Financial Problem Solving: Management Accounting Strategies

VerifiedAdded on 2024/05/17

|27

|6313

|171

Report

AI Summary

This report provides a comprehensive analysis of management accounting applications within a broader business environment. It defines management accounting and its systems, distinguishing it from financial accounting, and evaluates its benefits within organizations. The report explores various types of management accounting systems, managerial accounting reports, and methods, emphasizing the importance of relevant, reliable, accurate, and understandable information. It delves into cost analysis, including different types of costs and the preparation of income statements using absorption and marginal costing, alongside flexible budgeting. Furthermore, the document discusses budgeting processes, pricing strategies, supply and demand considerations, and costing activities, highlighting the use of SWOT analysis to improve financial positions. The report also identifies financial problems using indicators, defines financial governance, and discusses the characteristics of an effective management accountant, emphasizing the significance of timely reporting and full financial disclosure. Finally, it analyzes how management accounting can lead organizations to sustainable success by responding to financial problems effectively.

Application of management accounting to the wider

business environment

1

business environment

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction.....................................................................................................................................................................3

Task 1..............................................................................................................................................................................4

1.1 Define and explain management accounting (P1)...............................................................................................4

1.2 What is a management accounting system and why it is important to integrate it within an organization (P1)?4

1.3 Distinguish between management and financial accounting (P1).......................................................................4

1.4 Define and explain what the following different types of management accounting systems are and their

benefits for an organization (P1)................................................................................................................................5

1.5 Explain the different types of managerial accounting reports and methods used for reporting (P2)...................7

1.6 Discuss why the information should be relevant to the user, reliable, up to date accurate and understandable to

the user (P2)...............................................................................................................................................................8

1.7 Evaluate the benefits of management accounting systems and their application within an organizational

context (M1)...............................................................................................................................................................8

1.8 Critically evaluate how management accounting systems and management accounting reporting is integrated

within organisational processes. Provide justifications to your proposed methods and their benefits in an

organisational context (D1)........................................................................................................................................8

Task 2..............................................................................................................................................................................9

2.1 What is meant by cost? Briefly explain the different types of costs and cost analysis (P3)................................9

2.2 Define the following terms and discuss their concept (P3):................................................................................9

2.3 Calculate the costs using appropriate techniques of cost analysis to prepare an income statement by apply

Absorption costing and Marginal costing. (P3).......................................................................................................10

2.4 What is the minimum number of units that Zak needs to sell per year (for one of his products X) for him to

make a profit? Use the formula method...................................................................................................................14

2.5 Prepare a flexible budget for Zak and calculate the cost analysis......................................................................14

2.6 Accurately apply a range of management accounting techniques and produce appropriate financial reporting

documents (M2).......................................................................................................................................................15

2.7 Produce financial reports that accurately apply and interpret data for a range of business activities (D2).......15

Task 3............................................................................................................................................................................17

3.1 What are budgets and how are budgets prepared (P4)?.....................................................................................17

3.2 Discuss different types of budgets; capital and operating budgets (P4)?...........................................................17

3.3 Discuss different pricing strategies. How do competitors determine their price (P4)?.....................................18

3.4 What is meant by supply & demand considerations? How does supply and demand affect pricing (P4)?.......19

3.5 How do cost systems differ depending on the costing activity: job costing, process costing, batch costing and

contract costing (P4)?...............................................................................................................................................19

3.6 How does applying SWOT analysis improve the financial position of an organisation (P4)?..........................20

3.7 Analyse the use of different planning tools and their application for preparing and forecasting budgets (M3).

..................................................................................................................................................................................21

Task 4............................................................................................................................................................................22

4.1 Identify financial problems using indicators (P5);.............................................................................................22

4.2 Define financial governance and how this can be used to pre-empt or prevent financial problems. How do we

use financial governance to monitor strategy (P5)?.................................................................................................22

4.3 What are the characteristics of an effective management accountant? How can these skills be used to prevent

and/or deal with problems (P5)?..............................................................................................................................23

4.4 Discuss the significance of developing strategies and systems which require effective and timely reporting,

full disclosure of financial positions and are responsibly owned and governed for organisations. (P5).................23

4.5 Analyse how, in responding to financial problems, management accounting can lead organisations to

sustainable success (M4)..........................................................................................................................................24

4.6 Evaluate how planning tools for accounting respond appropriately to solving financial problems to lead

organisations to sustainable success (D3)................................................................................................................24

Conclusion....................................................................................................................................................................25

References:....................................................................................................................................................................26

2

Introduction.....................................................................................................................................................................3

Task 1..............................................................................................................................................................................4

1.1 Define and explain management accounting (P1)...............................................................................................4

1.2 What is a management accounting system and why it is important to integrate it within an organization (P1)?4

1.3 Distinguish between management and financial accounting (P1).......................................................................4

1.4 Define and explain what the following different types of management accounting systems are and their

benefits for an organization (P1)................................................................................................................................5

1.5 Explain the different types of managerial accounting reports and methods used for reporting (P2)...................7

1.6 Discuss why the information should be relevant to the user, reliable, up to date accurate and understandable to

the user (P2)...............................................................................................................................................................8

1.7 Evaluate the benefits of management accounting systems and their application within an organizational

context (M1)...............................................................................................................................................................8

1.8 Critically evaluate how management accounting systems and management accounting reporting is integrated

within organisational processes. Provide justifications to your proposed methods and their benefits in an

organisational context (D1)........................................................................................................................................8

Task 2..............................................................................................................................................................................9

2.1 What is meant by cost? Briefly explain the different types of costs and cost analysis (P3)................................9

2.2 Define the following terms and discuss their concept (P3):................................................................................9

2.3 Calculate the costs using appropriate techniques of cost analysis to prepare an income statement by apply

Absorption costing and Marginal costing. (P3).......................................................................................................10

2.4 What is the minimum number of units that Zak needs to sell per year (for one of his products X) for him to

make a profit? Use the formula method...................................................................................................................14

2.5 Prepare a flexible budget for Zak and calculate the cost analysis......................................................................14

2.6 Accurately apply a range of management accounting techniques and produce appropriate financial reporting

documents (M2).......................................................................................................................................................15

2.7 Produce financial reports that accurately apply and interpret data for a range of business activities (D2).......15

Task 3............................................................................................................................................................................17

3.1 What are budgets and how are budgets prepared (P4)?.....................................................................................17

3.2 Discuss different types of budgets; capital and operating budgets (P4)?...........................................................17

3.3 Discuss different pricing strategies. How do competitors determine their price (P4)?.....................................18

3.4 What is meant by supply & demand considerations? How does supply and demand affect pricing (P4)?.......19

3.5 How do cost systems differ depending on the costing activity: job costing, process costing, batch costing and

contract costing (P4)?...............................................................................................................................................19

3.6 How does applying SWOT analysis improve the financial position of an organisation (P4)?..........................20

3.7 Analyse the use of different planning tools and their application for preparing and forecasting budgets (M3).

..................................................................................................................................................................................21

Task 4............................................................................................................................................................................22

4.1 Identify financial problems using indicators (P5);.............................................................................................22

4.2 Define financial governance and how this can be used to pre-empt or prevent financial problems. How do we

use financial governance to monitor strategy (P5)?.................................................................................................22

4.3 What are the characteristics of an effective management accountant? How can these skills be used to prevent

and/or deal with problems (P5)?..............................................................................................................................23

4.4 Discuss the significance of developing strategies and systems which require effective and timely reporting,

full disclosure of financial positions and are responsibly owned and governed for organisations. (P5).................23

4.5 Analyse how, in responding to financial problems, management accounting can lead organisations to

sustainable success (M4)..........................................................................................................................................24

4.6 Evaluate how planning tools for accounting respond appropriately to solving financial problems to lead

organisations to sustainable success (D3)................................................................................................................24

Conclusion....................................................................................................................................................................25

References:....................................................................................................................................................................26

2

Introduction

Management accounting is the technique which is required to be used in all the businesses and in

this there will be a need to catty out various processes which includes interpretation, collection,

and analyzation of the information. In this report, all of the elements which are related to it such

as systems and reporting will be taken into consideration. Then the marginal and absorption

costing will be used to make the income statement and also the analysis will be carried out of the

variances from the budgets which are provided. There is the discussion which will be performed

about the budgets and other techniques to be used in the planning system. Then in the last part of

the assignment, there will be an explanation of the methods which can be used in the process of

dealing with financial problems.

3

Management accounting is the technique which is required to be used in all the businesses and in

this there will be a need to catty out various processes which includes interpretation, collection,

and analyzation of the information. In this report, all of the elements which are related to it such

as systems and reporting will be taken into consideration. Then the marginal and absorption

costing will be used to make the income statement and also the analysis will be carried out of the

variances from the budgets which are provided. There is the discussion which will be performed

about the budgets and other techniques to be used in the planning system. Then in the last part of

the assignment, there will be an explanation of the methods which can be used in the process of

dealing with financial problems.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 1

1.1 Define and explain management accounting (P1).

Management accounting is the process in which there will be various techniques which will be

undertaken and the main purpose will use all the resources which are present in the most

effective manner. By the help of this, it will be possible for the managers to increase the

shareholders and customers value. All the principles will be required to be applied under this as

by that it will be possible for the company to plan and organize all the activities in the proper

manner as the information will be provided which aids in decision making.

1.2 What is a management accounting system and why it is important to integrate it into an

organization (P1)?

In the business, it is required that all the resources shall be managed properly and for that, there

is the need of the proper information system by which all the information can be collected and

that is done by the management accounting system. This is integrated into the organization as by

the help of this there are various tasks which are performed. All the information which is needed

in the calculation of cost will be ascertained by it and also for the performance evaluation and

planning and controlling (Bukenya, 2014). The decisions which are to be made by the managers

will be made by the use of the data which is collected by this and it helps in proper management

as best decisions are taken. The information which is required by different departments is variant

and so due to this several types of information will have to be collected by the use of systems

and this is a difficult task which is to be performed in proper manner as all the activities in the

department will be based on this and will describe the success of organisation.

1.3 Distinguish between management and financial accounting (P1).

The difference between financial and management accounting is as follows:

Basis Financial accounting Management accounting

4

1.1 Define and explain management accounting (P1).

Management accounting is the process in which there will be various techniques which will be

undertaken and the main purpose will use all the resources which are present in the most

effective manner. By the help of this, it will be possible for the managers to increase the

shareholders and customers value. All the principles will be required to be applied under this as

by that it will be possible for the company to plan and organize all the activities in the proper

manner as the information will be provided which aids in decision making.

1.2 What is a management accounting system and why it is important to integrate it into an

organization (P1)?

In the business, it is required that all the resources shall be managed properly and for that, there

is the need of the proper information system by which all the information can be collected and

that is done by the management accounting system. This is integrated into the organization as by

the help of this there are various tasks which are performed. All the information which is needed

in the calculation of cost will be ascertained by it and also for the performance evaluation and

planning and controlling (Bukenya, 2014). The decisions which are to be made by the managers

will be made by the use of the data which is collected by this and it helps in proper management

as best decisions are taken. The information which is required by different departments is variant

and so due to this several types of information will have to be collected by the use of systems

and this is a difficult task which is to be performed in proper manner as all the activities in the

department will be based on this and will describe the success of organisation.

1.3 Distinguish between management and financial accounting (P1).

The difference between financial and management accounting is as follows:

Basis Financial accounting Management accounting

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

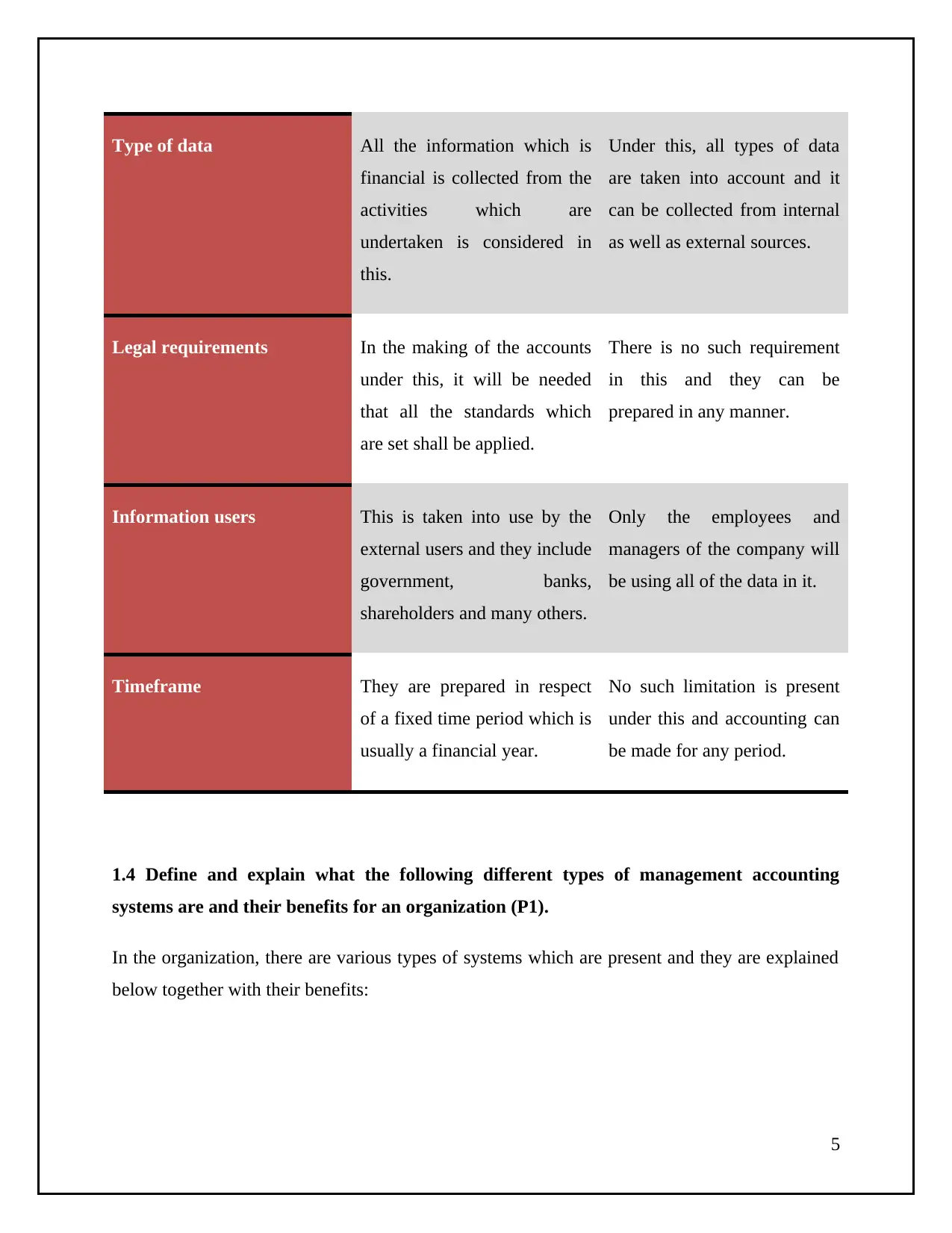

Type of data All the information which is

financial is collected from the

activities which are

undertaken is considered in

this.

Under this, all types of data

are taken into account and it

can be collected from internal

as well as external sources.

Legal requirements In the making of the accounts

under this, it will be needed

that all the standards which

are set shall be applied.

There is no such requirement

in this and they can be

prepared in any manner.

Information users This is taken into use by the

external users and they include

government, banks,

shareholders and many others.

Only the employees and

managers of the company will

be using all of the data in it.

Timeframe They are prepared in respect

of a fixed time period which is

usually a financial year.

No such limitation is present

under this and accounting can

be made for any period.

1.4 Define and explain what the following different types of management accounting

systems are and their benefits for an organization (P1).

In the organization, there are various types of systems which are present and they are explained

below together with their benefits:

5

financial is collected from the

activities which are

undertaken is considered in

this.

Under this, all types of data

are taken into account and it

can be collected from internal

as well as external sources.

Legal requirements In the making of the accounts

under this, it will be needed

that all the standards which

are set shall be applied.

There is no such requirement

in this and they can be

prepared in any manner.

Information users This is taken into use by the

external users and they include

government, banks,

shareholders and many others.

Only the employees and

managers of the company will

be using all of the data in it.

Timeframe They are prepared in respect

of a fixed time period which is

usually a financial year.

No such limitation is present

under this and accounting can

be made for any period.

1.4 Define and explain what the following different types of management accounting

systems are and their benefits for an organization (P1).

In the organization, there are various types of systems which are present and they are explained

below together with their benefits:

5

Cost accounting systems: This is the system with which all the cots which are incurred for any

product will be determined and then they will be used in the calculation of the total cost. By this,

it will be possible to establish the cost control, and the profitability of the company will be

maintained. There are various methods which are involved in this and they include process

costing in which cost is calculated in accordance with the processes which are undertaken and

then another method is job costing which is used when jobs are performed (Zaleha Abdul Rasid,

et. al., 2014.). In this, it shall be ensured that all the departments shall coordinate in a proper

manner so that proper establishment of the system takes place. There shall be such system which

will be easy to be understood by all so that they can carry out it in an effective manner and

benefit can be attained by that.

Inventory management systems: By the use of this system the matter which is related to

inventory will be managed in a proper manner. There will be suitable allocation which will be

made in relation to stock among all the departments which are present in the company so that

there are no issues which are faced. The requirement in relation to stock will be determined in

advance so that it can be managed accordingly.

Job costing systems: This is the system in which all the cost which are there will be calculated

and then they will be apportioned among the total units which have been manufactured and by

this the allocation will be made. This is useful in such cases in which there are same products are

6

Types of systems

Cost Accounting

system

Inventory

management

system

Job costing

system

Price optimising

system

product will be determined and then they will be used in the calculation of the total cost. By this,

it will be possible to establish the cost control, and the profitability of the company will be

maintained. There are various methods which are involved in this and they include process

costing in which cost is calculated in accordance with the processes which are undertaken and

then another method is job costing which is used when jobs are performed (Zaleha Abdul Rasid,

et. al., 2014.). In this, it shall be ensured that all the departments shall coordinate in a proper

manner so that proper establishment of the system takes place. There shall be such system which

will be easy to be understood by all so that they can carry out it in an effective manner and

benefit can be attained by that.

Inventory management systems: By the use of this system the matter which is related to

inventory will be managed in a proper manner. There will be suitable allocation which will be

made in relation to stock among all the departments which are present in the company so that

there are no issues which are faced. The requirement in relation to stock will be determined in

advance so that it can be managed accordingly.

Job costing systems: This is the system in which all the cost which are there will be calculated

and then they will be apportioned among the total units which have been manufactured and by

this the allocation will be made. This is useful in such cases in which there are same products are

6

Types of systems

Cost Accounting

system

Inventory

management

system

Job costing

system

Price optimising

system

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

made in the job which is undertaken and so it becomes easier to determine the cost. In this, the

preferences of customers are given are important and so the job is also performed accordingly

and then cost will be calculated by taking that into the account.

Price optimizing system: Price is required to be managed and for that, it is taken into use by

which proper control on price will be established. The demand will be considered in this as there

is a very important relationship that exists between the price and demand (De Toni, et. al., 2017).

There are various methods which are present and some of them are cost-plus pricing, discount

pricing, and penetration pricing.

1.5 Explain the different types of managerial accounting reports and methods used for

reporting (P2).

In the process of decision making it is needed that all the findings shall be recorded in a proper

manner and for that reporting is made and some of the most commonly used reports are as

follows:

Budgets: These are the plans which are made in respect of all the expenses which are required to

be made and by the help of this it will be possible to establish control and the evaluation of

performance will also be taking place. For making budgets, past data are taken into use together

with the forecasted one (Abdullahi and Kuwata, 2014). This will be one of the motivation factors

for the employees as they will be required to attain all the goals which are specified in them.

Job cost report: All the jobs which are performed in business will be considered and the

expenses which are made in relation to them will be identified. This will help in the evaluation of

all the activities and the ones in which highest cost is made will be evaluated to know the amount

of gain which is made in that (Legaspi, 2014). If there is less gain then the allocation will be

shifted to some more profitable job. By the help of this, it will be possible to reduce the wastage

which takes place and also all the resources will be utilized in the best manner.

Performance reports: Various evaluations are made and then the findings of them will be

recorded in this report as by that performance will be measured. The information which will be

used in this will be collected and presented in this so that it can be used in future also.

7

preferences of customers are given are important and so the job is also performed accordingly

and then cost will be calculated by taking that into the account.

Price optimizing system: Price is required to be managed and for that, it is taken into use by

which proper control on price will be established. The demand will be considered in this as there

is a very important relationship that exists between the price and demand (De Toni, et. al., 2017).

There are various methods which are present and some of them are cost-plus pricing, discount

pricing, and penetration pricing.

1.5 Explain the different types of managerial accounting reports and methods used for

reporting (P2).

In the process of decision making it is needed that all the findings shall be recorded in a proper

manner and for that reporting is made and some of the most commonly used reports are as

follows:

Budgets: These are the plans which are made in respect of all the expenses which are required to

be made and by the help of this it will be possible to establish control and the evaluation of

performance will also be taking place. For making budgets, past data are taken into use together

with the forecasted one (Abdullahi and Kuwata, 2014). This will be one of the motivation factors

for the employees as they will be required to attain all the goals which are specified in them.

Job cost report: All the jobs which are performed in business will be considered and the

expenses which are made in relation to them will be identified. This will help in the evaluation of

all the activities and the ones in which highest cost is made will be evaluated to know the amount

of gain which is made in that (Legaspi, 2014). If there is less gain then the allocation will be

shifted to some more profitable job. By the help of this, it will be possible to reduce the wastage

which takes place and also all the resources will be utilized in the best manner.

Performance reports: Various evaluations are made and then the findings of them will be

recorded in this report as by that performance will be measured. The information which will be

used in this will be collected and presented in this so that it can be used in future also.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory management report: all the information about the cost which will be incurred in the

production will be reported in this so that proper decision can be made in relation to it. By this,

the wastage which is performed will be identified and avoided. Also, the process will be

improved as the manner of working will be mentioned in this. The manner in which

improvements can be made will also be identified by the help of this.

1.6 Discuss why the information should be relevant to the user, reliable, up to date accurate

and understandable to the user (P2).

The information which is provided shall be relevant as by the use of that important decision are

made in the business and if the data will be incorrect then the whole process will be affected in

an adverse manner. Also, it shall be presented in an understandable manner so that all can easily

understand it as then only they will be able to use it in an effective way.

1.7 Evaluate the benefits of management accounting systems and their application within

an organizational context (M1).

By the use of the management accounting systems, there will be various benefits which will be

attained as all the required data will be made available and then it will also be helpful in the

decision making. Profits will be increased as the resources will be utilized in a proper manner

and there will be reduced which will be attained in cost (Lunkes, et. al., 2013). Best price will be

set which will lead to customer satisfaction and this will help in retaining them.

1.8 Critically evaluate how management accounting systems and management accounting

reporting is integrated within organizational processes. Provide justifications to your

proposed methods and their benefits in an organizational context (D1).

Both the systems and reports which are there are integrated as by the use of both company will

be able to achieve the goals and targets which are there. This is because the information needed

to make the process better is attained by systems and for the better understanding of that

recording is made by reports. All the activities are also connected as proper coordination is

established among all departments.

8

production will be reported in this so that proper decision can be made in relation to it. By this,

the wastage which is performed will be identified and avoided. Also, the process will be

improved as the manner of working will be mentioned in this. The manner in which

improvements can be made will also be identified by the help of this.

1.6 Discuss why the information should be relevant to the user, reliable, up to date accurate

and understandable to the user (P2).

The information which is provided shall be relevant as by the use of that important decision are

made in the business and if the data will be incorrect then the whole process will be affected in

an adverse manner. Also, it shall be presented in an understandable manner so that all can easily

understand it as then only they will be able to use it in an effective way.

1.7 Evaluate the benefits of management accounting systems and their application within

an organizational context (M1).

By the use of the management accounting systems, there will be various benefits which will be

attained as all the required data will be made available and then it will also be helpful in the

decision making. Profits will be increased as the resources will be utilized in a proper manner

and there will be reduced which will be attained in cost (Lunkes, et. al., 2013). Best price will be

set which will lead to customer satisfaction and this will help in retaining them.

1.8 Critically evaluate how management accounting systems and management accounting

reporting is integrated within organizational processes. Provide justifications to your

proposed methods and their benefits in an organizational context (D1).

Both the systems and reports which are there are integrated as by the use of both company will

be able to achieve the goals and targets which are there. This is because the information needed

to make the process better is attained by systems and for the better understanding of that

recording is made by reports. All the activities are also connected as proper coordination is

established among all departments.

8

Task 2

2.1 What is meant by cost? Briefly explain the different types of costs and cost analysis

(P3).

Cost is the amount which is spent by the company in the manufacturing if any product and this

involves various components such as material, labor, and overheads. There are various types of

costs such as direct which are directly related to production and then the indirect which are not in

direct relation. The classification can also be made as a variable which is fluctuating and fixed

costs.

2.2 Define the following terms and discuss their concept (P3):

Cost-volume-profit: This is the analysis in which the relation which is present among these three

components will be discussed. Is the cost will be less than the profit will be more (Kim, 2015).

The volume will also be affecting profit and cost.

Flexible budgeting: This is the budget in which standard in the set of some quantity and then

budget for other units can be made by modifying it. For this, all the amounts will be taken in

proportion.

Cost variances: This shows the differences which exist in the amount of cost which has been

budgeted and the actuals which are spent in the current period. For this variance analysis is taken

into use.

Absorption and Marginal costing: They are the costing methods used in which marginal is the

one in which all the variable components of cost are included and fixed cost is not apportioned

but in case of absorption this is not the case (Aurora, 2013). In that, all the fixed expenses are

also allocated.

Normal and standard costing: In normal costing all the actual amounts are taken into use for the

calculation of cost whereas in standard costing the targeted cost is taken into consideration.

9

2.1 What is meant by cost? Briefly explain the different types of costs and cost analysis

(P3).

Cost is the amount which is spent by the company in the manufacturing if any product and this

involves various components such as material, labor, and overheads. There are various types of

costs such as direct which are directly related to production and then the indirect which are not in

direct relation. The classification can also be made as a variable which is fluctuating and fixed

costs.

2.2 Define the following terms and discuss their concept (P3):

Cost-volume-profit: This is the analysis in which the relation which is present among these three

components will be discussed. Is the cost will be less than the profit will be more (Kim, 2015).

The volume will also be affecting profit and cost.

Flexible budgeting: This is the budget in which standard in the set of some quantity and then

budget for other units can be made by modifying it. For this, all the amounts will be taken in

proportion.

Cost variances: This shows the differences which exist in the amount of cost which has been

budgeted and the actuals which are spent in the current period. For this variance analysis is taken

into use.

Absorption and Marginal costing: They are the costing methods used in which marginal is the

one in which all the variable components of cost are included and fixed cost is not apportioned

but in case of absorption this is not the case (Aurora, 2013). In that, all the fixed expenses are

also allocated.

Normal and standard costing: In normal costing all the actual amounts are taken into use for the

calculation of cost whereas in standard costing the targeted cost is taken into consideration.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Activity-based costing: This is the method in which cost will be identified by considering the

activities which are performed and for that cost pools are made and the driver is determined in

respect of each of them.

Overhead costs: All the expenses which are incurred in the production of the product are

included in this other than that of the direct cost such as material and labor.

Fixed and variable cost: fixed cost is the one which does not change with the change in units but

the variable cost changes with the fluctuation in volume.

Cost allocation: The manner in which cost will be distributed among all the units and

departments will be included in this process. By this, the issues in this respect will be avoided.

Role of costing in setting price: In the setting, if the price the cost will be required as this is an

important component and profit will be added on this only.

Inventory costs and its different types: The amount which is spent on handling of the material is

covered in this and this includes ordering, holding and shortage cost.

Reduction of inventory costs and its benefits for an organization: For this proper control will be

required and by this, there will be an increase in the overall profits of the business (Vasile and

Croiteru, 2013).

Valuation methods: there are various methods by which valuation can be made such as FIFO,

LIFO, and weighted average. They help in determining the best value.

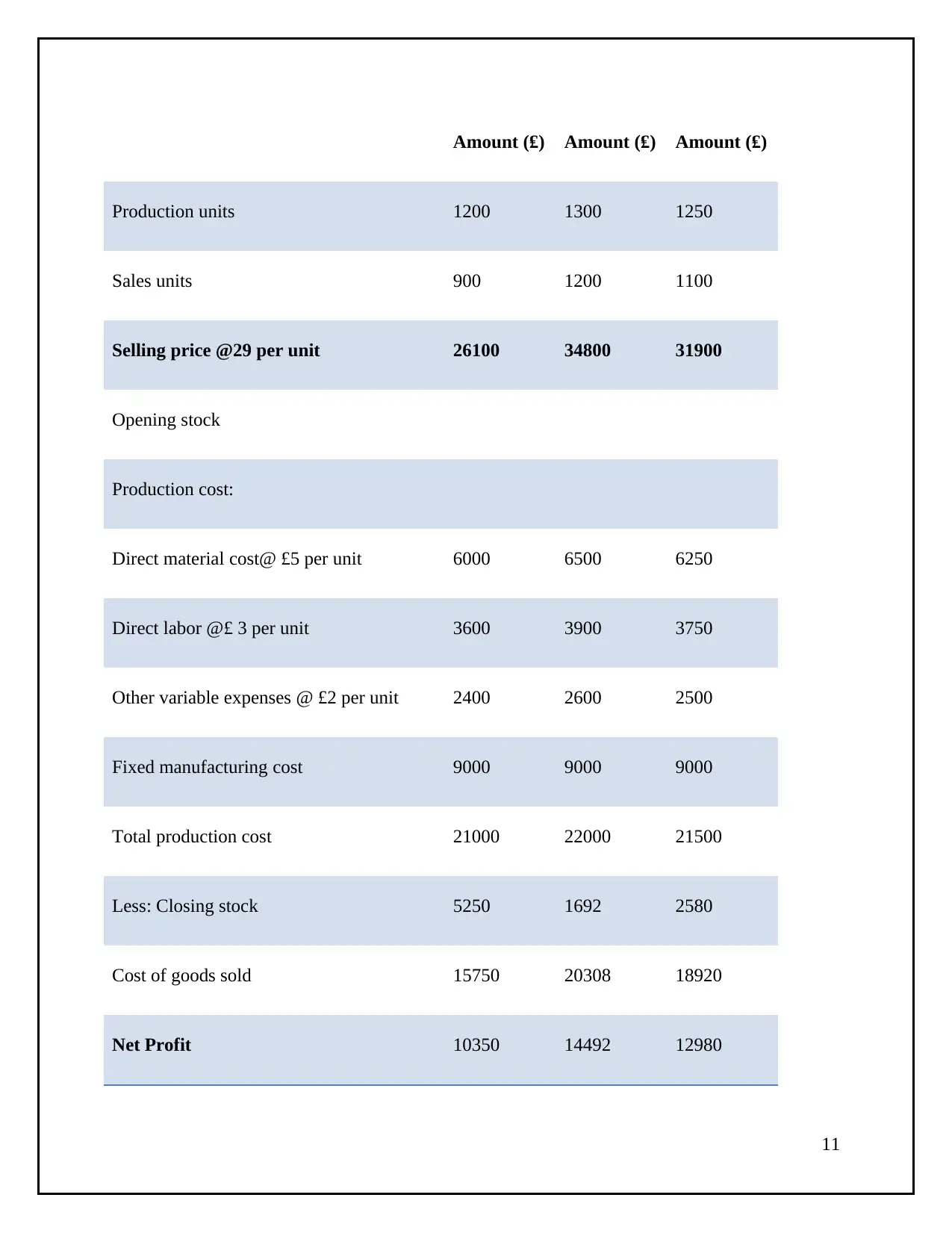

2.3 Calculate the costs using appropriate techniques of cost analysis to prepare an income

statement by apply Absorption costing and Marginal costing. (P3)

Income statement as per absorption costing

Particular Year 1 Year2 Year 3

10

activities which are performed and for that cost pools are made and the driver is determined in

respect of each of them.

Overhead costs: All the expenses which are incurred in the production of the product are

included in this other than that of the direct cost such as material and labor.

Fixed and variable cost: fixed cost is the one which does not change with the change in units but

the variable cost changes with the fluctuation in volume.

Cost allocation: The manner in which cost will be distributed among all the units and

departments will be included in this process. By this, the issues in this respect will be avoided.

Role of costing in setting price: In the setting, if the price the cost will be required as this is an

important component and profit will be added on this only.

Inventory costs and its different types: The amount which is spent on handling of the material is

covered in this and this includes ordering, holding and shortage cost.

Reduction of inventory costs and its benefits for an organization: For this proper control will be

required and by this, there will be an increase in the overall profits of the business (Vasile and

Croiteru, 2013).

Valuation methods: there are various methods by which valuation can be made such as FIFO,

LIFO, and weighted average. They help in determining the best value.

2.3 Calculate the costs using appropriate techniques of cost analysis to prepare an income

statement by apply Absorption costing and Marginal costing. (P3)

Income statement as per absorption costing

Particular Year 1 Year2 Year 3

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Amount (₤) Amount (₤) Amount (₤)

Production units 1200 1300 1250

Sales units 900 1200 1100

Selling price @29 per unit 26100 34800 31900

Opening stock

Production cost:

Direct material cost@ £5 per unit 6000 6500 6250

Direct labor @£ 3 per unit 3600 3900 3750

Other variable expenses @ £2 per unit 2400 2600 2500

Fixed manufacturing cost 9000 9000 9000

Total production cost 21000 22000 21500

Less: Closing stock 5250 1692 2580

Cost of goods sold 15750 20308 18920

Net Profit 10350 14492 12980

11

Production units 1200 1300 1250

Sales units 900 1200 1100

Selling price @29 per unit 26100 34800 31900

Opening stock

Production cost:

Direct material cost@ £5 per unit 6000 6500 6250

Direct labor @£ 3 per unit 3600 3900 3750

Other variable expenses @ £2 per unit 2400 2600 2500

Fixed manufacturing cost 9000 9000 9000

Total production cost 21000 22000 21500

Less: Closing stock 5250 1692 2580

Cost of goods sold 15750 20308 18920

Net Profit 10350 14492 12980

11

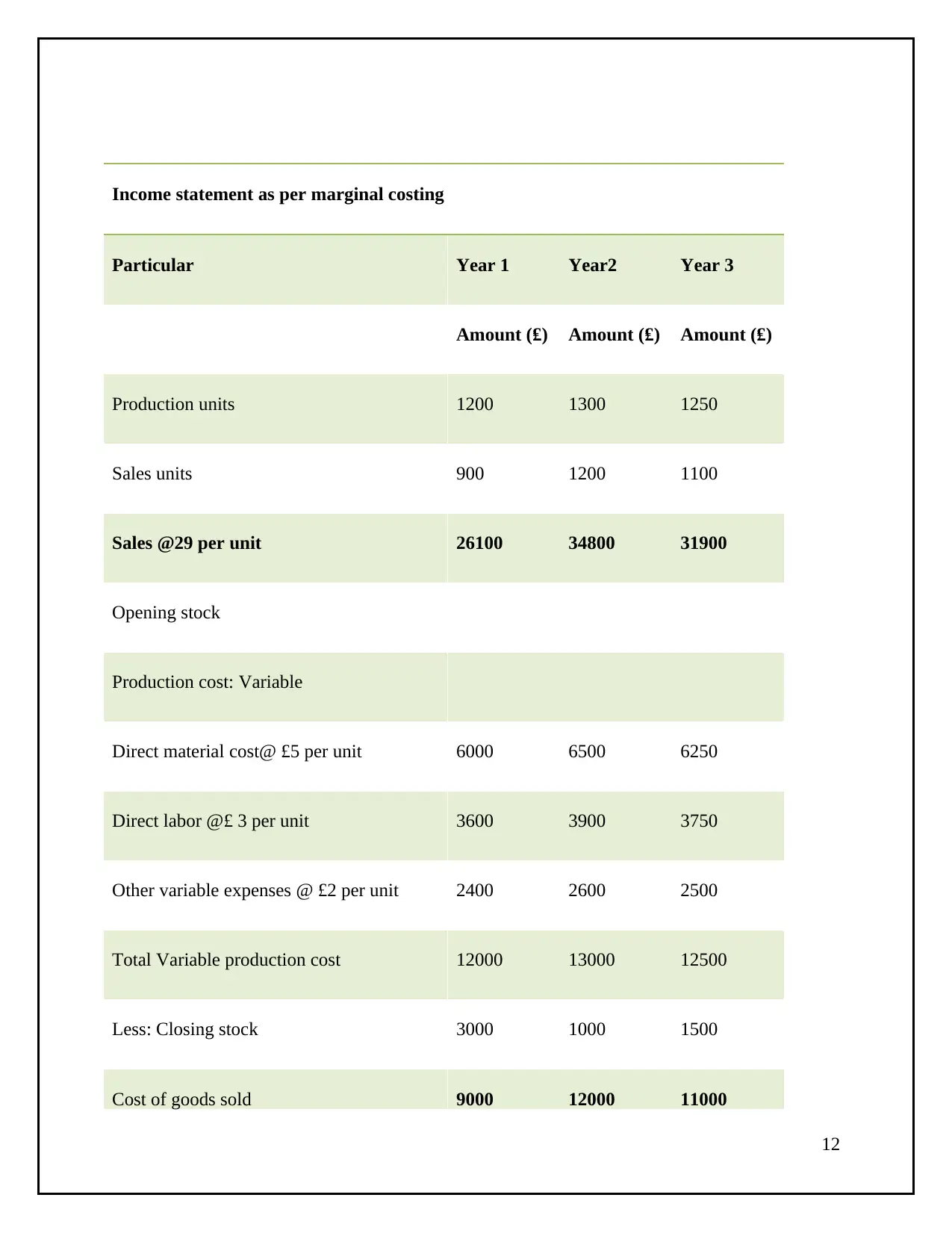

Income statement as per marginal costing

Particular Year 1 Year2 Year 3

Amount (₤) Amount (₤) Amount (₤)

Production units 1200 1300 1250

Sales units 900 1200 1100

Sales @29 per unit 26100 34800 31900

Opening stock

Production cost: Variable

Direct material cost@ £5 per unit 6000 6500 6250

Direct labor @£ 3 per unit 3600 3900 3750

Other variable expenses @ £2 per unit 2400 2600 2500

Total Variable production cost 12000 13000 12500

Less: Closing stock 3000 1000 1500

Cost of goods sold 9000 12000 11000

12

Particular Year 1 Year2 Year 3

Amount (₤) Amount (₤) Amount (₤)

Production units 1200 1300 1250

Sales units 900 1200 1100

Sales @29 per unit 26100 34800 31900

Opening stock

Production cost: Variable

Direct material cost@ £5 per unit 6000 6500 6250

Direct labor @£ 3 per unit 3600 3900 3750

Other variable expenses @ £2 per unit 2400 2600 2500

Total Variable production cost 12000 13000 12500

Less: Closing stock 3000 1000 1500

Cost of goods sold 9000 12000 11000

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.