Business Analysis and Interpretation of Financial Ratios Report

VerifiedAdded on 2020/06/04

|12

|1791

|475

Report

AI Summary

This report provides a detailed analysis of financial ratios and cash cycles for Boral Ltd and CSR Ltd. The analysis covers key ratios such as net profit margin, asset turnover ratio, current ratio, quick ratio, and debt-equity ratio, examining their trends and implications for each company's financial performance. The report also explores the cash cycle for both firms, evaluating their working capital management. Based on the ratio analysis, the report offers specific recommendations for each company to improve their financial performance, including restructuring capital structures, controlling indirect expenses, and optimizing asset utilization. The conclusion emphasizes the importance of regular ratio analysis and cash cycle computation for effective financial management and timely decision-making. The report includes tables with ratio calculations and provides references to relevant literature.

BUSINESS ANALYSIS AND

INTERPRETATION

INTERPRETATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Ratio.................................................................................................................................................1

Cash cycle........................................................................................................................................2

Recommendation.............................................................................................................................2

CONCLUSION................................................................................................................................3

Figure 1Net profit ratio....................................................................................................................1

Figure 2Asset turnover ratio............................................................................................................2

Figure 3Current ratio.......................................................................................................................3

Figure 4Quick ratio..........................................................................................................................4

Figure 5Debt equity ratio.................................................................................................................4

Figure 6Cash cycle ratio..................................................................................................................5

INTRODUCTION...........................................................................................................................1

Ratio.................................................................................................................................................1

Cash cycle........................................................................................................................................2

Recommendation.............................................................................................................................2

CONCLUSION................................................................................................................................3

Figure 1Net profit ratio....................................................................................................................1

Figure 2Asset turnover ratio............................................................................................................2

Figure 3Current ratio.......................................................................................................................3

Figure 4Quick ratio..........................................................................................................................4

Figure 5Debt equity ratio.................................................................................................................4

Figure 6Cash cycle ratio..................................................................................................................5

INTRODUCTION

Ratio analysis and cash cycle are important approaches that are used to measure firm’s

performance. In the current report, ratio analysis of selected firms is done and comments are

given on same. Along with this, recommendations are given upon which firms can improve their

performance. In this way, entire research work is carried out.

Ratio

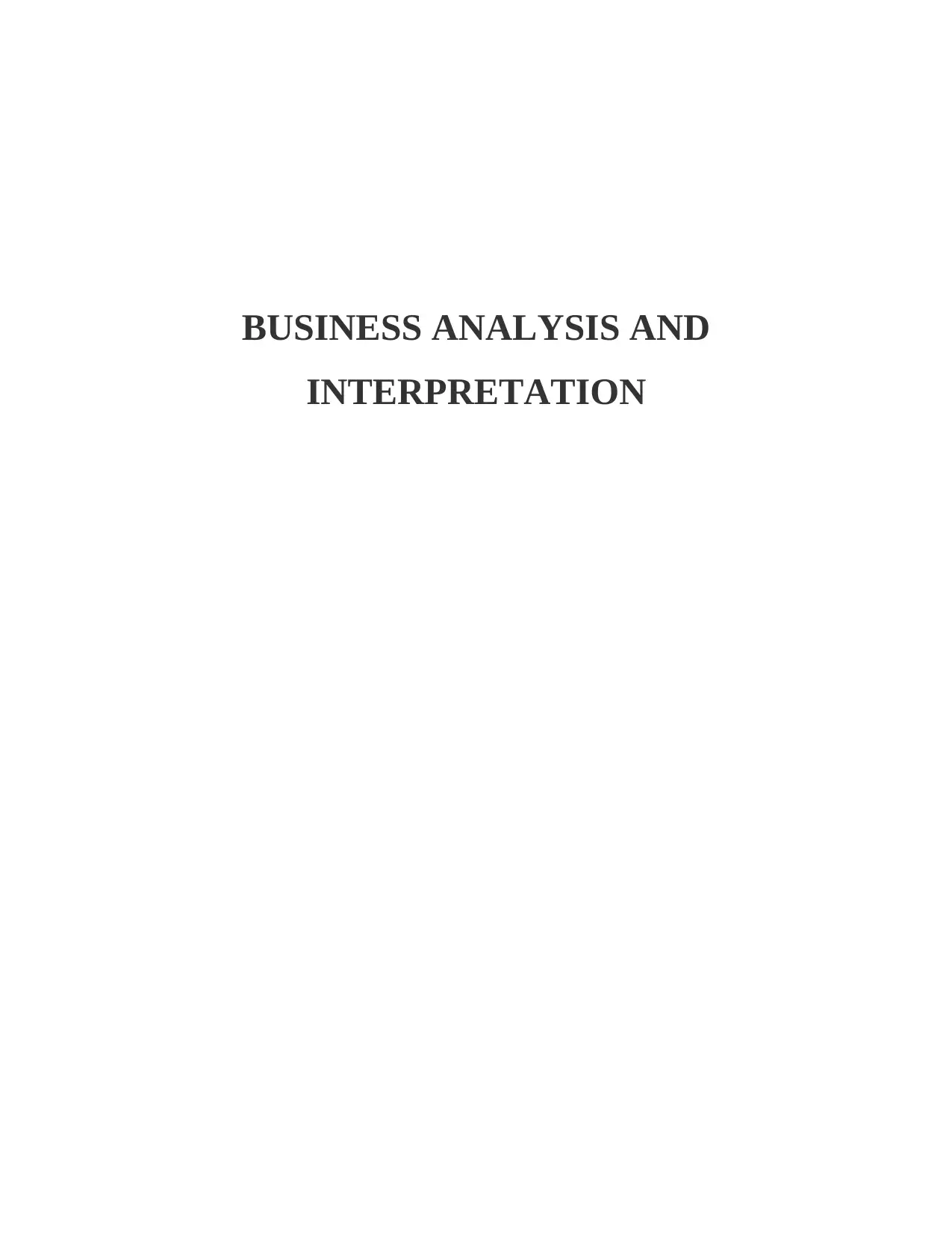

Net profit margin: Net profit margin reflects profitability percentage that is gained by the

firm after paying all direct and indirect expenses of business. This ratio is highly

important for the firms because it helps managers in understanding burden of indirect

expenses on business (Kumbirai, 2010). There are some limitations of this ratio because

it reflect impact of both direct and indirect expenses on firm’s profitability instead of this

it must only show impact of indiect expenses on firm profitability. Net profit ratio in case

of Boral Ltd increased from 4% to 5.94% and same in case of CSR Ltd raised from 5% to

6.18%. It can be said that greater profit is earned by later firm then former one.

2014 2015 2016

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

3.9%

6.0% 5.9%

5.0%

6.2% 6.2%

Chart Title

Boral Ltd CSR Ltd

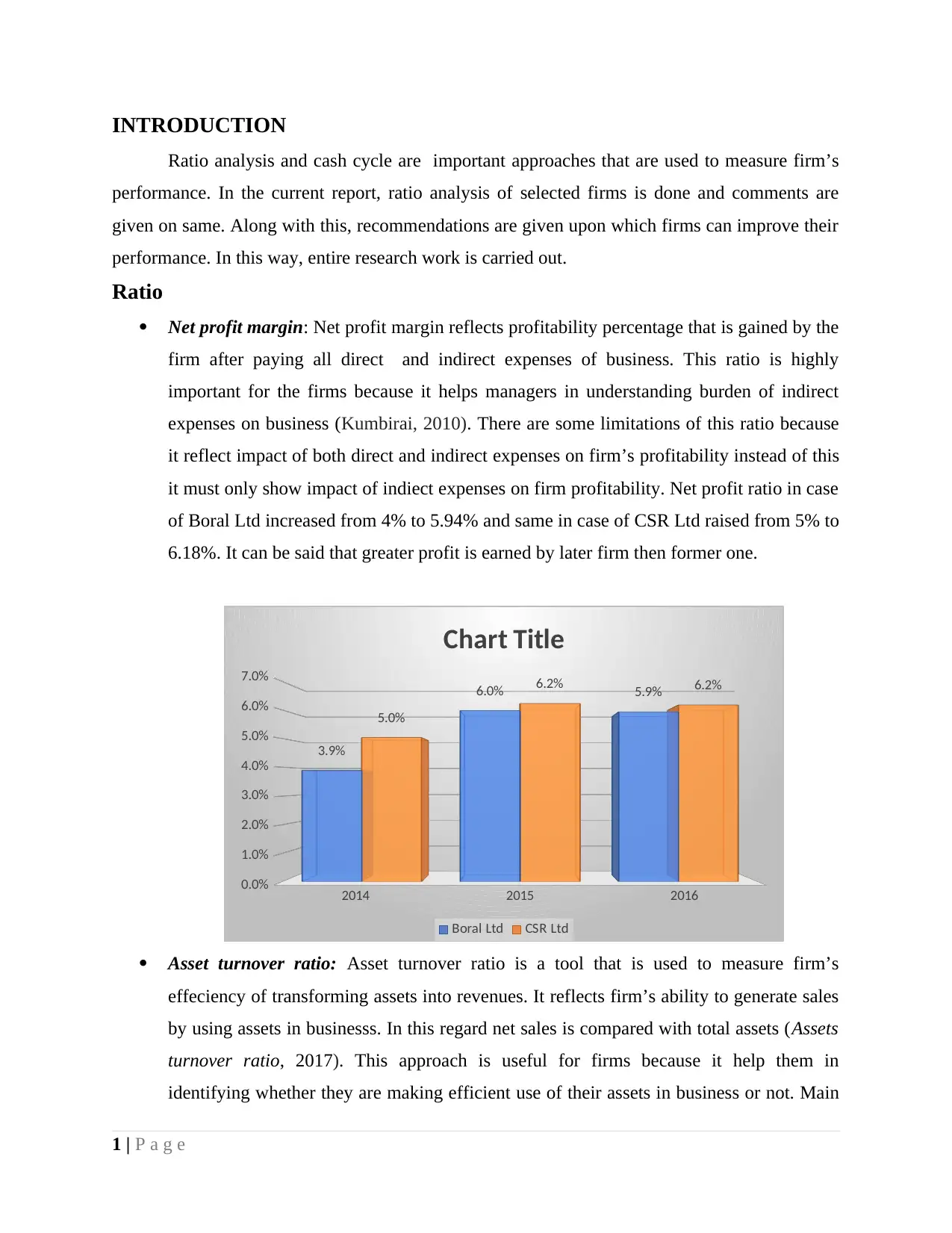

Asset turnover ratio: Asset turnover ratio is a tool that is used to measure firm’s

effeciency of transforming assets into revenues. It reflects firm’s ability to generate sales

by using assets in businesss. In this regard net sales is compared with total assets (Assets

turnover ratio, 2017). This approach is useful for firms because it help them in

identifying whether they are making efficient use of their assets in business or not. Main

1 | P a g e

Ratio analysis and cash cycle are important approaches that are used to measure firm’s

performance. In the current report, ratio analysis of selected firms is done and comments are

given on same. Along with this, recommendations are given upon which firms can improve their

performance. In this way, entire research work is carried out.

Ratio

Net profit margin: Net profit margin reflects profitability percentage that is gained by the

firm after paying all direct and indirect expenses of business. This ratio is highly

important for the firms because it helps managers in understanding burden of indirect

expenses on business (Kumbirai, 2010). There are some limitations of this ratio because

it reflect impact of both direct and indirect expenses on firm’s profitability instead of this

it must only show impact of indiect expenses on firm profitability. Net profit ratio in case

of Boral Ltd increased from 4% to 5.94% and same in case of CSR Ltd raised from 5% to

6.18%. It can be said that greater profit is earned by later firm then former one.

2014 2015 2016

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

3.9%

6.0% 5.9%

5.0%

6.2% 6.2%

Chart Title

Boral Ltd CSR Ltd

Asset turnover ratio: Asset turnover ratio is a tool that is used to measure firm’s

effeciency of transforming assets into revenues. It reflects firm’s ability to generate sales

by using assets in businesss. In this regard net sales is compared with total assets (Assets

turnover ratio, 2017). This approach is useful for firms because it help them in

identifying whether they are making efficient use of their assets in business or not. Main

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

limitation of assets turnover ratio is that, firms operating in different industry observes

varied conditions. All these have impact on firm’s profitability. Thus, if firms belong to

different industry it is not possible to measure their effeciency using this ratio. Assets

turnover ratio of Boral Ltd decreased from 0.75 to 0.73 between 2014 to 2016 and same

for CSR Ltd elevated from 0.86 to 1.06 which means that later firm is making better use

of its assets in business then former firm.

Figure 1Net profit ratio

2014 2015 2016

-25.00

-20.00

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

-15.06

15.15

-22.80

Chart Title

Boral Ltd CSR Ltd

Figure 2Asset turnover ratio

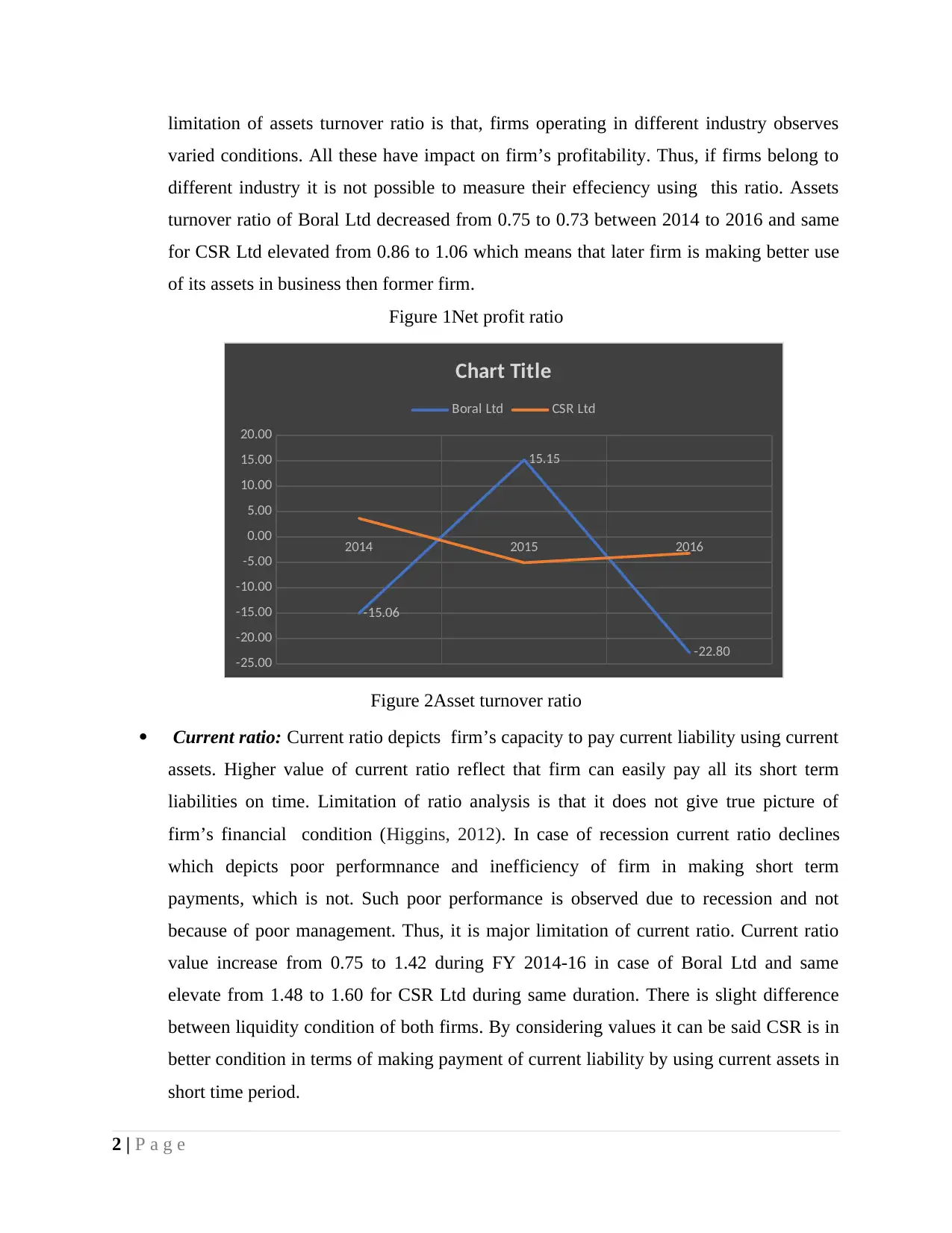

Current ratio: Current ratio depicts firm’s capacity to pay current liability using current

assets. Higher value of current ratio reflect that firm can easily pay all its short term

liabilities on time. Limitation of ratio analysis is that it does not give true picture of

firm’s financial condition (Higgins, 2012). In case of recession current ratio declines

which depicts poor performnance and inefficiency of firm in making short term

payments, which is not. Such poor performance is observed due to recession and not

because of poor management. Thus, it is major limitation of current ratio. Current ratio

value increase from 0.75 to 1.42 during FY 2014-16 in case of Boral Ltd and same

elevate from 1.48 to 1.60 for CSR Ltd during same duration. There is slight difference

between liquidity condition of both firms. By considering values it can be said CSR is in

better condition in terms of making payment of current liability by using current assets in

short time period.

2 | P a g e

varied conditions. All these have impact on firm’s profitability. Thus, if firms belong to

different industry it is not possible to measure their effeciency using this ratio. Assets

turnover ratio of Boral Ltd decreased from 0.75 to 0.73 between 2014 to 2016 and same

for CSR Ltd elevated from 0.86 to 1.06 which means that later firm is making better use

of its assets in business then former firm.

Figure 1Net profit ratio

2014 2015 2016

-25.00

-20.00

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

-15.06

15.15

-22.80

Chart Title

Boral Ltd CSR Ltd

Figure 2Asset turnover ratio

Current ratio: Current ratio depicts firm’s capacity to pay current liability using current

assets. Higher value of current ratio reflect that firm can easily pay all its short term

liabilities on time. Limitation of ratio analysis is that it does not give true picture of

firm’s financial condition (Higgins, 2012). In case of recession current ratio declines

which depicts poor performnance and inefficiency of firm in making short term

payments, which is not. Such poor performance is observed due to recession and not

because of poor management. Thus, it is major limitation of current ratio. Current ratio

value increase from 0.75 to 1.42 during FY 2014-16 in case of Boral Ltd and same

elevate from 1.48 to 1.60 for CSR Ltd during same duration. There is slight difference

between liquidity condition of both firms. By considering values it can be said CSR is in

better condition in terms of making payment of current liability by using current assets in

short time period.

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 2 3

-25.00

-20.00

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

-15.06

15.15

-22.80

3.64

-5.09 -3.23

Chart Title

Series1 Series2

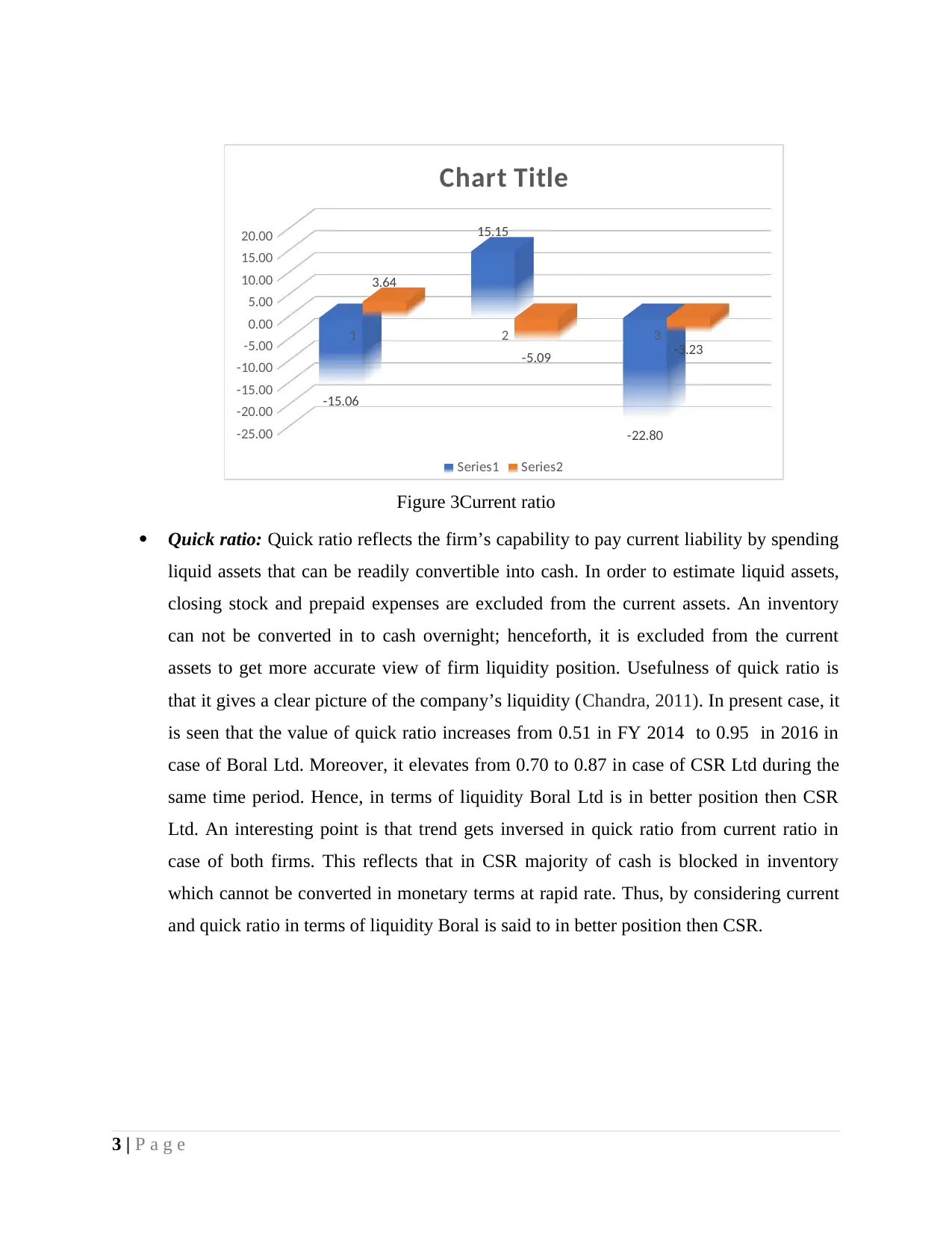

Figure 3Current ratio

Quick ratio: Quick ratio reflects the firm’s capability to pay current liability by spending

liquid assets that can be readily convertible into cash. In order to estimate liquid assets,

closing stock and prepaid expenses are excluded from the current assets. An inventory

can not be converted in to cash overnight; henceforth, it is excluded from the current

assets to get more accurate view of firm liquidity position. Usefulness of quick ratio is

that it gives a clear picture of the company’s liquidity (Chandra, 2011). In present case, it

is seen that the value of quick ratio increases from 0.51 in FY 2014 to 0.95 in 2016 in

case of Boral Ltd. Moreover, it elevates from 0.70 to 0.87 in case of CSR Ltd during the

same time period. Hence, in terms of liquidity Boral Ltd is in better position then CSR

Ltd. An interesting point is that trend gets inversed in quick ratio from current ratio in

case of both firms. This reflects that in CSR majority of cash is blocked in inventory

which cannot be converted in monetary terms at rapid rate. Thus, by considering current

and quick ratio in terms of liquidity Boral is said to in better position then CSR.

3 | P a g e

-25.00

-20.00

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

-15.06

15.15

-22.80

3.64

-5.09 -3.23

Chart Title

Series1 Series2

Figure 3Current ratio

Quick ratio: Quick ratio reflects the firm’s capability to pay current liability by spending

liquid assets that can be readily convertible into cash. In order to estimate liquid assets,

closing stock and prepaid expenses are excluded from the current assets. An inventory

can not be converted in to cash overnight; henceforth, it is excluded from the current

assets to get more accurate view of firm liquidity position. Usefulness of quick ratio is

that it gives a clear picture of the company’s liquidity (Chandra, 2011). In present case, it

is seen that the value of quick ratio increases from 0.51 in FY 2014 to 0.95 in 2016 in

case of Boral Ltd. Moreover, it elevates from 0.70 to 0.87 in case of CSR Ltd during the

same time period. Hence, in terms of liquidity Boral Ltd is in better position then CSR

Ltd. An interesting point is that trend gets inversed in quick ratio from current ratio in

case of both firms. This reflects that in CSR majority of cash is blocked in inventory

which cannot be converted in monetary terms at rapid rate. Thus, by considering current

and quick ratio in terms of liquidity Boral is said to in better position then CSR.

3 | P a g e

2014 2015 2016

-25.00

-20.00

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

-15.06

15.15

-22.80

3.64

-5.09 -3.23

Chart Title

Boral Ltd CSR Ltd

Figure 4Quick ratio

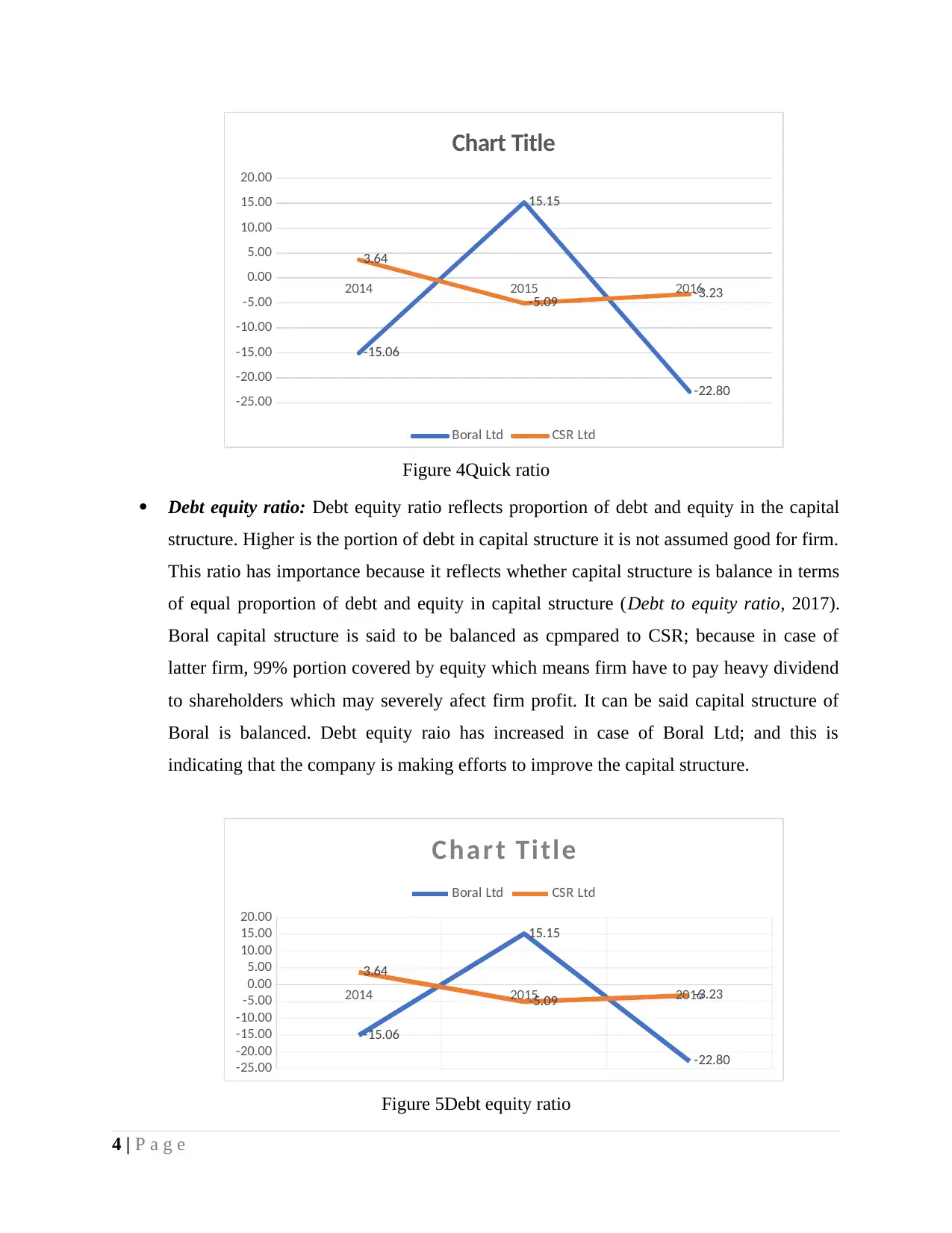

Debt equity ratio: Debt equity ratio reflects proportion of debt and equity in the capital

structure. Higher is the portion of debt in capital structure it is not assumed good for firm.

This ratio has importance because it reflects whether capital structure is balance in terms

of equal proportion of debt and equity in capital structure (Debt to equity ratio, 2017).

Boral capital structure is said to be balanced as cpmpared to CSR; because in case of

latter firm, 99% portion covered by equity which means firm have to pay heavy dividend

to shareholders which may severely afect firm profit. It can be said capital structure of

Boral is balanced. Debt equity raio has increased in case of Boral Ltd; and this is

indicating that the company is making efforts to improve the capital structure.

2014 2015 2016

-25.00

-20.00

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

-15.06

15.15

-22.80

3.64

-5.09 -3.23

Char t Title

Boral Ltd CSR Ltd

Figure 5Debt equity ratio

4 | P a g e

-25.00

-20.00

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

-15.06

15.15

-22.80

3.64

-5.09 -3.23

Chart Title

Boral Ltd CSR Ltd

Figure 4Quick ratio

Debt equity ratio: Debt equity ratio reflects proportion of debt and equity in the capital

structure. Higher is the portion of debt in capital structure it is not assumed good for firm.

This ratio has importance because it reflects whether capital structure is balance in terms

of equal proportion of debt and equity in capital structure (Debt to equity ratio, 2017).

Boral capital structure is said to be balanced as cpmpared to CSR; because in case of

latter firm, 99% portion covered by equity which means firm have to pay heavy dividend

to shareholders which may severely afect firm profit. It can be said capital structure of

Boral is balanced. Debt equity raio has increased in case of Boral Ltd; and this is

indicating that the company is making efforts to improve the capital structure.

2014 2015 2016

-25.00

-20.00

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

-15.06

15.15

-22.80

3.64

-5.09 -3.23

Char t Title

Boral Ltd CSR Ltd

Figure 5Debt equity ratio

4 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

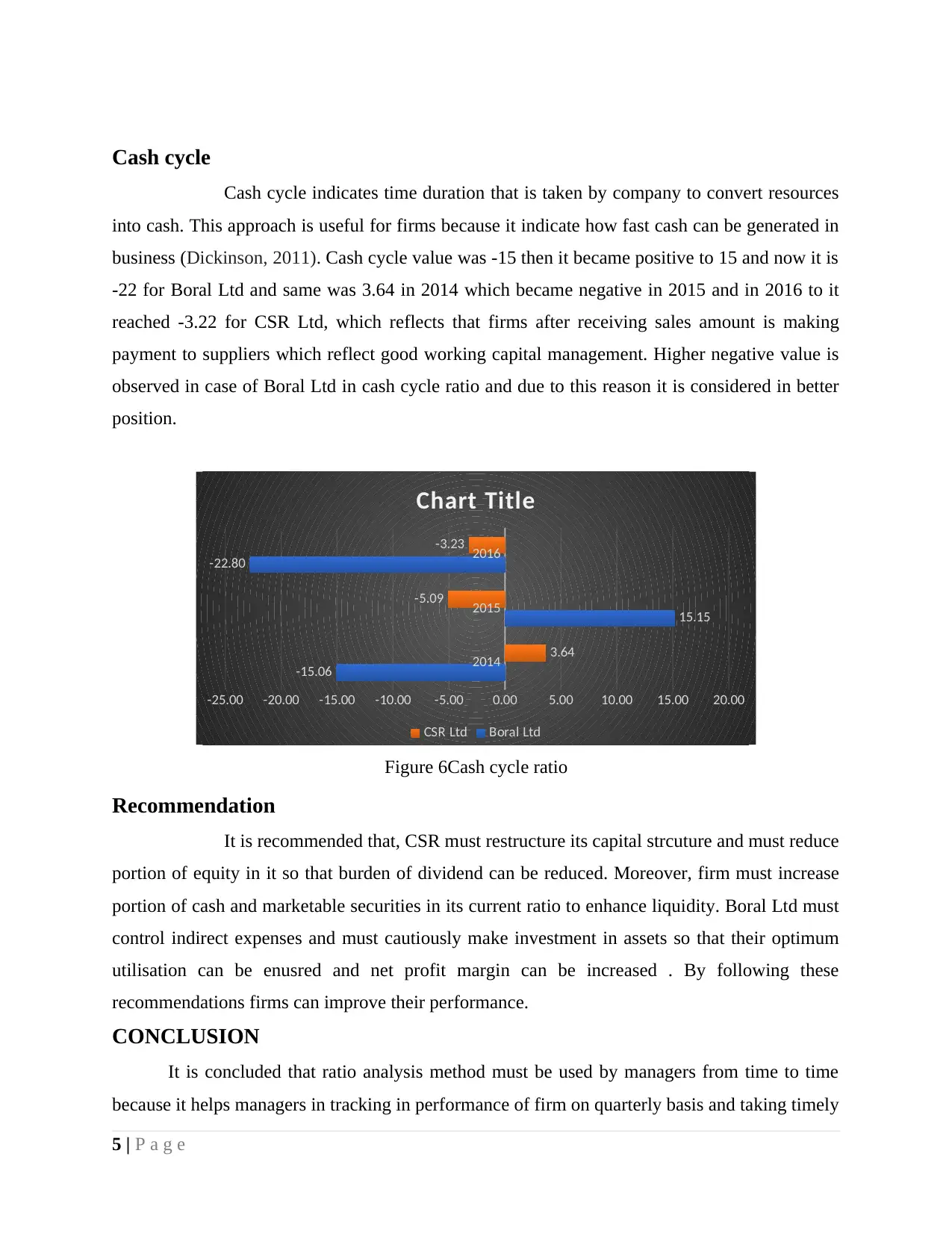

Cash cycle

Cash cycle indicates time duration that is taken by company to convert resources

into cash. This approach is useful for firms because it indicate how fast cash can be generated in

business (Dickinson, 2011). Cash cycle value was -15 then it became positive to 15 and now it is

-22 for Boral Ltd and same was 3.64 in 2014 which became negative in 2015 and in 2016 to it

reached -3.22 for CSR Ltd, which reflects that firms after receiving sales amount is making

payment to suppliers which reflect good working capital management. Higher negative value is

observed in case of Boral Ltd in cash cycle ratio and due to this reason it is considered in better

position.

2014

2015

2016

-25.00 -20.00 -15.00 -10.00 -5.00 0.00 5.00 10.00 15.00 20.00

-15.06

15.15

-22.80

3.64

-5.09

-3.23

Chart Title

CSR Ltd Boral Ltd

Figure 6Cash cycle ratio

Recommendation

It is recommended that, CSR must restructure its capital strcuture and must reduce

portion of equity in it so that burden of dividend can be reduced. Moreover, firm must increase

portion of cash and marketable securities in its current ratio to enhance liquidity. Boral Ltd must

control indirect expenses and must cautiously make investment in assets so that their optimum

utilisation can be enusred and net profit margin can be increased . By following these

recommendations firms can improve their performance.

CONCLUSION

It is concluded that ratio analysis method must be used by managers from time to time

because it helps managers in tracking in performance of firm on quarterly basis and taking timely

5 | P a g e

Cash cycle indicates time duration that is taken by company to convert resources

into cash. This approach is useful for firms because it indicate how fast cash can be generated in

business (Dickinson, 2011). Cash cycle value was -15 then it became positive to 15 and now it is

-22 for Boral Ltd and same was 3.64 in 2014 which became negative in 2015 and in 2016 to it

reached -3.22 for CSR Ltd, which reflects that firms after receiving sales amount is making

payment to suppliers which reflect good working capital management. Higher negative value is

observed in case of Boral Ltd in cash cycle ratio and due to this reason it is considered in better

position.

2014

2015

2016

-25.00 -20.00 -15.00 -10.00 -5.00 0.00 5.00 10.00 15.00 20.00

-15.06

15.15

-22.80

3.64

-5.09

-3.23

Chart Title

CSR Ltd Boral Ltd

Figure 6Cash cycle ratio

Recommendation

It is recommended that, CSR must restructure its capital strcuture and must reduce

portion of equity in it so that burden of dividend can be reduced. Moreover, firm must increase

portion of cash and marketable securities in its current ratio to enhance liquidity. Boral Ltd must

control indirect expenses and must cautiously make investment in assets so that their optimum

utilisation can be enusred and net profit margin can be increased . By following these

recommendations firms can improve their performance.

CONCLUSION

It is concluded that ratio analysis method must be used by managers from time to time

because it helps managers in tracking in performance of firm on quarterly basis and taking timely

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

action to improve it Cash cycle must be computed time to time to ensure that working capital is

managed in proper manner at workplace.

6 | P a g e

managed in proper manner at workplace.

6 | P a g e

REFERENCES

Books and Journals

Chandra, P., 2011. Financial management. Tata McGraw-Hill Education.

Dickinson, V., 2011. Cash flow patterns as a proxy for firm life cycle. The Accounting

Review. 86(6), pp.1969-1994.

Higgins, R.C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Kumbirai, M., 2010. A financial ratio analysis of commercial bank performance in South

Africa. African Review of Economics and Finance. 2(1), pp.30-53.

Online

Assets turnover ratio, 2017. [Online]. Available through:<

http://www.myaccountingcourse.com/financial-ratios/asset-turnover-ratio>. [Accessed on

30th August 2017].

Debt to equity ratio, 2017. [Online]. Available through:<

<http://www.myaccountingcourse.com/financial-ratios/debt-to-equity-ratio>. [Accessed on

30th August 2017].

7 | P a g e

Books and Journals

Chandra, P., 2011. Financial management. Tata McGraw-Hill Education.

Dickinson, V., 2011. Cash flow patterns as a proxy for firm life cycle. The Accounting

Review. 86(6), pp.1969-1994.

Higgins, R.C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Kumbirai, M., 2010. A financial ratio analysis of commercial bank performance in South

Africa. African Review of Economics and Finance. 2(1), pp.30-53.

Online

Assets turnover ratio, 2017. [Online]. Available through:<

http://www.myaccountingcourse.com/financial-ratios/asset-turnover-ratio>. [Accessed on

30th August 2017].

Debt to equity ratio, 2017. [Online]. Available through:<

<http://www.myaccountingcourse.com/financial-ratios/debt-to-equity-ratio>. [Accessed on

30th August 2017].

7 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

APPENDIX

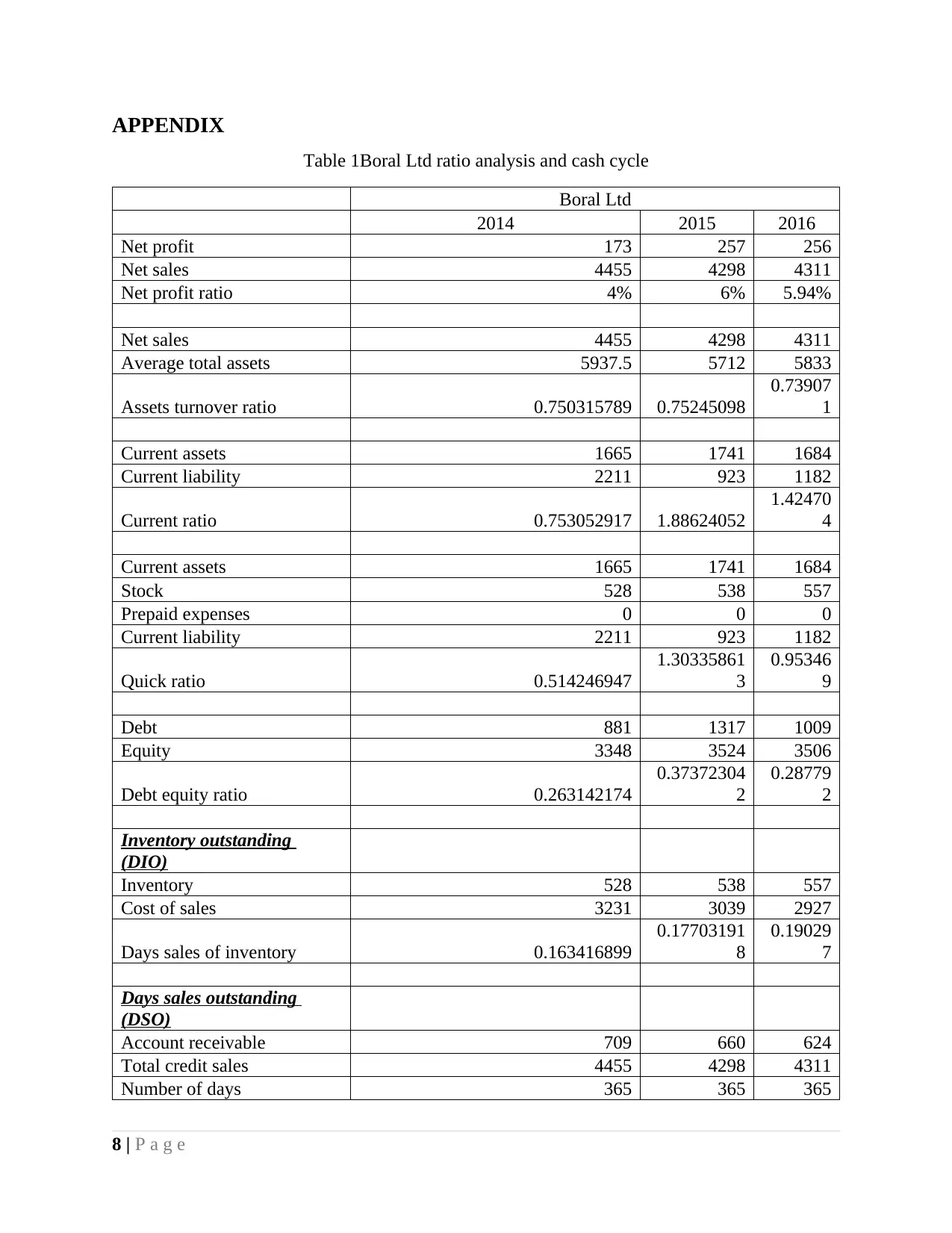

Table 1Boral Ltd ratio analysis and cash cycle

Boral Ltd

2014 2015 2016

Net profit 173 257 256

Net sales 4455 4298 4311

Net profit ratio 4% 6% 5.94%

Net sales 4455 4298 4311

Average total assets 5937.5 5712 5833

Assets turnover ratio 0.750315789 0.75245098

0.73907

1

Current assets 1665 1741 1684

Current liability 2211 923 1182

Current ratio 0.753052917 1.88624052

1.42470

4

Current assets 1665 1741 1684

Stock 528 538 557

Prepaid expenses 0 0 0

Current liability 2211 923 1182

Quick ratio 0.514246947

1.30335861

3

0.95346

9

Debt 881 1317 1009

Equity 3348 3524 3506

Debt equity ratio 0.263142174

0.37372304

2

0.28779

2

Inventory outstanding

(DIO)

Inventory 528 538 557

Cost of sales 3231 3039 2927

Days sales of inventory 0.163416899

0.17703191

8

0.19029

7

Days sales outstanding

(DSO)

Account receivable 709 660 624

Total credit sales 4455 4298 4311

Number of days 365 365 365

8 | P a g e

Table 1Boral Ltd ratio analysis and cash cycle

Boral Ltd

2014 2015 2016

Net profit 173 257 256

Net sales 4455 4298 4311

Net profit ratio 4% 6% 5.94%

Net sales 4455 4298 4311

Average total assets 5937.5 5712 5833

Assets turnover ratio 0.750315789 0.75245098

0.73907

1

Current assets 1665 1741 1684

Current liability 2211 923 1182

Current ratio 0.753052917 1.88624052

1.42470

4

Current assets 1665 1741 1684

Stock 528 538 557

Prepaid expenses 0 0 0

Current liability 2211 923 1182

Quick ratio 0.514246947

1.30335861

3

0.95346

9

Debt 881 1317 1009

Equity 3348 3524 3506

Debt equity ratio 0.263142174

0.37372304

2

0.28779

2

Inventory outstanding

(DIO)

Inventory 528 538 557

Cost of sales 3231 3039 2927

Days sales of inventory 0.163416899

0.17703191

8

0.19029

7

Days sales outstanding

(DSO)

Account receivable 709 660 624

Total credit sales 4455 4298 4311

Number of days 365 365 365

8 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Days sales outstanding 58.08866442

56.0493252

7

52.8322

9

Days payable outstanding

(DPO)

Account payable 649 342 608

Cost of sales/Number of days 8.852054795

8.32602739

7

8.01917

8

Days payable outstanding 73.31631074

41.0760118

5

75.8182

4

Cash cycle -15.06422942

15.1503453

4 -22.7957

Table 2CSR Ltd ratio analysis and cash cycle

CSR Ltd

2014 2015 2016

Net profit 88 126 142

Net sales 1747 2023 2299

Net profit ratio 5% 6% 6.18%

Net sales 1747 2023 2299

Average total assets 2019 2062 2167.5

Assets turnover ratio 0.865279842

0.98108632

4

1.06066

9

Current assets 632 705 786

Current liability 425 466 489

Current ratio 1.487058824

1.51287553

6

1.60736

2

Current assets 632 705 786

Stock 326 320 349

Prepaid expenses 6 5 11

Current liability 425 466 489

Quick ratio 0.705882353

0.81545064

4

0.87116

6

Debt 34 0 2

Equity 1099 1146 1184

Debt equity ratio 0.030937216 0

0.00168

9

9 | P a g e

56.0493252

7

52.8322

9

Days payable outstanding

(DPO)

Account payable 649 342 608

Cost of sales/Number of days 8.852054795

8.32602739

7

8.01917

8

Days payable outstanding 73.31631074

41.0760118

5

75.8182

4

Cash cycle -15.06422942

15.1503453

4 -22.7957

Table 2CSR Ltd ratio analysis and cash cycle

CSR Ltd

2014 2015 2016

Net profit 88 126 142

Net sales 1747 2023 2299

Net profit ratio 5% 6% 6.18%

Net sales 1747 2023 2299

Average total assets 2019 2062 2167.5

Assets turnover ratio 0.865279842

0.98108632

4

1.06066

9

Current assets 632 705 786

Current liability 425 466 489

Current ratio 1.487058824

1.51287553

6

1.60736

2

Current assets 632 705 786

Stock 326 320 349

Prepaid expenses 6 5 11

Current liability 425 466 489

Quick ratio 0.705882353

0.81545064

4

0.87116

6

Debt 34 0 2

Equity 1099 1146 1184

Debt equity ratio 0.030937216 0

0.00168

9

9 | P a g e

Inventory outstanding

(DIO)

Inventory 326 320 349

Cost of sales 1235 1369 1527

Days sales of inventory 0.263967611

0.23374726

1

0.22855

3

Days sales outstanding

(DSO)

Account receivable 251 269 320

Total credit sales 1747 2023 2299

Number of days 365 365 365

Days sales outstanding 52.44132799

48.5343549

2 50.8047

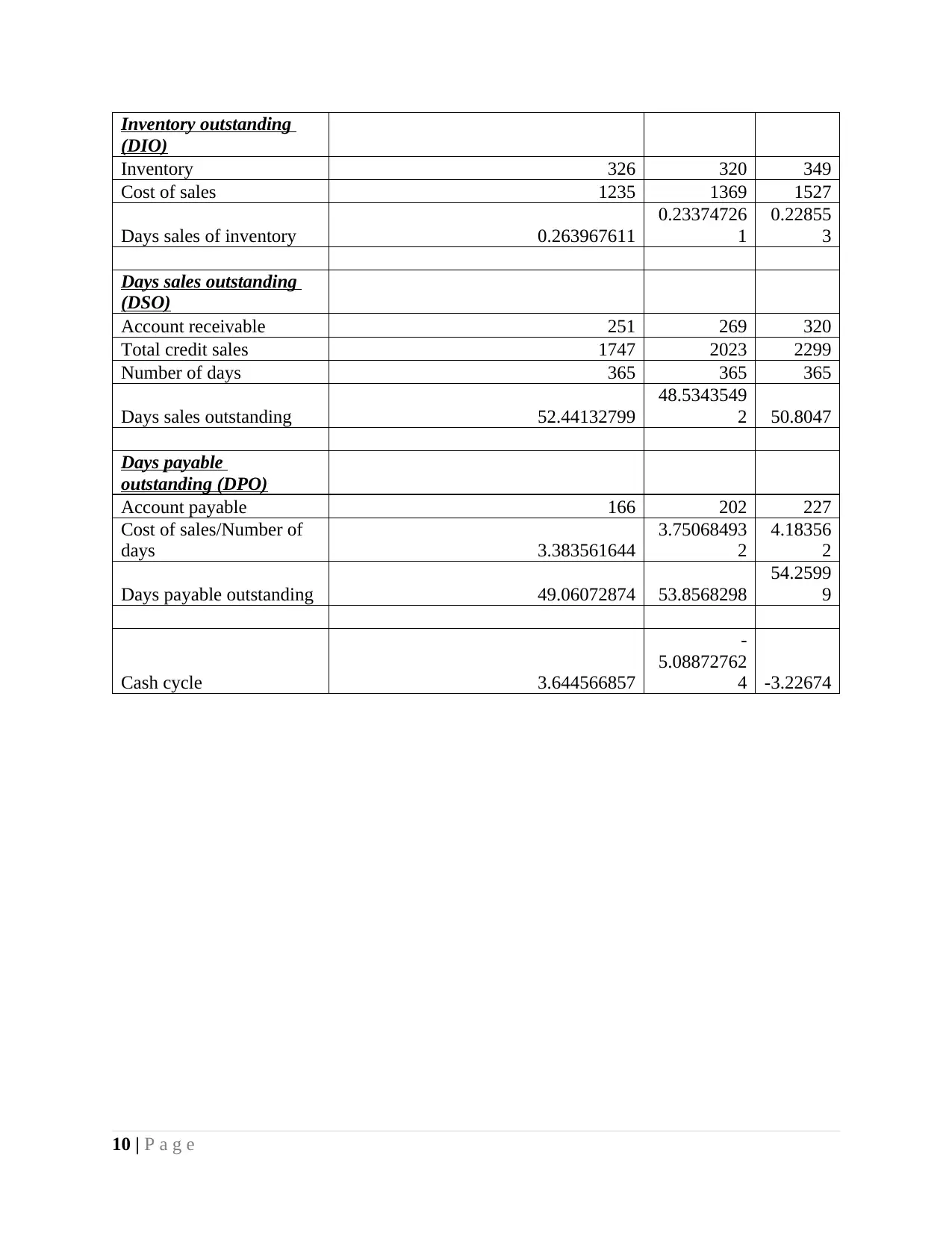

Days payable

outstanding (DPO)

Account payable 166 202 227

Cost of sales/Number of

days 3.383561644

3.75068493

2

4.18356

2

Days payable outstanding 49.06072874 53.8568298

54.2599

9

Cash cycle 3.644566857

-

5.08872762

4 -3.22674

10 | P a g e

(DIO)

Inventory 326 320 349

Cost of sales 1235 1369 1527

Days sales of inventory 0.263967611

0.23374726

1

0.22855

3

Days sales outstanding

(DSO)

Account receivable 251 269 320

Total credit sales 1747 2023 2299

Number of days 365 365 365

Days sales outstanding 52.44132799

48.5343549

2 50.8047

Days payable

outstanding (DPO)

Account payable 166 202 227

Cost of sales/Number of

days 3.383561644

3.75068493

2

4.18356

2

Days payable outstanding 49.06072874 53.8568298

54.2599

9

Cash cycle 3.644566857

-

5.08872762

4 -3.22674

10 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.