Corporate Accounting Report: ACC00713, S1 2019, Financial Analysis

VerifiedAdded on 2022/11/13

|12

|2464

|66

Report

AI Summary

This report provides a comprehensive analysis of corporate accounting principles, specifically focusing on the application of AASB 15 (Revenue from Contracts with Customers) and its implications for financial reporting. The report is divided into two main parts. Part A delves into the requirements of revenue recognition and measurement under AASB 15, discussing the changes introduced by the standard and their impact on businesses. Part B assesses the financial performance of Reckon Ltd, a software company, through the analysis of key financial ratios. The report examines profitability, efficiency, and liquidity ratios, comparing the financial performance of Reckon Ltd over two years (2017 and 2018). The analysis includes calculations and interpretations of various ratios such as net profit margin, return on equity, return on assets, total asset turnover, inventory turnover, debtor turnover, current ratio, liquid ratio, and gearing ratio. The report concludes by summarizing the key findings and emphasizing the importance of financial ratio analysis in making informed business decisions.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CORPORATE ACCOUNTING

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................3

Part A...........................................................................................................................................3

Recognition of Revenue..............................................................................................................3

Measurement of Revenue............................................................................................................4

Part B...........................................................................................................................................5

Analysis of Key Financial Ratios................................................................................................6

Conclusion.......................................................................................................................................8

Reference.........................................................................................................................................9

CORPORATE ACCOUNTING

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................3

Part A...........................................................................................................................................3

Recognition of Revenue..............................................................................................................3

Measurement of Revenue............................................................................................................4

Part B...........................................................................................................................................5

Analysis of Key Financial Ratios................................................................................................6

Conclusion.......................................................................................................................................8

Reference.........................................................................................................................................9

2

CORPORATE ACCOUNTING

Introduction

The assessment which is being considered in this assessment is subdivided into two parts

which is Part a and Part b. The first part of the assessment deals with the accounting treatment

which is associated with the revenue which is generated from a contract. The assessment would

be discussing the revenue recognition requirements according to the provisions of the AASB

115. The assessment would be assessing the requirements of the standards for the purpose of

recognition of revenue of the business (Pro Bono Australia. 2019). In the second part of the

assessment, financial performance of the business would be assessed for Reckon Ltd. In order to

assess the financial performance of the business, key financial ratios of the business are

computed considering the financial statements of the business for the current year (Asx.com.au.

2019). The performance of the business would be depending on the ratios of the business.

The regulatory framework which is followed by the management of the company are

appropriate as the same is consistent with the conceptual framework which is used for the

purpose of reporting different items in the financial statements of the business. The case shows

the recognition and measurement criteria which is followed by businesses in case the business is

engaged in generation of revenue from contracts.

Discussion

Part A

Recognition of Revenue

The introduction of AASB 15 has replaced both AASB 118 Revenue and AASB 111

Construction contracts and appropriate provides significant provisions in order to make the

reporting framework which is followed by businesses more effective. The major changes which

CORPORATE ACCOUNTING

Introduction

The assessment which is being considered in this assessment is subdivided into two parts

which is Part a and Part b. The first part of the assessment deals with the accounting treatment

which is associated with the revenue which is generated from a contract. The assessment would

be discussing the revenue recognition requirements according to the provisions of the AASB

115. The assessment would be assessing the requirements of the standards for the purpose of

recognition of revenue of the business (Pro Bono Australia. 2019). In the second part of the

assessment, financial performance of the business would be assessed for Reckon Ltd. In order to

assess the financial performance of the business, key financial ratios of the business are

computed considering the financial statements of the business for the current year (Asx.com.au.

2019). The performance of the business would be depending on the ratios of the business.

The regulatory framework which is followed by the management of the company are

appropriate as the same is consistent with the conceptual framework which is used for the

purpose of reporting different items in the financial statements of the business. The case shows

the recognition and measurement criteria which is followed by businesses in case the business is

engaged in generation of revenue from contracts.

Discussion

Part A

Recognition of Revenue

The introduction of AASB 15 has replaced both AASB 118 Revenue and AASB 111

Construction contracts and appropriate provides significant provisions in order to make the

reporting framework which is followed by businesses more effective. The major changes which

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CORPORATE ACCOUNTING

has been made in the process of revenue recognition is to allocate revenue in accordance with the

satisfaction of the performance obligations of a contract (Wagenhofer 2014). In case of a

contracting business, the new standard requires businesses to effectively assess the performance

obligation of the contract, determine what values applies to each performance obligations and the

appropriately record the same as revenue in the financial records which is maintained in the

business.

As per the provisions of Para 31 of ASA 15, the entity of the business can recognize the

revenue when the entity satisfies a performance obligation of the business when the promised

good or services is transferred to the customer (Bloom and Kamm 2014). An asset would be

considered to be transferred when the customer obtains control over the usage of the asset

(Aasb.gov.au. 2019). Therefore, it can be reasonably stated that a revenue would be recognized

in a business if the performance obligation of a contract is satisfied or when the goods which was

promised has been transferred to the customers of the business (Yeaton 2015). In the case of

businesses which are engaged in performance of a long-term contract than the revenue can be

effectively be recognized when it can be appropriately be measured the revenue which can be

generated by the business. It is also to be noted that the costs which is incurred for the

completion of the project should also be recognized along side with the revenue which is

generated by the business (Srivastava 2014). The important consideration in this aspect is that

the revenue which is generated by the business must be appropriately measurable. As per the

provisions of Para 44 of AASB 15 an entity can appropriately recognize revenue from a

performance obligation, if the entity is satisfied that the business would be able to appropriately

measure the progress which is made by the business in terms of the contract which is provided

by the business (Aasb.gov.au. 2019).

CORPORATE ACCOUNTING

has been made in the process of revenue recognition is to allocate revenue in accordance with the

satisfaction of the performance obligations of a contract (Wagenhofer 2014). In case of a

contracting business, the new standard requires businesses to effectively assess the performance

obligation of the contract, determine what values applies to each performance obligations and the

appropriately record the same as revenue in the financial records which is maintained in the

business.

As per the provisions of Para 31 of ASA 15, the entity of the business can recognize the

revenue when the entity satisfies a performance obligation of the business when the promised

good or services is transferred to the customer (Bloom and Kamm 2014). An asset would be

considered to be transferred when the customer obtains control over the usage of the asset

(Aasb.gov.au. 2019). Therefore, it can be reasonably stated that a revenue would be recognized

in a business if the performance obligation of a contract is satisfied or when the goods which was

promised has been transferred to the customers of the business (Yeaton 2015). In the case of

businesses which are engaged in performance of a long-term contract than the revenue can be

effectively be recognized when it can be appropriately be measured the revenue which can be

generated by the business. It is also to be noted that the costs which is incurred for the

completion of the project should also be recognized along side with the revenue which is

generated by the business (Srivastava 2014). The important consideration in this aspect is that

the revenue which is generated by the business must be appropriately measurable. As per the

provisions of Para 44 of AASB 15 an entity can appropriately recognize revenue from a

performance obligation, if the entity is satisfied that the business would be able to appropriately

measure the progress which is made by the business in terms of the contract which is provided

by the business (Aasb.gov.au. 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CORPORATE ACCOUNTING

Measurement of Revenue

The provisions of Para 46 of AASB 15 states that when the performance obligation of the

business would be satisfied then the entity needs to recognize the revenue which the transaction

price which is allocated to the performance obligation. In addition to this, the provisions of Para

47 of AASB 15 further provides that the business would be considering the term of contract and

customary practices of the business to determine the transaction prices of the contract

(Aasb.gov.au. 2019). It is to be further notes that the transaction price which is being considered

by the entity may comprises of fixed amounts, variable amounts or both and the same would be

depending on the nature of the contract which is made by the management of the company

(Barker and McGeachin 2013). This shows that the management of the company plays a vital

role in measuring the revenue which is generated by the business during the period.

The standard also provides for appropriate disclosures which needs to be presented in the

financial statement of the business so that the management of the company is able to

appropriately disclose information regarding the nature, amount, timing and uncertainty of

revenue and cash flows arising from contracts with customers (McCarthy and McCarthy 2014).

The standard also requires the management to provide for appropriate disclosures regarding the

contracts which is undertaken by the business and also different judgements which is considered

by the management of the company.

Part B

This part would be analyzing the financial performance of the business of Reckno Ltd

which is considered for this assessment. Reckon ltd is a computer software company which

provides accounting software which can be used for the purpose of reporting and also for

maintaining appropriate books of accounts of the business. The business of Reckon provides

CORPORATE ACCOUNTING

Measurement of Revenue

The provisions of Para 46 of AASB 15 states that when the performance obligation of the

business would be satisfied then the entity needs to recognize the revenue which the transaction

price which is allocated to the performance obligation. In addition to this, the provisions of Para

47 of AASB 15 further provides that the business would be considering the term of contract and

customary practices of the business to determine the transaction prices of the contract

(Aasb.gov.au. 2019). It is to be further notes that the transaction price which is being considered

by the entity may comprises of fixed amounts, variable amounts or both and the same would be

depending on the nature of the contract which is made by the management of the company

(Barker and McGeachin 2013). This shows that the management of the company plays a vital

role in measuring the revenue which is generated by the business during the period.

The standard also provides for appropriate disclosures which needs to be presented in the

financial statement of the business so that the management of the company is able to

appropriately disclose information regarding the nature, amount, timing and uncertainty of

revenue and cash flows arising from contracts with customers (McCarthy and McCarthy 2014).

The standard also requires the management to provide for appropriate disclosures regarding the

contracts which is undertaken by the business and also different judgements which is considered

by the management of the company.

Part B

This part would be analyzing the financial performance of the business of Reckno Ltd

which is considered for this assessment. Reckon ltd is a computer software company which

provides accounting software which can be used for the purpose of reporting and also for

maintaining appropriate books of accounts of the business. The business of Reckon provides

5

CORPORATE ACCOUNTING

appropriate accounting solutions to the different entities which are looking to switch to

computerized accounting settings in the business.

If the management of the company adopts AASB 15, the business would be able to

appropriately report on the contract agreements which is entered into by the business for

software development of different entities (Aasb.gov.au. 2019). The new standards would

require the management to recognize revenue for the period on the basis of satisfaction of the

performance obligation of the business. The new standard would definitely enhance the

efficiency in the reporting framework which is followed by the business. The new standard

would also provide appropriate disclosures regarding the business and provide a clear

understanding regarding the revenue recognition policies which is followed by the management

of the company.

Analysis of Key Financial Ratios

The ratios of the business are considered to be important estimates which help the

management of the company take major decisions regarding the operations of the business. The

ratios of the business ate considered to be important as the same helps the management to

identify the trends in the business and on the basis of the same take appropriate decisions

regarding the operations of the business (Babalola and Abiola 2013). The ratios of the company

also demonstrate whether the financial position of the business is appropriate and effectively

formulate strategies for the purpose of enhancing the revenue which is to be generated by the

business.

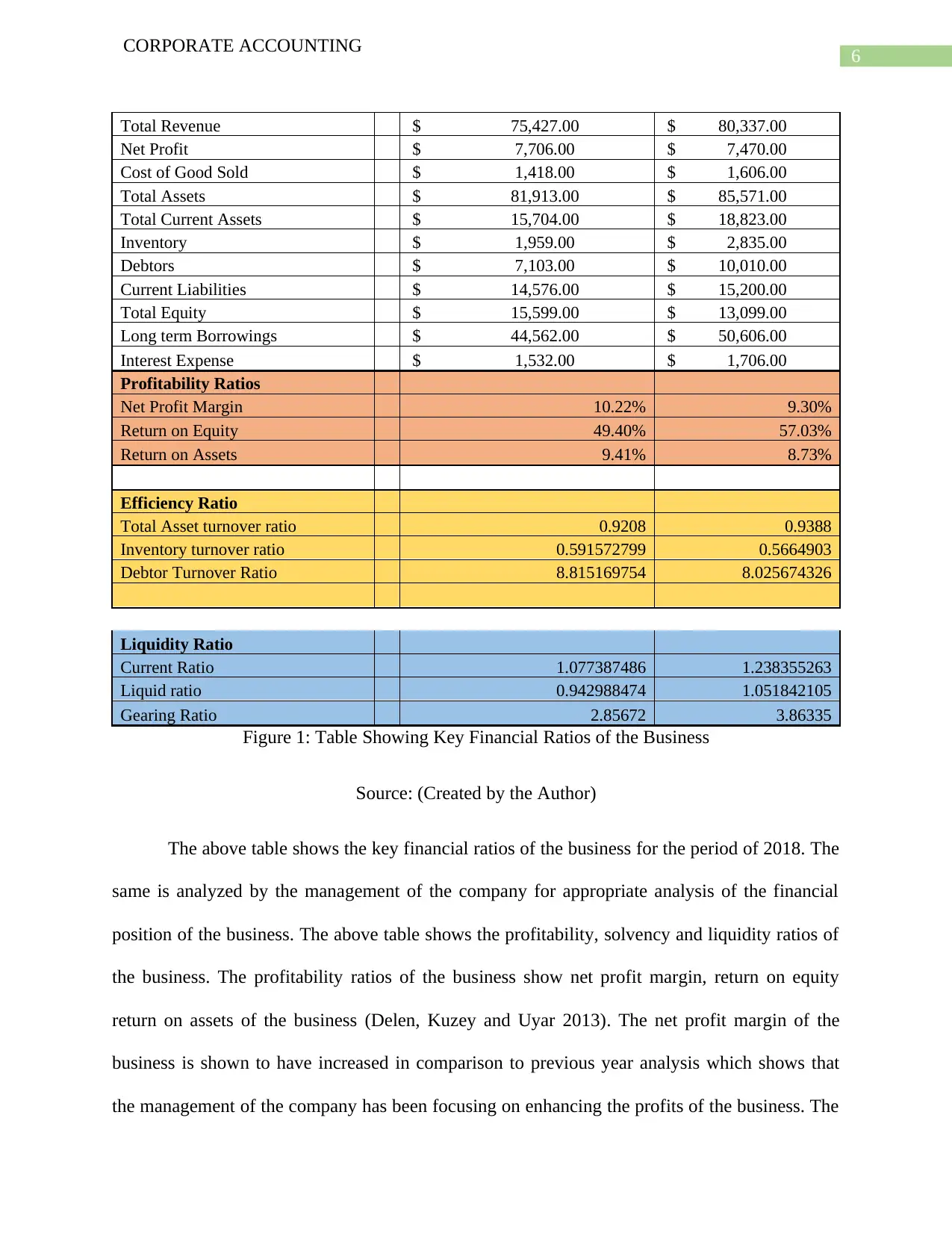

Key Financial Ratios of the Business

Reckon ltd

Particulars 2018 2017

$*000 $*000

CORPORATE ACCOUNTING

appropriate accounting solutions to the different entities which are looking to switch to

computerized accounting settings in the business.

If the management of the company adopts AASB 15, the business would be able to

appropriately report on the contract agreements which is entered into by the business for

software development of different entities (Aasb.gov.au. 2019). The new standards would

require the management to recognize revenue for the period on the basis of satisfaction of the

performance obligation of the business. The new standard would definitely enhance the

efficiency in the reporting framework which is followed by the business. The new standard

would also provide appropriate disclosures regarding the business and provide a clear

understanding regarding the revenue recognition policies which is followed by the management

of the company.

Analysis of Key Financial Ratios

The ratios of the business are considered to be important estimates which help the

management of the company take major decisions regarding the operations of the business. The

ratios of the business ate considered to be important as the same helps the management to

identify the trends in the business and on the basis of the same take appropriate decisions

regarding the operations of the business (Babalola and Abiola 2013). The ratios of the company

also demonstrate whether the financial position of the business is appropriate and effectively

formulate strategies for the purpose of enhancing the revenue which is to be generated by the

business.

Key Financial Ratios of the Business

Reckon ltd

Particulars 2018 2017

$*000 $*000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CORPORATE ACCOUNTING

Total Revenue $ 75,427.00 $ 80,337.00

Net Profit $ 7,706.00 $ 7,470.00

Cost of Good Sold $ 1,418.00 $ 1,606.00

Total Assets $ 81,913.00 $ 85,571.00

Total Current Assets $ 15,704.00 $ 18,823.00

Inventory $ 1,959.00 $ 2,835.00

Debtors $ 7,103.00 $ 10,010.00

Current Liabilities $ 14,576.00 $ 15,200.00

Total Equity $ 15,599.00 $ 13,099.00

Long term Borrowings $ 44,562.00 $ 50,606.00

Interest Expense $ 1,532.00 $ 1,706.00

Profitability Ratios

Net Profit Margin 10.22% 9.30%

Return on Equity 49.40% 57.03%

Return on Assets 9.41% 8.73%

Efficiency Ratio

Total Asset turnover ratio 0.9208 0.9388

Inventory turnover ratio 0.591572799 0.5664903

Debtor Turnover Ratio 8.815169754 8.025674326

Liquidity Ratio

Current Ratio 1.077387486 1.238355263

Liquid ratio 0.942988474 1.051842105

Gearing Ratio 2.85672 3.86335

Figure 1: Table Showing Key Financial Ratios of the Business

Source: (Created by the Author)

The above table shows the key financial ratios of the business for the period of 2018. The

same is analyzed by the management of the company for appropriate analysis of the financial

position of the business. The above table shows the profitability, solvency and liquidity ratios of

the business. The profitability ratios of the business show net profit margin, return on equity

return on assets of the business (Delen, Kuzey and Uyar 2013). The net profit margin of the

business is shown to have increased in comparison to previous year analysis which shows that

the management of the company has been focusing on enhancing the profits of the business. The

CORPORATE ACCOUNTING

Total Revenue $ 75,427.00 $ 80,337.00

Net Profit $ 7,706.00 $ 7,470.00

Cost of Good Sold $ 1,418.00 $ 1,606.00

Total Assets $ 81,913.00 $ 85,571.00

Total Current Assets $ 15,704.00 $ 18,823.00

Inventory $ 1,959.00 $ 2,835.00

Debtors $ 7,103.00 $ 10,010.00

Current Liabilities $ 14,576.00 $ 15,200.00

Total Equity $ 15,599.00 $ 13,099.00

Long term Borrowings $ 44,562.00 $ 50,606.00

Interest Expense $ 1,532.00 $ 1,706.00

Profitability Ratios

Net Profit Margin 10.22% 9.30%

Return on Equity 49.40% 57.03%

Return on Assets 9.41% 8.73%

Efficiency Ratio

Total Asset turnover ratio 0.9208 0.9388

Inventory turnover ratio 0.591572799 0.5664903

Debtor Turnover Ratio 8.815169754 8.025674326

Liquidity Ratio

Current Ratio 1.077387486 1.238355263

Liquid ratio 0.942988474 1.051842105

Gearing Ratio 2.85672 3.86335

Figure 1: Table Showing Key Financial Ratios of the Business

Source: (Created by the Author)

The above table shows the key financial ratios of the business for the period of 2018. The

same is analyzed by the management of the company for appropriate analysis of the financial

position of the business. The above table shows the profitability, solvency and liquidity ratios of

the business. The profitability ratios of the business show net profit margin, return on equity

return on assets of the business (Delen, Kuzey and Uyar 2013). The net profit margin of the

business is shown to have increased in comparison to previous year analysis which shows that

the management of the company has been focusing on enhancing the profits of the business. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE ACCOUNTING

increase in the profits of the business I mainly due to decrease in the costs of the business which

automatically enhances the profits of the business. The return on equity shows a decline which is

an indicator that the management is not meeting the expectations of the shareholders or in other

words not declaring appropriate dividends according to the profits which is generated by the

business. On the other hand, the return on asset estimate is shown to have increased from

previous year which is a clear sign that the management of the company is appropriately utilizing

the assets of the business for the purpose of generating appropriate revenue for the business.

The efficiency ratio of the business comprises of inventory turnover ratio, debtor turnover

ratio and asset turnover ratio. The inventory and debtor turnover ratio of the business shows that

the management of the company has effectively made changes in the both the policies as the

estimates which is computed for 2018 shows significant improvements (Edmonds et al. 2013).

This shows that the management of the company is trying to maintain its efficiency in

operational process of the business.

The net ratio which is computed in the table above is liquidity ratios of the business

which are considered to be indicators of whether the business is successful or not. The analysis

of yje current ratio of the business suggest that the management of the company is trying to make

improvements in the liquidity position of the business. The current ratio of the business is shown

to have increased which is a favorable sign for the management of the company. The gearing

ratio of the business is shown to have reduced significantly which is mainly due to the efforts of

the business to reduce the debts of the business. This also means that the management of the

company is trying to reduce the overall risks which is associated with use of debt capital in the

business.

CORPORATE ACCOUNTING

increase in the profits of the business I mainly due to decrease in the costs of the business which

automatically enhances the profits of the business. The return on equity shows a decline which is

an indicator that the management is not meeting the expectations of the shareholders or in other

words not declaring appropriate dividends according to the profits which is generated by the

business. On the other hand, the return on asset estimate is shown to have increased from

previous year which is a clear sign that the management of the company is appropriately utilizing

the assets of the business for the purpose of generating appropriate revenue for the business.

The efficiency ratio of the business comprises of inventory turnover ratio, debtor turnover

ratio and asset turnover ratio. The inventory and debtor turnover ratio of the business shows that

the management of the company has effectively made changes in the both the policies as the

estimates which is computed for 2018 shows significant improvements (Edmonds et al. 2013).

This shows that the management of the company is trying to maintain its efficiency in

operational process of the business.

The net ratio which is computed in the table above is liquidity ratios of the business

which are considered to be indicators of whether the business is successful or not. The analysis

of yje current ratio of the business suggest that the management of the company is trying to make

improvements in the liquidity position of the business. The current ratio of the business is shown

to have increased which is a favorable sign for the management of the company. The gearing

ratio of the business is shown to have reduced significantly which is mainly due to the efforts of

the business to reduce the debts of the business. This also means that the management of the

company is trying to reduce the overall risks which is associated with use of debt capital in the

business.

8

CORPORATE ACCOUNTING

The financial information which is available to the management of the company can be

used by the management of the company to take appropriate decisions regarding the business and

also helps the management to forecast the future activities of the business.

Conclusion

The above discussion effectively shows the changes which have brought about in the

revenue recognition principle by the introduction of the new standard which is AASB 15. The

new standard replaces AASB 118 and AASB 111 and the same helps in appropriate disclosures

which is to be provided by the business. The first part deals with revenue recognition and

measurement of revenue principles which is stated in AASB 15. The second part deals with

performance of the business of Reckon Ltd which is a software-based company. The financial

performance of the business is evaluated on the basis of key financial ratios of the business

which is effectively computed and analysed in the above discussion.

CORPORATE ACCOUNTING

The financial information which is available to the management of the company can be

used by the management of the company to take appropriate decisions regarding the business and

also helps the management to forecast the future activities of the business.

Conclusion

The above discussion effectively shows the changes which have brought about in the

revenue recognition principle by the introduction of the new standard which is AASB 15. The

new standard replaces AASB 118 and AASB 111 and the same helps in appropriate disclosures

which is to be provided by the business. The first part deals with revenue recognition and

measurement of revenue principles which is stated in AASB 15. The second part deals with

performance of the business of Reckon Ltd which is a software-based company. The financial

performance of the business is evaluated on the basis of key financial ratios of the business

which is effectively computed and analysed in the above discussion.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CORPORATE ACCOUNTING

Reference

Aasb.gov.au. (2019). [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB15_12-14.pdf [Accessed 24 May

2019].

Aasb.gov.au. (2019). [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB118_07-04_COMPoct10_01-11.pdf

[Accessed 24 May 2019].

Asx.com.au. (2019). [online] Available at:

https://www.asx.com.au/asx/share-price-research/company/RKN [Accessed 24 May 2019].

Babalola, Y.A. and Abiola, F.R., 2013. Financial ratio analysis of firms: A tool for decision

making. International journal of management sciences, 1(4), pp.132-137.

Barker, R. and McGeachin, A., 2013. Why is there inconsistency in accounting for liabilities in

IFRS? An analysis of recognition, measurement, estimation and conservatism. Accounting and

Business Research, 43(6), pp.579-604.

Bloom, R. and Kamm, J., 2014. Revenue recognition: how we got here and where it will take

us. Financial Executive, 30(3), pp.48-53.

CORPORATE ACCOUNTING

Reference

Aasb.gov.au. (2019). [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB15_12-14.pdf [Accessed 24 May

2019].

Aasb.gov.au. (2019). [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB118_07-04_COMPoct10_01-11.pdf

[Accessed 24 May 2019].

Asx.com.au. (2019). [online] Available at:

https://www.asx.com.au/asx/share-price-research/company/RKN [Accessed 24 May 2019].

Babalola, Y.A. and Abiola, F.R., 2013. Financial ratio analysis of firms: A tool for decision

making. International journal of management sciences, 1(4), pp.132-137.

Barker, R. and McGeachin, A., 2013. Why is there inconsistency in accounting for liabilities in

IFRS? An analysis of recognition, measurement, estimation and conservatism. Accounting and

Business Research, 43(6), pp.579-604.

Bloom, R. and Kamm, J., 2014. Revenue recognition: how we got here and where it will take

us. Financial Executive, 30(3), pp.48-53.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CORPORATE ACCOUNTING

Delen, D., Kuzey, C. and Uyar, A., 2013. Measuring firm performance using financial ratios: A

decision tree approach. Expert Systems with Applications, 40(10), pp.3970-3983.

Edmonds, T.P., McNair, F.M., Olds, P.R. and Milam, E.E., 2013. Fundamental financial

accounting concepts. New York, NY: McGraw-Hill Irwin.

McCarthy, M. and McCarthy, R., 2014. Financial statement preparers' revenue decisions:

Accuracy in applying rules-based standards and the IASB-FASB revenue recognition

model. Journal of Accounting and Finance, 14(6), p.21.

Pro Bono Australia. (2019). Impact of Accounting Standard Changes in Recognition of Revenue

| PBA. [online] Available at: https://probonoaustralia.com.au/news/2017/07/impact-accounting-

standard-changes-recognition-revenue/ [Accessed 24 May 2019].

Srivastava, A., 2014. Selling-price estimates in revenue recognition and the usefulness of

financial statements. Review of Accounting Studies, 19(2), pp.661-697.

Wagenhofer, A., 2014. The role of revenue recognition in performance reporting. Accounting

and Business Research, 44(4), pp.349-379.

Yeaton, K., 2015. A new world of revenue recognition: revenue from contracts with customers.

The CPA Journal, 85(7), p.50.

CORPORATE ACCOUNTING

Delen, D., Kuzey, C. and Uyar, A., 2013. Measuring firm performance using financial ratios: A

decision tree approach. Expert Systems with Applications, 40(10), pp.3970-3983.

Edmonds, T.P., McNair, F.M., Olds, P.R. and Milam, E.E., 2013. Fundamental financial

accounting concepts. New York, NY: McGraw-Hill Irwin.

McCarthy, M. and McCarthy, R., 2014. Financial statement preparers' revenue decisions:

Accuracy in applying rules-based standards and the IASB-FASB revenue recognition

model. Journal of Accounting and Finance, 14(6), p.21.

Pro Bono Australia. (2019). Impact of Accounting Standard Changes in Recognition of Revenue

| PBA. [online] Available at: https://probonoaustralia.com.au/news/2017/07/impact-accounting-

standard-changes-recognition-revenue/ [Accessed 24 May 2019].

Srivastava, A., 2014. Selling-price estimates in revenue recognition and the usefulness of

financial statements. Review of Accounting Studies, 19(2), pp.661-697.

Wagenhofer, A., 2014. The role of revenue recognition in performance reporting. Accounting

and Business Research, 44(4), pp.349-379.

Yeaton, K., 2015. A new world of revenue recognition: revenue from contracts with customers.

The CPA Journal, 85(7), p.50.

11

CORPORATE ACCOUNTING

CORPORATE ACCOUNTING

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.