University Audit Report: DIPL Financial Analysis and Procedures

VerifiedAdded on 2020/02/24

|7

|905

|180

Report

AI Summary

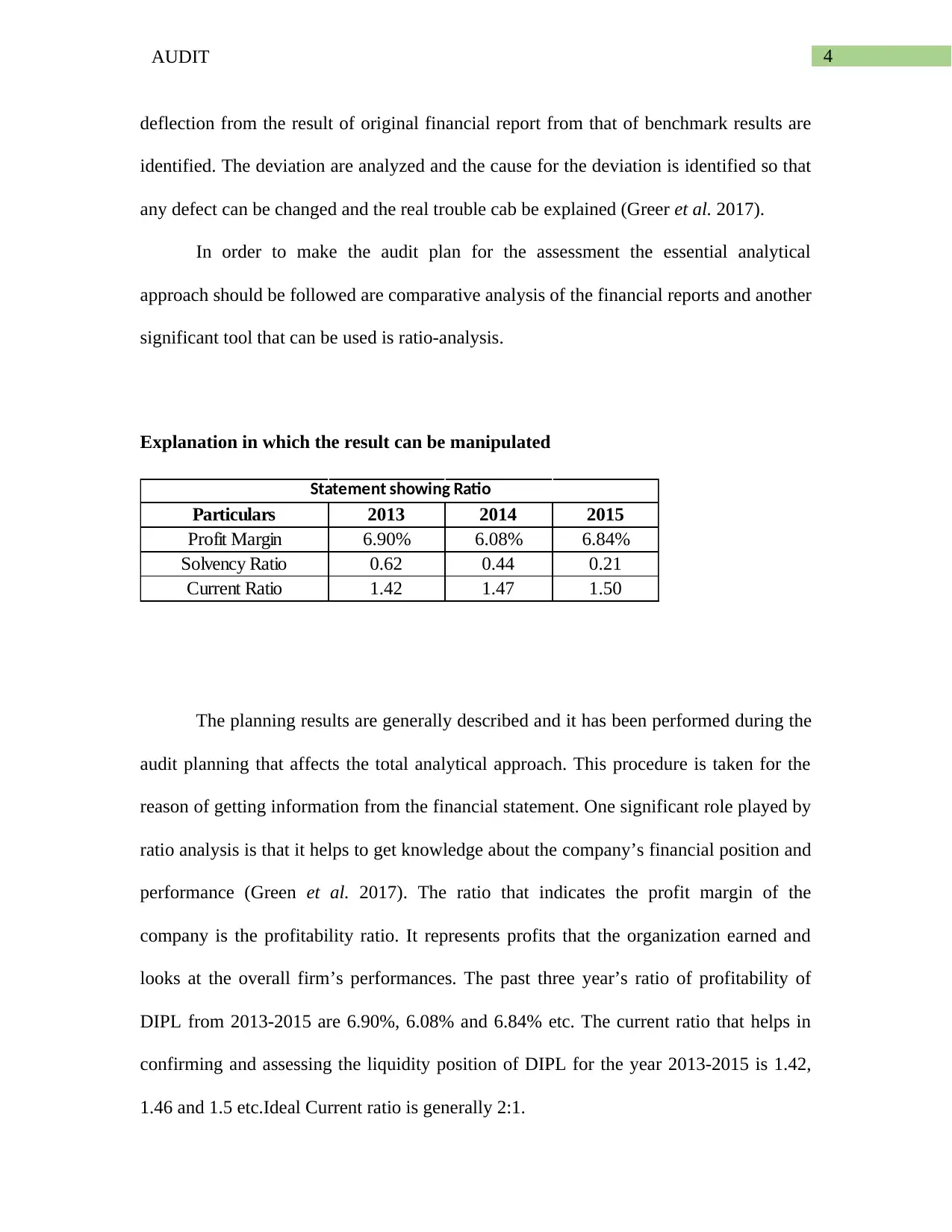

This audit report examines the financial statements of DIPL, focusing on the application of analytical procedures. The report outlines the importance of audit plans and the assessor's role in maintaining reasonable costs and minimizing misunderstandings. It details the analytical process, including the use of financial reports, common sizing, and benchmarking. The report also explains how results can be manipulated and provides an analysis of DIPL's financial ratios, including profitability, current, and solvency ratios from 2013 to 2015. The assessor's role in understanding the company's relative position and potential risks is highlighted. The report references relevant academic sources to support its analysis.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.