Managerial Finance: Comparative Financial Ratio Analysis Report

VerifiedAdded on 2023/01/16

|20

|3987

|64

Report

AI Summary

This report provides a comprehensive analysis of managerial finance, focusing on the comparative financial performance of GlaxoSmithKline plc and Reckitt Benckiser Group plc. The analysis involves calculating and evaluating ten key financial ratios for the years 2017 and 2018, including current ratio, quick ratio, net profit margin, gross profit margin, gearing ratio, price-earning ratio, earnings per share, return on capital employed, average inventory turnover period, and dividend payout ratio. The report assesses the financial position, performance, and investment potential of both companies based on these ratios. Additionally, it discusses the limitations of financial ratios and investment appraisal techniques, and offers recommendations to improve the financial performance of the comparatively weaker company. The report concludes with an overview of the findings and includes a list of references.

Managerial Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK ..............................................................................................................................................1

PORTFOLIO 1.................................................................................................................................1

(a) Calculation of different financial ratios for two years (2017 – 2018):..................................1

c. Recommendation in order to improve the poorly performing business..................................4

d. Limitation of financial ratios...................................................................................................5

PORTFOLIO 2.................................................................................................................................6

(a). Calculation of financial ratios for two years (2017 – 2018):................................................6

Payback Period:...........................................................................................................................6

b. Limitation of using investment appraisal technique.............................................................10

CONCLUSION..............................................................................................................................11

REFERENCES .............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK ..............................................................................................................................................1

PORTFOLIO 1.................................................................................................................................1

(a) Calculation of different financial ratios for two years (2017 – 2018):..................................1

c. Recommendation in order to improve the poorly performing business..................................4

d. Limitation of financial ratios...................................................................................................5

PORTFOLIO 2.................................................................................................................................6

(a). Calculation of financial ratios for two years (2017 – 2018):................................................6

Payback Period:...........................................................................................................................6

b. Limitation of using investment appraisal technique.............................................................10

CONCLUSION..............................................................................................................................11

REFERENCES .............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

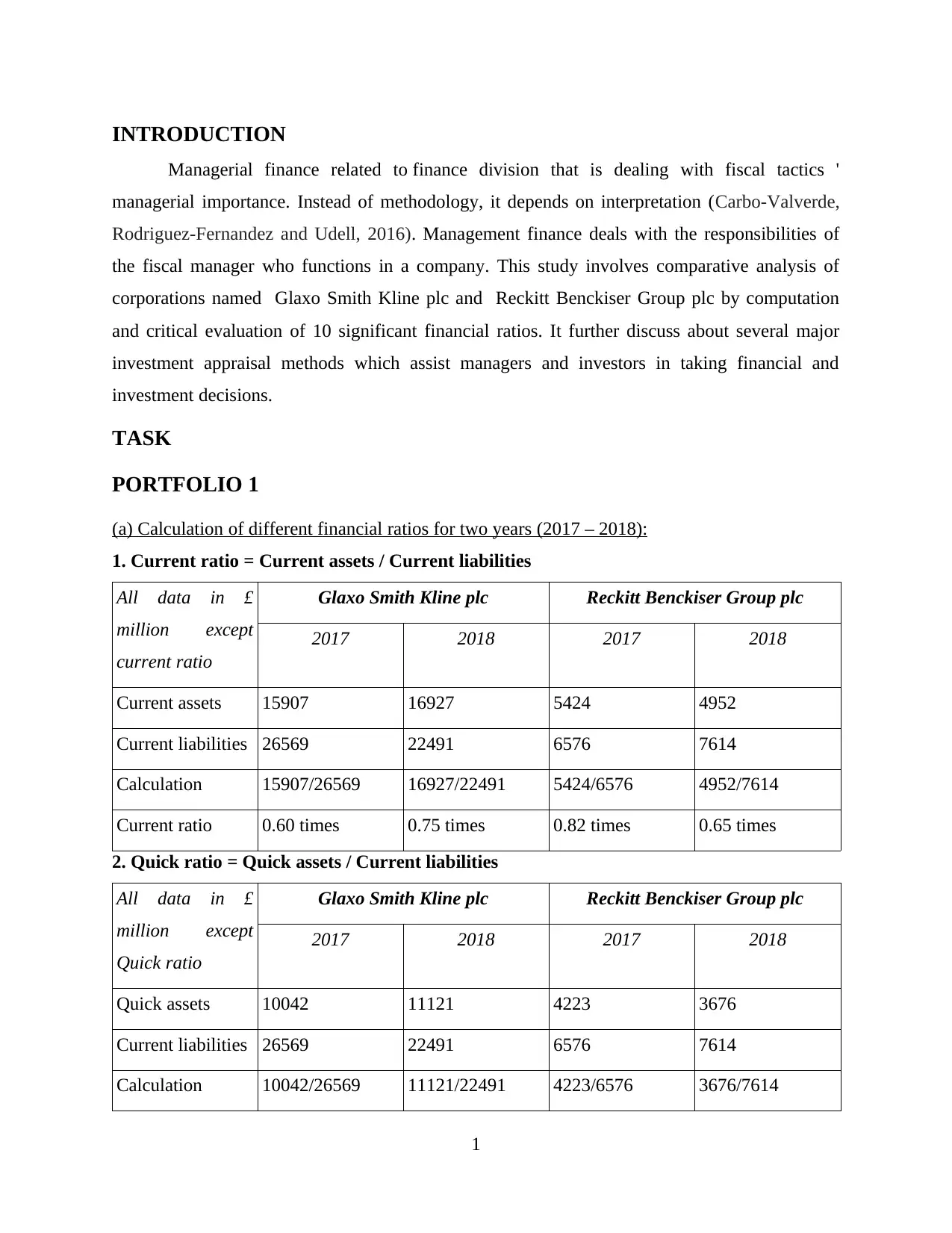

INTRODUCTION

Managerial finance related to finance division that is dealing with fiscal tactics '

managerial importance. Instead of methodology, it depends on interpretation (Carbo‐Valverde,

Rodriguez‐Fernandez and Udell, 2016). Management finance deals with the responsibilities of

the fiscal manager who functions in a company. This study involves comparative analysis of

corporations named Glaxo Smith Kline plc and Reckitt Benckiser Group plc by computation

and critical evaluation of 10 significant financial ratios. It further discuss about several major

investment appraisal methods which assist managers and investors in taking financial and

investment decisions.

TASK

PORTFOLIO 1

(a) Calculation of different financial ratios for two years (2017 – 2018):

1. Current ratio = Current assets / Current liabilities

All data in £

million except

current ratio

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Current assets 15907 16927 5424 4952

Current liabilities 26569 22491 6576 7614

Calculation 15907/26569 16927/22491 5424/6576 4952/7614

Current ratio 0.60 times 0.75 times 0.82 times 0.65 times

2. Quick ratio = Quick assets / Current liabilities

All data in £

million except

Quick ratio

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Quick assets 10042 11121 4223 3676

Current liabilities 26569 22491 6576 7614

Calculation 10042/26569 11121/22491 4223/6576 3676/7614

1

Managerial finance related to finance division that is dealing with fiscal tactics '

managerial importance. Instead of methodology, it depends on interpretation (Carbo‐Valverde,

Rodriguez‐Fernandez and Udell, 2016). Management finance deals with the responsibilities of

the fiscal manager who functions in a company. This study involves comparative analysis of

corporations named Glaxo Smith Kline plc and Reckitt Benckiser Group plc by computation

and critical evaluation of 10 significant financial ratios. It further discuss about several major

investment appraisal methods which assist managers and investors in taking financial and

investment decisions.

TASK

PORTFOLIO 1

(a) Calculation of different financial ratios for two years (2017 – 2018):

1. Current ratio = Current assets / Current liabilities

All data in £

million except

current ratio

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Current assets 15907 16927 5424 4952

Current liabilities 26569 22491 6576 7614

Calculation 15907/26569 16927/22491 5424/6576 4952/7614

Current ratio 0.60 times 0.75 times 0.82 times 0.65 times

2. Quick ratio = Quick assets / Current liabilities

All data in £

million except

Quick ratio

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Quick assets 10042 11121 4223 3676

Current liabilities 26569 22491 6576 7614

Calculation 10042/26569 11121/22491 4223/6576 3676/7614

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

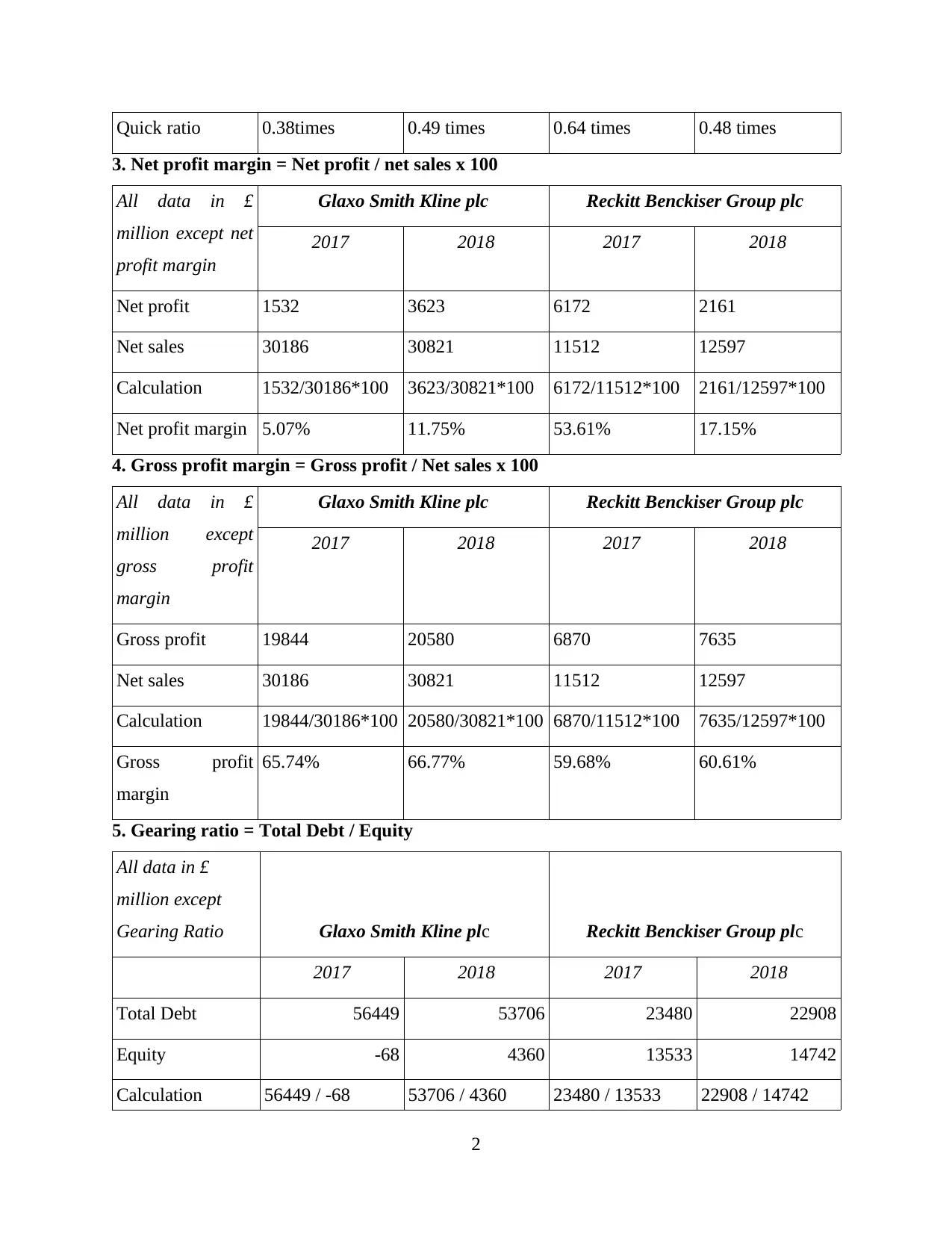

Quick ratio 0.38times 0.49 times 0.64 times 0.48 times

3. Net profit margin = Net profit / net sales x 100

All data in £

million except net

profit margin

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Net profit 1532 3623 6172 2161

Net sales 30186 30821 11512 12597

Calculation 1532/30186*100 3623/30821*100 6172/11512*100 2161/12597*100

Net profit margin 5.07% 11.75% 53.61% 17.15%

4. Gross profit margin = Gross profit / Net sales x 100

All data in £

million except

gross profit

margin

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Gross profit 19844 20580 6870 7635

Net sales 30186 30821 11512 12597

Calculation 19844/30186*100 20580/30821*100 6870/11512*100 7635/12597*100

Gross profit

margin

65.74% 66.77% 59.68% 60.61%

5. Gearing ratio = Total Debt / Equity

All data in £

million except

Gearing Ratio Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Total Debt 56449 53706 23480 22908

Equity -68 4360 13533 14742

Calculation 56449 / -68 53706 / 4360 23480 / 13533 22908 / 14742

2

3. Net profit margin = Net profit / net sales x 100

All data in £

million except net

profit margin

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Net profit 1532 3623 6172 2161

Net sales 30186 30821 11512 12597

Calculation 1532/30186*100 3623/30821*100 6172/11512*100 2161/12597*100

Net profit margin 5.07% 11.75% 53.61% 17.15%

4. Gross profit margin = Gross profit / Net sales x 100

All data in £

million except

gross profit

margin

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Gross profit 19844 20580 6870 7635

Net sales 30186 30821 11512 12597

Calculation 19844/30186*100 20580/30821*100 6870/11512*100 7635/12597*100

Gross profit

margin

65.74% 66.77% 59.68% 60.61%

5. Gearing ratio = Total Debt / Equity

All data in £

million except

Gearing Ratio Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Total Debt 56449 53706 23480 22908

Equity -68 4360 13533 14742

Calculation 56449 / -68 53706 / 4360 23480 / 13533 22908 / 14742

2

Gearing Ratio -830.13 12.32 1.74 1.55

6. Price earning ratio = Market Price Per Share / Earning Per Share

All data in £

million Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Market Price Per

Share 1361 1491.2 6841 5964

Earning Price Per

Share 0.3152 0.7455 8.3859 2.9361

Calculation 1361 / .3152 1491.2 / .7455 6841 / 8.3859 5964 / 2.9361

Price Earning Ratio 4317.89 2000.27 815.77 2031.26

7. Earning per share = Net Profit / Ordinary Numbers of Shares

All data in £ Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Net Profit 1532 3623 6172 2161

Ordinary Numbers

of Shares 4860 4860 736 736

Calculation 1532/4860 3623/4860 6172/736 2161/736

EPS 0.3152 0.7455 8.3859 2.9361

8. Return on capital employed = Operating profit (EBIT) / Capital employed *100

All data in £

million except

Return on capital

employed ratio

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

EBIT 6061 7064 2963 3280

Capital employed 29812 35575 30437 30036

3

6. Price earning ratio = Market Price Per Share / Earning Per Share

All data in £

million Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Market Price Per

Share 1361 1491.2 6841 5964

Earning Price Per

Share 0.3152 0.7455 8.3859 2.9361

Calculation 1361 / .3152 1491.2 / .7455 6841 / 8.3859 5964 / 2.9361

Price Earning Ratio 4317.89 2000.27 815.77 2031.26

7. Earning per share = Net Profit / Ordinary Numbers of Shares

All data in £ Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Net Profit 1532 3623 6172 2161

Ordinary Numbers

of Shares 4860 4860 736 736

Calculation 1532/4860 3623/4860 6172/736 2161/736

EPS 0.3152 0.7455 8.3859 2.9361

8. Return on capital employed = Operating profit (EBIT) / Capital employed *100

All data in £

million except

Return on capital

employed ratio

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

EBIT 6061 7064 2963 3280

Capital employed 29812 35575 30437 30036

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

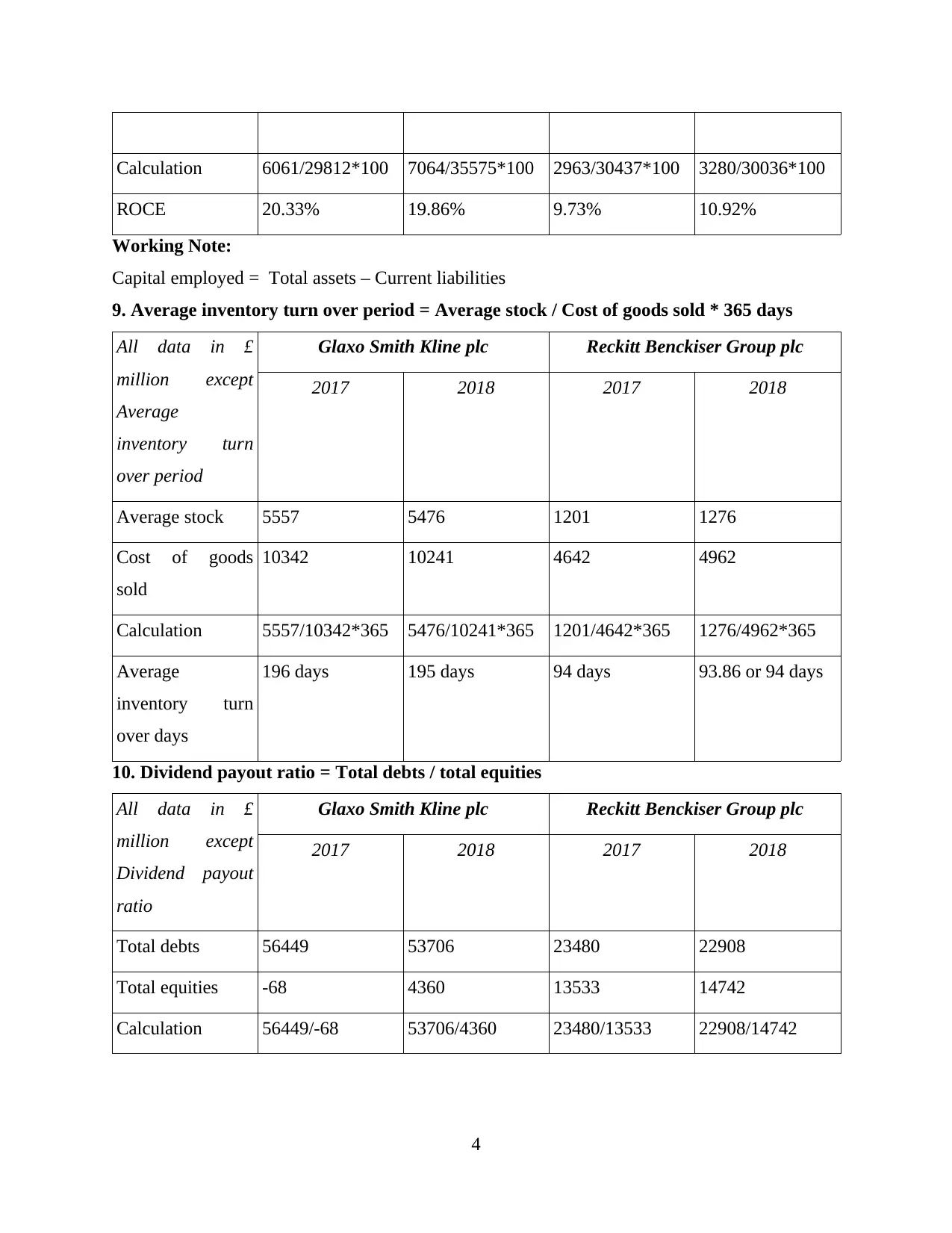

Calculation 6061/29812*100 7064/35575*100 2963/30437*100 3280/30036*100

ROCE 20.33% 19.86% 9.73% 10.92%

Working Note:

Capital employed = Total assets – Current liabilities

9. Average inventory turn over period = Average stock / Cost of goods sold * 365 days

All data in £

million except

Average

inventory turn

over period

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Average stock 5557 5476 1201 1276

Cost of goods

sold

10342 10241 4642 4962

Calculation 5557/10342*365 5476/10241*365 1201/4642*365 1276/4962*365

Average

inventory turn

over days

196 days 195 days 94 days 93.86 or 94 days

10. Dividend payout ratio = Total debts / total equities

All data in £

million except

Dividend payout

ratio

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Total debts 56449 53706 23480 22908

Total equities -68 4360 13533 14742

Calculation 56449/-68 53706/4360 23480/13533 22908/14742

4

ROCE 20.33% 19.86% 9.73% 10.92%

Working Note:

Capital employed = Total assets – Current liabilities

9. Average inventory turn over period = Average stock / Cost of goods sold * 365 days

All data in £

million except

Average

inventory turn

over period

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Average stock 5557 5476 1201 1276

Cost of goods

sold

10342 10241 4642 4962

Calculation 5557/10342*365 5476/10241*365 1201/4642*365 1276/4962*365

Average

inventory turn

over days

196 days 195 days 94 days 93.86 or 94 days

10. Dividend payout ratio = Total debts / total equities

All data in £

million except

Dividend payout

ratio

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Total debts 56449 53706 23480 22908

Total equities -68 4360 13533 14742

Calculation 56449/-68 53706/4360 23480/13533 22908/14742

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Dividend payout

ratio

-830.13 12.31 1.73 1.55

(b) Evaluation of performance, financial position and investment potential.

1. Current ratio

2017 (in times) 2018 (in times)

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0.6

0.75

0.82 0.85

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

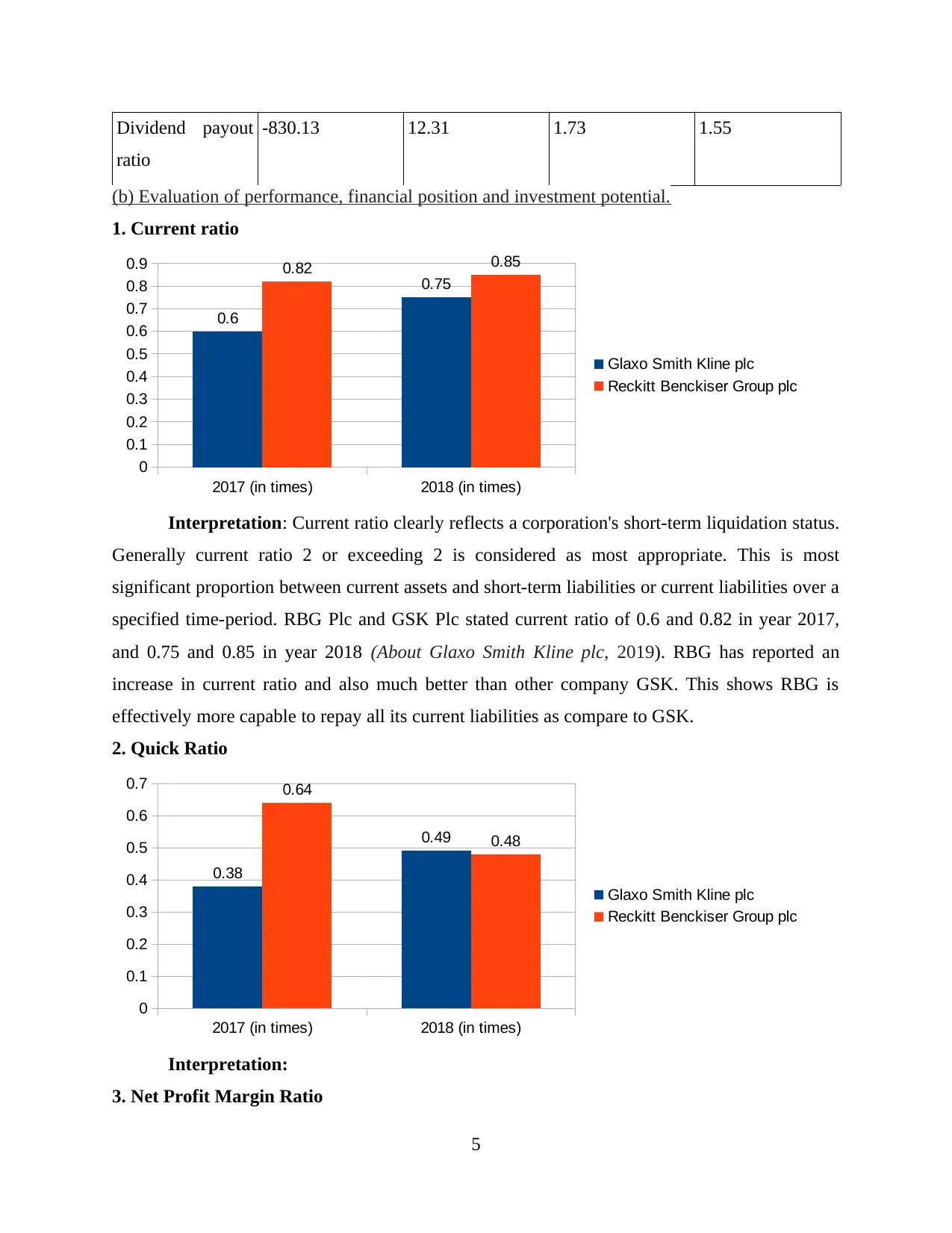

Interpretation: Current ratio clearly reflects a corporation's short-term liquidation status.

Generally current ratio 2 or exceeding 2 is considered as most appropriate. This is most

significant proportion between current assets and short-term liabilities or current liabilities over a

specified time-period. RBG Plc and GSK Plc stated current ratio of 0.6 and 0.82 in year 2017,

and 0.75 and 0.85 in year 2018 (About Glaxo Smith Kline plc, 2019). RBG has reported an

increase in current ratio and also much better than other company GSK. This shows RBG is

effectively more capable to repay all its current liabilities as compare to GSK.

2. Quick Ratio

2017 (in times) 2018 (in times)

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.38

0.49

0.64

0.48

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

Interpretation:

3. Net Profit Margin Ratio

5

ratio

-830.13 12.31 1.73 1.55

(b) Evaluation of performance, financial position and investment potential.

1. Current ratio

2017 (in times) 2018 (in times)

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0.6

0.75

0.82 0.85

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

Interpretation: Current ratio clearly reflects a corporation's short-term liquidation status.

Generally current ratio 2 or exceeding 2 is considered as most appropriate. This is most

significant proportion between current assets and short-term liabilities or current liabilities over a

specified time-period. RBG Plc and GSK Plc stated current ratio of 0.6 and 0.82 in year 2017,

and 0.75 and 0.85 in year 2018 (About Glaxo Smith Kline plc, 2019). RBG has reported an

increase in current ratio and also much better than other company GSK. This shows RBG is

effectively more capable to repay all its current liabilities as compare to GSK.

2. Quick Ratio

2017 (in times) 2018 (in times)

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.38

0.49

0.64

0.48

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

Interpretation:

3. Net Profit Margin Ratio

5

2017 (in %) 2018 (in %)

0

10

20

30

40

50

60

5.07

11.75

53.61

17.15

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

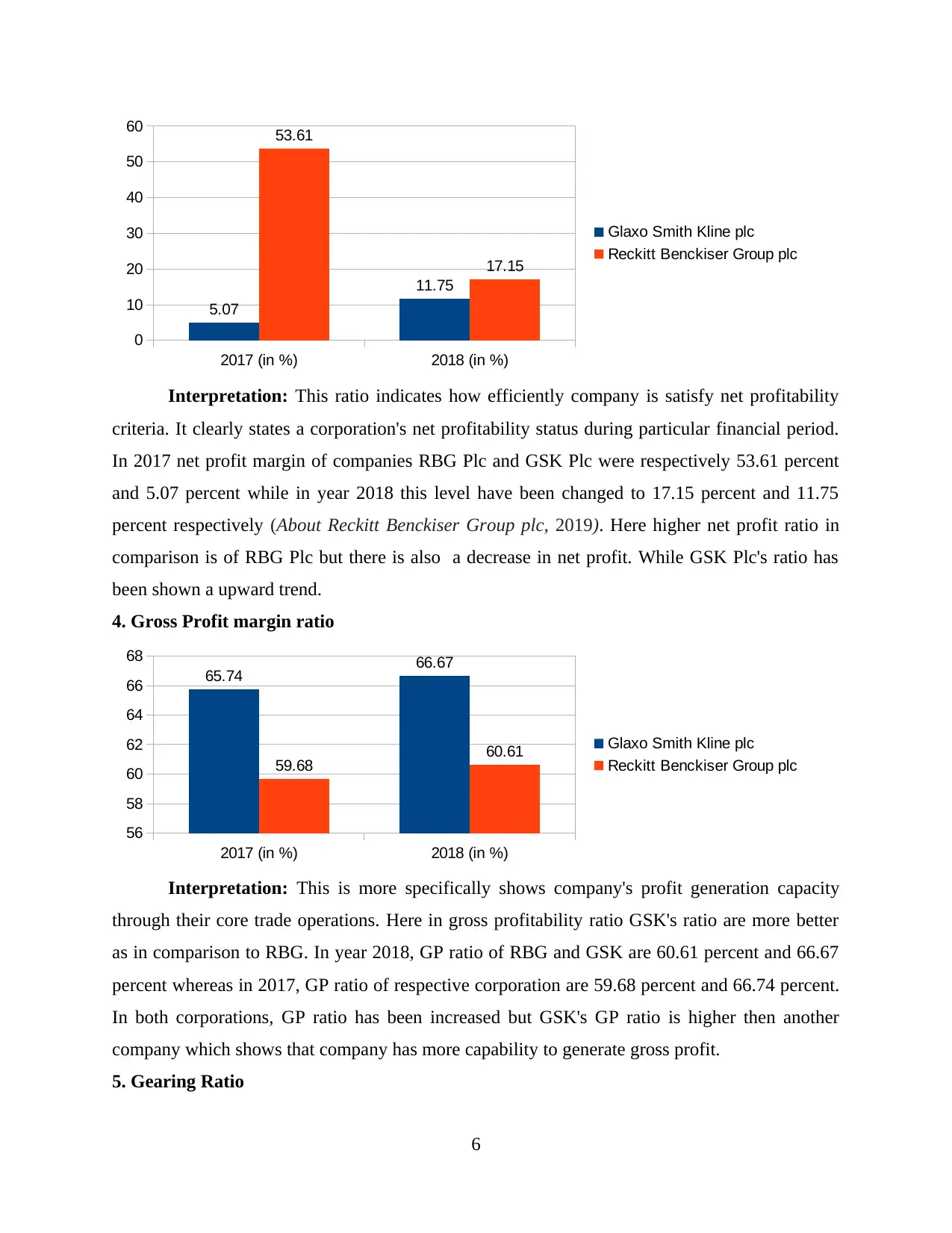

Interpretation: This ratio indicates how efficiently company is satisfy net profitability

criteria. It clearly states a corporation's net profitability status during particular financial period.

In 2017 net profit margin of companies RBG Plc and GSK Plc were respectively 53.61 percent

and 5.07 percent while in year 2018 this level have been changed to 17.15 percent and 11.75

percent respectively (About Reckitt Benckiser Group plc, 2019). Here higher net profit ratio in

comparison is of RBG Plc but there is also a decrease in net profit. While GSK Plc's ratio has

been shown a upward trend.

4. Gross Profit margin ratio

2017 (in %) 2018 (in %)

56

58

60

62

64

66

68

65.74 66.67

59.68 60.61 Glaxo Smith Kline plc

Reckitt Benckiser Group plc

Interpretation: This is more specifically shows company's profit generation capacity

through their core trade operations. Here in gross profitability ratio GSK's ratio are more better

as in comparison to RBG. In year 2018, GP ratio of RBG and GSK are 60.61 percent and 66.67

percent whereas in 2017, GP ratio of respective corporation are 59.68 percent and 66.74 percent.

In both corporations, GP ratio has been increased but GSK's GP ratio is higher then another

company which shows that company has more capability to generate gross profit.

5. Gearing Ratio

6

0

10

20

30

40

50

60

5.07

11.75

53.61

17.15

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

Interpretation: This ratio indicates how efficiently company is satisfy net profitability

criteria. It clearly states a corporation's net profitability status during particular financial period.

In 2017 net profit margin of companies RBG Plc and GSK Plc were respectively 53.61 percent

and 5.07 percent while in year 2018 this level have been changed to 17.15 percent and 11.75

percent respectively (About Reckitt Benckiser Group plc, 2019). Here higher net profit ratio in

comparison is of RBG Plc but there is also a decrease in net profit. While GSK Plc's ratio has

been shown a upward trend.

4. Gross Profit margin ratio

2017 (in %) 2018 (in %)

56

58

60

62

64

66

68

65.74 66.67

59.68 60.61 Glaxo Smith Kline plc

Reckitt Benckiser Group plc

Interpretation: This is more specifically shows company's profit generation capacity

through their core trade operations. Here in gross profitability ratio GSK's ratio are more better

as in comparison to RBG. In year 2018, GP ratio of RBG and GSK are 60.61 percent and 66.67

percent whereas in 2017, GP ratio of respective corporation are 59.68 percent and 66.74 percent.

In both corporations, GP ratio has been increased but GSK's GP ratio is higher then another

company which shows that company has more capability to generate gross profit.

5. Gearing Ratio

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2017 2018

0

2

4

6

8

10

12

14

0

12.32

1.74 1.55

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

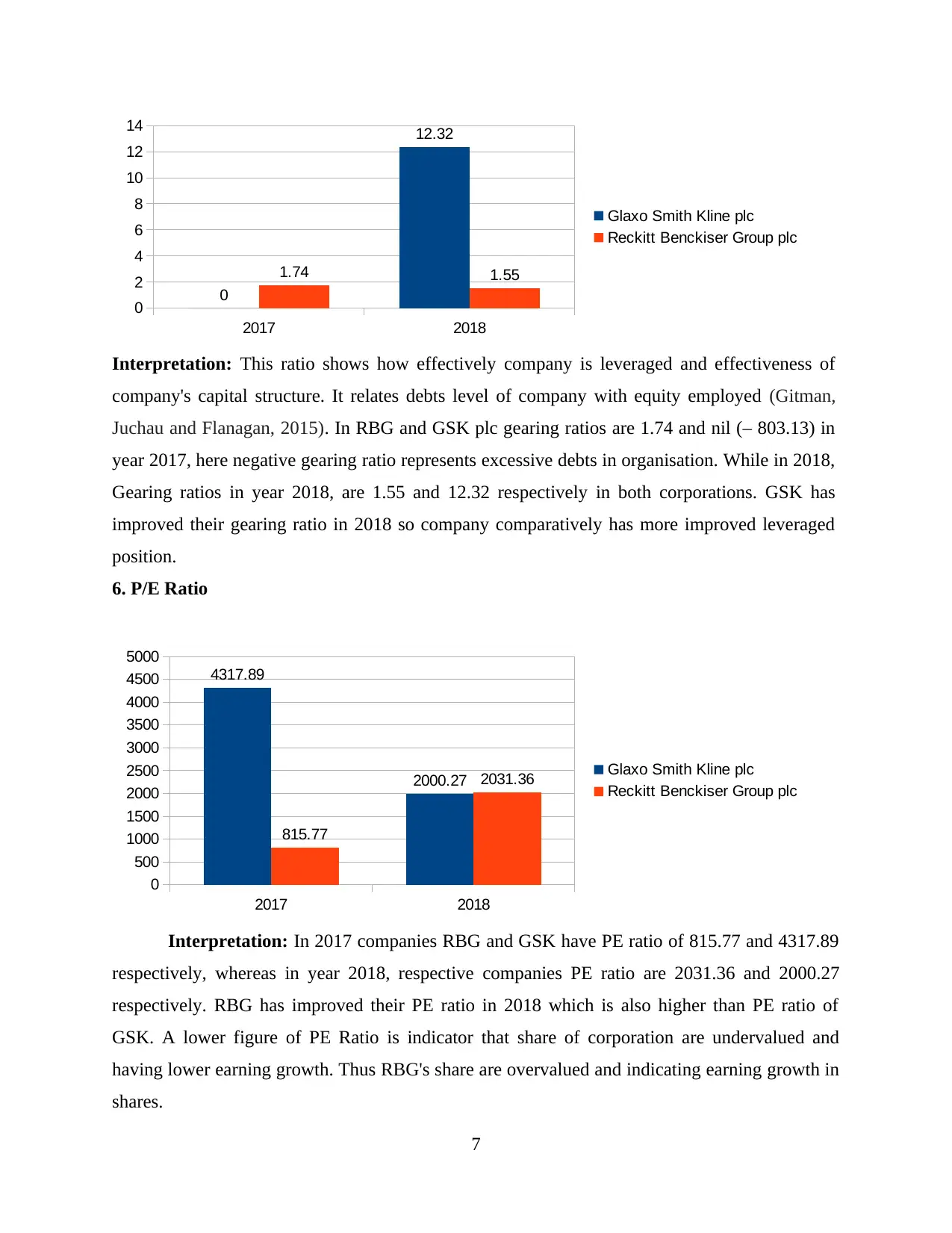

Interpretation: This ratio shows how effectively company is leveraged and effectiveness of

company's capital structure. It relates debts level of company with equity employed (Gitman,

Juchau and Flanagan, 2015). In RBG and GSK plc gearing ratios are 1.74 and nil (– 803.13) in

year 2017, here negative gearing ratio represents excessive debts in organisation. While in 2018,

Gearing ratios in year 2018, are 1.55 and 12.32 respectively in both corporations. GSK has

improved their gearing ratio in 2018 so company comparatively has more improved leveraged

position.

6. P/E Ratio

2017 2018

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

4317.89

2000.27

815.77

2031.36 Glaxo Smith Kline plc

Reckitt Benckiser Group plc

Interpretation: In 2017 companies RBG and GSK have PE ratio of 815.77 and 4317.89

respectively, whereas in year 2018, respective companies PE ratio are 2031.36 and 2000.27

respectively. RBG has improved their PE ratio in 2018 which is also higher than PE ratio of

GSK. A lower figure of PE Ratio is indicator that share of corporation are undervalued and

having lower earning growth. Thus RBG's share are overvalued and indicating earning growth in

shares.

7

0

2

4

6

8

10

12

14

0

12.32

1.74 1.55

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

Interpretation: This ratio shows how effectively company is leveraged and effectiveness of

company's capital structure. It relates debts level of company with equity employed (Gitman,

Juchau and Flanagan, 2015). In RBG and GSK plc gearing ratios are 1.74 and nil (– 803.13) in

year 2017, here negative gearing ratio represents excessive debts in organisation. While in 2018,

Gearing ratios in year 2018, are 1.55 and 12.32 respectively in both corporations. GSK has

improved their gearing ratio in 2018 so company comparatively has more improved leveraged

position.

6. P/E Ratio

2017 2018

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

4317.89

2000.27

815.77

2031.36 Glaxo Smith Kline plc

Reckitt Benckiser Group plc

Interpretation: In 2017 companies RBG and GSK have PE ratio of 815.77 and 4317.89

respectively, whereas in year 2018, respective companies PE ratio are 2031.36 and 2000.27

respectively. RBG has improved their PE ratio in 2018 which is also higher than PE ratio of

GSK. A lower figure of PE Ratio is indicator that share of corporation are undervalued and

having lower earning growth. Thus RBG's share are overvalued and indicating earning growth in

shares.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

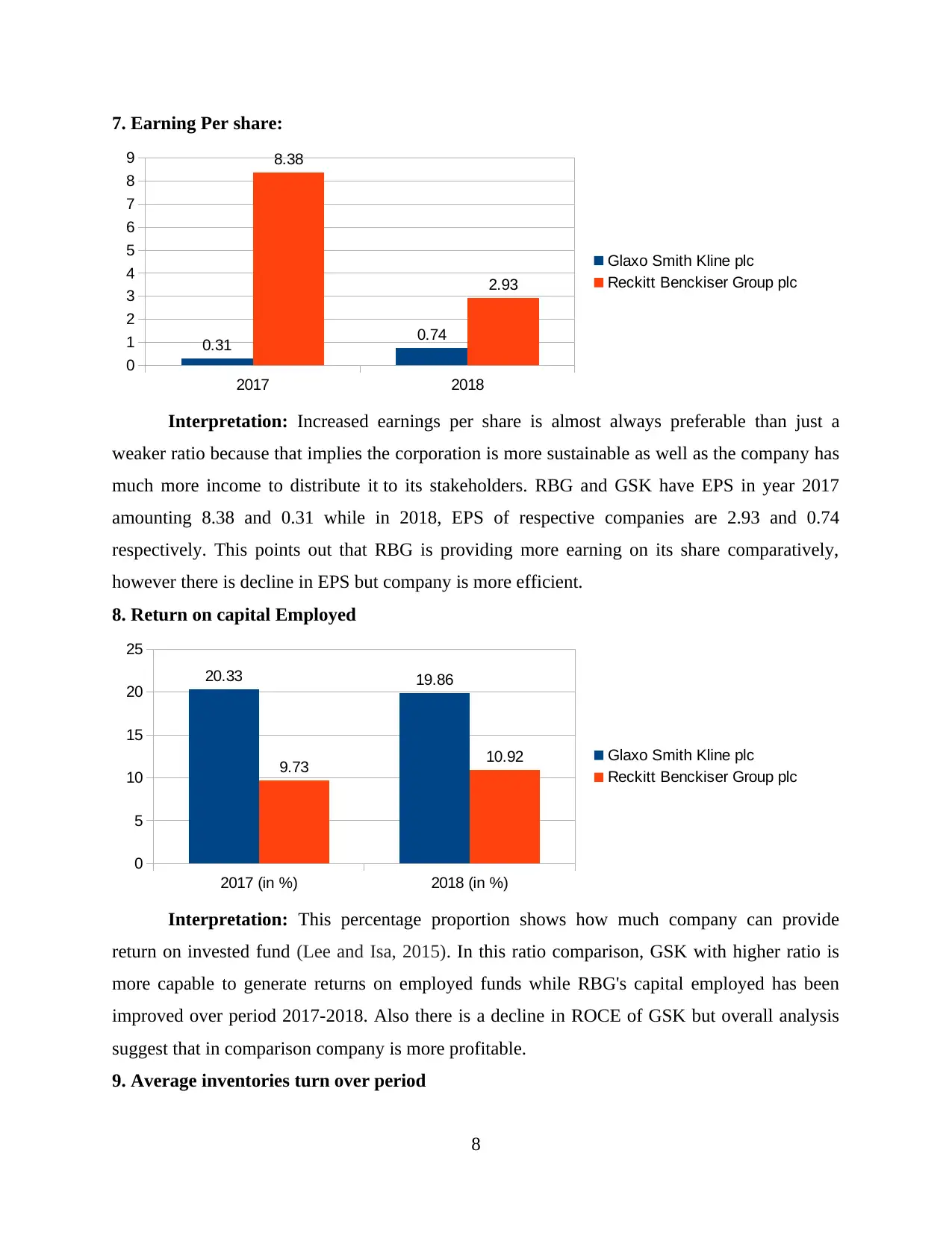

7. Earning Per share:

2017 2018

0

1

2

3

4

5

6

7

8

9

0.31 0.74

8.38

2.93

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

Interpretation: Increased earnings per share is almost always preferable than just a

weaker ratio because that implies the corporation is more sustainable as well as the company has

much more income to distribute it to its stakeholders. RBG and GSK have EPS in year 2017

amounting 8.38 and 0.31 while in 2018, EPS of respective companies are 2.93 and 0.74

respectively. This points out that RBG is providing more earning on its share comparatively,

however there is decline in EPS but company is more efficient.

8. Return on capital Employed

2017 (in %) 2018 (in %)

0

5

10

15

20

25

20.33 19.86

9.73 10.92 Glaxo Smith Kline plc

Reckitt Benckiser Group plc

Interpretation: This percentage proportion shows how much company can provide

return on invested fund (Lee and Isa, 2015). In this ratio comparison, GSK with higher ratio is

more capable to generate returns on employed funds while RBG's capital employed has been

improved over period 2017-2018. Also there is a decline in ROCE of GSK but overall analysis

suggest that in comparison company is more profitable.

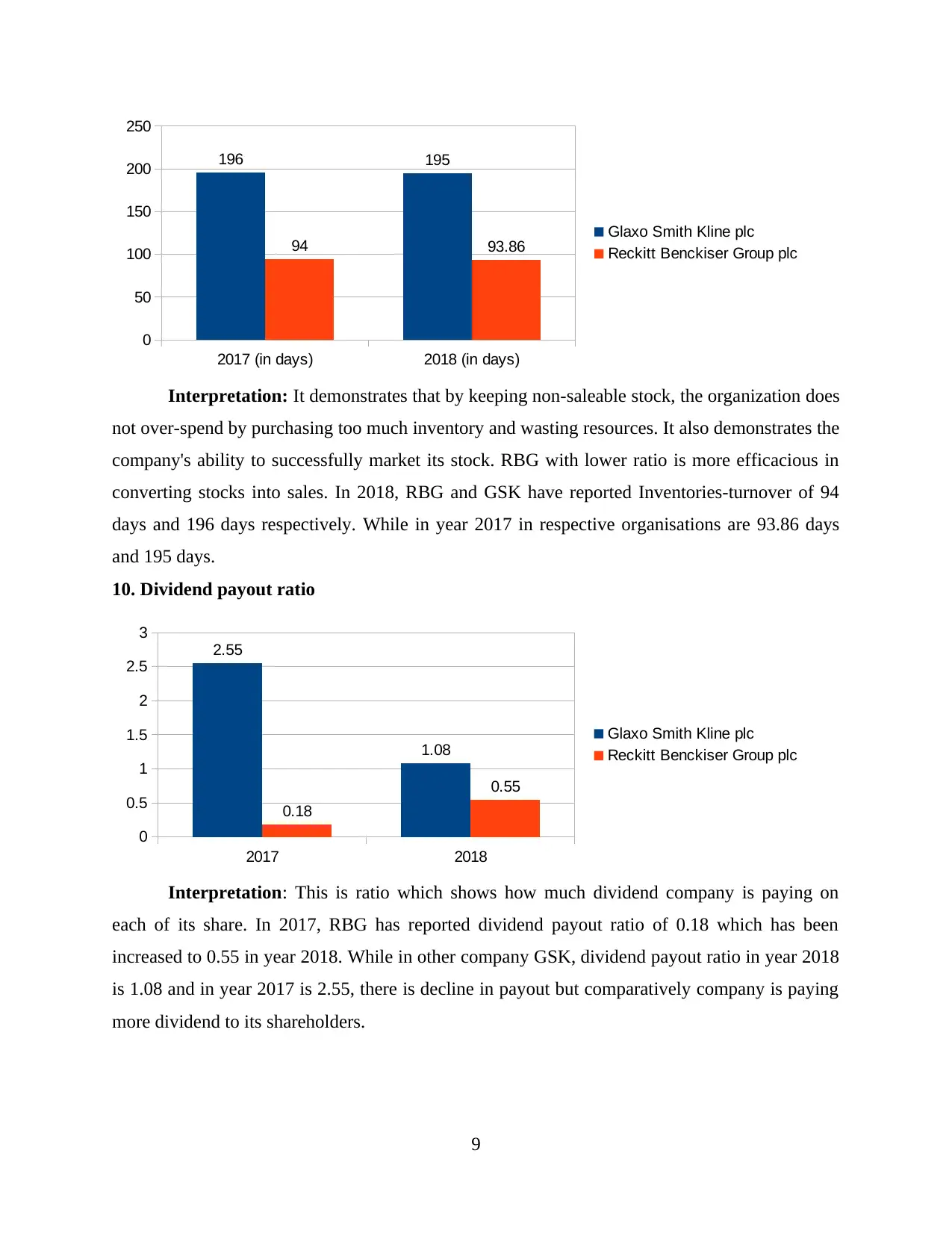

9. Average inventories turn over period

8

2017 2018

0

1

2

3

4

5

6

7

8

9

0.31 0.74

8.38

2.93

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

Interpretation: Increased earnings per share is almost always preferable than just a

weaker ratio because that implies the corporation is more sustainable as well as the company has

much more income to distribute it to its stakeholders. RBG and GSK have EPS in year 2017

amounting 8.38 and 0.31 while in 2018, EPS of respective companies are 2.93 and 0.74

respectively. This points out that RBG is providing more earning on its share comparatively,

however there is decline in EPS but company is more efficient.

8. Return on capital Employed

2017 (in %) 2018 (in %)

0

5

10

15

20

25

20.33 19.86

9.73 10.92 Glaxo Smith Kline plc

Reckitt Benckiser Group plc

Interpretation: This percentage proportion shows how much company can provide

return on invested fund (Lee and Isa, 2015). In this ratio comparison, GSK with higher ratio is

more capable to generate returns on employed funds while RBG's capital employed has been

improved over period 2017-2018. Also there is a decline in ROCE of GSK but overall analysis

suggest that in comparison company is more profitable.

9. Average inventories turn over period

8

2017 (in days) 2018 (in days)

0

50

100

150

200

250

196 195

94 93.86 Glaxo Smith Kline plc

Reckitt Benckiser Group plc

Interpretation: It demonstrates that by keeping non-saleable stock, the organization does

not over-spend by purchasing too much inventory and wasting resources. It also demonstrates the

company's ability to successfully market its stock. RBG with lower ratio is more efficacious in

converting stocks into sales. In 2018, RBG and GSK have reported Inventories-turnover of 94

days and 196 days respectively. While in year 2017 in respective organisations are 93.86 days

and 195 days.

10. Dividend payout ratio

2017 2018

0

0.5

1

1.5

2

2.5

3

2.55

1.08

0.18

0.55

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

Interpretation: This is ratio which shows how much dividend company is paying on

each of its share. In 2017, RBG has reported dividend payout ratio of 0.18 which has been

increased to 0.55 in year 2018. While in other company GSK, dividend payout ratio in year 2018

is 1.08 and in year 2017 is 2.55, there is decline in payout but comparatively company is paying

more dividend to its shareholders.

9

0

50

100

150

200

250

196 195

94 93.86 Glaxo Smith Kline plc

Reckitt Benckiser Group plc

Interpretation: It demonstrates that by keeping non-saleable stock, the organization does

not over-spend by purchasing too much inventory and wasting resources. It also demonstrates the

company's ability to successfully market its stock. RBG with lower ratio is more efficacious in

converting stocks into sales. In 2018, RBG and GSK have reported Inventories-turnover of 94

days and 196 days respectively. While in year 2017 in respective organisations are 93.86 days

and 195 days.

10. Dividend payout ratio

2017 2018

0

0.5

1

1.5

2

2.5

3

2.55

1.08

0.18

0.55

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

Interpretation: This is ratio which shows how much dividend company is paying on

each of its share. In 2017, RBG has reported dividend payout ratio of 0.18 which has been

increased to 0.55 in year 2018. While in other company GSK, dividend payout ratio in year 2018

is 1.08 and in year 2017 is 2.55, there is decline in payout but comparatively company is paying

more dividend to its shareholders.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.