Financial Management: Project and Bond Analysis Assignment Solution

VerifiedAdded on 2019/10/31

|6

|778

|184

Homework Assignment

AI Summary

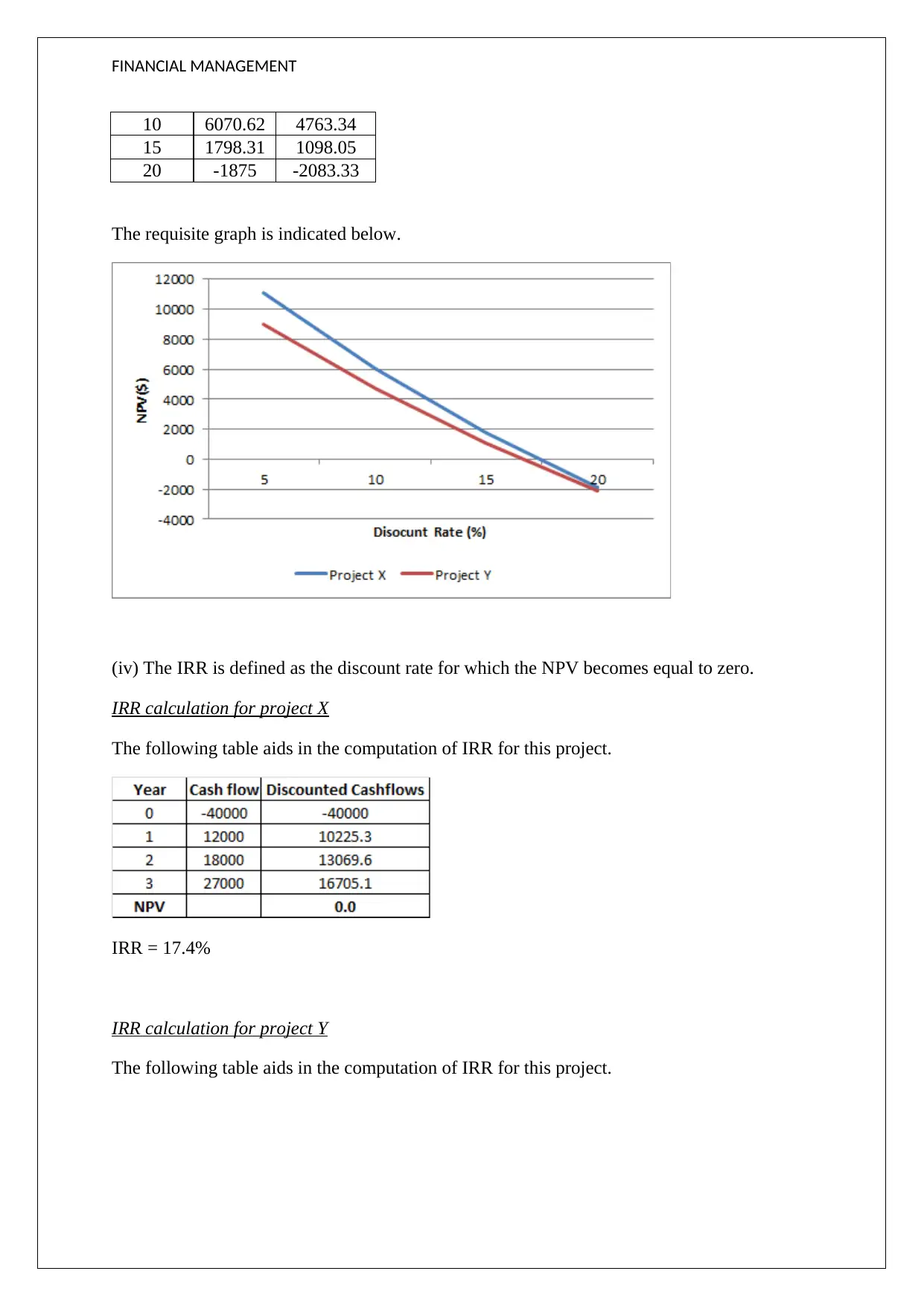

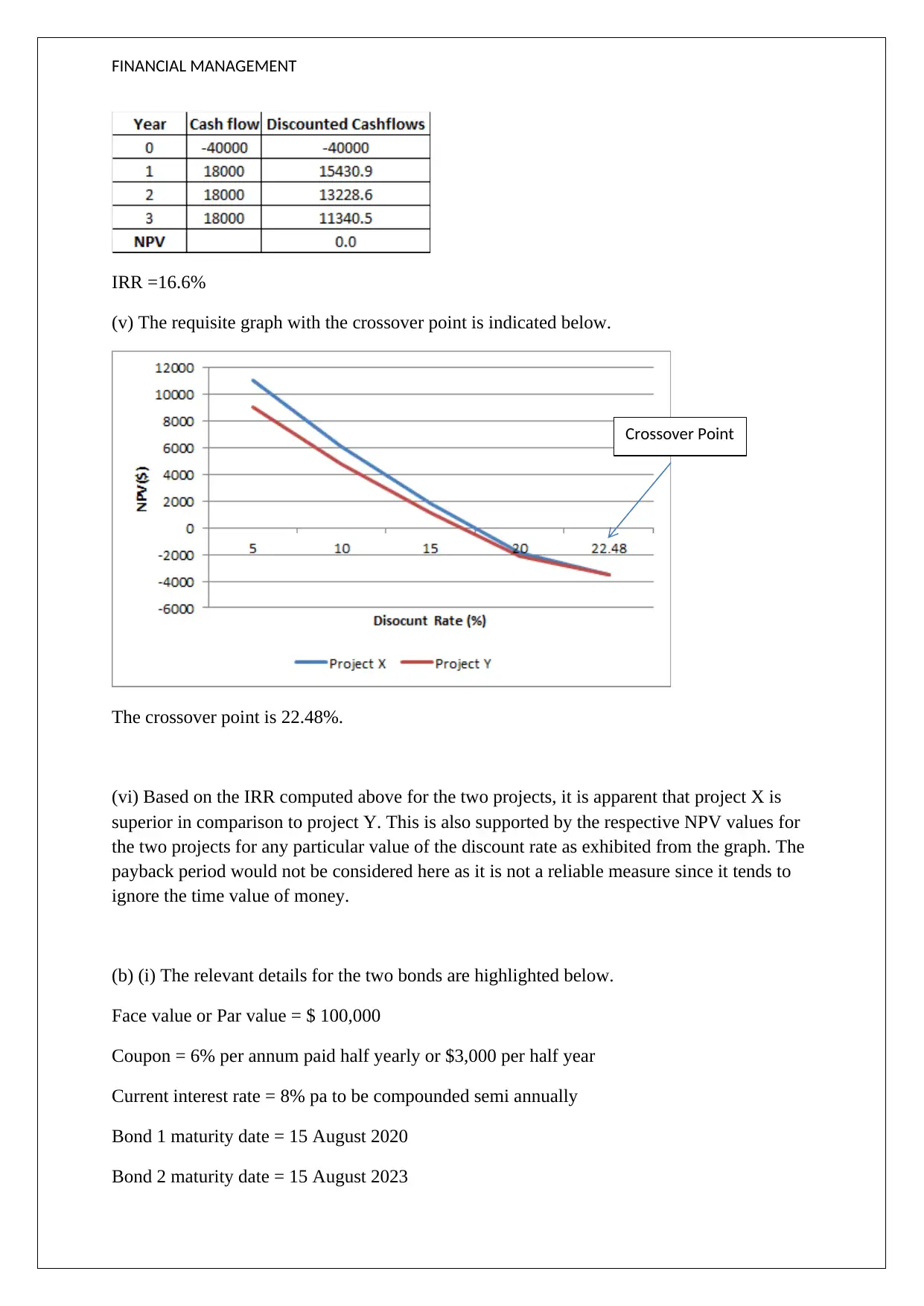

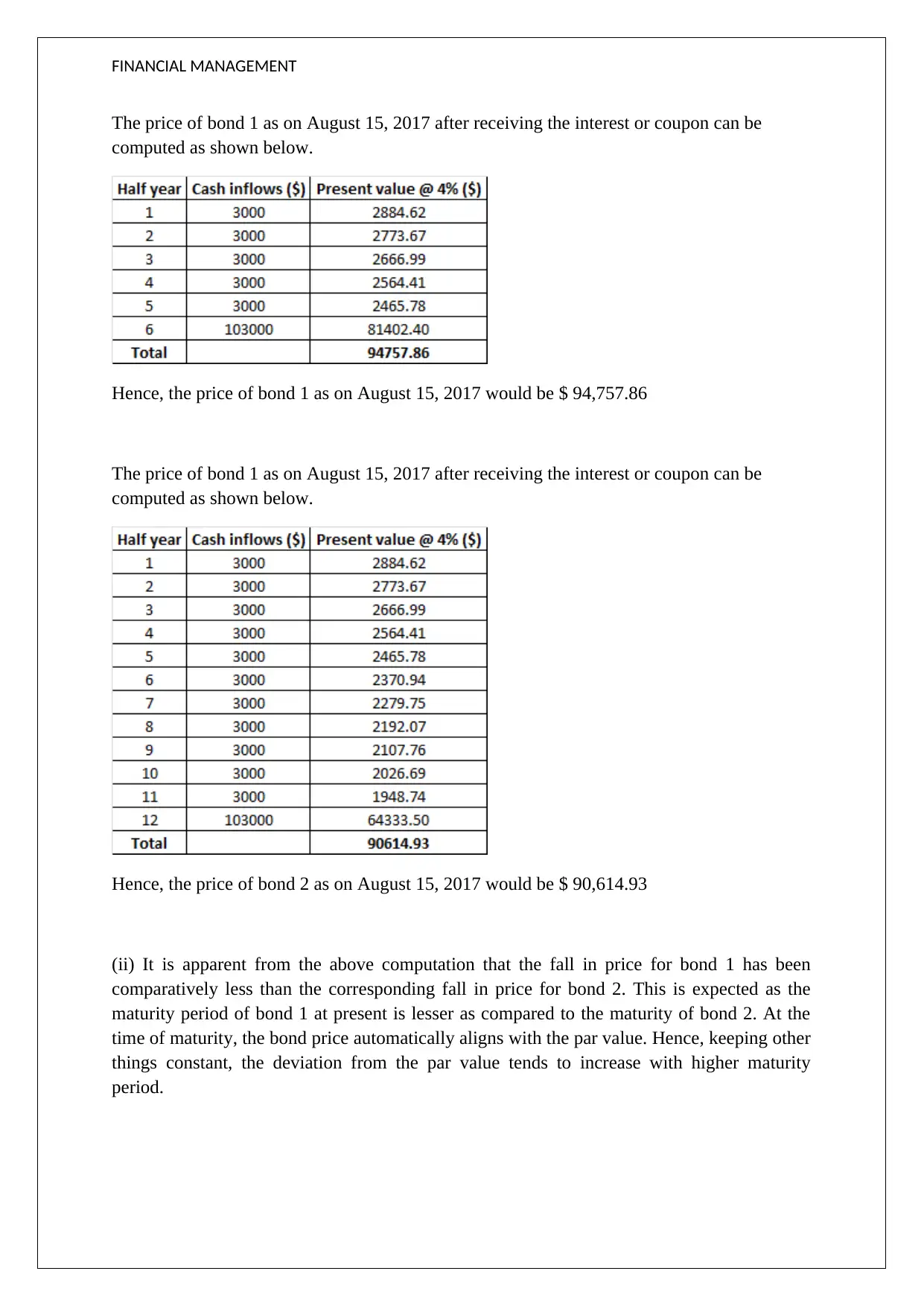

This assignment solution addresses a financial management problem, focusing on project and bond analysis. The solution begins with the calculation of the payback period for two projects, Project X and Project Y, comparing their investment recovery times. It then explores the limitations of the payback period, emphasizing the importance of considering the time value of money. The solution proceeds with the computation of the Net Present Value (NPV) for both projects at varying discount rates, supported by a graphical representation. It then delves into the Internal Rate of Return (IRR) calculation for each project, determining the discount rate at which the NPV equals zero, and includes a graph showing the crossover point. Based on IRR and NPV, the solution recommends Project X over Project Y. The assignment also covers bond valuation, calculating the prices of two bonds with differing maturity dates. The solution explains the inverse relationship between bond prices and interest rates, demonstrating how changes in interest rates impact bond values. It also illustrates the effect of maturity period on bond price fluctuations.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.