Financial Performance Analysis of Chef One (2017-2018): A Report

VerifiedAdded on 2022/11/26

|7

|1704

|150

Report

AI Summary

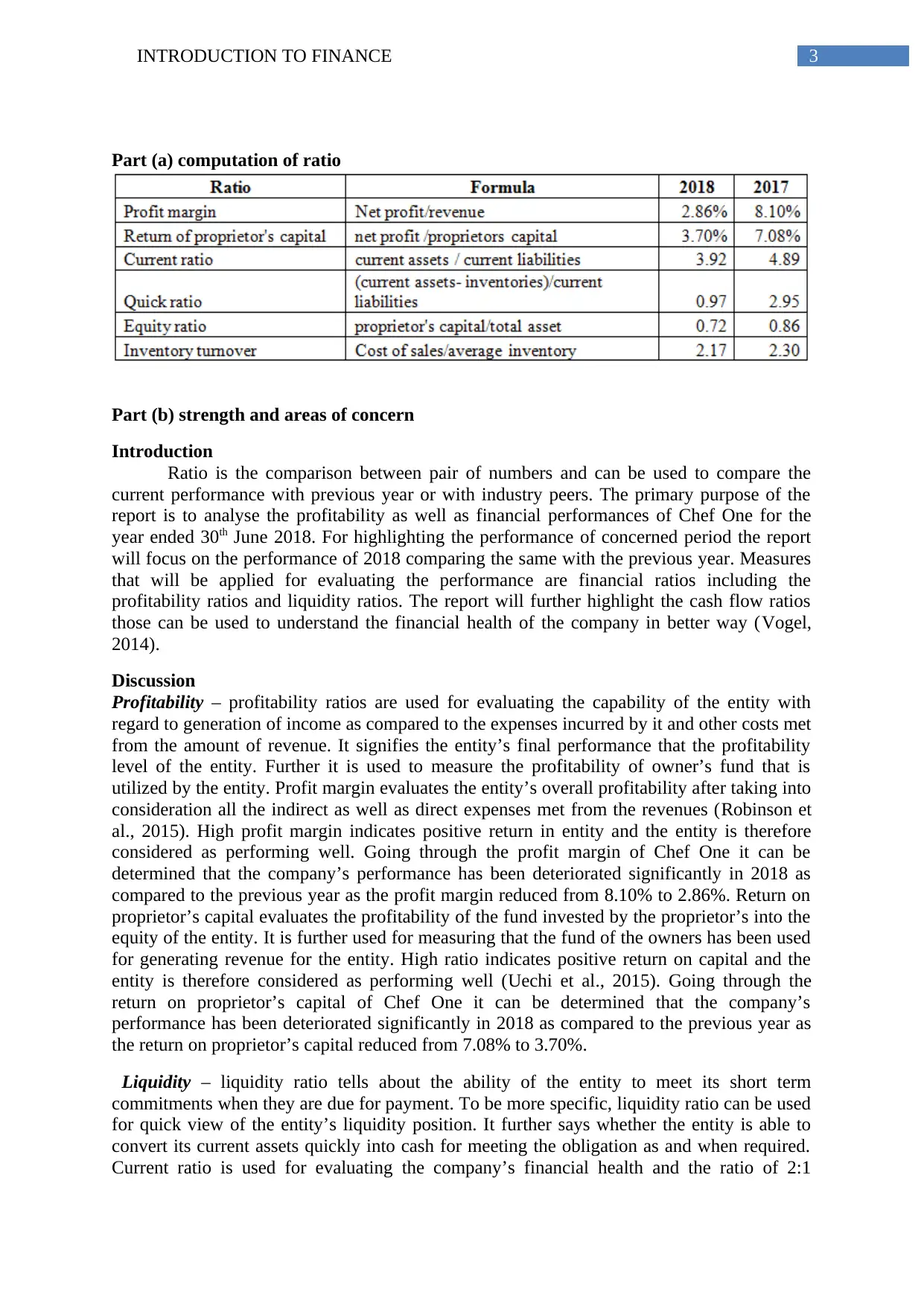

This report provides a comprehensive financial analysis of Chef One, examining its performance for the year ended June 30, 2018, compared to the previous year. The analysis utilizes various financial ratios, including profitability ratios (profit margin, return on proprietor’s capital), liquidity ratios (current ratio, quick ratio), and stability ratios (equity ratio, inventory turnover). The report identifies both strengths and weaknesses, highlighting a decline in profitability, liquidity, and stability in 2018, with areas of concern including increased costs, negative cash balance, and increased debt financing. The report concludes with recommendations for improvement, such as enhancing cash position and minimizing expenses. The report also discusses cash flow ratios that can be used to understand the financial health of the company. The analysis is based on the financial data provided in the assignment brief, and it aims to provide insights into the financial health and performance of Chef One.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.