Finance Project: Portfolio Combinations and Regression Analysis

VerifiedAdded on 2022/12/28

|6

|1263

|75

Project

AI Summary

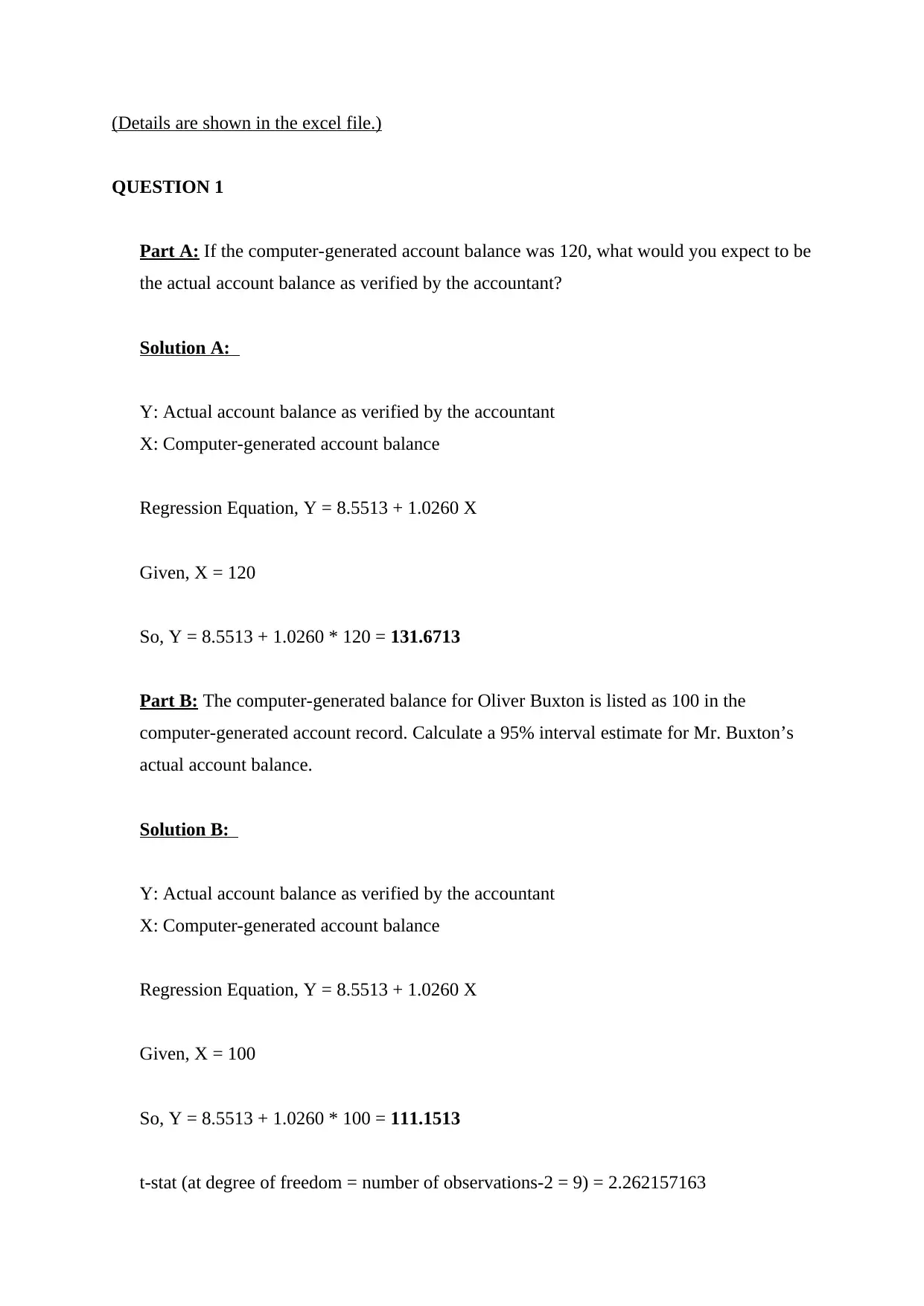

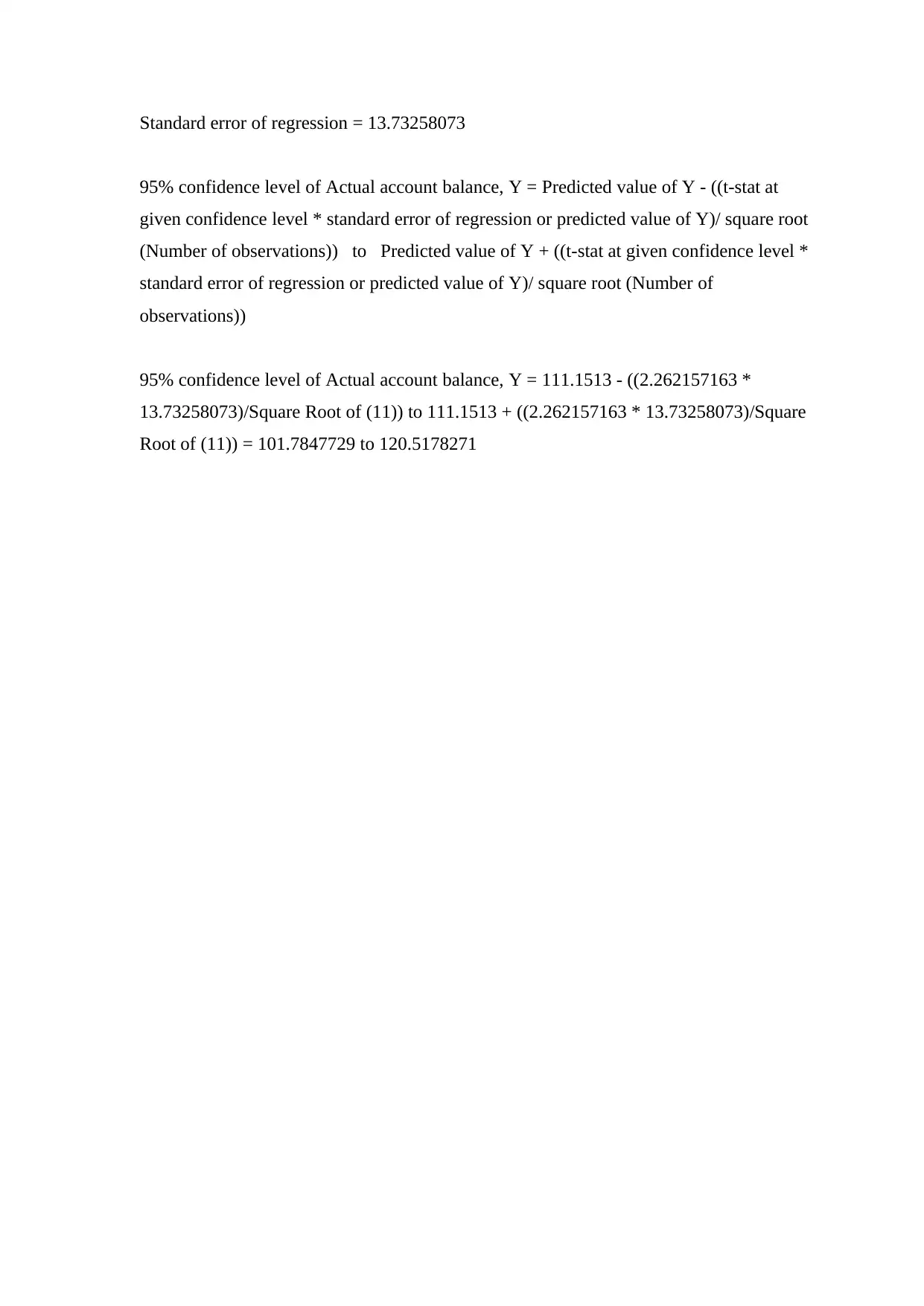

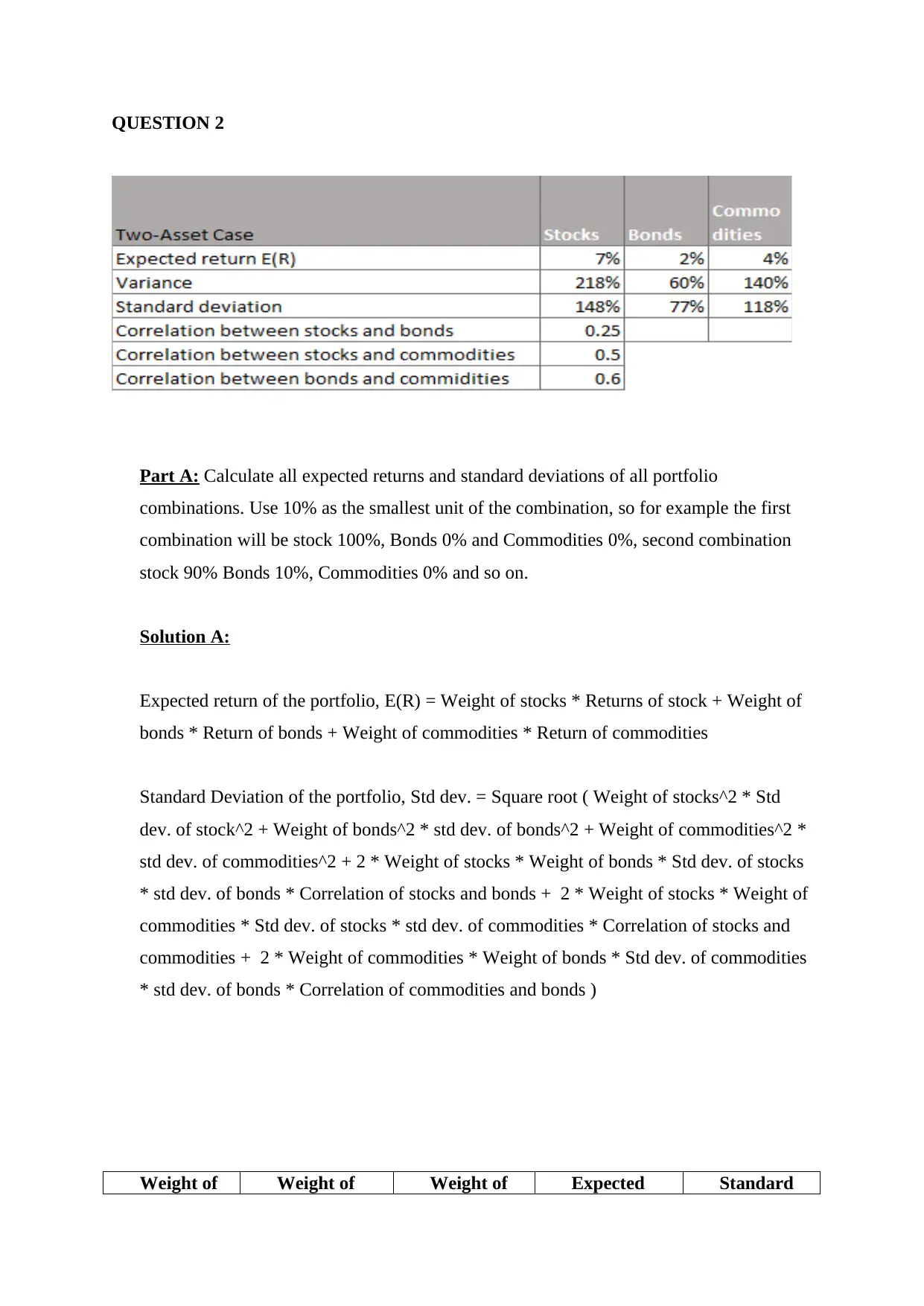

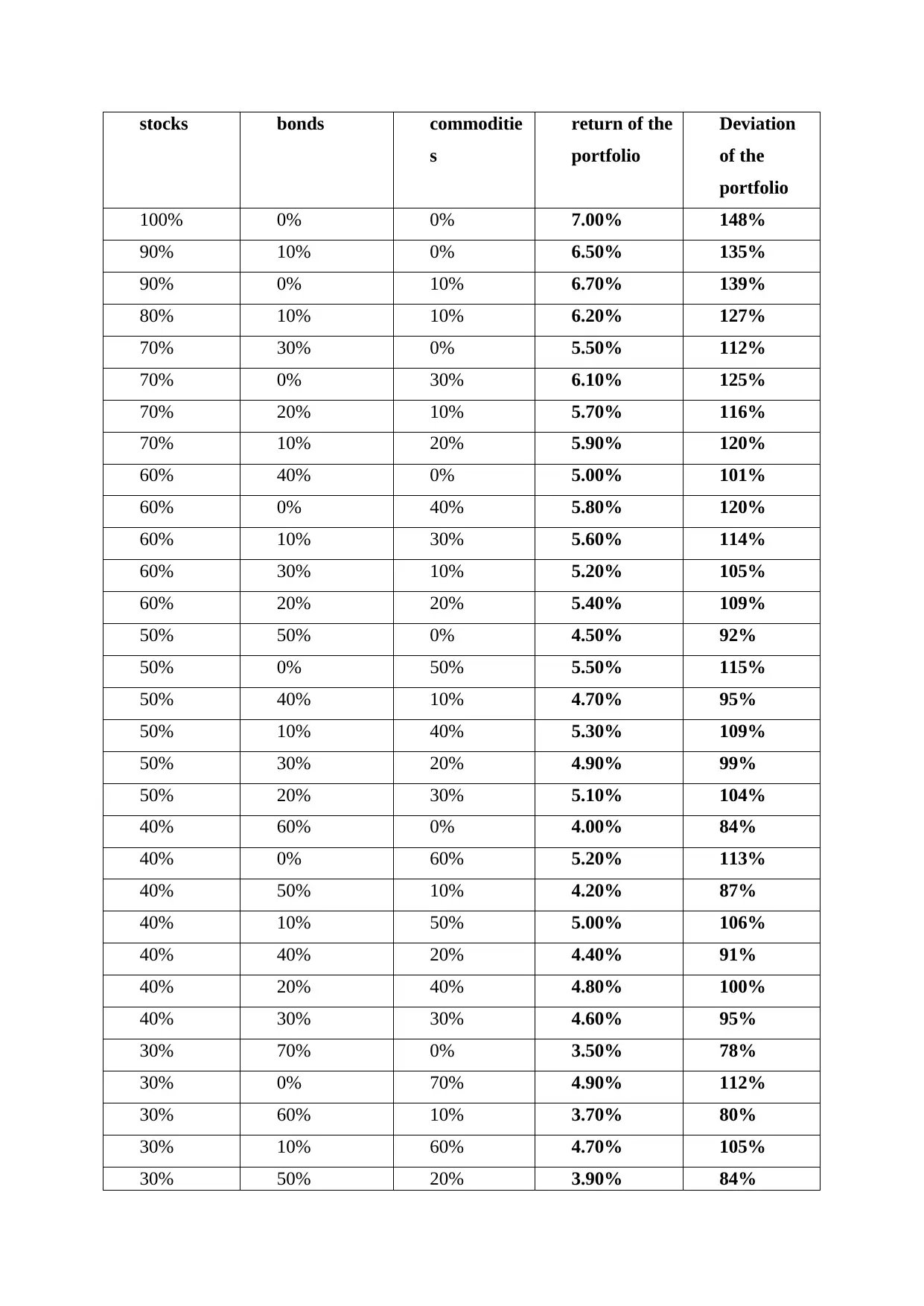

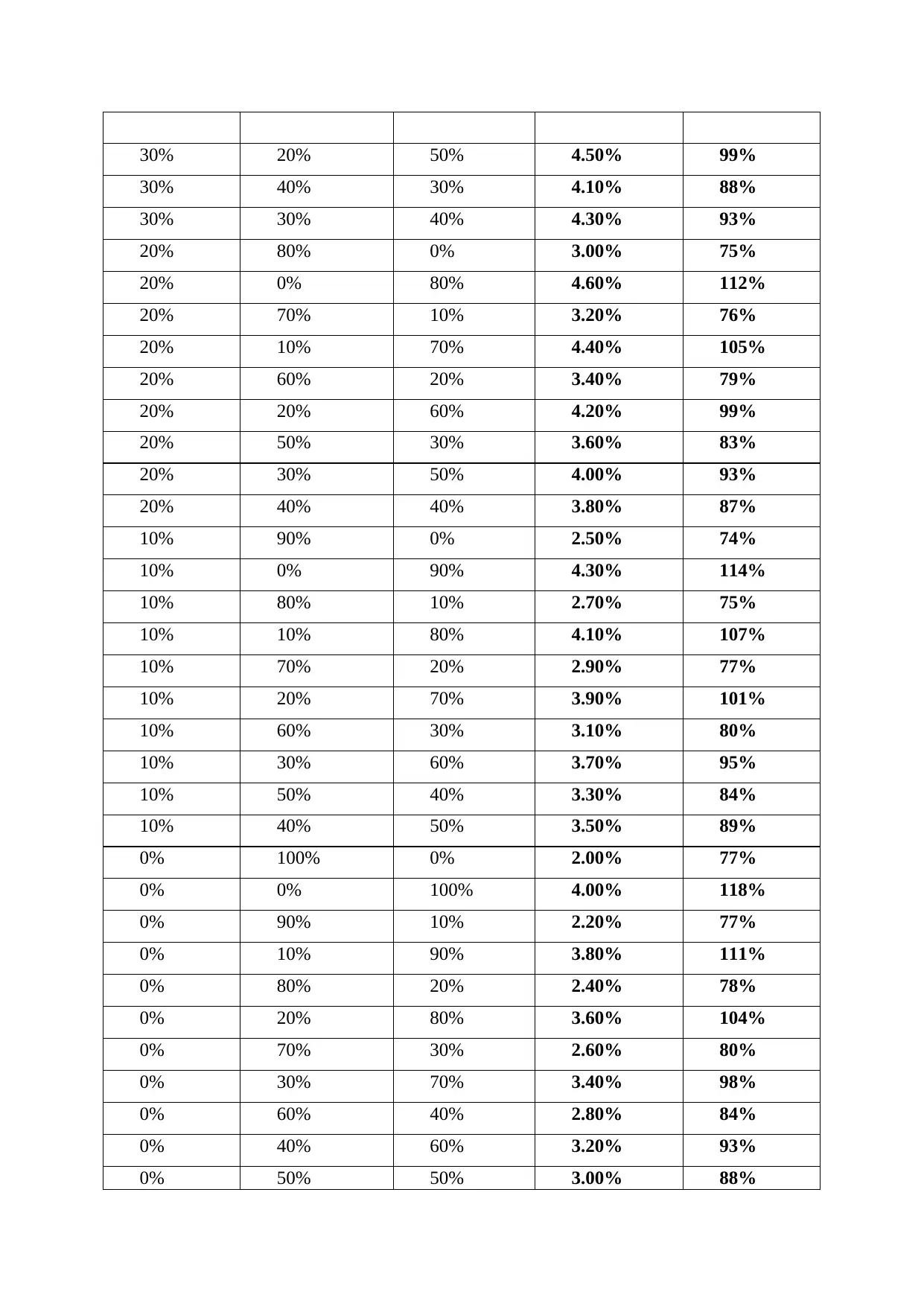

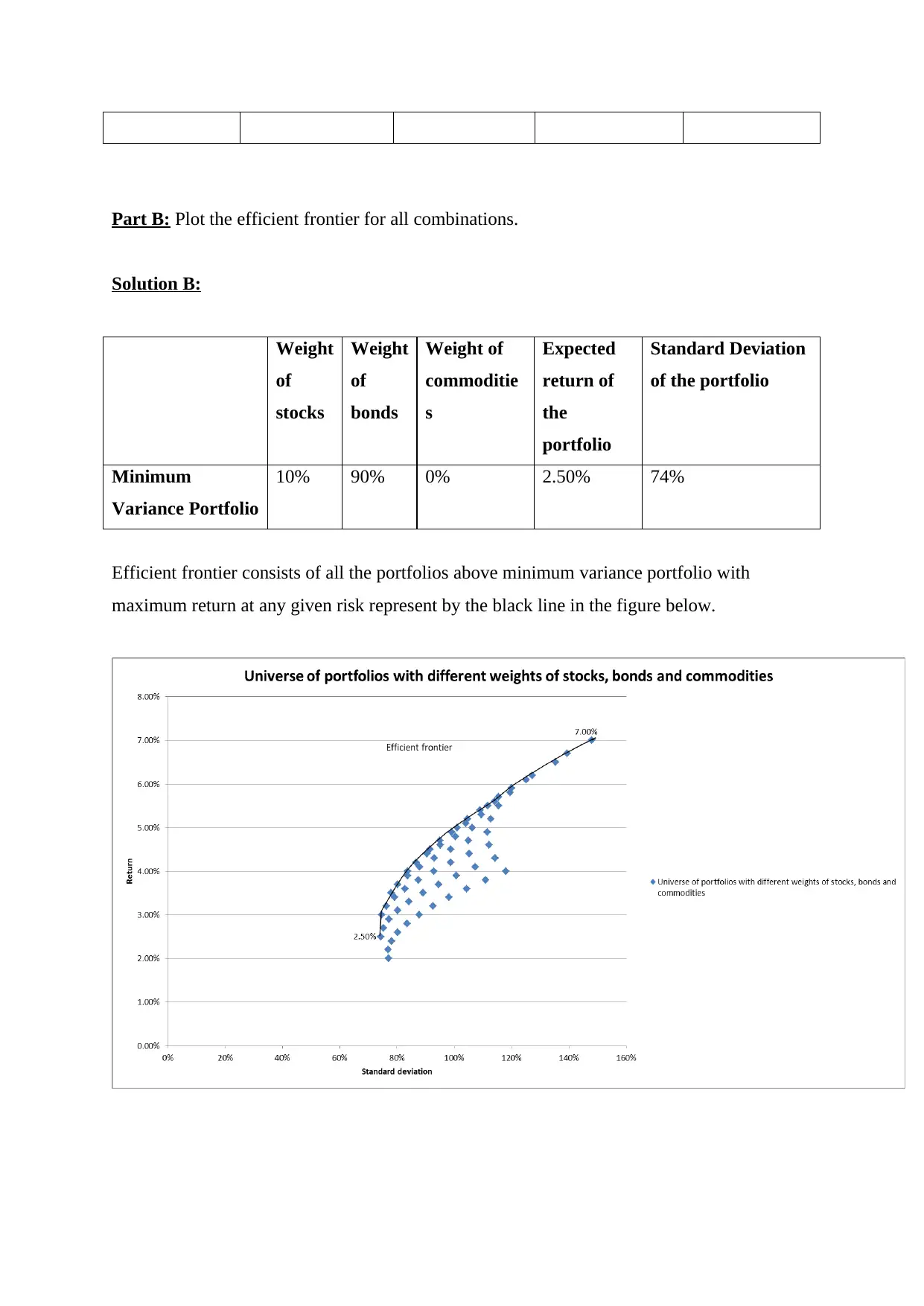

This project analyzes financial data, focusing on regression analysis and portfolio optimization. Question 1 involves predicting actual account balances based on computer-generated balances and calculating a 95% confidence interval for a specific account. Question 2 requires the calculation of expected returns and standard deviations for various portfolio combinations of stocks, bonds, and commodities. The analysis includes creating an efficient frontier to identify optimal portfolio allocations. The project utilizes regression equations and statistical methods to evaluate and optimize investment strategies, providing a comprehensive understanding of financial modeling and portfolio management.

1 out of 6

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.