a point where cost is equal to the revenue. This is a sales level where in which

there is no profit and no loss. Hence, by using this technique, public organizations identify that

what amount of sales they need to generate in order to cover cost. On the basis of estimation of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.