Detailed Analysis and Comparison of Investment Projects Report

VerifiedAdded on 2020/03/28

|13

|3013

|38

Project

AI Summary

This project report provides a comprehensive analysis of two investment proposals presented by Mark and Paul. The first proposal involves investing in a restaurant, with detailed sales, labor, and cash budgets developed to assess its financial performance. The report utilizes budgeting techniques to project revenue, expenses, and cash flow over a four-month period, highlighting the potential for high returns but also acknowledging practical challenges in managing high revenue. The second proposal focuses on investing in new machinery, evaluated using capital budgeting techniques such as Net Present Value (NPV), Payback Period, and Average Rate of Return (ARR). A comparative analysis is conducted to determine the superior investment opportunity, concluding that the restaurant investment offers higher profitability despite its complexities. The report emphasizes the importance of financial analysis in making informed investment decisions.

Running Head: business report 1

Project Report: Business Report

Project Report: Business Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business report 2

Executive summary

This report has been prepared to analyze 2 investment projects. In this report, both the

investment techniques have been analyzed according to the different methods. This report

briefs the user about the different techniques which could be used to analyze an investment

proposal. In this report, purpose of the report, scope of the report, limitations etc have been

given firstly. Further, scope and nature of investments have been analyzed. In addition,

investment opportunity of both the investment proposal has been studied. Lastly, the

comparison has been done between both the projects and recommendation has been given

accordingly.

Executive summary

This report has been prepared to analyze 2 investment projects. In this report, both the

investment techniques have been analyzed according to the different methods. This report

briefs the user about the different techniques which could be used to analyze an investment

proposal. In this report, purpose of the report, scope of the report, limitations etc have been

given firstly. Further, scope and nature of investments have been analyzed. In addition,

investment opportunity of both the investment proposal has been studied. Lastly, the

comparison has been done between both the projects and recommendation has been given

accordingly.

Business report 3

Contents

Introduction.......................................................................................................................4

Nature and scope of investment........................................................................................4

First Investment opportunity.............................................................................................4

Sales budget..................................................................................................................6

Labor budget.................................................................................................................6

Cash budget..................................................................................................................6

Overview and analysis of budgets................................................................................7

Practical issues of investment.......................................................................................7

Second Investment opportunity........................................................................................7

Comparison.......................................................................................................................8

Conclusion:.......................................................................................................................8

References.........................................................................................................................9

Appendix.........................................................................................................................10

Contents

Introduction.......................................................................................................................4

Nature and scope of investment........................................................................................4

First Investment opportunity.............................................................................................4

Sales budget..................................................................................................................6

Labor budget.................................................................................................................6

Cash budget..................................................................................................................6

Overview and analysis of budgets................................................................................7

Practical issues of investment.......................................................................................7

Second Investment opportunity........................................................................................7

Comparison.......................................................................................................................8

Conclusion:.......................................................................................................................8

References.........................................................................................................................9

Appendix.........................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business report 4

Introduction:

The given case study depict that two investment proposals have been offered by the

Mark and Paul in front of the investor to invest into the proposals and enhance the worth of

invested amount. In this paper, various methods and tools have been taken into consideration

to analyze the best investment proposal of the company. Capital budgeting techniques have

been used in this report to analyze the first investment proposal and budgeting techniques

have been used in this report to analyze the second investment proposal offered by the Mark

and Paul. According to this report, the main motto of this paper is to analyze the best

investment proposal which would provide the investors more return and the proposal of the

investment would be attractive for the investors (Bierman, 2010). Additionally, the scope and

limitation of both the investment has been analyzed and it has been found that the scope of

the proposal is high return and opportunities in the market whereas the limitations are

managing the investment amount.

Nature and scope of investment:

Investments are crucial for every person to manage the invested amount and the return

from that investment. Basically, individual saves the amount and invest it into the various

business opportunities or in the market to enhance the worth of their money. In financial

terms, individual buys the financial products and various other similar products to enhance

the worth of their amount and enhance the return from those products. Basically the nature of

investments is dynamic and viable and offers various scopes to the investors (Lafond and

Roychowdhury, 2008). Both the given investment proposals are also dynamic in nature as the

return is not similar in all the four months and offers various opportunities to the investors to

enhance the worth and gain more return from the market.

First Investment opportunity:

First opportunities offered by the Mark and Paul depict that the investment could be

done in restaurant. This investment would offer them various opportunities. For this option,

investors are required to spend some money in buying the noncurrent assets which would be

required to run the restaurant. This business proposal offers the different revenue and

expenses style to the company. Following are the overview of the investment proposal which

could be evaluated through budgeting technique to reach over a conclusion:

Restaurant Purchase and Expenses

Introduction:

The given case study depict that two investment proposals have been offered by the

Mark and Paul in front of the investor to invest into the proposals and enhance the worth of

invested amount. In this paper, various methods and tools have been taken into consideration

to analyze the best investment proposal of the company. Capital budgeting techniques have

been used in this report to analyze the first investment proposal and budgeting techniques

have been used in this report to analyze the second investment proposal offered by the Mark

and Paul. According to this report, the main motto of this paper is to analyze the best

investment proposal which would provide the investors more return and the proposal of the

investment would be attractive for the investors (Bierman, 2010). Additionally, the scope and

limitation of both the investment has been analyzed and it has been found that the scope of

the proposal is high return and opportunities in the market whereas the limitations are

managing the investment amount.

Nature and scope of investment:

Investments are crucial for every person to manage the invested amount and the return

from that investment. Basically, individual saves the amount and invest it into the various

business opportunities or in the market to enhance the worth of their money. In financial

terms, individual buys the financial products and various other similar products to enhance

the worth of their amount and enhance the return from those products. Basically the nature of

investments is dynamic and viable and offers various scopes to the investors (Lafond and

Roychowdhury, 2008). Both the given investment proposals are also dynamic in nature as the

return is not similar in all the four months and offers various opportunities to the investors to

enhance the worth and gain more return from the market.

First Investment opportunity:

First opportunities offered by the Mark and Paul depict that the investment could be

done in restaurant. This investment would offer them various opportunities. For this option,

investors are required to spend some money in buying the noncurrent assets which would be

required to run the restaurant. This business proposal offers the different revenue and

expenses style to the company. Following are the overview of the investment proposal which

could be evaluated through budgeting technique to reach over a conclusion:

Restaurant Purchase and Expenses

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business report 5

Machinery/ equipment $ 1,10,000

Furniture (tables and chairs) $ 30,000

Vehicle (Deliveries) $ 43,000

Utensils (cups, plates) $ 18,000

Produce (for 1 week) $ 10,000

Drinks (For 1 month) $ 20,000

Jun-01 Bank $ 80,000

Purchase of $10,000 for a week from June 1 and the amount of purchase

would be given to suppliers from 1 august.

Purchase of $ 20,000 for 1 month from July-1 and the amount

of purchase would be given to suppliers periodically which is as

follows:

10% in current month

45% in second month

45% in third month

Labour

Number of casual labour 3

Working in a day (hours) 6 hours

In a week (days) 6 days

Rate

$ 23 per

hour

Drawings

$ 10000 each per

month

Overhead $ 5,000

Sales

20000 meals in first month

18000 meals in second month

18000 meals in third month

22000 in forth month

Average selling price $ 45

Drink sales would be triples the amount of

meals per month.

Drink Price $ 6

Machinery/ equipment $ 1,10,000

Furniture (tables and chairs) $ 30,000

Vehicle (Deliveries) $ 43,000

Utensils (cups, plates) $ 18,000

Produce (for 1 week) $ 10,000

Drinks (For 1 month) $ 20,000

Jun-01 Bank $ 80,000

Purchase of $10,000 for a week from June 1 and the amount of purchase

would be given to suppliers from 1 august.

Purchase of $ 20,000 for 1 month from July-1 and the amount

of purchase would be given to suppliers periodically which is as

follows:

10% in current month

45% in second month

45% in third month

Labour

Number of casual labour 3

Working in a day (hours) 6 hours

In a week (days) 6 days

Rate

$ 23 per

hour

Drawings

$ 10000 each per

month

Overhead $ 5,000

Sales

20000 meals in first month

18000 meals in second month

18000 meals in third month

22000 in forth month

Average selling price $ 45

Drink sales would be triples the amount of

meals per month.

Drink Price $ 6

Business report 6

The above details have been used to make the budgeting reports of the proposals

(Radebaugh, Gray and Black, 2006).

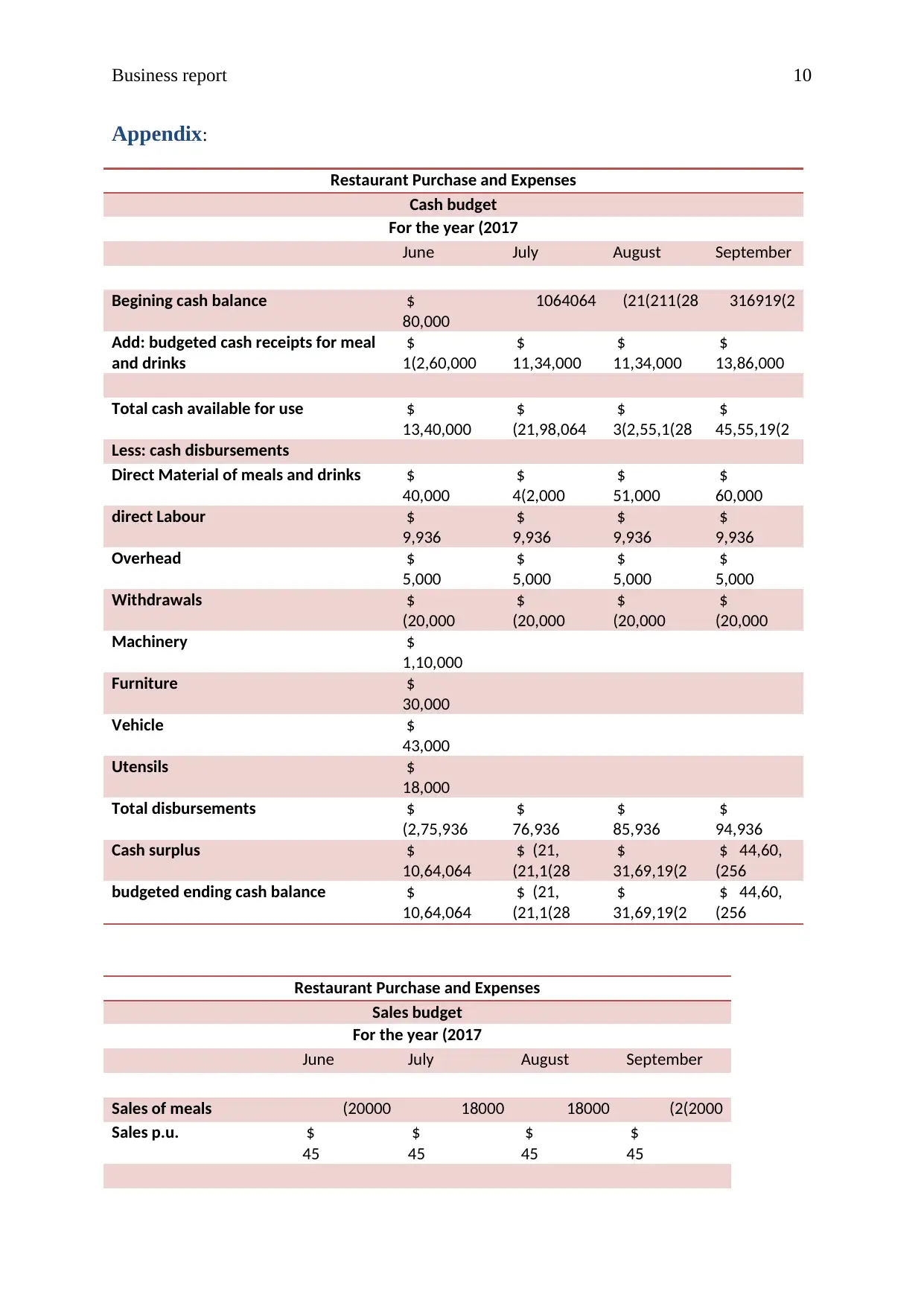

Sales budget:

This budget report depicts the user about various predictions in concern of future

about the products sales and services sales of business. Mainly, sales budgets are prepared by

the firms to recognize the sum of selling unit and revenue of the business opportunity. So that

strategy and policy of the business could be made accordingly.

This case study depict about the total sales of the business which could be 20000,

18000, 18000 and 22000 units in Jun, July, Aug and Sept correspondingly of products

(meals) and the drinks of the business units would be 60000, 54000, 54000 and 66000 units

in Jun, July, Aug and Sept correspondingly. Thus restaurant’s total sales would be

$12,60,000, $11,34,000, $11,34,000 and $13,86,000.

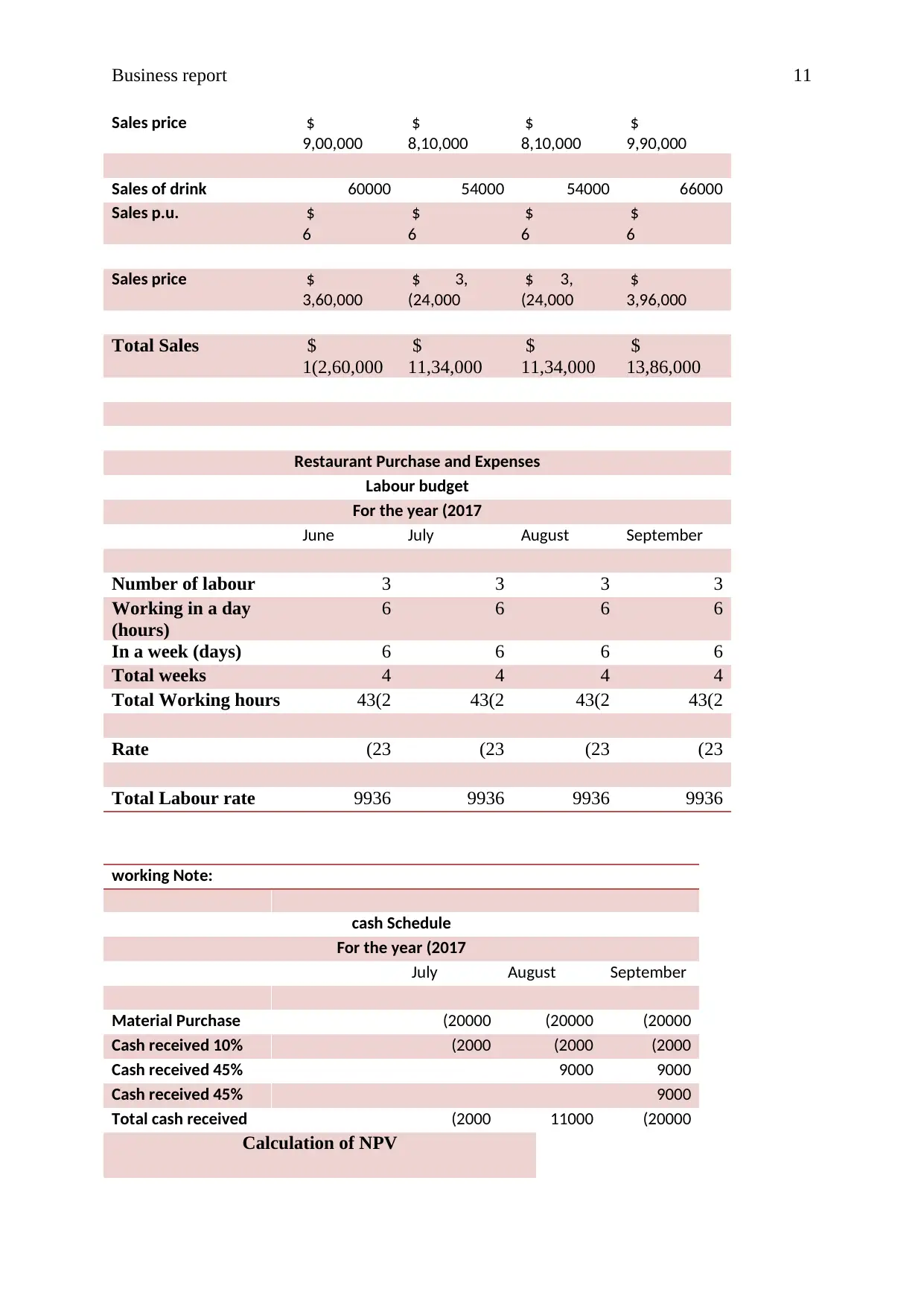

Labor budget:

This budget report depicts the user about various predictions in concern of future

about the labour hour and labour cost of business. Mainly, labour budgets are prepared by the

firms to recognize the sum of total hours and cost of the business in terms of labour. So that

strategy and policy of the business could be made accordingly (Needles, Powers and Crosson,

2013).

This case study depict that the total labour unit which would be required in the

business are 432, 432, 432 and 432 in Jun, July, Aug and Sept. The labour per hour rate is

$23. So the company’s total labour cost will be $9936, $9936, $9936 and $9936 in Jun,

July, Aug and Sept respectively.

Cash budget:

This budget report depicts the user about various predictions in concern of future

about the cash inflow and outflow of business. Mainly, cash budgets are prepared by the

firms to recognize the sum of total cash flow of the business. So that strategy and policy of

the business could be made accordingly.

The above details have been used to make the budgeting reports of the proposals

(Radebaugh, Gray and Black, 2006).

Sales budget:

This budget report depicts the user about various predictions in concern of future

about the products sales and services sales of business. Mainly, sales budgets are prepared by

the firms to recognize the sum of selling unit and revenue of the business opportunity. So that

strategy and policy of the business could be made accordingly.

This case study depict about the total sales of the business which could be 20000,

18000, 18000 and 22000 units in Jun, July, Aug and Sept correspondingly of products

(meals) and the drinks of the business units would be 60000, 54000, 54000 and 66000 units

in Jun, July, Aug and Sept correspondingly. Thus restaurant’s total sales would be

$12,60,000, $11,34,000, $11,34,000 and $13,86,000.

Labor budget:

This budget report depicts the user about various predictions in concern of future

about the labour hour and labour cost of business. Mainly, labour budgets are prepared by the

firms to recognize the sum of total hours and cost of the business in terms of labour. So that

strategy and policy of the business could be made accordingly (Needles, Powers and Crosson,

2013).

This case study depict that the total labour unit which would be required in the

business are 432, 432, 432 and 432 in Jun, July, Aug and Sept. The labour per hour rate is

$23. So the company’s total labour cost will be $9936, $9936, $9936 and $9936 in Jun,

July, Aug and Sept respectively.

Cash budget:

This budget report depicts the user about various predictions in concern of future

about the cash inflow and outflow of business. Mainly, cash budgets are prepared by the

firms to recognize the sum of total cash flow of the business. So that strategy and policy of

the business could be made accordingly.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business report 7

this case study depict that the total cash inflow of this business opportunity could be

$13,40,000, $21,98,064, 32,55,128 and $45,55,192 in Jun, July, Aug and Sept respectively.

Same time, cash outflow of business opportunity will be $2,75,936, $76,936, $85,936 and

$94,936 in Jun, July, Aug and Sept. so the total cash flow of business opportunity will be

$10,64,064, $21,21,128, $31,69,192 and $44,60,256 in Jun, July, Aug and Sept

correspondingly (Van der Stede, 2001).

Overview and analysis of budgets:

The above budgeting estimations and calculations depict that the investment

opportunity offered by Mark and Paul of restaurant would offer high returns to the investors.

The budget reports depict that the revenue, cash inflow etc of the company are quite higher

than the expenses of the company. The budgeting of the company depict that the revenues are

viable and the company is required to manage the expenses and revenue in current manner so

that high profits could be made by the company. Further, all the budgets are connected to

each other (Garrison et al, 2010). These budgets express the great performance of the

restaurant investment proposal.

Practical issues of investment:

Through it has been found that the investment proposal is quite great in terms of profit

but it has been found, that it is not easy for a restaurant to manage the expenses with this

much high revenue. It has also been found that huge requirement of money is required by the

company to invest into the restaurant.

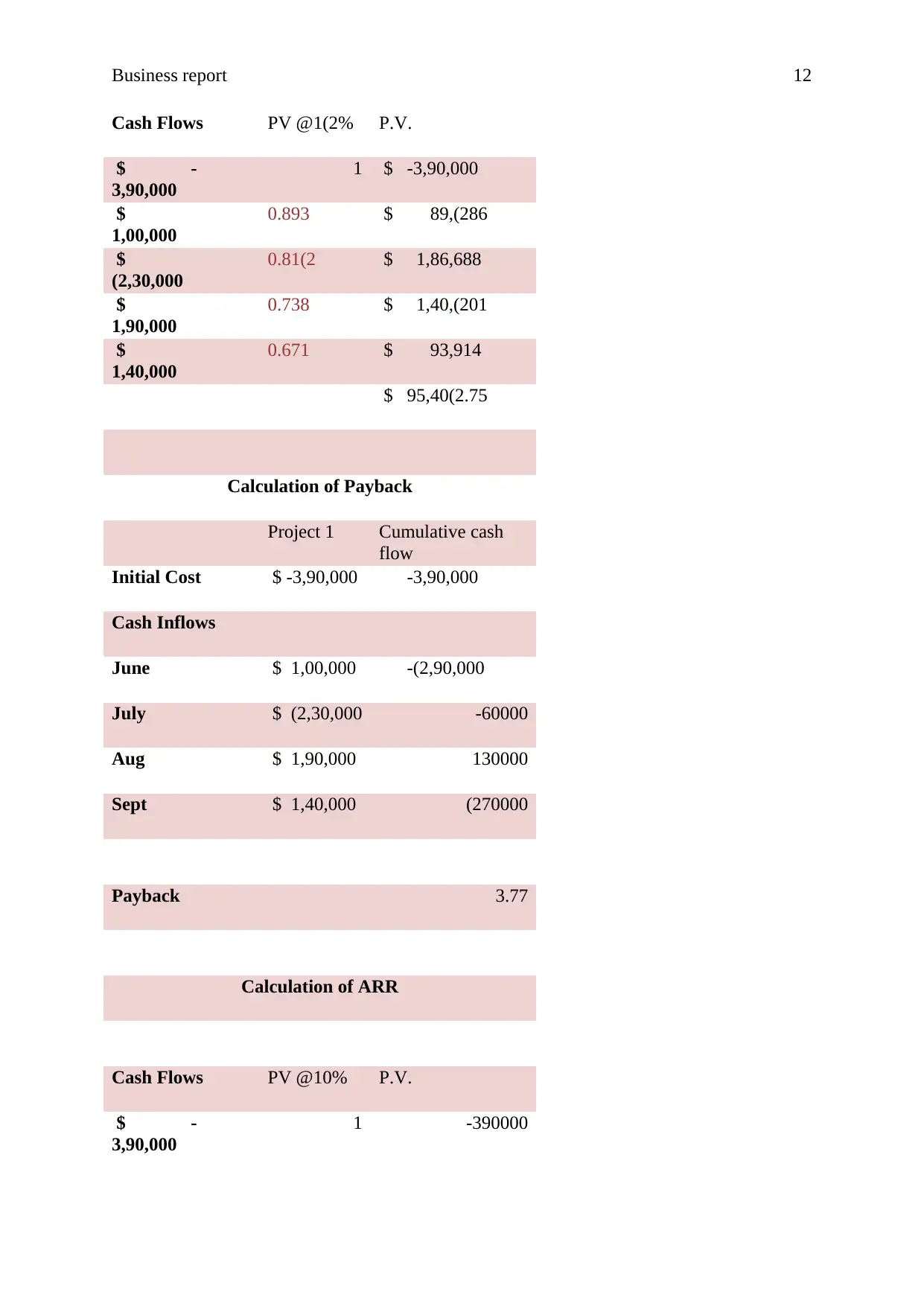

Second Investment opportunity:

Second opportunities offered by the Mark and Paul depict that the investment could

be done in new machineries. This investment would offer them various opportunities. For this

option, investors are required to spend some money in buying the financial assets which

would be required to enhance the worth of invested amount. This business proposal offers the

different revenue in each month. Following are the overview of the investment proposal

which could be evaluated through capital budgeting technique to reach over a conclusion:

Initial Cost

$ -

3,90,000

Cash Inflows

June $

this case study depict that the total cash inflow of this business opportunity could be

$13,40,000, $21,98,064, 32,55,128 and $45,55,192 in Jun, July, Aug and Sept respectively.

Same time, cash outflow of business opportunity will be $2,75,936, $76,936, $85,936 and

$94,936 in Jun, July, Aug and Sept. so the total cash flow of business opportunity will be

$10,64,064, $21,21,128, $31,69,192 and $44,60,256 in Jun, July, Aug and Sept

correspondingly (Van der Stede, 2001).

Overview and analysis of budgets:

The above budgeting estimations and calculations depict that the investment

opportunity offered by Mark and Paul of restaurant would offer high returns to the investors.

The budget reports depict that the revenue, cash inflow etc of the company are quite higher

than the expenses of the company. The budgeting of the company depict that the revenues are

viable and the company is required to manage the expenses and revenue in current manner so

that high profits could be made by the company. Further, all the budgets are connected to

each other (Garrison et al, 2010). These budgets express the great performance of the

restaurant investment proposal.

Practical issues of investment:

Through it has been found that the investment proposal is quite great in terms of profit

but it has been found, that it is not easy for a restaurant to manage the expenses with this

much high revenue. It has also been found that huge requirement of money is required by the

company to invest into the restaurant.

Second Investment opportunity:

Second opportunities offered by the Mark and Paul depict that the investment could

be done in new machineries. This investment would offer them various opportunities. For this

option, investors are required to spend some money in buying the financial assets which

would be required to enhance the worth of invested amount. This business proposal offers the

different revenue in each month. Following are the overview of the investment proposal

which could be evaluated through capital budgeting technique to reach over a conclusion:

Initial Cost

$ -

3,90,000

Cash Inflows

June $

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business report 8

1,00,000

July

$

2,30,000

Aug

$

1,90,000

Sept

$

1,40,000

This case study depict that the capital budgeting techniques have been investigated

over the above cash outflow and inflow. Net present value, Payback period and ARR

techniques have been calculated (Brewer, Garrison and Noreen, 2005). All the three

techniques depict about the different result which are total return of $ 95,402.72 according to

NPV technique in 4 months, entire amount could be get back according to the payback period

technique in 3.77 years by the company and the average return % of this investment proposal

is 30.79% according to ARR technique. Thus it has been found that this investment would

offer positive return to the customers.

Comparison:

Both investment opportunities offered by Mark and Paul has been analyzed to reach

over a conclusion that which one is the best one to invest and enhance the worth of the

amount. Through the calculations, it has been found that the investment in first proposal

would be more profitable for the company as the profits are higher into that proposal through

various issues are linked with it whereas the profits are lower into the second proposals and

offer less return to the customers.

Conclusion:

Finally, through this study, it could be said that the both the opportunities are better

but the first opportunity is best one as it offers huge return to the investors. Through the

calculations, it has been found that the investment in first proposal would be more profitable

for the company as the profits are higher into that proposal through various issues are linked

with it whereas the profits are lower into the second proposals and offer less return to the

customers.

1,00,000

July

$

2,30,000

Aug

$

1,90,000

Sept

$

1,40,000

This case study depict that the capital budgeting techniques have been investigated

over the above cash outflow and inflow. Net present value, Payback period and ARR

techniques have been calculated (Brewer, Garrison and Noreen, 2005). All the three

techniques depict about the different result which are total return of $ 95,402.72 according to

NPV technique in 4 months, entire amount could be get back according to the payback period

technique in 3.77 years by the company and the average return % of this investment proposal

is 30.79% according to ARR technique. Thus it has been found that this investment would

offer positive return to the customers.

Comparison:

Both investment opportunities offered by Mark and Paul has been analyzed to reach

over a conclusion that which one is the best one to invest and enhance the worth of the

amount. Through the calculations, it has been found that the investment in first proposal

would be more profitable for the company as the profits are higher into that proposal through

various issues are linked with it whereas the profits are lower into the second proposals and

offer less return to the customers.

Conclusion:

Finally, through this study, it could be said that the both the opportunities are better

but the first opportunity is best one as it offers huge return to the investors. Through the

calculations, it has been found that the investment in first proposal would be more profitable

for the company as the profits are higher into that proposal through various issues are linked

with it whereas the profits are lower into the second proposals and offer less return to the

customers.

Business report 9

References:

Bierman, H., (2010). An introduction to accounting and managerial finance: a merger of

equals. World Scientific.

Brewer, P.C., Garrison, R.H. and Noreen, E.W., (2005). Introduction to managerial

accounting. McGraw-Hill Irwin.

Lafond, R. and Roychowdhury, S., (2008). Managerial ownership and accounting

conservatism. Journal of accounting research, 46(1), pp.101-135.

Needles, B., Powers, M. and Crosson, S., (2013). Financial and managerial accounting.

Nelson Education.

Garrison, R.H., Noreen, E.W., Brewer, P.C. and McGowan, A., (2010). Managerial

accounting. Issues in Accounting Education, (25(4), pp.79(2-793.

Radebaugh, L.H., Gray, S.J. and Black, E.L., (2006). International accounting and

multinational enterprises. New York, NY: John Wiley & Sons.

Van der Stede, W.A., (2001). Measuring ‘tight budgetary control’. Management Accounting

Research, 1(2(1), pp.119-137.

References:

Bierman, H., (2010). An introduction to accounting and managerial finance: a merger of

equals. World Scientific.

Brewer, P.C., Garrison, R.H. and Noreen, E.W., (2005). Introduction to managerial

accounting. McGraw-Hill Irwin.

Lafond, R. and Roychowdhury, S., (2008). Managerial ownership and accounting

conservatism. Journal of accounting research, 46(1), pp.101-135.

Needles, B., Powers, M. and Crosson, S., (2013). Financial and managerial accounting.

Nelson Education.

Garrison, R.H., Noreen, E.W., Brewer, P.C. and McGowan, A., (2010). Managerial

accounting. Issues in Accounting Education, (25(4), pp.79(2-793.

Radebaugh, L.H., Gray, S.J. and Black, E.L., (2006). International accounting and

multinational enterprises. New York, NY: John Wiley & Sons.

Van der Stede, W.A., (2001). Measuring ‘tight budgetary control’. Management Accounting

Research, 1(2(1), pp.119-137.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Business report 10

Appendix:

Restaurant Purchase and Expenses

Cash budget

For the year (2017

June July August September

Begining cash balance $

80,000

1064064 (21(211(28 316919(2

Add: budgeted cash receipts for meal

and drinks

$

1(2,60,000

$

11,34,000

$

11,34,000

$

13,86,000

Total cash available for use $

13,40,000

$

(21,98,064

$

3(2,55,1(28

$

45,55,19(2

Less: cash disbursements

Direct Material of meals and drinks $

40,000

$

4(2,000

$

51,000

$

60,000

direct Labour $

9,936

$

9,936

$

9,936

$

9,936

Overhead $

5,000

$

5,000

$

5,000

$

5,000

Withdrawals $

(20,000

$

(20,000

$

(20,000

$

(20,000

Machinery $

1,10,000

Furniture $

30,000

Vehicle $

43,000

Utensils $

18,000

Total disbursements $

(2,75,936

$

76,936

$

85,936

$

94,936

Cash surplus $

10,64,064

$ (21,

(21,1(28

$

31,69,19(2

$ 44,60,

(256

budgeted ending cash balance $

10,64,064

$ (21,

(21,1(28

$

31,69,19(2

$ 44,60,

(256

Restaurant Purchase and Expenses

Sales budget

For the year (2017

June July August September

Sales of meals (20000 18000 18000 (2(2000

Sales p.u. $

45

$

45

$

45

$

45

Appendix:

Restaurant Purchase and Expenses

Cash budget

For the year (2017

June July August September

Begining cash balance $

80,000

1064064 (21(211(28 316919(2

Add: budgeted cash receipts for meal

and drinks

$

1(2,60,000

$

11,34,000

$

11,34,000

$

13,86,000

Total cash available for use $

13,40,000

$

(21,98,064

$

3(2,55,1(28

$

45,55,19(2

Less: cash disbursements

Direct Material of meals and drinks $

40,000

$

4(2,000

$

51,000

$

60,000

direct Labour $

9,936

$

9,936

$

9,936

$

9,936

Overhead $

5,000

$

5,000

$

5,000

$

5,000

Withdrawals $

(20,000

$

(20,000

$

(20,000

$

(20,000

Machinery $

1,10,000

Furniture $

30,000

Vehicle $

43,000

Utensils $

18,000

Total disbursements $

(2,75,936

$

76,936

$

85,936

$

94,936

Cash surplus $

10,64,064

$ (21,

(21,1(28

$

31,69,19(2

$ 44,60,

(256

budgeted ending cash balance $

10,64,064

$ (21,

(21,1(28

$

31,69,19(2

$ 44,60,

(256

Restaurant Purchase and Expenses

Sales budget

For the year (2017

June July August September

Sales of meals (20000 18000 18000 (2(2000

Sales p.u. $

45

$

45

$

45

$

45

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Business report 11

Sales price $

9,00,000

$

8,10,000

$

8,10,000

$

9,90,000

Sales of drink 60000 54000 54000 66000

Sales p.u. $

6

$

6

$

6

$

6

Sales price $

3,60,000

$ 3,

(24,000

$ 3,

(24,000

$

3,96,000

Total Sales $

1(2,60,000

$

11,34,000

$

11,34,000

$

13,86,000

Restaurant Purchase and Expenses

Labour budget

For the year (2017

June July August September

Number of labour 3 3 3 3

Working in a day

(hours)

6 6 6 6

In a week (days) 6 6 6 6

Total weeks 4 4 4 4

Total Working hours 43(2 43(2 43(2 43(2

Rate (23 (23 (23 (23

Total Labour rate 9936 9936 9936 9936

working Note:

cash Schedule

For the year (2017

July August September

Material Purchase (20000 (20000 (20000

Cash received 10% (2000 (2000 (2000

Cash received 45% 9000 9000

Cash received 45% 9000

Total cash received (2000 11000 (20000

Calculation of NPV

Sales price $

9,00,000

$

8,10,000

$

8,10,000

$

9,90,000

Sales of drink 60000 54000 54000 66000

Sales p.u. $

6

$

6

$

6

$

6

Sales price $

3,60,000

$ 3,

(24,000

$ 3,

(24,000

$

3,96,000

Total Sales $

1(2,60,000

$

11,34,000

$

11,34,000

$

13,86,000

Restaurant Purchase and Expenses

Labour budget

For the year (2017

June July August September

Number of labour 3 3 3 3

Working in a day

(hours)

6 6 6 6

In a week (days) 6 6 6 6

Total weeks 4 4 4 4

Total Working hours 43(2 43(2 43(2 43(2

Rate (23 (23 (23 (23

Total Labour rate 9936 9936 9936 9936

working Note:

cash Schedule

For the year (2017

July August September

Material Purchase (20000 (20000 (20000

Cash received 10% (2000 (2000 (2000

Cash received 45% 9000 9000

Cash received 45% 9000

Total cash received (2000 11000 (20000

Calculation of NPV

Business report 12

Cash Flows PV @1(2% P.V.

$ -

3,90,000

1 $ -3,90,000

$

1,00,000

0.893 $ 89,(286

$

(2,30,000

0.81(2 $ 1,86,688

$

1,90,000

0.738 $ 1,40,(201

$

1,40,000

0.671 $ 93,914

$ 95,40(2.75

Calculation of Payback

Project 1 Cumulative cash

flow

Initial Cost $ -3,90,000 -3,90,000

Cash Inflows

June $ 1,00,000 -(2,90,000

July $ (2,30,000 -60000

Aug $ 1,90,000 130000

Sept $ 1,40,000 (270000

Payback 3.77

Calculation of ARR

Cash Flows PV @10% P.V.

$ -

3,90,000

1 -390000

Cash Flows PV @1(2% P.V.

$ -

3,90,000

1 $ -3,90,000

$

1,00,000

0.893 $ 89,(286

$

(2,30,000

0.81(2 $ 1,86,688

$

1,90,000

0.738 $ 1,40,(201

$

1,40,000

0.671 $ 93,914

$ 95,40(2.75

Calculation of Payback

Project 1 Cumulative cash

flow

Initial Cost $ -3,90,000 -3,90,000

Cash Inflows

June $ 1,00,000 -(2,90,000

July $ (2,30,000 -60000

Aug $ 1,90,000 130000

Sept $ 1,40,000 (270000

Payback 3.77

Calculation of ARR

Cash Flows PV @10% P.V.

$ -

3,90,000

1 -390000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.