Comparative Financial Ratio Analysis of Oman and Oredo Telecom

VerifiedAdded on 2021/05/30

|16

|2851

|93

Report

AI Summary

This report provides a detailed comparative financial analysis of Oman Telecommunication and Oredo Telecommunication, examining their performance across two financial years, 2016 and 2017. The analysis utilizes twelve key financial ratios, including current ratio, quick ratio, receivables turnover, asset turnover, and profitability ratios like net profit margin and earnings per share, along with debt and leverage ratios. The report calculates and interprets these ratios for both companies, offering insights into their liquidity, efficiency, profitability, and solvency. The conclusion summarizes the findings, highlighting the relative strengths and weaknesses of each company based on the calculated financial metrics. This comprehensive analysis is crucial for understanding the financial health and performance trends of these telecommunication companies.

FINANCE 1

SUMMARY

This report analyse performance of the two companies using ratio analysis. The two

companies are “Oman Telecommunication” and “Oredo Telecommunication”. In this report,

twelve financial ratios are calculated considering two financial years 2017 and 2016. Further

this report ends with conclusion of the outcome.

SUMMARY

This report analyse performance of the two companies using ratio analysis. The two

companies are “Oman Telecommunication” and “Oredo Telecommunication”. In this report,

twelve financial ratios are calculated considering two financial years 2017 and 2016. Further

this report ends with conclusion of the outcome.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE 2

Contents

RATIO ANALYSIS....................................................................................................................................3

1. Current ratios.............................................................................................................................3

2. Quick ratios................................................................................................................................4

3. Receivables turnover ratios.......................................................................................................5

4. Asset turnover ratios.................................................................................................................6

5. Fixed Asset turnover ratios........................................................................................................7

6. Net profit margin.......................................................................................................................8

7. Earnings per share.....................................................................................................................9

8. Debt to asset ratio...................................................................................................................10

9. Debt to equity ratio.................................................................................................................11

10. Interest coverage ratios.......................................................................................................12

11. Return on Equity (ROE)........................................................................................................13

12. Return on Investment (ROI).................................................................................................14

REFERENCES........................................................................................................................................16

Contents

RATIO ANALYSIS....................................................................................................................................3

1. Current ratios.............................................................................................................................3

2. Quick ratios................................................................................................................................4

3. Receivables turnover ratios.......................................................................................................5

4. Asset turnover ratios.................................................................................................................6

5. Fixed Asset turnover ratios........................................................................................................7

6. Net profit margin.......................................................................................................................8

7. Earnings per share.....................................................................................................................9

8. Debt to asset ratio...................................................................................................................10

9. Debt to equity ratio.................................................................................................................11

10. Interest coverage ratios.......................................................................................................12

11. Return on Equity (ROE)........................................................................................................13

12. Return on Investment (ROI).................................................................................................14

REFERENCES........................................................................................................................................16

FINANCE 3

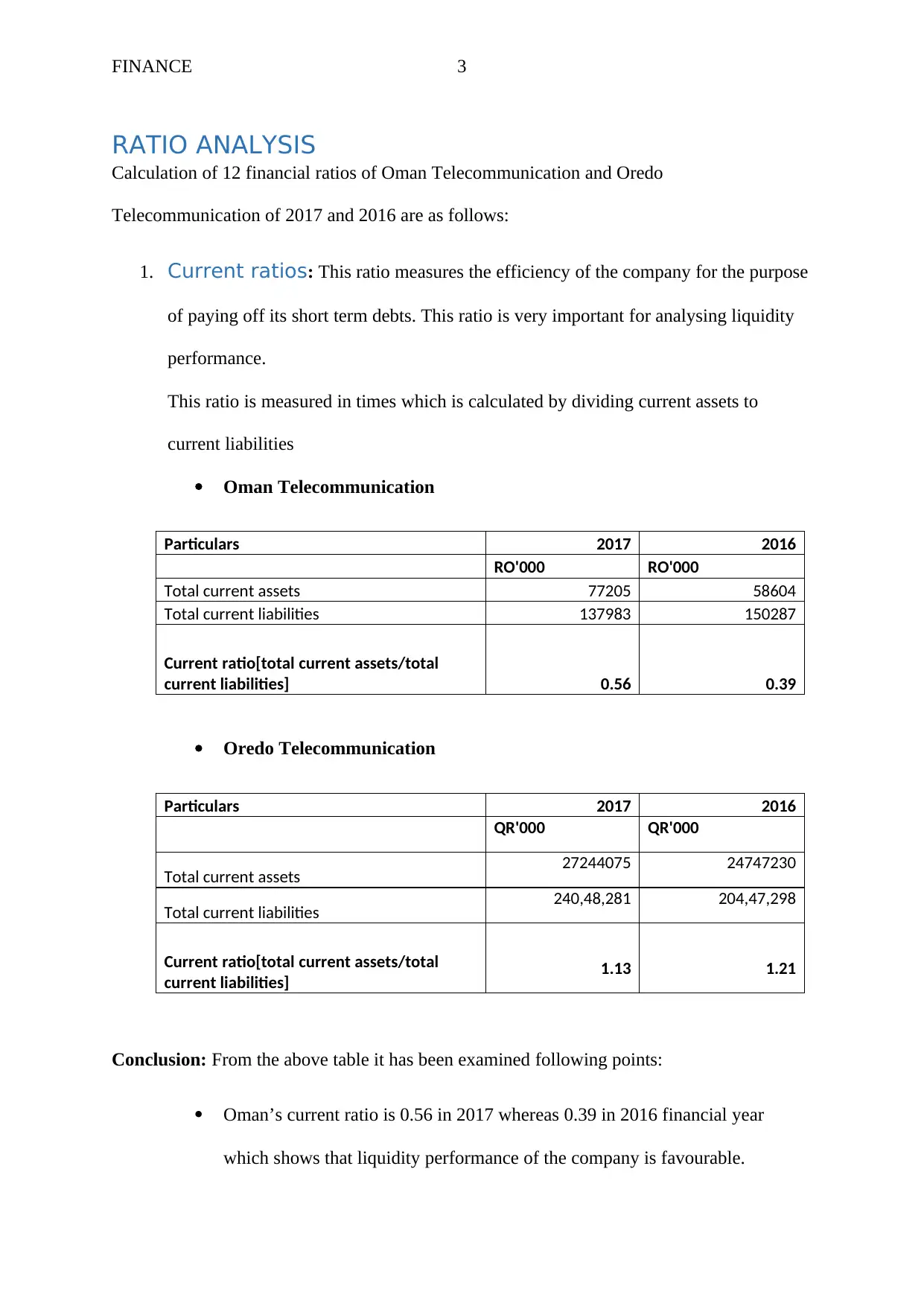

RATIO ANALYSIS

Calculation of 12 financial ratios of Oman Telecommunication and Oredo

Telecommunication of 2017 and 2016 are as follows:

1. Current ratios: This ratio measures the efficiency of the company for the purpose

of paying off its short term debts. This ratio is very important for analysing liquidity

performance.

This ratio is measured in times which is calculated by dividing current assets to

current liabilities

Oman Telecommunication

Particulars 2017 2016

RO'000 RO'000

Total current assets 77205 58604

Total current liabilities 137983 150287

Current ratio[total current assets/total

current liabilities] 0.56 0.39

Oredo Telecommunication

Particulars 2017 2016

QR'000 QR'000

Total current assets 27244075 24747230

Total current liabilities 240,48,281 204,47,298

Current ratio[total current assets/total

current liabilities] 1.13 1.21

Conclusion: From the above table it has been examined following points:

Oman’s current ratio is 0.56 in 2017 whereas 0.39 in 2016 financial year

which shows that liquidity performance of the company is favourable.

RATIO ANALYSIS

Calculation of 12 financial ratios of Oman Telecommunication and Oredo

Telecommunication of 2017 and 2016 are as follows:

1. Current ratios: This ratio measures the efficiency of the company for the purpose

of paying off its short term debts. This ratio is very important for analysing liquidity

performance.

This ratio is measured in times which is calculated by dividing current assets to

current liabilities

Oman Telecommunication

Particulars 2017 2016

RO'000 RO'000

Total current assets 77205 58604

Total current liabilities 137983 150287

Current ratio[total current assets/total

current liabilities] 0.56 0.39

Oredo Telecommunication

Particulars 2017 2016

QR'000 QR'000

Total current assets 27244075 24747230

Total current liabilities 240,48,281 204,47,298

Current ratio[total current assets/total

current liabilities] 1.13 1.21

Conclusion: From the above table it has been examined following points:

Oman’s current ratio is 0.56 in 2017 whereas 0.39 in 2016 financial year

which shows that liquidity performance of the company is favourable.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE 4

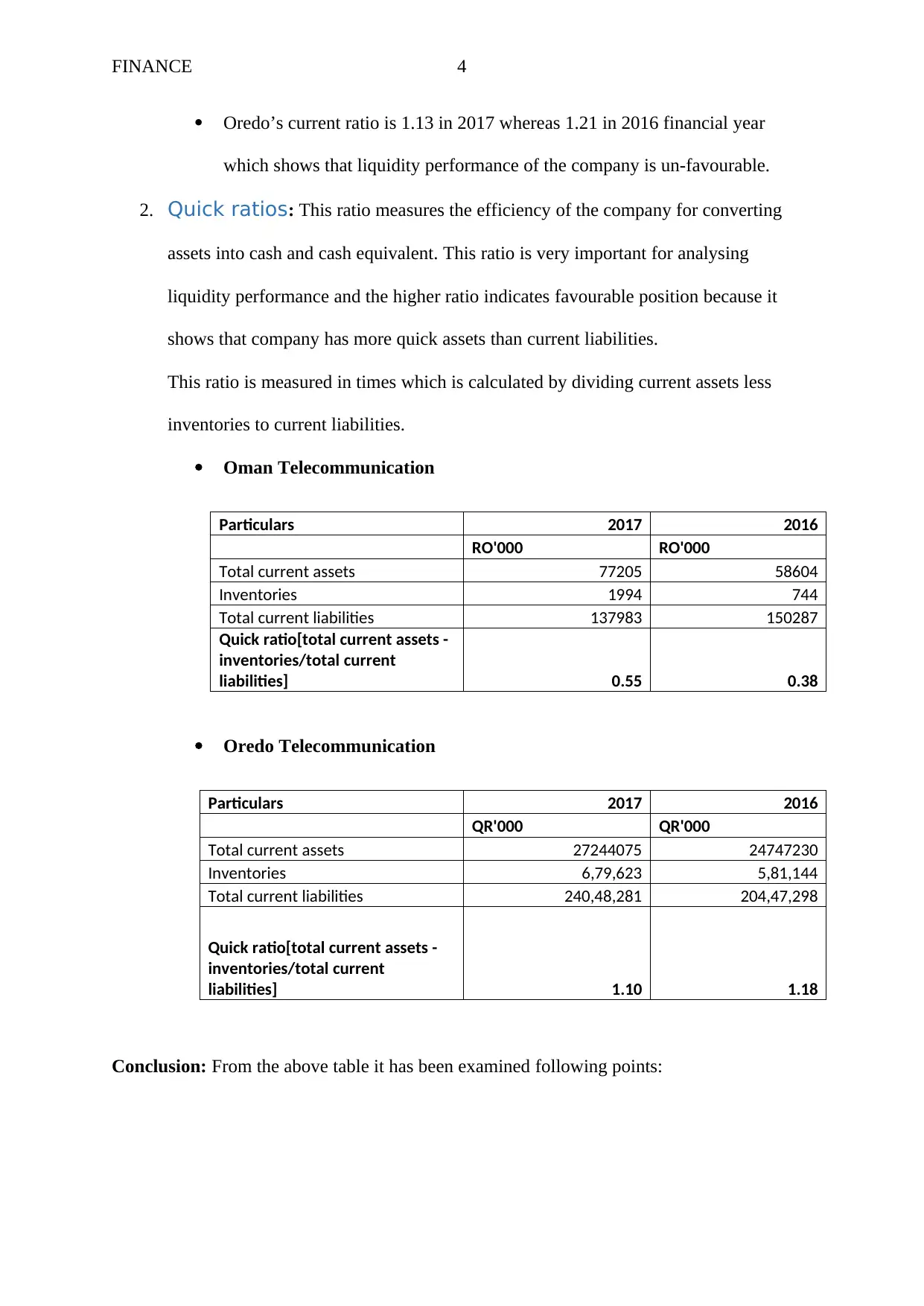

Oredo’s current ratio is 1.13 in 2017 whereas 1.21 in 2016 financial year

which shows that liquidity performance of the company is un-favourable.

2. Quick ratios: This ratio measures the efficiency of the company for converting

assets into cash and cash equivalent. This ratio is very important for analysing

liquidity performance and the higher ratio indicates favourable position because it

shows that company has more quick assets than current liabilities.

This ratio is measured in times which is calculated by dividing current assets less

inventories to current liabilities.

Oman Telecommunication

Particulars 2017 2016

RO'000 RO'000

Total current assets 77205 58604

Inventories 1994 744

Total current liabilities 137983 150287

Quick ratio[total current assets -

inventories/total current

liabilities] 0.55 0.38

Oredo Telecommunication

Particulars 2017 2016

QR'000 QR'000

Total current assets 27244075 24747230

Inventories 6,79,623 5,81,144

Total current liabilities 240,48,281 204,47,298

Quick ratio[total current assets -

inventories/total current

liabilities] 1.10 1.18

Conclusion: From the above table it has been examined following points:

Oredo’s current ratio is 1.13 in 2017 whereas 1.21 in 2016 financial year

which shows that liquidity performance of the company is un-favourable.

2. Quick ratios: This ratio measures the efficiency of the company for converting

assets into cash and cash equivalent. This ratio is very important for analysing

liquidity performance and the higher ratio indicates favourable position because it

shows that company has more quick assets than current liabilities.

This ratio is measured in times which is calculated by dividing current assets less

inventories to current liabilities.

Oman Telecommunication

Particulars 2017 2016

RO'000 RO'000

Total current assets 77205 58604

Inventories 1994 744

Total current liabilities 137983 150287

Quick ratio[total current assets -

inventories/total current

liabilities] 0.55 0.38

Oredo Telecommunication

Particulars 2017 2016

QR'000 QR'000

Total current assets 27244075 24747230

Inventories 6,79,623 5,81,144

Total current liabilities 240,48,281 204,47,298

Quick ratio[total current assets -

inventories/total current

liabilities] 1.10 1.18

Conclusion: From the above table it has been examined following points:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE 5

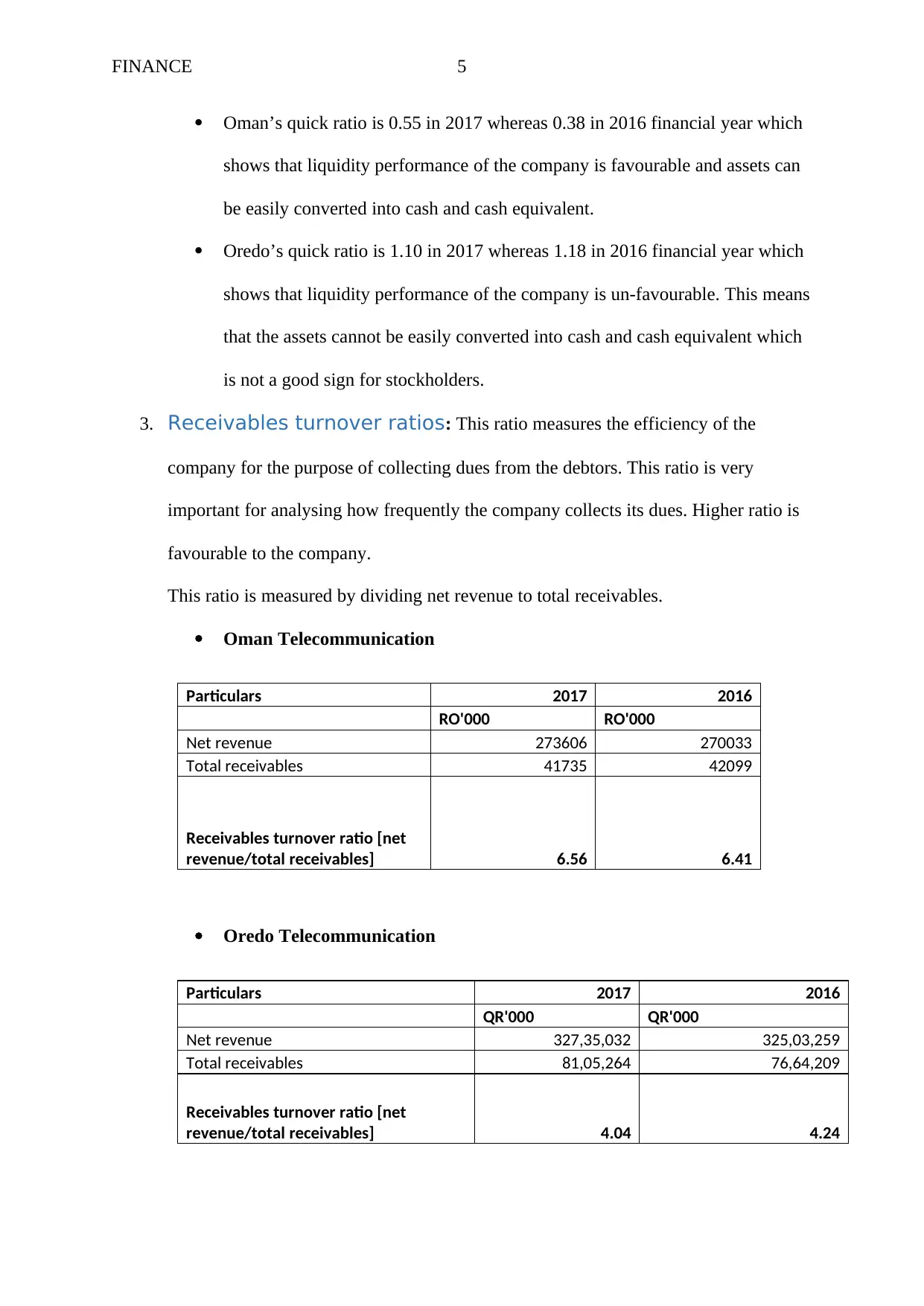

Oman’s quick ratio is 0.55 in 2017 whereas 0.38 in 2016 financial year which

shows that liquidity performance of the company is favourable and assets can

be easily converted into cash and cash equivalent.

Oredo’s quick ratio is 1.10 in 2017 whereas 1.18 in 2016 financial year which

shows that liquidity performance of the company is un-favourable. This means

that the assets cannot be easily converted into cash and cash equivalent which

is not a good sign for stockholders.

3. Receivables turnover ratios: This ratio measures the efficiency of the

company for the purpose of collecting dues from the debtors. This ratio is very

important for analysing how frequently the company collects its dues. Higher ratio is

favourable to the company.

This ratio is measured by dividing net revenue to total receivables.

Oman Telecommunication

Particulars 2017 2016

RO'000 RO'000

Net revenue 273606 270033

Total receivables 41735 42099

Receivables turnover ratio [net

revenue/total receivables] 6.56 6.41

Oredo Telecommunication

Particulars 2017 2016

QR'000 QR'000

Net revenue 327,35,032 325,03,259

Total receivables 81,05,264 76,64,209

Receivables turnover ratio [net

revenue/total receivables] 4.04 4.24

Oman’s quick ratio is 0.55 in 2017 whereas 0.38 in 2016 financial year which

shows that liquidity performance of the company is favourable and assets can

be easily converted into cash and cash equivalent.

Oredo’s quick ratio is 1.10 in 2017 whereas 1.18 in 2016 financial year which

shows that liquidity performance of the company is un-favourable. This means

that the assets cannot be easily converted into cash and cash equivalent which

is not a good sign for stockholders.

3. Receivables turnover ratios: This ratio measures the efficiency of the

company for the purpose of collecting dues from the debtors. This ratio is very

important for analysing how frequently the company collects its dues. Higher ratio is

favourable to the company.

This ratio is measured by dividing net revenue to total receivables.

Oman Telecommunication

Particulars 2017 2016

RO'000 RO'000

Net revenue 273606 270033

Total receivables 41735 42099

Receivables turnover ratio [net

revenue/total receivables] 6.56 6.41

Oredo Telecommunication

Particulars 2017 2016

QR'000 QR'000

Net revenue 327,35,032 325,03,259

Total receivables 81,05,264 76,64,209

Receivables turnover ratio [net

revenue/total receivables] 4.04 4.24

FINANCE 6

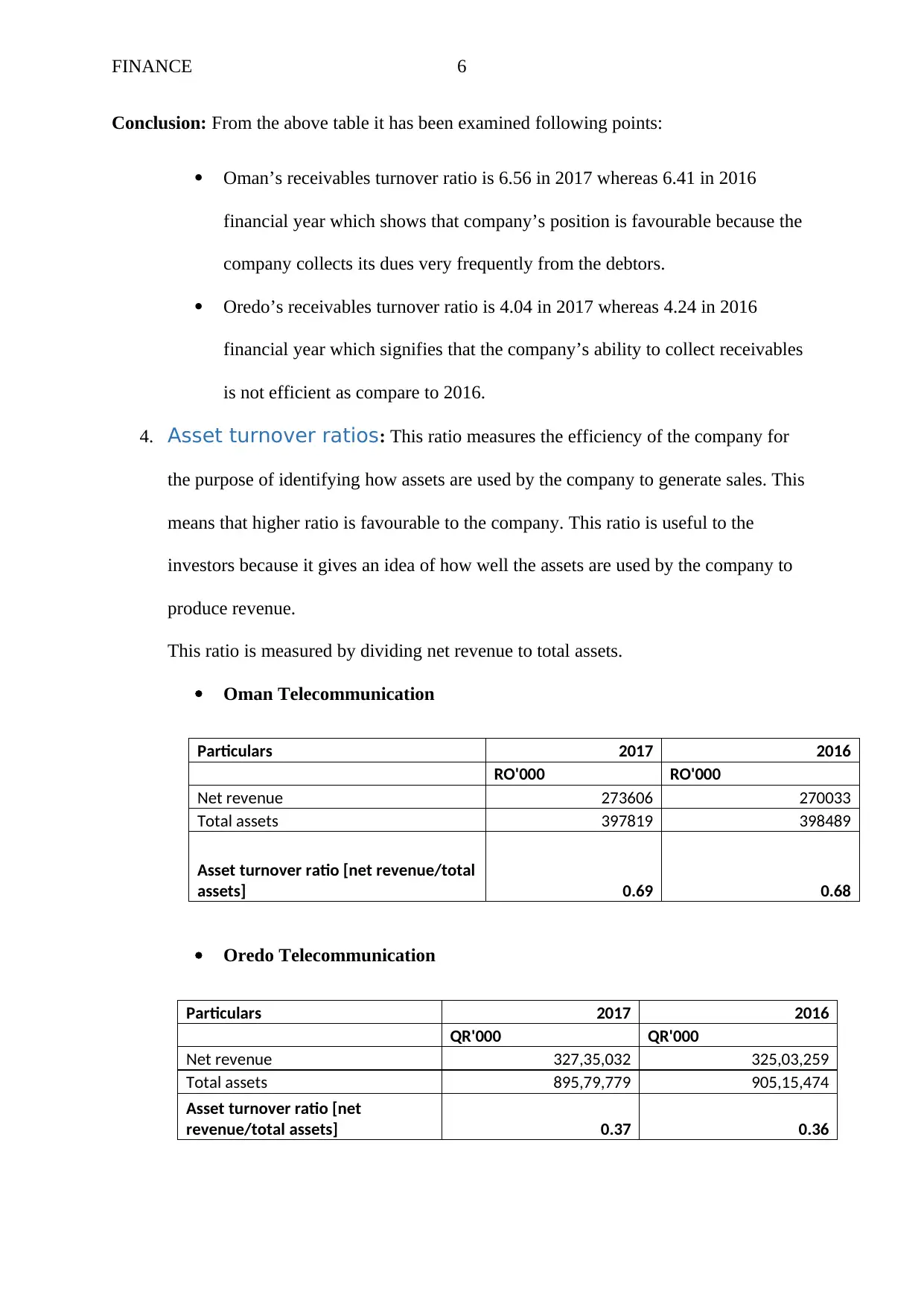

Conclusion: From the above table it has been examined following points:

Oman’s receivables turnover ratio is 6.56 in 2017 whereas 6.41 in 2016

financial year which shows that company’s position is favourable because the

company collects its dues very frequently from the debtors.

Oredo’s receivables turnover ratio is 4.04 in 2017 whereas 4.24 in 2016

financial year which signifies that the company’s ability to collect receivables

is not efficient as compare to 2016.

4. Asset turnover ratios: This ratio measures the efficiency of the company for

the purpose of identifying how assets are used by the company to generate sales. This

means that higher ratio is favourable to the company. This ratio is useful to the

investors because it gives an idea of how well the assets are used by the company to

produce revenue.

This ratio is measured by dividing net revenue to total assets.

Oman Telecommunication

Particulars 2017 2016

RO'000 RO'000

Net revenue 273606 270033

Total assets 397819 398489

Asset turnover ratio [net revenue/total

assets] 0.69 0.68

Oredo Telecommunication

Particulars 2017 2016

QR'000 QR'000

Net revenue 327,35,032 325,03,259

Total assets 895,79,779 905,15,474

Asset turnover ratio [net

revenue/total assets] 0.37 0.36

Conclusion: From the above table it has been examined following points:

Oman’s receivables turnover ratio is 6.56 in 2017 whereas 6.41 in 2016

financial year which shows that company’s position is favourable because the

company collects its dues very frequently from the debtors.

Oredo’s receivables turnover ratio is 4.04 in 2017 whereas 4.24 in 2016

financial year which signifies that the company’s ability to collect receivables

is not efficient as compare to 2016.

4. Asset turnover ratios: This ratio measures the efficiency of the company for

the purpose of identifying how assets are used by the company to generate sales. This

means that higher ratio is favourable to the company. This ratio is useful to the

investors because it gives an idea of how well the assets are used by the company to

produce revenue.

This ratio is measured by dividing net revenue to total assets.

Oman Telecommunication

Particulars 2017 2016

RO'000 RO'000

Net revenue 273606 270033

Total assets 397819 398489

Asset turnover ratio [net revenue/total

assets] 0.69 0.68

Oredo Telecommunication

Particulars 2017 2016

QR'000 QR'000

Net revenue 327,35,032 325,03,259

Total assets 895,79,779 905,15,474

Asset turnover ratio [net

revenue/total assets] 0.37 0.36

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE 7

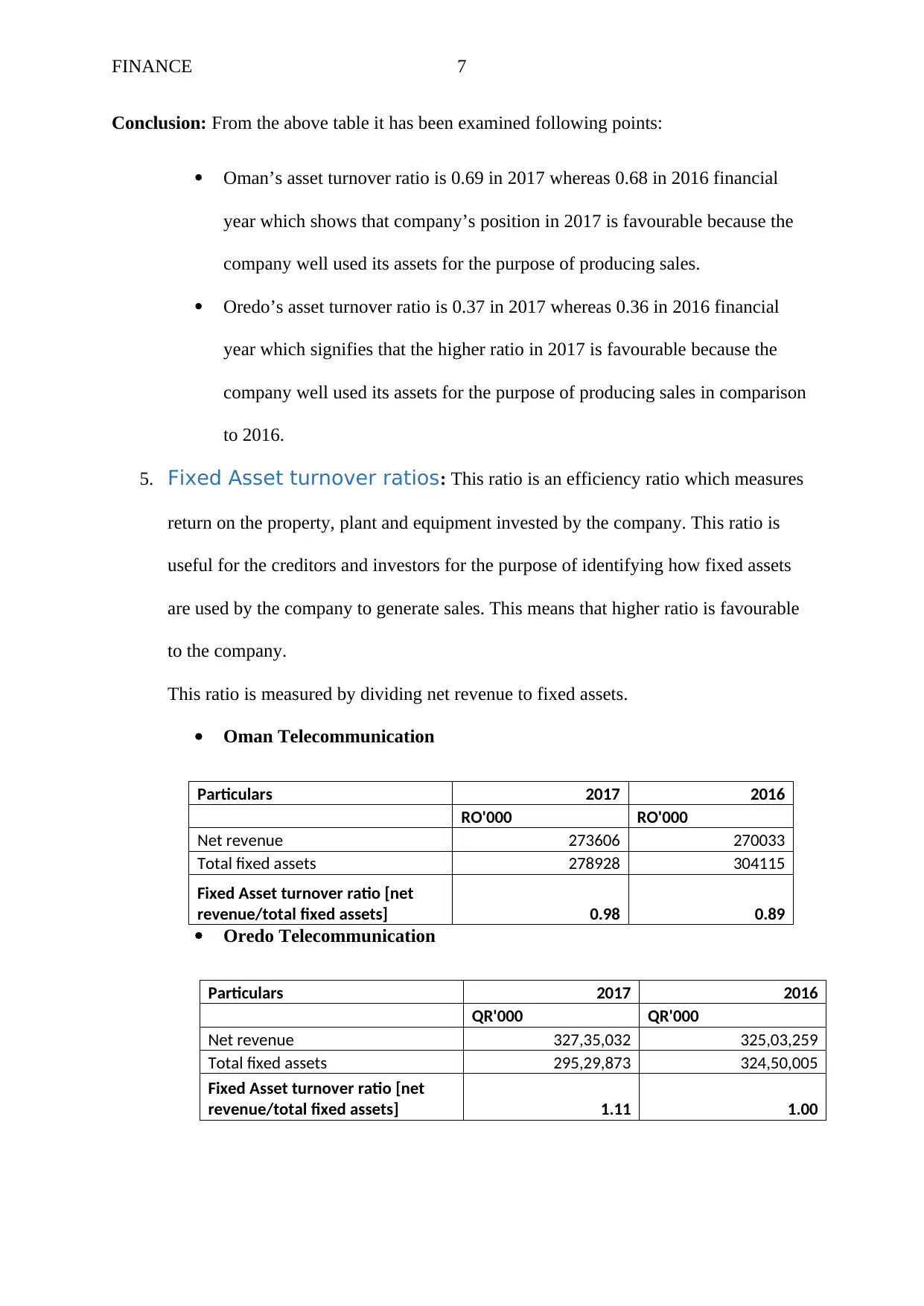

Conclusion: From the above table it has been examined following points:

Oman’s asset turnover ratio is 0.69 in 2017 whereas 0.68 in 2016 financial

year which shows that company’s position in 2017 is favourable because the

company well used its assets for the purpose of producing sales.

Oredo’s asset turnover ratio is 0.37 in 2017 whereas 0.36 in 2016 financial

year which signifies that the higher ratio in 2017 is favourable because the

company well used its assets for the purpose of producing sales in comparison

to 2016.

5. Fixed Asset turnover ratios: This ratio is an efficiency ratio which measures

return on the property, plant and equipment invested by the company. This ratio is

useful for the creditors and investors for the purpose of identifying how fixed assets

are used by the company to generate sales. This means that higher ratio is favourable

to the company.

This ratio is measured by dividing net revenue to fixed assets.

Oman Telecommunication

Particulars 2017 2016

RO'000 RO'000

Net revenue 273606 270033

Total fixed assets 278928 304115

Fixed Asset turnover ratio [net

revenue/total fixed assets] 0.98 0.89

Oredo Telecommunication

Particulars 2017 2016

QR'000 QR'000

Net revenue 327,35,032 325,03,259

Total fixed assets 295,29,873 324,50,005

Fixed Asset turnover ratio [net

revenue/total fixed assets] 1.11 1.00

Conclusion: From the above table it has been examined following points:

Oman’s asset turnover ratio is 0.69 in 2017 whereas 0.68 in 2016 financial

year which shows that company’s position in 2017 is favourable because the

company well used its assets for the purpose of producing sales.

Oredo’s asset turnover ratio is 0.37 in 2017 whereas 0.36 in 2016 financial

year which signifies that the higher ratio in 2017 is favourable because the

company well used its assets for the purpose of producing sales in comparison

to 2016.

5. Fixed Asset turnover ratios: This ratio is an efficiency ratio which measures

return on the property, plant and equipment invested by the company. This ratio is

useful for the creditors and investors for the purpose of identifying how fixed assets

are used by the company to generate sales. This means that higher ratio is favourable

to the company.

This ratio is measured by dividing net revenue to fixed assets.

Oman Telecommunication

Particulars 2017 2016

RO'000 RO'000

Net revenue 273606 270033

Total fixed assets 278928 304115

Fixed Asset turnover ratio [net

revenue/total fixed assets] 0.98 0.89

Oredo Telecommunication

Particulars 2017 2016

QR'000 QR'000

Net revenue 327,35,032 325,03,259

Total fixed assets 295,29,873 324,50,005

Fixed Asset turnover ratio [net

revenue/total fixed assets] 1.11 1.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE 8

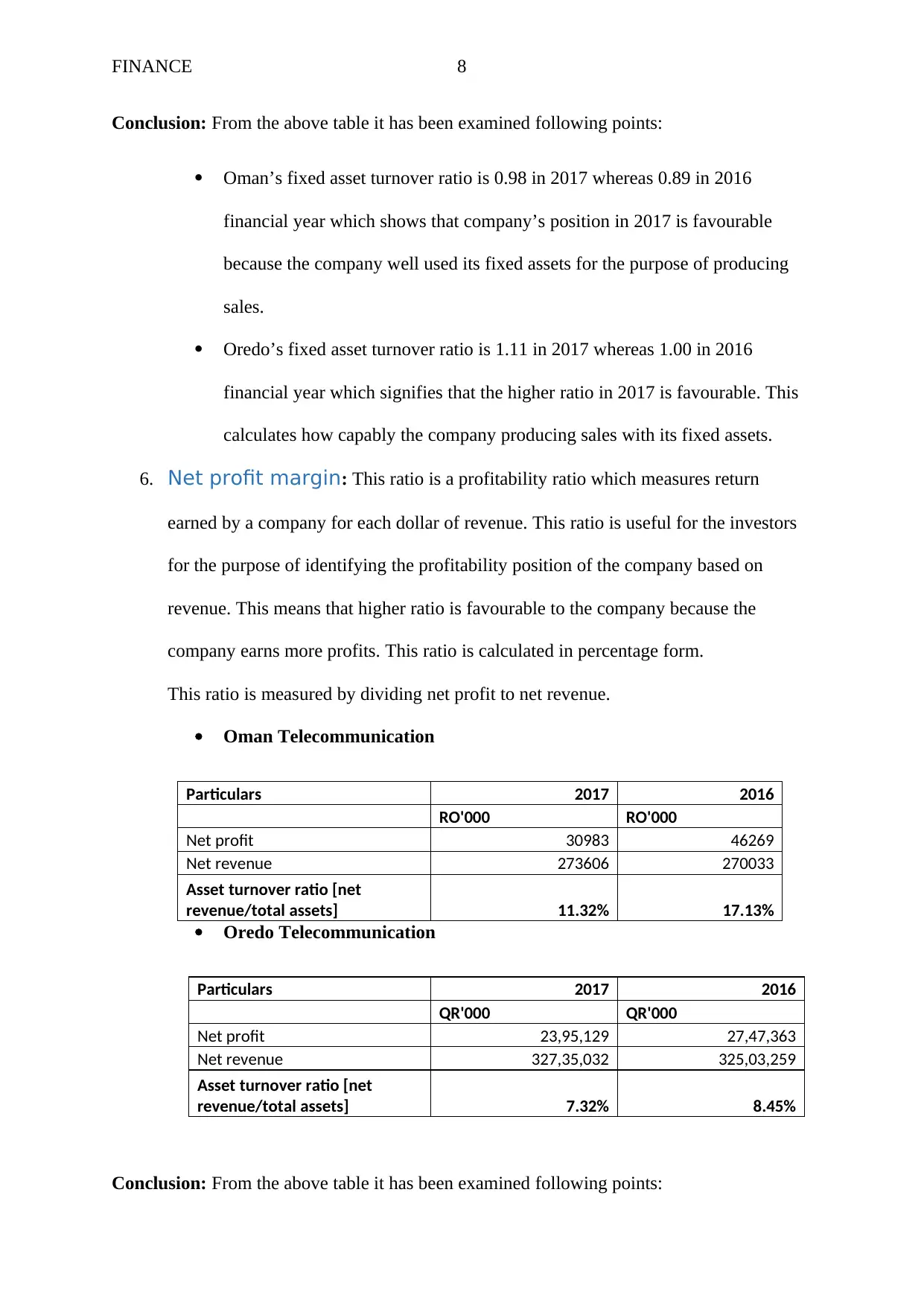

Conclusion: From the above table it has been examined following points:

Oman’s fixed asset turnover ratio is 0.98 in 2017 whereas 0.89 in 2016

financial year which shows that company’s position in 2017 is favourable

because the company well used its fixed assets for the purpose of producing

sales.

Oredo’s fixed asset turnover ratio is 1.11 in 2017 whereas 1.00 in 2016

financial year which signifies that the higher ratio in 2017 is favourable. This

calculates how capably the company producing sales with its fixed assets.

6. Net profit margin: This ratio is a profitability ratio which measures return

earned by a company for each dollar of revenue. This ratio is useful for the investors

for the purpose of identifying the profitability position of the company based on

revenue. This means that higher ratio is favourable to the company because the

company earns more profits. This ratio is calculated in percentage form.

This ratio is measured by dividing net profit to net revenue.

Oman Telecommunication

Particulars 2017 2016

RO'000 RO'000

Net profit 30983 46269

Net revenue 273606 270033

Asset turnover ratio [net

revenue/total assets] 11.32% 17.13%

Oredo Telecommunication

Particulars 2017 2016

QR'000 QR'000

Net profit 23,95,129 27,47,363

Net revenue 327,35,032 325,03,259

Asset turnover ratio [net

revenue/total assets] 7.32% 8.45%

Conclusion: From the above table it has been examined following points:

Conclusion: From the above table it has been examined following points:

Oman’s fixed asset turnover ratio is 0.98 in 2017 whereas 0.89 in 2016

financial year which shows that company’s position in 2017 is favourable

because the company well used its fixed assets for the purpose of producing

sales.

Oredo’s fixed asset turnover ratio is 1.11 in 2017 whereas 1.00 in 2016

financial year which signifies that the higher ratio in 2017 is favourable. This

calculates how capably the company producing sales with its fixed assets.

6. Net profit margin: This ratio is a profitability ratio which measures return

earned by a company for each dollar of revenue. This ratio is useful for the investors

for the purpose of identifying the profitability position of the company based on

revenue. This means that higher ratio is favourable to the company because the

company earns more profits. This ratio is calculated in percentage form.

This ratio is measured by dividing net profit to net revenue.

Oman Telecommunication

Particulars 2017 2016

RO'000 RO'000

Net profit 30983 46269

Net revenue 273606 270033

Asset turnover ratio [net

revenue/total assets] 11.32% 17.13%

Oredo Telecommunication

Particulars 2017 2016

QR'000 QR'000

Net profit 23,95,129 27,47,363

Net revenue 327,35,032 325,03,259

Asset turnover ratio [net

revenue/total assets] 7.32% 8.45%

Conclusion: From the above table it has been examined following points:

FINANCE 9

Oman’s net profit margin is 11.32% in 2017 whereas 17.13% in 2016 financial

year which shows that company’s profitability position in 2017 is not sound

because the company has decreased its profit margin in comparison to 2016.

Oredo’s net profit margin is 7.32% in 2017 whereas in 2016 financial year it

was 8.45% which signifies that the lower ratio in 2017 is not favourable

because the company has decreased its profit margin in comparison to 2016.

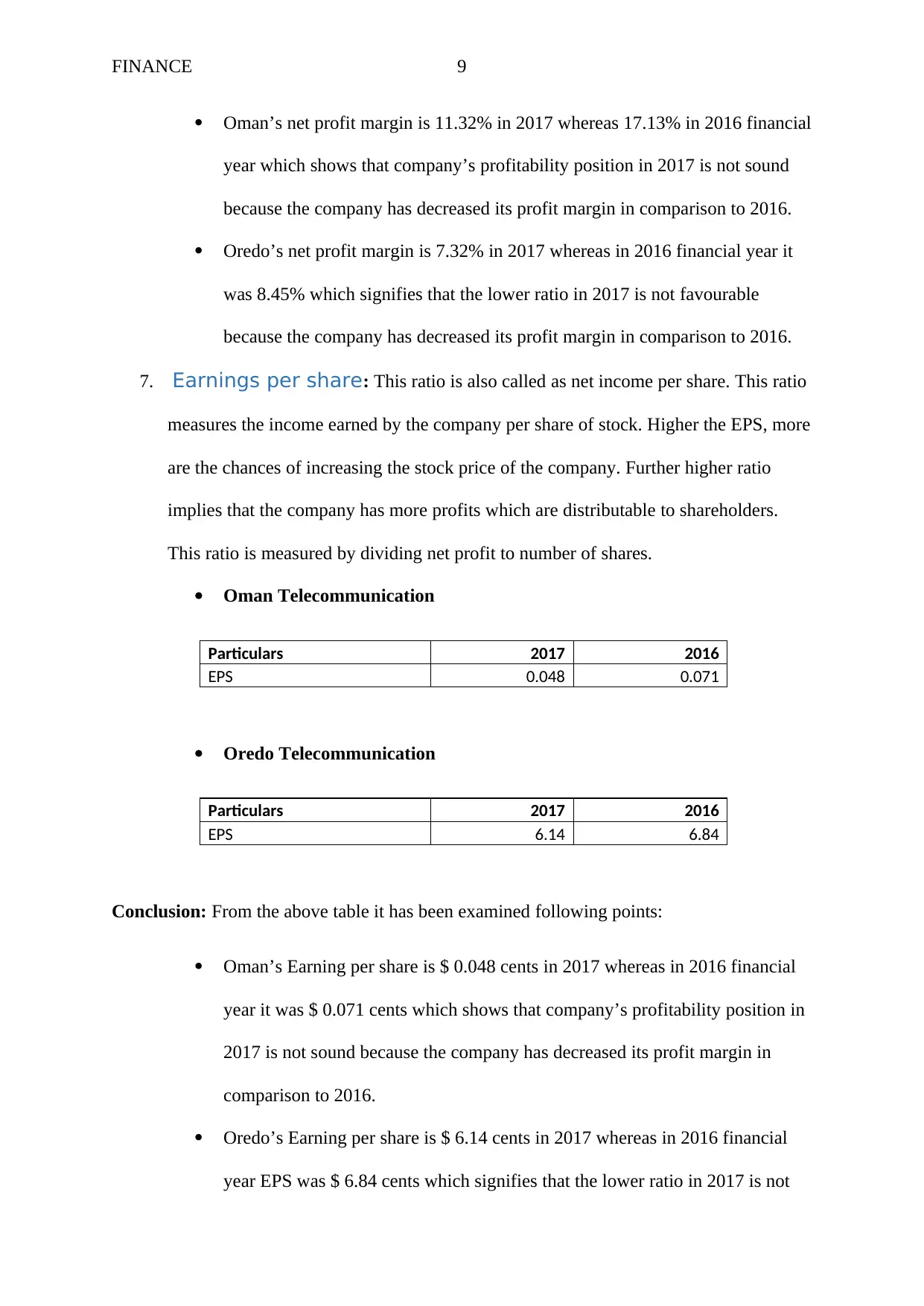

7. Earnings per share: This ratio is also called as net income per share. This ratio

measures the income earned by the company per share of stock. Higher the EPS, more

are the chances of increasing the stock price of the company. Further higher ratio

implies that the company has more profits which are distributable to shareholders.

This ratio is measured by dividing net profit to number of shares.

Oman Telecommunication

Particulars 2017 2016

EPS 0.048 0.071

Oredo Telecommunication

Particulars 2017 2016

EPS 6.14 6.84

Conclusion: From the above table it has been examined following points:

Oman’s Earning per share is $ 0.048 cents in 2017 whereas in 2016 financial

year it was $ 0.071 cents which shows that company’s profitability position in

2017 is not sound because the company has decreased its profit margin in

comparison to 2016.

Oredo’s Earning per share is $ 6.14 cents in 2017 whereas in 2016 financial

year EPS was $ 6.84 cents which signifies that the lower ratio in 2017 is not

Oman’s net profit margin is 11.32% in 2017 whereas 17.13% in 2016 financial

year which shows that company’s profitability position in 2017 is not sound

because the company has decreased its profit margin in comparison to 2016.

Oredo’s net profit margin is 7.32% in 2017 whereas in 2016 financial year it

was 8.45% which signifies that the lower ratio in 2017 is not favourable

because the company has decreased its profit margin in comparison to 2016.

7. Earnings per share: This ratio is also called as net income per share. This ratio

measures the income earned by the company per share of stock. Higher the EPS, more

are the chances of increasing the stock price of the company. Further higher ratio

implies that the company has more profits which are distributable to shareholders.

This ratio is measured by dividing net profit to number of shares.

Oman Telecommunication

Particulars 2017 2016

EPS 0.048 0.071

Oredo Telecommunication

Particulars 2017 2016

EPS 6.14 6.84

Conclusion: From the above table it has been examined following points:

Oman’s Earning per share is $ 0.048 cents in 2017 whereas in 2016 financial

year it was $ 0.071 cents which shows that company’s profitability position in

2017 is not sound because the company has decreased its profit margin in

comparison to 2016.

Oredo’s Earning per share is $ 6.14 cents in 2017 whereas in 2016 financial

year EPS was $ 6.84 cents which signifies that the lower ratio in 2017 is not

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE 10

favourable because the company has decreased its profit margin in comparison

to 2016.

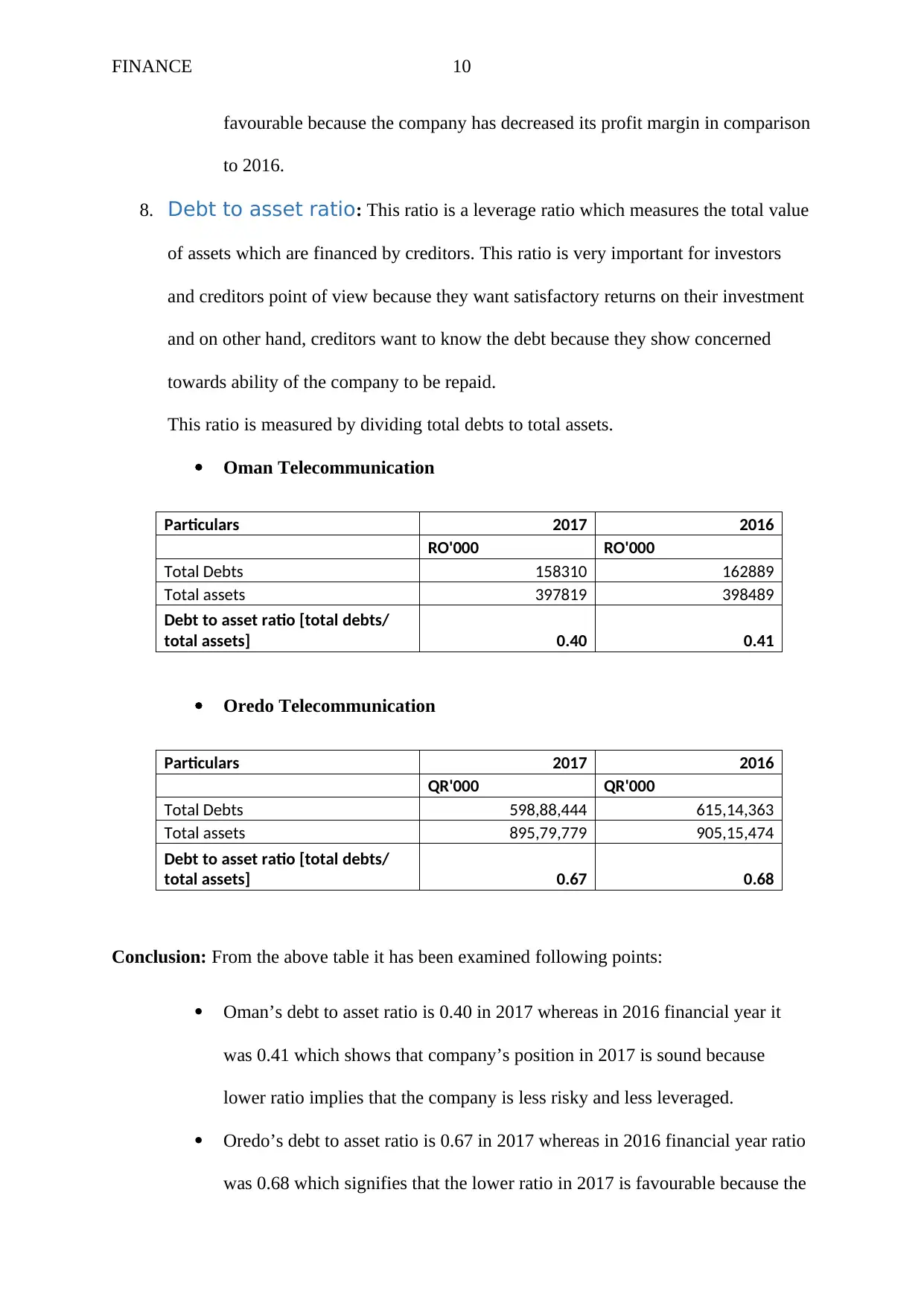

8. Debt to asset ratio: This ratio is a leverage ratio which measures the total value

of assets which are financed by creditors. This ratio is very important for investors

and creditors point of view because they want satisfactory returns on their investment

and on other hand, creditors want to know the debt because they show concerned

towards ability of the company to be repaid.

This ratio is measured by dividing total debts to total assets.

Oman Telecommunication

Particulars 2017 2016

RO'000 RO'000

Total Debts 158310 162889

Total assets 397819 398489

Debt to asset ratio [total debts/

total assets] 0.40 0.41

Oredo Telecommunication

Particulars 2017 2016

QR'000 QR'000

Total Debts 598,88,444 615,14,363

Total assets 895,79,779 905,15,474

Debt to asset ratio [total debts/

total assets] 0.67 0.68

Conclusion: From the above table it has been examined following points:

Oman’s debt to asset ratio is 0.40 in 2017 whereas in 2016 financial year it

was 0.41 which shows that company’s position in 2017 is sound because

lower ratio implies that the company is less risky and less leveraged.

Oredo’s debt to asset ratio is 0.67 in 2017 whereas in 2016 financial year ratio

was 0.68 which signifies that the lower ratio in 2017 is favourable because the

favourable because the company has decreased its profit margin in comparison

to 2016.

8. Debt to asset ratio: This ratio is a leverage ratio which measures the total value

of assets which are financed by creditors. This ratio is very important for investors

and creditors point of view because they want satisfactory returns on their investment

and on other hand, creditors want to know the debt because they show concerned

towards ability of the company to be repaid.

This ratio is measured by dividing total debts to total assets.

Oman Telecommunication

Particulars 2017 2016

RO'000 RO'000

Total Debts 158310 162889

Total assets 397819 398489

Debt to asset ratio [total debts/

total assets] 0.40 0.41

Oredo Telecommunication

Particulars 2017 2016

QR'000 QR'000

Total Debts 598,88,444 615,14,363

Total assets 895,79,779 905,15,474

Debt to asset ratio [total debts/

total assets] 0.67 0.68

Conclusion: From the above table it has been examined following points:

Oman’s debt to asset ratio is 0.40 in 2017 whereas in 2016 financial year it

was 0.41 which shows that company’s position in 2017 is sound because

lower ratio implies that the company is less risky and less leveraged.

Oredo’s debt to asset ratio is 0.67 in 2017 whereas in 2016 financial year ratio

was 0.68 which signifies that the lower ratio in 2017 is favourable because the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE 11

lower ratio implies that the company is less risky and less leveraged. Hence,

overall risk of the company is sound.

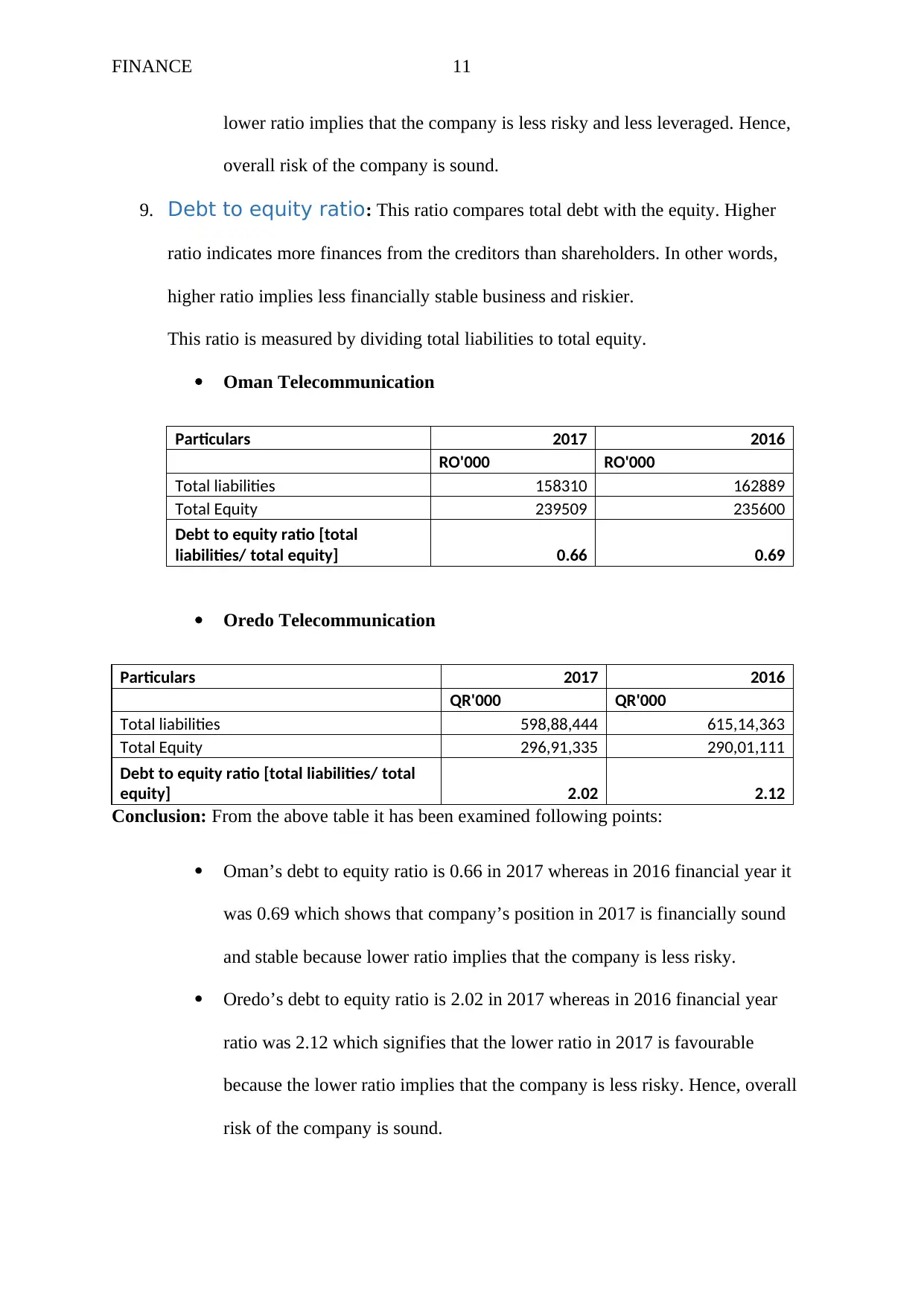

9. Debt to equity ratio: This ratio compares total debt with the equity. Higher

ratio indicates more finances from the creditors than shareholders. In other words,

higher ratio implies less financially stable business and riskier.

This ratio is measured by dividing total liabilities to total equity.

Oman Telecommunication

Particulars 2017 2016

RO'000 RO'000

Total liabilities 158310 162889

Total Equity 239509 235600

Debt to equity ratio [total

liabilities/ total equity] 0.66 0.69

Oredo Telecommunication

Particulars 2017 2016

QR'000 QR'000

Total liabilities 598,88,444 615,14,363

Total Equity 296,91,335 290,01,111

Debt to equity ratio [total liabilities/ total

equity] 2.02 2.12

Conclusion: From the above table it has been examined following points:

Oman’s debt to equity ratio is 0.66 in 2017 whereas in 2016 financial year it

was 0.69 which shows that company’s position in 2017 is financially sound

and stable because lower ratio implies that the company is less risky.

Oredo’s debt to equity ratio is 2.02 in 2017 whereas in 2016 financial year

ratio was 2.12 which signifies that the lower ratio in 2017 is favourable

because the lower ratio implies that the company is less risky. Hence, overall

risk of the company is sound.

lower ratio implies that the company is less risky and less leveraged. Hence,

overall risk of the company is sound.

9. Debt to equity ratio: This ratio compares total debt with the equity. Higher

ratio indicates more finances from the creditors than shareholders. In other words,

higher ratio implies less financially stable business and riskier.

This ratio is measured by dividing total liabilities to total equity.

Oman Telecommunication

Particulars 2017 2016

RO'000 RO'000

Total liabilities 158310 162889

Total Equity 239509 235600

Debt to equity ratio [total

liabilities/ total equity] 0.66 0.69

Oredo Telecommunication

Particulars 2017 2016

QR'000 QR'000

Total liabilities 598,88,444 615,14,363

Total Equity 296,91,335 290,01,111

Debt to equity ratio [total liabilities/ total

equity] 2.02 2.12

Conclusion: From the above table it has been examined following points:

Oman’s debt to equity ratio is 0.66 in 2017 whereas in 2016 financial year it

was 0.69 which shows that company’s position in 2017 is financially sound

and stable because lower ratio implies that the company is less risky.

Oredo’s debt to equity ratio is 2.02 in 2017 whereas in 2016 financial year

ratio was 2.12 which signifies that the lower ratio in 2017 is favourable

because the lower ratio implies that the company is less risky. Hence, overall

risk of the company is sound.

FINANCE 12

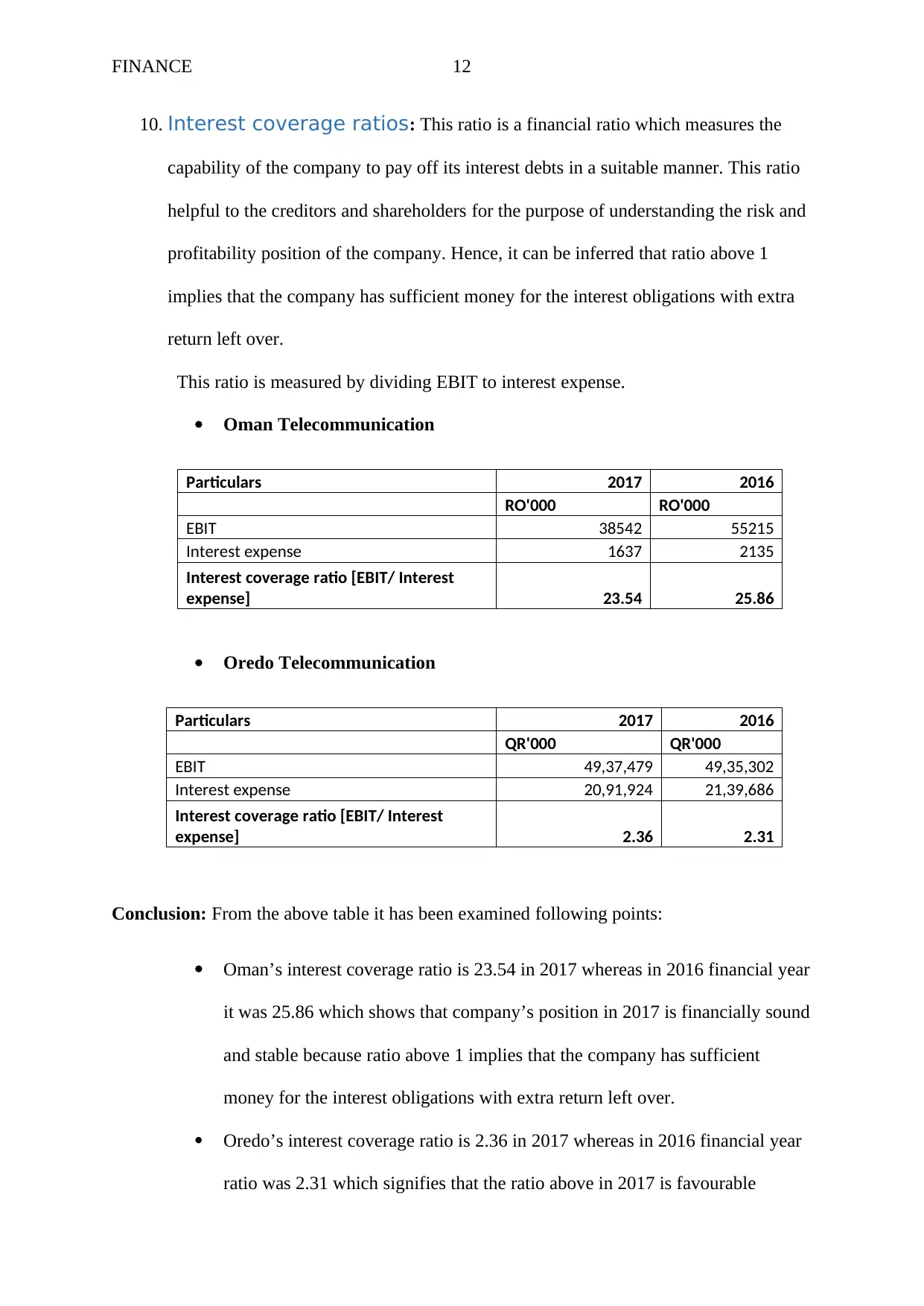

10. Interest coverage ratios: This ratio is a financial ratio which measures the

capability of the company to pay off its interest debts in a suitable manner. This ratio

helpful to the creditors and shareholders for the purpose of understanding the risk and

profitability position of the company. Hence, it can be inferred that ratio above 1

implies that the company has sufficient money for the interest obligations with extra

return left over.

This ratio is measured by dividing EBIT to interest expense.

Oman Telecommunication

Particulars 2017 2016

RO'000 RO'000

EBIT 38542 55215

Interest expense 1637 2135

Interest coverage ratio [EBIT/ Interest

expense] 23.54 25.86

Oredo Telecommunication

Particulars 2017 2016

QR'000 QR'000

EBIT 49,37,479 49,35,302

Interest expense 20,91,924 21,39,686

Interest coverage ratio [EBIT/ Interest

expense] 2.36 2.31

Conclusion: From the above table it has been examined following points:

Oman’s interest coverage ratio is 23.54 in 2017 whereas in 2016 financial year

it was 25.86 which shows that company’s position in 2017 is financially sound

and stable because ratio above 1 implies that the company has sufficient

money for the interest obligations with extra return left over.

Oredo’s interest coverage ratio is 2.36 in 2017 whereas in 2016 financial year

ratio was 2.31 which signifies that the ratio above in 2017 is favourable

10. Interest coverage ratios: This ratio is a financial ratio which measures the

capability of the company to pay off its interest debts in a suitable manner. This ratio

helpful to the creditors and shareholders for the purpose of understanding the risk and

profitability position of the company. Hence, it can be inferred that ratio above 1

implies that the company has sufficient money for the interest obligations with extra

return left over.

This ratio is measured by dividing EBIT to interest expense.

Oman Telecommunication

Particulars 2017 2016

RO'000 RO'000

EBIT 38542 55215

Interest expense 1637 2135

Interest coverage ratio [EBIT/ Interest

expense] 23.54 25.86

Oredo Telecommunication

Particulars 2017 2016

QR'000 QR'000

EBIT 49,37,479 49,35,302

Interest expense 20,91,924 21,39,686

Interest coverage ratio [EBIT/ Interest

expense] 2.36 2.31

Conclusion: From the above table it has been examined following points:

Oman’s interest coverage ratio is 23.54 in 2017 whereas in 2016 financial year

it was 25.86 which shows that company’s position in 2017 is financially sound

and stable because ratio above 1 implies that the company has sufficient

money for the interest obligations with extra return left over.

Oredo’s interest coverage ratio is 2.36 in 2017 whereas in 2016 financial year

ratio was 2.31 which signifies that the ratio above in 2017 is favourable

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.