Analysis of Management Accounting Systems and Financial Performance

VerifiedAdded on 2020/09/09

|23

|7767

|2468

Report

AI Summary

This report delves into the core concepts of management accounting, differentiating it from financial accounting and exploring various systems like cost accounting, job costing, and inventory management. It analyzes the application of these systems within Khaadi, a case study, highlighting their importance in planning, controlling, decision-making, and problem-solving. The report further examines different methods used for management accounting reporting, including cost reports, performance reports, and budgetary control. It covers essential elements such as fixed costs, variable costs, and variance analysis. Furthermore, the report investigates how organizations adapt managerial accounting systems to address financial problems, emphasizing the use of benchmarks, key performance indicators, and budgetary targets. Finally, it evaluates how accounting planning tools contribute to sustainable success, incorporating strategic planning and various planning tools such as budgeting and costing systems. This analysis provides a comprehensive understanding of management accounting's role in organizational financial health and strategic decision-making, using the case study of Khaadi.

Table of Contents

DEFINITION:....................................................................................................................................................................... 4

PRINCIPLES OF MANAGEMENT ACCOUNTING..................................................................................................................4

1. DESIGNING AND COMPILING :...................................................................................................................................4

2. MANAGEMENT BY EXCEPTION :................................................................................................................................4

3. INTEGRETION :...........................................................................................................................................................4

4. USE OF RETURN ON INVESTMENT :...........................................................................................................................4

5. CONTROLLABLE AND UNCONTROLLABLE COSTS :.....................................................................................................4

DIFFERENCES BETWEEN FINANCIAL AND MANAGEMENT ACCOUNTING..........................................................................4

MANAGEMENT ACCOUNTING :.........................................................................................................................................4

FINANACIAL ACCOUNTING :..............................................................................................................................................4

FOLLOWING ESSENTIALS OF MANAGEMENT ACCOUNTING SYSTEM................................................................................5

Types of Management Accounting Systems (MAS)...........................................................................................................5

COST- ACCOUNTING SYSTEM............................................................................................................................................5

JOB- COSTING SYSTEM......................................................................................................................................................5

INVENTORY MANAGEMENT SYSTEM....................................................................................................................................5

PRIZE- OPTIMIZING SYSTEM..............................................................................................................................................6

INTEGRATION OF MANAGEMNT ACCOUNTING WITHIN KHAADI AND ITS USEFLNESS FOR THE MANAGEMNET.............6

1. PLANNING..................................................................................................................................................................... 6

2. CONTROLLING...............................................................................................................................................................6

3. DECISION-MAKING........................................................................................................................................................6

4. GOAL SETTING...............................................................................................................................................................6

5. PROBLEM-SOLVING.......................................................................................................................................................6

DIFFERENT METHODS USED FOR MANAGEMENT ACCOUNTING REPORTING..................................................................6

LOII........................................................................................................................................................................................ 7

COST:..................................................................................................................................................................................... 7

FIXED COSTS:.........................................................................................................................................................................7

CVP:....................................................................................................................................................................................... 7

COST VARIANCE:...................................................................................................................................................................7

INVENTORY COSTS:...............................................................................................................................................................7

MARGINAL COSTING:............................................................................................................................................................7

ABSORPTION COSTING:.........................................................................................................................................................8

FIFO:...................................................................................................................................................................................... 9

LIFO:.................................................................................................................................................................................... 10

WEIGHTED AVERAGE COST (WAC) :....................................................................................................................................10

VARIANCE ANALYSIS :..........................................................................................................................................................10

SALES PRICE VARIANCE:......................................................................................................................................................10

DEFINITION:....................................................................................................................................................................... 4

PRINCIPLES OF MANAGEMENT ACCOUNTING..................................................................................................................4

1. DESIGNING AND COMPILING :...................................................................................................................................4

2. MANAGEMENT BY EXCEPTION :................................................................................................................................4

3. INTEGRETION :...........................................................................................................................................................4

4. USE OF RETURN ON INVESTMENT :...........................................................................................................................4

5. CONTROLLABLE AND UNCONTROLLABLE COSTS :.....................................................................................................4

DIFFERENCES BETWEEN FINANCIAL AND MANAGEMENT ACCOUNTING..........................................................................4

MANAGEMENT ACCOUNTING :.........................................................................................................................................4

FINANACIAL ACCOUNTING :..............................................................................................................................................4

FOLLOWING ESSENTIALS OF MANAGEMENT ACCOUNTING SYSTEM................................................................................5

Types of Management Accounting Systems (MAS)...........................................................................................................5

COST- ACCOUNTING SYSTEM............................................................................................................................................5

JOB- COSTING SYSTEM......................................................................................................................................................5

INVENTORY MANAGEMENT SYSTEM....................................................................................................................................5

PRIZE- OPTIMIZING SYSTEM..............................................................................................................................................6

INTEGRATION OF MANAGEMNT ACCOUNTING WITHIN KHAADI AND ITS USEFLNESS FOR THE MANAGEMNET.............6

1. PLANNING..................................................................................................................................................................... 6

2. CONTROLLING...............................................................................................................................................................6

3. DECISION-MAKING........................................................................................................................................................6

4. GOAL SETTING...............................................................................................................................................................6

5. PROBLEM-SOLVING.......................................................................................................................................................6

DIFFERENT METHODS USED FOR MANAGEMENT ACCOUNTING REPORTING..................................................................6

LOII........................................................................................................................................................................................ 7

COST:..................................................................................................................................................................................... 7

FIXED COSTS:.........................................................................................................................................................................7

CVP:....................................................................................................................................................................................... 7

COST VARIANCE:...................................................................................................................................................................7

INVENTORY COSTS:...............................................................................................................................................................7

MARGINAL COSTING:............................................................................................................................................................7

ABSORPTION COSTING:.........................................................................................................................................................8

FIFO:...................................................................................................................................................................................... 9

LIFO:.................................................................................................................................................................................... 10

WEIGHTED AVERAGE COST (WAC) :....................................................................................................................................10

VARIANCE ANALYSIS :..........................................................................................................................................................10

SALES PRICE VARIANCE:......................................................................................................................................................10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SALES VOLUME VARIANCE:.................................................................................................................................................10

MATERIAL RATE VARIANCE:................................................................................................................................................11

MATERIAL QUANTITY VARIANCE:........................................................................................................................................11

LABOUR EFFICIENCY VARIANCE:..........................................................................................................................................11

LABOUR RATE VARIANCE:...................................................................................................................................................11

Direct Labor Rate Variance:.........................................................................................................................................12

VPOH RATE VARIANCE:.......................................................................................................................................................12

VPOH EFFICIENCY VARIANCE:..............................................................................................................................................12

FIXED P.O.H VARIANCE:.......................................................................................................................................................12

FORMULA:...................................................................................................................................................................... 12

BUDGET........................................................................................................................................................................... 15

COST REPORT..................................................................................................................................................................16

PERFORMANCE REPORT..................................................................................................................................................16

DISADVANTAGES AND ADVANTAGES OF DIFFERENT KINDS OF PLANNING TOOLS USED FOR BUDGETARY CONTROL...16

MERITS OF BUDGETARY CONTROL..................................................................................................................................16

DISADVANTAGES OF BUDGETARY CONTROL...................................................................................................................17

THE USE OF DIFFERENT PLANNING TOOLS AND THEIR APPLICATION FOR PREPARING AND FORECASTING BUDGETS...17

Use of Control and Planning Budget:..................................................................................................................................17

Pricing:................................................................................................................................................................................ 17

Costing System:...................................................................................................................................................................17

Strategic planning:..............................................................................................................................................................17

COMPARE HOW ORGANIZATIONS ARE ADAPTING MANAGERIAL ACCOUNTING SYSTEMS TO RESPONDING TO

FINANCIAL PROBLEMS.....................................................................................................................................................17

TOOLS AND TECHNIQUES OF MANAGEMENT ACCOUNTANT..........................................................................................17

FINANCIAL PLANNING :.......................................................................................................................................................17

FINANCIAL STATEMENT ANALYSIS:.....................................................................................................................................18

COST ACCOUNTING:............................................................................................................................................................18

CASH FLOW ANALYSIS:........................................................................................................................................................18

STANDARD COSTING:..........................................................................................................................................................18

MARGINAL COSTING:..........................................................................................................................................................18

BUDGETARY COSTING:........................................................................................................................................................18

AN ORGANIZATION CAN REACT TO FINANCIAL PROBLEMS USING THE FOLLOWING MANAGERIAL ACCOUNTING

METHODS........................................................................................................................................................................ 18

CAPITAL BUDGET:................................................................................................................................................................19

OPERATING BUDGET:..........................................................................................................................................................19

BEHAVIOURAL IMPLICATIONS OF BUDGETS:......................................................................................................................19

1

MATERIAL RATE VARIANCE:................................................................................................................................................11

MATERIAL QUANTITY VARIANCE:........................................................................................................................................11

LABOUR EFFICIENCY VARIANCE:..........................................................................................................................................11

LABOUR RATE VARIANCE:...................................................................................................................................................11

Direct Labor Rate Variance:.........................................................................................................................................12

VPOH RATE VARIANCE:.......................................................................................................................................................12

VPOH EFFICIENCY VARIANCE:..............................................................................................................................................12

FIXED P.O.H VARIANCE:.......................................................................................................................................................12

FORMULA:...................................................................................................................................................................... 12

BUDGET........................................................................................................................................................................... 15

COST REPORT..................................................................................................................................................................16

PERFORMANCE REPORT..................................................................................................................................................16

DISADVANTAGES AND ADVANTAGES OF DIFFERENT KINDS OF PLANNING TOOLS USED FOR BUDGETARY CONTROL...16

MERITS OF BUDGETARY CONTROL..................................................................................................................................16

DISADVANTAGES OF BUDGETARY CONTROL...................................................................................................................17

THE USE OF DIFFERENT PLANNING TOOLS AND THEIR APPLICATION FOR PREPARING AND FORECASTING BUDGETS...17

Use of Control and Planning Budget:..................................................................................................................................17

Pricing:................................................................................................................................................................................ 17

Costing System:...................................................................................................................................................................17

Strategic planning:..............................................................................................................................................................17

COMPARE HOW ORGANIZATIONS ARE ADAPTING MANAGERIAL ACCOUNTING SYSTEMS TO RESPONDING TO

FINANCIAL PROBLEMS.....................................................................................................................................................17

TOOLS AND TECHNIQUES OF MANAGEMENT ACCOUNTANT..........................................................................................17

FINANCIAL PLANNING :.......................................................................................................................................................17

FINANCIAL STATEMENT ANALYSIS:.....................................................................................................................................18

COST ACCOUNTING:............................................................................................................................................................18

CASH FLOW ANALYSIS:........................................................................................................................................................18

STANDARD COSTING:..........................................................................................................................................................18

MARGINAL COSTING:..........................................................................................................................................................18

BUDGETARY COSTING:........................................................................................................................................................18

AN ORGANIZATION CAN REACT TO FINANCIAL PROBLEMS USING THE FOLLOWING MANAGERIAL ACCOUNTING

METHODS........................................................................................................................................................................ 18

CAPITAL BUDGET:................................................................................................................................................................19

OPERATING BUDGET:..........................................................................................................................................................19

BEHAVIOURAL IMPLICATIONS OF BUDGETS:......................................................................................................................19

1

COMPARE HOW ORGANISATIONS ARE ADAPTING MANAGE MENT ACCOUNTING SYSTEMS TO RESPOND TO

FINANCIAL PROBLEMS?..................................................................................................................................................20

USING BENCHMARKS, FINANCIAL AND NON-FINANCIAL KEY PERFORMANCE INDICATORS, & BUDGETARY TARGETS

TO IDENTIFY FINANCIAL PROBLE MS AND FINANCIAL VARIANCES. EXPLAIN BY USING BENCH MARKS AND BUDGETING

TARGETS HELP IDENTIFY FINANCIAL PROBLEMS AND FINANCIAL VARIANCES:...................................................................20

ANALYSIS OF HOW MANAGEMENT ACCOUNTING CAN LEAD ORGANIZATION'S KHAADI OF SUSTAINABLE SUCCESS IN

RESPONDING TO FINANCIAL PROBLEMS.......................................................................................................................20

THROUGH DEVELOPING EFFECTIVE STRATEGIES AND PROCESSES WHICH INCLUDE ACCURATE AND PROMPT

DOCUMENTATION, WHICH ALSO INCLUDES DISCLOSURE OF ALL FINANCIAL SITUATIONS THAT ARE PROPERLY

GOVERNED AND HELD AMONG THOSE WHO OCCUPY THEM?.....................................................................................21

Strategic planning is concerned with the development of decision making on the kinds of markets and businesses in

which the Khaadi and Gul Ahmed operates and includes competitive decisions on market competition strategies.

Strategic planning also utilizes financial analysis information from different management systems such as pricing,

budgeting and quality measurement systems and also internally and externally organizational sources......................21

EVALUATE HOW ACCOUNTING PLANNING TOOLS ADDRESS FINANCIAL PROBLEMS APPROPRIATELY TO LEAD

ORGANISATIONS TO SUSTAINABLE SUCCESS:.................................................................................................................21

PLANNING AND CONTROLLING:..........................................................................................................................................21

IMPLEMENTING PLANS:......................................................................................................................................................21

COMPETITIVE EDGE:............................................................................................................................................................21

Bibliography........................................................................................................................................................................ 22

2

FINANCIAL PROBLEMS?..................................................................................................................................................20

USING BENCHMARKS, FINANCIAL AND NON-FINANCIAL KEY PERFORMANCE INDICATORS, & BUDGETARY TARGETS

TO IDENTIFY FINANCIAL PROBLE MS AND FINANCIAL VARIANCES. EXPLAIN BY USING BENCH MARKS AND BUDGETING

TARGETS HELP IDENTIFY FINANCIAL PROBLEMS AND FINANCIAL VARIANCES:...................................................................20

ANALYSIS OF HOW MANAGEMENT ACCOUNTING CAN LEAD ORGANIZATION'S KHAADI OF SUSTAINABLE SUCCESS IN

RESPONDING TO FINANCIAL PROBLEMS.......................................................................................................................20

THROUGH DEVELOPING EFFECTIVE STRATEGIES AND PROCESSES WHICH INCLUDE ACCURATE AND PROMPT

DOCUMENTATION, WHICH ALSO INCLUDES DISCLOSURE OF ALL FINANCIAL SITUATIONS THAT ARE PROPERLY

GOVERNED AND HELD AMONG THOSE WHO OCCUPY THEM?.....................................................................................21

Strategic planning is concerned with the development of decision making on the kinds of markets and businesses in

which the Khaadi and Gul Ahmed operates and includes competitive decisions on market competition strategies.

Strategic planning also utilizes financial analysis information from different management systems such as pricing,

budgeting and quality measurement systems and also internally and externally organizational sources......................21

EVALUATE HOW ACCOUNTING PLANNING TOOLS ADDRESS FINANCIAL PROBLEMS APPROPRIATELY TO LEAD

ORGANISATIONS TO SUSTAINABLE SUCCESS:.................................................................................................................21

PLANNING AND CONTROLLING:..........................................................................................................................................21

IMPLEMENTING PLANS:......................................................................................................................................................21

COMPETITIVE EDGE:............................................................................................................................................................21

Bibliography........................................................................................................................................................................ 22

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DEFINITION:

The Institute of Cost and Management Accountants, London, has defined Management Accounting as: “The application

of professional knowledge and skill in the preparation of accounting information in such a way as to assist management

in the formulation of policies and in the planning and control of the operation of the undertakings”. (Tuovila, 2019)

PRINCIPLES OF MANAGEMENT ACCOUNTING

The following principles of management accounting are:

1. DESIGNING AND COMPILING :

In order to satisfy the requirements of the particular company and/or specific issue, accounting data, documents,

reports, statements and other proof of previous, current or future outcomes should be intended and compiled. It

implies that the accounting management system is intended to present the appropriate information in such a manner.

2. MANAGEMENT BY EXCEPTION :

When presenting data to management, the principle of exceptional leadership is followed. It implies that the

management accounting system follows the budgetary control system and regular costing methods. This compares the

real performance with the predefined performance to evaluate the variances.

3. INTEGRETION :

It indicates that all of the management's necessary information is built so they can be used successfully at the maximum,

while providing the accounting service at the minimum cost.

4. USE OF RETURN ON INVESTMENT :

Return on investment is otherwise called Capital Employed Return. The return rate demonstrates the company

concern's effectiveness. The capital used is calculated in terms of actual cash value for this purpose.

5. CONTROLLABLE AND UNCONTROLLABLE COSTS :

Costs are categorized into two kinds, i.e. controllable and uncontrollable, based on cost controllability. Taking measures

to control uncontrollable expenses is meaningless. Therefore, the accounting leadership scheme can provide

controllable cost control methods. (Dominic, 2019)

DIFFERENCES BETWEEN FINANCIAL AND MANAGEMENT ACCOUNTING

MANAGEMENT ACCOUNTING :

It is used internally. It is not governed by any law. Its consumers are an organization's management. It helps to make

internal decisions. It is not mandatory to prepare and present financial statements. It will not be audited. There is no

specified rate in which statements are prepared and presented. Monetary and non-monetary data includes

management reports.

FINANACIAL ACCOUNTING :

It is mainly used for external reporting, although it is also reviewed by management. It must be provided in accordance

with norms. Shareholders, investors and regulators are its consumers. It helps outsiders to make investment decisions

and regulators to monitor them. It is compulsory to prepare and present. It is necessary to audit financial statements.

Financial information for the financial year must be prepared and submitted. Financial accounts only include financial

data. (AccountingTools, 2018)

3

The Institute of Cost and Management Accountants, London, has defined Management Accounting as: “The application

of professional knowledge and skill in the preparation of accounting information in such a way as to assist management

in the formulation of policies and in the planning and control of the operation of the undertakings”. (Tuovila, 2019)

PRINCIPLES OF MANAGEMENT ACCOUNTING

The following principles of management accounting are:

1. DESIGNING AND COMPILING :

In order to satisfy the requirements of the particular company and/or specific issue, accounting data, documents,

reports, statements and other proof of previous, current or future outcomes should be intended and compiled. It

implies that the accounting management system is intended to present the appropriate information in such a manner.

2. MANAGEMENT BY EXCEPTION :

When presenting data to management, the principle of exceptional leadership is followed. It implies that the

management accounting system follows the budgetary control system and regular costing methods. This compares the

real performance with the predefined performance to evaluate the variances.

3. INTEGRETION :

It indicates that all of the management's necessary information is built so they can be used successfully at the maximum,

while providing the accounting service at the minimum cost.

4. USE OF RETURN ON INVESTMENT :

Return on investment is otherwise called Capital Employed Return. The return rate demonstrates the company

concern's effectiveness. The capital used is calculated in terms of actual cash value for this purpose.

5. CONTROLLABLE AND UNCONTROLLABLE COSTS :

Costs are categorized into two kinds, i.e. controllable and uncontrollable, based on cost controllability. Taking measures

to control uncontrollable expenses is meaningless. Therefore, the accounting leadership scheme can provide

controllable cost control methods. (Dominic, 2019)

DIFFERENCES BETWEEN FINANCIAL AND MANAGEMENT ACCOUNTING

MANAGEMENT ACCOUNTING :

It is used internally. It is not governed by any law. Its consumers are an organization's management. It helps to make

internal decisions. It is not mandatory to prepare and present financial statements. It will not be audited. There is no

specified rate in which statements are prepared and presented. Monetary and non-monetary data includes

management reports.

FINANACIAL ACCOUNTING :

It is mainly used for external reporting, although it is also reviewed by management. It must be provided in accordance

with norms. Shareholders, investors and regulators are its consumers. It helps outsiders to make investment decisions

and regulators to monitor them. It is compulsory to prepare and present. It is necessary to audit financial statements.

Financial information for the financial year must be prepared and submitted. Financial accounts only include financial

data. (AccountingTools, 2018)

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FOLLOWING ESSENTIALS OF MANAGEMENT ACCOUNTING SYSTEM

Types of Management Accounting Systems (MAS)

1. Cost-accounting systems

2. Job-costing system

3. Inventory management systems

4. Price-optimizing systems

COST- ACCOUNTING SYSTEM

Corporations like Khaadi apply the framework of costing system for approximate cost determination of its products in

order to carry out inventory valuation, analysis of profitability, and control costs. The costs are allocated in cost

accounting system on the basis of either costs incurred due to activity or traditional costing system. It is essential to

estimate the costs of products for effective functioning of Khaadi’s business. This system aims at determining the costs

of productions through calculating the direct and variable costs incurred at every production step and also the fixed

costs like equipment depreciation. Costing process can calculate and report expenses separately and then correlate

input figures to actual results or revenue to aid the company's management in assessing financial performance. Business

managers depend on general and cost-specific accounting information as any of the company's activities can be clarified

through its value. Cost accounting is known to be the key concept of management accounting as it incorporates the

analytical tools such as budgetary control marginal costing, absorption costing, and inventory control that are used

by management to effectively discharge their reproducibility. (XPLAIND, 2019)

JOB- COSTING SYSTEM

Job costing refers to the system of allocating production costs to the product's individual items or batches. It is applied if

the manufactured products differ from each other. It involves collecting data on the costs of a single company or

production work. You may need the details to submit price data under the agreement to a customer in which expenses

are refunded. Therefore, the information is useful to assess the reliability of the Khaadi’s valuation process, which must

be capable of quoting rates which require reasonable income. In addition, the information may be used to assign

inventory costs to processed products. The job costing system needs three types of direct information workers, direct

materials, and overhead to be accumulated. (AccountingTools, 2018)

INVENTORY MANAGEMENT SYSTEM

Inventory management relates to the technique used by the company to control and supervise the ordering use and

storage of elements used in the manufacturing of the products it sells. Inventory management system mixes the use of

barcode scanners, desktop software, mobile phones and barcode printers to simplify inventory management such as

consumer goods, stocks and supplies. It is also the practice of monitoring and supervising the quantities for sale of the

manufactured goods. The goal of inventory management is to understand the current inventory levels accurately and to

minimize over blocking and understanding situations. Managers should have insight to be willing to make appropriate

inventory decisions by an accurate tracking of quantities around the stocking location. A Khaadi's stock is one of the

main resources and savings funds which are related to selling products. Inventory management system functions are the

following: generating purchase orders, acquiring, relocating, changing and disposing of stock. It also makes marketing

orders, pick-ups, packing and consumer delivery. This executes process checks and records, produces, handles, plans,

and exchanges actual stock statements and barcode labels for printing. The advantages of an Khaadi's inventory

management program include increasing the Khaadi's bottom line, enhancing the quality of the inventory, and

improving the company's workflow. (Pontius, 2019)

PRIZE- OPTIMIZING SYSTEM

Price management relates to applying mathematical analysis to the Khaadi to decide how customers can respond across

different channels to different prices of their goods and services. It is also used to evaluate the costs that a Khaadi

4

Types of Management Accounting Systems (MAS)

1. Cost-accounting systems

2. Job-costing system

3. Inventory management systems

4. Price-optimizing systems

COST- ACCOUNTING SYSTEM

Corporations like Khaadi apply the framework of costing system for approximate cost determination of its products in

order to carry out inventory valuation, analysis of profitability, and control costs. The costs are allocated in cost

accounting system on the basis of either costs incurred due to activity or traditional costing system. It is essential to

estimate the costs of products for effective functioning of Khaadi’s business. This system aims at determining the costs

of productions through calculating the direct and variable costs incurred at every production step and also the fixed

costs like equipment depreciation. Costing process can calculate and report expenses separately and then correlate

input figures to actual results or revenue to aid the company's management in assessing financial performance. Business

managers depend on general and cost-specific accounting information as any of the company's activities can be clarified

through its value. Cost accounting is known to be the key concept of management accounting as it incorporates the

analytical tools such as budgetary control marginal costing, absorption costing, and inventory control that are used

by management to effectively discharge their reproducibility. (XPLAIND, 2019)

JOB- COSTING SYSTEM

Job costing refers to the system of allocating production costs to the product's individual items or batches. It is applied if

the manufactured products differ from each other. It involves collecting data on the costs of a single company or

production work. You may need the details to submit price data under the agreement to a customer in which expenses

are refunded. Therefore, the information is useful to assess the reliability of the Khaadi’s valuation process, which must

be capable of quoting rates which require reasonable income. In addition, the information may be used to assign

inventory costs to processed products. The job costing system needs three types of direct information workers, direct

materials, and overhead to be accumulated. (AccountingTools, 2018)

INVENTORY MANAGEMENT SYSTEM

Inventory management relates to the technique used by the company to control and supervise the ordering use and

storage of elements used in the manufacturing of the products it sells. Inventory management system mixes the use of

barcode scanners, desktop software, mobile phones and barcode printers to simplify inventory management such as

consumer goods, stocks and supplies. It is also the practice of monitoring and supervising the quantities for sale of the

manufactured goods. The goal of inventory management is to understand the current inventory levels accurately and to

minimize over blocking and understanding situations. Managers should have insight to be willing to make appropriate

inventory decisions by an accurate tracking of quantities around the stocking location. A Khaadi's stock is one of the

main resources and savings funds which are related to selling products. Inventory management system functions are the

following: generating purchase orders, acquiring, relocating, changing and disposing of stock. It also makes marketing

orders, pick-ups, packing and consumer delivery. This executes process checks and records, produces, handles, plans,

and exchanges actual stock statements and barcode labels for printing. The advantages of an Khaadi's inventory

management program include increasing the Khaadi's bottom line, enhancing the quality of the inventory, and

improving the company's workflow. (Pontius, 2019)

PRIZE- OPTIMIZING SYSTEM

Price management relates to applying mathematical analysis to the Khaadi to decide how customers can respond across

different channels to different prices of their goods and services. It is also used to evaluate the costs that a Khaadi

4

decides will best meet its goals, such as optimizing operating profit. Exploring an alternative through the highest

achievable or cost-effective performance under the constraints provided by increasing desired aspects and reducing

unwanted aspects.

INTEGRATION OF MANAGEMNT ACCOUNTING WITHIN KHAADI AND ITS USEFLNESS FOR THE MANAGEMNET

THE BENEFITS OF MANAGEMENT ACCOUNTING SYSTEMS AND THEIR APPLICATIONS

Management accounting is primarily used to generate data within an organization for executives. While financial

accounting is of greatest benefit to stakeholders, financial accounting enables to achieve inner organizational goals.

1. Planning

2. Controlling

3. Decision-Making

4. Problem-Solving

5. Goal setting

1. PLANNING

Future planning is a main focus of financial accounting. Management auditors create more comprehensive reports than

economic accountants. They can include particular product data, market reach and regional data

2. CONTROLLING

The managerial accounting data provides managers a higher feeling of control over the achievement of an organization.

During the control stage, executives examine managerial accounting quantitative and qualitative reviews and make

further choices.

3. DECISION-MAKING

Accounting management also perceives how certain choices can influence the conduct of a manager. A manager makes

long-term choices with a permanent effect, thus using financial accounting to create plans and communicate data with

the objective of enhancing management choices.

4. GOAL SETTING

Accounting management also perceives how certain choices can influence the conduct of a manager. A manager makes

lengthy-term choices that have a permanent effect, thus using financial accounting to create proposals and

communicate data with the aim of enhancing management choices

5. PROBLEM-SOLVING

Unlike financial accounting, which concentrates on historical data, management accounting perceives real performance

and relates it to objectives and outlooks for the future. This data is used to define problems that may emerge from

expenditures or changes in manufacturing and to create options (toppr, 2019)

DIFFERENT METHODS USED FOR MANAGEMENT ACCOUNTING REPORTING

Managerial accounting relies on internal financial reporting data received. Controlling, planning and decision-making are

applied for management accounting. Management accountants are based on the balance sheet, report of profit and

analysis of cash flow. However, in evaluating corporate information, they also apply other forms of accounting reports.

Which can involve monitoring of the budgets, material and quality.

1. Cost Report

2. Performance Report

5

achievable or cost-effective performance under the constraints provided by increasing desired aspects and reducing

unwanted aspects.

INTEGRATION OF MANAGEMNT ACCOUNTING WITHIN KHAADI AND ITS USEFLNESS FOR THE MANAGEMNET

THE BENEFITS OF MANAGEMENT ACCOUNTING SYSTEMS AND THEIR APPLICATIONS

Management accounting is primarily used to generate data within an organization for executives. While financial

accounting is of greatest benefit to stakeholders, financial accounting enables to achieve inner organizational goals.

1. Planning

2. Controlling

3. Decision-Making

4. Problem-Solving

5. Goal setting

1. PLANNING

Future planning is a main focus of financial accounting. Management auditors create more comprehensive reports than

economic accountants. They can include particular product data, market reach and regional data

2. CONTROLLING

The managerial accounting data provides managers a higher feeling of control over the achievement of an organization.

During the control stage, executives examine managerial accounting quantitative and qualitative reviews and make

further choices.

3. DECISION-MAKING

Accounting management also perceives how certain choices can influence the conduct of a manager. A manager makes

long-term choices with a permanent effect, thus using financial accounting to create plans and communicate data with

the objective of enhancing management choices.

4. GOAL SETTING

Accounting management also perceives how certain choices can influence the conduct of a manager. A manager makes

lengthy-term choices that have a permanent effect, thus using financial accounting to create proposals and

communicate data with the aim of enhancing management choices

5. PROBLEM-SOLVING

Unlike financial accounting, which concentrates on historical data, management accounting perceives real performance

and relates it to objectives and outlooks for the future. This data is used to define problems that may emerge from

expenditures or changes in manufacturing and to create options (toppr, 2019)

DIFFERENT METHODS USED FOR MANAGEMENT ACCOUNTING REPORTING

Managerial accounting relies on internal financial reporting data received. Controlling, planning and decision-making are

applied for management accounting. Management accountants are based on the balance sheet, report of profit and

analysis of cash flow. However, in evaluating corporate information, they also apply other forms of accounting reports.

Which can involve monitoring of the budgets, material and quality.

1. Cost Report

2. Performance Report

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

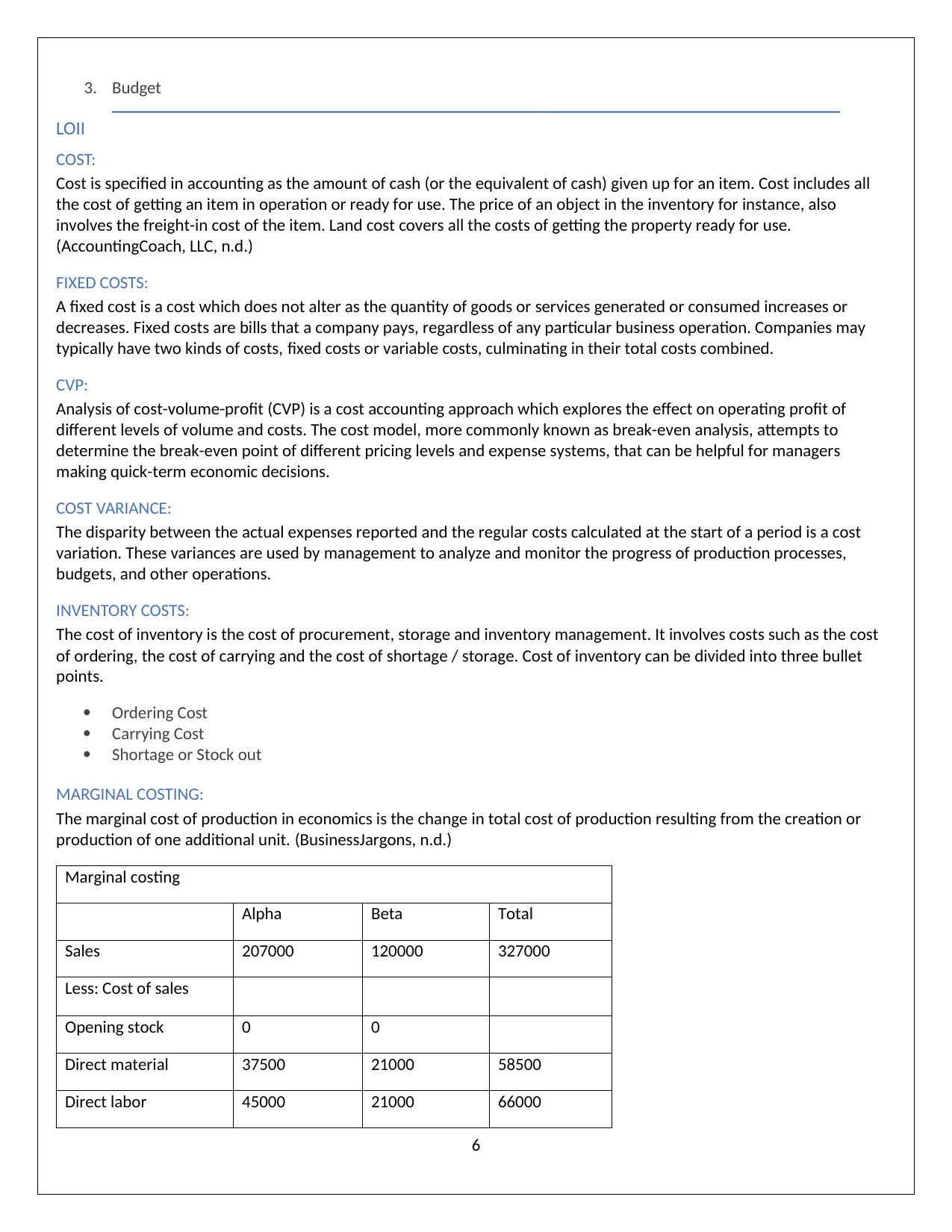

3. Budget

LOII

COST:

Cost is specified in accounting as the amount of cash (or the equivalent of cash) given up for an item. Cost includes all

the cost of getting an item in operation or ready for use. The price of an object in the inventory for instance, also

involves the freight-in cost of the item. Land cost covers all the costs of getting the property ready for use.

(AccountingCoach, LLC, n.d.)

FIXED COSTS:

A fixed cost is a cost which does not alter as the quantity of goods or services generated or consumed increases or

decreases. Fixed costs are bills that a company pays, regardless of any particular business operation. Companies may

typically have two kinds of costs, fixed costs or variable costs, culminating in their total costs combined.

CVP:

Analysis of cost-volume-profit (CVP) is a cost accounting approach which explores the effect on operating profit of

different levels of volume and costs. The cost model, more commonly known as break-even analysis, attempts to

determine the break-even point of different pricing levels and expense systems, that can be helpful for managers

making quick-term economic decisions.

COST VARIANCE:

The disparity between the actual expenses reported and the regular costs calculated at the start of a period is a cost

variation. These variances are used by management to analyze and monitor the progress of production processes,

budgets, and other operations.

INVENTORY COSTS:

The cost of inventory is the cost of procurement, storage and inventory management. It involves costs such as the cost

of ordering, the cost of carrying and the cost of shortage / storage. Cost of inventory can be divided into three bullet

points.

Ordering Cost

Carrying Cost

Shortage or Stock out

MARGINAL COSTING:

The marginal cost of production in economics is the change in total cost of production resulting from the creation or

production of one additional unit. (BusinessJargons, n.d.)

Marginal costing

Alpha Beta Total

Sales 207000 120000 327000

Less: Cost of sales

Opening stock 0 0

Direct material 37500 21000 58500

Direct labor 45000 21000 66000

6

LOII

COST:

Cost is specified in accounting as the amount of cash (or the equivalent of cash) given up for an item. Cost includes all

the cost of getting an item in operation or ready for use. The price of an object in the inventory for instance, also

involves the freight-in cost of the item. Land cost covers all the costs of getting the property ready for use.

(AccountingCoach, LLC, n.d.)

FIXED COSTS:

A fixed cost is a cost which does not alter as the quantity of goods or services generated or consumed increases or

decreases. Fixed costs are bills that a company pays, regardless of any particular business operation. Companies may

typically have two kinds of costs, fixed costs or variable costs, culminating in their total costs combined.

CVP:

Analysis of cost-volume-profit (CVP) is a cost accounting approach which explores the effect on operating profit of

different levels of volume and costs. The cost model, more commonly known as break-even analysis, attempts to

determine the break-even point of different pricing levels and expense systems, that can be helpful for managers

making quick-term economic decisions.

COST VARIANCE:

The disparity between the actual expenses reported and the regular costs calculated at the start of a period is a cost

variation. These variances are used by management to analyze and monitor the progress of production processes,

budgets, and other operations.

INVENTORY COSTS:

The cost of inventory is the cost of procurement, storage and inventory management. It involves costs such as the cost

of ordering, the cost of carrying and the cost of shortage / storage. Cost of inventory can be divided into three bullet

points.

Ordering Cost

Carrying Cost

Shortage or Stock out

MARGINAL COSTING:

The marginal cost of production in economics is the change in total cost of production resulting from the creation or

production of one additional unit. (BusinessJargons, n.d.)

Marginal costing

Alpha Beta Total

Sales 207000 120000 327000

Less: Cost of sales

Opening stock 0 0

Direct material 37500 21000 58500

Direct labor 45000 21000 66000

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

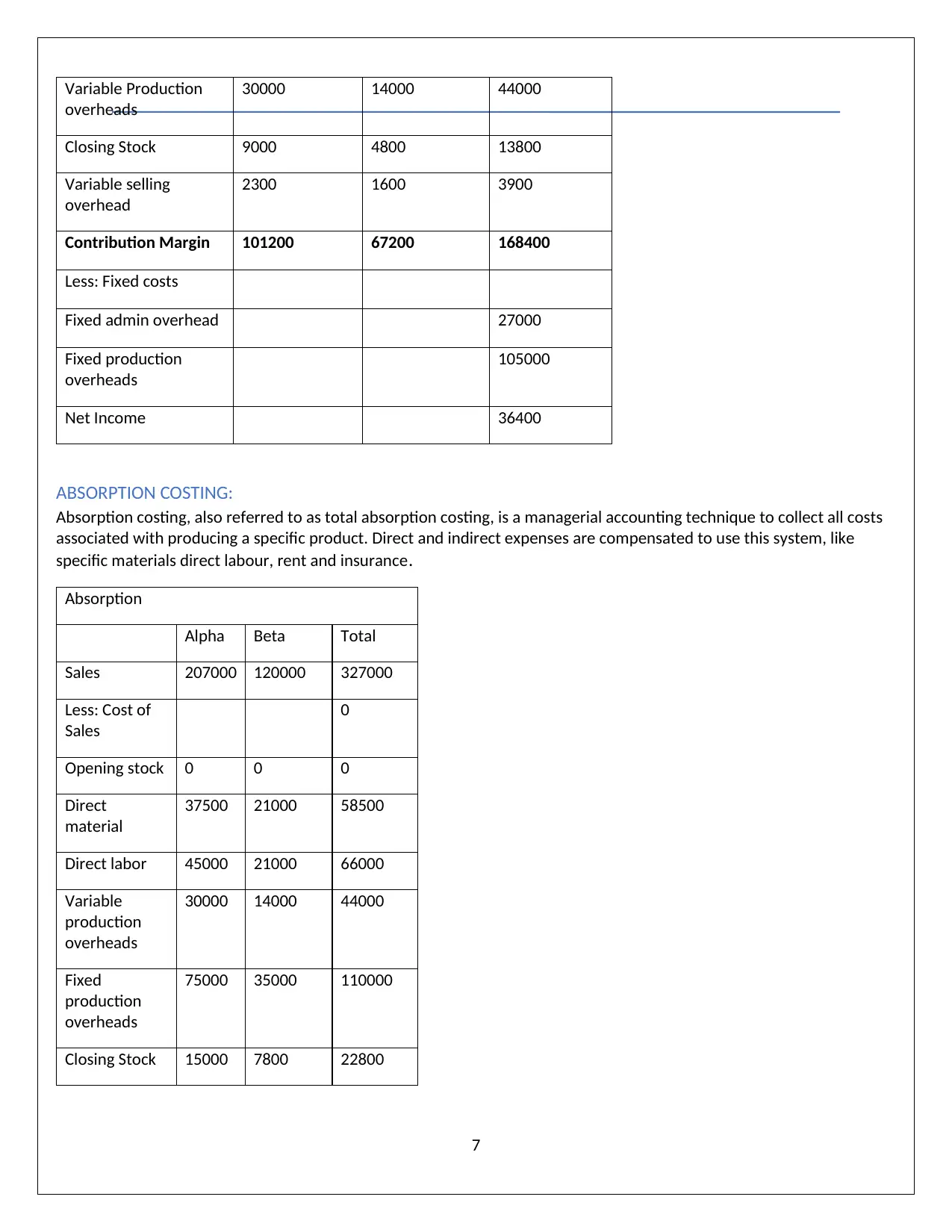

Variable Production

overheads

30000 14000 44000

Closing Stock 9000 4800 13800

Variable selling

overhead

2300 1600 3900

Contribution Margin 101200 67200 168400

Less: Fixed costs

Fixed admin overhead 27000

Fixed production

overheads

105000

Net Income 36400

ABSORPTION COSTING:

Absorption costing, also referred to as total absorption costing, is a managerial accounting technique to collect all costs

associated with producing a specific product. Direct and indirect expenses are compensated to use this system, like

specific materials direct labour, rent and insurance.

Absorption

Alpha Beta Total

Sales 207000 120000 327000

Less: Cost of

Sales

0

Opening stock 0 0 0

Direct

material

37500 21000 58500

Direct labor 45000 21000 66000

Variable

production

overheads

30000 14000 44000

Fixed

production

overheads

75000 35000 110000

Closing Stock 15000 7800 22800

7

overheads

30000 14000 44000

Closing Stock 9000 4800 13800

Variable selling

overhead

2300 1600 3900

Contribution Margin 101200 67200 168400

Less: Fixed costs

Fixed admin overhead 27000

Fixed production

overheads

105000

Net Income 36400

ABSORPTION COSTING:

Absorption costing, also referred to as total absorption costing, is a managerial accounting technique to collect all costs

associated with producing a specific product. Direct and indirect expenses are compensated to use this system, like

specific materials direct labour, rent and insurance.

Absorption

Alpha Beta Total

Sales 207000 120000 327000

Less: Cost of

Sales

0

Opening stock 0 0 0

Direct

material

37500 21000 58500

Direct labor 45000 21000 66000

Variable

production

overheads

30000 14000 44000

Fixed

production

overheads

75000 35000 110000

Closing Stock 15000 7800 22800

7

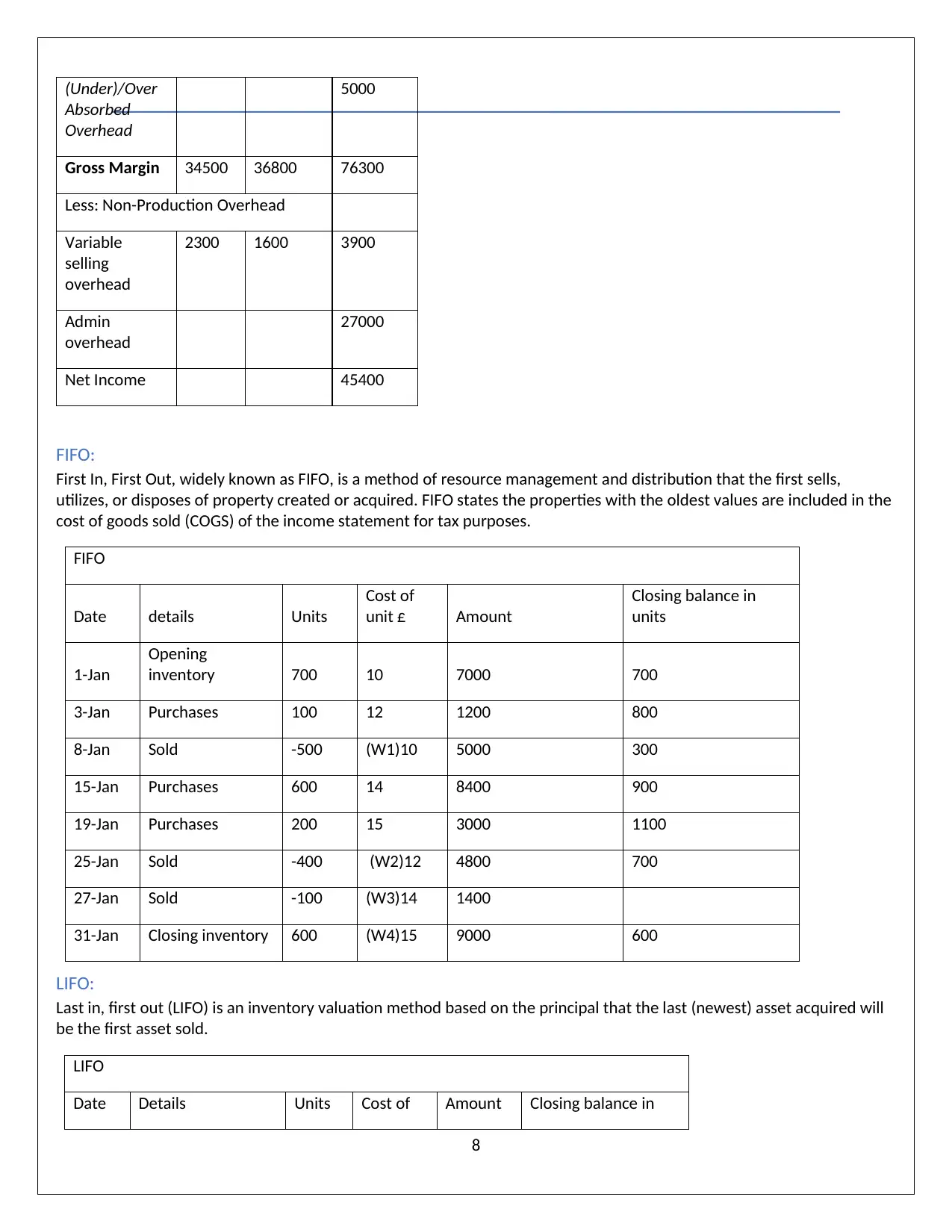

(Under)/Over

Absorbed

Overhead

5000

Gross Margin 34500 36800 76300

Less: Non-Production Overhead

Variable

selling

overhead

2300 1600 3900

Admin

overhead

27000

Net Income 45400

FIFO:

First In, First Out, widely known as FIFO, is a method of resource management and distribution that the first sells,

utilizes, or disposes of property created or acquired. FIFO states the properties with the oldest values are included in the

cost of goods sold (COGS) of the income statement for tax purposes.

FIFO

Date details Units

Cost of

unit £ Amount

Closing balance in

units

1-Jan

Opening

inventory 700 10 7000 700

3-Jan Purchases 100 12 1200 800

8-Jan Sold -500 (W1)10 5000 300

15-Jan Purchases 600 14 8400 900

19-Jan Purchases 200 15 3000 1100

25-Jan Sold -400 (W2)12 4800 700

27-Jan Sold -100 (W3)14 1400

31-Jan Closing inventory 600 (W4)15 9000 600

LIFO:

Last in, first out (LIFO) is an inventory valuation method based on the principal that the last (newest) asset acquired will

be the first asset sold.

LIFO

Date Details Units Cost of Amount Closing balance in

8

Absorbed

Overhead

5000

Gross Margin 34500 36800 76300

Less: Non-Production Overhead

Variable

selling

overhead

2300 1600 3900

Admin

overhead

27000

Net Income 45400

FIFO:

First In, First Out, widely known as FIFO, is a method of resource management and distribution that the first sells,

utilizes, or disposes of property created or acquired. FIFO states the properties with the oldest values are included in the

cost of goods sold (COGS) of the income statement for tax purposes.

FIFO

Date details Units

Cost of

unit £ Amount

Closing balance in

units

1-Jan

Opening

inventory 700 10 7000 700

3-Jan Purchases 100 12 1200 800

8-Jan Sold -500 (W1)10 5000 300

15-Jan Purchases 600 14 8400 900

19-Jan Purchases 200 15 3000 1100

25-Jan Sold -400 (W2)12 4800 700

27-Jan Sold -100 (W3)14 1400

31-Jan Closing inventory 600 (W4)15 9000 600

LIFO:

Last in, first out (LIFO) is an inventory valuation method based on the principal that the last (newest) asset acquired will

be the first asset sold.

LIFO

Date Details Units Cost of Amount Closing balance in

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

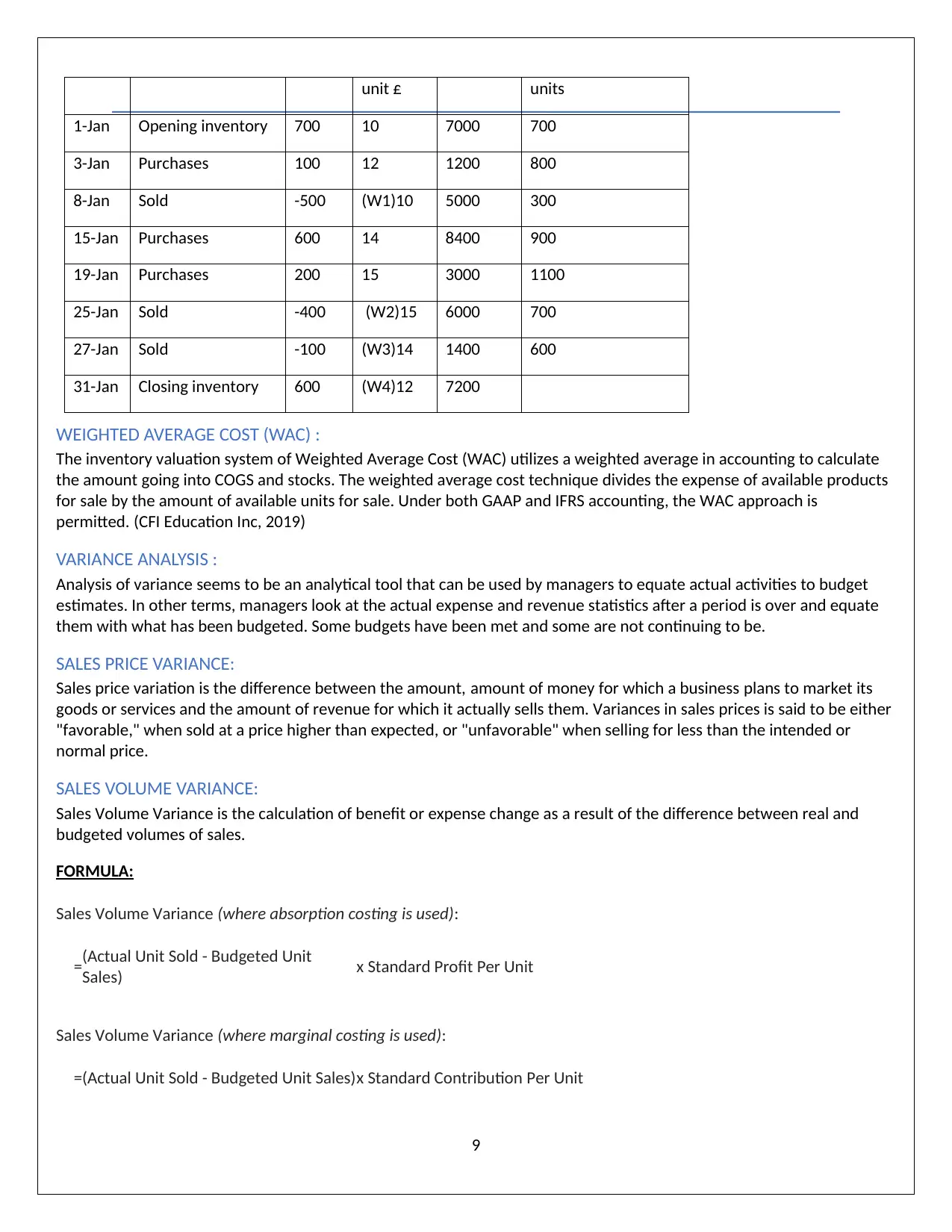

unit £ units

1-Jan Opening inventory 700 10 7000 700

3-Jan Purchases 100 12 1200 800

8-Jan Sold -500 (W1)10 5000 300

15-Jan Purchases 600 14 8400 900

19-Jan Purchases 200 15 3000 1100

25-Jan Sold -400 (W2)15 6000 700

27-Jan Sold -100 (W3)14 1400 600

31-Jan Closing inventory 600 (W4)12 7200

WEIGHTED AVERAGE COST (WAC) :

The inventory valuation system of Weighted Average Cost (WAC) utilizes a weighted average in accounting to calculate

the amount going into COGS and stocks. The weighted average cost technique divides the expense of available products

for sale by the amount of available units for sale. Under both GAAP and IFRS accounting, the WAC approach is

permitted. (CFI Education Inc, 2019)

VARIANCE ANALYSIS :

Analysis of variance seems to be an analytical tool that can be used by managers to equate actual activities to budget

estimates. In other terms, managers look at the actual expense and revenue statistics after a period is over and equate

them with what has been budgeted. Some budgets have been met and some are not continuing to be.

SALES PRICE VARIANCE:

Sales price variation is the difference between the amount, amount of money for which a business plans to market its

goods or services and the amount of revenue for which it actually sells them. Variances in sales prices is said to be either

"favorable," when sold at a price higher than expected, or "unfavorable" when selling for less than the intended or

normal price.

SALES VOLUME VARIANCE:

Sales Volume Variance is the calculation of benefit or expense change as a result of the difference between real and

budgeted volumes of sales.

FORMULA:

Sales Volume Variance (where absorption costing is used):

=(Actual Unit Sold - Budgeted Unit

Sales) x Standard Profit Per Unit

Sales Volume Variance (where marginal costing is used):

=(Actual Unit Sold - Budgeted Unit Sales)x Standard Contribution Per Unit

9

1-Jan Opening inventory 700 10 7000 700

3-Jan Purchases 100 12 1200 800

8-Jan Sold -500 (W1)10 5000 300

15-Jan Purchases 600 14 8400 900

19-Jan Purchases 200 15 3000 1100

25-Jan Sold -400 (W2)15 6000 700

27-Jan Sold -100 (W3)14 1400 600

31-Jan Closing inventory 600 (W4)12 7200

WEIGHTED AVERAGE COST (WAC) :

The inventory valuation system of Weighted Average Cost (WAC) utilizes a weighted average in accounting to calculate

the amount going into COGS and stocks. The weighted average cost technique divides the expense of available products

for sale by the amount of available units for sale. Under both GAAP and IFRS accounting, the WAC approach is

permitted. (CFI Education Inc, 2019)

VARIANCE ANALYSIS :

Analysis of variance seems to be an analytical tool that can be used by managers to equate actual activities to budget

estimates. In other terms, managers look at the actual expense and revenue statistics after a period is over and equate

them with what has been budgeted. Some budgets have been met and some are not continuing to be.

SALES PRICE VARIANCE:

Sales price variation is the difference between the amount, amount of money for which a business plans to market its

goods or services and the amount of revenue for which it actually sells them. Variances in sales prices is said to be either

"favorable," when sold at a price higher than expected, or "unfavorable" when selling for less than the intended or

normal price.

SALES VOLUME VARIANCE:

Sales Volume Variance is the calculation of benefit or expense change as a result of the difference between real and

budgeted volumes of sales.

FORMULA:

Sales Volume Variance (where absorption costing is used):

=(Actual Unit Sold - Budgeted Unit

Sales) x Standard Profit Per Unit

Sales Volume Variance (where marginal costing is used):

=(Actual Unit Sold - Budgeted Unit Sales)x Standard Contribution Per Unit

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

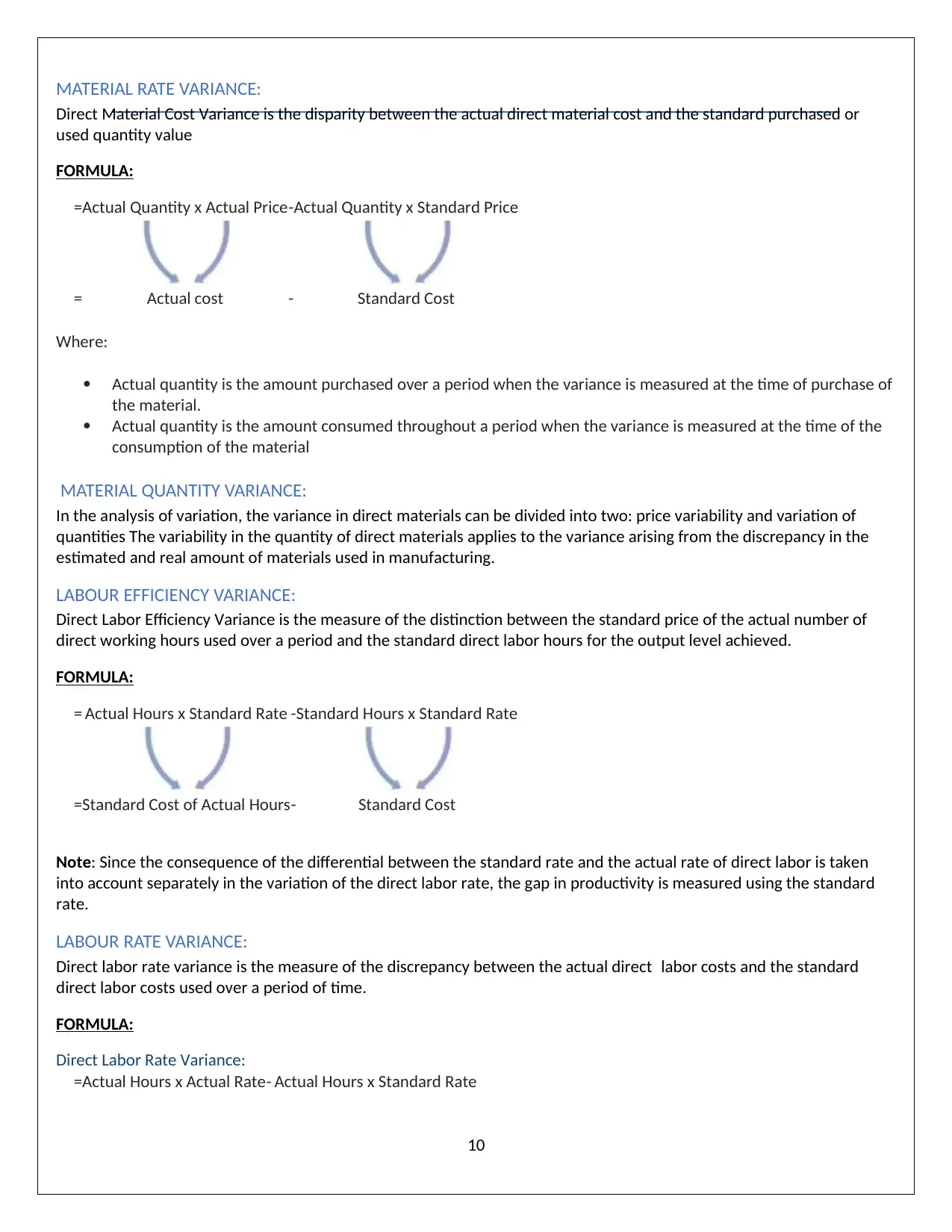

MATERIAL RATE VARIANCE:

Direct Material Cost Variance is the disparity between the actual direct material cost and the standard purchased or

used quantity value

FORMULA:

=Actual Quantity x Actual Price-Actual Quantity x Standard Price

= Actual cost - Standard Cost

Where:

Actual quantity is the amount purchased over a period when the variance is measured at the time of purchase of

the material.

Actual quantity is the amount consumed throughout a period when the variance is measured at the time of the

consumption of the material

MATERIAL QUANTITY VARIANCE:

In the analysis of variation, the variance in direct materials can be divided into two: price variability and variation of

quantities The variability in the quantity of direct materials applies to the variance arising from the discrepancy in the

estimated and real amount of materials used in manufacturing.

LABOUR EFFICIENCY VARIANCE:

Direct Labor Efficiency Variance is the measure of the distinction between the standard price of the actual number of

direct working hours used over a period and the standard direct labor hours for the output level achieved.

FORMULA:

= Actual Hours x Standard Rate -Standard Hours x Standard Rate

=Standard Cost of Actual Hours- Standard Cost

Note: Since the consequence of the differential between the standard rate and the actual rate of direct labor is taken

into account separately in the variation of the direct labor rate, the gap in productivity is measured using the standard

rate.

LABOUR RATE VARIANCE:

Direct labor rate variance is the measure of the discrepancy between the actual direct labor costs and the standard

direct labor costs used over a period of time.

FORMULA:

Direct Labor Rate Variance:

=Actual Hours x Actual Rate- Actual Hours x Standard Rate

10

Direct Material Cost Variance is the disparity between the actual direct material cost and the standard purchased or

used quantity value

FORMULA:

=Actual Quantity x Actual Price-Actual Quantity x Standard Price

= Actual cost - Standard Cost

Where:

Actual quantity is the amount purchased over a period when the variance is measured at the time of purchase of

the material.

Actual quantity is the amount consumed throughout a period when the variance is measured at the time of the

consumption of the material

MATERIAL QUANTITY VARIANCE:

In the analysis of variation, the variance in direct materials can be divided into two: price variability and variation of

quantities The variability in the quantity of direct materials applies to the variance arising from the discrepancy in the

estimated and real amount of materials used in manufacturing.

LABOUR EFFICIENCY VARIANCE:

Direct Labor Efficiency Variance is the measure of the distinction between the standard price of the actual number of

direct working hours used over a period and the standard direct labor hours for the output level achieved.

FORMULA:

= Actual Hours x Standard Rate -Standard Hours x Standard Rate

=Standard Cost of Actual Hours- Standard Cost

Note: Since the consequence of the differential between the standard rate and the actual rate of direct labor is taken

into account separately in the variation of the direct labor rate, the gap in productivity is measured using the standard

rate.

LABOUR RATE VARIANCE:

Direct labor rate variance is the measure of the discrepancy between the actual direct labor costs and the standard

direct labor costs used over a period of time.

FORMULA:

Direct Labor Rate Variance:

=Actual Hours x Actual Rate- Actual Hours x Standard Rate

10

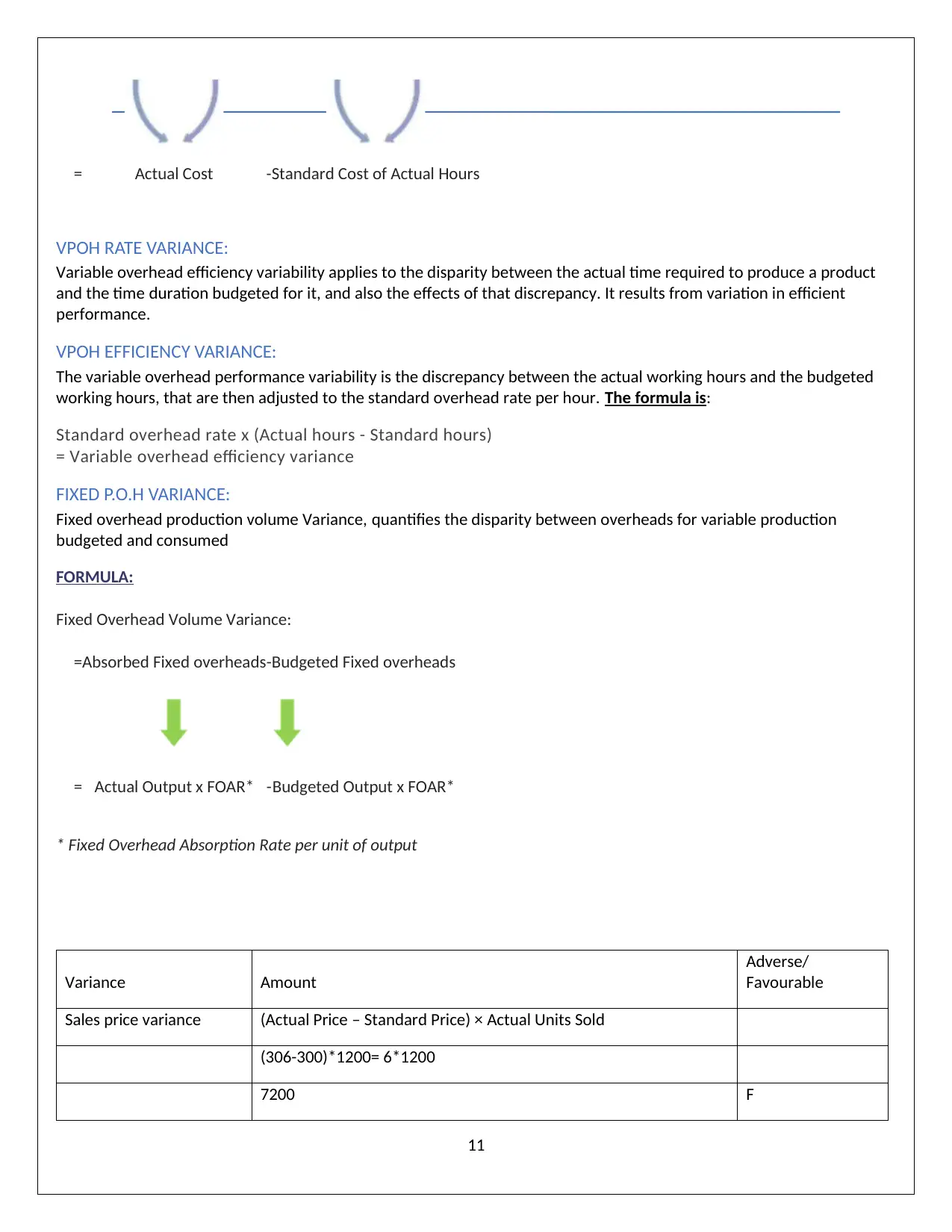

= Actual Cost -Standard Cost of Actual Hours

VPOH RATE VARIANCE:

Variable overhead efficiency variability applies to the disparity between the actual time required to produce a product

and the time duration budgeted for it, and also the effects of that discrepancy. It results from variation in efficient

performance.

VPOH EFFICIENCY VARIANCE:

The variable overhead performance variability is the discrepancy between the actual working hours and the budgeted

working hours, that are then adjusted to the standard overhead rate per hour. The formula is:

Standard overhead rate x (Actual hours - Standard hours)

= Variable overhead efficiency variance

FIXED P.O.H VARIANCE:

Fixed overhead production volume Variance, quantifies the disparity between overheads for variable production

budgeted and consumed

FORMULA:

Fixed Overhead Volume Variance:

=Absorbed Fixed overheads-Budgeted Fixed overheads

= Actual Output x FOAR* -Budgeted Output x FOAR*

* Fixed Overhead Absorption Rate per unit of output

Variance Amount

Adverse/

Favourable

Sales price variance (Actual Price – Standard Price) × Actual Units Sold

(306-300)*1200= 6*1200

7200 F

11

VPOH RATE VARIANCE:

Variable overhead efficiency variability applies to the disparity between the actual time required to produce a product

and the time duration budgeted for it, and also the effects of that discrepancy. It results from variation in efficient

performance.

VPOH EFFICIENCY VARIANCE:

The variable overhead performance variability is the discrepancy between the actual working hours and the budgeted

working hours, that are then adjusted to the standard overhead rate per hour. The formula is:

Standard overhead rate x (Actual hours - Standard hours)

= Variable overhead efficiency variance

FIXED P.O.H VARIANCE:

Fixed overhead production volume Variance, quantifies the disparity between overheads for variable production

budgeted and consumed

FORMULA:

Fixed Overhead Volume Variance:

=Absorbed Fixed overheads-Budgeted Fixed overheads

= Actual Output x FOAR* -Budgeted Output x FOAR*

* Fixed Overhead Absorption Rate per unit of output

Variance Amount

Adverse/

Favourable

Sales price variance (Actual Price – Standard Price) × Actual Units Sold

(306-300)*1200= 6*1200

7200 F

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.